Cartoon – Pandemic Results

Here are 11 health systems and hospitals with strong operational metrics and solid financial positions, according to reports from Fitch Ratings, Moody’s Investors Service and S&P Global Ratings.

1. Morristown, N.J.-based Atlantic Health System has an “Aa3” rating and stable outlook with Moody’s. The credit rating agency expects the health system to continue to generate favorable operating performance and to maintain double-digit operating cash flow margins and solid debt coverage.

2. Charlotte, N.C.-based Atrium Health has an “Aa3” rating and stable outlook with Moody’s and an “AA-” rating and stable outlook with S&P. Atrium and Winston-Salem, N.C.-based Wake Forest Baptist Health merged in October. The addition of the Winston-Salem service area and Wake Forest Baptist’s academic and research programs enhances Atrium’s position within the highly competitive North Carolina healthcare market, S&P said.

3. Dallas-based Baylor Scott & White Health has an “Aa3” rating and stable outlook with Moody’s. The system has strong liquidity and is the largest nonprofit health system in Texas, Moody’s said. The credit rating agency expects Baylor Scott & White Health to continue to benefit from its centralized operating model, proven ability to execute complex strategies and well-developed planning abilities.

4. Pittsfield, Mass.-based Berkshire Health System has an “AA-” rating and stable outlook with Fitch. The health system has improved its liquidity while investing in facilities without increasing its debt load, Fitch said. The credit rating agency expects the system to maintain a strong financial profile.

5. Mishawaka, Ind.-based Franciscan Alliance has an “Aa3” rating and stable outlook with Moody’s. The system has leading positions in key markets and a strong cash position, Moody’s said. The credit rating agency expects the system to sustain double-digit operating cash flow margins.

6. Falls Church, Va.-based Inova Health System has an “Aa2” rating and stable outlook with Moody’s. The system has a strong financial profile, and Moody’s expects Inova’s balance sheet to remain exceptionally strong.

7. Palo Alto, Calif.-based Lucile Packard Children’s Hospital at Stanford has an “AA-” rating and stable outlook with Fitch. The hospital is nationally known, has a strong market position and is one of two key clinical partners of Stanford University, Fitch said.

8. Grand Blanc, Mich.-based McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The health system has a strong financial profile and a leading market position over a broad service area that covers much of Michigan, Fitch said.

9. Winston-Salem, N.C.-based Novant Health has an “AA-” rating and stable outlook with Fitch. The system has strong margins, and each of its markets has met or exceeded budgeted expectations over the past four years, Fitch said.

10. Renton, Wash.-based Providence has an “Aa3” rating and stable outlook with Moody’s. Providence has a large revenue base and a leading market share in most of its markets, according to Moody’s. The credit rating agency expects the system’s operations to improve this year.

11. Livonia, Mich.-based Trinity Health has an “AA-” rating and stable outlook with Fitch. The rating is driven by Trinity’s national size and scale, with significant market presence in several states, Fitch said. The credit rating agency expects the system’s operating margins to improve in the long term.

Mercy Hospital & Medical Center in Chicago filed for bankruptcy protection Feb. 10, amid its plan to close that has been contested in the community.

The Chapter 11 plan includes the discontinuation of inpatient acute care services, Mercy’s owner, Livonia, Mich.-based Trinity Health, said in a bankruptcy filing.

Mercy said it plans to cease operations of all departments, except for basic emergency services, on May 31.

“There have been many steps that preceded the difficult decision to file for Chapter 11,” Trinity said.

In a news release announcing the bankruptcy, Mercy said it was losing staff and “experiencing mounting financial losses” that are challenging its ability to provide safe patient care.

Mercy said its losses have averaged about $5 million per month and reached $30.2 million for the first six months of fiscal year 2021. Further, the hospital has accumulated debt of more than $303.2 million over the last seven years, and the hospital needs more than $100 million in upgrades and modernizations.

The Chapter 11 bankruptcy filing comes just weeks after the Illinois Health Facilities and Services Review Board rejected Trinity’s plan to build an outpatient center in the neighborhood where it is closing the 170-year-old inpatient hospital. The same board unanimously rejected Trinity’s plan to close the hospital in December.

