Headlines recently blared about the new review that looked at how effective masks are at preventing the transmission of flu-like disease. Cochrane reviews are well respected, and the media coverage about the recent review has been hard to parse. So is that it, end of story on masks? Not if you skip the media headlines and read the actual review!

One of the most persistent economic narratives of 2021 and 2022 was that of missing workers. Many Americans seemed to have simply vanished from the labor force during the pandemic, leaving employers in a lurch.

That’s no longer the case, White House economists argue in a new post presenting evidence that labor supply has returned to its pre-pandemic trend.

Why it matters:

It would be way less painful if the U.S. labor market were to come into a better, non-inflationary balance because labor supply increased, rather than labor demand decreased.

And contrary to a widespread economic narrative of the last couple of years, that seems to be happening — as the Biden team seeks to emphasize.

State of play:

There has been ample speculation about why labor supply was depressed in the aftermath of the pandemic, the White House Council of Economic Advisers notes.

Maybe fear of COVID, or long COVID symptoms, kept people out of work. Maybe it was excess savings from the pandemic, or reassessment of life priorities, or a “collective loss of work ethic.”

Nah. It increasingly looks as if it just took some time for potential workers to match up with jobs and return to the labor force.

By the numbers:

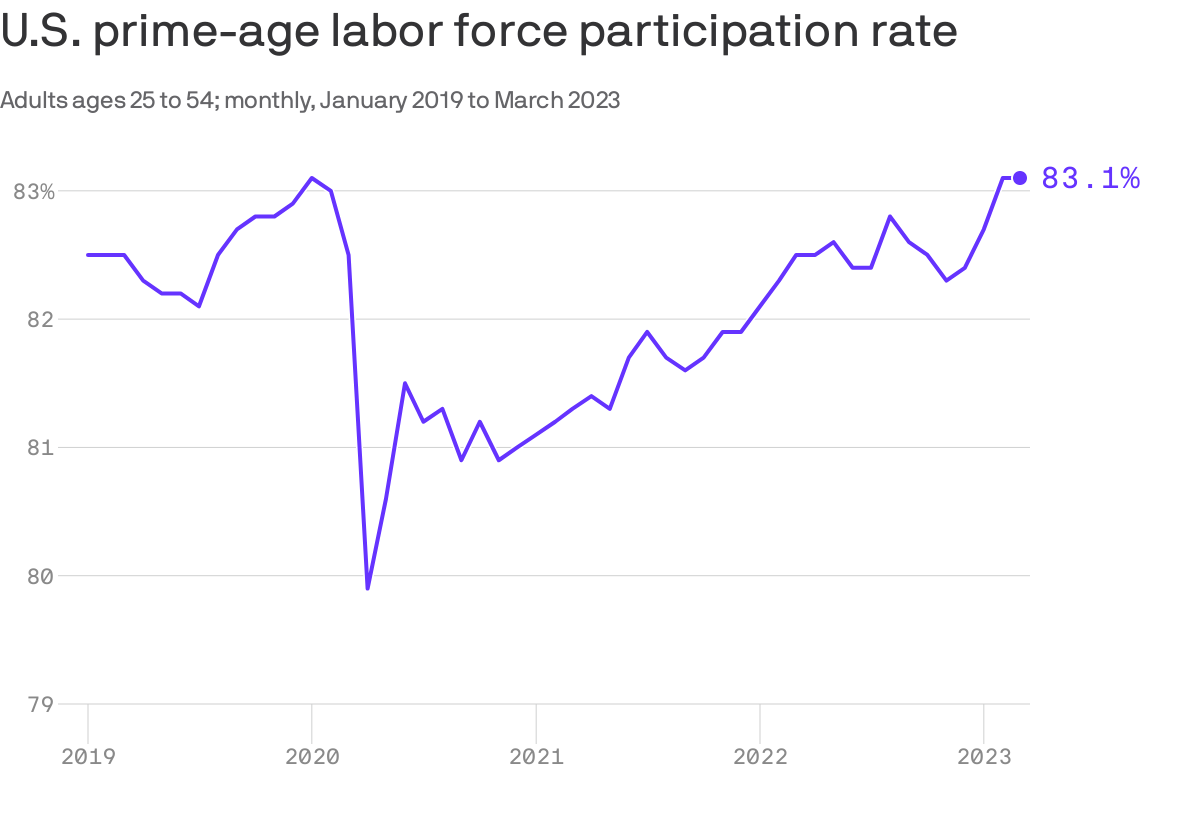

The share of prime-age workers — those between 25 and 54 — who are part of the workforce is now a tick higher than it was before the pandemic: 83.1%, compared with 83.0% in February 2020.

The overall participation rate is down (62.6%, from 63.3% in February 2020), but that is due to the Baby Boom generation retiring. It’s on track with what forecasters at the Congressional Budget Office anticipated before the pandemic.

Moreover, immigration rates surged in 2022 after a pandemic collapse, also adding to the supply of labor.

What they’re saying:

“The swift but lagged response of labor supply to surging demand suggests that with time workers do respond to favorable economic conditions,” the White House economists write.

“There are many plausible reasons that explain why this response is lagged. Most obviously, the job search process itself is not frictionless; it may take workers some time to find a good job,” they wrote.

“Also, if households adapted to the pandemic in ways that can take a while to unwind (such as giving up formal child care), this would delay the labor supply response to growing demand.”

The bottom line:

“There’s still an inaccurate view that prime-age labor supply is depressed,

