While many hospitals face financial hardships and rising expenses from the COVID-19 pandemic, several large health systems ended 2021 with profits above $1 billion.

These big health systems attributed the financial performance to several factors, including bigger investment gains and higher-acuity patients.

Seven health systems that posted net income of $1 billion last year:

1. Pittsburgh-based UPMC, an integrated delivery system with 40 hospitals, recorded a net income of $1.1 billion in 2021, driven by an operating income of $843 million and nonoperating gains of $810 million.

2. AdventHealth, a 48-hospital system based in Altamonte Springs, Fla., recorded a net income of $1.5 billion in 2021. The net income included an operating income of $994.6 million and investment gains of $517.7 million. In 2020, the health system’s net income was $914.8 million.

3. Cleveland Clinicreported a 66.7 percent increase in net income for the 12 months ended Dec. 31. The 19-hospital system saw its net income hit $2.2 billion, including an operating income of $746.3 million and investment gains of $1.4 billion.

4. Rochester, Minn.-based Mayo Clinic’s net income for 2021 was $3.6 billion, up from $2.5 billion a year earlier. The results included an operating income of $1.2 billion.

5. Driven by strong investment gains, Oakland, Calif.-based Kaiser Permanenterecorded a net income of $8.1 billion in 2021, an increase of $1.7 billion from 2020. The sharp rise in net income from the integrated delivery system with 39 hospitals included $7.5 billion in other income, including investment gains, and $611 million in operating income for 2021.

6. Nashville, Tenn.-based HCA Healthcare, a 182-hospital system, reported a net income of $7.7 billion in 2021, including investment gains and operating profits.

7. Tenet Healthcare, a 60-hospital system based in Dallas, reported net income of $1.5 billion on revenues of $19.5 billion in 2021. Tenet ended the 12-month period with an operating income of $2.9 billion, up from $2 billion recorded one year before. It also recorded losses on nonoperating activities and said its results for the year ending Dec. 31 included a pretax gain of $406 million associated with the divestiture of five Miami area hospitals, as well as stimulus funds totaling $205 million.

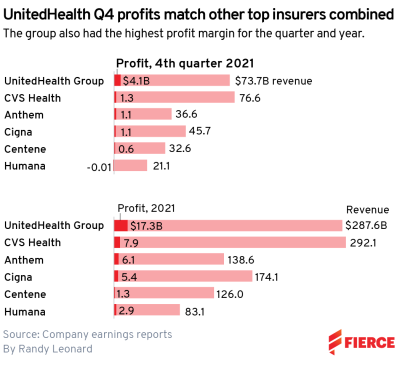

UnitedHealth Group was the most profitable payer in 2021, bringing in more than double the profit of itsnext-closest competitor with $17.3 billion in earnings.

CVS Health recorded the second-highest profit for the year among six major national insurers, earning $7.9 billion. CVS did bring in the highest revenue for the year, though, edging out UnitedHealth with $292.1 billion.

UHG reported $287.6 billion in revenue for 2021, according to the company’s earnings report.

Both healthcare giants expect to top $300 billion in revenue this year, according to their forecasts.

UnitedHealth was also the fourth quarter’s most profitable company, raking in $4.1 billion, which matched what its competitors earned combined, according to the filings.

UnitedHealth Group’s results represented significant growth over both the full-year and fourth quarter of 2020. According to its earnings report, this was driven in part by gains in Medicare Advantage and Medicaid at UnitedHealthcare as well as another quarter of double-digit growth at Optum.

CVS was also the next-highest earner in Q4, with $1.3 billion in profit on $76.6 billion in revenue. UHG was just behind on revenue with $73.7 billion.

CVS Health executives said that the retail business outperformed expectations in the fourth quarter amid increased demand for COVID-19 tests and booster shots.

The healthcare giant performed 32 million tests and 59 million vaccine doses over the course of the year, with 8 million tests and 20 million vaccinations reported in the fourth quarter alone.

While CVS and UnitedHealth duked it out for the top spot, all six of the big national payers were profitable for 2021, though Humana did post a $14 million loss for the fourth quarter.

Centene Corporation lands in sixth place for the year in profitability, bringing in $1.3 billion in profit on $126 billion in revenue. It also reported $599 million in profit for Q4.

Humana earned $2.9 billion for the year and $83.1 billion in revenue despite the Q4 loss, according to the company’s earnings report. Executives said the insurer braced for headwinds related to COVID-19 during the year and also saw disappointing growth in new Medicare Advantage members.

Anthem and Cigna fall in the middle of the pack, according to our review. They both reported about $1.1 billion in profit for Q4, though Cigna was ahead with $45.7 billion in revenue.

