Regular readers of HEALTH CARE un-covered know that I write frequently about the huge amounts of money the health insurance industry’s pharmacy benefit managers (PBMs) extract from the prescription drug supply chain. I also submitted a comment letter to the Federal Trade Commission two and a half years ago urging it to launch an investigation into PBM business practices that have contributed to the closure of hundreds of independent pharmacies across the country and to millions of Americans walking away from the pharmacy counter without their medications.

On a bipartisan basis, the FTC did launch an inquiry into the PBM business, and today the Commission issued a damning interim report that confirmed what industry critics, including me, have been saying:

Just six companies now control 95% of the pharmacy benefit market, and these Big Insurance-owned middlemen “profit at the expense of patients by inflating drug costs and squeezing Main Street pharmacies.” Below you’ll find the commission’s statement on its preliminary findings.

Last year, we also published a profile of one of the industry’s most vocal critics in Congress, Rep. Earl L. “Buddy” Carter (R-Ga.), a pharmacist by trade who has seen PBM’s profiteering firsthand. In a press release this morning, Carter said:

Since day one in Congress, I’ve been calling on the FTC to investigate PBMs, which use deceptive and anti-competitive practices to line their own pockets while reducing patients’ access to affordable, quality health care. I’m proud that the FTC launched a bipartisan investigation into these shadowy middlemen, and its preliminary findings prove yet again that it’s time to bust up the PBM monopoly. We are losing more than one pharmacy per day in this country, causing pharmacy deserts and taking the most accessible health care professionals in America out of people’s communities. I am calling on the FTC to promptly complete its investigation and begin enforcement actions if – and when – it uncovers illegal and anti-competitive PBM practices.

Carter and several other members of Congress have introduced bipartisan bills to rein in PBMs. The House has passed PBM reform legislation but the Senate has not yet done so, but there is growing support in both chambers to enact one or more bills by the end of the year. The FTC’s interim report should make that more likely to happen.

Read the FTC’s full press release below:

FTC Releases Interim Staff Report on Prescription Drug Middlemen

Report details how prescription drug middleman profit at the expense of patients by inflating drug costs and squeezing Main Street pharmacies

The Federal Trade Commission today published an interim report on the prescription drug middleman industry that underscores the impact pharmacy benefit managers (PBMs) have on the accessibility and affordability of prescription drugs.

The interim staff report, which is part of an ongoing inquiry launched in 2022 by the FTC, details how increasing vertical integration and concentration has enabled the six largest PBMs to manage nearly 95 percent of all prescriptions filled in the United States.

This vertically integrated and concentrated market structure has allowed PBMs to profit at the expense of patients and independent pharmacists, the report details.

“The FTC’s interim report lays out how dominant pharmacy benefit managers can hike the cost of drugs—including overcharging patients for cancer drugs,” said FTC Chair Lina M. Khan. “The report also details how PBMs can squeeze independent pharmacies that many Americans—especially those in rural communities—depend on for essential care. The FTC will continue to use all our tools and authorities to scrutinize dominant players across healthcare markets and ensure that Americans can access affordable healthcare.”

The report finds that PBMs wield enormous power over patients’ ability to access and afford their prescription drugs, allowing PBMs to significantly influence what drugs are available and at what price. This can have dire consequences, with nearly 30 percent of Americans surveyed reporting rationing or even skipping doses of their prescribed medicines due to high costs, the report states.

The interim report also finds that PBMs hold substantial influence over independent pharmacies by imposing unfair, arbitrary, and harmful contractual terms that can impact independent pharmacies’ ability to stay in business and serve their communities.

The Commission’s interim report stems from special orders the FTC issued in 2022, under Section 6(b) of the FTC Act, to the six largest PBMs—Caremark Rx, LLC; Express Scripts, Inc.; OptumRx, Inc.; Humana Pharmacy Solutions, Inc.; Prime Therapeutics LLC; and MedImpact Healthcare Systems, Inc. In 2023, the FTC issued additional orders to Zinc Health Services, LLC, Ascent Health Services, LLC, and Emisar Pharma Services LLC, which are each rebate aggregating entities, also known as “group purchasing organizations,” that negotiate drug rebates on behalf of PBMs.

