Baptist Health said reimbursements for the medications were determined by a payment model that was later invalidated, and the insurer continues to benefit from a “windfall” of underpayments due to the health system, according to the lawsuit.

The suit comes months after the CMS finalized a rule that aimed to fix years of illegal payment cuts in the 340B program. Hospitals had previously argued the solution didn’t consider how MA insurers would benefit financially from the remedy.

Dive Insight:

The 340B program requires pharmaceutical companies to give discounts — which can range from 25% to 50% of the medication’s cost — to providers who serve low-income communities.

The program aims to help safety-net providers better serve vulnerable groups, and it has grown significantly since 340B was created in 1992.

But in 2018, the CMS cut Medicare payments for certain drugs acquired under the 340B program, setting off a legal challenge that hospitals eventually won in front of the Supreme Court four years later.

To fix the underpayments, regulators decided to pay each hospital in 340B a lump sum that would total $9 billion overall. But the fix needed to be budget neutral, so the CMS would cut payments to all hospitals for non-drug items and services over 16 years.

In comments on the proposal, the American Hospital Association argued there was a “significant problem” with the plan, noting many MA insurers pay hospitals according to traditional Medicare rates.

Payers would benefit from reducing the non-drug payments to hospitals, and wouldn’t be required to repay 340B providers for the lower payments between 2018 and 2022, commenters argued on the rule, which was finalized in November.

In response, regulators said they appreciated the concerns, but that they were outside the scope of the rule and “CMS cannot interfere in the payment rates that MAOs [Medicare Advantage organizations] set in contracts with providers and facilities.”

In the Baptist lawsuit, the health system reported it contacted Humana multiple times about retroactive adjustments and remedy payments, but the insurer’s counsel disputed any obligation to make those payments.

“Humana’s refusal to act has worked a substantial windfall to Humana as it continues to hold funds provided by CMS for Humana’s Medicare Advantage plans without reimbursing Baptist Health for the amounts owed to it under the Agreement,” the system said in the lawsuit.

Humana said it does not comment on ongoing litigation.

In Sunday’s Axios’ AM, Mike Allen observed “Republicans know immigration alone could sink Biden. So, Trump and House Republicans will kill anything, even if it meets or exceeds their wishes. Biden knows immigration alone could sink him. So he’s willing to accept what he once considered unacceptable — to save himself.”

Mike called this a “truth Bomb” and he’s probably right: the polarizing issue of immigration is tantamount to a bomb falling on the political system forcing well-entrenched factions to re-think and alter their strategies.

In 2024, in U.S. healthcare, three truth bombs are in-bound. They’re the culmination of shifts in the U.S.’ economic, demographic, social and political environment and fueled by accelerants in social media and Big Data.

Truth bomb: The regulatory protections that have buoyed the industry’s growth are no longer secure.

Despite years of effectively lobbying for protections and money, the industry’s major trade groups face increasingly hostile audiences in city hall, state houses and the U.S. Congress.

The focus of these: the business practices that regulators think protect the status quo at the public’s expense. Example: while the U.S. House spent last week in their districts, Senate Committees held high profile hearings about Medicare Advantage marketing tactics (Finance Committee), consumer protections in assisted living (Special Committee on Aging), drug addiction and the opioid misuse (Banking) and drug pricing (HELP). In states, legislators are rationalizing budgets for Medicaid and public health against education, crime and cybersecurity and lifting scope of practice constraints that limit access.

Drug makers face challenges to patents (“march in rights”) and state-imposed price controls. The FTC and DOJ are challenging hospital consolidation they think potentially harmful to consumer choice and so. Regulators and lawmakers are less receptive to sector-specific wish lists and more supportive of populist-popular rules that advance transparency, disable business relationships that limit consumer choices and cede more control to individuals. Given that the industry is built on a business-to-business (B2B) chassis, preparing for a business to consumer (B2C) time bomb will be uncomfortable for most.

Truth bomb: Affordability in U.S. is not its priority.

The Patient Protection and Affordability Act 2010 advanced the notion that annual healthcare spending growth should not exceed more than 1% of the annual GDP. It also advanced the premise that spending should not exceed 9.5% of household adjusted gross income (AGI) and associated affordability with access to insurance coverage offering subsidies and Medicaid expansion incentives to achieve near-universal coverage. In 2024, that percentage is 8.39%.

Like many elements of the ACA, these constructs fell short: coverage became its focus; affordability secondary.

The ranks of the uninsured shrank to 9% even as annual aggregate spending increased more than 4%/year. But employers and privately insured individuals saw their costs increase at a double-digit pace: in the process, 41% of the U.S. population now have unpaid medical debt: 45% of these have income above $90,000 and 61% have health insurance coverage. As it turns out, having insurance is no panacea for affordability: premiums increase just as hospital, drug and other costs increase and many lower- and middle-income consumers opt for high-deductible plans that expose them to financial insecurity. While lowering spending through value-based purchasing and alternative payments have shown promise, medical inflation in the healthcare supply chain, unrestricted pricing in many sectors, the influx of private equity investing seeking profit maximization for their GPs, and dependence on high-deductible insurance coverage have negated affordability gains for consumers and increasingly employers. Benign neglect for affordability is seemingly hardwired in the system psyche, more aligned with soundbites than substance.

Truth bomb: The effectiveness of the system is overblown.

Numerous peer reviewed studies have quantified clinical and administrative flaws in the system. For instance, a recent peer reviewed analysis in the British Medical Journal concluded “An estimated 795 000 Americans become permanently disabled or die annually across care settings because dangerous diseases are misdiagnosed. Just 15 diseases account for about 50.7% of all serious harms, so the problem may be more tractable than previously imagined.”

