On Monday, Fitch Ratings, the New York City-based credit rating agency, released a report predicting that the US not-for-profit hospital sector will see average operating margins reset in the one-to-two percent range, rather than returning to historical levels of above three percent.

Following disruptions from the pandemic that saw utilization drop and operating costs rise, hospitals have seen a slower-than-expected recovery.

But, according to Fitch, these rebased margins are unlikely to lead to widespread credit downgrades as most hospitals still carry robust balance sheets and have curtailed capital spending in response.

The Gist:As labor costs stabilize and volumes return, the median hospital has been able to maintain a positive operating margin for the past ten months.

But nonprofit hospitals are in a transitory period, one with both continued challenges—including labor costs that rebased at a higher rate and ongoing capital restraints—and opportunities—including the increase in outpatient demand, which has driven hospital outpatient revenue up over 40 percent from 2020 levels.

While the future margin outlook for individual hospitals will depend on factors that vary greatly across markets, organizations that thrive in this new era will be the ones willing to pivot, take risks, and invest heavily in outpatient services.

Last Monday, two lawsuits were filed that strike at a fundamental challenge facing the U.S. health system:

In the District Court of NJ, a class action lawsuit (ANN LEWANDOWSKI v THE PENSION & BENEFITS COMMITTEE OF JOHNSON AND JOHNSON) was filed against J&J alleging the company had mismanaged health benefits in violation of the Employee Retirement Income Security Act (“ERISA”). As noted in the 74-page filing “This case principally involves mismanagement of prescription-drug benefits. “Over the past several years, defendants breached their fiduciary duties and mismanaged Johnson and Johnson’s prescription-drug benefits program, costing their ERISA plans and their employees millions of dollars in the form of higher payments for prescription drugs, higher premiums, higher deductibles, higher coinsurance, higher copays, and lower wages or limited wage growth… Defendants’ mismanagement is most evident in (but not limited to) the prices it agreed to pay one of its vendors—its Pharmacy Benefits Manager (“PBM”)—for many generic drugs that are widely available at drastically lower prices.”

The issue is this: what liability risk does a self-insured employer have in providing health benefits to their employees?

Is the structure of the plan, the selection of providers and vendors, and costs and prices experienced by employees subject to litigation? What’s the role of the employer in protecting employees against unnecessary costs?

On the same day, in the District Court of Eastern Wisconsin, an 85-page class action lawsuit was filed against Advocate-Aurora Health (AAH) claiming it “uses its market power to raise prices, limit competition and harm consumers in Wisconsin:

Forces commercial health plans to include all its “overpriced facilities” in-network even when they would prefer to include only some facilities.

Goes to “extreme efforts to drive out innovative insurance products that save commercial health plans and their members money.”

Suppresses competition through “secret and restrictive contract terms that have been the subject of bipartisan criticism.”

Acquires new facilities, which then allows it to raise prices due to reduced competition

… without intervention, the health system will continue to use “anticompetitive contracting and negotiating tactics to raise prices on Wisconsin commercial health plans and their members and use those funds for aggressive acquisitions and executive compensation.”

The issue is this: is a health system’s liable when its consolidation activities result in higher prices for services provided communities and employers in communities where they operate?

Is there a direct causal relationship between a system’s consolidation activities and their prices, and how should alleged harm be measured and remedied?

Two complicated issues for two reputable mega-players in the U.S. health system. Both lawsuits were brought as class actions which guarantees widespread media attention and a protracted legal process. And each contributes directly to the gradual erosion of public trust in the health system since the plaintiffs essentially claim the business practices of J&J and Advocate-Aurora willfully harm the individuals they pledge to serve.

In the November 2023 Keckley Poll, I asked the sample of 817 U.S. adults to assess the health system overall. The results were clear:

69% think the system is fundamentally flawed and in need of major change vs. 7% who think otherwise.

60% believe it puts its profits above patient care vs. 13% who disagree.

74% think price controls are needed vs. 7% who disagree.

83% believe having health insurance that’s ‘affordable and comprehensive’ is essential to financial security vs 3% who disagree.

52% feel confident in their ability to navigate the U.S. system “when I have a problem” vs. 32% who have mixed feelings and 16% who aren’t.

And 76% think politicians avoid dealing with healthcare issues because they’re complex and politically risky vs/ 6% who think they tackle them head-on.

The poll also asked their level of trust and confidence in five major institutions “to develop a plan for the U.S. health system that maximizes what it has done well and corrects its major flaws.”

Clearly, trust and confidence in the health system is low, and expectations about solutions fall primarily on hospitals and doctors. Lawsuits like these widen suspicion that the industry’s dominated first and foremost by Big Businesses focused on their own profitability before all else. And they pose particular problems for sectors in healthcare dominated by not-for-profit and public ownership i.e. hospitals, home care, public health agencies and others.

My take

These lawsuits address two distinct issues: the roles of employers in designing their health benefits for employees including the use of PBMs, and the justification for consolidation of hospital and ancillary services in markets.

But each lawsuit s predicated on a legal theory that prices set by organizations are geared more to corporate profits than public good and justifiable costs.

Pricing is the Achilles of the health system. Pushback against price transparency by some, however justified, has amplified exposure to litigation risk like these two and contributed to the public’s loss of trust in the system.

It is unlikely greater price transparency and business practice disclosures by J&J and Advocate-Aurora could have avoided these lawsuits, but it’s clearly a message that needs consideration in every organization.

Healthcare organizations and their trade groups can no longer defend against lack of transparency by defaulting to the complexity of our supply chains and payment systems. They’re excuses. The realities of generative AI and interoperability assure information driven healthcare that’s publicly accessible and inclusive of prices, costs, outcomes and business practices. In the process, the public’s interest will heighten and lawsuits will increase.

