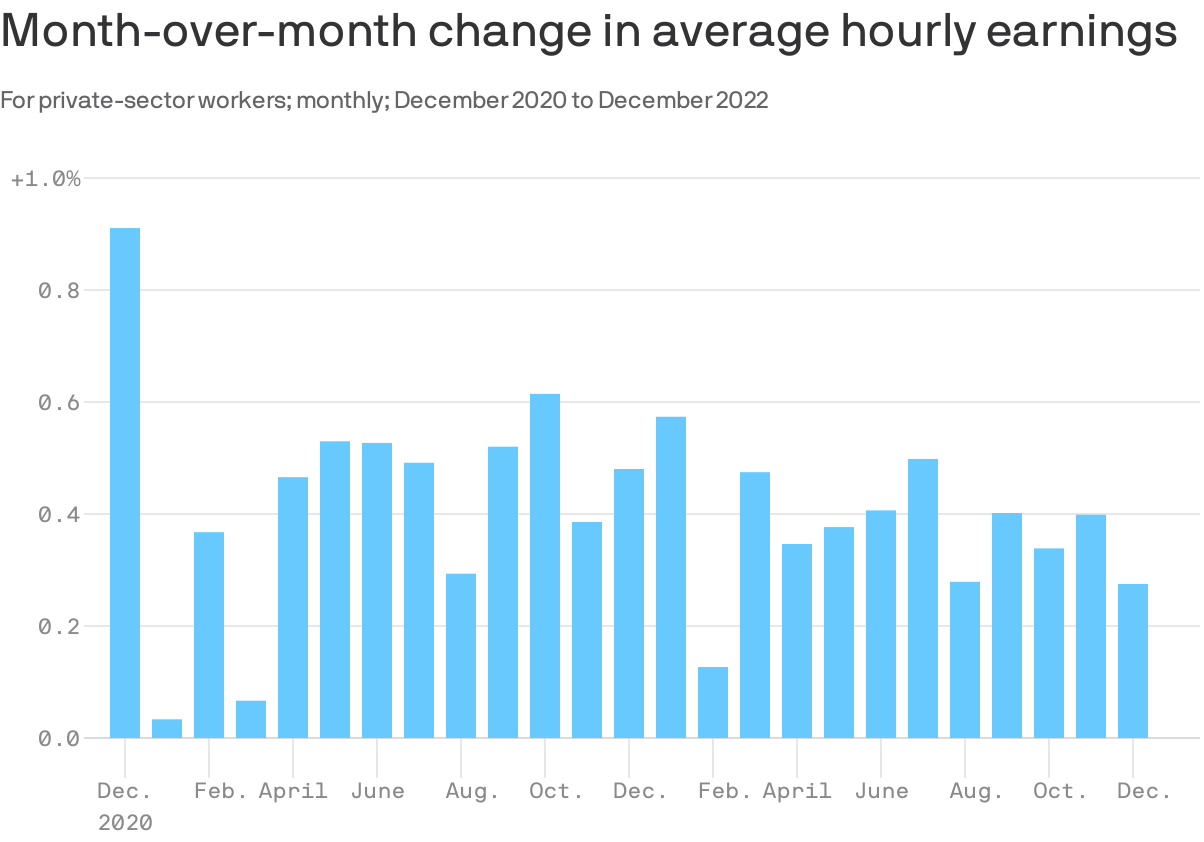

The Goldilocks nature of these jobs numbers is particularly apparent in the wage data.

By the numbers: Average hourly earnings rose by 0.3% in December, and are up 4.6% over the last year. Over the last three months, worker pay rose at a 4.1% annual rate.

Wages are rising, but unlike a year ago, the pace is consistent with the economy settling into the 2% inflation that the Fed seeks.

For example, there were stretches in 2018 and 2019 that featured wage growth similar to that in Q4 paired with low inflation levels — which meant rising real wages for workers.

In other words, current pay growth, if sustained, would help diminish the Fed’s fears of an upward spiral of wages and prices. Also, it sets workers up to see gains in their real compensation, if and when inflation comes down.

The intrigue: It appears that a surge in earnings initially reported in November was a head fake. The Labor Department revised those numbers to show a 0.4% rise in hourly earnings, not the 0.6% first reported.

The original figures had been a source of alarm among Fed watchers, suggesting the central bank might need to step up its monetary tightening campaign.

