With input from stakeholders across the industry, Modern Healthcare outlines six challenges health care is likely to face in 2023—and what leaders can do about them.

1. Financial difficulties

In 2023, health systems will likely continue to face financial difficulties due to ongoing staffing problems, reduced patient volumes, and rising inflation.

According to Tina Wheeler, U.S. health care leader at Deloitte, hospitals can expect wage growth to continue to increase even as they try to contain labor costs. They can also expect expenses, including for supplies and pharmaceuticals, to remain elevated.

Health systems are also no longer able to rely on federal Covid-19 relief funding to offset some of these rising costs. Cuts to Medicare reimbursement rates could also negatively impact revenue.

“You’re going to have all these forces that are counterproductive that you’re going to have to navigate,” Wheeler said.

In addition, Erik Swanson, SVP of data and analytics at Kaufman Hall, said the continued shift to outpatient care will likely affect hospitals’ profit margins.

“The reality is … those sites of care in many cases tend to be lower-cost ways of delivering care, so ultimately it could be beneficial to health systems as a whole, but only for those systems that are able to offer those services and have that footprint,” he said.

2. Health system mergers

Although hospital transactions have slowed in the last few years, market watchers say mergers are expected to rebound as health systems aim to spread their growing expenses over larger organizations and increase their bargaining leverage with insurers.

“There is going to be some organizational soul-searching for some health systems that might force them to affiliate, even though they prefer not to,” said Patrick Cross, a partner at Faegre Drinker Biddle & Reath. “Health systems are soliciting partners, not because they are on the verge of bankruptcy, but because they are looking at their crystal ball and not seeing an easy road ahead.”

Financial challenges may also lead more physician practices to join health systems, private-equity groups, larger practices, or insurance companies.

“Many independent physicians are really struggling with their ability to maintain their independence,” said Joshua Kaye, chair of U.S. health care practice at DLA Piper. “There will be a fair amount of deal activity. The question will be more about the size and specialty of the practices that will be part of the next consolidation wave.”

3. Recruiting and retaining staff

According to data from Fitch Ratings, health care job openings reached an all-time high of 9.2% in September 2022—more than double the average rate of 4.2% between 2010 and 2019. With this trend likely to continue, organizations will need to find effective ways to recruit and retain workers.

Currently, some organizations are upgrading their processes and technology to hire people more quickly. They are also creating service-level agreements between recruiting and hiring teams to ensure interviews are scheduled within 48 hours or decisions are made within 24 hours.

Eric Burch, executive principal of operations and workforce services at Vizient, also predicted that there will be a continued need for contract labors, so health systems will need to consider travel nurses in their staffing plans.

“It’s really important to approach contract labor vendors as a strategic partner,” Burch said. “So when you need the staff, it’s a partnership and they’re able to help you get to your goals, versus suddenly reaching out to them and they don’t know your needs when you’re in crisis.”

When it comes to retention, Tochi Iroku-Malize, president of the American Academy of Family Physicians (AAFP), said health systems are adequately compensated for their work and have enough staff to alleviate potential burnout.

AAFP also supports legislation to streamline prior authorization in the Medicare Advantage program and avoid additional cuts to Medicare payments, which will help physicians provide care to patients with less stress.

4. Payer-provider contract disputes

A potential recession, along with the ensuing job cuts that typically follow, would limit insurers’ commercial business, which is their most profitable product line. Instead, many people who lose their jobs will likely sign up for Medicaid plans, which is much less profitable.

Because of increased labor, supply, and infrastructure costs, Brad Ellis, senior director at Fitch Ratings, said providers could pressure insurers into increasing the amount they pay for services. This will lead insurers to passing these increased costs onto members’ premiums.

Currently, Ellis said insurers are keeping an eye on how legislators finalize rules to implement the No Surprise Act’s independent resolution process. Regulators will also begin issuing fines for payers who are not in compliance with the law’s price transparency requirement.

5. Investment in digital health

Much like 2022, investment in digital health is likely to remain strong but subdued in 2023.

“You’ll continue to see layoffs, and startup funding is going to be hard to come by,” said Russell Glass, CEO of Headspace Health.

However, investors and health care leaders say they expect a strong market for digital health technology, such as tools for revenue cycle management and hospital-at-home programs.

According to Julian Pham, founding and managing partner at Third Culture Capital, he expects corporations such as CVS Health to continue to invest in health tech companies and for there to be more digital health mergers and acquisitions overall.