The inadequacy of personnel and funding in primary and preventive health services is well-documented as the administrative burden of the system—almost 20% of its spending. Satisfaction is low. Outcomes are impressive for hard-to-diagnose and treat conditions but modest at best for routine care. It’s easier to talk about value than define and measure it in our system: that allows everyone to declare their value propositions without challenge.

Truth bombs are falling in U.S. healthcare. They’re well-documented and financed. They take no prisoners and exact mass casualties.

Most healthcare organizations default to comfortable defenses. That’s not enough. Cyberwarfare, precision-guided drones and dirty bombs require a modernized defense. Lacking that, the system will be a commoditized public utility for most in 15 years.

PS: Last week’s report, “The Holy War between Hospitals and Insurers…” (The Keckley Report – Paul Keckley) prompted understandable frustration from hospitals that believe insurers do not serve the public good at a level commensurate with the advantages they enjoy in the industry. However, justified, pushback by hospitals against insurers should be framed in the longer-term context of the role and scope of services each should play in the system long-term. There are good people in both sectors attempting to serve the public good. It’s not about bad people; it’s about a flawed system.

Recently published in Stat, this article outlines how the launch of telehealth platforms by pharmaceutical companies, most notably Eli Lilly’s LillyDirect, portends a gamechanger for DTC prescription marketing.

Spurred by the escalating demand for Eli Lilly’s Zepbound and Mounjaro GLP-1 drugs, LillyDirect connects consumers with a third-party telehealth provider for prescriptions, an online pharmacy for fulfillment, and in-house payment support through streamlined coupon applications and prior authorization troubleshooting. In exchange, Eli Lilly gets access to reams of patient data, in addition to boosted sales. Pharma companies insist that the platforms have proper firewalls in place, as no money directly changes hands between them and their affiliated telehealth providers.

The Gist:With so manyothercompanies hopping on the GLP-1 virtual prescription bandwagon, it’s no wonder why pharma companies are opting to enter the market directly. What LillyDirect offers is not fundamentally different than platforms like Ro or Teladoc: using telehealth to blur the lines between prescription and over-the-counter medications by empowering consumers to seek out the care they want.

However, Eli Lilly’s control of the drug supply, ability to offer coupons, relationships with pharmacy benefit managers, and inherent brand association with the drugs give it a leg up on the competition.

By replacing “talk to your doctor about” with “visit our website for”, these consumer-focused platforms perpetuate the ongoing fragmentation of care and risk tapping into the potentially harmful side of consumerization in healthcare.

Three critical healthcare struggles will define the year to come with cutthroat competition and intense disputes being played out in public:

1. A Nation Divided Over Abortion Rights

2. The Generative AI Revolution In Medicine

3. The Tug-Of-War Over Healthcare Pricing American healthcare, much like any battlefield, is fraught with conflict and turmoil. As we navigate 2024, the wars ahead seem destined to intensify before any semblance of peace can be attained. Let me know your thoughts once you read mine.

Modern medicine, for most of its history, has operated within a collegial environment—an industry of civility where physicians, hospitals, pharmaceutical companies and others stayed in their lanes and out of each other’s business.

It used to be that clinicians made patient-centric decisions, drugmakers and hospitals calculated care/treatment costs and added a modest profit, while insurers set rates based on those figures. Businesses and the government, hoping to save a little money, negotiated coverage rates but not at the expense of a favored doctor or hospital. Disputes, if any, were resolved quietly and behind the scenes.

Times have changed as healthcare has taken a 180-degree turn. This year will be characterized by cutthroat competition and intense disputes played out in public. And as the once harmonious world of healthcare braces for battle, three critical struggles take centerstage. Each one promises controversy and profound implications for the future of medicine:

1. A Nation Divided Over Abortion Rights

For nearly 50 years, from the landmark Roe v. Wade decision in 1973 to its overruling by the 2022 Dobbs case, abortion decisions were the province of women and their doctors. This dynamic has changed in nearly half the states.

This spring, the Supreme Court is set to hear another pivotal case, this one on mifepristone, an important drug for medical abortions. The ruling, expected in June, will significantly impact women’s rights and federal regulatory bodies like the FDA.

Traditionally, abortions were surgical procedures. Today, over half of all terminations aremedically induced, primarily using a two-drug combination, including mifepristone. Since its approval in 2000, mifepristone has been prescribed to over 5 million women, and it boasts an excellent safety record. But anti-abortion groups, now challenging this method, have proposed stringent legal restrictions: reducing the administration window from 10 to seven weeks post-conception, banning distribution of the drug by mail, and mandating three in-person doctor visits, a burdensome requirement for many. While physicians could still prescribe misoprostol, the second drug in the regimen, its effectiveness alone pales in comparison to the two-drug combo.

Should the Supreme Court overrule and overturn the FDA’s clinical expertise on these matters, abortion activists fear the floodgates will open, inviting new challenges against other established medications like birth control.

In response, several states have fortified abortion rights through ballot initiatives, a trend expected to gain momentum in the November elections. This legislative action underscores a significant public-opinion divide from the Supreme Court’s stance. In fact, a survey published in Nature Human Behavior reveals that 60% of Americans support legal abortion.

Path to resolution: Uncertain. Traditionally, SCOTUS rulings have mirrored public opinion on key social issues, but its deviation on abortion rights has failed to shift public sentiment, setting the stage for an even fiercer clash in years to come. A Supreme Court ruling that renders abortion unconstitutional would contradict the principles outlined in the Dobbs decision, but not all states will enact protective measures. As a result, America’s divide on abortion rights is poised to deepen.

2. The Generative AI Revolution In Medicine

A year after ChatGPT’s release, an arms race in generative AI is reshaping industries from finance to healthcare. Organizations are investing billions to get a technological leg up on the competition, but this budding revolution has sparked widespread concern.