It is a good reminder — for both policymakers and those of us in the media — to not overreact to single-month shifts in any volatile data series.

Financial analysts have said that 2022 may have been the worst year for hospital finances in decades. This year looks like it will be yet another year of financial underperformance, with rural providers in especially dire circumstances.

What’s driving this bleak financial reality? It’s “primarily an expense story,” said Erik Swanson, a senior vice president at Kaufman Hall‘s data analytics practice.

“Growth in expenses has vastly outpaced growth in revenues — since pre-pandemic levels since last year, and even the year prior — such that margins are ultimately being pushed downward. And hospitals’ median operating margin is still below zero on a cumulative basis,” he declared, referring to 2021 and 2020.

Here’s some context about how dismal this situation is: Even in 2020, a year in which hospitals saw extraordinary losses during the first few months of the pandemic, they still reported operating margins of 2%.

What’s even more disconcerting is that hospitals are underperforming financially pretty much across the board, Swanson said.

Even Kaiser Permanente, one of the country’s largest health systems with an integrated delivery model, reported a $1.5 billion loss for the third quarter of 2022.

Rural hospitals are in even worse shape, but more on that below.

Other hospitals have been forced to shutter service lines to offset these financial losses. Some are also turning to integration and consolidation.

For example, Hermann Area District Hospital in Missouri said last month that it is seeking a “deeper affiliation” with Mercy Health or another provider. This announcement came after the hospital eliminated its home health agency as a cost-cutting measure. In December, the hospital projected a loss of $2 million for 2022.

We can also look at the mega-merger between Atrium Health and Advocate Aurora Health, which was completed last month. The deal, which is designed for cost synergy, creates the fifth-largest nonprofit integrated health system in the U.S.

The merger was finalized one day after North Carolina Attorney General Josh Stein expressed concern about how the deal could impact rural communities. He said that while he didn’t have a legal basis within his office’s limited statutory authority to block the deal, he was worried that it could further restrict access to healthcare in rural and underserved communities.

Stein brings up an extremely valid concern. Rural hospitals’ dismal financial circumstances are becoming more and more worrisome — in fact, about 30% of all rural hospitals are at risk of closing in the near future, according to a recent report from the Center for Healthcare Quality and Payment Reform (CHQPR).

A crucial reason for this is that it is more expensive to deliver healthcare in rural areas — usually because of smaller patient volumes and higher costs for attracting staff. Another factor is that payments rural hospitals receive from commercial health plans isn’t enough to cover the cost of delivering care to patients in rural areas, said Harold Miller, CEO of CHQPR.

“Many people assume that private commercial insurance plans pay more than Medicare and Medicaid. But for small rural hospitals, the exact opposite is true,” he said. “In many cases, Medicare is their best payer. And private health plans actually pay them well below their costs — well below what they pay their larger hospitals. One of the biggest drivers of rural hospital losses is the payments they receive from private health plans.”

In Miller’s view, rural hospitals perform two main functions: taking care of sick people in the hospital and being there for people in case they need to go to the hospital.

To fulfill the latter job, rural hospitals must operate 24/7 emergency rooms. These hospitals get paid when there’s an emergency, but not when there isn’t — even though the hospital is incurring costs by operating and staffing these units.

“Rural hospitals have a physician on duty 24/7 to be available for emergencies. But they don’t get paid for that by most payers. Medicare does pay them for that, but other payers don’t. If the hospital is doing two different things, we should be paying them for both of those things. Hospitals should be paid for what I refer to as ‘standby capacity,’” Miller said.

He bolstered his argument by pointing to these analogies: Do we only pay firefighters when there’s a fire? Do we only pay police officers when there’s a crime?

It’s also important to remember that rural hospitals are in the midst of transitioning to a post-pandemic environment, now without the pandemic-era financial assistance they received from the government, said Brock Slabach, chief operations officer at the National Rural Health Association.

“Rural providers are looking to move into the future without the benefit of those extra payments. And they’re in an environment of really high inflation. It’s over 8%, and for some goods and services in the healthcare sector, that’s going to be over 20% in terms of increased prices. Wages and salaries have also gone up significantly. But patient volumes have maintained below average or average. That all presents a huge challenge,” Slabach said.

Rural providers across the country are dealing with the stressors Slabach described and clamoring for more government help. For example, the Michigan Health & Hospital Association sought more money from the state last month after having to take 1,700 beds offline.