Last Thursday, Seattle-based Providence Health System announced it is refunding nearly $21 million in medical bills paid by low-income residents of Washington and erasing $137 million more in outstanding debt for others. Other systems are likely to follow as pressure con mounts on large, not-for-profit systems to modify their business practices in sensitive areas like patient debt collection, price transparency, executive compensation, investment activities and others.

Not-for profit systems control the majority of the 2,987 nongovernment not-for-profit community hospitals in the U.S. Some lawmakers think it’s time to revisit to revisit the tax exemption. It has the attention of the American Hospital Association which lists “protecting not-for-profit hospitals’ the tax-exempt status” among its 15 Advocacy Priorities in 2024 (it was not on their list in 2023).

Background: Per a recent monograph in Health Affairs: “The Internal Revenue Service (IRS) uses the Community Benefit Standard (CBS), a set of 10 holistically analyzed metrics, to assess whether nonprofit hospitals benefit community health sufficiently to justify their tax-exempt status. Nonprofit hospitals risk losing their tax exemption if assessed as underinvesting in improving community health. This exemption from federal, state, and local property taxes amounts to roughly $25 billion annually.

However, accumulating evidence shows that many nonprofit hospitals’ investments in community health meet the letter, but not the spirit, of the CBS.

Indeed, a 2021 study showed that for every $100 in total expenses nonprofit hospitals spend just $2.30 on charity care (a key component of community benefit)—substantially less than the $3.80 of every $100 spent by for-profit hospitals. A 2022 study looked at the cost of caring for Medicaid patients that goes unreimbursed and is therefore borne by the hospital (another key component of community benefit); the researchers found that nonprofit hospitals spend no more than for-profit hospitals ($2.50 of every $100 of total expense).”

In its most recent study, the AHA found the value of CBS well-in-excess of the tax exemption by a factor of 9:1. But antagonism toward the big NFP systems has continued to mount and feelings are intense…

Insurers think NFP systems exist to gain leverage in markets & states over insurers in contract negotiations and network design. They’ll garner support from sympathetic employers and lawmakers, federal anti-consolidation and price transparency rulings and in the court of public opinion where frustration with the system is high.

State officials see the mega- NFP systems as monopolies that don’t deserve their tax exemptions while the state’s public health, mental health and social services programs struggle.

Some federal lawmakers think the NFP systems are out of control requiring closer scrutiny and less latitude. They think the tax exemption qualifiers should be re-defined, scrutinized more aggressively and restricted.

Well-publicized investments by NFP systems in private equity backed ventures has lent to criticism among labor unions and special interests that allege systems have abandoned community health for Wall Street shareholders.

Investor-owned multi-hospital operators believe the tax exemption is an unfair advantage to NFPs while touting studies showing their own charity care equivalent or higher.

Other key NFP and public sector hospital cohorts cry foul: Independent hospitals, academic medical centers, safety-net (aka ‘essential’) hospitals, rural health clinics & hospitals, children’s hospitals, rural health providers, public health providers et al think they get less because the big NFPs get more.

And the physicians, nurses and workforces employed by Big NFP systems are increasingly concerned by systemization that limits their wages, cuts their clinical autonomy and compromises their patients’ health.

My take:

The big picture is this: the growth and prominence of multi-hospital systems mirrors the corporatization in most sectors of the economy: retail, technology, banking, transportation and even public utilities. The trifecta of community stability—schools, churches and hospitals—held out against corporatization, standardization and franchising that overtook the rest. But modernization required capital, the public’s expectations changed as social media uprooted news coverage and regulators left doors open for “new and better” that ceded local control to distant corporate boards.

Along the way, investor-owned hospitals became alternatives to not-for-profits, and loose networks of hospitals that shared purchasing and perhaps religious values gave way to bigger multi-state ownership and obligated groups.

The attention given large NFP hospital systems like Providence and others is not surprising. These brands are ubiquitous. Their deals with private equity and Big Tech are widely chronicled in industry journalism and passed along in unfiltered social media. And their collective financial position seems strong: Moody’s, Fitch, Kaufman Hall and others say utilization has recovered, pandemic recovery is near-complete and, despite lingering concerns about workforce issues, growth in their core businesses plus diversification in new businesses are their foci. (See Hospital Section below).

I believe not-for-profit hospital systems are engines for modernizing health delivery in communities and a lightening rod for critics who think their efforts more self-serving than for the public good.

Most consumers (55%) think they earn their tax exemption but 34% have mixed feelings and 10% disagree. (Keckley Poll November 20, 2023). That’s less than a convincing defense.

That’s why the threat to the tax exemption risk is real, and why every organization must be prepared. Equally important, it’s why AHA, its state associations and allies should advance fresh thinking about ways re-define CBS and hardwire the distinction between organizations that exist for the primary purpose of benefiting their shareholders and those that benefit health and wellbeing in their communities.

PS: Must reading for industry watchers is a new report from by Health Management Associates (HMA) and Leavitt Partners, an HMA company, with support from Arnold Ventures. The 70-page report provides a framework for comparing the increasingly crowned field of 120 entities categorized in 3 groups: Hybrids (6.9 million), Delivery (5.8 million) and Enablers 17.5 million

“At the start of the movement, value-based arrangements primarily involved traditional providers and payers engaging in relatively straight-forward and limited contractual arrangements. In recent years, the industry has expanded organically to include a broader ecosystem of risk-bearing care delivery organizations and provider enablement entities with capabilities and business models aligned with the functions and aims of accountable care…Inclusion criteria for the 120 VBD entities included in this analysis were:

1-Serve traditional Medicare, MA, and/or Medicaid populations. Entities that are focused solely on commercial populations were excluded

2-Operate in population-based, total cost of care APMs—not only bundled payment models.