In addition, he predicted that investors, pharmaceutical companies, and insurers will show more interest in digital therapeutics, which are software applications prescribed by clinicians.

“As a physician, I’ve always dreamed of a future where I could prescribe an app,” Pham said. “Is it the right time? Time will tell. A lot needs to happen in digital therapeutics and it’s going to be hard.”

6. Health equity efforts

This year, CMS will continue rolling out new health equity initiatives and quality measurements for providers and insurers who serve marketplace, Medicare, and Medicaid beneficiaries. Some new quality measures include maternal health, opioid related adverse events, and social need/risk factor screenings.

CMS, the Joint Commission, and the National Committee for Quality Assurance are also partnering together to establish standards for health equity and data collection.

In addition, HHS is slated to restore a rule under the Affordable Care Act that prohibits discrimination based on a person’s gender identity or sexual orientation. According to experts, this rule may conflict with recently passed state laws that ban gender-affirming care for minors.

“It’s something that’s going to bear out in the courts and will likely lack clarity. We’ll see differences in what different courts decide,” said Lindsey Dawson, associate director of HIV policy and director of LGBTQ health policy at the Kaiser Family Foundation. “The Supreme Court acknowledged that there was this tension. So it’s an important place to watch and understand better moving forward.”

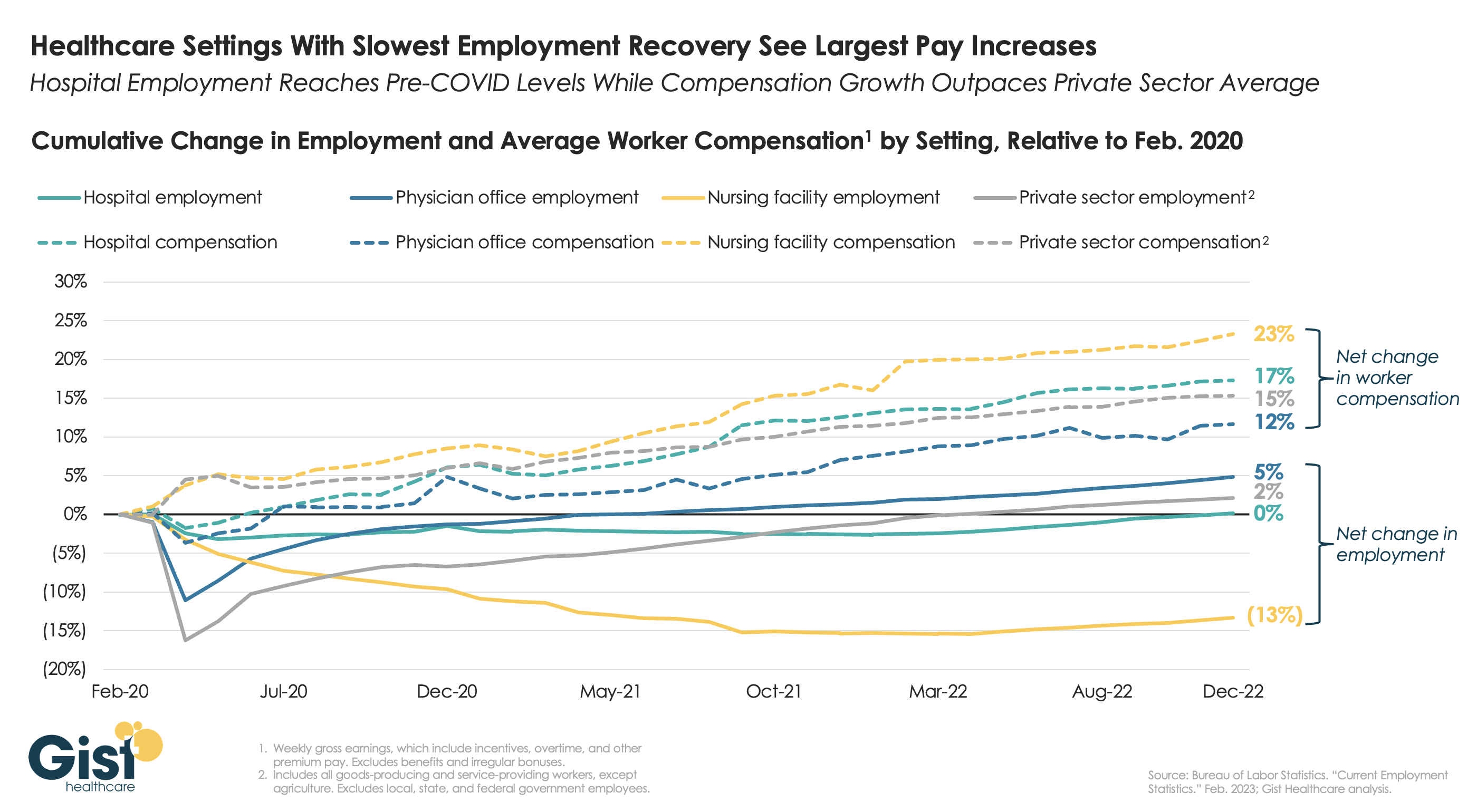

The healthcare sector has been navigating an intransigent staffing crisis since the widespread layoffs during the first few months of COVID. The graphic above uses Bureau of Labor Statistics data to illustrate the impact of this labor shock on both total employment and employee compensation.

Across key healthcare settings, workplaces with the slowest recovery of total workers have seen the largest increases in employee earnings.Hospital employment largely tracked with the rest of the private sector; however, hospitals raised employee compensation by two percent more than the private sector, while recovering two percent fewer jobs.

It is important to note that the relationship between employment levels and employee compensation is not causal, as evidenced by the ongoing labor shortages in nursing facilities, despite boosting average pay over 20 percent. Rather, the data suggest that, for as long as the tight labor market persists,pay raises alone are not sufficient to recruit and retain talent. Plus, while inflation may be abating, it has still outpaced earnings growth since December 2021.

Given that many healthcare workers saw pay bumps early in the pandemic, some are left still feeling underpaid, even if their compensation over the past three years has more than kept pace with inflation.

CFOs are planning to increase their compensation spend in 2023, with 86% of finance chiefs noting they plan to raise it by at least 3% year-over-year, according to a recent survey by Gartner.