that immigration is way down, and that labor force participation rates aren’t back on trend following the pandemic shock to our economy,” Ernie Tedeschi, the chief economist at the CEA, tells Axios.

In fact, he said, tight labor markets “pull folks back into the workforce and, while we have more to do to break down barriers to entry, the ‘missing worker’ story doesn’t quite apply anymore.”

In late February, Crystal Run Healthcare, a Middletown, NY-based physician group with nearly 400 providers, became part of UHG’s Optum division.

A local paper broke the news after obtaining an email from Crystal Run’s CEO, as neither company issued a press release, though UHG has since confirmed the acquisition. In addition to pandemic-related financial difficulties, Crystal Run recently shuttered its health plan after large losses, and its Medicare accountable care organization failed to earn savings in 2021.

Crystal Run expands Optum’s footprint in the Hudson Valley region north of New York City, following the acquisition of Mount Kisco, NY-based Caremount Medical in 2022. The company’s broader New York metro area footprint includes Connecticut-based ProHEALTH and New Jersey-based Riverside Medical Group, the three of which Optum has since integrated into a single tri-state medical group.

The Gist: Optum continues to secure its place as the country’s largest aggregator of physicians, now employing or aligning with over 70,000 doctors nationwide.

Not only does every new deal by UHG bolster its vertical integration strategy, but they also shine a light on gaps in federal antitrust regulations. UHG must only disclose deals that comprise a “significant” portion of its business, a threshold that excludes physician groups as large as Crystal Run—making it difficult to fully examine transactions that are subscale according to regulations, but may be significant for healthcare delivery in a local market.

Some state governments, including New York, are exploring ways to increase state antitrust scrutiny of provider acquisitions. But inmulti-state markets where only the federal government has the authority for full oversight, UHG’s acquisition strategies are proving difficult to even monitor, much less intervene.

On Tuesday, Milwaukee, WI-based Froedtert Health and Neenah, WI-based ThedaCare shared they have signed a letter of intent to form a $5B, 18-hospital system.

The merger would unite Froedtert’s southeast Wisconsin service area with ThedaCare’s northeast and central Wisconsin footprint, linking tertiary care patients in ThedaCare’s high-growth service areas in the Fox Valley to Froedtert’s Medical College of Wisconsin in Milwaukee. As the systems serve non-overlapping markets, the merger is not expected to receive challenge from federal regulators.