3- Focus on primary care and/or select specialties that are relevant to total cost of care models (i.e., nephrology, oncology, behavioral health, cardiology, palliative care). Those exclusively focused on specialty areas geared toward episodic models (e.g., MSK) were excluded. –

4-Share accountability for cost and quality outcomes. Business models must be aligned with provider performance in total cost of care arrangements. Vendors that support VBP but do not share accountability for outcomes were excluded.

Creating a great rating agency presentation is imperative to telling your story. I’ve probably seen a thousand presentations across the past three decades and I can say without a doubt that a great presentation will find its way into the rating committee. Show me a crisp, detailed, well-organized presentation, and I’ll show you a ratings analyst who walks away with high confidence that the management team can navigate the industry challenges ahead.

During the pandemic, Kaufman Hall recommended that hospitals move financial performance to the top of the presentation agenda. Better presentations chronicled the immediate, “line item by line item” steps management was taking to stop the financial bleeding and access liquidity. We still recommend this level of detail in your presentations, but as many hospitals relocate their bottom line, management teams are now returning to discussing longer-term strategy and financial performance in their presentations.

Beyond the facts and figures, many hospitals ask me what the rating analysts REALLY want to know. Over those one thousand presentations I’ve seen, the presentations that stood out the most addressed the three themes below:

What makes your organization essential? Hospitals maintain limited price elasticity as Medicare and Medicaid typically comprise at least half of patient service revenue, leaving only a small commercial slice to subsidize operations. The ability to negotiate meaningful rate increases with payers will largely rest on the ability to prove why the hospital is a “must-have” in the network. In other words, a health plan that can’t sell a product without a hospital in its network is the definition of essential. This conversation now also includes Medicare Advantage plans as penetration rates increase rapidly across the country. Essentiality may be demonstrated by distinct services, strong clinical outcomes and robust medical staff, multiple access points across a certain geography, or data that show the hospital is a low-cost alternative compared to other providers. Volume trends, revenue growth, and market share show that essentiality. A discussion on essentiality is particularly needed for independent providers who operate in crowded markets.

What makes your financial performance durable? Many hospitals are showing a return to better performance in recent quarters. Showing how your organization will sustain better financial results is important. Analysts will want to know what the new “run rate” is and why it is durable. What are the undergirding factors that make the better margins sustainable? Drivers may include negotiated rate increases from commercial payers and revenue cycle improvements. On the expense side, a well-chronicled plan to achieve operating efficiencies should receive material airtime in the presentation, particularly regarding labor. It is universally understood that high labor costs are a permanent, structural challenge for hospitals, so any effort to bend the labor cost curve will be well received. Management should also isolate non-recurring revenue or expenses that may drive results, such as FEMA funds or 340B settlements. To that end, many states have established new direct-to-provider payment programs which may be meaningful for hospitals. Expect questions on whether these funds are subject to annual approval by the state or CMS. The analysts will take a sharpened pencil to a growing reliance on these funds.

The durability of financial performance should be represented with highly detailed multi-year projections complete with computed margin, debt, and liquidity ratios. Know that analysts will create their own conservative projections if these are not provided, which effectively limits your voice in the rating committee.

We also recommend that hospitals include a catalogue of MTI and bank covenants in the presentation. Complying with covenants are part of the agreement that hospitals make with their lenders, and it is the organization’s responsibility to report how it’s performing against these covenants. General philosophy on headroom to covenants also provides insight to management’s operating philosophy. For example, is it the organization’s goal to have narrow, adequate, or ample headroom to the covenants and why? As the rating agencies will tell you, ratings are not solely based on covenant performance, but all rating factors influence your ability to comply with the covenants.

What makes your capital plan affordable? Every rating committee will ask what the hospital’s future capital needs are and how those capital needs will be supported by cash flow, also known as “capital capacity.” To answer that question, a hospital must understand what it can afford, based on financial projections. Funding sources may require debt, which requires a debt capacity analysis with goals on debt burden, coverage, and liquidity targets. Over the years, better presentations explain the organization’s capital model, outline the funding sources, and discuss management’s tolerance for leverage.

There is always a lot to cover when meeting with the rating agencies and a near endless array of metrics and indicators to provide. As I’ve written before, how you tell the story is as important as the story itself. If you can weave these three themes throughout the presentation, then you will have a greater shot at having your best voice heard in rating committee.

In Sunday’s Axios’ AM, Mike Allen observed “Republicans know immigration alone could sink Biden. So, Trump and House Republicans will kill anything, even if it meets or exceeds their wishes. Biden knows immigration alone could sink him. So he’s willing to accept what he once considered unacceptable — to save himself.”

Mike called this a “truth Bomb” and he’s probably right: the polarizing issue of immigration is tantamount to a bomb falling on the political system forcing well-entrenched factions to re-think and alter their strategies.

In 2024, in U.S. healthcare, three truth bombs are in-bound. They’re the culmination of shifts in the U.S.’ economic, demographic, social and political environment and fueled by accelerants in social media and Big Data.

Truth bomb: The regulatory protections that have buoyed the industry’s growth are no longer secure.

Despite years of effectively lobbying for protections and money, the industry’s major trade groups face increasingly hostile audiences in city hall, state houses and the U.S. Congress.

The focus of these: the business practices that regulators think protect the status quo at the public’s expense. Example: while the U.S. House spent last week in their districts, Senate Committees held high profile hearings about Medicare Advantage marketing tactics (Finance Committee), consumer protections in assisted living (Special Committee on Aging), drug addiction and the opioid misuse (Banking) and drug pricing (HELP). In states, legislators are rationalizing budgets for Medicaid and public health against education, crime and cybersecurity and lifting scope of practice constraints that limit access.

Drug makers face challenges to patents (“march in rights”) and state-imposed price controls. The FTC and DOJ are challenging hospital consolidation they think potentially harmful to consumer choice and so. Regulators and lawmakers are less receptive to sector-specific wish lists and more supportive of populist-popular rules that advance transparency, disable business relationships that limit consumer choices and cede more control to individuals. Given that the industry is built on a business-to-business (B2B) chassis, preparing for a business to consumer (B2C) time bomb will be uncomfortable for most.

