Last week was significant for healthcare:

- Tuesday, the, FTC, and DOJ announced creation of a task force focused on tackling “unfair and illegal pricing” in healthcare. The same day, HHS joined FTC and DOJ regulators in launching an investigation with the DOJ and FTC probing private equity’ investments in healthcare expressing concern these deals may generate profits for corporate investors at the expense of patients’ health, workers’ safety and affordable care.

- Thursday’s State of the Union address by President Biden (SOTU) and the Republican response by Alabama Senator Katey Britt put the spotlight on women’s reproductive health, drug prices and healthcare affordability.

- Friday, the Senate passed a $468 billion spending bill (75-22) that had passed in the House Wednesday (339-85) averting a government shutdown. The bill postpones an $8 billion reduction in Medicaid disproportionate share hospital payments for a year, allocates $4.27 billion to federally qualified health centers through the end of the year and rolls back a significant portion of a Medicare physician pay cut that kicked in on Jan. 1. Next, Congress must pass appropriations for HHS and other agencies before the March 22 shutdown.

- And all week, the cyberattack on Optum’s Change Healthcare discovered February 21 hovered as hospitals, clinics, pharmacies and others scrambled to manage gaps in transaction processing. Notably, the American Hospital Association and others have amplified criticism of UnitedHealth Group’s handling of the disruption, having, bought Change for $13 billion in October, 2022 after a lengthy Department of Justice anti-trust review. This week, UHG indicates partial service of CH support will be restored. Stay tuned.

Just another week for healthcare: Congressional infighting about healthcare spending. Regulator announcements of new rules to stimulate competition and protect consumers in the healthcare market. Lobbying by leading trade groups to protect funding and disable threats from rivals. And so on.

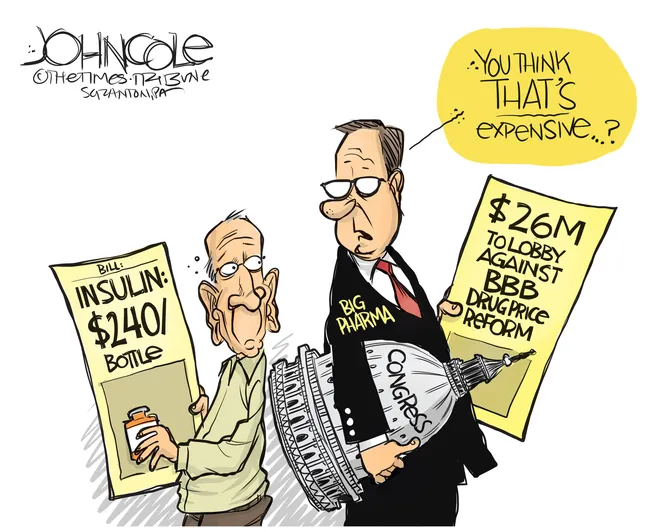

At the macro level, it’s understandable: healthcare is an attractive market, especially in its services sectors. Since the pandemic, prices for services (i.e. physicians, hospitals et al) have steadily increased and remain elevated despite the pressures of transparency mandates and insurer pushback. By contrast, prices for most products (drugs, disposables, technologies et al) have followed the broader market pricing trends where prices for some escalated fast and then dipped.

While some branded prescription medicines are exceptions, it is health services that have driven the majority of health cost inflation since the pandemic.

UnitedHealth Group’s financial success is illustrative:

it’s big, high profile and vertically integrated across all major services sectors. In its year end 2023 financial report (January 12, 2024) it reported revenues of $371.6 Billion (up 15% Year-Over-Year), earnings from operations up 14%, cash flows from operations of $29.1 Billion (1.3x Net Income), medical care ratio at 83.2% up from 82% last year, net earnings of $23.86/share and adjusted net earnings of $25.12/share and guidance its 2024 revenues of $400-403 billion. They buy products using their scale and scope leverage to pay less for services they don’t own less and products needed to support them. It’s a big business in a buyer’s market and that’s unsettling to many.