The December vote from the review board came after months of protests from physicians, healthcare advocates and community organizers, who say that closing the hospital would create a healthcare desert on Chicago’s South Side.

The state review board has a meeting to discuss the closure March 16.

Patient volumes were uneven in 2020, and a new report shows volumes will likely remain below pre-pandemic levels in 2021. This indicates challenges for hospitals looking to stabilize their finances — but there are some key strategies that can help.

Though hospital finances recovered to some extent by the end of 2020, the industry is not out of the woods yet. However, with strategic investments, especially in outpatient care and technology, hospitals and health systems can help buoy their finances in this challenging time, industry observers said.

Patient volumes have fluctuated wildly after the Covid-19 pandemic hit as Covid-19 patients flocked to hospitals and those needing or seeking elective surgery and other care staying away. Not surprisingly, this has had a significant impact on health systems’ financial health.

But outpatient settings and digital solutions offer some revenue-generating opportunities for hospitals.

“A number of the major players and some of the bigger regional systems in the country now are in a place where they get more of their revenue from the outpatient side as opposed to the inpatient side,” said Dr. Sanjay Saxena, global healthcare leader, Payers, Providers, Health Care Systems & Services and managing director at Boston Consulting Group, in a phone interview.

In fact, outpatient care was the only healthcare setting that saw an increase in patient volumes in 2020. Though emergency department visits and inpatient volumes were down from July to December last year compared to the same period in 2019, outpatient volumes actually increased by 5%, according to a report by consumer credit reporting agency TransUnion.

Healthcare providers that have well-established and expansive outpatient and ambulatory care businesses will be able to weather patient volume trends better in 2021 than those who do not, said Saxena.

Take HCA Healthcare, for example. The Nashville, Tennessee-based healthcare giant’s revenues jumped to $14.2 billion in the fourth quarter of last year, up from $13.5 billion in the same period in 2019. HCA’s ability to move care outside of the inpatient setting to the ambulatory environment really helped their financial performance, said Saxena.

On the other hand, smaller and more rural hospitals, which depend heavily on ED and inpatient care, may face a challenging year, he added.

Another key investment for hospitals will be in digital solutions to help them manage the ups and downs of patient volume.

“Resilience as a broad topic for provider executives is absolutely top of mind,” said Gurpreet Singh, health services leader at PriceWaterhouseCoopers, in a phone interview. “And resiliency can be achieved in a number of different ways. One way is [figuring out] — can you predict demand a little bit better?”

Patient demand forecasting solutions will be popular, with 74% of health executives recently surveyed by PwC’s Health Research Institute saying their organizations would invest more in predictive modeling in 2021.

Further, hospitals will see savings in some unexpected places. For example, with an increasingly remote and mobile healthcare workforce, hospitals may see cost savings on real estate and facility leases, said Singh.

They can use these savings to invest further in telehealth and at-home care programs to expand care outside of the four walls of the hospital, he added.

The industry has to come to terms with changes brought on by the Covid-19 pandemic, including the shifts in care delivery and patient preferences.

“Some of these things are structurally significant changes,” said Saxena. “Organizations ignore these things…at their peril. Some leading organizations and systems will find a way to embrace [these changes] and leapfrog others in the market coming out of 2021.”

Tower Health said it is cutting salaries of executives and managers amid financial losses linked to the COVID-19 pandemic.

The West Reading, Pa.-based health system has struggled financially in the last two fiscal years. It recorded an operating loss of $378.2 million in fiscal year 2020, as well as an operating deficit of $178.8 million the year prior. And last November, the health system said it would consider selling six of its Philadelphia-area hospitals, including those it has purchased since 2017 from Franklin, Tenn.-based Community Health Systems, as part of a financial turnaround plan.

To help offset the financial damage, about 400 Tower Health executives and managers will have their pay cut, beginning in their Feb. 19 paychecks, according to The Philadelphia Inquirer, which cites a letter CEO Clint Matthews wrote to staff. Executives will have their pay cut by 15 percent, and directors, senior directors and associate vice presidents will have their pay cut by 10 percent.