Many rural hospitals can’t escape their fate. From 2010 to 2021, there were 136 rural hospital closures. There were only two closures in 2021, and Slabach said 2022 produced a similarly low number. But these low totals are due to government relief, he explained. Slabach said he’s expecting an increase in rural hospital closures in 2023.

When a rural hospital closes, it means community members have to travel far distances for emergency or inpatient care. Miller pointed out another problem: in many rural communities, the hospital is the only place people can go to get laboratory or imaging work done. The hospital might also be the only source of primary care for the community. Shuttering these hospitals would be a massive blow to rural Americans’ healthcare access.

In the face of these potentially devastating blows to patient access, financial analysts’ outlook is bleak.

Higher inflation and costly labor expenses will continue to have negative effects on hospitals — both rural and urban — in 2023, according to an analysis from Moody’s. Expenses will also continue to increase due to supply chain bottlenecks, the need for more robust cybersecurity investments and longer hospital stays due to higher levels of patient acuity.

All of this doom and gloom begs the question — are any hospitals doing well financially?

The answer is yes, a select few. Let’s look at the three largest for-profit health systems in the nation — Community Health Systems, HCA Healthcare and Tenet Healthcare. As of 2020, these three public health systems accounted for about 8% of hospital beds in the U.S.

These three systems all had positive operating margins for the majority of the pandemic, including most recently in the third quarter of 2022.

Large public health systems have shareholders to report to and stock prices to worry about. Does this mean they’re more likely to deny care to patients who can’t afford it while other hospitals pick up the slack?

Slabach said it’s tough to say.

“Obviously, hospitals try to mitigate their exposure to risk when it comes to taking care of patients. Most hospitals do a really good job of providing services and care to people who don’t have insurance or don’t have the means to pay. But that gets stressed in this current financial environment. So indeed, there may be instances where what you suggested might happen, but it’s not because they want to deny services or deny care. It’s because they have a bigger picture they have to maintain,” Slabach said.

And the big picture involving dollar signs for hospitals looks pretty bleak in 2023.

Two nonprofit insurers, Long Beach, CA-based SCAN Group and Portland, OR-based CareOregon, have agreed to merge. The new organization—which will take the name HealthRight Group, while retaining the SCAN and CareOregon brands in local markets—will have $6.8B in annual revenue and cover around 800K lives.

Continuing their previous areas of focus, SCAN will cater primarily to Medicare Advantage (MA) beneficiaries, and CareOregon will prioritize serving managed Medicaid enrollees. Executives from both companies cited scale as the primary motivation for the merger, with the companies aiming to both strengthen their foothold in current markets and expand their reach into new ones.

The deal, which still needs approval from state regulators, is expected to close in 2023.

The Gist: HealthRight stands to be a strong player in the booming government-backed, managed care market in states currently dominated by large payers like Kaiser Permanente and UnitedHealthcare.

SCAN has differentiated itself with services dedicated to underserved populations, including creating a MA plan designed for LGBTQ+ seniors, and offering California’s only integrated dual-eligible, special needs plans. We expect the addition of CareOregon’s 319K managed Medicaid members to provide a larger platform for these targeted initiatives, and we wouldn’t be surprised to see more nonprofit insurers joining forces with HealthRight to better compete with current market heavyweights.

Charlotte, NC-based Atrium Health and Downers Grove, IL- and Milwaukee, WI-based Advocate Aurora Health have formally combined to become the nation’s fifth-largest nonprofit health system. Taking the name Advocate Health, the $27B system will control 67 hospitals across six states in the Midwest and Southeast. The merger, announced in May of this year, unites the systems on even footing, with equal representation on a new board of directors, and a co-CEO arrangement for the first 18 months. The Atrium, Advocate, and Aurora brands will continue to be used in their respective local markets.

The Gist: Structuring Advocate Health as a joint operating agreement, and creating a new superstructure atop the two legacy systems, should allow the combined entity more flexibility in local decision-making, while still potentially generating cost savings from back-office efficiencies.

While we expect these kinds of mega-mergers between large regional systems to continue, it remains to be seen whether the newly combined systems can successfully create value by building larger “platforms” of care to win consumer loyalty, deploying digital capabilities, attracting talent, and becoming more desirable partners for nontraditional players.