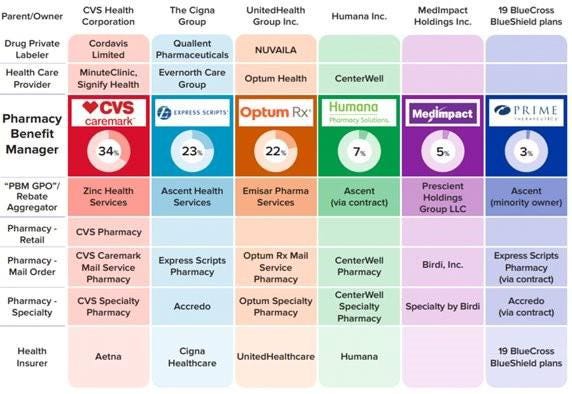

PBMs are part of complex vertically integrated health care conglomerates, and the PBM industry is highly concentrated. As shown in the below image, this concentration and integration gives them significant power over the pharmaceutical supply chain. The percentages reflect the amount of prescriptions filled in the United States.

The interim report highlights several key insights gathered from documents and data obtained from the FTC’s orders, as well as from publicly available information:

Concentration and vertical integration: The market for pharmacy benefit management services has become highly concentrated, and the largest PBMs are now also vertically integrated with the nation’s largest health insurers and specialty and retail pharmacies.

The top three PBMs processed nearly 80 percent of the approximately 6.6 billion prescriptions dispensed by U.S. pharmacies in 2023, while the top six PBMs processed more than 90 percent.

Pharmacies affiliated with the three largest PBMs now account for nearly 70 percent of all specialty drug revenue.

Significant power and influence: As a result of this high degree of consolidation and vertical integration, the leading PBMs now exercise significant power over Americans’ ability to access and afford their prescription drugs.

The largest PBMs often exercise significant control over what drugs are available and at what price, and which pharmacies patients can use to access their prescribed medications.

PBMs oversee these critical decisions about access to and affordability of life-saving medications, without transparency or accountability to the public.

Self-preferencing: Vertically integrated PBMs appear to have the ability and incentive to prefer their own affiliated businesses, creating conflicts of interest that can disadvantage unaffiliated pharmacies and increase prescription drug costs.

PBMs may be steering patients to their affiliated pharmacies and away from smaller, independent pharmacies.

These practices have allowed pharmacies affiliated with the three largest PBMs to retain high levels of dispensing revenue in excess of their estimated drug acquisition costs, including nearly $1.6 billion in excess revenue on just two cancer drugs in under three years.

Unfair contract terms: Evidence suggests that increased concentration gives the leading PBMs leverage to enter contractual relationships that disadvantage smaller, unaffiliated pharmacies.

The rates in PBM contracts with independent pharmacies often do not clearly reflect the ultimate total payment amounts, making it difficult or impossible for pharmacists to ascertain how much they will be compensated.

Efforts to limit access to low-cost competitors: PBMs and brand drug manufacturers negotiate prescription drug rebates some of which are expressly conditioned on limiting access to potentially lower-cost generic and biosimilar competitors.

Evidence suggests that PBMs and brand pharmaceutical manufacturers sometimes enter agreements to exclude lower-cost competitor drugs from the PBM’s formulary in exchange for increased rebates from manufacturers.

The report notes that several of the PBMs that were issued orders have not been forthcoming and timely in their responses, and they still have not completed their required submissions, which has hindered the Commission’s ability to perform its statutory mission. FTC staff have demanded that the companies finalize their productions required by the 6(b) orders promptly. If, however, any of the companies fail to fully comply with the 6(b) orders or engage in further delay tactics, the FTC can take them to district court to compel compliance.

The FTC remains committed to providing timely updates as the Commission receives and reviews additional information.

