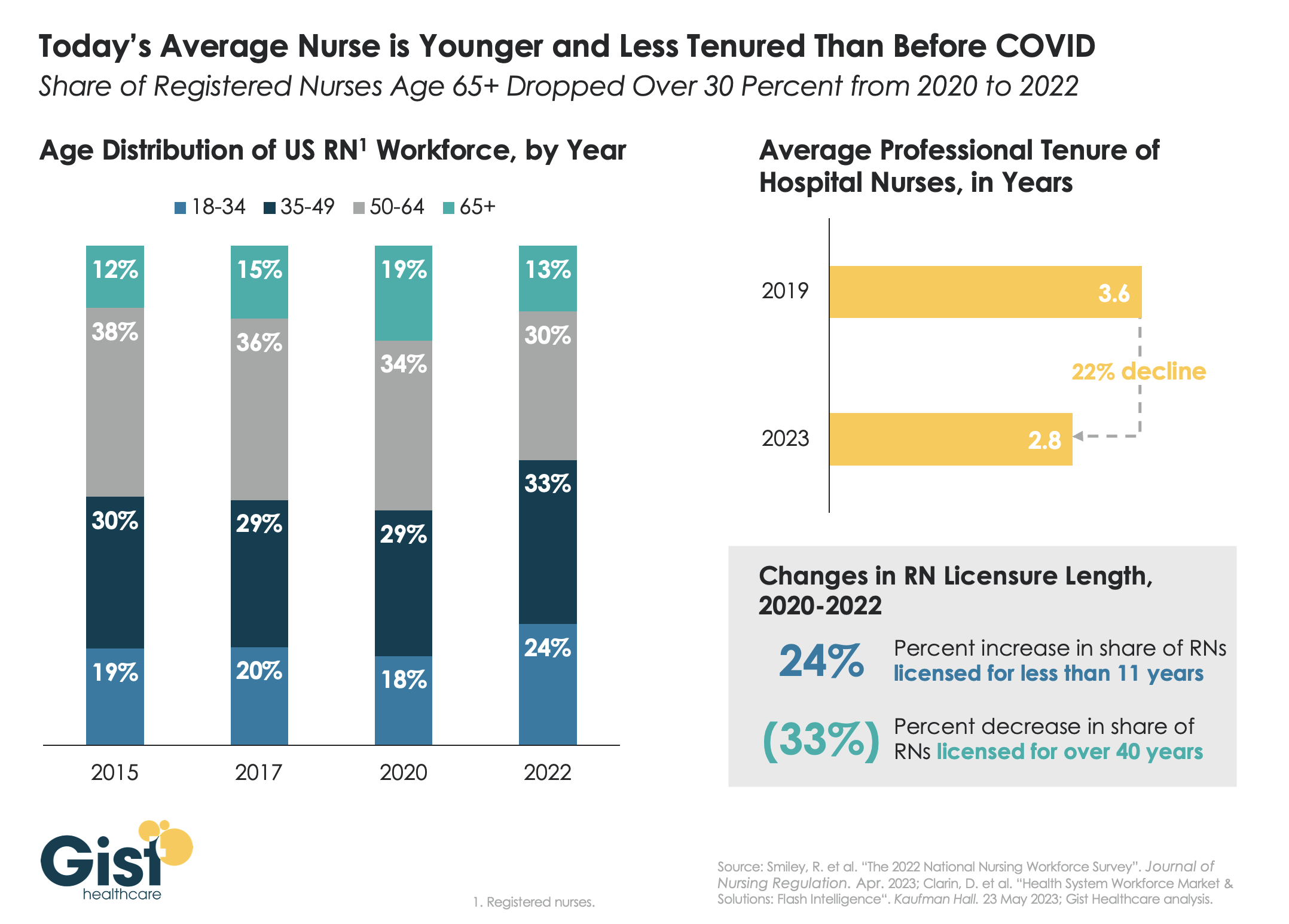

Last week we discussed how hospitals are still struggling to retain talent. This week’s graphic offers one explanation for this trend:

a significant share of older nurses, who continued to work during the height of the pandemic, have now exited the workforce, and health systems are even more reliant on younger nurses.

Between 2020 and 2022, the number of nurses ages 65 and older decreased by 200K, resulting in a reduction of that age cohort from 19 percent to 13 percent of the total nursing workforce. While the total number of nurses in the workforce still increased, the younger nurses filling these roles are both earlier in their nursing careers (thus less experienced), and more likely to change jobs.

Case in point:

From 2019 to 2023, the average tenure of a hospital nurse dropped by 22 percent. The wave of Baby Boomer nurse retirements has also resulted in a 33 percent decrease from 2020 to 2022 in the number of registered nurses who have been licensed for over 40 years.

Given these shifts, hospitals must adjust their current recruitment, retention, training, and mentorship initiatives to match the needs of younger, early-career nurses.

We recently spoke with a health system COO who wanted help playing out scenarios regarding the relationship between specialist physicians and their private equity (PE) partners. The system is located in one of the markets referenced in a recent study that has some of the highest levels of private equity ownership in the country. One physician group, whose doctors provide almost all the system’s coverage for a key specialty, has worked with PE partners for five years, and the relationship is not going well. “We’re hearing that many of the younger doctors want to leave. And many of the others are close to retirement,” he shared.