Truth bomb: Affordability in U.S. is not its priority.

The Patient Protection and Affordability Act 2010 advanced the notion that annual healthcare spending growth should not exceed more than 1% of the annual GDP. It also advanced the premise that spending should not exceed 9.5% of household adjusted gross income (AGI) and associated affordability with access to insurance coverage offering subsidies and Medicaid expansion incentives to achieve near-universal coverage. In 2024, that percentage is 8.39%.

Like many elements of the ACA, these constructs fell short: coverage became its focus; affordability secondary.

The ranks of the uninsured shrank to 9% even as annual aggregate spending increased more than 4%/year. But employers and privately insured individuals saw their costs increase at a double-digit pace: in the process, 41% of the U.S. population now have unpaid medical debt: 45% of these have income above $90,000 and 61% have health insurance coverage. As it turns out, having insurance is no panacea for affordability: premiums increase just as hospital, drug and other costs increase and many lower- and middle-income consumers opt for high-deductible plans that expose them to financial insecurity. While lowering spending through value-based purchasing and alternative payments have shown promise, medical inflation in the healthcare supply chain, unrestricted pricing in many sectors, the influx of private equity investing seeking profit maximization for their GPs, and dependence on high-deductible insurance coverage have negated affordability gains for consumers and increasingly employers. Benign neglect for affordability is seemingly hardwired in the system psyche, more aligned with soundbites than substance.

Truth bomb: The effectiveness of the system is overblown.

Numerous peer reviewed studies have quantified clinical and administrative flaws in the system. For instance, a recent peer reviewed analysis in the British Medical Journal concluded “An estimated 795 000 Americans become permanently disabled or die annually across care settings because dangerous diseases are misdiagnosed. Just 15 diseases account for about 50.7% of all serious harms, so the problem may be more tractable than previously imagined.”

The inadequacy of personnel and funding in primary and preventive health services is well-documented as the administrative burden of the system—almost 20% of its spending. Satisfaction is low. Outcomes are impressive for hard-to-diagnose and treat conditions but modest at best for routine care. It’s easier to talk about value than define and measure it in our system: that allows everyone to declare their value propositions without challenge.

Truth bombs are falling in U.S. healthcare. They’re well-documented and financed. They take no prisoners and exact mass casualties.

Most healthcare organizations default to comfortable defenses. That’s not enough. Cyberwarfare, precision-guided drones and dirty bombs require a modernized defense. Lacking that, the system will be a commoditized public utility for most in 15 years.

PS: Last week’s report, “The Holy War between Hospitals and Insurers…” (The Keckley Report – Paul Keckley) prompted understandable frustration from hospitals that believe insurers do not serve the public good at a level commensurate with the advantages they enjoy in the industry. However, justified, pushback by hospitals against insurers should be framed in the longer-term context of the role and scope of services each should play in the system long-term. There are good people in both sectors attempting to serve the public good. It’s not about bad people; it’s about a flawed system.

Earlier this month, we released our year-end report on hospital and health system M&A activity in 2023. As a follow-up to that report, here are our thoughts on the five most interesting transactions announced in the past year.[1]

The creation of Risant Health and its planned acquisition of Geisinger Health. This was the transaction that created the most buzz in 2023, promising the formation of a platform—supported by Kaiser Permanente—dedicated to the advancement of value-based care. Risant Health will be created by the Kaiser Foundation Hospitals and will acquire Geisinger as its first member. It will seek to add additional systems to the platform once the acquisition of Geisinger has been finalized.

Novant Health’s acquisition of three hospitals from Tenet Healthcare. This transaction represented several of the 2023 M&A trends highlighted in our year-end report. It offers an example of for-profit health system portfolio realignment: Tenet announced that the proceeds of the sale—a pre-tax book gain of approximately $1.6 billion—will be used primarily for debt retirement. It also offers an example of regional market development, as Novant continues to expand its network in North and South Carolina. And with a valuation of the deal at 16 times adjusted EBITDA—based on the $2.4 billion sale price and $150 million adjusted EBITDA reported in the press release—this transaction reflects the value of investing in high-growth markets: in this case, coastal South Carolina.

Henry Ford Health System’s joint venture with Ascension. Offering another example of regional market development, this transaction, when finalized, would also provide an example of how secular and faith-based organizations can work together in partnership. The press release announcing the transaction noted that both organizations “are committed to working to maintain the Catholic identity of the Ascension Michigan facilities included in the transaction.”

The combination of BJC Health System and Saint Luke’s Health System. This transaction, announced in May 2023, closed on January 1, 2024, and provides an example of the cross-market transactions that have emerged as a significant trend in hospital and health system M&A. Also—given the relatively close geographic alignment of the two systems—it provides another example of regional market development. It is the largest of the regional development transactions called out in our year-end report: others included the Novant/Tenet transaction described above, as well as the combination of Froedtert Health and ThedaCare in eastern Wisconsin and Vandalia Health’s development of a statewide network in West Virginia.[2]

Centura Health’s acquisition of Steward Health’s Utah care sites. In another example of a for-profit system divesting its interest in a geographic market, Steward Health announced the sale of its Utah care sites—including five hospitals and more than 35 medical group clinics—to Centura Health, which is part of CommonSpirit Health. CommonSpirit will own the assets, which will be managed by Centura Health. For Centura, the transaction offers an opportunity to enter the growing Utah market, which has demographics similar to its home base in Colorado.

We are early in the year, but 2024 has started with a bang: the announced acquisition of Summa Health, based in Akron, Ohio, by General Catalyst’s Healthcare Assurance Transformation Corporation (HATCo).[3]The acquisition, when completed, would launch HATCo on its path to fulfill one of the three goals set forth during the October 2023 announcement of its formation: “acquiring and operating a health system for the long term where we can demonstrate the blueprint of [healthcare] transformation for the rest of the industry.”