VillageMD, which is majority owned by Walgreens Boots Alliance, plans to shell out nearly $9 billion to pick up medical practice Summit Health, the parent company of urgent care clinic chain CityMD.

The deal, announced Monday morning, is valued at $8.9 billion and includes investments from Walgreens Boots Alliance and Cigna Corp’s healthcare unit Evernorth, which will also become a minority owner in VillageMD. Bloomberg first reported on a potential deal back in late October.

The deal will expand Walgreen’s reach into primary, specialty and urgent care. The transaction creates one of the largest independent provider groups in the U.S., the organizations said. Combined, VillageMD and Summit Health will operate more than 680 provider locations in 26 markets. The two companies will have 20,000 employees.

Walgreens said Monday it will invest $3.5 billion through an even mix of debt and equity to support the acquisition, which is expected to close in the first quarter of 2023. The company will remain the largest and consolidating shareholder of VillageMD with about 53% stake.

Walgreens also raised its fiscal year 2025 sales goal for its U.S. healthcare business to between $14.5 billion and $16 billion from $11 billion to $12 billion previously. That business segment is now expected to achieve positive adjusted EBITDA by the end of fiscal year 2023.

Last year, Walgreens invested $5.2 billion in VillageMD and said it planned to open at least 600 Village Medical at Walgreens primary-care practices across the country by 2025 and 1,000 by 2027.

The deal comes amid a frenzy of M&A activity in the past two years. Major retailers like CVS, Walgreens and Amazon are ramping up their focus on providing medical services to gain bigger footholds in the healthcare market.

Drugstore rival CVS Health won the bidding war for home health and technology services company Signify Health and plans to shell out $8 billion to acquire the company. Amazon also plans to buy primary care provider One Medical for $3.9 billion.

The M&A move signals that Walgreens wants to become a “dominant entity in the overall healthcare services ecosystem,” according to David Larsen, healthcare IT and digital health analyst at financial services firm BTIG.

“Walgreens Boots Alliance is graduating up from being a drug retail store to owning the life-cycle of members’ health,” he wrote in an analyst’s note. “We view this transaction as being a statement by the market that primary care continues to be one of the key drivers of healthcare long-term.”

The deal also will put additional pressure on CVS Health to break into the primary care business “sooner rather than later,” Larsen wrote.

“I think at the most strategic level, I think there continues to be recognition that an integrated, coordinated, connected model of care is one that will ultimately deliver the best results. You see this through Optum’s acquisition of Kelsey-Seybold Clinic and VillageMD’s acquisition of Summit Health,” Tim Barry, CEO and chair of VillageMD, said in an interview with Fierce Healthcare.

“If we’re going to ultimately stem the rising tide of this fee-for-service healthcare system, we need a better solution, and that solution needs to have doctors working with other doctors in a coordinated way and trying to solve the unique problems that these patients have and making sure that the right doctors are accessing the patient at the right time, and doing it all underneath the umbrella of a risk-based contract,” Barry said.

He added, “We think that this is going to continue to be where healthcare goes. And, we have to do it in a way that is integrated and value-oriented. Any organization focused on doing that, and doing that at size and scale, is going to continue, I think, to be the successful winners of our healthcare system.”

In 2019, Summit Medical Group, a physician-owned and governed multispecialty group, merged with CityMD, a leading urgent care company in New York City. The combined organization, Summit Health, has more than 370 locations in New Jersey, New York, Connecticut, Pennsylvania and Oregon.

VillageMD provides value-based primary care for patients at traditional free-standing practices, Village Medical at Walgreens practices, at home and via virtual visits. VillageMD and Village Medical have grown to 22 markets and are responsible for more than 1.6 million patients, according to the company.

Barry said the combination of VillageMD and Summit Health-CityMD will enable the organizations to scale up value-based care and build out integrated primary and specialty care services.

“If you look at the long history of Summit Health, it’s an organization that has done some very innovative things. The way that they deliver multispecialty care, it is truly integrated, it’s truly connected and they are known as the preeminent brand in their marketplace. They also have CityMD, which is one of the more unique and differentiated urgent care models out there in the market. They really are a best-of-breed organization,” he said.

“When I look at what we’ve been able to do at VillageMD, we built this incredible model of value-based primary care delivery. The idea of bringing these two organizations together to bring those best-of-breed capabilities under one umbrella was just so compelling. We will soon be able to offer a more comprehensive, integrated and connected model by also offering other specialty services to our patients, but all still done through a value or risk-based reimbursement structure.”