“We’re really concerned about what could happen if the group implodes.” The key issue: the doctors signed very restrictive noncompete agreements when they sold their practice, which could prohibit them from working in the market.

The health system would consider bringing some of the doctors into their employed medical group, but executives are worried this might be impossible for the duration of the noncompete agreements. “If these doctors can’t stay locally, we might have to rebuild that specialty from scratch. And I can’t imagine how disruptive that would be,” he worried.

When the FTC announced a proposed rule earlier this year that would ban employers from imposing noncompete agreements, many health systems reacted with alarm, fearing the that the freedom to move would lead to frequent bidding wars, ultimately driving up the cost of physician talent in the market.

But the situation shows how perspectives would change depending on who holds the noncompete.

Mid-sized markets like this one, where coverage for several specialties may come from single groups, are particularly vulnerable. Regardless, this situation highlights the need to diversify physician relationships to guard against getting caught in a “coverage crisis”.

Of all the pandemic’s impacts still felt today, disruptions to the healthcare workforce and rising labor costs may be most impactful to current health system operations.

Over the next three editions of the Weekly Gist, we’ll be exploring the lingering effects of this workforce crisis, with a focus on nurse staffing and recruitment.

While wage increases helped reduce hospital registered nurse (RN) turnover rates from 27 percent in 2021 to 23 percent in 2022, nurses—along with hospital employees in general—are still changing jobs at higher rates than before the pandemic.

Over half of all hospitals still face nurse vacancy rates above 15 percent, a slight improvement from 2022 but still far more than before the pandemic.

While the worst of nursing turnover appears to have passed, the “rebasing” of wages (for nursing, 27 percent higher compared to 2019) will provide ongoing pressure to strained hospital margins.

A recent physician survey conducted by strategic healthcare communications firm Jarrard Inc. uncovered a startling finding: only 36 percent of physicians employed by or affiliated with not-for-profit health systems trust that their system’s leaders are honest and transparent. In contrast, a slight majority of physicians working with investor-owned health systems and practices answered that question in the opposite.

Overall, only around half of physicians trust their organization’s leaders when it comes to financial, operational, and patient care decision-making. Unsurprisingly, doctors put the most trust in peer physicians, by a wide margin.

The Gist: While the numbers, especially for nonprofit systems, are stark, this survey reflects an on-the-ground reality felt at health systems in recent years. Physician fatigue has spiked in the wake of the pandemic.

And health system-physician relationships are also being disrupted by cost pressures, payer and investor acquisitions, and the shift of care to ambulatory settings. We’ve heard from physicians that, compared to hospital owners, investor-backed systems provide greater transparency and clearer financial goals centered around the success of the business.

That physicians trust their peers so highly suggests a path forward: provide physician leaderswith greater transparency into system performance and agency over strategy, with clear goals and metrics.

Last week the Department of Justice (DOJ) and the Federal Trade Commission (FTC) proposed thirteen new merger guidelines that, if finalized, would provide federal regulators greater ability to scrutinize mergers across all industries, including healthcare.

The guidelines expand which mergers could be potentially illegal and therefore worth probing, including those with lower monetary value and those in which the newly combined organization would control 30 percent or greater market share, and would increase scrutiny on transactions that are part of a series of multiple acquisitions by an organization. They also seek to limit the ability of an organization to justify an acquisition on the grounds that the weaker party in the deal would be unable to continue to operate. Comments on the guidelines are being accepted until September 18.

The Gist: To date, federal regulators have struggled to prevent non-traditional mergers between companies that provide different services, operate in different markets, or are below the monetary threshold for review.

The proposed guidelines would significantly increase FTC and DOJ scrutiny at all levels of hospital mergers, and also jeopardize physician and other care asset acquisitions by health systems, payers, and private equity-backed organizations. They are the latest from the Biden Administration in a recent, multi-part push to reduce consolidation through greater antitrust enforcement.

This effort includes last month’s proposal to add additional reporting requirements for mergers outlined in the Hart-Scott-Rodino Act, as well as the FTC’s move earlier this month to withdraw two antitrust policy statements focused on healthcare markets that both agencies say are now “outdated.” Those now-rescinded statements provided guidance on antitrust safety zones, including for accountable care organizations participating in the Medicare Shared Savings Program and for mergers between two hospitals in which one is much smaller.

In January 2023, the Rockefeller Institute published a three-part blog series on trends to watch in healthcare in 2023. The series covered broad issues related to the healthcare workforce, economy, and health policy, and highlighted internal industry changes and trends in service delivery, quality, and equity.

Here, we provide a recap and mid-year update on those trends.

The Public Health Emergency:

In January, we anticipated the COVID-19 federal public health emergency (PHE) would end at some point during the year and its ending would impact the industry by rolling back flexibilities and programs that were temporarily put in place to combat the pandemic. The end of the PHE, while not a “trend” per se, held significant potential to alter the trajectory of trends in healthcare coverage, access, and care delivery that were occurring during the pandemic.