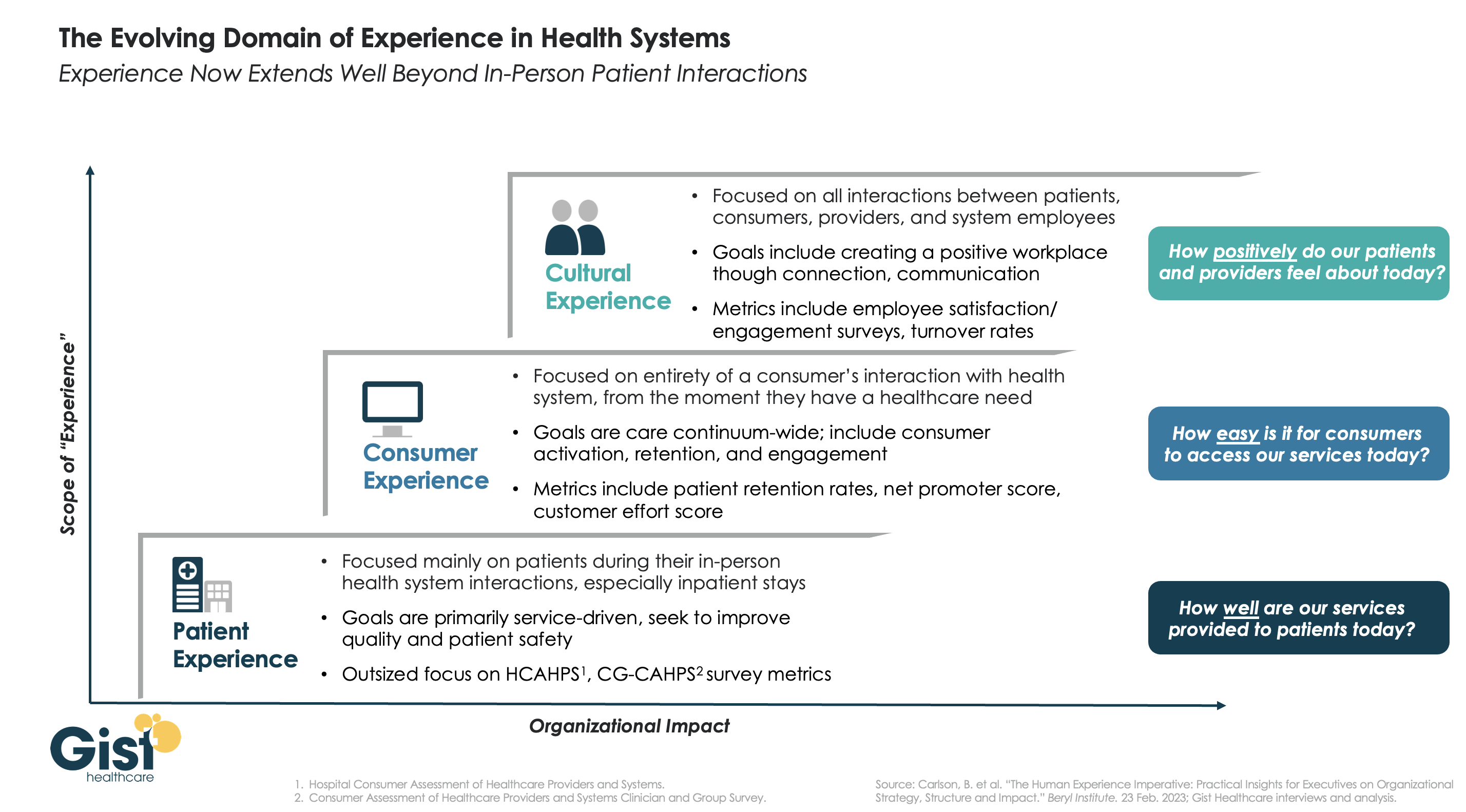

In this week’s graphic, we highlight the importance of broadening the domain of health system experience initiatives beyond patients to include consumers and even employees.

While reimbursements tied to HCAHPS (Hospital Consumer Assessment of Healthcare Providers and Systems) and CG-CAHPS (Clinician and Group Consumer Assessment of Healthcare Providers and Systems) scores have made patient experience a main focus for years, an increasingly consumer-driven healthcare industry means that health systems must consider the experience of all consumers in their markets, with the hopes of meeting their needs and eventually welcoming them as new—or retuning—patients.

Embracing this mindset requires focusing on the entirety of a consumer’s interactions with the health system and the tracking of non-traditional metrics that measure the strength and value of their relationship to the system. Some systems are expanding their experience purview even further by also focusing on the working conditions and morale of their providers and other staff, as a healthy workplace environment serves to better both the patient and consumer experience. Easily accessible services and positive interactions with providers and other staff can determine a consumer’s view of their experience before any care is actually delivered.

Cultural and strategic shifts that integrate experience from the top down into all operational facets of the health system will ultimately strengthen consumer loyalty, employee retention, and the financial health of the system.

For many providers, 2023 provided a return to profitability (albeit at modest levels) following the devastating operating and investment losses experienced in 2022.Kaufman Hall’s National Hospital Flash Report data illustrated generally improving operating margins throughout the year, leveling off at 2.0% in November on a year-to-date basis.

This level of performance is commendable given 2022 and early 2023 margins, although it is still well below the 3% to 4% range which we believe is needed for long-term sustainability in the not-for-profit healthcare world. We may well have reached a point of stability with respect to operating performance, but at a lower level.

The question for hospital and health system leaders is whether this level of operating stability provides sustainability?