The Commission voted 4-1 to allow staff to issue the interim report, with Commissioner Melissa Holyoak voting no. Chair Lina M. Khan issued a statement joined by Commissioners Rebecca Kelly Slaughter and Alvaro Bedoya. Commissioners Andrew N. Ferguson and Melissa Holyoak each issued separate statements. The Federal Trade Commission develops policy initiatives on issues that affect competition, consumers, and the U.S. economy. The FTC will never demand money, make threats, tell you to transfer money, or promise you a prize. Follow the FTC on social media, read consumer alerts and the business blog, and sign up to get the latest FTC news and alerts.

Last week, 2 important economic reports were released that provide a retrospective and prospective assessment of the U.S. health economy:

The CBO National Health Expenditure Forecast to 2032:

“Health care spending growth is expected to outpace that of the gross domestic product (GDP) during the coming decade, resulting in a health share of GDP that reaches 19.7% by 2032 (up from 17.3% in 2022). National health expenditures are projected to have grown 7.5% in 2023, when the COVID-19 public health emergency ended. This reflects broad increases in the use of health care, which is associated with an estimated 93.1% of the population being insured that year… During 2027–32, personal health care price inflation and growth in the use of health care services and goods contribute to projected health spending that grows at a faster rate than the rest of the economy.”

The Congressional Budget Office forecast that from 2024 to 2032:

National Health Expenditures will increase 52.6%: $5.048 trillion (17.6% of GDP) to $7,705 trillion (19.7% of GDP) based on average annual growth of: +5.2% in 2024 increasing to +5.6% in 2032

NHE/Capita will increase 45.6%: from $15,054 in 2024 to $21,927 in 2032

Physician services spending will increase 51.2%: from $1006.5 trillion (19.9% of NHE) to $1522.1 trillion (19.7% of total NHE)

Hospital spending will increase 51.6%: from $1559.6 trillion (30.9% of total NHE) in 2024 to $2366.3 trillion (30.7% of total NHE) in 2032.

Prescription drug spending will increase 57.1%: from 463.6 billion (9.2% of total NHE) to 728.5 billion (9.4% of total NHE)

The net cost of insurance will increase 62.9%: from 328.2 billion (6.5% of total NHE) to 534.7 billion (6.9% of total NHE).

The U.S. Population will increase 4.9%: from 334.9 million in 2024 to 351.4 million in 2032.

The Bureau of Labor Statistics CPI Report for May 2024 and Last 12 Months (May 2023-May2024):

“The Consumer Price Index for All Urban Consumers (CPI-U) was unchanged in May on a seasonally adjusted basis, after rising 0.3% in April… Over the last 12 months, the all-items index increased 3.3% before seasonal adjustment. More than offsetting a decline in gasoline, the index for shelter rose in May, up 0.4% for the fourth consecutive month. The index for food increased 0.1% in May. … The index for all items less food and energy rose 0.2% in May, after rising 0.3 % the preceding month… The all-items index rose 3.3% for the 12 months ending May, a smaller increase than the 3.4% increase for the 12 months ending April. The all items less food and energy index rose 3.4 % over the last 12 months. The energy index increased 3.7%for the 12 months ending May. The food index increased 2.1%over the last year.

Medical care services, which represents 6.5% of the overall CPI, increased 3.1%–lower than the overall CPI. Key elements included in this category reflect wide variance: hospital and OTC prices exceeded the overall CPI while insurance, prescription drugs and physician services were lower.

Physicians’ services CPI (1.8% of total impact): LTM: +1.4%

Hospital services CPI (1.0% of total impact): LTM: +7.3%

Prescription drugs (.9% of total impact) LTM +2.4%

Over the Counter Products (.4% of total impact) LTM 5.9%

Health insurance (.6% of total) LTM -7.7%

Other categories of greater impact on the overall CPI than medical services are Shelter (36.1%), Commodities (18.6%), Food (13.4%), Energy (7.0%) and Transportation (6.5%).

Three key takeaways from these reports:

The health economy is big and getting bigger. But it’s less obvious to consumers in the prices they experience than to employers, state and federal government who fund the majority of its spending. Notably, OTC products are an exception: they’re a direct OOP expense for most consumers. To consumers, especially renters and young adults hoping to purchase homes, the escalating costs of housing have considerably more impact than health prices today but directly impact on their ability to afford coverage and services. Per Redfin, mortgage rates will hover at 6-7% through next year and rents will increase 10% or more.