Mid-year Update: As predicted, the PHE was not renewed and ended on May 11, 2023. The most notable impact of the non-renewal of the PHE was the end of continuous Medicaid public health insurance coverage. The Kaiser Family Foundation’s Medicaid Enrollment Tracker shows that, as of July 5, 2023, 1,652,000 Medicaid enrollees were disenrolled by the District of Columbia and 28 states reporting data. For context, this means that 39% of people with a completed renewal were disenrolled in reporting states, though disenrollment rates varied significantly across those states from 16 percent in Virginia to 75 percent in South Carolina. The eligibility redetermination process that can lead to a potential disenrollment is being conducted differently in each state with some states moving quickly to make redeterminations and others doing the process more deliberately over the course of the year with a clear intent to avoid shedding people from the Medicaid program because of an inability to submit administrative paperwork.

The process for eligibility renewals will continue to play out over the course of the next year since states have until mid-2024 to update all Medicaid enrollees’ eligibility status. Also notable are some changes made under the purview of the PHE that persist despite the emergency’s conclusion. For example, access to COVID-19 vaccinations and certain COVID-19 treatments generally have not been affected. Some telehealth flexibilities that were allowed under the PHE are also staying in effect, at least until the end of 2024.

Healthcare Workforce Shortages:

Prior to the pandemic, larger demographic trends in society were already impacting the supply of the healthcare workforce. The number of people aging and needing healthcare services was growing while the number of people available to provide care was not keeping pace thus creating a long-term healthcare workforce shortage.

Mid-year Update:The workforce shortage continues. As outlined in a May 23rd Becker’s Hospital Review article, several sources point to a continued shortage. They include a report that says the US could see a deficit of 200,000 to 450,000 registered nurses by 2025. Within the next five years, another report also projects a shortage of more than 3.2 million lower-wage healthcare workers, such as medical assistants, home health aides, and nursing assistants. As a result, some healthcare providers are becoming more creative in their efforts to counteract the workforce shortage: creating alumni networks from which to recruit or providing other benefits to their workforce, such as housing or educational assistance. Policymakers can help counteract the negative impacts of the workforce shortage through a variety of strategies. With the shortage expected to continue, it will be important to enact additional policies that bolster the workforce.

Price Inflation:

As we noted, price inflation was significant in 2022 but was not unique to the health sector.Inflation was particularly exacerbated by the re-opening of the economy after the pandemic, the continued war in Ukraine, and supply chain challenges.

Mid-year Update: Prices for many consumer goods and services increased faster than usual, with overall inflation reaching a four-decade high in mid-2022. The Bureau of Labor Statistics (BLS) reported inflation rates have slowed, with overall prices growing by 6 percent in February 2023 compared to the previous year. Interestingly, prices for medical care increased only 2.3 percent. Similarly, BLS reported that the average price of health care in the United States increased by 0.7 percent in the 12 months ending May 2023, following a previous increase of 1.1 percent. The slower price growth in healthcare compared to other sectors of the economy is highly unusual,[i] and while inflation is not easily influenced by state-level policymakers’ actions alone, the trend is still worth monitoring to better understand the impacts on healthcare access and quality. As of early July, the latest predictions from PwC are that healthcare costs will rise 7% in 2024.

Declining Margins at Hospitals:

Previous analysis by the consulting firm Kaufman Hall predicted that more than half of all hospitals would have negative margins at the end of 2022. As we noted, this was due to such factors as higher-than-normal expenses for staff, supplies, and pharmaceuticals and lower revenues.

Mid-year Update: The latest report from Kaufman Hall offers data that shows a reversal in this trend for the first part of 2023. May was the third consecutive month in which hospital margins were positive after operating in the red for most of 2022. The return to normal is largely driven by revenues that are more in line with pre-pandemic levels. With revenues returning to more normal levels, expenses will be particularly important to watch for the remainder of 2023. If hospital expenses continue to outweigh revenues, policymakers may need to evaluate the financial health of providers and the potential impact that may have on access to services for patients.

Private Equity in Healthcare:

We predicted that private equity (PE) would continue to grow in healthcare, pointing to a PwC consulting report that indicated that PE companies still had plenty of “dry powder,” or money, to invest in 2023.

Mid-year Update:There has been a slowdown in private equity deals over the last year. But it is notable that there were still 200 private equity deals in healthcare in the first quarter of 2023, according to PitchBook’s healthcare services report released in May 2023. While lower than the year before, this is still considered active when compared to pre-pandemic PE dealmaking. Because of the waning of the pandemic and stability returning to the healthcare sector, it is more likely that PE deals stabilize in 2023. And some industry predictions indicate that dealmaking will bounce back further in the second half of 2023. As noted in our previous blog, it will be important to monitor the proliferation of PE in healthcare and determine its impact on healthcare markets, care delivery, innovation, and quality.

Consolidations:

Like many other industries, consolidations of all sorts have been happening in healthcare. The consolidations are both vertical—combining two or more stages of production normally operated by separate companies into one company, such as when hospitals or insurers employ physicians and/or acquire physician practices or other entities like pharmacies—and horizontal—combining organizations that provide the same or similar services, such as hospitals acquiring hospitals.