CFOs are still facing a tight labor market in 2023. As CFOs weigh increased turnover and a more remote workforce, “they’re thinking through, how do they use compensation as a lever to engage and retain talent across their workforce,” said Alexander Bant, chief of research in the Gartner finance practice.

Only 5% of the 279 CFOs surveyed stated they planned to reduce their compensation spend in 2023, according to Gartner.

Dive Insight:

While CFOs typically budget more for compensation every year, ongoing inflationary pressures and a still-tight labor market puts compensation plans “front and center” in CFOs’ “ability to engage and retain top talent,” Bant said in an interview.

However, this does not mean finance chiefs will be budgeting for sweeping pay raises across their entire workforce — CFOs are “not trying to keep up with inflation across the board,” Bant said.

Rather, they are working with other members of the C-Suite such as the chief human resource officer and using tools like advanced analytics to single out and reward top performers which might be at more risk of departing for other opportunities, he said.

“CFOs are being more deliberate about how they allocate that money,” Bant said.

While the pace of wage growth slowed in the fourth quarter of 2022, according to recent data from the Labor Department, tamping down fears of a wage-price spiral, the war on talent remains a top worry for finance chiefs. Raising compensation can allow companies to be more competitive in the face of ongoing talent shortages, especially as workforce needs change.

For those companies which are moving employees back into the office, for example, raising compensation can help them to better compete against the remote or hybrid work opportunities which are becoming increasingly common, for example, Bant said.

Upping compensation can also help firms to find or hold onto employees with the key skills they need in areas such as digital transformation. Despite cost pressures, 43% of finance chiefs said they plan to increase their companies’ technology spend by 10%or more, according to the Gartner survey.

“What we’re hearing is, ’Yes, we are right-sizing parts of our organization and reducing head count in certain areas, but at the same time, we still have open roles and we’re still searching for talent in those areas that align to our digital transformation priorities,” Bant said of the search for technology talent.

Such skills still come at a premium, for that matter, despite the recent spat of layoffs across high-profile tech companies such as Google parent Alphabet, IBM and Microsoft. While these companies have reduced staff, they may not be letting go of employees with critical hardcore coding, data analytics or artificial intelligence related skills, Bant said.

“There is more talent available from technology companies, but that doesn’t mean that talent necessarily has the technical skills to drive the digital transformations that many CFOs and their leadership teams need,” he said.

The shortage of accountants is one of the main concerns keeping KPMG’s Greg Engel up at night. The firm is teaming up with universities to expand the talent pool.

KPMG’s Greg Engel likens the accounting profession to the turtle in the proverbial race with the hare — a turtle that’s seeking to pull ahead even as it competes with flashier industry sectors for workers.