Proportionate to National Health Expenditure growth, spending for hospitals and physician services will remain at current levels while spending for prescription drugs and health insurance will increase. That’s certain to increase attention to price controls and heighten tension between insurers and providers.

There’s scant evidence the value agenda aka value-based purchases, alternative payment models et al has lowered spending nor considered significant in forecasts.

The health economy is expanding above the overall rates of population growth, overall inflation and the U.S. economy. GDP. Its long-term sustainability is in question unless monetary policies enable other industries to grow proportionately and/or taxpayers agree to pay more for its services. These data confirm its unit costs and prices are problematic.

As Campaign 2024 heats up with the economy as its key issue, promises to contain health spending, impose price controls, limit consolidation and increase competition will be prominent.

Public sector actions

will likely feature state initiatives to lower cost and spend taxpayer money more effectively.

Private sector actions

will center on employer and insurer initiatives to increase out of pocket payments for enrollees and reduce their choices of providers.

Thus, these reports paint a cautionary picture for the health economy going forward. Each sector will feel cost-containment pressure and each will claim it is responding appropriately. Some actually will.

PS: The issue of tax exemptions for not-for-profit hospitals reared itself again last week.

The Committee for a Responsible Federal Budget—a conservative leaning think tank—issued a report arguing the exemption needs to be ended or cut. In response,

the American Hospital Association issued a testy reply claiming the report’s math misleading and motivation ill-conceived.

This issue is not going away: it requires objective analysis, fresh thinking and new voices. For a recap, see the Hospital Section below.

Two important reports released last Wednesday point to a disconnect in how policymakers are managing the U.S. economy and how the health economy fits.

Report One: The Federal Reserve Open Market Meeting

At its meeting last week, the Governors of the Federal Open Market Committee (FOMC) voted unanimously to keep the target range for the federal funds rate at 5% to 5.25%–the first time since last March that the Fed has concluded a policy meeting without raising interest rates.

In its statement by Chairman Powell, the central bank left open the possibility of additional rate hikes this year which means interest rates could hit 5.6% before trending slightly lower in 2024.

In conjunction with the (FOMC) meeting, meeting participants submitted projections of the most likely outcomes for each year from 2023 to 2025 and over the longer run:

Median

2023

2024

2025

Longer Run

Longer Run Range

% Change in GDP

1.1

1.1

1.8

1.8

1.6-2.5

Unemployment rate &

4.1

4.5

4.5

4.0

3.6-4.4

PCE Inflation rate

3.2

2.5

2.1

2.0

2.0

Core PCE Inflation

3.9

2.6

2.2

*

*

*Longer-run projections for core PCE inflation are not collected.

Notes re: the Fed’s projections based on these indicators:

The GDP (a measure of economic growth) is expected to increase 1% more this year than anticipated in its March 2023 analysis while estimates for 2024 were lowered just slightly by 0.1%. Economic growth will continue but at a slower pace.

The unemployment rate is expected to increase to 4.1% by the end of 2023, a smaller rise in joblessness than the previous estimate of 4.5%. (As of May, the unemployment rate was 3.7%). Unemployment is returning to normalcy impacting the labor supply and wages.

inflation: as measured by the Personal Consumption Expenditures index, will be 3.2% at the end of 2023 vs. 3.3% they previously projected. By the end of 2024, it expects inflation will be 2.5% reaching 2.1% at the end of 2025. Its 2.0% target is within reach on or after 2025 barring unforeseen circumstances.

Core inflation projections, which excludes energy and food prices, increased: the Fed now anticipates 3.9% by the end of 2023–0.3% above the March estimate. Price concerns will continue among consumers.

Based on these projections, two conclusions about nation’s monetary policy may be deduced the Fed’s report and discussion:

The Fed is cautiously optimistic about the U.S. economy in for the near term (through 2025) while acknowledging uncertainty exists.

Interest rates will continue to increase but at a slower rate than 2022 making borrowing and operating costs higher and creditworthiness might also be under more pressure.