Barry is bullish on the combined capabilities of the two companies in the primary and specialty care markets.

“We’ll be delivering a consistent value-based model of integrated, multispecialty care in a way that delivers the best clinical results on the planet,” he said.

Jeff Alter, CEO of Summit Health-CityMD, said in a statement that the deal adds Summit Health’s expertise and geographic coverage to VillageMD’s proven value-based primary care approach.

The acquisition also expands Walgreens’ reach into providing medical care directly to patients. “This transaction accelerates growth opportunities through a strong market footprint and wide network of providers and patients across primary, specialty and urgent care,” Roz Brewer, CEO of Walgreens Boots Alliance, said in a statement.

With Cigna’s investment, the combined company will be able to tap into Evernorth’s health services capabilities to potentially lower healthcare costs, Barry said. Evernorth encompasses Cigna’s health services businesses including pharmacy benefit manager Express Scripts

“In order to be a risk-based provider or a value-based provider, you have to have contracts with a payer that allows you to work in this value or risk-based construct. We learned over the years that Cigna has been a really good partner to us on that journey,” Barry said.

“There are companies that [Cigna] has purchased over the years that have different specializations and capabilities that we believe ultimately will allow us to deliver better care to our patients,” he noted. “Evernorth has some capabilities tied to behavioral health, and they have some capabilities tied to the management of specialty pharmaceutical spend, which everyone knows those costs continue to be soaring. We both liked the idea of supporting an organization like ours that’s going to continue to grow and continues to be focused on risk and value.”

With the investment in VillageMD and Summit Health, Cigna gets a leg up in the primary care space as it looks to build out its Evernorth division.

“Our collaboration with VillageMD accelerates our efforts to improve the way care is accessed and delivered,” said Eric Palmer, CEO of Evernorth, in a statement. “Harnessing the breadth of Evernorth’s health services capabilities and connecting them with physicians who provide care in a value-based model like VillageMD, helps more people to get the right care at the right time—driving better health and value.”

Consolidation continues across the healthcare industry with many hospitals and health systems looking to complete planned acquisitions or sales by the end of 2022 or early 2023.

Here are 15 planned hospital or health system sales that Becker’s Hospital Review has reported on in the last month:

1-2. El Segundo, Calif.-based Pipeline Health System, which filed for Chapter 11 bankruptcy in October, has agreed to sell two hospitals — Weiss Memorial Hospital in Chicago and West Suburban Medical Center in Oak Park, Ill. — to Princeton, N.J.-based Ramco Healthcare Holdings and Resilience Healthcare.

Pending approval of a motion submitted Nov. 22 to the U.S. Bankruptcy Court for the Southern District of Texas, Resilience is expected to assume operations of the two hospitals on Dec. 2.

Since acquiring ownership of the hospitals in 2019, Pipeline said it has invested $60 million to improve facilities, add technology and expand clinical programs. The hospitals employ a combined total of 1,700 employees.

3-4. The Centurion Foundation, an Atlanta-based nonprofit organization, has inked an asset purchase agreement to acquire the CharterCare Health Partners system from Los Angeles-based Prospect Medical Holdings.

Two hospitals are included in the transaction: Providence, R.I.-based Roger Williams Medical Center and Our Lady of Fatima Hospital. The change in control application process is expected to be submitted to the Rhode Island Department of Health and the state attorney general before the end of 2022.

5. West Reading, Pa.-based Tower Health plans to sell Chestnut Hill Hospital in Philadelphia to Temple University Health System for $28 million. The news comes less than a year after the health system closed two other hospitals: Brandywine Hospital in Coatesville, Pa., and Jennersville Hospital in West Grove, Pa.

Tower Health plans to rebuild around its flagship Reading Hospital and the two other hospitals it acquired for $423 million from Franklin, Tenn.-based Community Health Systems: Phoenixville Hospital and Pottstown Hospital. It also owns St. Christopher’s Hospital for Children in Philadelphia in a joint venture with Drexel University.

6. As of Nov. 14, potential buyers can submit offers for Singing River Health System, a three-hospital system with locations in Ocean Springs, Pascagoula and Gulfport, Miss.

