Retail giant Walmart announced the 2024 opening of four new health centers in Oklahoma.

Oklahoma joins Missouri and Arizona as the third state Walmart Health will enter in 2024.

The 5,570-square-foot centers will be located next to Walmart retail locations and will include primary care, labs, X-rays, EKG, behavioral health, dental, hearing and telehealth services, according to an April 26 Walmart news release.

The health centers will use the Epic EHR system. The new locations will be in the Oklahoma City area, according to the release.

I have been both a frontline officer and a staff officer at a health system. I started a solo practice in 1977 and cared for my rheumatology, internal medicine and geriatrics patients in inpatient and outpatient settings. After 23 years in my solo practice, I served 18 years as President and CEO of a profitable, CMS 5-star, 715-bed, two-hospital healthcare system.

From 2015 to 2020, our health system team added 0.6 years of healthy life expectancy for 400,000 folks across the socioeconomic spectrum. We simultaneously decreased healthcare costs 54% for 6,000 colleagues and family members. With our mentoring, four other large, self-insured organizations enjoyed similar measurable results. We wanted to put our healthcare system out of business. Who wants to spend a night in a hospital?

During the frontline part of my career, I had the privilege of “Being in the Room Where It Happens,” be it the examination room at the start of a patient encounter, or at the end of life providing comfort and consoling family. Subsequently, I sat at the head of the table, responsible for most of the hospital care in Southwest Florida. [1]

Many folks commenting on healthcare have never touched a patient nor led a large system. Outside consultants, no matter how competent, have vicarious experience that creates a different perspective.

At this point in my career, I have the luxury of promoting what I believe is in the best interests of patients — prevention and quality outcomes. Keeping folks healthy and changing the healthcare industry’s focus from a “repair shop” mentality to a “prevention program” will save the industry and country from bankruptcy. Avoiding well-meaning but inadvertent suboptimal care by restructuring healthcare delivery avoids misery and saves lives.

RESPONDING TO AN ATTACK

Preemptive reinvention is much wiser than responding to an attack. Unfortunately, few industries embrace prevention. The entire healthcare industry, including health systems, physicians, non-physician caregivers, device manufacturers, pharmaceutical firms, and medical insurers, is stressed because most are experiencing serious profit margin squeeze. Simultaneously the public has ongoing concerns about healthcare costs. While some medical insurance companies enjoyed lavish profits during COVID, most of the industry suffered. Examples abound, and Paul Keckley, considered a dean among long-time observers of the medical field, recently highlighted some striking year-end observations for 2022. [2]

Recent Siege Examples

Transparency is generally good but can and has led to tarnishing the noble profession of caring for others. Namely, once a sector starts bleeding, others come along, exacerbating the exsanguination. Current literature is full of unflattering public articles that seem to self-perpetuate, and I’ve highlighted standout samples below.

The Federal Government is the largest spender in the healthcare industry and therefore the most influential. Not surprisingly, congressional lobbying was intense during the last two weeks of 2022 in a partially successful effort to ameliorate spending cuts for Medicare payments for physicians and hospitals. Lobbying spend by Big Pharma, Blue Cross/Blue Shield, American Hospital Association, and American Medical Association are all in the top ten spenders again. [3, 4, 5] These organizations aren’t lobbying for prevention, they’re lobbying to keep the status quo.

Concern about consistent quality should always be top of mind. “Diagnostic Errors in the Emergency Department: A Systematic Review,” shared by the Agency for Healthcare Research and Quality, compiled 279 studies showing a nearly 6% error rate for the 130 million people who visit an ED yearly. Stroke, heart attack, aortic aneurysm, spinal cord injury, and venous thromboembolism were the most common harms. The defense of diagnostic errors in emergency situations is deemed of secondary importance to stabilizing the patient for subsequent diagnosing. Keeping patients alive trumps everything. Commonly, patient ED presentations are not clear-cut with both false positive and negative findings. Retrospectively, what was obscure can become obvious. [6, 7]

Spending mirrors motivations. The Wall Street Journal article “Many Hospitals Get Big Drug Discounts. That Doesn’t Mean Markdowns for Patients” lays out how the savings from a decades-old federal program that offers big drug discounts to hospitals generally stay with the hospitals. Hospitals can chose to sell the prescriptions to patients and their insurers for much more than the discounted price. Originally the legislation was designed for resource-challenged communities, but now some hospitals in these programs are profiting from wealthy folks paying normal prices and the hospitals keeping the difference. [8]

“Hundreds of Hospitals Sue Patients or Threaten Their Credit, a KHN Investigation Finds. Does Yours?” Medical debt is a large and growing problem for both patients and providers. Healthcare systems employ collection agencies that typically assess and screen a patient’s ability to pay. If the credit agency determines a patient has resources and has avoided paying his/her debt, the health system send those bills to a collection agency. Most often legitimately impoverished folks are left alone, but about two-thirds of patients who could pay but lack adequate medical insurance face lawsuits and other legal actions attempting to collect payment including garnishing wages or placing liens on property. [9]

“Hospital Monopolies Are Destroying Health Care Value,” written by Rep. Victoria Spartz (R-Ind.) in The Hill, includes a statement attributed to Adam Smith’s The Wealth of Nations, “that the law which facilitates consolidation ends in a conspiracy against the public to raise prices.” The country has seen over 1,500 hospital mergers in the past twenty years — an example of horizontal consolidation. Hospitals also consolidate vertically by acquiring physician practices. As of January 2022, 74 percent of physicians work directly for hospitals, healthcare systems, other physicians, or corporate entities, causing not only the loss of independent physicians but also tighter control of pricing and financial issues. [10] The healthcare industry is an attractive target to examine. Everyone has had meaningful healthcare experiences, many have had expensive and impactful experiences. Although patients do not typically understand the complexity of providing a diagnosis, treatment, and prognosis, the care receiver may compare the experience to less-complex interactions outside healthcare that are customer centric and more satisfying.