Report Two: CMS

On the same day as the Fed meeting, the actuaries at the Centers for Medicare and Medicaid Services (CMS) released their projections for overall U.S. national healthcare spending for the next several years:

“CMS projects that over 2022-2031, average annual growth in NHE (5.4%) will outpace average annual growth in gross domestic product (GDP) (4.6%), resulting in an increase in the health spending share of GDP from 18.3% in 2021 to 19.6% in 2031. The insured percentage of the population is projected to have reached a historic high of 92.3% in 2022 (due to high Medicaid enrollment and gains in Marketplace coverage). It is expected to remain at that rate through 2023. Given the expiration of the Medicaid continuous enrollment condition on March 31, 2023 and the resumption of Medicaid redeterminations, Medicaid enrollment is projected to fall over 2023-2025, most notably in 2024, with an expected net loss in enrollment of 8 million beneficiaries. If current law provisions in the Affordable Care Act are allowed to expire at the end of 2025, the insured share of the population is projected to be 91.2%. In 2031, the insured share of the population is projected to be 90.5%, similar to pre-pandemic levels.”

The report includes CMS’ assumptions for 4 major payer categories:

Medicare Part D: Several provisions from the Inflation Reduction Act (IRA) are expected to result in out-of-pocket savings for individuals enrolled in Medicare Part D. These provisions have notable effects on the growth rates for total out-of-pocket spending for prescription drugs, which are projected to decline by 5.9% in 2024, 4.2% in 2025, and 0.2% in 2026.

Medicare: Average annual expenditure growth of 7.5% is projected for Medicare over 2022-2031. In 2022, the combination of fee-for-service beneficiaries utilizing emergent hospital care at lower rates and the reinstatement of payment rate cuts associated with the Medicare Sequester Relief Act of 2022 resulted in slower Medicare spending growth of 4.8% (down from 8.4% in 2021).

Medicaid: On average, over 2022-2031, Medicaid expenditures are projected to grow by 5.0%. With the end of the continuous enrollment condition in 2023, Medicaid enrollment is projected to decline over 2023-2025, with most of the net loss in enrollment (8 million) occurring in 2024 as states resume annual Medicaid redeterminations. Medicaid enrollment is expected to increase and average less than 1% through 2031, with average expenditure growth of 5.6% over 2025-2031.

Private Health Insurance: Over 2022-2031, private health insurance spending growth is projected to average 5.4%. Despite faster growth in private health insurance enrollment in 2022 (led by increases in Marketplace enrollment related to the American Rescue Plan Act’s subsidies), private health insurance expenditures are expected to have risen 3.0% (compared to 5.8% in 2021) due to lower utilization growth, especially for hospital services.

And for the 3 major recipient/payee categories:

Hospitals: Over 2022-2031, hospital spending growth is expected to average 5.8% annually. In 2023, faster growth in hospital utilization rates and accelerating growth in hospital prices (related to economy wide inflation and rising labor costs) are expected to lead to faster hospital spending growth of 9.3%. For 2025-2031, hospital spending trends are expected to normalize (with projected average annual growth of 6.1%) as there is a transition away from pandemic public health emergency funding impacts on spending.

Physicians and Clinical Services: Growth in physician and clinical services spending is projected to average 5.3% over 2022-2031. An expected deceleration in growth in 2022, to 2.4% from 5.6% in 2021, reflects slowing growth in the use of services following the pandemic-driven rebound in use in 2021. For 2025-2031, average spending growth for physician and clinical services is projected to be 5.7%, with an expectation that average Medicare spending growth (8.1%) for these services will exceed that of average Private Health Insurance growth (4.6%) partly as a result of comparatively faster growth in Medicare enrollment.

Prescription Drugs: Total expenditures for retail prescription drugs are projected to grow at an average annual rate of 4.6% over 2022-2031. For 2025-2031, total spending growth on prescription drugs is projected to average 4.8%, reflecting the net effects of key IRA provisions: Part D benefit enhancements (putting upward pressure on Medicare spending growth) and price negotiations/inflation rebates (putting downward pressure on Medicare and out-of-pocket spending growth).