The Gist: These two systems have partnered previously, striking a joint venture last fall to build two health campuses with micro-hospitals, which likely served as the operational test case for merger plans already in the works.

The pace of consolidation has quickened in the Badger State, with Gundersen Health System and Bellin Health completing a merger last fall to form an 11-hospital system.

While interstate mega-mergers have defined recent health system M&A trends, these types of regional mergers, which bring together systems in adjacent but non-overlapping markets, could serve to bolster the combined system’s value proposition as a partner to employers and other healthcare entities in the state and beyond.

At a recent meeting of physician leaders, we sat next to the head of the health system’s bariatric surgery program. Given the recent and rapid uptake of GLP-1 inhibitors like Ozempic and Wegovy, we asked how he thought these drugs, which can generate dramatic weight loss, would affect his practice.

He chuckled, “they’re really good drugs…they could put me out of business!

It’s too early to say if they’ll be effective over a lifetime, but there’s no doubt they’re going to have a huge impact on our work.” It got us thinking about the other reverberations this class of drugs could have on care needs, if a majority of obese Americans had access to them.

Some effects are obvious.

We could see significant declines in treatment needs for chronic diseases like obesity and heart failure, for which obesity is a strong risk factor. Given that obese patients are much more likely to need joint replacement surgery, we could see a big hit to that demand—although some patients who are poor candidates for surgery because of weight-related complications could become eligible.

Even longer-term, if American’s aren’t dying of chronic disease, we’ll still die of something, so expect diseases of advanced age, like Alzheimer’s and many cancers, to increase. Other pharmaceutical innovations, like the growth of immunotherapy and more targeted cancer treatments, also have the potential to radically alter how disease is managed.

We may be at the beginning of another wave of disruptive medical innovation on the order of the introduction of statins in the 1990s, which combined with minimally invasive catheterization, slashed the need for bypass surgery.

Given their sky-high prices, it’s too soon to tell how quickly the use of these new obesity drugs will grow, but innovations like these will serve to pull more care out of hospitals and into less invasive outpatient medical management.

Using data from Kaufman Hall’s National Hospital Flash Report, as well as publicly available investor reports for some of the nation’s largest nonprofit health systems, the graphic above takes stock of the current state of health system margins.

The median US hospital has now maintained a negative operating margin for a full year. Some good news may be on the horizon, as the picture is slightly less gloomy than a year ago, with year-over-yearrevenues increasing seven points more than total expenses.

However, the external conditions suppressing operating margins aren’t expected to abate, and many large health systems are still struggling.

Among large national non-profits Ascension, CommonSpirit Health, Providence, and Trinity Health, operating income in FY 2022 decreased 180 percent on average, and investment returns fell by 150 percent on average, compared to the year prior.

While health systems’ drop in investment returns mirrors the overall stock market downturn, and is largely comprised of unrealized returns, systems may not be able to rely on investment income to make up for ongoing operating losses.

Published in the April edition of Health Affairs Forefront, this piece unpacks why payers and other corporations have replaced health systems as the top bidders for primary care practices, driving up practice purchase prices from hundreds of dollars to tens of thousands of dollars per patient. While corporate players like UnitedHealth Group, Amazon, and Walgreens have spent an estimated $50B on primary care, it pales in comparison to the potential “$1T opportunity” in value-based care projected by McKinsey and Company.

The authors argue that this tantalizing opportunity exists because the Centers for Medicare and Medicaid Services (CMS) invited corporations to “re-insure” Medicare through capitated arrangements in Medicare Advantage (MA) and its Direct Contracting program.

While CMS intended to promote risk and value-based incentives to improve care quality and costs, the incentive structures baked into these programs have afforded payers record profits, despite neither improving patient outcomes nor reducing government healthcare spending.

The Gist: While the critiques of MA reimbursement structures in this piece are familiar, they are woven together into a convincing rebuke of the “unintended consequences” of CMS’s value-based care policy.