Mid-year Update: Consolidations of all sorts of healthcare entities continued in 2023 with some of the biggest potential consolidations yet. Those include the proposed merger of two major bi-coastal health system providers: Geisinger, based in Pennsylvania, and Kaiser, based in California. Although the deal must still go through regulatory approval, if completed, the two systems will create a nonprofit that will look to add five or six more systems nationally over the next five years. Other notable consolidations include the finalization of tech-giant Amazon’s purchase of One Medical, a primary care network. And Optum, one of the largest conglomerates that is a subsidiary of United Health Group, increased its net revenue growth by 25% to $54.1 billion in the first quarter of 2023, primarily due to more patients visiting OptumHealth clinics and growth in OptumRx pharmacy scripts processed. Optum’s growth is likely to continue in 2023 as they expect to add another 10,000 physicians. Case in point, in February of this year, Optum paid an undisclosed sum for Crystal Run Healthcare, a network of nearly 400 providers in New York. A goal of consolidation has been better coordination of patient care for improved outcomes and value. Results have been mixed and it is therefore an important trend for policymakers and researchers to monitor and to ensure the impacts are positive.

Alternate Payment Models:

Alternate payment models (APMs) in healthcare have been expanding especially since enactment of the Patient Protection and Affordable Care Act in 2010. They are primarily being developed by the Center for Medicare and Medicaid Innovation (CMMI) which has driven payment policy (including APMs) in the two big government healthcare programs: Medicaid and Medicare. There have been several iterations of APMs—over 50 models—but the one common theme is that all of them generally seek to reward better care.

Mid-year Update: Since the start of 2023, the most notable expansion of the trend toward more alternate payment models was CMMI’s introduction of a new primary care-focused APM called Making Care Primary. In addition to this model, it is expected that the Centers for Medicaid and Medicare Services (CMS), which oversees the operation of these two large public health insurance programs, will introduce more new payment models in 2023, including one that allows states to manage the total cost of care in a given region. This may take various forms, including something akin to Maryland’s global budget, which is used statewide. Since the total cost of care model has yet to be officially revealed, this trend and the emergence of any new developments is worth watching in the second half of 2023. Policymakers can learn from these various payment models and use them to inform the plans implemented in their own state or region in order to improve healthcare.

Attention to Health Equity:

A notable aspect of the pandemic was the disparate impact it had on people of color and other marginalized groups. In response, policymakers and providers began paying more attention to the underlying cause of these disparities. In 2021, President Joe Biden signed an executive order to focus federal resources and attention on reducing health disparities.

Mid-year Update: Increased attention to health equity in healthcare has continued. Ernst and Young, an international consulting group, released its first-ever report on the state of health equity in the United States, which involved a survey of over 500 providers to begin tracking their methods for, and progress in, addressing health disparities. More recently, in June 2023, The Joint Commission on the Accreditation of Healthcare Organizations (JCAHO) announced that it will be adding a certification program for healthcare organizations specifically targeted towards improving health equity. While attention to equity has grown, what will be interesting to watch in the second half of 2023 is the degree to which such efforts are having an impact on actually reducing disparities. Understanding the impacts of various interventions can help policymakers expand efforts that are effective.

Digital TeleHealth Delivery Expansion:

The use of digital health expanded dramatically from 2020 to 2022 as social distancing practices were adopted and telehealth options became more widely available. As noted in our blog series, digital health “includes mobile health (mHealth), health information technology (IT), wearable devices, telehealth and telemedicine, and personalized medicine.” It also includes, “mobile medical apps and software that support the clinical decisions doctors make every day to do artificial intelligence and machine learning.”

Mid-year Update: At the end of 2022 and the start of 2023, the ability to infuse capital to drive the expansion of digital health seemed tenuous, in part due to the collapse of Silicon Valley Bank (SVB). As noted by the publication Pitchbook and CB Insights, venture capital funding in the digital health space totaled $7.5 billion in 2022, a 57 percent year-over-year drop. Although the fast pace of investment in digital health may have slowed since its explosion during the pandemic, the expansion of digital health continues. Our January blog suggested that areas such as behavioral health, care at home, and maternal health were areas to watch. In 2023, digital access is expanding in other areas, such as in-home urgent primary care to allow for the treatment of complex injuries and illnesses with the goal of reducing emergency department visits. And other important digital health deals are still occurring: health tech startup Florence picked up Zipnosis from Bright Health to expand its virtual care capabilities. And with the launch of consumer-facing tech products, such as Chat GPT and Apple Vision Pro in the first half of 2023, additional opportunities for applying such technologies in healthcare may fuel further expansion of digital health. Policies that are developed in the future may want to support the growth of such innovation, while also being mindful to monitor the potential impacts on care.

Expansion of Non-Traditional Providers:

In January, we noted an emergence of companies in healthcare whose genesis was something other than healthcare. The blog pointed to examples of how companies such as Walgreens, CVS, and Amazon were expanding their offerings in healthcare.