In Hollywood, screenwriters recently emerged victorious from a 150-day strike, partially focused on the threat of AI as a replacement for human workers. In the media realm, prominent organizations like The New York Times, along with a bevy of celebs and influencers, have initiated copyright infringement lawsuits against OpenAI, the developer of ChatGPT.

The healthcare sector faces its own unique battles. Insurers are leveraging AI to speed up and intensify claim denials, prompting providers to counter with AI-assisted appeals.

But beyond corporate skirmishes, the most profound conflict involves the doctor-patient relationship. Physicians, already vexed by patients who self-diagnose with “Dr. Google,” find themselves unsure whether generative AI will be friend or foe. Unlike traditional search engines, GenAI doesn’t just spit out information. It provides nuanced medical insights based on extensive, up-to-date research. Studies suggest that AI can already diagnose and recommend treatments with remarkable accuracy and empathy, surpassing human doctors in ever-more ways.

Path to resolution: Unfolding. While doctors are already taking advantage of AI’s administrative benefits (billing, notetaking and data entry), they’re apprehensive that ChatGPT will lead to errors if used for patient care. In this case, time will heal most concerns and eliminate most fears. Five years from now, with ChatGPT predicted to be 30 times more powerful, generative AI systems will become integral to medical care. Advanced tools, interfacing with wearables and electronic health records, will aid in disease management, diagnosis and chronic-condition monitoring, enhancing clinical outcomes and overall health.

3. The Tug-Of-War Over Healthcare Pricing

From routine doctor visits to complex hospital stays and drug prescriptions, every aspect of U.S. healthcare is getting more expensive. That’s not news to most Americans, half of whom say it is very or somewhat difficult to afford healthcare costs.

But people may be surprised to learn how the pricing wars will play out this year—and how the winners will affect the overall cost of healthcare.

Throughout U.S. healthcare, nurses are striking as doctors are unionizing. After a year of soaring inflation, healthcare supply-chain costs and wage expectations are through the roof. A notable example emerged in California, where a proposed $25 hourly minimum wage for healthcare workers was later retracted by Governor Newsom amid budget constraints.

Financial pressures are increasing. In response, thousands of doctors have sold their medical practices to private equity firms. This trend will continue in 2024 and likely drive up prices, as much as 30% higher for many specialties.

Meanwhile, drug spending will soar in 2024 as weight-loss drugs (costing roughly $12,000 a year) become increasingly available. A groundbreaking sickle cell disease treatment, which uses the controversial CRISPR technology, is projected to cost nearly $3 million upon release.

To help tame runaway prices, the Centers for Medicare & Medicaid Services will reduce out-of-pocket costs for dozens of Part B medications “by $1 to as much as $2,786 per average dose,” according to White House officials. However, the move, one of many price-busting measures under the Inflation Reduction Act, has ignited a series of legal challenges from the pharmaceutical industry.

Big Pharma seeks to delay or overturn legislation that would allow CMS to negotiate prices for 10 of the most expensive outpatient drugs starting in 2026.

Path to resolution: Up to voters. With national healthcare spending expected to leap from $4 trillion to $7 trillion by 2031, the pricing debate will only intensify. The upcoming election will be pivotal in steering the financial strategy for healthcare. A Republican surge could mean tighter controls on Medicare and Medicaid and relaxed insurance regulations, whereas a Democratic sweep could lead to increased taxes, especially on the wealthy. A divided government, however, would stall significant reforms, exacerbating the crisis of unaffordability into 2025.

Is Peace Possible?

American healthcare, much like any battlefield, is fraught with conflict and turmoil. As we navigate 2024, the wars ahead seem destined to intensify before any semblance of peace can be attained.

Yet, amidst the strife, hope glimmers: The rise of ChatGPT and other generative AI technologies holds promise for revolutionizing patient empowerment and systemic efficiency, making healthcare more accessible while mitigating the burden of chronic diseases. The debate over abortion rights, while deeply polarizing, might eventually find resolution in a legislative middle ground that echoes Roe’s protections with some restrictions on how late in pregnancy procedures can be performed.

Unfortunately, some problems need to get worse before they can get better. I predict the affordability of healthcare will be one of them this year. My New Year’s request is not to shoot the messenger.

A new perspective on how technology, transformation efforts, and other changes have affected payers, health systems, healthcare services and technology, and pharmacy services.

The acute strain from labor shortages, inflation, and endemic COVID-19 on the healthcare industry’s financial health in 2022 is easing. Much of the improvement is the result of transformation efforts undertaken over the last year or two by healthcare delivery players, with healthcare payers acting more recently. Even so, health-system margins are lagging behind their financial performance relative to prepandemic levels. Skilled nursing and long-term-care profit pools continue to weaken. Eligibility redeterminations in a strong employment economy have hurt payers’ financial performance in the Medicaid segment. But Medicare Advantage and individual segment economics have held up well for payers.

As we look to 2027, the growth of the managed care duals population (individuals who qualify for both Medicaid and Medicare) presents one of the most substantial opportunities for payers. On the healthcare delivery side, financial performance will continue to rebound as transformation efforts, M&A, and revenue diversification bear fruit. Powered by adoption of technology, healthcare services and technology (HST) businesses, particularly those that offer measurable near-term improvements for their customers, will continue to grow, as will pharmacy services players, especially those with a focus on specialty pharmacy.

Below, we provide a perspective on how these changes have affected payers, health systems, healthcare services and technology, and pharmacy services, and what to expect in 2024 and beyond.

The fastest growth in healthcare may occur in several segments

We estimate that healthcare profit pools will grow at a 7 percent CAGR, from $583 billion in 2022 to $819 billion in 2027. Profit pools continued under pressure in 2023 due to high inflation rates and labor shortages; however, we expect a recovery beginning in 2024, spurred by margin and cost optimization and reimbursement-rate increases.