PROFIT-MARGIN SQUEEZE

Both nonprofit and for-profit hospitals must publish financial statements. Three major bond rating agencies (Fitch Ratings, Moody’s Investors Service, and S & P Global Ratings) and other respected observers like KaufmanHall, collate, review, and analyze this publicly available information and rate health systems’ financial stability.

One measure of healthcare system’s financial strength is operating margin, the amount of profit or loss from caring for patients. In January of 2023 the median, or middle value, of hospital operating margin index was -1.0%, which is an improvement from January 2022 but still lags 2021 and 2020.

Erik Swanson, SVP at KaufmanHall, says 2022,

“Is shaping up to be one of the worst financial years on record for hospitals. Expense pressures — particularly with the cost of labor — outpaced revenues and drove poor performance. While emergency department visits and operating room minutes increased slightly, hospitals struggled to discharge patients due to internal staffing shortages and shortages at post-acute facilities,” [11]

Another force exacerbating health system finance is the competent, if relatively new retailers (CVS, Walmart, Walgreens, and others) that provide routine outpatient care affordably. Ninety percent of Americans live within ten miles of a Walmart and 50% visit weekly. CVS and Walgreens enjoy similar penetration. Profit-margin squeeze, combined with new convenient options to obtain routine care locally, will continue disrupting legacy healthcare systems.

Providers generate profits when patients access care. Additionally, “easy” profitable outpatient care can and has switched to telemedicine. Kaiser-Permanente (KP), even before the pandemic, provided about 50% of the system’s care through virtual visits. Insurance companies profit when services are provided efficiently or when members don’t use services. KP has the enviable position of being both the provider and payor for their members. The balance between KP’s insurance company and provider company favors efficient use of limited resources. Since COVID, 80% of all KP’s visits are virtual, a fact that decreases overhead, resulting in improved profit margins. [12]

On the other hand, KP does feel the profit-margin squeeze because labor costs have risen. To avoid a nurse labor strike, KP gave 21,000 nurses and nurse practitioners a 22.5% raise over four years. KP’s most recent quarter reported a net loss of $1.5B, possibly due to increased overhead. [13]

The public, governmental agencies, and some healthcare leaders are searching for a more efficient system with better outcomes

at a lower cost. Our nation cannot continue to spend the most money of any developed nation and have the worst outcomes. In a globally competitive world, limited resources must go to effective healthcare, balanced with education, infrastructure, the environment, and other societal needs. A new healthcare model could satisfy all these desires and needs.

Even iconic giants are starting to feel the pain of recent annual losses in the billions. Ascension Health, Cleveland Clinic, Jefferson Health, Massachusetts General Hospital, ProMedica, Providence, UPMC, and many others have gone from stable and sustainable to stressed and uncertain. Mayo Clinic had been a notable exception, but recently even this esteemed system’s profit dropped by more than 50% in 2022 with higher wage and supply costs up, according to this Modern Healthcare summary. [14]

The alarming point is even the big multigenerational health system leaders who believed they had fortress balance sheets are struggling. Those systems with decades of financial success and esteemed reputations are in jeopardy. Changing leadership doesn’t change the new environment.

Nonprofit healthcare systems’ income typically comes from three sources — operations, namely caring for patients in ways that are now evolving as noted above; investments, which are inherently risky evidence by this past year’s record losses; and philanthropy, which remains fickle particularly when other investment returns disappoint potential donors. For-profit healthcare systems don’t have the luxury of philanthropic support but typically are more efficient with scale and scope.

The most stable and predictable source of revenue in the past was from patient care. As the healthcare industry’s cost to society continues to increase above 20% of the GDP, most medically self-insured employers and other payors will search for efficiencies. Like it or not, persistently negative profit margins will transform healthcare.

Demand for nurses, physicians, and support folks is increasing, with many shortages looming near term. Labor costs and burnout have become pressing stresses, but more efficient delivery of care and better tools can ameliorate the stress somewhat. If structural process and technology tools can improve productivity per employee, the long-term supply of clinicians may keep up. Additionally, a decreased demand for care resulting from an effective prevention strategy also could help.

Most other successful industries work hard to produce products or services with fewer people. Remember what the industrial revolution did for America by increasing the productivity of each person in the early 1900s. Thereafter, manufacturing needed fewer employees.

PATIENTS’ NEEDS AND DESIRES

Patients want to live a long, happy and healthy life. The best way to do this is to avoid illness, which patients can do with prevention because 80% of disease is self-inflicted. When prevention fails, or the 20% of unstoppable episodic illness kicks in, patients should seek the best care.