Mid-year Update:Non-traditional entities continue to expand in the healthcare space. Notable examples include the recent acquisitions and expansions made by CVS. One of these expansions is being done through its affiliation with the insurance company, Aetna. Through Aetna, CVS has entered the insurance exchange market in four more states in 2023, in addition to the 12 states in which it already operates. CVS also closed a deal in the first half of 2023 to acquire Oak Street Health for over $10 billion. And, in March 2023, CVS announced it had officially acquired Signify Health, a digital telehealth company that enables more care to occur in-home. As noted earlier, Amazon officially completed its deal to acquire OneMedical and United Health Group is working on expanding its use of value-based care through a partnership with Walmart. Monitoring the impact of these emerging companies in healthcare will be important for policymakers that have historically only focused on more traditional providers, such as hospitals. These non-traditional entrants, in many cases, are large organizations with substantial resources and their impact may be just as significant if not greater than traditional providers.

Conclusion

These trends merit close attention in the second half of 2023. As healthcare takes on new shapes, the implications for those in the sector and all who depend on it will be huge. In addition, there are important implications for state and federal policymakers who will need to consider how these trends impact access, affordability, and quality of health care, so they can determine whether and how government might help to accelerate beneficial innovations, invest in promising trends, prevent or reverse harmful trends, and monitor the impacts on consumers.

As first half 2023 financial results are reported and many prepare for a busy last half, strategic planning for healthcare services providers and insurers point to 4 issues requiring attention in every boardroom and C suite:

Private equity maturity wall:

The last half of 2023 (and into 2024) is a buyer’s market for global PE investments in healthcare services: 40% of PE investments in hospitals, medical groups and insurtech will hit their maturity wall in the next 12 months. Valuations of companies in these portfolios are below their targeted range; limited partner’ investing in PE funds is down 28% from pre-pandemic peak while fund raising by large, publicly traded, global funds dominate fund raising lifting PE dry powder to a record $3.7 trillion going into the last half of 2023.

In the U.S. healthcare services market, conditions favor well-capitalized big players—global private equity funds and large cap aggregators (i.e., Optum, CVS, Goldman Sachs, Blackstone et al) who have $1 trillion to invest in deals that enhance their platforms. Deals done via special purpose acquisition corporations (SPACS) and smaller PE funds in physicians, hospitals, ambulatory services and others are especially vulnerable. (see Bain and Pitchbook citations below). Addressing the growing role of large-cap PE and strategic investors as partners, collaborators, competitors or disruptors is table stakes for most organizations recognizing they have the wind at their backs.

Consolidation muscle by DOJ and FTC:

Healthcare is in the crosshair of the FTC and DOJ, especially hospitals and health insurers. Hospital markets have become increasingly concentrated: only 12% of the 306 Hospital Referral Regions is considered unconcentrated vs. 23% in 2008. In the 384 insurance markets, 23% are unconcentrated, down from 35% in 2020. Wages for healthcare workers are lower, prices for consumers are higher and choices fewer in concentrated markets prompting stricter guidelines announced last week by the oversight agencies. Big hospitals and big insurers are vulnerable to intensified scrutiny. (See Regulatory Action section below).

Defamatory attacks on nonprofit health systems:

In the past 3 years, private, not-for-profit multi-hospital systems have been targeted for excess profits, inadequate charity care and executive compensation. Labor unions (i.e., SEIU) and privately funded foundations (i.e., West, Arnold Venture, Lown Institute) have joined national health insurers in claims that NFP systems are price gaugers undeserving of the federal, state and local tax exemptions they enjoy. It comes at a time when faith in the U.S. health system is at a modern-day low (Gallup), healthcare access and affordability concerns among consumers are growing and hospital price transparency still lagging (36% are fully compliant with the 2021 Executive Order).

Notably, over the last 20 years, NFP hospitals have become less dominant as a share of all hospitals (61% in 2002 vs. 58% last year) while investor-owned hospitals have shown dramatic growth (from 15% in 2002 to 24% last year). Thus, the majority of local NFP hospitals have joined systems creating prominent brands and market dominance in most regions. But polling indicates many of these brands is more closely associated with “big business” than “not-for-profit health” so they’re soft targets for critics. It is likely unflattering attention to large, NFP systems will increase in the next 12 months prompting state and federal regulatory actions and erosion of public support. (See New England Journal citation in Quotables below)

Campaign 2024 healthcare rhetoric:

Republican candidates will claim healthcare is not affordable and blame Democrats. Democrats will counter that the Affordable Care Act’s expanded coverage and the Biden administration’s attack on drug prices (vis a vis the Inflation Reduction Act) illustrate their active attention to healthcare in contrast to the GOP’s less specific posturing.

Campaigns in both parties will call for increased regulation of hospitals, prescription drug manufacturers, health insurers and PBMs. All will cast the health industry as a cesspool for greed and corruption, decry its performance on equitable access, affordability, price transparency and improvements in the public’s health and herald its frontline workers (nurses, physicians et al) as innocent victims of a system run amuck.

To date, 16 candidates (12 R, 3 D, 1 I) have announced they’re candidates for the White House while campaigns for state and local office are also ramping up in 46 states where local, state and national elections are synced. Healthcare will figure prominently in all. In campaign season, healthcare is especially vulnerable to misinformation and hyper-attention to its bad actors. Until November 5, 2024, that’s reality.