Thus, CMS Actuaries believe spending for healthcare will be considerably higher than the growth of the overall economy (GDP) and inflation and become 19.6% of the total US economy in 2031. And it also projects that the economy will absorb annual spending increases for hospitals (5.8%) physician and clinical services (5.3%) and prescription drugs (4.6%).

My take:

Side-by-side, these reports present a curious projection for the U.S. economy through 2031: the overall economy will return to a slightly lower-level pre-pandemic normalcy and the healthcare industry will play a bigger role despite pushback from budget hawks preferring lower government spending and employers and consumers frustrated by high health prices today.

They also point to two obvious near-term problems:

1-The Federal Reserve pays inadequate attention to the healthcare economy. In Chairman Powell’s press conference following release of the FOMC report, there was no comment relating healthcare demand or spending to the broader economy nor a question from any of the 20 press corps relating healthcare to the overall economy. In his opening statement (below), Chairman Powell reiterated the Fed’s focus on prices and called out food, housing and transportation specifically but no mention of healthcare prices and costs which are equivalent or more stressful to household financial security:

“Good afternoon. My colleagues and I remain squarely focused on our dual mandate to promote maximum employment and stable prices for the American people…My colleagues and I are acutely aware that high inflation imposes hardship as it erodes purchasing power, especially for those least able to meet the higher costs of essentials like food, housing, and transportation. We are highly attentive to the risks that high inflation poses to both sides of our mandate, and we are strongly committed to returning inflation to our 2% objective.”

2-Congress is reticent to make substantive changes in Medicare and other healthcare programs despite its significance in the U.S. economy. It’s politically risky. In the June 2 Congressional standoff to lift the $31.4 debt ceiling, cuts to Medicare and Social Security were specifically EXCLUDED. Medicare is 12% of mandated spending in the 2022 federal budget and is expected to grow from a rate of 4.8% in 2022 to 8% in 2023—good news for investors in Medicare Advantage but concerning to consumers and employers facing higher prices as a result.

Even simplifying the Medicare program to replace its complicated Parts A, B, C, and D programs or addressing over-payments to Medicare Advantage plans (in 2022, $25 billion per MedPAC and $75 billion per USC) is politically tricky. It’s safer for elected officials to support price transparency (hospitals, drugs & insurers) and espouse replacing fee for service payments with “value” than step back and address the bigger issue: how should the health system be structured and financed to achieve lower costs and better health…not just for seniors or other groups but everyone.

These two realities contribute to the disconnect between the Fed and CMS. Looking back 20 years across 4 Presidencies, two economic downturns and the pandemic, it’s also clear the health economy’s emergence did not occur overnight as the Fed navigated its monetary policy. Consider:

National health expenditures were $1.366 trillion (13.3% of GDP) in 2000 and $4.255 billion in 2021 (18.3% of the GDP). This represents 210% increase in nominal spending and a 37.5% increase in the relative percentage of the nation’s GDP devoted to healthcare. No other sector in the economy has increased as much.

In the same period, the population increased 17% from 282 million to 334 million while per capita healthcare spending increased 166% from $4,845 to $12,914. This disproportionate disconnect between population and health spending growth is attributed by economists to escalating unit costs increases for the pills, facilities, technologies and specialty-provider services we use—their underlying cost escalation notably higher than other industries.

There were notable changes in where dollars were spent: hospitals were unchanged (from $415 billion/30.4% of total spending to $1.323 trillion/31.4% of total spending), physician services shrank (from $288.2 billion/21.1% of total spending to 664.6 billion/15.6% pf total spending), prescription drugs were unchanged (from $122.3 billion/8.95% to $378 billion/8.88% of total spending) and public health increased slightly (from $43 billion/$3.2% of total spending to $187.6 billion/4.4% of total spending).

And striking differences in sources of funding: out of pocket spending shrank from $193.6/14.2% of payments to $433 billion/10.2% % of payments; private insurance shrank from $441 billion/32.3% of payments to $1.21 trillion/28.4% of total payments; Medicare grew from $224.8 billion/16.5% of payments to $900.8 billion/21.2% of payments; Medicaid + CHIP grew from $203.4 billion/14.9% to $756.2 billion/17.8% of payments; and Veterans Health grew from $19.1 billion/1.4% of payments to $106.0 billion/2.5% of payments.