The choice of the “best care” should not necessarily rest just on convenience but rather objective outcomes. Closest to home may be important for take-out food, but not healthcare.

Care typically can be divided into three categories — acute, urgent, and elective. Common examples of acute care include childbirth, heart attack, stroke, major trauma, overdoses, ruptured major blood vessel, and similar immediate, life-threatening conditions. Urgent intervention examples include an acute abdomen, gall bladder inflammation, appendicitis, severe undiagnosed pain and other conditions that typically have positive outcomes even with a modest delay of a few hours.

Most every other condition can be cared for in an appropriate timeframe that allows for a car trip of a few hours. These illnesses can range in severity from benign that typically resolve on their own to serious, which are life-threatening if left undiagnosed and untreated. Musculoskeletal aches are benign while cancer is life-threatening if not identified and treated.

Getting the right diagnosis and treatment for both benign and malignant conditions is crucial but we’re not even near perfect for either. That’s unsettling.

In a 2017 study,

“Mayo Clinic reports that as many as 88 percent of those patients [who travel to Mayo] go home [after getting a second opinion] with a new or refined diagnosis — changing their care plan and potentially their lives. Conversely, only 12 percent receive confirmation that the original diagnosis was complete and correct. In 21 percent of the cases, the diagnosis was completely changed; and 66 percent of patients received a refined or redefined diagnosis. There were no significant differences between provider types [physician and non-physician caregivers].” [15]

The frequency of significant mis- or refined-diagnosis and treatment should send chills up your spine. With healthcare we are not talking about trivial concerns like a bad meal at a restaurant, we are discussing life-threatening risks. Making an initial, correct first decision has a tremendous influence on your outcome.

Sleeping in your own bed is nice but secondary to obtaining the best outcome possible, even if car or plane travel are necessary. For urgent and elective diagnosis/treatment, travel may be a

good option. Acute illness usually doesn’t permit a few hours of grace, although a surprising number of stroke and heart attack victims delay treatment through denial or overnight timing. But even most of these delayed, recognized illnesses usually survive. And urgent and elective care gives the patient the luxury of some time to get to a location that delivers proven, objective outcomes, not necessarily the one closest to home.

Measuring quality in healthcare has traditionally been difficult for the average patient. Roadside billboards, commercials, displays at major sporting events, fancy logos, name changes and image building campaigns do not relate to quality. Confusingly, some heavily advertised metrics rely on a combination of subjective reputational and lagging objective measures. Most consumers don’t know enough about the sources of information to understand which ratings are meaningful to outcomes.

Arguably, hospital quality star ratings created by the Centers for Medicare and Medicaid Services (CMS) are the best information for potential patients to rate hospital mortality, safety, readmission, patient experience, and timely/effective care. These five categories combine 47 of the more than 100 measures CMS publicly reports. [16]

A 2017 JAMA article by lead author Dr. Ashish Jha said:

“Found that a higher CMS star rating was associated with lower patient mortality and readmissions. It is reassuring that patients can use the star ratings in guiding their health care seeking decisions given that hospitals with more stars not only offer a better experience of care, but also have lower mortality and readmissions.”

The study included only Medicare patients who typically are over 65, and the differences were most apparent at the extremes, nevertheless,

“These findings should be encouraging for policymakers and consumers; choosing 5-star hospitals does not seem to lead to worse outcomes and in fact may be driving patients to better institutions.” [17]

Developing more 5-star hospitals is not only better and safer for patients but also will save resources by avoiding expensive complications and suffering.

As a patient, doing your homework before you have an urgent or elective need can change your outcome for the better. Driving a

couple of hours to a CMS 5-star hospital or flying to a specialty hospital for an elective procedure could make a difference.

Business case studies have noted that hospitals with a focus on a specific condition deliver improved outcomes while becoming more efficient. [18] Similarly, specialty surgical areas within general hospitals have also been effective in improving quality while reducing costs. Mayo Clinic demonstrated this with its cardiac surgery department. [19] A similar example is Shouldice Hospital near Toronto, a focused factory specializing in hernia repairs. In the last 75 years, the Shouldice team has completed four hundred thousand hernia repairs, mostly performed under local anesthesia with the patient walking to and from the operating room. [20] [21]

THE BOTTOM LINE

The Mayo Brother’s quote, “The patient’s needs come first,” is more relevant today than when first articulated over a century ago. Driving treatment into distinct categories of acute, urgent, and elective, with subsequent directing care to the appropriate facilities, improves the entire care process for the patient. The saved resources can fund prevention and decrease the need for future care. The healthcare industry’s focus has been on sickness,

not prevention. The virtuous cycle’s flywheel effect of distinct categories for care and embracing prevention of illness will decrease misery and lower the percentage of GDP devoted to healthcare.

Editor’s note: This is a multi-part series on reinventing the healthcare industry. Part 2 addresses physicians, non-physician caregivers, and communities’ responses to the coming transformation.

Walgreens’ growing U.S. healthcare segment is continuing to bolster the retail health chain’s financial performance. The business, which includes value-based provider VillageMD, recorded $1.6 billion in sales in the second quarter, an increase of $1.1 billion from last year.