My take:

These issues frame the near-term context for strategic planning in every sector of U.S. healthcare. They do not define the long-term destination of the system nor roles key sectors and organizations will play. That’s unknown.

What’s known for sure is that AI will modify up to 70% of the tasks in health delivery and financing and disrupt its workforce.

Black Swans like the pandemic will prompt attention to gaps in service delivery and inequities in access.

People will be sick, injured, die and be born.

And the economics of healthcare will force uncomfortable discussions about its value and performance.

In the U.S. system, attention to regulatory issues is a necessary investment by organizations in every state and at the federal level. Details about these efforts is readily accessible on websites for each organization’s trade group. They’re the rule changes, laws and administrative actions to which all are attentive. They’re today’s issues.

Less attention is given the long-term. That focus is often more academic than practical—much the same as Robert Oppenheimer’s early musings about the future of nuclear fusion. But the Manhattan Project produced two bombs (Little Boy and Fat Man) that detonated above the Japanese cities of Hiroshima and Nagasaki in 1945, triggering the end of World War II.

The four issues above should be treated as near and present dangers to the U.S. health system requiring attention in every organization. But responses to these do not define the future of the U.S. system. That’s the Manhattan Project that’s urgently needed in our system.

Peter Drucker, the hall of fame management guru, once famously said that the hardest business organization to run in America was a hospital. If that comment was true so many years ago, imagine what Drucker would have to say about the difficulty of hospital management right now.

Hospital financial performance suffered significantly in 2022 and recovery during 2023 has been quite slow. This trend suggests the question,

“What steps are hospital C-suites taking to recover pre-Covid financial stability?”

Erik Swanson manages all analyses for our monthly Kaufman Hall Flash Report and he and I speculated that an industry-wide hospital recovery could not be achieved without reductions in force across the hospital ecosystem. Some research on our part determined that no official organization tracks hospital layoffs over time but we wondered if we could use our Flash Report data, which is provided to us by Syntellis Performance Solutions, to reach an informed conclusion.

What we were able to do was prepare three types of charts, as follows:

The first chart measures net employee percentage change by month. This chart shows whether overall hospital employment is increasing or decreasing over time and by how much.

The second chart attempts to establish the median turnover for hospitals over an annual period and then measure the deviation from that turnover rate. A greater deviation from what might be termed “normal turnover” suggests that an increasing number of hospitals are using reductions in force to more quickly reduce the cost of doing business.

The third chart shows average FTEs per occupied bed on a comparative basis looking at month-to-month and year-to-year statistics.

The first chart, Net Employee Percentage Change by Month, begins at January 1, 2018, and continues to March 1, 2023 (Figure 1). Overall additions to hospital employment remained generally positive through January 1, 2020. Overall hospital employment then went generally negative from March 2020 (the onset of Covid restrictions) to March 2022. The reductions in hospital employees during this period were likely the result of the “great resignation” during the worst of the Covid pandemic. But then, from July 2022 to March 2023, overall hospital employees demonstrated by the Flash Report dropped dramatically with an overall 2% decrease at the March 2023 date. This statistic suggests more than simply increased hospital turnover, but rather a formal layoff process initiated across many hospital organizations, along with aggressive management of contract labor.

Figure 1: Net Employee Percentage Change by Month

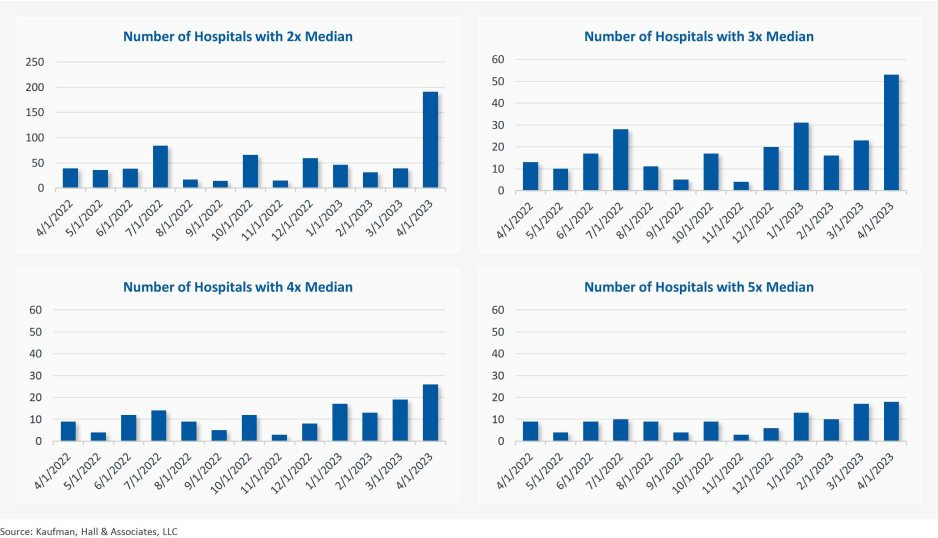

The second chart demonstrates the deviation from expected turnover at levels of 2x, 3x, 4x, and 5x by number of hospitals (Figure 2). No matter which measure you examine, the deviation of employees from expected turnover spiked significantly in April 2023 and even more so in May 2023. This again suggests the aggressive management of labor costs that likely could not occur without the intentional reduction of actual positions and/or the cost of these positions.