In a statement shared with Becker’s on Feb. 8, the health system said it “is undertaking several initiatives as part of a coordinated plan to improve operations, strengthen care delivery and address the ongoing financial impact of COVID-19.”

“These actions include compensation reductions for executives and managerial employees, along with operational improvements to reduce costs and enhance revenue,” according to the Tower Health statement.

The salary cuts will be in effect until June 30, and do not affect front-line clinical or support staff, who received merit increases in January.

Tower Health projects cost savings of about $11.6 million because of the pay cuts.

“Reducing management compensation is a difficult but necessary decision that will stabilize and strengthen our financial performance as we continue to meet the challenges of the COVID-19 pandemic, as well as our ongoing mission of providing compassionate, accessible, high-quality, cost-effective healthcare to our communities,” the health system said.

https://mailchi.mp/2c6956b2ac0d/the-weekly-gist-january-29-2021?e=d1e747d2d8

As the oft-cited 10,000 Baby Boomers continue to age into Medicare each day, Medicare Advantage (MA) enrollment keeps accelerating. The graphic above highlights growth in the MA ranks across the last decade, showing that enrollment has more than doubled since 2010. By the end of this year, an estimated 42 percent of Medicare beneficiaries will get their benefits through a private health insurer.

While seniors like MA plans for the growing number of supplemental benefits they can offer—which now include adult day care services, home-based palliative care, and in-home support services—health insurers are gravitating to these plans due to their attractive economics.

Health insurers’ average gross margin per member, per month (PMPM) for MA plans is significantly higher than in individual or group market plans, a spread that increased in 2020 due to reduced utilization. PMPM margins for MA plans were up an average of 35 percent through September 2020 compared to 2019.

Payers have been blanketing the market with plan options in recent years; the number of MA plans offered has increased 49 percent since 2017, although the MA market is increasingly concentrated. In spite of numerous headlines about venture-backed startups like Oscar, Bright Health Plan, and Devoted Health posting double- or triple-digit growth numbers, the MA market is still dominated by UnitedHealthcare and Humana, which together account for 44 percent of all MA enrollees nationwide.