VillageMD sales were up 30%, including a boost from its recent acquisition of medical group Summit Health. Specialty pharmacy Shields Health Solutions grew sales 41%, while at-home care provider CareCentrix’s sales were up 25%.

Thanks in part to a jump in revenue in its healthcare segment, Walgreens’ results beat Wall Street expectations even as profit declined more than 20% amid lower COVID-19 vaccine volumes and test sales, higher salary costs, opioid litigation charges and costs associated with its $3.5 billion investment in its Summit acquisition.

Dive Insight:

Walgreens has been working to expand its business scope beyond pharmacies to more consumer-centric healthcare, and has acquired a number of companies to build out its growing U.S. healthcare division.

In its earnings results for the second quarter ended Feb. 28, the business reported gross profit of $32 million, as income from Shields and CareCentrix was offset by VillageMD expansion costs. VillageMD added 133 clinics compared to the second quarter last year.

“With the closing of VillageMD’s acquisition of Summit Health, [Walgreens] is now one of the largest players in primary care,” CEO Roz Brewer said in the company’s earnings release on Tuesday.

VillageMD also acquired a Connecticut-based medical group in March for an undisclosed amount. That group, called Starling Physicians, operates more than 30 primary care and multi-specialty practices across the state.

Starling “will contribute heavily to revenue and EBITDA growth in the second half of 2023,” said Walgreens CFO James Kehoe on a Tuesday morning call with investors. “Overall, the primary care business and the specialty care business is doing really, really well.”

Despite the recent deals, Walgreens is moving beyond its peak investment period in healthcare, management said on the call. VillageMD, for example, plans to concentrate growth and investments in specific markets where it can be “hyper-relevant” moving forward, according to Walgreens President John Standley.

In healthcare, as in life, people devote a lot of time and attention to the way things should be. They’d be better off focusing on what actually could be.

As an example, 57% to 70% of American voters believe our nation “should” adopt a single-payer healthcare system like Medicare For All. Likewise, public health advocates insist that more of the nation’s $4 trillion healthcare budget “should” be spent on combating the social determinants of health: things like housing insecurity, low-wage jobs and other socioeconomic stresses. Neither of these ideas will happen, nor will dozens of positive healthcare solutions that “should” happen.

When the things that should happen don’t, there’s always a reason. In healthcare, the biggest roadblock to change is what I call the conglomerate of monopolies, which includes hospitals, drug companies, private-equity-staked physicians and commercial health insurers. These powerful entities exert monopolistic control over the delivery and financing of the country’s medical care. And they remain fiercely opposed to any change in healthcare that would limit their influence or income.

This article concludes my five-part series on medical monopolies with an explanation of why (a) “should” won’t happen in healthcare but (b) industrywide disruption will.

Why government won’t lead the way

With the U.S. Senate split 51-49 and with virtually no chance of either party securing the 60 votes needed to avoid a filibuster, Congress will, at most, tinker with the medical system. That means no Medicare For All and no radical redistribution of healthcare funds.

Even if elected officials started down the path of major reform, healthcare’s incumbents would lobby, threaten to withhold campaign contributions (which have exceeded $700 million annually for the past three years) and swat down any legislative effort that might harm their interests.

In American politics, money talks. That won’t change soon, even if voters believe it should.

American employers won’t lead, either

Private payers wield significant power and influence of their own. In fact, the Fortune 500 represents two-thirds of the U.S. GDP, generating more than $16 trillion in revenue. And they provide health insurance to more than half the American population.

With all that clout, you’d think business executives would demand more from healthcare’s conglomerate of monopolies. You might assume they’d want to push back against the prevailing “fee for service” payment model, replacing it with a form of reimbursement that rewards doctors and hospitals for the quality (not quantity) of care they provide. You’d think they would insist that employees get their care through technologically advanced, multispecialty medical groups, which deliver superior outcomes when compared to solo physician practices.

Instead, companies take a more passive position. In fact, employers are willing to shoulder 5% to 6% increases in insurance premiums each year (double their average rate of revenue growth) without putting up much or any resistance.

One reason they tolerate hefty rate hikes—rather than battling insurers, hospitals and doctors— involves a surprising truth about insurance premiums. Business leaders have figured out how to transfer much of their added premium costs to employees in the form of high-deductible health plans. A high deductible plan forces the beneficiary to pay “first dollar” for their medical care, which significantly reduces the premium cost paid by the employer.

Businesses also realize that high deductibles will only financially burden employees who experience an unexpected, catastrophic illness or accident. Meaning, most workers won’t feel the sting in a typical year. As for employees with ongoing, expensive medical problems, employers typically don’t mind watching them walk out the door over high out-of-pocket costs. Their departures only reduce the company’s medical spend in future years.

Finally, businesses know that employee medical costs are tax deductible, which cushions the impact of premium increases. So, what starts as a 6% annual increase ends up costing employees 3%, the government 1% and businesses only 2%. In today’s strong labor market, which boasts the lowest unemployment rate in 54 years, businesses are reluctant to demand changes from healthcare’s biggest players—regardless of whether they should.