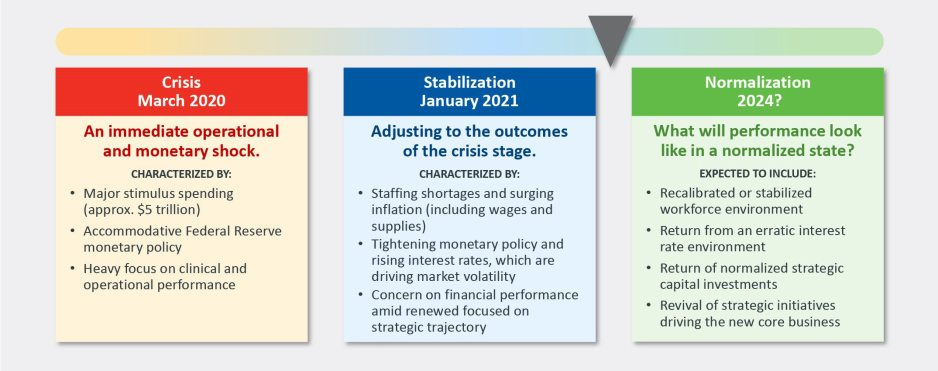

From stabilization to normalization

Since the pandemic began in 2020, the progress of recovery has been viewed over three phases: crisis, stabilization, and normalization. In last year’s outlook, we noted that we were in the midst of a potentially multi-year stabilization phase, which would continue to be marked with volatility—including ongoing labor market dislocations, inflationary pressures, and restrictive monetary policies. As we enter 2024, there are signs that we are now at the bridge between stabilization and normalization (Figure 1).

Figure 1: The Three Phases of Recovery from the Covid Pandemic

“The question for hospital and health system leaders is whether that level of stability provides sustainability?”

These signs include evidence that the first two indicators for normalization—a recalibrated or stabilized workforce environment and a return from an erratic interest rate environment—are coming into place. In our 2023 State of Healthcare Performance Improvement survey, respondents indicated that the spike in contract labor utilization that has been a dominant factor in operating expense increases was subsiding. Sixty percent of respondents said that utilization of contract labor was decreasing, and 36% said it was holding steady. Only 4% noted an increase in contract labor usage. Overall employee cost inflation seems to be subsiding as well: for all three labor categories in our survey (clinical, administrative, and support services), more organizations were able to hold salary increases to the 0% – 5% range in 2023 than in 2022.

There is good news on the interest rate front as well. After a series of rate increases in 2023, the Federal Reserve has held steady the last six months and has signaled rate cuts in 2024. Inflation has cooled markedly (albeit not yet at target levels), and employment rates have held steady. The Fed may have achieved a “soft landing” that satisfies its dual mandate of stable prices and maximum sustainable employment. Borrowing costs for not-for-profit hospital issuers have declined nearly 100 basis points in the last two months and we are expecting a return to more normal issuance levels in the first half of 2024.

There are other indications of normalization, including in the rating agencies’ outlooks for 2024. Regardless of the headline, all saw significant improvement in healthcare performance 2023.

The final answer to the question of whether the healthcare industry is entering the normalization phase likely will hinge on the last two indicators. Will we see a return of normalized strategic capital investments, and will we see a revival of strategic initiatives driving the core business (perhaps newly imagined)?

In effect, are health care systems simply surviving or are they thriving?

Looking forward, several factors could either bolster or undermine healthcare leaders’ confidence and willingness to resume a more normal level of investment in both capital needs and strategic growth. These include:

Politics and the 2024 elections. When North Carolina—a state that has traditionally leaned “red”—decided to opt into the Affordable Care Act’s (ACA’s) Medicaid expansion in 2023, it seemed that political debates over the ACA might be in the rearview mirror. But last November, former president Trump—currently the leading candidate for the Republican presidential nomination after strong wins in the Iowa caucuses and New Hampshire primary—indicated his intent to replace the ACA with something else. President Biden is now making protection and expansion of the ACA a key part of his 2024 campaign. What had appeared to be a settled issue may be a significant point of contention in the 2024 presidential election and beyond.

Although we do not anticipate any significant healthcare-related legislation in advance of the 2024 elections, healthcare leaders should be prepared for renewed attention to the costs of government-funded healthcare programs leading up to and following the elections. The national debt has increased rapidly over the past 20 years, tripling from $11 trillion in 2003 to $33 trillion in 2023. If the deficit and national debt become an important issue in the election, a move toward a balanced budget—akin to the Balanced Budget Act of 1997—post election could lead to further cuts to Medicare and Medicaid.

Temporary relief payments. Health systems continue to receive one-time cash infusions through the 340B settlement, Federal Emergency Management Agency (FEMA) payments and other governmental programs. Approximately 1,600 hospitals have or will be receiving a lump-sum payment to compensate them for a change in the Department of Health & Human Services’ (HHS’s) reimbursement rates for the 340B program from 2018 to 2022, which was ruled unlawful by the Supreme Court in a 2022 decision. The total amount to be distributed is approximately $9 billion and began hitting bank accounts in January 2024.

But what the right hand giveth, the left hand taketh away. Budget neutrality requirements will force HHS to recoup this offset—amounting to approximately $7.8 billion—which it will do by reducing payments for non-drug items and services to all Outpatient Prospective Payment System (OPPS) providers by 0.5% until the offset has been fully recouped, beginning in calendar year 2026. HHS estimates that this process will take approximately 16 years. Is this a harbinger of lower payments on other key governmental programs?

Many hospitals also continue to receive Covid-related payments from FEMA for expenses occurred during the pandemic. In addition, state supplemental payments—especially under Medicaid managed care and fee-for-service programs—are providing some relief. The Centers for Medicare & Medicaid Services has issued a proposed rule, however, that would limit states’ use of provider-based funding sources, such as provider taxes, and cap the rate of growth for state-directed payments.