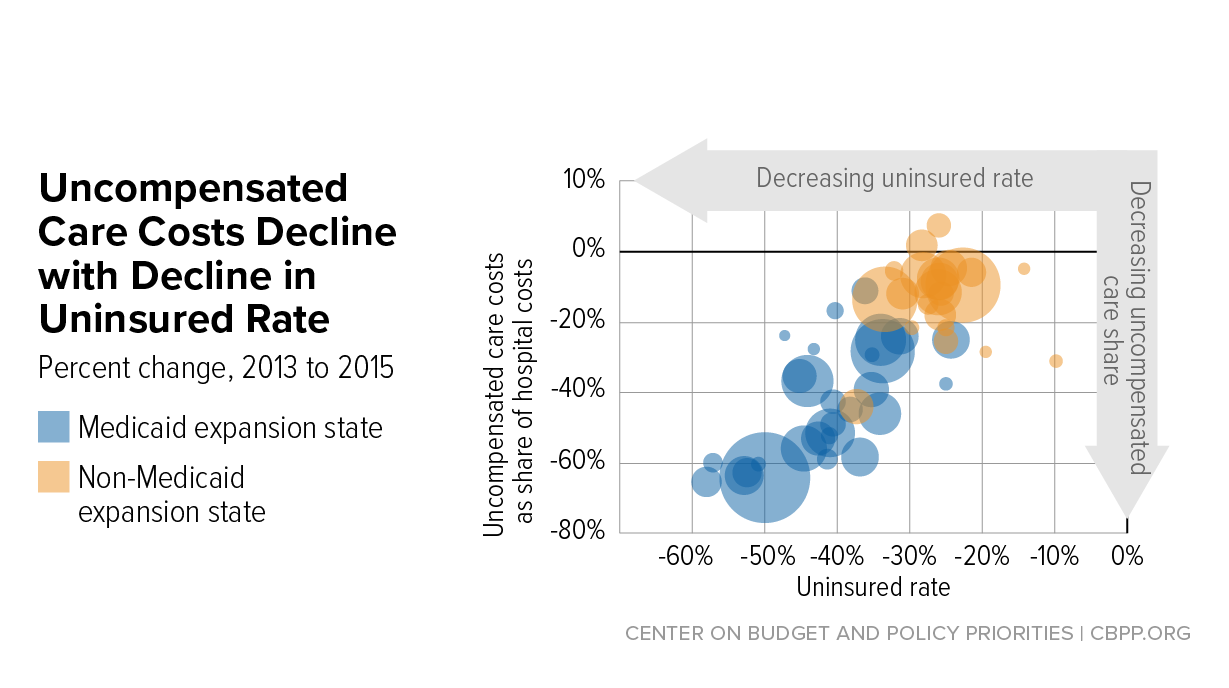

Hospital uncompensated care costs were up from $41.3B in 2018 and $38.4B in 2017, revealing an upward trend, according to AHA data.

Hospital uncompensated care costs increased right before the COVID-19 pandemic hit, according to new data from the American Hospital Association (AHA).

AHA data showed that hospitals incurred a new high of $41.61 billing in uncompensated care costs in 2019, the most recent year for which the group had complete data.

Uncompensated care costs in 2019 were up from $41.3 billion in 2018 and $38.4 billion in 2017 and were the second-highest per AHA records. Hospitals reported the most uncompensated care costs in 2013 when they incurred $46.8 billion.

Hospital uncompensated care costs decreased after the all-time high in 2013, but have recently started to tick back up after holding steady at $38.4 in 2016 and 2017.

In just the last 20 years, hospitals of all types have provided more than $660 billion in uncompensated care to patients, AHA reported. And that figure does not fully account for other ways in which provides provide financial assistance to patients of limited means, the group stated.

Each year, AHA aggregates data on uncompensated care, or care provided for which no reimbursement is received by hospitals from patients or payers. The data comes from the group’s Annual Survey of Hospitals, a comprehensive report of hospital financial data.

Uncompensated care is the sum of a hospital’s bad debt and financial assistance it provides, AHA explained.

Bad debt occurs when a hospital does not expect to obtain reimbursement for care provided, such as when patients are unable to pay their financial responsibility and do not qualify for financial assistance or are unwilling to pay their bills.

Hospitals also provide varying levels of financial assistance, AHA added. Financial assistance supports patients who cannot afford to pay and qualify for support from the hospital based on policies it has established based on the facility’s mission, financial condition, and geographic location, among other factors.

Combined, bad debt and financial assistance charges total a hospital’s uncompensated care charges, which is then multiplied by a hospital’s cost-to-charge ratio to determine total uncompensated care costs.

AHA noted that it expressed uncompensated care in costs versus charges because of significant variations in hospital payer mixes. Publishing the information as costs rather than charges enables better comparison across hospitals, the group said.

Nearly half of hospitals (48 percent) have seen bad debt and uncompensated care increase recently as a result of the ongoing COVID-19 pandemic, an analysis from consulting firm Kaufman Hall revealed.

More than 40 percent of hospitals also reported increases in percentage of uninsured or self-pay patients (44 percent) and the percentage of Medicaid patients (41 percent), which both contribute to unfunded or underfunded care at hospitals.

“The challenges brought on by the COVID-19 pandemic have affected nearly every aspect of hospital financial and clinical operations,” Lance Robinson, a managing director at Kaufman Hall, said at the time. “Organizations have responded to the challenge by adjusting their operations and strengthening important community relationships.”

Hospital uncompensated care costs – and bad debt as a result – are likely to increase in 2020 as hospitals come to terms with the impact COVID-19 has had on their financial health.

Already, hospitals have lost an estimated $323 billion in 2020 as a result of the COVID-19 pandemic, according to earlier projections from AHA.

About half of US hospitals also started the year in the red, AHA and Kaufman Hall stated in a recent report. The organizations predicted that hospital margins would sink to -7 percent in the second half of 2020 without comprehensive financial support from the government, but could decrease to a low of -11 percent if COVID-19 continued to periodically surge as it has.