Leading the healthcare transformation

If there were a job opening for “Leader of the American Healthcare Revolution,” the applicant pool would be shallow.

Elected officials would shy away, fearing the loss of campaign contributions. Businesses and top executives would pass on the opportunity, preferring to shift insurance costs to employees and the government. Patients would feel overwhelmed by the task and the power of the incumbents. Doctors, nurses and hospitals—despite their frustrations with the current system—would want to take small steps, fearful of the conglomerate of monopolies and the risks of disruptive change.

To revolutionize American medicine, a leader must possess three characteristics:

Sufficient size and financial reserves to disrupt the entire industry (not just a small piece of it).

Presence across the country to leverage economies of scale.

Willingness to accept the risks of radical change in exchange for the potential to generate massive profits.

Whoever leads the way won’t make these investments because it “should happen.” They will take the chance because the upside is dramatically better than sitting on the sidelines.

The likely winner: American retailers

Amazon, CVS, Walmart and other retail giants are the only entities that fit the revolutionary criteria above. In healthcare’s game of monopoly, they’re the ones willing to take high-stakes risks and capable of disrupting the industry.

For years, these retailers have been acquiring the necessary game pieces (including pharmacy services, health-insurance capabilities and innovative care-delivery organizations) to someday take over American healthcare.

CVS Health owns health insurer Aetna. It bought value-based care company Signify Health for $8 billion, along with national primary care provider OakStreet Health for $10.6 billion. Walmart recently entered into a 10-year partnership with the nation’s largest insurance company, UnitedHealth, gaining access to its 60,000 employed physicians. Walmart then acquired LHC, a massive home-health provider. Finally, Amazon recently purchased primary-care provider One Medical for $3.9 billion and maintains close ties with nearly all of the country’s self-funded businesses.

Harvard business professor Clay Christensen noted that disruptive change almost always comes from outsiders. That’s because incumbents cling to overly expensive and inefficient systems. The same holds true in American healthcare.

The retail giants can see that healthcare is exorbitantly priced, uncoordinated, inconvenient and technologically devoid. And they recognize the hundreds of billions of dollars of revenue and they could earn by offering a consumer-focused, highly efficient alternative.

How will the transformation happen?

Initially, I believe the retail giants will take a two-pronged approach. They’ll (a) continue to promote fee-for-service medical services through their pharmacies and retail clinics (in-store and virtual) while (b) embracing every opportunity to grow their market share in Medicare Advantage, the capitated option for people over age 65.

And within Medicare Advantage, they’ll look for ways to leverage sophisticated IT systems and economies of scale, thus providing care that is better coordinated, technologically supported and lower cost than what’s available now.

Rather than including all community doctors in their network, they’ll rely on their own clinicians, augmented by a limited cohort of the highest-performing medical groups in the area. And rather than including every hospital as an inpatient option, they’ll contract with highly respected centers of excellence for procedures like heart surgery, neurosurgery, total-joint replacement and transplants, trading high volume for low prices.

Over time, they’ll reach out to self-funded businesses to offer proven, superior clinical outcomes, plus guaranteed, lower total costs. Then they’ll make a capitated model their preferred insurance plan for all companies and individuals. Along the way, they’ll apply consumer-driven medical technologies, including next generations of ChatGPT, to empower patients, provide continuous care for people with chronic diseases and ensure the medical care provided is safe and most efficacious.

Tommy Lasorda, the long-time manager of the Los Angeles Dodgers, once remarked, “There are three types of people. Those who watch what happens, those that make it happen and those who wonder what just happened.”

Lasorda’s quip describes healthcare today. The incumbents are watching closely but failing to see the big picture as retailer acquire medical groups and home health capabilities. The retail giants are making big moves, assembling the pieces needed to completely transform American medicine as we think of it today. Finally, tens of thousands of clinicians and thousands of hospital administrators are either ignoring or underestimating the retail giants. And, when they get left behind, they’ll wonder: What just happened?

The conglomerate of monopolies rule medicine today. Amazon, CVS and Walmart believe they should rule. And if I had to bet on who will win, I’d put my money on the retail giants.

We’ve updated our annual comparison of the relative size of the largest healthcare companies, with the graphic below comparing 2022 revenues to 2019 for a sense of how different companies and industry sectors weathered the pandemic.

The annual revenues of the five largest health systems in 2022 pale in comparison to the industry’s true giants—and the gap only widened over the pandemic. The largest health systems averaged just 5 percent annual growth since 2019, while the largest companies in each other healthcare subsector have grown revenues by over 10 percent annually.

Unsurprisingly, the pandemic drove Pfizer’s revenue to a record $100B in 2022—over half of that was driven by the company’s COVID vaccine and antiviral treatment, Paxlovid. Amazon’s 2022 revenue was nearly double its pre-COVID level. While very little of that growth came from healthcare, it enabled the company to fund investments like its all-cash $3.9B purchase of One Medical, which closed this week.

Even the nation’s largest health systems cannot compete with that kind of firepower, and looking beyond revenue paints an even more difficult picture. According to Kaufman Hall, although the median hospital has grown its revenue by 15 percent, it has seen expenses climb 20 percent, and lost 26 percent of margin since 2019.