Anthemearned $6.1 billion in profit on $138.6 billion in revenue for the year, and executives shrugged off concerns about the Medicare Advantage market, saying its performance in open enrollment met expectations. In addition, it’s seeing growth at its in-house pharmacy benefit manager, IngenioRx, as it expands clientele.

Driven by strong investment gains, Oakland, Calif.-based Kaiser Permanente recorded a net income of $8.1 billion in 2021, an increase of $1.7 billion from 2020, according to its financial results released Feb. 11. However, its operating income fell sharply.

For the 12 months ended Dec. 31, the integrated healthcare provider with 39 hospitals recorded an operating revenue of $93.1 billion, up from $88.7 billion recorded last year. Additionally, Kaiser saw its expenses rise 6.9 percent to $92.5 billion in 2021.

In 2021, Kaiser saw its operating income fall to $611 million, an operating margin of 0.7 percent. This compares to a $2.2 billion operating income in 2020 and an operating margin of 2.5 percent.

Kaiser attributed the sharp decrease in operating income to an increase in care delivery expenses due to COVID-19 surges.

Total other income and expenses, which includes investment income, reached $7.5 billion in 2021. In 2020, Kaiser saw a gain of $4.1 billion.

“Our financial performance underscores the strength of our integrated model, which allows us to weather unexpected challenges such as the COVID-19 pandemic while continuing to serve our members,” said Kathy Lancaster, Kaiser Permanente executive vice president and CFO.

In 2021, Kaiser also said its health plan membership grew by 185,000 members. It now has more than 12.5 million members.

The second year of the pandemic did not dampen UnitedHealth Group’s finances, and the company actually surpassed its initial 2021 revenue and profit projections, Bob writes.

The big picture: UnitedHealth’s revenue has tripled from 2010 to 2021, and profit has almost quadrupled. The company continues to make more of its money from owning doctor groups and controlling pharmacy benefits instead of relying on health insurance.

The boom in global mergers and acquisitions in 2021 will surge into 2022, fueled by abundant investment capital, historically low interest rates and a rebound in global economic growth, according to a survey of 345 corporate dealmakers in the U.S. by KPMG.

“Based on the volume of new pitches in November and December — transactions that would come to market in Q1 and Q2 of 2022 — there are no signs of a slowing deal market,” according to Philip Isom, global head of M&A at KPMG. While facing high valuations, “most investors have limited time horizons to invest in, so they may be willing to reach further on price than they have historically.”

More than 80% of the survey respondents across several industries expect total M&A valuations to rise further next year, with about one out of every three predicting at least a 10% increase, KPMG said. Dealmakers said transaction levels will remain robust because companies “need to remain on the offense with the competition” and “feel pressure from investors to raise their own valuations.”

Dive Insight:

Worldwide deal value from January until mid-November this year hit $5.1 trillion, the highest level since 2015 and a 34% gain compared with all of 2020, KPMG said. U.S. transactions rose to $2.9 trillion, or 55% more than during all of last year.

M&A has soared in 2021 as the economy recovered from a pandemic shock, record monetary and fiscal stimulus pumped up liquidity and many companies sought through acquisitions to regain their footing after months of lockdowns and persistent supply chain disruptions.

A widespread labor shortage will probably push up dealmaking next year. One-third of survey respondents said they want to use M&A to acquire talent, KPMG said.

Also, companies increasingly use acquisitions to change their business or operating models, KPMG said, noting that industrial and financial services companies buy companies that help speed their digital transformation.

“The aim is to increase efficiencies and contribute to having more agile workforces,” according to Carole Streicher, KPMG’s deal advisory and strategy service group leader in the U.S.

Private equity firms will continue to push up the volume and value of M&A next year, after increasing their involvement in transaction value by more than 55% so far in 2021, KPMG said. PE firms have pursued deals this year in part because of the prospect of an increase in corporate capital gains taxes.

Growing support for sustainability among investors, regulators and other stakeholders may prompt M&A, “as businesses look at their ecological footprint and consider purchasing, rationalizing or divesting assets,” KPMG said. Investors are likely to consider sustainable businesses more adaptable to market shifts.

Finally, concerns about the potential for rising borrowing costs may prompt dealmakers who rely on debt financing to speed up acquisition plans. Federal Reserve Chair Jerome Powell late last month said policymakers at their two-day meeting beginning Tuesday will likely consider speeding up the withdrawal of accommodation.