The shortage of accounting talent is one of the main concerns keeping Engel — vice chair of tax in the U.S. for the Big Four accounting firm — up at night as he assesses the new year’s challenges, even as KPMG has undertaken numerous initiatives to ease the talent crunch.

At the same time, he sees a potential silver lining for his sector in the recent surge of layoffs in the formerly sizzling tech sector that has won over some college graduates who might have otherwise gone into accounting.

“A lot of people went to the technology sector because it was exciting. But now that Meta and Twitter and all these other companies are laying off people, kids going into college might go, ‘wait a minute, maybe KPMG sounds a little better than Twitter,’” Engel said in an interview. “Accounting is that boring, stable profession that doesn’t do as well in hugely expansive economies but does great when the economy’s on the downslide.”

Making accounting’s case

Historically, the Big Four accounting and consulting firms have mounted robust programs designed to recruit and train accounting students right out of colleges and major universities.

KPMG, along with PwC, Ernst & Young and Deloitte, hire thousands of graduates and students each year out of colleges, often training them through internships which lead to full-time jobs. Many of the certified public accountants go on to be controllers, tax directors and even CFOs. The entry level accounting salary range at such programs in the tax area can be roughly in the $70,000 to $80,000 range, depending on the market, according to some industry estimates.

“The hallmark of the Big Four was to train people really, really well,” Engel said. The longer employees stay at a firm, the better their prospects after they leave, Engel said.

That means an employee who leaves after a couple years could probably join a company’s accounting department at a lower level, he said. But if the employee leaves after rising to the level of senior manager, he or she could join the same company as controller — and those who leave as a partner might join as a CFO, Engel said.

CFO machine showing signs of wear

But the machine generating CPAs and CFOs has shown signs of wear in recent years. For one thing, KPMG has not been immune to the Great Resignation. It was hit by the surge in turnover that weakened the middle ladder rungs of its workforce. “There’s a kind of battle in the middle,” Engel said. The company responded in part by hiring experienced accountants from companies like Apple and Home Depot, he said.

At the same time, accounting has attracted fewer students in recent years. The total number of U.S. students completing a Bachelor’s degree in accounting fell about 8% in the 2019-2020 school year compared with the 2011-2012 period, shrinking to 52,481 graduates from 57,482, according to a 2021 report from the American Institute of Certified Public Accountants.

Priming the pipeline

Firms and accounting organizations have been taking deliberative steps in recent years to boost their case with talent and solve the talent shortage. For instance, the AICPA and the Department of Labor announced in November that they had teamed up to cultivate candidates and expand the pool of professionals, CFO Dive reported.

If students are not deterred by the accounting profession’s long hours and subdued reputation, they may feel reluctant to put in the credit hours required before taking the exam to become a Certified Public Accountant. That typically means a student will need more study beyond that of a four-year degree.

In an effort to make the extra course work pay off, KPMG worked with a number of universities to develop a Master in Accounting and Data Analytics Program that gives students the data analysis skills that are increasingly important in the field.

Recently, an additional seven universities were added to the program and KPMG has pledged to provide more than $7 million in scholarships. The schools added to the program included some historically Black Colleges and Universities such as Howard University School of Business and North Carolina Agricultural and Technical State University. Other universities that offer the program include Villanova University and The Ohio State University.

Separately, KPMG has teamed up with Engel’s alma mater, the University of Northern Iowa in Cedar Falls, Iowa, to help strengthen the accounting program and opportunities for students attending Des Moines Area Community College.

The company will also aim to provide internships to the students who often attend school at night or part-time, which can make it difficult to obtain the credit hours needed to become a CPA.

“We’re going to start adding people to the profession with two-year associates degrees,” Engel said, noting that similar programs are cropping up elsewhere. “We’ll give them a pathway to add the extra courses and programs they need.”

It covers 589,901 healthcare workers and 166,087 registered nurses from 272 facilities and 32 states. Participants were asked to report data on turnover, retention, vacancy rates, recruitment metrics and staffing strategies from January to December 2021.

The survey found a wide range of helpful figures for understanding the financial fallout of one of healthcare’s hardest labor disruptions:

The average hospital lost $7.1 million in 2021 to higher turnover rates.

The average hospital loses $5.2 to $9 million on RN turnover yearly.

The average turnover cost for a staff RN is $46,100, up more than 15 percent from the 2020 average.

The average hospital can save $262,300 per year for each percentage point it drops from its RN turnover rate.