Nearly a year after the first confirmed case of COVID-19 in the U.S., some of the nation’s largest health systems made a case for the need to accelerate toward value-based arrangements and potentially acquiring or partnering with health plans to become an integrated system.

Amid new records for deaths and cases from the novel coronavirus, executives gathered virtually for J.P. Morgan’s 39th annual healthcare conference, which typically draws prominent healthcare leaders to San Francisco at the start of each year.

The pandemic has been a heavily discussed topic during the digital gathering. One theme has been health systems either acknowledging they are on the hunt for health insurer acquisitions and partnerships or advocating for such arrangements as result of the challenges.

Anu Singh, managing director and the leader of the mergers, acquisitions and partnerships practice at consultancy Kaufman Hall, said it’s a natural migration for health systems, though it does come with some risk.

“If you want to move into the realm of being a population health manager, and take greater responsibility for your patient bases, you’re going to have to be thinking about maintaining their health,” Singh said. “And that’s typically something that, at least traditionally and historically, has been driven a little bit more by the health plan.”

For Utah’s Intermountain Healthcare, the lessons of the pandemic are clear: The industry needs to move away from a system that rewards volume. Intermountain is a fully integrated system that manages both providers and an insurance unit.

“It is becoming increasingly apparent that systems that are well integrated, especially systems that understand how to take risks, have prospered in the face of the terrible burden, caring for people in the midst of the first pandemic in 100 years,” Intermountain CEO Marc Harrison said Monday.

From his vantage point, Harrison said it has been interesting to watch the consternation around telehealth visits.

“Lots of folks who are really still caught in the volume-based system are actively switching patients back from tele- or distance to in-person visits so they can maximize revenue,” he said. “I understand that. But that’s a really great example of poorly aligned incentives.”

Intermountain has managed to stay in the black as many other systems have struggled financially as a result of the pandemic driving down patient volumes. It reported net income of $167 million through the first nine months of 2020, compared with $919 million the year prior.

Another integrated system, Baylor Scott and White Health, the largest nonprofit system in Texas, said such diversification has helped buoy its finances as hospital and clinic operations bottomed out in the spring due to the virus.

Baylor Scott and White illustrated this point by showing how operating income for its clinical segment took a nosedive in the spring while operating income for its health plan remained relatively steady.

The theme of integrated health systems also seemed to be on the minds of investors. CommonSpirit Health executives were asked during their presentation if buying or creating a health plan was on their radar as the system has a sizable footprint of 140 hospitals across the country.

“I think this is a interesting question, one that of course we’ve discussed many times strategically,” CFO Daniel Morissette said, noting the system does have a number of regional plans. “At this time, we have no plan of having a national CommonSpirit branded plan.” However, Morissette said the system would consider a partnership opportunity.

On the other hand, Midwest-based Advocate Aurora Health said it is actively on the hunt for a potential insurer deal as part of its long-term strategy.

“We do believe that having health plan capability, not necessarily having our own, but partnering for health plan capability, is going to be critical to our success, and we are taking steps to do that,” CEO Jim Skogsbergh said during the virtual conference.

Kaufman Hall said in its latest report that it expects more payer-provider partnerships as a result of the pandemic. “Limitations on fee-for-service payment structures exposed by the pandemic may increase the number of payer-provider partnerships around new payment and care delivery models,” according to the report.

Singh of Kaufman Hall said it’s not surprising that some may lean more toward a partnership due to the risks of starting a new venture, especially an insurance unit that can have “catastrophic loss”. Systems with less experience of moving toward implementing value-based initiatives may be more vulnerable to such risk.

It’s why he thinks partnerships may be a good fit, at least at first. Payers and providers can work together to improve the health of certain populations and then share in the cost savings.

Here are 14 health systems with strong operational metrics and solid financial positions, according to reports from Fitch Ratings, Moody’s Investors Service and S&P Global Ratings.

1. St. Louis-based Ascension has an “AA+” rating and stable outlook with Fitch and an “Aa2” rating and stable outlook with Moody’s. The system has a strong financial profile and a significant presence in several key markets, Fitch said. The credit rating agency expects Ascension will continue to produce healthy operating margins.