Thus, if these trends continue…

Aggregate payments to providers from government programs will play a bigger role and payments from privately insured individuals and companies will play a lesser role.

Hospital price increases will exceed price increases for physician services and prescription drugs.

Spending for healthcare will (continue to) exceed overall economic growth requiring additional funding from taxpayers, employers and consumers AND/OR increased dependence on private investments that require shareholder return AND/OR a massive restructure of the entire system to address its structure and financing.

What’s clear from these reports is the enormity of the health economy today and tomorrow, the lack of adequate attention and Congressional Action to address its sustainability and the range of unintended, negative consequences on households and every other industry if left unattended. It’s illustrative of the disconnect between the Fed and CMS: one assumes it controls the money supply while delegating to the other spending and policies independent of broader societal issues and concerns.

The health economy needs fresh attention from inside and outside the industry. Its impact includes not only the wellbeing of its workforce and services provided its users. It includes its direct impact on household financial security, community health and the economic potential of other industries who get less because healthcare gets more.

Securing the long-term sustainability of the U.S. economy and its role in world affairs cannot be appropriately addressed unless its health economy is more directly integrated and scrutinized. That might be uncomfortable for insiders but necessary for the greater good. Recognition of the disconnect between the Fed and CMS is a start!

American Medical Association President Jack Resneck Jr., MD, detailed in a post on the medical group’s website the “Kafkaesque” prior authorization process that an unnamed insurance company allegedly put one of his patients through.

Dr. Resneck, a San Francisco-based dermatologist, was treating a patient with severe head-to-toe eczema, who was unable to sleep because of the condition, according to the post. Dr. Resneck found a medication that allowed the patient to sleep and return to work.

Several months later, however, the patient was unable to get the prescription refilled at the pharmacy, according to the report. Dr. Resneck completed the paperwork describing how well the patient had responded to the medication, as required by the insurance company, and faxed it over. The prior authorization request for the prescription refill was rejected.

Dr. Resneck said the insurance company rejected the refill on the grounds that the patient no longer met the severity criteria because not enough of his body was covered and he was not missing enough sleep.

The insurance company allegedly wanted to take the patient off the medication for several weeks to let his eczema flare up again, according to the post. It took more than 20 additional telephone calls until the patient’s prescription was refilled.

This week, California Governor Gavin Newsom announced the state has struck a 10-year, $50M partnership with nonprofit drugmaker Civica Rx to produce three versions of generic insulin.

These are intended to be made available nationwide for list prices of no more than $30 a vial.

Production is slated to begin in late 2023 at Civica’s Petersburg, VA plant, and Food and Drug Administration approval will be required. This deal advances California’s CalRx initiative to produce and distribute generic drugs at low costs; according to a Newsom administration official, the low-cost insulin will be available to state residents through mail-order and retail pharmacies. This is the first state-level partnership for Civica, a health system collaborative whose members now cover a third of all US hospital capacity.

The Gist:Since Congress capped insulin copays for Medicare beneficiaries at $35 per month, there’s been a remarkable sea change in the pricing of the drug. Last week, Sanofi joined Eli Lilly and Novo Nordisk, the three of which together control 90 percent of the US insulin market, in dramatically reducing insulin list prices and capping out-of-pocket costs (including for the uninsured), bringing them in line with the costs now paid by Medicare beneficiaries.

Given that most Americans needing insulin are already covered by these policies, the impact of California’s initiative may be muted. However, it sets an important precedent for state partnership in pharmaceutical productionthat will surely expand to other drugs (Newsom stated generic naloxone could be next)—and works to position Newsom as an advocate for lower drug costs, should he seek higher office.