Through poorly designing incentives, CMS paved a runway for corporate America to capture the lion’s share of the financial returns of value-based care, paying prices for primary care that health systems can’t match.

Meanwhile, despite skyrocketing valuations for primary care practices, primary care services remain underfunded and inadequately reimbursed, pushing primary care groups closer to payers with excess profits to invest.

More than two years after Congress acted to shield patients from surprise medical bills, lawmakers are turning to another source of unexpected medical costs: the fees that hospitals tack on for services provided in clinics they own.

Why it matters:

As health systems push more care outside hospital walls, they’re charging extra “facility fees” for common services like blood tests, X-rays and, in some cases, even telehealth visits.

Critics say the practice drives up health care costs while padding hospital profits and incentivizing more consolidation. But hospitals argue the fees cover the cost of nurses, lab technicians, medical records and equipment — and that limiting them could reduce patient care.

But five states are currently considering laws to curb facility fees for certain services or strengthen existing laws, per the National Academy for State Health Policy, which has proposed model legislation.

Connecticut is updating a 2015 law that required notifications when facility fees were being charged by hospitals.

“Rising costs remain a barrier for far too many people and result in many people putting off care because they can’t afford it,” Deidre Gifford, executive director of the Connecticut Office of Health Strategy, said last month, when Democratic Gov. Ned Lamont proposed a package of reforms.

Colorado lawmakers are targeting the practice, despite mounting hospital resistance, Kaiser Health News reported.

And Texas legislators are weighing prohibitions on off-campus fees — a move the Texas Hospital Association brands “unprecedented and dangerous.”

Lawmakers in Indiana and Massachusetts are eyeing similar moves.

How it works:

Many health services can be provided in both hospital and outpatient settings. But some patients who visit an offsite clinic are billed as if they were treated in the hospital.

Some might receive a facility fee if they haven’t yet met their health plan deductible. Others could see the added cost reflected later in higher premiums and copays.

A 2020 Rand report found facility and related professional charges factored in employers and private insurers paying 224% of what Medicare would have paid for the same services at the same facilities.

Some business groups like the Employers’ Forum of Indiana are advocating for bans or moratoriums on the fees, citing the increased cost of offering competitive benefits.

The other side:

Hospitals maintain that facility fees are needed to cover essential infrastructure like electronic health record systems and other overhead costs. Some refer to them as “people fees,” saying they cover the expenses of nurses, lab technicians, pharmacists and other essential staff.

Texas hospitals are concerned about what they say is the broad definition of a facility fee in pending legislation in the state’s Senate, saying it could eliminate all hospital payments besides those that go to physicians.

“We need to quantify what problem we’re trying to solve,” said Cameron Duncan, vice president of advocacy at the Texas Hospital Association.

The group said the bill as originally filed would result in 69% of Texas hospitals closing their outpatient clinics.

The intrigue:

Insurers that negotiated covered costs with hospitals and health systems have remained largely quiet on the fees.

And the vagaries of hospital pricing means transparency requirements alone may not give patients warning about added fees.

“It’s not clear from data either that the fees are consistent, or that you could decipher that the fee is consistent for each type of procedure,” said Vicki Veltri, senior policy fellow at National Academy for State Health Policy and former leader of the Connecticut Office of Health Strategy.

The bottom line:

Patients increasingly get charged like they’re in a hospital even if they didn’t set foot in one as physicians’ offices are increasingly scooped up by massive health systems.

While those health systems tout access and efficiencies to drive down health care costs, facility fees are driving more lawmakers and regulators to do a reality check.

Cindy Powers was driven into bankruptcy by 19 life-saving abdominal operations. Medical debt started stacking up for Lindsey Vance after she crashed her skateboard and had to get nine stitches in her chin. And for Misty Castaneda, open heart surgery for a disease she’d had since birth saddled her with $200,000 in bills.