CVS Health is close to a deal to acquire primary care provider Oak Street Health for around $10.5 billion, including debt, marking the latest move among major healthcare stakeholders in acquiring primary care companies, the Wall Street Journal reports.

According to people with knowledge of the matter who spoke to the Journal, the two companies are discussing a deal in which CVS would acquire Oak Street for a price of around $39 a share. If the deal goes through, it could be announced as soon as this week.

According to the Journal, “the Oak Street acquisition would further the company’s long-term shift to broaden into businesses beyond retail pharmacy by adding doctors who can more fully manage patients’ care.”

Oak Street has more than 160 centers across 21 states and focuses mainly on caring for patients enrolled in Medicare. The company, which is based in Chicago, was founded in 2012 and specializes in caring for patients under value-based care arrangements.

Aetna, which is owned by CVS, has a growing Medicare Advantage business that would likely tie in with Oak Street’s clinics, which care for about 159,000 patients under value-based arrangements, the Journal reports.

The move is the latest among major healthcare stakeholders acquiring primary care companies. In September 2022, CVS announced an $8 billion deal to acquire home healthcare company Signify Health.

Meanwhile, Amazon in July 2022 announced a $3.9 billion deal to acquire primary care company One Medical, Humana in September 2022 announced its intention to spend up to $550 million to purchase 20 CenterWell Senior Primary Care clinics, and Walgreens Boots Alliance in November 2022 announced a roughly $9 billion deal to acquire Summit Health.

On Tuesday, Amazon unveiled its latest healthcare offering, RxPass, which will deliver generic prescription drugs to Prime members who pay an additional flat $5 monthly surcharge. The service, which currently covers 53 medications for common conditions, requires consumers to pay out-of-pocket rather than through insurance, but does not limit the number of drugs a subscriber can receive for the flat monthly fee.

RxPass is not yet able to ship medications to eight states, including (notably) California, Texas, and Pennsylvania.

The Gist:Paying $60 a year to avoid the hassle of going to a pharmacy or dealing with another mail-order delivery program will be a very attractive offer for many of the 168M US-based Amazon Prime subscribers, as much for the convenience as for the potential cost savings.

But the concept isn’t novel. Case in point: Walmart continues to offer its $4 generic drug program, launched in 2006. Given that the average Prime member is 37 years old, Amazon’s flat-fee service offering will target a younger demographic with fewer medication needs—and complement the service offered by PillPack, acquired in 2018, which is built for older customers on multiple medications. An evolutionary, not revolutionary, step in Amazon’s ongoing moves into healthcare.

Under new guidance released by the Food and Drug Administration (FDA) on Tuesday, retail pharmacies can now dispense mifepristone, the first in a two-drug sequence for medication abortions. This move follows a December 2021 change that allows mail-order pharmacies to ship prescribed mifepristone, which previously could only be dispensed in-person by approved clinics. The medication will still require a prescription, and will remain highly restricted, or even illegal, in states that have implemented strict abortion bans.

Pharmacies opting to dispense the drug will face requirements that go beyond other medications, such as keeping the identity of the prescribing provider anonymous. Retail pharmacy chains CVS and Walgreens each announced plans to become certified to dispense mifepristone in locations where it is legal.

The Gist:Abortion pills, currently used in used in more than half of pregnancy terminations, are becoming more sought-after in the wake of last year’s Supreme Court ruling overturning the federal right to abortion. This FDA action is the latest move by the Biden administration to expand access to abortion—though its impact will be felt unevenly across states, even with the Department of Justice stating the Postal Service can legally deliver the medications anywhere in the US.

VillageMD, which is majority owned by Walgreens Boots Alliance, plans to shell out nearly $9 billion to pick up medical practice Summit Health, the parent company of urgent care clinic chain CityMD.

The deal, announced Monday morning, is valued at $8.9 billion and includes investments from Walgreens Boots Alliance and Cigna Corp’s healthcare unit Evernorth, which will also become a minority owner in VillageMD. Bloomberg first reported on a potential deal back in late October.

The deal will expand Walgreen’s reach into primary, specialty and urgent care. The transaction creates one of the largest independent provider groups in the U.S., the organizations said. Combined, VillageMD and Summit Health will operate more than 680 provider locations in 26 markets. The two companies will have 20,000 employees.

Walgreens said Monday it will invest $3.5 billion through an even mix of debt and equity to support the acquisition, which is expected to close in the first quarter of 2023. The company will remain the largest and consolidating shareholder of VillageMD with about 53% stake.

Walgreens also raised its fiscal year 2025 sales goal for its U.S. healthcare business to between $14.5 billion and $16 billion from $11 billion to $12 billion previously. That business segment is now expected to achieve positive adjusted EBITDA by the end of fiscal year 2023.

Last year, Walgreens invested $5.2 billion in VillageMD and said it planned to open at least 600 Village Medical at Walgreens primary-care practices across the country by 2025 and 1,000 by 2027.

The deal comes amid a frenzy of M&A activity in the past two years. Major retailers like CVS, Walgreens and Amazon are ramping up their focus on providing medical services to gain bigger footholds in the healthcare market.

Drugstore rival CVS Health won the bidding war for home health and technology services company Signify Health and plans to shell out $8 billion to acquire the company. Amazon also plans to buy primary care provider One Medical for $3.9 billion.