Figure 2: Number of Hospitals with Deviations from Expected Turnover at 2x, 3x, 4x, and 5x the Median

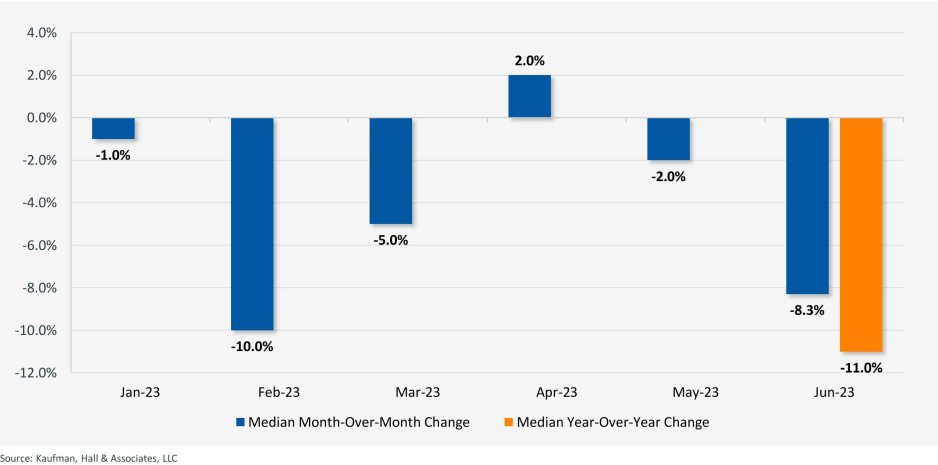

The last chart provides a remarkable set of observations (Figure 3). FTEs per adjusted occupied bed (AOB) declined by 8.3% between June 2023 and July 2023. The year-over-year variation for July 2023 was a decline of 11.01%. Our data further reveals that the FTE per AOB statistic has declined in five of the past six months on a month-over-month basis.

Figure 3: Median Change in FTEs per Adjusted Occupied Bed by Month

The conclusion here is that the return of the hospital industry to pre-Covid financial results has been no walk in the park. 2022 was, of course, a dismal financial year for the hospital industry. And while 2023 has shown improvement, the usual management steps to recovery have been only moderately effective. The data and analysis above demonstrate that C-suites across America are moving to stronger measures to assure the financial survivability and competitiveness of their organizations.

There is no revenue solve here, or at least not in the current environment: costs must come down and they must come down materially. From the sense and the trend of the data it would seem that hospital executive teams get the joke.

Value-based healthcare, the holy grail of American medicine, has three parts: excellent clinical quality, convenient access and affordability for all.

And as with the holy grail of medieval legend, the quest for value-based care has been filled with failure.

In the 20th century, U.S. medical groups and hospital systems could—at best—achieve two elements of value-based care, but always at the sacrifice of the third. Until recently, American medicine lacked the clinical knowhow, technology and operational excellence to accomplish all three, simultaneously. We now have the tools. The only thing missing is “system-ness.”

What Is System-ness?

System-ness is the effective and efficient coordination of healthcare’s many parts: outpatient and inpatient, primary and specialty care, financing and care delivery, prevention and treatment.

By bringing these disparate pieces together within a well-functioning system, healthcare providers have the opportunity to maximize clinical outcomes, weed out waste, lower overall costs and provide greater levels of convenience and access.

Who Are The Search Parties?

In the future, system-ness will be the variable that determines whether healthcare transformation is led by (a) incumbent health systems like Kaiser Permanente and Geisinger Health or (b) the retail giants like Amazon, CVS and Walmart. The latter group has become an ever-growing threat in the healthcare arms race, quickly amassing their own (though still modest) systems of care through billion-dollar acquisitions.

Although both the incumbents and new entrants will struggle to implement value-based care on a national scale, the victor stands to earn hundreds of billions of dollars in added revenue and tens of billions in profits.

To better understand the power of system-ness, and the challenges all organizations will face in providing it, here are three examples of value-based-care solutions implemented successfully by Kaiser Permanente.

1. Preventing Problems, Managing Disease

Research demonstrates that preventive medicine and early intervention reduce heart attacks, strokes and cancer. Yet our nation falls far short in these areas when compared to its global peers.

One example is hypertension, the leading cause of strokes and a major contributor to heart attacks. With help from doctors, nearly all patients can keep high blood pressure under control. Yet, nationally, hypertension is controlled only 60% of the time.

We see similarly poor rates of performance when it comes to prevention and screening for cancers of the colon, breast and lung.

Undoing these troubling trends requires system-ness. In Kaiser Permanente, 90% of patients had their blood pressure controlled and were screened for cancer. Getting there required a comprehensive electronic health record, a willingness for every doctor (regardless of specialty) to focus on prevention, leadership that communicated the value of prevention and a salary structure that rewarded group excellence.