As all of these payment programs dry up over the next few years, hospitals will need to replace the revenue and/or get leaner on the expense side in order to maintain today’s level of performance.

The hollowing of the commercial health insurance market. Our colleague, Joyjit Saha Choudhury, recently published a blog on the hollowing of the commercial health insurance market, driven by long-term concerns over the affordability of healthcare. While volumes have been recovering to pre-pandemic levels, this hollowing threatens the loss of the most profitable volumes and will pressure hospitals and health systems to create and deliver value, compete for inclusion in narrow networks, and develop more direct relationships with the employer community.

Related, the growing penetration of Medicare Advantage plans is reducing the number of traditional Medicare beneficiaries. Many CFOs report that these programs can be the most difficult with which to work given their high denial rates and required pre-authorization rates. A new rule requiring insurers to streamline prior authorizations for Medicare Advantage, Medicaid, and Affordable Care Act plans may help alleviate this issue; however, it will be incumbent upon management teams to stay ahead of them. Aging demographics are also reducing the percentage of commercially insured patients for many hospitals and health systems, further exacerbating the problem. This combination of fewer commercial patients (who often subsidize governmental patients) and more pressure on receiving the duly owed commercial revenue threatens to be an ongoing headache for management teams.

Ongoing impact of the Baby Boom generation. Despite the good news on inflation—and indications that the Fed may begin lowering interest rates in 2024—the economy is by no means out of the woods yet. The Baby Boom generation, which holds more than 50% of the wealth in the U.S. and is seemingly price agnostic, still has many years of spending ahead, in healthcare and general purchasing. This will likely continue to pressure inflation, especially in the healthcare sector, where demand will continue to grow. As the generation starts to shrink, the resulting wealth transfer will be the largest ever in our country’s history and have profound (and unforeseen) consequences on the overall economy and healthcare in general.

In sum, these other factors will continue to affect the sector (both positively and negatively) and require health system management teams to navigate an everchanging world. While many signs point toward short-term relief, the longer-term challenges persist. Improvements in the short term may, however, provide the opportunity to reposition organizations for the future.

How hospitals and health systems should respond

Healthcare leaders should view ongoing uncertainty in the political and economic climate as a tailwind as much as a headwind. This uncertainty, in other words, should be a motivation to put in place strategies that will buffer healthcare organizations from potential bumps in the road ahead. Setting balance sheet strategy should be a part of an organization’s planning process.

How an organization sets that strategy, measures its performance, and makes improvements will set apart top-performing organizations.

Although heightened debt issuance early in 2024 signals a return for many systems to a climate of investment, there is still limited energy around strategy and debt conversations in many boardrooms, especially in those organizations where financial improvement continues to lag. The last two years have illustrated that hospitals and health systems will not be able to cut their way to profitability. Lackluster performance cannot and will not improve without some level of strategic change, whether it is through market share gains, payer mix shift, or operational improvements. This strategic change requires investment and investment requires capital. Capital can be obtained in many forms—whether through growth in capital reserves, improved cash flow, or new debt issuance—but is essential for change. Reengaging in conversations about strategy and growth should be an imperative in 2024 and will require reexamining how that growth is funded.

Healthcare leaders should engage their partners as they continue or refocus on:

Changing the conversation from debt capacity to capital capacity. Management teams need to determine what they can afford to spend on capital if the new normal of cash flow will be constrained going forward. Capital capacity is and should be agnostic to the source of that capital, such as debt, cash flow from operations, or liquidity reserves. Healthcare leaders must focus on what they can spend, before deciding how to fund that spending. The conversation will need to balance investment for the future with maintaining key credit metrics in the short term.

Conducting a capitalization analysis. Separate but related to the previous entry, how much leverage should your organization have relative to its overall capitalization? Ostensibly, many organizations have been paying principal while curtailing borrowing needs, so capitalization may have improved. While that may be the case, many organizations have depleted reserves and/or experienced investment losses that have reduced capitalization. Understanding where the organization stands is an essential next step.

Evaluating surplus return. Consider surplus return as investment income net of interest expense. Organizations should evaluate their ability to reliably generate both operating cash flow and net surplus. How an organization’s balance sheet is positioned to generate returns and manage risk will be a critical success factor.

Focusing on the metrics that matter. These include operating cashflow margin, cash to debt, debt to revenue, and days cash on hand. As key metrics for rating analysts and investors continue to evolve, management teams need to make sure they are focused on the correct numbers. The discussion should be dually focused on ensuring adequate-to-ample headroom to basic financial covenants as well as a comparison to key medians and peers. Strong financial planning will address how these metrics can be improved over time through synergies, growth, and diversification strategies.

Although it has been a difficult few years, hospitals and health systems seem to have moved onto a more stable footing over the last twelve months. In order to build upon the upward trajectory, now is the time to harness strategy, planning, and investment to move organizations from stability to sustainability.

The upheaval of the past few years has permanently changed the healthcare landscape, and while many sectors of the industry continue to endure financial hardship, there is reason for cautious optimism in 2024 as healthcare begins to see a return on investment in technology and a resurgence in dealmaking.

This year, BDO surveyed healthcare CFOs to discover their plans, priorities, and concerns heading into 2024.

In today’s newsletter, I’ve outlined the top research findings that every healthcare leader needs to know to prepare for the year ahead.

Top 3 Workforce Investment Areas

Clinician burnout and staffing shortages remain challenging in the healthcare industry, but BDO’s survey indicated that many CFOs are bullish that the worst is behind them, with 47% stating they feel that in 2024, the talent shortage will represent less of a risk than in 2023.

Investment in the workforce is crucial to addressing staffing challenges, and in the year ahead, healthcare CFOs intend to invest in the following ways:

1. Training: 48% of CFOs plan to spend more on training, in part to buttress ongoing investment in new technologies like AI that can help with predictive staffing and financial reporting.