To improve margins, hospitals need to control labor costs by decreasing dependence on travel and agency staff, but only 22.7 percent anticipate being able to do so.

For every 20 travel RNs eliminated, a hospital can save $4.2 million on average.

In the past 5 years, the average hospital turned over 100.5 percent of its workforce:

In 2021, hospitals set a goal of reducing turnover by 4.8 percent. Instead, it increased 6.4 percent and ranged from 5.1 percent to 40.8 percent. The current average hospital turnover rate nationally is 25.9 percent, according to the report.

While 72.6 percent of hospitals have a formal nurse retention strategy, less than half of those (44.5 percent) have a measurable goal.

Overall, 55.5 percent of hospitals do not have a measurable nurse retention goal.

Retirement is the number four reason staff RNs leave, and it is expected to remain a primary driver through 2030. More than half (52.8 percent) of hospitals today have a strategy to retain senior nurses. In 2018, only 21.6 percent had one.

Historically, RN turnover has trended below the hospital average across all staff. For the first time since conducting the survey, this is no longer true:

In the past five years, the average hospital turned over 95.7 percent of its RN workforce.

Close to a third (31.0 percent) of all newly hired RNs left within a year, with first year turnover accounting for 27.7 percent of all RN separations. Given the projected surge in retirements, expect to see the more tenured groups edge up creating an inverted bell curve.

Operating room RNs continue to be the toughest to recruit, while labor and delivery RNs are trending easier to recruit than in the year prior.

Hospitals are experiencing a dramatically higher RN vacancy rate (17 percent) compared to last year’s rate of 9.9 percent.

The vast majority (81.3 percent) reported a vacancy rate higher than 10 percent.

Healthcare added almost 45,000 jobs in November, but many hospitals and health systems will continue to struggle to meet staffing needs, retain top executives and providers, and foster long-term pipelines for talent, Ted Chien, president and CEO of independent consulting firm SullivanCotter, wrote in a Dec. 15 article for Nasdaq.

Hospitals and health systems are living “paycheck to paycheck” and unable to make long-term investments at the height of the current workforce crisis, Mr. Chien said.

The challenge boils down to a healthcare delivery problem, not a demand problem.

Baby Boomers are the greatest source of care demand on the healthcare system, but are unable to contribute to the provider workforce in the numbers needed to achieve balance, according to Mr. Chien. To compound that issue, burnout is a major factor why “too many” frontline workers have left or plan to exit healthcare, he said.

Last year, an estimated 333,942 healthcare providers dropped out of the workforce, including about 53,000 nurse practitioners, which has led hospitals to spend more on contract labor and feeling more pressure to consolidate, according to an October report published by Definitive Healthcare.

Long term, a continued lack of healthcare workers would force hospitals to operate in a heightened crisis mode, according to Mr. Chien, depriving non-critical patients of sufficient health prevention and demanding too much of providers who are already overly taxed.

Mr. Chien highlighted three key areas to tackle the workforce crisis: smarter technology, resilient teams and excellent leadership.

Technologies that alleviate providers’ administrative burdens will be critical to reduce burnout and keep caregivers focused on patient care, while smarter tech can also forge pipelines for future providers by streamlining clinical experience operations and aligning student placements with existing opportunities.

Building resilient teams begins with competitive pay and robust benefit packages, which fosters trust and demonstrates that a hospital values its staff, according to Mr. Chen. Supporting career growth, including upskilling and redeploying staff when appropriate, empowers employees.

Lastly, capable executive leadership teams, under intense scrutiny from industry stakeholders, must clearly outline their hospital or health system’s strategy and provide the change needed to support their staff. Lack of trust in leaders drives staff out of healthcare, so it is crucial to recruit and retain “modern, strategic thinkers with depth of experience who are prepared to lead,” Mr. Chien wrote.

The majority of hospitals are predicted to have negative margins in 2022, marking the worst year financially for hospitals since the beginning of the Covid-19 pandemic.

In Part 1 of Radio Advisory’s Hospital of the Future series, host Rachel (Rae) Woods invites Advisory Board experts Monica Westhead, Colin Gelbaugh, and Aaron Mauck to discuss why factors like workforce shortages, post-acute financial instability, and growing competition are contributing to this troubling financial landscape and how hospitals are tackling these problems.

As we emerge from the global pandemic, health care is restructuring. What decisions should you be making, and what do you need to know to make them? Explore the state of the health care industry and its outlook for next year by visiting advisory.com/HealthCare2023.