Supervisors from Jackson County — which owns the health systems — gave the green light for proposals to sell Singing River Health System. Potential buyers have until March 10 to submit their bids.

7-9. New Orleans-based LCMC Health plans to acquire three Tulane University hospitals — New Orleans-based Tulane Medical Center; Covington, La.-based Lakeview Regional Medical Center; and Metairie, La.-based Tulane Lakeside Hospital — from Nashville, Tenn.-based HCA Healthcare.

LCMC Health will purchase the three hospitals for $150 million, expanding its portfolio to nine hospitals in the New Orleans area. The two parties hope to finalize the deal by the end of 2022 or early 2023.

10-12. Peoria, Ill.-based UnityPoint Health – Central Illinois and Des Moines, Iowa-based UnityPoint Health plans to spin off three Illinois hospitals to Urbana, Ill.-based Carle Health.

The transaction results in Carle Health taking over as the parent organization of UnityPoint Health – Central Illinois, which includes Peoria-based Methodist and Procter, and Pekin (Ill.) Hospitals and affiliated clinics, Peoria-based UnityPlace and Methodist College.

An April 1 closing date is anticipated, pending all regulatory approvals.

13. Hill Country Memorial Hospital in Fredericksburg, Texas, has entered into an agreement to become part of San Antionio-based Methodist Healthcare System.

Hill Country Memorial has 15 locations, including a hospital, an urgent care clinic, and primary and specialty care offices. Methodist Healthcare — a 50-50 co-ownership between HCA Healthcare and Methodist Healthcare Ministries of South Texas — has more than 30 facilities, including eight hospitals and nine freestanding emergency departments.

The transaction is expected to be completed in early 2023.

14. Orlando (Fla.) Health plans to acquire Sabanera Health Dorado, an acute care hospital in Puerto Rico.

The hospital will change its name to Doctors’ Center Hospital-Orlando Health Dorado, according to Orlando Health, which will team up with four additional hospitals operated by the Doctors’ Center Hospital team. The operation of all five hospitals will remain with the Doctors’ Center Hospital group.

15. Tacoma, Wash.-based MultiCare Health System and Yakima (Wash.) Valley Memorial reached an acquisition agreement, according to an Oct. 21 news release shared with Becker’s Hospital Review.

Terms of the agreement include Memorial becoming a wholly owned subsidiary of MultiCare, MultiCare investing in new programs, installing an integrated electronic health record, and providing a sustainable future for Yakima’s only hospital. The transaction is subject to routine regulatory approval and closing conditions.

Wall Street’s roil has stabilized somewhat in recent days, with the S&P 500 brushing up against its 200-day moving average and rising more than 10 percent since its October lows, as of publication time.

The index’s 50-day moving average is trending up, according to financial data firm Refinitiv. But it still must climb another 7.4 percent to form a “golden cross,” which is when a stock or index’s short-term moving average rises above one of its longer-term moving averages. The S&P 500’s 20-day and 100-day moving averages are closer to the milestone, only needing increases of 5 percent and 1.2 percent, respectively.

The Dow Jones Industrial Average has already formed a small golden cross: its 20-day moving average is 1.2 percent higher than its 200-day moving average.

Investors Optimistic about Healthcare Sector

– Investors are most optimistic about the Healthcare sector, which is trading close to its 3-year average “price to earnings-per-share” ratio of 48.1x, according to Simply Wall Street.

– Analysts are expecting an annual earnings growth of 13.4 percent, higher than the sector’s past year earnings growth of 5 percent.

– Merck and Johnson & Johnson were among last week’s top gainers driving the market.

Inflation Appears to be Slowing

– The recent lower-than-expected inflation figures could indicate it is slowing.

– The Fed may continue raising rates, considering the strength in recent labor market and retail sales data.

Cash reserves, an important indicator of financial stability, are dropping for hospitals and health systems across the U.S.

Both large and small health systems are affected by rising labor and supply costs while reimbursement remains low. St. Louis-based Ascension reported days cash on hand dropped from 336 at the end of the 2021 fiscal year to 259 as of June 30, 2022, the end of the fiscal year. The system also reported accounts receivable increased three days from 47.3 in 2021 to 50.3 in 2022 because commercial payers were slow, especially in large dollar claims.

Trinity Health, based in Livonia, Mich., also reported days cash on hand dropped to 211 in fiscal year 2022, ending June 30, compared to 254 days at the end of 2021. Trinity attributed the 43-day decrease in cash on hand to “investment losses and the recoupment of the majority of the Medicare cash advances.”