The M&A move signals that Walgreens wants to become a “dominant entity in the overall healthcare services ecosystem,” according to David Larsen, healthcare IT and digital health analyst at financial services firm BTIG.

“Walgreens Boots Alliance is graduating up from being a drug retail store to owning the life-cycle of members’ health,” he wrote in an analyst’s note. “We view this transaction as being a statement by the market that primary care continues to be one of the key drivers of healthcare long-term.”

The deal also will put additional pressure on CVS Health to break into the primary care business “sooner rather than later,” Larsen wrote.

“I think at the most strategic level, I think there continues to be recognition that an integrated, coordinated, connected model of care is one that will ultimately deliver the best results. You see this through Optum’s acquisition of Kelsey-Seybold Clinic and VillageMD’s acquisition of Summit Health,” Tim Barry, CEO and chair of VillageMD, said in an interview with Fierce Healthcare.

“If we’re going to ultimately stem the rising tide of this fee-for-service healthcare system, we need a better solution, and that solution needs to have doctors working with other doctors in a coordinated way and trying to solve the unique problems that these patients have and making sure that the right doctors are accessing the patient at the right time, and doing it all underneath the umbrella of a risk-based contract,” Barry said.

He added, “We think that this is going to continue to be where healthcare goes. And, we have to do it in a way that is integrated and value-oriented. Any organization focused on doing that, and doing that at size and scale, is going to continue, I think, to be the successful winners of our healthcare system.”

In 2019, Summit Medical Group, a physician-owned and governed multispecialty group, merged with CityMD, a leading urgent care company in New York City. The combined organization, Summit Health, has more than 370 locations in New Jersey, New York, Connecticut, Pennsylvania and Oregon.

VillageMD provides value-based primary care for patients at traditional free-standing practices, Village Medical at Walgreens practices, at home and via virtual visits. VillageMD and Village Medical have grown to 22 markets and are responsible for more than 1.6 million patients, according to the company.

Barry said the combination of VillageMD and Summit Health-CityMD will enable the organizations to scale up value-based care and build out integrated primary and specialty care services.

“If you look at the long history of Summit Health, it’s an organization that has done some very innovative things. The way that they deliver multispecialty care, it is truly integrated, it’s truly connected and they are known as the preeminent brand in their marketplace. They also have CityMD, which is one of the more unique and differentiated urgent care models out there in the market. They really are a best-of-breed organization,” he said.

“When I look at what we’ve been able to do at VillageMD, we built this incredible model of value-based primary care delivery. The idea of bringing these two organizations together to bring those best-of-breed capabilities under one umbrella was just so compelling. We will soon be able to offer a more comprehensive, integrated and connected model by also offering other specialty services to our patients, but all still done through a value or risk-based reimbursement structure.”

Barry is bullish on the combined capabilities of the two companies in the primary and specialty care markets.

“We’ll be delivering a consistent value-based model of integrated, multispecialty care in a way that delivers the best clinical results on the planet,” he said.

Jeff Alter, CEO of Summit Health-CityMD, said in a statement that the deal adds Summit Health’s expertise and geographic coverage to VillageMD’s proven value-based primary care approach.

The acquisition also expands Walgreens’ reach into providing medical care directly to patients. “This transaction accelerates growth opportunities through a strong market footprint and wide network of providers and patients across primary, specialty and urgent care,” Roz Brewer, CEO of Walgreens Boots Alliance, said in a statement.

With Cigna’s investment, the combined company will be able to tap into Evernorth’s health services capabilities to potentially lower healthcare costs, Barry said. Evernorth encompasses Cigna’s health services businesses including pharmacy benefit manager Express Scripts

“In order to be a risk-based provider or a value-based provider, you have to have contracts with a payer that allows you to work in this value or risk-based construct. We learned over the years that Cigna has been a really good partner to us on that journey,” Barry said.

“There are companies that [Cigna] has purchased over the years that have different specializations and capabilities that we believe ultimately will allow us to deliver better care to our patients,” he noted. “Evernorth has some capabilities tied to behavioral health, and they have some capabilities tied to the management of specialty pharmaceutical spend, which everyone knows those costs continue to be soaring. We both liked the idea of supporting an organization like ours that’s going to continue to grow and continues to be focused on risk and value.”

With the investment in VillageMD and Summit Health, Cigna gets a leg up in the primary care space as it looks to build out its Evernorth division.

“Our collaboration with VillageMD accelerates our efforts to improve the way care is accessed and delivered,” said Eric Palmer, CEO of Evernorth, in a statement. “Harnessing the breadth of Evernorth’s health services capabilities and connecting them with physicians who provide care in a value-based model like VillageMD, helps more people to get the right care at the right time—driving better health and value.”