Big business is not new to healthcare:

it’s been dominant in every sector but of late more a focus of unflattering regulator and media attention. Coupled with growing public discontent about the system’s effectiveness and affordability, it seems it’s near a tipping point.

David Johnson, one of the most thoughtful analysts of the health industry, reminded his readers last week that the current state of affairs in U.S. healthcare is not new citing the January 1970 Fortune cover story “Our Ailing Medical System”

“American medicine, the pride of the nation for many years, stands now on the brink of chaos. To be sure, our medical practitioners have their great moments of drama and triumph. But much of U.S. medical care, particularly the everyday business of preventing and treating routine illnesses, is inferior in quality, wastefully dispensed, and inequitably financed…

Whether poor or not, most Americans are badly served by the obsolete, overstrained medical system that has grown up around them helter-skelter. … The time has come for radical change.”

Johnson added: “The healthcare industry, however, cannot fight gravity forever. Consumerism, technological advances and pro-market regulatory reforms are so powerful and coming so fast that status-quo healthcare cannot forestall their ascendance. Properly harnessed, these disruptive forces have the collective power necessary for U.S. healthcare to finally achieve the 1970 Fortune magazine goal of delivering “good care to every American with little increase in cost.”

He’s right.

I believe the U.S. health system as we know it has reached its tipping point. The big-name organizations in every sector see it and have nominal contingency plans in place; the smaller players are buying time until the shoe drops. But I am worried.

I am worried the system’s future is in the hands of hyper-partisanship by both parties seeking political advantage in election cycles over meaningful creation of a health system that functions for the greater good.

I am worried that the industry’s aversion to price transparency, meaningful discussion about affordability and consistency in defining quality, safety and value will precipitate short-term gamesmanship for reputational advantage and nullify systemness and interoperability requisite to its transformation.

I am worried that understandably frustrated employers will drop employee health benefits to force the system to needed accountability.

I am worried that the growing armies of under-served and dissatisfied populations will revolt.

I am worried that its workforce is ill-prepared for a future that’s technology-enabled and consumer centric.

I am worried that the industry’s most prominent trade groups are concentrating more on “warfare” against their rivals and less about the long-term future of the system.

I am worried that transformational change is all talk.

It’s time to start an adult conversation about the future of the system. The starting point: acknowledging that it’s not about bad people; it’s about systemic flaws in its design and functioning. Fixing it requires balancing lag indicators about its use, costs and demand with assumptions about innovations that hold promise to shift its trajectory long-term. It requires employers to actively participate: in 2009-2010, Big Business mistakenly chose to sit out deliberations about the Affordable Care Act. And it requires independent, visionary facilitation free from bias and input beyond the DC talking heads that have dominated reform thought leadership for 6 decades.

Or, collectively, we can watch events like last week’s roll by and witness the emergence of a large public utility serving most and a smaller private option for those that afford it. Or something worse.

P.S. Today, thousands will make the pilgrimage to Orlando for HIMSS24 kicking off with a keynote by Robert Garrett, CEO of Hackensack Meridian Health tomorrow about ‘transformational change’ and closing Friday with a keynote by Nick Saban, legendary Alabama football coach on leadership. In between, the meeting’s 24 premier supporters and hundreds of exhibitors will push their latest solutions to prospects and customers keenly aware healthcare’s future is not a repeat of its past primarily due to technology. Information-driven healthcare is dependent on technologies that enable cost-effective, customized evidence-based care that’s readily accessible to individuals where and when they want it and with whom.

And many will be anticipating HCA Mission Health’s (Asheville NC) Plan of Action response due to CMS this Wednesday addressing deficiencies in 6 areas including CMS Deficiency 482.12 “which ensures that hospitals have a responsible governing body overseeing critical aspects of patient care and medical staff appointments.” Interest is high outside the region as the nation’s largest investor-owned system was put in “immediate jeopardy” of losing its Medicare participation status last year at Mission. FYI: HCA reported operating income of $7.7 billion (11.8% operating margin) on revenues of $65 billion in 2023.