Several segments can expect higher growth in profit pools:

Within payer, Medicare Advantage, spurred by the rapid increase in the duals population; the group business, due to recovery of margins post-COVID-19 pandemic; and individual

Within health systems, outpatient care settings such as physician offices and ambulatory surgery centers, driven by site-of-care shifts

Within HST, the software and platforms businesses (for example, patient engagement and clinical decision support)

Within pharmacy services, with specialty pharmacy continuing to experience rapid growth

On the other hand, some segments will continue to see slow growth, including general acute care and post-acute care within health systems, and Medicaid within payers (Exhibit 1).

Several factors will likely influence shifts in profit pools. Two of these are:

Change in payer mix. Enrollment in Medicare Advantage, and particularly the duals population, will continue to grow. Medicare Advantage enrollment has grown historically by 9 percent annually from 2019 to 2022; however, we estimate the growth rate will reduce to 5 percent annually from 2022 to 2027, in line with the latest Centers for Medicare & Medicaid Services (CMS) enrollment data.1 Finally, the duals population enrolled in managed care is estimated to grow at more than a 9 percent CAGR from 2022 through 2027.

We also estimate commercial segment profit pools to rebound as EBITDA margins likely return to historical averages by 2027. Growth is likely to be partially offset by enrollment changes in the segment, prompted by a shift from fully insured to self-insured businesses that could accelerate as employers seek to cut costs if the economy slows. Individual segment profit pools are estimated to expand at a 27 percent CAGR from 2022 to 2027 as enrollment rises, propelled by enhanced subsidies, Medicaid redeterminations, and other potential favorable factors (for example, employer conversions through the Individual Coverage Health Reimbursement Arrangement offered by the Affordable Care Act); EBITDA margins are estimated to improve from 2 percent in 2022 to 5 to 7 percent in 2027. On the other hand, Medicaid enrollment could decline by about ten million lives over the next five years based on our estimates, given recent legislation allowing states to begin eligibility redeterminations (which were paused during the federal public health emergency declared at the start of the COVID-19 pandemic2).

Accelerating value-based care (VBC). Based on our estimates, 90 million lives will be in VBC models by 2027, from 43 million in 2022. This expansion will be fueled by an increase in commercial VBC adoption, greater penetration of Medicare Advantage, and the Medicare Shared Savings Program (MSSP) model in Medicare fee-for-service. Also, substantial growth is expected in the specialty VBC model, where penetration in areas like orthopedics and nephrology could more than double in the next five years.

VBC models are undergoing changes as CMS updates its risk adjustment methodology and as models continue to expand beyond primary care to other specialties (for example, nephrology, oncology, and orthopedics). We expect established models that offer improvements in cost and quality to continue to thrive. The transformation of VBC business models in response to pressures from the current changes could likely deliver outsized improvement in cost and quality outcomes. The penetration of VBC business models is likely to lead to shifts in health delivery profit pools, from acute-care settings to other sites of care such as ambulatory surgical centers, physician offices, and home settings.

Payers: Government segments are expected to be 65 percent larger than commercial segments by 2027

In 2022, overall payer profit pools were $60 billion. Looking ahead, we estimate EBITDA to grow to $78 billion by 2027, a 5 percent CAGR, as the market recovers and approaches historical trends. Drivers are likely to be margin recovery of the commercial segment, inflation-driven incremental premium rate rises, and increased participation in managed care by the duals population. This is likely to be partially offset by margin compression in Medicare Advantage due to regulatory pressures (for example, risk adjustment, decline in the Stars bonus, and technical updates) and membership decline in Medicaid resulting from the expiration of the public health emergency.

We estimate increased labor costs and administrative expenses to reduce payer EBITDA by about 60 basis points in 2023. In addition, health systems are likely to push for reimbursement rate increases (up to about 350 to 400 basis-point incremental rate increases from 2023 to 2027 for the commercial segment and about 200 to 250 basis points for the government segment), according to McKinsey analysis and interviews with external experts.3

Our estimates also suggest that the mix of payer profit pools is likely to shift further toward the government segment (Exhibit 2). Overall, the profit pools for this segment are estimated to be about 65 percent greater than the commercial segment by 2027 ($36 billion compared with $21 billion). This shift would be a result of increasing Medicare Advantage penetration, estimated to reach 52 percent in 2027, and likely continued growth in the duals segment, expanding EBITDA from $7 billion in 2022 to $12 billion in 2027.

Profit pools for the commercial segment declined from $18 billion in 2019 to $15 billion in 2022. We now estimate the commercial segment’s EBITDA margins to regain historical levels by 2027, and profit pools to reach $21 billion, growing at a 7 percent CAGR from 2022 to 2027. Within this segment, a shift from fully insured to self-insured businesses could accelerate in the event of an economic slowdown, which prompts employers to pay greater attention to costs. The fully insured group enrollment could drop from 50 million in 2022 to 46 million in 2027, while the self-insured segment could increase from 108 million to 113 million during the same period.

Health systems: Transformation efforts help accelerate EBITDA recovery

In 2023, health-system profit pools continued to face substantial pressure due to inflation and labor shortages. Estimated growth was less than 5 percent from 2022 to 2023, remaining below prepandemic levels. Health systems have undertaken major transformation and cost containment efforts, particularly within the labor force, helping EBITDA margins recover by up to 100 basis points; some of this recovery was also volume-driven.

Looking ahead, we estimate an 11 percent CAGR from 2023 to 2027, or total EBITDA of $366 billion by 2027 (Exhibit 3). This reflects a rebound from below the long-term historical average in 2023, spurred by transformation efforts and potentially higher reimbursement rates. We anticipate that health systems will likely seek reimbursement increases in the high single digits or higher upon contract renewals (or more than 300 basis points above previous levels) in response to cost inflation in recent years.