Chicago-based CommonSpirit Health reported days cash on hand decreased by 69 days in the last year. The 140-hospital health system reported 245 days cash on hand at the 2021 fiscal year’s end June 30, and 176 days for 2022.

Lehigh Valley Health Network in Allentown, Pa., said unfavorable trends in the capital market led to investment losses and a drop in days cash on hand from 216 to 150 days in the 2022 fiscal year ending June 30. The health system also had a scheduled repayment of $191.1 million in advance Medicare dollars as well as $25 million in deferred payroll tax payments.

Philadelphia-based Thomas Jefferson Universityreported cash on hand for clinical operations dropped by 10.9 days in just the last quarter due to nonoperating investment losses and repaying government advances, which equaled about five days cash on hand. The health system reported 158.5 days cash on hand as of Sept. 30.

While the large health systems’ days cash on hand are dropping, they still have deep reserves. Smaller hospitals and health systems are in a more dire situation. Doylestown (Pa.) Hospital reported as of Sept. 30 the system had 81 days cash on hand, and Moody’s downgraded the hospital in June after the days cash on hand dropped below 100.

Kaweah Health in Visalia, Calif., saw reserves plummet since the pandemic began from 130 to 84 days cash on hand. Gary Herbst, CEO of Kaweah Health, blamed lost elective procedures, high labor costs, inflation and more for the system’s financial issues.

“The COVID-19 pandemic, and its aftermath, have brought District hospitals to the brink of financial collapse,” Mr. Herbst wrote in an open letter to Gov. Gavin Newsom published in the Visalia Times Delta. He asked Mr. Newsom to provide additional funding for public district hospitals. “Without your help, it will soon be virtually impossible for Medi-Cal patients to receive anything but emergency medical care in the State of California.”

Private equity groups have invested about $1 trillion into nearly 8,000 healthcare transactions in the past decade, and some experts are pushing for more scrutiny of its increasing influence on the industry amid concern it may be causing higher medical bills and diminished quality of care, a Nov. 14 Kaiser Health News report said.

Because such investment groups typically invest less than $101 million, such transactions do not attract automatic antitrust reviews at the federal level, the report continued. That represents more than 90 percent of private equity investments in the industry.

Nevertheless, companies owned or managed by private equity groups have agreed to pay fines of more than $500 million since 2014 in over 30 lawsuits under the False Claims Act, which deals with false billing submissions, KHN’s investigation found.

The problem may be most acute in certain specialist fields and in certain metropolitan areas. While private equity, for example, plays a role in just 14 percent of gastroenterology practices nationwide, it controls about 75 percent of that market in at least five metropolitan areas across five states, including Texas and North Carolina, according to research from UC Berkeley’s Nicholas C. Petris Center.

And private equity pockets may be getting deeper. In 2021 alone, over $206 billion was invested by such groups in healthcare, and there is plenty of “dry powder” around for more, KHN reported. The Healthcare Private Equity Association, for example, which boasts about 100 investment companies as members, says the firms have $3 trillion in assets awaiting allocation.

Private equity, like everything else, may have some poor performers but it doesn’t help to generalize as groups “vary tremendously” in how they operate their healthcare investments, Robert Homchick, a Seattle attorney, told KHN.

“Private equity has some bad actors, but so does the rest of the [healthcare] industry,” he said. “I think it’s wrong to paint them all with the same brush.”

Concerns remain, however, that, at least in some cases, private equity involvement is simply a vehicle for maximizing returns, often at the expense of patients. In addition to the $500 million fines, there is also evidence of some private equity groups pushing through additional testing and mandated patient numbers to boost returns, often in medically questionable scenarios, the report said, citing the example of National Spine and Pain Centers previously owned by private equity group Sentinel Partners.

In that case, National Spine paid $3.3 million in a whistleblower case related to allegations of unnecessary treatment and testing, KHN said.

The scope of such private equity dominance in some markets worries many industry observers, and much more needs to be done to help reel in such potential abuses, they say.

“We’re still at the stage of understanding the scope of the problem,” said Laura Alexander, former vice president of policy at the nonprofit American Antitrust Institute, which collaborated on the Petris Center research. “One thing is clear: Much more transparency and scrutiny of these deals is needed.”