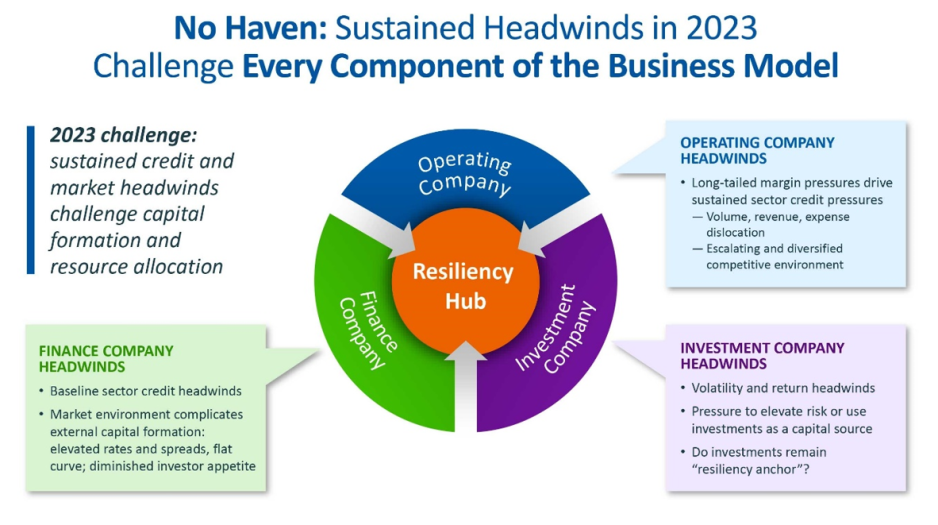

For the first time in recent history, we saw all three

functions of the not-for-profit healthcare system’s

financial structure suffer significant and sustained

dislocation over the course of the year 2022

(Figure above).

The headwinds disrupting these functions

are carrying over into 2023, and it is uncertain how

long they will continue to erode the operating and

financial performance of not-for-profit hospitals

and health systems.

The Operating Function is challenged by elevated

expenses, uncertain recovery of service volumes, and

an escalating and diversified competitive environment.

The Finance Function is challenged by a more

difficult credit environment (all three rating agencies

now have a negative perspective on the not-forprofit healthcare sector), rising rates for debt, and

a diminished investor appetite for new healthcare

debt issuance. Total healthcare debt issuance in

2022 was $28 billion, down sharply from a trailing

two-year average of $46 billion.

The Investment Function is challenged by volatility and

heightened risk in markets concerned with the Federal

Reserve’s tightening of monetary policy and the

prospect of a recession. The S&P 500—a major stock

index—was down almost 20% in 2022. Investments

had served as a “resiliency anchor” during the first

two years of the pandemic; their ability to continue

to serve that function is now in question.

A significant factor in Operating Function challenges is

labor: both increases in the cost of labor and staffing

shortages that are forcing many organizations to

run at less than full capacity. In Kaufman Hall’s 2022

State of Healthcare Performance Improvement Survey, for

example, 67% of respondents had seen year-over-year

increases of more than 10% for clinical staff wages,

and 66% reported that they had run their facilities at

less-than-full capacity because of staffing shortages.

These are long-term challenges,

dependent in part on

increasing the pipeline of new talent entering healthcare

professions, and they will not be quickly resolved.

Recovery of returns from the Investment Function

is similarly uncertain. Ideally, not-for-profit health

systems can maintain a one-way flow of funds into

the Investment Function, continuing to build the

basis that generates returns. Organizations must now

contemplate flows in the other direction to access

funds needed to cover operating losses, which in

many cases would involve selling invested assets at a

loss in a down market and reducing the basis available

to generate returns when markets recover.

The current situation demonstrates why financial

reserves are so important:

many not-for-profit

hospitals and health systems will have to rely on

them to cover losses until they can reach a point

where operations and markets have stabilized, or

they have been able to adjust their business to a

new, lower margin environment. As noted above,

relief funding and the MAAP program helped bolster

financial reserves after the initial shock of the

pandemic. As the impact of relief funding wanes

and organizations repay remaining balances under

the MAAP program, Days Cash on Hand has begun

to shrink, and the need to cover operating losses is

hastening this decline. From its highest

point in 2021, Days Cash on Hand had decreased, as

of September 2022, by:

29% at the 75th percentile, declining from 302 to 216

DCOH (a drop of 86 days)

28% at the 50th percentile, declining from 202 to 147

DCOH (a drop of 55 days)

49% at the 25th percentile, declining from 67 to 34

DCOH (a drop of 33 days)

Financial reserves are playing the role

for which they were intended; the only

question is whether enough not-for-profit

hospitals and health systems have built

sufficient reserves to carry them through

what is likely to be a protracted period of

recovery from the pandemic.

KEY TAKEAWAYS

All three functions of the not-for-profit healthcare

system’s financial structure—operations, finance,

and investments—suffered significant and

sustained dislocation over the course of 2022.

These headwinds will continue to challenge not-forprofit

hospitals and health systems well into 2023.

Days Cash on Hand is showing a steady decline, as

the impact of relief funding recedes and the need

to cover operating losses persists.

Financial reserves are playing a critical role in

covering operating losses as hospitals and health

systems struggle to stabilize their operational and

financial performance.

Conclusion

Not-for-profit hospitals and health systems serve

many community needs. They provide patients

access to healthcare when and where they need it.

They invest in new technologies and treatments that

offer patients and their families lifesaving advances

in care. They offer career opportunities to a broad

range of highly skilled professionals, supporting the

economic health of the communities they serve.

These services and investments are expensive and

cannot be covered solely by the revenue received

from providing care to patients.

Strong financial reserves are the foundation of good

financial stewardship for not-for-profit hospitals and

health systems.

Financial reserves help fund needed

investments in facilities and technology, improve an

organization’s debt capacity, enable better access to

capital at more affordable interest rates, and provide a

critical resource to meet expenses when organizations

need to bridge periods of operational disruption or

financial distress.

Many hospitals and health systems today are relying

on the strength of their reserves to navigate a difficult

environment; without these reserves, they would

not be able to meet their expenses and would be at

risk of closure.

Financial reserves, in other words,

are serving the very purpose for which they are

intended—ensuring that hospitals and health systems

can continue to serve their communities in the face of

challenging operational and financial headwinds.

When these headwinds have subsided, rebuilding these

reserves should be a top priority to ensure that our

not-for-profit hospitals and health systems can remain

a vital resource for the communities they serve.