These are three of an estimated 100 million Americans who have amassed nearly $200 billion in collective medical debt — almost the size of Greece’s economy — according to the Kaiser Family Foundation.

Now lawmakers in at least a dozen states and the U.S. Congress have pushed legislation to curtail the financial burden that’s pushed many into untenable situations: forgoing needed care for fear of added debt, taking a second mortgage to pay for cancer treatment or slashing grocery budgets to keep up with payments.

Some of the bills would create medical debt relief programs or protect personal property from collections, while others would lower interest rates, keep medical debt from tanking credit scores or require greater transparency in the costs of care.

In Colorado, House lawmakers approved a measure Wednesday that would lower the maximum interest rate for medical debt to 3%, require greater transparency in costs of treatment and prohibit debt collection during an appeals process.

If it became law, Colorado would join Arizona in having one of the lowest medical debt interest rates in the country. North Carolina lawmakers have also started mulling a 5% interest ceiling.

But there are opponents. Colorado Republican state Sen. Janice Rich said she worried that the proposal could “constrain hospitals’ debt collecting ability and hurt their cash flow.”

For patients, medical debt has become a leading cause of personal bankruptcy, with an estimated $88 billion of that debt in collections nationwide, according to the Consumer Financial Protection Bureau. Roughly 530,000 people reported falling into bankruptcy annually due partly to medical bills and time away from work, according to a 2019 study from the American Journal of Public Health.

Powers’ family ended up owing $250,000 for the 19 life-saving abdominal surgeries. They declared bankruptcy in 2009, then the bank foreclosed on their home.

“Only recently have we begun to pick up the pieces,” said James Powers, Cindy’s husband, during his February testimony in favor of Colorado’s bill.

In Pennsylvania and Arizona, lawmakers are considering medical debt relief programs that would use state funds to help eradicate debt for residents. A New Jersey proposal would use federal funds from the American Rescue Plan Act to achieve the same end.

Bills in Florida and Massachusetts would protect some personal property — such as a car that is needed for work — from medical debt collections and force providers to be more transparent about costs. Florida’s legislation received unanimous approval in House and Senate committees on its way to votes in both chambers.

In Colorado, New York, New Jersey, Illinois, Massachusetts and the U.S. Congress lawmakers are contemplating bills that would bar medical debt from being included on consumer reports, thereby protecting debtors’ credit scores.

Castaneda, who was born with a congenital heart defect, found herself $200,000 in debt when she was 23 and had to have surgery. The debt tanked her credit score and, she said, forced her to rely on her emotionally abusive husband’s credit.

For over a decade Castaneda wanted out of the relationship, but everything they owned was in her husband’s name, making it nearly impossible to break away. She finally divorced her husband in 2017.

“I’m trying to play catch-up for the last 20 years,” said Castaneda, 45, a hairstylist from Grand Junction on Colorado’s Western Slope.

Medical debt isn’t a strong indicator of people’s credit-worthiness, said Isabel Cruz, policy director at the Colorado Consumer Health Initiative.

While buying a car beyond your means or overspending on vacation can partly be chalked up to poor decision making, medical debt often comes from short, acute-care treatments that are unexpected — leaving patients with hefty bills that exceed their budgets.

For both Colorado bills — to limit interest rates and remove medical debt from consumer reports — a spokesperson for Democratic Gov. Jared Polis said the governor will “review these policies with a lens towards saving people money on health care.”

While neither bill garnered stiff political opposition, a spokesperson for the Colorado Hospital Association said the organization is working with sponsors to amend the interest rate bill “to align the legislation with the multitude of existing protections.”

The association did not provide further details.

To Vance, protecting her credit score early could have had a major impact. Vance’s medical debt began at age 19 from the skateboard crash, and then was compounded when she broke her arm soon after. Now 39, she has never been able to qualify for a credit card or car loan. Her in-laws cosigned for her Colorado apartment.

“My credit identity was medical debt,” she said, “and that set the tone for my life.”