Measures to tackle rising costs include improving labor productivity and the application of technological innovation across both administration and care delivery workflows (for example, further process standardization and outsourcing, increased use of digital care, and early adoption of AI within administrative workflows such as revenue cycle management). Despite these measures, 2027 industry EBITDA margins are estimated to be 50 to 100 basis points lower than in 2019, unless there is material acceleration in performance transformation efforts.

There are some meaningful exceptions to this overall outlook for health systems. Although post-acute-care profit pools could be severely affected by labor shortages (particularly nurses), other sites of care might grow (for example, non-acute and outpatient sites such as physician offices and ambulatory surgery centers). We expect accelerated adoption of VBC to drive growth.

HST profit pools will grow in technology-based segments

HST is estimated to be the fastest-growing sector in healthcare. In 2021, we estimated HST profit pools to be $51 billion. In 2022, according to our estimates, the HST profit pool shrank to $49 billion, reflecting a contracting market, wage inflation pressure, and the drag of fixed-technology investment that had not yet fulfilled its potential. Looking ahead, we estimate a 12 percent CAGR in 2022–27 due to the long-term underlying growth trend and rebound from the pandemic-related decline (Exhibit 4). With the continuing technology adoption in healthcare, the greatest acceleration is likely to happen in software and platforms as well as data and analytics, with 15 percent and 22 percent CAGRs, respectively.

In 2023, we observed an initial recovery in the HST market, supported by lower HST wage pressure and continued adoption of technology by payers and health systems searching for ways to become more efficient (for example, through automation and outsourcing).

Three factors account for the anticipated recovery and growth in HST.First, we expect continued demand from payers and health systems searching to improve efficiency, address labor challenges, and implement new technologies (for example, generative AI). Second, payers and health systems are likely to accept vendor price increases for solutions delivering measurable improvements. Third, we expect HST companies to make operational changes that will improve HST efficiency through better technology deployment and automation across services.

Pharmacy services will continue to grow

The pharmacy market has undergone major changes in recent years, including the impact of the COVID-19 pandemic, the establishment of partnerships across the value chain, and an evolving regulatory environment. Total pharmacy dispensing revenue continues to increase, growing by 9 percent to $550 billion in 2022,4 with projections of a 5 percent CAGR, reaching $700 billion in 2027.5Specialty pharmacy is one of the fastest growing subsegments within pharmacy services and accounts for 40 percent of prescription revenue6; this subsegment is expected to reach nearly 50 percent of prescription revenue in 2027 (Exhibit 5). We attribute its 8 percent CAGR in revenue growth to increases in utilization and pricing as well as the continued expansion of pipeline therapies (for example, cell and gene therapies and oncology and rare disease therapies) and expect that the revenue growth will be partially offset by reimbursement pressures, specialty generics, and increased adoption of biosimilars. Specialty pharmacy dispensers are also facing an evolving landscape with increased manufacturer contract pharmacy pressures related to the 340B Drug Pricing Program. With restrictions related to size and location of contract pharmacies that covered entities can use, the specialty pharmacy subsegment has seen accelerated investment in hospital-owned pharmacies.

Retail and mail pharmacies continue to face margin pressure and a contraction of profit pools due to reimbursement pressure, labor shortages, inflation, and a plateauing of generic dispensing rates.7Many chains have recently announced8 efforts to rationalize store footprints while continuing to augment additional services, including the provision of healthcare services.

Over the past year, there has also been increased attention to broad-population drugs such as GLP-1s (indicated for diabetes and obesity). The number of patients meeting clinical eligibility criteria for these drugs is among the largest of any new drug class in the past 20 to 30 years. The increased focus on these drugs has amplified conversations about care and coverage decisions, including considerations around demonstrated adherence to therapy, utilization management measures, and prescriber access points (for example, digital and telehealth services). As we look ahead, patient affordability, cost containment, and predictability of spending will likely remain key themes in the sector.The Inflation Reduction Act is poised to change the Medicare prescription Part D benefit, with a focus on reducing beneficiary out-of-pocket spending, negotiating prices for select drugs, and incentivizing better management of high-cost drugs. These changes, coupled with increased attention to broad-population drugs and the potential of high-cost therapies (such as cell and gene therapies), have set the stage for a shift in care and financing models.

The US healthcare industry faced demanding conditions in 2023, including continuing high inflation rates, labor shortages, and endemic COVID-19. However, the industry has adapted. We expect accelerated improvement efforts to help the industry address its challenges in 2024 and beyond, leading to an eventual return to historical-average profit margins.

Healthcare is big business. That’s why JP Morgan Chase is hosting its 42nd Healthcare Conference in San Francisco starting today– the same week Congress reconvenes in DC with the business of healthcare on its agenda as well. The predispositions of the two toward the health industry could not be more different.

Context: the U.S. Health System in the Global Economy

Though the U.S. population is only 4% of the world total, our spending for healthcare products and services represents 45% of global healthcare market. Healthcare is 17.4% of U.S. GDP vs. an average of 9.6% for the economies in the 37 other high-income economies of the world. It is the U.S.’ biggest private employer (17.2 million) accounting for 24% of total U.S. job growth last year (BLS). And it’s a growth industry: annual health spending growth is forecast to exceed 4%/year for the foreseeable future and almost 5% globally—well above inflation and GDP growth. That’s why private investments in healthcare have averaged at least 15% of total private investing for 20+ years. That’s why the industry’s stability is central to the economy of the world.

The developed health systems of the world have much in common: each has three major sets of players:

Service Providers: organizations/entities that provide hands-on services to individuals in need (hospitals, physicians, long-term care facilities, public health programs/facilities, alternative health providers, clinics, et al). In developed systems of the world, 50-60% of spending is in these sectors.