2. Recruitment: 48% of CFOs will spend more on recruiting, as the talent shortfall tightens an already restricted pool of candidates.

3. Compensation & Benefits: Alongside greater spending on recruiting itself, 46% of CFOs intend to increase compensation and benefits as a means of attracting talent from competitors and retaining current staff.

Transaction Plans

Dealmaking turned a corner in 2023, with activity returning to pre-pandemic levels in Q2. Despite fluctuating interest rates and the volatility of an election year, we can expect more transactions in 2024, with 72% of CFOs planning some kind of deal, relative to their organization’s financial health and liquidity. An increase in antitrust activity, however, could impact the size and type of deals that see success. Healthcare CFOs planning a large deal should be prepared for heightened scrutiny.

While we expect to see a wide range of deals taking place over the next year, two specific deal types are worth calling out:

1. Carve-outs/Divestitures: We may see an uptick in enterprise sales, carve-outs, and divestitures, particularly for institutions that have been struggling financially — 31% of institutions that violated their bond or loan covenants in 2023 are planning to pursue deals of this kind.

2. Private Equity (PE) and Venture Capital (VC): Nearly one in five (19%) CFOs, particularly those working with physician groups, plan to explore PE and VC investment as avenues toward scaling, sharing services, and safeguarding succession planning.

Service Line Investment Plans

There are still many areas where CFOs are intending to increase investment, but changed market conditions mean that some core areas of healthcare may see decreased investment as the industry realigns:

1. Specialty Services: Fifty-two percent of CFOs plan to increase their investments in specialty services like cardiology, oncology, and dermatology, while 23% of CFOs intend to partner with a capital provider or operator.

2. Service Expansion: Home care (51%), virtual/telehealth (48%), and ambulatory service centers (49%) are also priority areas for investment as institutions continue to expand and maintain access to healthcare outside of traditional hospital and clinic settings.

3. Primary Care: Although primary care remains at the heart of the healthcare industry, many CFOs (42%) have in fact signaled an intent to reduce investment in this area, reassessing their primary care strategies due to significant cash flow pressures and ongoing realignment as the retail market gains ground.

Want to know more about healthcare leaders’ plans for the year ahead? Get more insights and data in BDO’s 2024 Healthcare CFO Outlook Survey.

Where are you planning on increasing investment in your organization this year? Let me know in the comments below.

Saint Peter’s Healthcare System in New Brunswick, N.J., was six years ahead of the C-suite streamlining curve.

The health system slimmed down its leadership structure in 2017, President and CEO Les Hirsch told Becker’s. A top-heavy executive team grew unsustainable as the system struggled financially, operating at a loss. Saint Peter’s board decided to combine the president and CEO positions — which were previously split in two. Then, as president and CEO, Mr. Hirsch cut five vice presidents’ positions, including the consolidation of the chief information officer and chief medical information officer roles. More than 20 middle-manager positions were also cut or consolidated.

The streamlining of senior leadership positions alone at the time eliminated over $4 million in salaries and benefits, according to Mr. Hirsch. With the old leadership structure, Saint Peter’s spent about 2.4% of its revenue on senior leaders’ compensation. Last year, that percentage sank to 1.34%.

But finances shouldn’t be the only consideration for a health system planning to whittle down its structure.

“The good news is, we’re lean,” Mr. Hirsch said. “The bad news is, we’re lean.”

Since consolidating the president and CEO roles — and not having a chief operating officer — succession planning is more complicated, per Mr. Hirsch.

“There’s no designated No. 2,” he said. “Our senior leadership team structure is very flat.”

A condensed C-suite also means more work for some members of the leadership team — which is taken in stride, Mr. Hirsch said. There’s no specific “planning” department, so executives put their heads together on strategy, growth and development initiatives. There is no government relations officer, but Mr. Hirsch, as CEO, takes primary responsibility for this function and is very active in advocacy.

Anyone who works on a lean team like this also “has to be a generalist,” Mr. Hirsch said. He stays up to date on the literature and sends relevant articles to other executives.

“Considering our size as one of the few remaining single-hospital health systems in New Jersey, we don’t have the luxury of having somebody specifically responsible for artificial intelligence or other niche responsibilities as these are functions that are absorbed within people’s roles,” Mr. Hirsch said. “And we all develop the knowledge needed so that we can understand how new ideas or resources may apply to us. When you’re smaller and don’t have the scale of these mega-organizations, you have to do more yourself. You roll up your sleeves.”

Despite these challenges, a little can go a long way; three departmental administrators now split the job once shared by seven people at Saint Peter’s. There’s been no hit to efficiency; “they’re more effective in their roles as departmental administrators than anybody that I’ve ever seen,” Mr. Hirsch said.

The changes to streamline management were also well-received by the workforce. Often layoffs affect front-line workers more than management or senior leadership — which may have contributed to the lack of outcry, per Mr. Hirsch. But he primarily attributes the positive reception to intentional transparency.

“Most importantly, I’m a very active communicator. So, I communicated about it. It wasn’t that there was some intrigue and mystery in the organization that people were hearing by rumor,” Mr. Hirsch said.

“Rumors — like fear — are two things that equate to being like a cancer in an organization,” he continued. “I always want to do everything I possibly can to set the facts straight and communicate with people. If it’s not confidential and I can communicate it, I will. In fact, I’ll err more on the side of communicating than keeping information close to the vest.”

Regardless of who is affected by layoffs, executives should always handle them with sensitivity, Mr. Hirsch emphasized; the right choice for an organization is not always the easy choice for its people.

“It’s always painful when you’re making these kinds of changes because they affect people, and you always have to go about those changes in a very thoughtful, considerate, and compassionate way,” Mr. Hirsch said. “You’re eliminating roles and impacting people’s lives, their careers and their family. So, I always keep that top of mind.”