2. Continuous Care, Without Interruption

Most doctors’ offices are open Monday to Friday during normal business hours—only one-fourth of the time that a medical problem might occur.

At night and on weekends, patients have no choice but to visit ERs. There, they often wait hours for care, surrounded by people with communicable diseases. Their non-emergent problems generate bills 12-times higher than if they’d waited to be seen in a doctor’s office.

There’s a better way. In large-enough medical groups, hundreds of clinicians can provide round-the-clock care on a rotating, virtual basis—using video to assess patients and make evidence-based recommendations.

This approach, pioneered by physicians in the Mid-Atlantic Permanente Medical group, solved the patient’s problem immediately 70% of the time without a trip to the ER and, for the other 30%, enabled coordination of medical care with the ER staff.

3. Specialized Medicine, Immediate Attention

When a primary care physician needs added expertise (from a dermatologist, urologist or orthopedist), it’s usually the responsibility of the patient to make their own specialty appointments, check with insurance for coverage and provide their medical records.

This takes hours or days to coordinate and can delay care by weeks, resulting in avoidable complications.

But in a well-structured system, there’s no need to wait. Using telehealth tools at Kaiser Permanente, primary care doctors can connect instantly with dozens of different specialists—often while the patient is still in the exam room. Once connected, the specialist evaluates the patient and provides immediate expertise.

This way, care is not only faster and less expensive, but also better coordinated. Data from within Kaiser Permanente show that these virtual consultations resolve the patient’s problem 40% of the time without having to schedule another appointment. For the other 60%, the diagnostic process can begin immediately.

The Foundations For System-ness

Few organizations in the U.S. can or do offer these system-based improvements. Doing so requires skilled physician leadership, a shift in the financial model and a willingness to accept risk.

In fact, most organizations across the U.S. that claim to operate “value-based” systems actually rely on doctors who are scattered across the community, disconnected from each other and paid on the basis of volume (fee-for-service) rather than value (capitation).

As a result, patient care is fragmented and uncoordinated, leading to repeated tests and ineffective treatments, thus increasing medical costs and compromising medical outcomes.

Value-based care (superior quality, access and affordability) requires teams of clinicians working together as one—all paid on a capitated basis.

Without capitation, dermatologists will insist on seeing every patient in their office where they can bill insurance five-times more than with a tele-dermatology visit. And gastroenterology specialists will insist that all patients have colonoscopy rather than recommending low-risk patients do a safe, convenient, at-home colon cancer screening (called a fecal immunochemical test or “FIT”) at 5% of the cost.

In these cases, individual doctors don’t consciously make care inconvenient for patients. Rather, it is the only choice they have when working in a fee-for-service payment model. Ultimately, system-ness is best achieved when health systems are integrated, prepaid, tech-enabled and physician-led.

Amazon, CVS, Walmart Know About Systems

These three companies are global leaders in “system-ness,” at least in retail. Combined, they have a market cap of $1.88 trillion, employ 3.4 million Americans and are looking to take a slice of U.S. healthcare’s $4.3 trillion annual expenditures.

Already, they manage complex order-entry and fulfillment systems. They use technology to streamline everything from customer service to supply-chain management. They are led through a clear and effective reporting structure.

In terms of competing for healthcare’s holy grail, these are huge competitive advantages compared to today’s uncoordinated, individualized, leaderless healthcare industry.

As retailers vie to bring their system knowhow to American medicine, they are acquiring the pieces needed to compete with the healthcare incumbents. They’ve spent tens of billions of dollars on medical groups that are committed to value-based care (One Medical, Oak Street Health, etc.). They’ve also spent massive sums on home-health companies (Signify) and on pharmacies (PillPak), along with expanding their in-store, at-home and online care options. Many of these care-delivery subsidiaries are focused on Medicare Advantage, the capitated half of Medicare where financial success is dependent on high quality medical care provided at lower cost.

What’s more, all these retailers have a national presence with brick-and mortar facilities in nearly every community in the country—a leg up on nearly every existing health system.

Who Will Win—And Why?

Trying to pick the victor in the battle to transform American medicine at this point is like selecting the winner of a heavy-weight championship boxing match after three evenly matched rounds. Intangibles like stamina, courage and willingness to absorb pain have yet to be tested.

In The Innovator’s Dilemma, the late Clayton Christensen examined historical battles between incumbent organizations and new entrants. After analyzing dozens of industries, he concluded new entrants routinely become the victors because the incumbents move too slowly and fail to embrace the need for major change.

And from that perspective, if I had to wager, I’d put my money on the retail giants.

But there’s an even more worrisome potential outcome: neither those inside nor outside of healthcare will make the necessary investments or accept the risk of leading systemic change. As a result, the movement toward value-based healthcare will stall and die.

In that context, purchasers of healthcare (businesses, the government and patients) will encounter a difficult reality: over the next eight years, medical costs will nearly double, creating an unaffordable and unsustainable scenario. As a result, our nation will likely experience reduced medical coverage, increased rationing, ever-longer delays for care and a growth in health disparities.

If that day arrives, our country will regret its inaction.