Telemedicine is supposed to make consumers’ lives easier, right? One of us had the opposite experience when managing a sick kid this week. My 14-year-old has been sick with a bad respiratory illness for over a week. We saw her pediatrician in-person, testing negative for COVID (multiple times), flu, and strep. Over the week, her symptoms worsened, and rather than haul her back to the doctor, we decided to give our health plan’s telemedicine service a try. To the plan’s credit, the video visit was easy to schedule, and we were connected to a doctor within minutes. He agreed that symptoms and timeline warranted an antibiotic, and said he was sending the prescription to our pharmacy as we wrapped up the call.

Here’s where the challenges began. We went to our usual CVS a few hours later, and they had no record of the prescription. (Note to telemedicine users: write down the name of your provider. The pharmacy asked to search for the script by the doctor’s name, which I didn’t remember—and holding up the line of a dozen other customers to fumble with the app seemed like the wrong call.)

We left and contacted the telemedicine service to see if the prescription had been transmitted, and after a half hour on hold, were finally transferred to pharmacy support. It turns out that the telemedicine service transmits their prescriptions via “e-fax”, so it was difficult to confirm if the pharmacy had received it. Not to be confused with e-prescribing, e-fax is literally an emailed image of a prescription, with none of the safeguards and communication capabilities of true electronic prescribing.

The helpful service representative kindly offered to call the pharmacy and placed us on hold—only to get a message that the pharmacy was closed for lunch and not accepting calls! Several hours later, which included being on hold for 75 minutes (!!!) with our CVS, my daughter finally got her medication.

Despite the slick app and teleconferencing system, the operations behind the virtual visit still relied on the very analog processes of phone trees and faxes—which created a level of irritation that rivaled trying to land Taylor Swift tickets for the same kid. It was a stark reminder of how far healthcare has to go to deliver a truly digital, consumer-centered experience.

A recent STAT News article highlights a concerning new trend in direct-to-consumer pharmaceutical marketing, enabled by access to virtual care. Pitched as a tool for patient empowerment, pharmaceutical companies are now offering consumers immediate treatment for a variety of health conditions at the click of a button that says, “Talk to a doctor now.”

Over 90 percent of eligible patients receive a prescription for the drug they “clicked” on, after connecting with a virtual care provider on a third-party telehealth platform. Not only does this practice give drug companies direct access to prospective patients, but it also delivers lucrative data on patient age, zip code, and medication history that can be used to target marketing efforts.

The Gist: Articles like this remind us why the US is one of only two countries in the world that allows direct-to-consumer marketing of prescription drugs (the other, interestingly, is New Zealand).

As the number of Americans with a primary care provider continues to decline, this kind of Amazon-style, easy-button drug shopping experience will be increasingly appealing to many consumers. But wherever innovation outpaces regulation, situations in which for-profit companies prioritize profits over providing the best care for patients are sure to occur.

While we support the idea of greater consumer empowerment in healthcare, we worry that this highly fragmented approach to consumer-driven health can result in abuse and patient harm.

In a unanimous decision, the Justices found that the Department of Health and Human Services (HHS) exceeded its legal authority when it cut Medicare reimbursement rates for outpatient drugs by 28.5 percent at 340B-eligible hospitals in 2018. The justices wrote that the Centers for Medicare and Medicaid Services (CMS) shouldn’t have cut payments to these hospitals without first surveying their average drug acquisition costs, as required by statute.

CMS must now figure out how to repay 340B hospitals the difference in reimbursement for 2018 and 2019, the two years the unlawful cuts were in effect, during which time it redistributed those savings to all hospitals in the form of higher reimbursement for outpatient services. (For an explainer on the mechanics of the 340B program, see our overview here, and for more details on this Supreme Court case, see our summary here.)

The Gist: This decision was a narrow ruling on administrative grounds, and did not touch on the larger policy debates concerning the 340B program. While 340B-eligible health systems can breathe a momentary sigh of relief, they are still facing significant, ongoing revenue disruptions as at least 17 pharmaceutical manufacturers are restricting discounted drug sales to contract pharmacies.

Scrutiny of the 340B program, which has grown to include over 40 percent of US hospitals, will continue to raise questions aboutwhether there are better ways to subsidize the operations of hospitals serving low-income patients, and to ensure that underserved patients have access to lifesaving treatments.