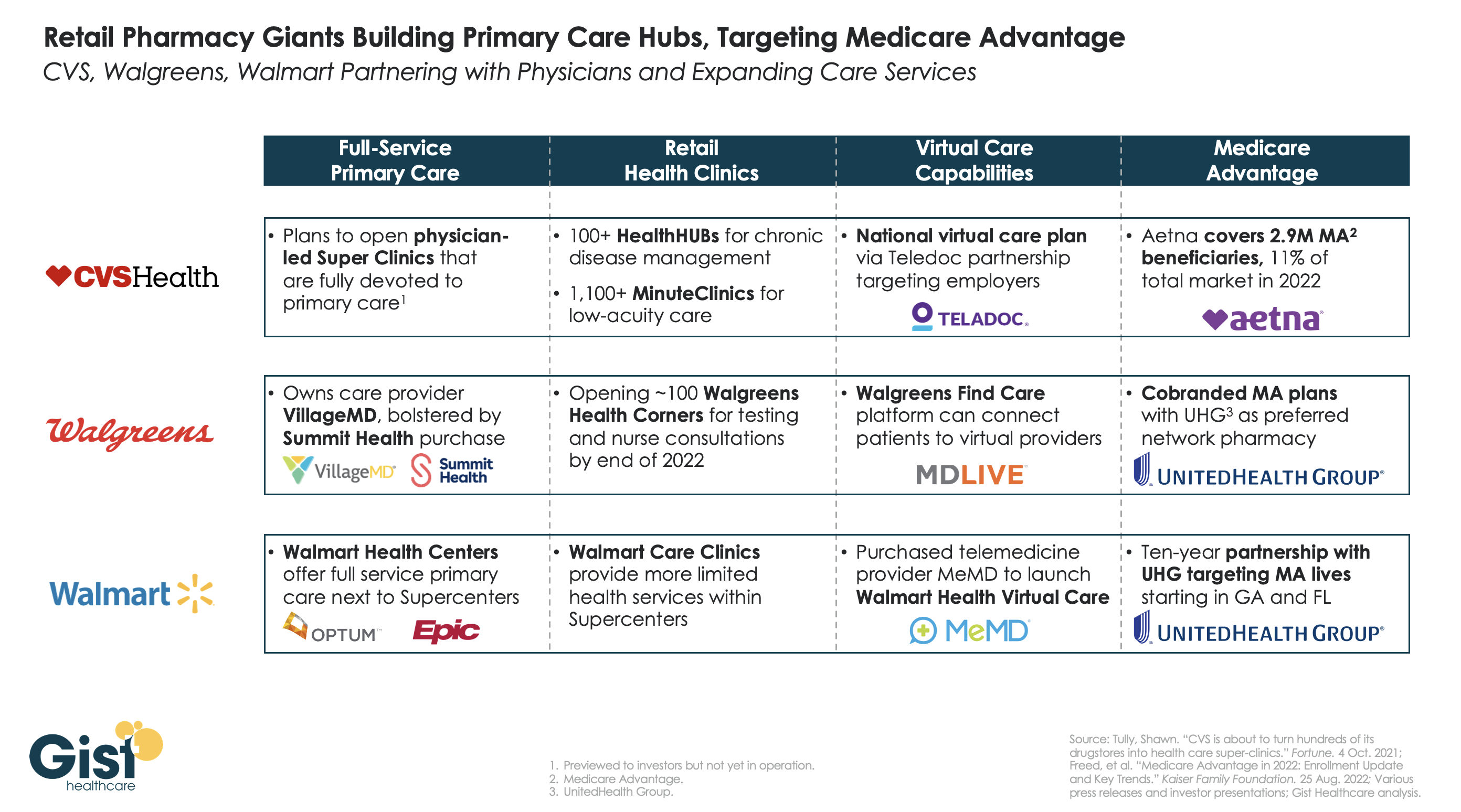

Retailers and insurers are building out their primary care strategies in a bid to become the new front door for patients seeking healthcare services, especially seniors on highly profitable Medicare Advantage (MA) plans. In the graphic above, we examine the capabilities of three of the largest pharmacy chains—CVS Health, Walgreens, and Walmart—to deliver full-service primary care across in-person and virtual settings.

CVS pioneered the pivot to care provision in 2006 with its acquisition of MinuteClinic, which now has over 1,000 locations. The company has further expanded its concept of pairing retail and pharmacy services with primary care by opening over 100 HealthHUBs, which provide an expanded slate of care services. However, CVS lags competitors in the rollout of full-service primary care practices, with its proposed physician-led Super Clinics still stuck in the planning stages.

Walgreens, with its majority stake in VillageMD (on track for 200 co-branded practices by the end of the year) and the recent acquisition of Summit Health (which operates another 370 primary and urgent care clinics) has assembled the most impressive primary care footprint of the three companies.

Walmart, the largest by number of stores but also the newest to healthcare, has opened more than 25 Walmart Health Centers, a step up from earlier experimentation with in-store care clinics, offering more services and partnering with Epic Systems to integrate electronic health records.

CVS’s key advantage over its competitors comes from its payer business, having acquired Aetna in 2018, now the fourth-largest MA payer by membership. Walgreens and Walmart have both aligned themselves with UnitedHealth Group (UHG) to participate in MA, with Walmart having struck a ten-year partnership to steer UHG MA beneficiaries to Walmart Health Centers in Florida and Georgia.

While aligning with UHG expands the reach of these retail giants into MA risk, UHG, whose OptumHealth division is by far the largest employer of physicians nationwide, remains the healthcare juggernaut most poised to unseat incumbent providers as the home for consumers’ healthcare needs.