Dealmakers face some headwinds. Democrats in the Senate have yet to muster enough support for a roughly $2 trillion social policy bill that would help sustain economic growth. Meanwhile, the outbreak of the omicron variant of COVID-19 has highlighted the fragility of financial markets and the economy to any setbacks in curbing the pandemic.

Survey respondents identified several factors that will influence dealmaking next year, with 61% underscoring high valuations, 56% pointing to liquidity and other economic considerations, and 55% noting intense competition for a limited number of highly valued acquisition targets, KPMG said.

Still, only 7% of the survey respondents said they expect deal volumes to decline in their industries next year.

Survey respondents work at companies in industries ranging from media and financial services to energy and technology, with 194 of them CFOs, CEOs or other C-suite executives.

Attending a recent executive retreat with one of our member health systems, we heard the CEO make a statement that really resonated with us. Referring to the current workforce crisis—pervasive shortages, pressure to increase compensation, outsized reliance on contract labor to fill critical gaps—the CEO made the assertion that this situation isn’t temporary. Rather, it’s the “new normal”, at least for the next several years.

The Great Resignation that’s swept across the American economy in the wake of COVID has not spared healthcare; every system we talk to is facing alarmingly high vacancy rates as nurses, technicians, and other staff head for the exits. The CEO made a compelling case that the labor cost structure of the system has reset at a level between 20 and 30 percent more expensive than before the pandemic, and executives should begin to turn attention away from stop-gap measures (retention bonuses and the like) to more permanent solutions (rethinking care models, adjusting staffing ratios upward, implementing process automation).

That seemed like an important insight to us. It’s increasingly clear as we approach a third year of the pandemic: there is no “post-COVID world” in which things will go back to normal. Rather, we’ll have to learn to live in the “new normal,” revisiting basic assumptions about how, where, and by whom care is delivered.

If hospital labor costs have indeed permanently reset at a higher level, that implies the need for a radical restructuring of the fundamental economic model of the health system—razor-thin margins won’t allow for business to continue as usual. Long overdue, perhaps, and a painful evolution for sure—but one that could bring the industry closer to the vision of “right care, right place, right time” promised by population health advocates for over a decade.

Hospitals saw operating margins continue to erode in October, declining 12% from September under the weight of rising labor costs, according to a national median of more than 900 health systems calculated by Kaufman Hall. It was the second consecutive monthly drop and comes as facilities are preparing for the fast-spreading omicron variant of the coronavirus.

Although expenses remained highly elevated, patient days and average length of stay fell for the first time in months in October, likely reflecting lower hospitalization rates as the pressure of treating large numbers of COVID cases began to ease, Kaufman Hall said in its latest report.

At the same time, operating room minutes rose 6.8% from September, pointing to renewed patient interest in elective procedures.

Dive Insight:

Doctors and nurses have barely caught a breath from the most recent surge in inpatient volumes driven by the delta variant. Now, hospitals face the possibility of a fresh wave of cases led by omicron.

“Performance could continue to suffer in the coming months as hospitals face sustained labor increases and the uncertainties of the emerging omicron variant,” according to the Kaufman Hall report.

The new variant has not been detected in the U.S. as of Wednesday morning, but Canada is amongthe 20 countries that have confirmed cases.

Scientists are scrambling to understand the characteristics of the omicron variant. Anthony Fauci, director of the National Institute of Allergy and Infectious Diseases, told a White House press briefing Tuesday that omicron’s mutation profile points to “increased transmissibility and immune evasion.” But it is too soon to tell whether omicron will cause more severe disease than other COVID-19 variants, or how well current vaccines and treatments work against it, Fauci said.

Moderna CEO Stéphane Bancel told the Financial Times he thought existing vaccines would be less effective against omicron than earlier variants. Moderna, Pfizer, Johnson & Johnson and other manufacturers are already working to adapt their vaccines to combat the new threat, first reported by South African scientists on Nov. 24.

Regeneron also said its COVID-19 antibody drug, the top-selling treatment in the U.S., might be less effective against omicron. The company said it is now conducting tests to determine how the variant affects its drug.

The median hospital operating margin, not including federal Coronavirus Aid, Relief, and Economic Security Act funding, was down 31.5% in October, compared to pre-pandemic levels in the same month of 2019, according to Kaufman Hall’s snapshot. Hospitals in the West, South and Midwest that were hardest hit by the delta variant saw year-over-year margin declines.

Total labor expenses rose nearly 3% from September to October, 12.6% compared to October 2020 and 14.8% compared to October 2019, Kaufman Hall said. Full-time equivalents per adjusted occupied bed decreased 4.5% versus 2020 and 4% versus 2019, suggesting higher salaries due to nationwide labor shortages, rather than increased staffing levels, are driving up labor expenses.