2. Charlotte, N.C.-based Atrium Health has an “Aa3” rating and stable outlook with Moody’s and an “AA-” rating and stable outlook with S&P. Atrium and Winston-Salem, N.C.-based Wake Forest Baptist Health merged in October. The addition of the Winston-Salem service area and Wake Forest Baptist’s academic and research programs enhance Atrium’s position within the highly competitive North Carolina healthcare market, S&P said.

3. Phoenix-based Banner Health has an “AA-” rating and stable outlook with Fitch and S&P. Banner’s financial profile is strong, even taking into consideration the market volatility that occurred in the first quarter of 2020, Fitch said. The credit rating agency expects the system to continue to improve operating margins and to generate cash flow sufficient to sustain strong key financial metrics.

4. Dallas- based Baylor Scott & White Health has an “Aa3” rating and stable outlook with Moody’s. The system has strong liquidity and is the largest nonprofit health system in Texas, Moody’s said. The credit rating agency expects Baylor Scott & White Health to continue to benefit from its centralized operating model, proven ability to execute complex strategies and well-developed planning abilities.

5. Newark, Del.-based ChristianaCare Health System has an “Aa2” rating and stable outlook with Moody’s. The health system has extensive clinical depth and includes Delaware’s largest teaching hospital, Moody’s said. The system’s strong market position will help it resume near pre-pandemic level margins in fiscal year 2021, according to Moody’s.

6. Falls Church, Va.-based Inova Health System has an “Aa2” rating and stable outlook with Moody’s. The system has a strong financial profile, and Moody’s expects Inova’s balance sheet to remain exceptionally strong.

7. Philadelphia-based Main Line Health has an “AA” rating and stable outlook with Fitch. The credit rating agency expects the system’s operations to recover after the COVID-19 pandemic and for it to resume its track record of strong operating cash flow margins.

8. Rochester, Minn.-based Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The system has an excellent reputation and generates strong patient demand at its academic medical centers in Minnesota, Arizona and Florida, Moody’s said. The credit rating agency said strong patient demand and proactive expense control measures would likely fuel good results for Mayo for the fiscal year that ended Dec. 31.

9. Midland-based MidMichigan Health has an “AA-” rating and stable outlook with Fitch. The system generated healthy operational levels through fiscal year 2020, and Fitch expects it to continue generating strong cash flow.

10. Chicago-based Northwestern Memorial HealthCare has an “Aa2” rating and stable outlook with Moody’s. The health system had strong pre-COVID margins and liquidity, Moody’s said. The credit rating agency expects the system to maintain strong operating cash flow margins.

11. Winston-Salem, N.C.-based Novant Health has an “AA-” rating and stable outlook with Fitch. The system has strong margins and each of its markets have met or exceeded budgeted expectations over the past four years, Fitch said.

12. Albuquerque, N.M.-based Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The health system has a strong financial profile and a leading market position in Albuquerque and throughout New Mexico, Fitch said. The credit rating agency said it believes Presbyterian Healthcare Services is more resilient to pandemic disruptions than most other hospital systems.

13. Renton, Wash.-based Providence has an “Aa3” rating and stable outlook with Moody’s. Providence has a large revenue base and a leading market share in most of its markets, according to Moody’s. The credit rating agency expects the system’s operations to improve this year.

14. Livonia, Mich.-based Trinity Health has an “AA-” rating and stable outlook with Fitch. The rating is driven by Trinity’s national size and scale, with significant market presence in several states, Fitch said. The credit rating agency expects the system’s operating margins to improve in the long term.

Hospital margins and revenues continued to fall in November, while expenses remained above 2019 levels, according to Kaufman Hall’s December Flash report, which examines metrics from the previous month.

The median hospital operating margin in November was 2.5 percent year to date with funding from the Coronavirus Aid, Relief and Economic Security Act. Without the funds, the median hospital operating margin narrowed to -1.1 percent.

Skyrocketing COVID-19 cases are already stretching hospitals’ capacity, and Kaufman Hall expects the situation to worsen in coming months as holiday gatherings and colder weather push case counts up even further.