Innovators: organizations/entities that develop products and services used by service providers to prevent/treat health problems: drug and device manufacturers, HIT, retail health, self-diagnostics, OTC products et al. In developed systems of the world, 20-30% is spend in these.

Administrators, Watchdogs & Regulators: Organizations that influence and establish regulations, oversee funding and adjudicate relationships between service providers and innovators that operate in their systems: elected officials including Congress, regulators, government agencies, trade groups, think tanks et al. In the developed systems of the world, administration, which includes insurance, involves 5-10% of its spending (though it is close to 20% in the U.S. system due to the fragmentation of our insurance programs).

In the developed systems of the world, including the U.S., the role individual consumers play is secondary to the roles health professionals play in diagnosing and treating health problems. Governments (provincial/federal) play bigger roles in budgeting and funding their systems and consumer out-of-pocket spending as a percentage of total health spending is higher than the U.S. All developed and developing health systems of the world include similar sectors and all vary in how their governments regulate interactions between them. All fund their systems through a combination of taxes and out-of-pocket payments by consumers. All depend on private capital to fund innovators and some service providers. And all are heavily regulated.

In essence, that makes the U.S. system unique are (1) the higher unit costs and prices for prescription drugs and specialty services, (2) higher administrative overhead costs, (3) higher prevalence of social health issues involving substance abuse, mental health, gun violence, obesity, et al (4) the lack of integration of our social services/public health and health delivery in communities and (5) lack of a central planning process linked to caps on spending, standardization of care based on evidence et al.

So, despite difference in structure and spending, developed systems of the world, like the U.S. look similar:

The Current Climate for the U.S. Health Industry

The global market for healthcare is attractive to investors and innovators; it is less attractive to most service providers since their business models are less scalable. Both innovator and service provider sectors require capital to expand and grow but their sources vary: innovators are primarily funded by private investors vs. service providers who depend more on public funding. Both are impacted by the monetary policies, laws and political realities in the markets where they operate and both are pivoting to post-pandemic new normalcy. But the outlook of investors in the current climate is dramatically different than the predisposition of the U.S. Congress toward healthcare:

Healthcare innovators and their investors are cautiously optimistic about the future. The dramatic turnaround in the biotech market in 4Q last year coupled with investor enthusiasm for generative AI and weight loss drugs and lower interest rates for debt buoy optimism about prospects at home and abroad. The FDA approved 57 new drugs last year—the most since 2018. Big tech is partnering with established payers and providers to democratize science, enable self-care and increase therapeutic efficacy. That’s why innovators garner the lion’s share of attention at JPM. Their strategies are longer-term focused: affordability, generative AI, cost-reduction, alternative channels, self-care et al are central themes and the welcoming roles of disruptors hardwired in investment bets. That’s the JPM climate in San Franciso.

By contrast, service providers, especially the hospital and long-term care sectors, are worried. In DC, Congress is focused on low-hanging fruit where bipartisan support is strongest and political risks lowest i.e.: price transparency, funding cuts, waste reduction, consumer protections, heightened scrutiny of fraud and (thru the FTC and DOJ) constraints on horizontal consolidation to protect competition. And Congress’ efforts to rein in private equity investments to protect consumer choice wins votes and worries investors. Thus, strategies in most service provider sectors are defensive and transactional; longer-term bets are dependent on partnerships with private equity and corporate partners. That’s the crowd trying to change Congress’ mind about cuts and constraints.

The big question facing JPM attendees this week and in Congress over the next few months is the same: is the U.S. healthcare system status quo sustainable given the needs in other areas at home and abroad?

Investors and organizations at JPM think the answer is no and are making bets with their money on “better, faster, cheaper” at home and abroad. Congress agrees, but the political risks associated with transformative changes at home are too many and too complex for their majority.

For healthcare investors and operators, the distance between San Fran and DC is further and more treacherous than the 2808 miles on the map.

The JPM crowd sees a global healthcare future that welcomes change and needs capital; Congress sees a domestic money pit that’s too dicey to handle head-on–two views that are wildly divergent.

Last week, the Food and Drug Administration (FDA) announced the approval of Eli Lilly’s drug tirzepatide for treating obesity. The drug, which will be sold under the name Zepbound for obesity, is already branded as Mounjaro for diabetes treatment.

While Novo Nordisk’s blockbuster semaglutide drug (sold as Wegovy for obesity and Ozempic for diabetes) works only as a GLP-1 agonist, tirzepatide also targets a second receptor and has been shown to elicit greater weight loss.

Spurred by trial results demonstrating significant health benefits beyond weight loss tied to these drugs, the American Medical Association House of Delegates voted this week to adopt a policy advocating for insurance coverage of GLP-1-based obesity treatments, affirming that it regards obesity as a disease, and that patients left untreated for the condition are at greater risk for serious health consequences.

To date, most insurers and self-funded employers have resisted covering weight loss drugs due to their prices: Zepbound has a list price of $1,060 per month, while Wegovy is priced at around $1,300 per month.

The Gist:We have entered a new era in treating obesity.

Even with payers and employers dragging their feet over coverage decisions, and Medicare remaining prohibited from covering weight-loss drugs by law, consumer demand for the drugs has been strong enough to outpace supply. Zepbound’s approval will hopefully both improve availability and exert downward pricing pressure.

While these drugs will undoubtedly contribute to higher healthcare spending in the short term, the long-term benefits of significant weight loss, combined with cardiovascular risk reduction, could lower healthcare costs over the patient’s lifespan—although the payer “holding the bag” for the cost today may not see the return, given that as many as 20 percent of individuals with commercial insurance switch carriers every year.

This week, Express Scripts, the nation’s second-largest pharmacy benefit manager (PBM), which is owned by health insurer Cigna, announced a new pricing model.