Total non-labor expenses, however, decreased 1% in October from September for supplies, drugs and purchased services, following months of increases.

“Broader economic trends such as U.S. labor shortages are adding to the extreme pressures of the pandemic. Hospitals face greater uncertainties in the coming months as a result, as COVID-19 cases and hospitalizations appear to once again be on the upswing before many have even had a chance to recover from the last surge,” Erik Swanson, a senior vice president of data and analytics at Kaufman Hall said.

Tenet and its subsidiary USPI have entered into a $1.2 billion deal to acquire ambulatory surgery center operator SurgCenter Development, expanding on a previous $1.1 billion cash deal inked with SCD last year.

Under the new deal announced Monday, Tenet will acquire SCD’s ownership interests in 92 ambulatory surgery centers and other support services in 21 states.

In addition to the acquisition, USPI and SCD plan to enter into a five-year partnership and development agreement in which SCD will help facilitate “continuity and support for SCD’s facilities and physician partners.” USPI will also have exclusivity on developing new projects with SCD during the five-year agreement.

Dive Insight:

Despite being a legacy hospital operator, Tenet’s outpatient surgery business is key to its long-term strategy.

After the latest deal closes, USPI will operate 440 surgery centers in 35 states, Tenet said Tuesday. The acquisition will boost USPI’s footprint in existing markets, such as Florida where it already operates 47 centers and will gain an additional 15. USPI will also enter new markets, such as Michigan, with a sizable footprint at the outset, executives said Tuesday.

The deal includes 65 mature centers and 27 that have opened in the past year or will soon open and start performing their first cases. Tenet may also spend an additional $250 million to acquire equity interests from physician owners.

Tenet leaders touted SCD’s service line mix, pointing out that a significant portion of the cases performed by these centers are for musculoskeletal care, which includes total joint and spine procedures.

The deal is expected to generate $175 million in EBITDA during the first year, executives said.

SVB Leerink analysts characterized the deal as savvy and said it will reshape the company’s earnings towards a “faster growing, higher margin, and improved capital return profile.”

Heading into 2021, Tenet had expected a greater share of its earnings power to come from its outpatient surgery business. This deal accelerates that aim over the long-term.

In 2014, Tenet’s ambulatory surgery business accounted for just 5% of the company’s overall earnings. Prior to this latest deal, Tenet expected the unit to account for 42% of its overall earnings in 2021.

This latest announcement follows Tenet’s deal in October with Compass Surgical Partners to acquire its ownership and management interests in nine ambulatory surgery centers located in Florida, North Carolina and Texas for an undisclosed sum.

Hospitals’ performances declined “by almost every metric” during September as volumes dropped, average patient stays rose and expenses increased “dramatically” due to labor and supply chain issues, Kaufman Hall wrote in its latest monthly report.

Although revenue increased compared to this time last year, the industry analyst said that these pressures have led median change in hospital operating margin to decline 18.2% from August to September, not including CARES act funding.

These declines were greatest across regions heavily affected by the recent delta surge, with the west part of the country seeing the largest year-over-year drop in its median change in operating EBITDA margin (38%), Kaufman Hall wrote.

Hospital size also played a role in margin performance, they wrote, with hospitals containing more than 500 beds seeing year-over-year declines of 36% while those with 25 or fewer beds actually seeing their margins increase year over year.

Adjusted discharges dropped 5.1% month over month but remained up 11.4% year over year. Patient days similarly dropped 1.4% month over month, “reflecting a decrease in COVID-19-related hospitalizations,” but are still up 11.4% year over year, according to the report. Notably, the average length of stay saw increases across the board—0.7% month over month and 4.8% year over year.

Expenses and revenues continued their hand-in-hand climb during September.

For the former, total expenses grew 2.2% month over month and 11.2% year over year. Labor expenses increased 1.4% month over month at the same time as workers per patient bed declined, the group wrote. Other non-labor expenses, including drugs and medical supplies, also saw a 1.3% month-over-month increase.

“Multiple factors are contributing to alarming and sustained increases in hospital expenses,” Erik Swanson, a senior vice president of data and analytics with Kaufman Hall. “Growth in labor expenses are outpacing increases in hours worked, suggesting hospitals are paying more due to nationwide labor shortages. Rising supply and drug expenses also point to worldwide supply chain issues.”

Hospital revenues saw their seventh consecutive month of year-to-date increases when compared to 2020 and 2019 alike, “due in part to yearly rate changes and the continued rise in higher acuity cases,” Kaufman Hall wrote. Specifically, gross operating revenues minus CARES grew 12.3% year over year from 2020 and 12.3% year over year from 2019, with inpatient revenue rising faster than outpatient revenue.

Month over month was a different story, however, with gross operating revenue without CARES dropping 1.4%. While inpatient revenue was up 1.5% from August, a 3.3% decline in outpatient revenue “suggests that consumer worries about accessing care during the recent delta surge have led to another downswing,” Kaufman Hall wrote.

Kaufman Hall’s reports incorporate data from more than 900 U.S. hospitals. The September numbers follow early warnings of delta-fueled recovery roadblocks from the group’s preceding monthly reports as well as recent hospital chain earnings calls highlighting high revenues, costs and COVID-19 patient counts.

Operating cash flow margins for nonprofit hospitals fell to a median 7% in 2020.

A shortage of nurses and other workers will continue to erode hospital financial performance into 2022, according to a new Healthcare Quarterly report from Moody’s.

A rise in COVID-19 cases in various regions of the United States has contributed to a wave of nurses, often burned out, resigning to take care of family, to work in less acute healthcare settings such as ambulatory care or to pursue higher-paying contract opportunities, such as becoming a travel nurse.

Hospitals are also having difficulty finding other types of healthcare workers, such as respiratory therapists and imaging technicians, as well as nonclinical workers in areas such as dietary, housekeeping and environmental services.

WHY THIS MATTERS

The report holds no surprises for hospital executives, who already know the financial affect labor shortages are having on revenue. But Moody’s confirms projections that rising costs will make it difficult for hospitals to rebuild margins to pre-COVID-19 levels.

Labor shortages are driving up costs and also may be limiting the number of lucrative elective procedures, resulting in lost revenue. Not-for-profit hospitals saw operating cash flow margins fall to a median 7% in 2020, from 8.3% in the three prior years, according to Moody’s median data.

Hospitals using contract nurses report that hourly wages are very high, in some cases higher now with the Delta variant than during earlier COVID-19 surges. Many hospitals and health systems have also increased minimum wages for nonclinical workers and are finding they must compete with other service sectors, such as the food industry, to attract nonclinical staff.

Given their substantial reliance on government reimbursement from Medicare and Medicaid, most healthcare providers maintain limited pricing flexibility to offset the costs of higher wages. While there are opportunities for more lucrative commercial insurance contracts, rates are the subject of intense negotiations, limiting providers’ pricing power, Moody’s said.

Providers with strong liquidity and diversified cash flow will remain better positioned to manage stress from cost constraints. Hospitals are taking steps to retain nurses, including developing “float pools” of nurses who can work in multiple departments, increasing retention and merit pay, and expanding healthcare benefits such as mental health and child care services.

LifeBridge Health, a not-for-profit health system operating in Baltimore and Carroll County, Maryland, paid its nursing staff retention bonuses in December 2020 as the labor market tightened. To recruit nurses, many systems are offering signing bonuses in exchange for multi-year work commitments as well as scholarship and loan forgiveness programs with local nursing schools.

While these strategies will ease the effect of labor shortages over the long term, they will cause hospitals’ costs to increase in 2022 as salaries and benefits typically represent at least half of a hospital’s expenses. Labor shortages will also likely spark an increase in unionization efforts or lead to more difficult negotiations between unions and providers, potentially increasing costs via new contracts.

THE LARGER TREND

The quarterly report focused on the impact of labor shortages and cost pressures for various sectors, including hospitals, insurers, pharmaceuticals, healthcare services such as staffing firms and health insurers.

Health insurers are less affected by labor shortages, wage pressure and potentially burgeoning inflation than many other healthcare sectors, Moody’s said. Insurers reset premiums each year, which helps them to offset inflation. But if the government does not keep up with payment, providers will look to insurers to make up the shortfall.

Large physician staffing companies, such as Envision Healthcare Corporation and Team Health Holdings, will experience pressure on their profitability as it becomes harder and more expensive to fill open positions as burnout and retirements decrease the number of doctors available to work.

Travel nurse staffing has higher profit margin resilience compared to physician staffing, the report said.

For real estate investment trusts, worker shortages are slowing net operating income growth for REITs to invest in senior housing and skilled nursing facilities.

Growth in salaries and benefits has exceeded hospitals’ expense growth, a trend likely to continue for the remainder of 2021 andinto 2022, Moody’s said in an earlier October report.

In one bright spot in the earlier report, Moody’s noted recent rises in nursing school enrollment indicating a more robust long-term staffing pipeline. However, the aging population, combined with a healthcare workforce that may be retiring from their jobs or quitting due to burnout, represent long-term healthcare staffing challenges nationwide.