It is giving employers and health plans the option to pay pharmacies up to 15 percent over acquisition costs, plus a dispensing fee, for covered drugs. This payment structure was popularized by the Mark Cuban Cost Plus Drugs Company, founded by the billionaire businessman in reaction to the opaque pricing and complicated discounts and rebates common among PBMs.

While Cigna is not promising that this new pricing model will result in lower prices, it says it will improve transparency and should benefit retail pharmacies, who will split the markup with Express Scripts.

Cigna projects that only some employers will lower their healthcare spending through the cost-plus model, and that patient cost-sharing should be similar under both approaches.

The Gist:Between disruptive competitors like Cuban’s venture and increasing scrutiny from Congress, PBMs are facing new pressures to improve transparency and account for their role in rising drug costs.

This move by Cigna is an attempt to address at least one of those concerns, possibly intended to preempt regulatory and legislative action.

After years of complaints surrounding their business practices, it appears that the Congressional tide may be turning toward PBM industry reform. However,patients—who by and large are unaware of what PBMs are or do—won’t be satisfied till they see their out-of-pocket prescription drug costs go down.

Next up on this front: seeing which provisions targeting PBMs, many which have bipartisan support, make it into the Senate’s broad healthcare legislation planned for the end of this year, and in what form that bill ultimately passes.

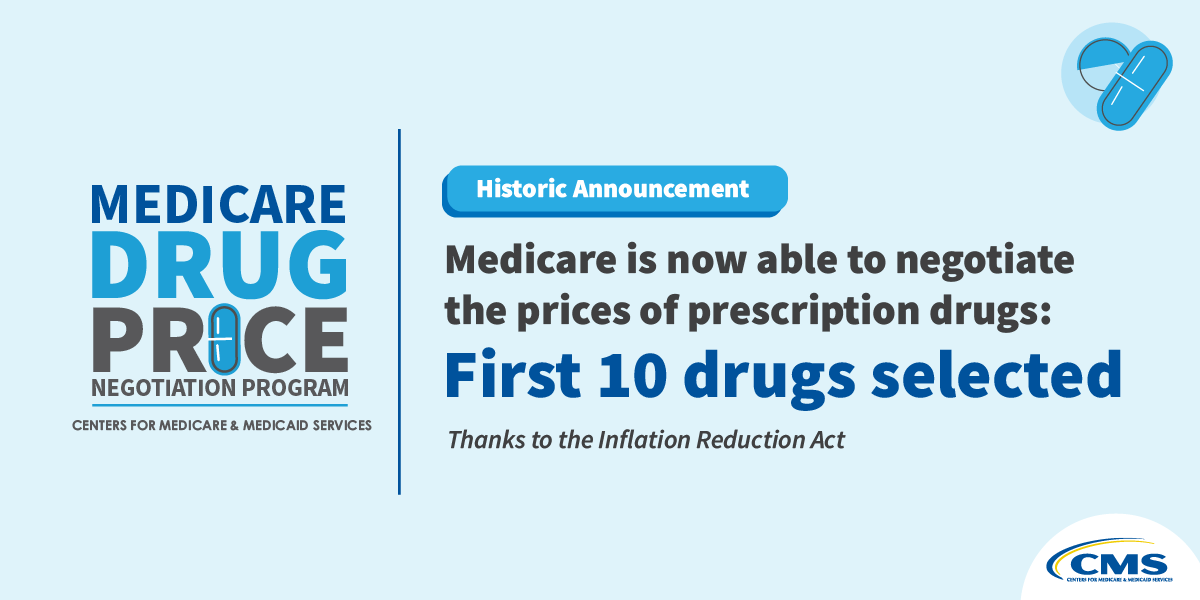

Last week, the Centers for Medicare and Medicaid Services (CMS) released the list of the first round of prescription drugs chosen for Medicare Part D price negotiations. The 2022 Inflation Reduction Act (IRA) granted CMS the authority to negotiate directly with pharmaceutical manufacturers, establishing a process that will ramp up to include 20 drugs per year and cover Part B medicines by 2029.

The majority of the initial 10 medications, including Eliquis, Jardiance, and Xarelto, are highly utilized across Medicare beneficiaries, treating mainly diabetes and cardiovascular disease. But three of the drugs (Enbrel, Imbruvica, and Stelara) are very high-cost drugs used by fewer than 50k beneficiaries to treat some cancers and autoimmune diseases.

Together the 10 drugs cost Medicare about $50B annually, comprising 20 percent of Part D spending. Drug manufacturers must now engage with CMS in a complex negotiation process, with negotiated prices scheduled to go into effect in 2026.

The Gist:

Most of the drugs on this list are not a surprise, with the Biden administration prioritizing more common chronic disease medications, with large total spend for the program, over the most expensive drugs, many of which are exempted by the IRA’s minimum seven-year grace period for new pharmaceuticals.

However, pharmaceutical companies are threatening to derail the process before it even begins. Several companies with drugs on the list have already filed lawsuits against the government on the grounds that the entire negotiation program is unconstitutional.

While President Biden is already touting lowering drug prices as a key plank of his reelection pitch, it will take years before these negotiations translate into lower costs for beneficiaries and reduced government spending. There also may be adverse unintended consequences, as drug companies may raise prices for commercial payers while increasing rebates to stabilize net prices, leading to higher costs for some consumers.

Still, it’s a step in the right direction for the US, given that we pay 2.4 times more than peer countries for prescription medications.

Last Tuesday, the Center for Medicare and Medicaid Services (CMS) announced the first 10 medicines that will be subject to price negotiations with Medicare starting in 2026 per authorization in the Inflation Reduction Act (2022). It’s a big deal but far from a done deal.

Here are the 10:

Eliquis, for preventing strokes and blood clots, from Bristol Myers Squibb and Pfizer

Jardiance, for Type 2 diabetes and heart failure, from Boehringer Ingelheim and Eli Lilly

Xarelto, for preventing strokes and blood clots, from Johnson & Johnson

Januvia, for Type 2 diabetes, from Merck

Farxiga, for chronic kidney disease, from AstraZeneca

Entresto, for heart failure, from Novartis

Enbrel, for arthritis and other autoimmune conditions, from Amgen

Imbruvica, for blood cancers, from AbbVie and Johnson & Johnson

Stelara, for Crohn’s disease, from Johnson & Johnson

Fiasp and NovoLog insulin products, for diabetes, from Novo Nordisk

Notably, they include products from 10 of the biggest drug manufacturers that operate in the U.S. including 4 headquartered here (Johnson and Johnson, Merck, Lilly, Amgen) and the list covers a wide range of medical conditions that benefit from daily medications.

But only one cancer medicine was included (Johnson & Johnson and AbbVie’s Imbruvica for lymphoma) leaving cancer drugs alongside therapeutics for weight loss, Crohn’s and others to prepare for listing in 2027 or later.

And CMS included long-acting insulins in the inaugural list naming six products manufactured by the Danish pharmaceutical giant Novo Nordisk while leaving the competing products made by J&J and others off. So, there were surprises.

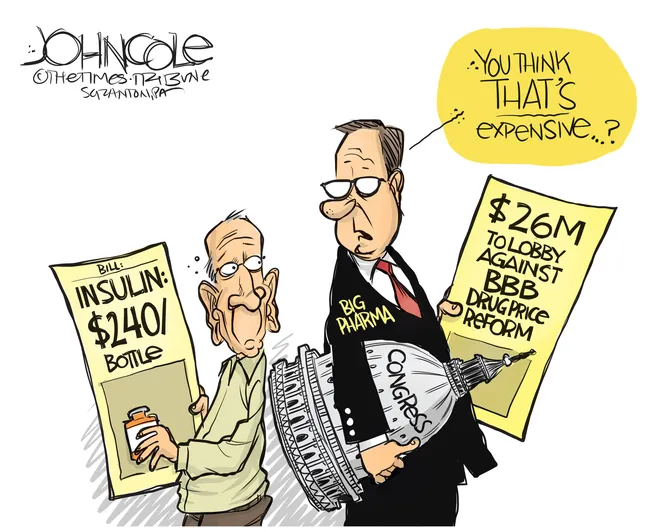

To date, 8 lawsuits have been filed against the U.S. Department of Health and Human Services by drug manufacturers and the likelihood litigation will end up in the Supreme Court is high.

These cases are being brought because drug manufacturers believe government-imposed price controls are illegal. The arguments will be closely watched because they hit at a more fundamental question:

what’s the role of the federal government in making healthcare in the U.S. more affordable to more people?

Every major sector in healthcare– hospitals, health insurers, medical device manufacturers, physician organizations, information technology companies, consultancies, advisors et al may be impacted as the $4.6 trillion industry is scrutinized more closely . All depend on its regulatory complexity to keep prices high, outsiders out and growth predictable. The pharmaceutical industry just happens to be its most visible.

The Pharmaceutical Industry

The facts are these:

66% of American’s take one or more prescriptions: There were 4.73 billion prescriptions dispensed in the U.S. in 2022

Americans spent $633.5 billion on their medicines in 2022 and will spend $605-$635 billion in 2025.

This year (2023), the U.S. pharmaceutical market will account for 43.7% of the global pharmaceutical market and more than 70% of the industry’s profits.

41% of Americans say they have a fair amount or a great deal of trust in pharmaceutical companies to look out for their best interests and 83% favor allowing Medicare to negotiate pricing directly with drug manufacturers (the same as Veteran’s Health does).

There were 1,106 COVID-19 vaccines and drugs in development as of March 18, 2023.

The U.S. industry employs 811,000 directly and 3.2 million indirectly including the 325,000 pharmacists who earn an average of $129,000/year and 447,000 pharm techs who earn $38,000.

And, in the U.S., drug companies spent $100 billion last year for R&D.

It’s a big, high-profile industry that claims 7 of the Top 10 highest paid CEOs in healthcare in its ranks, a persistent presence in social media and paid advertising for its brands and inexplicably strong influence in politics and physician treatment decisions.

The industry is not well liked by consumers, regulators and trading partners but uses every legal lever including patents, couponing, PBM distortion, pay-to-delay tactics, biosimilar roadblocks et al to protect its shareholders’ interests. And it has been effective for its members and advisors.

My take:

It’s easy to pile-on to criticism of the industry’s opaque pricing, lack of operational transparency, inadequate capture of drug efficacy and effectiveness data and impotent punishment against its bad actors and their enablers.

It’s clear U.S. pharma consumers fund the majority of the global industry’s profits while the rest of the world benefits.

And it’s obvious U.S. consumers think it appropriate for the federal government to step in. The tricky part is not just government-imposed price controls for a handful of drugs; it’s how far the federal government should play in other sectors prone to neglect of affordability and equitable access.

There will be lessons learned as this Inflation Reduction Act program is enacted alongside others in the bill– insulin price caps at $35/month per covered prescription, access to adult vaccines without cost-sharing, a yearly cap ($2,000 in 2025) on out-of-pocket prescription drug costs in Medicare and expansion of the low-income subsidy program under Medicare Part D to 150% of the federal poverty level starting in 2024. And since implementation of these price caps isn’t until 2026, plenty of time for all parties to negotiate, spin and adapt.

But the bigger impact of this program will be in other sectors where pricing is opaque, the public’s suspicious and valid and reliable data is readily available to challenge widely-accepted but flawed assertions about quality, value, access and outcomes. It’s highly likely hospitals will be next.