A New York physician has been charged with manslaughter in the second degree and is facing other felonies related to the overdose death of a patient, New York Attorney General Letitia James announced Feb. 19.

Sudipt Deshmukh, MD, allegedly prescribed a lethal mix of opioids and other controlled substances that resulted in the overdose death of a patient. The physician allegedly knew the patient struggled with addiction.

An indictment, unsealed Feb. 18, alleges that between 2006 and 2016, Dr. Deshmukh ignored his professional responsibilities by prescribing combinations of opioid painkillers and other controlled substances, including hydrocodone, methadone and morphine, without regard to the risk of death associated with the combinations of those drugs.

Dr. Deshmukh is facing several felony charges, including healthcare fraud, for allegedly causing Medicare to pay for medically unnecessary prescriptions.

The indictment comes after the attorney general’s office filed a felony complaint against Dr. Deshmukh in August. In 2019, the New York State Office of Professional Medical Conduct found that he committed several counts of misconduct.

Dr. Christine Choi, 32, a medical resident at Harbor-UCLA Medical Center in Torrance, prepares to enter an isolation area for COVID-19 inpatients. Health care providers must face daily patient death and suffering.

Soon after the COVID-19 pandemic began last spring, Christine Choi, DO, a second-year medical resident at Harbor-UCLA Medical Center, volunteered to enter COVID-19 patient rooms. Since then, she has worked countless nights in the intensive care unit in full protective gear, often tasked with giving the sickest patients and their families the grim choice between intubation or near-certain death.

“I’m offering this guy two terrible options, and that’s how I feel about work: I can’t fix this for you and it sucks, and I’m sorry that the choices I’m giving you are both terrible,” Choi told the Los Angeles Times’ Soumya Karlamangla about one patient encounter.

While Choi exhibits an “almost startlingly positive attitude” in her work, it’s no match for the psychological burdens placed on her shoulders by the global pandemic, Karlamangla wrote. When an older female COVID-19 patient died in the hospital recently, her husband — in the same hospital with the same diagnosis — soon began struggling to breathe. Sensing that he had little time left, Choi held a mobile phone at his bedside so that each of his children could come on screen to tell him they loved him. “I was just bawling in my [personal protective equipment],” Choi said. “The sound of the family members crying — I probably will never forget that,” she said.

It was not the first time the young doctor helped family members say goodbye to a loved one, and it would not be the last. Health care providers like Choi have had to work through unimaginable tragedies and unprecedented circumstances because of COVID-19, with little time to dedicate to their own mental health or well-being.

It has been nearly a year since the US reported what was believed at the time to be its first coronavirus death in Washington State. Since then, the pandemic death toll has mushroomed to nearly 500,000 nationwide, including 49,000 Californians. These numbers are shocking, and yet they do not capture the immeasurable emotional weight that falls on the health care providers with the most intimate view of COVID-19’s deadly progression.“The horror of the pandemic has unfolded largely outside public view and inside hospitals, piling a disproportionate share of the trauma on the people whose work takes them inside their walls,” Karlamangla wrote.

Experts are deeply concerned about the psychological and physical burdens that providers must bear, and the fact that there is still no end in sight. “At least with a natural disaster, it happens, people get scattered all over the place, property gets damaged or flooded, but then we begin to rebuild,” Lawrence Palinkas, PhD, MA, a medical anthropologist at USC, told Karlamangla. “We’re not there yet, and we don’t know when that will actually occur.”

Sixty-eight percent of providers said they feel emotionally drained from their work, 59% feel burned out, 57% feel overworked, and 50% feel frustrated. The poll asked providers who say they feel burned out what contributes most to that viewpoint. One doctor from the Central Valley wrote:

“Short staffed due to people out with COVID. I’m seeing three times as many patients, with no time to chart or catch up. Little appreciation or contact from my bosses. I have never had an N95 [mask]. The emotional toll this pandemic is taking. Being sick myself and spreading it to my wife and young kids. Still not fully recovered but needing to be at work due to physician shortages. Lack of professional growth, and a sense of lack of appreciation at work and feeling overworked. The sadness of the COVID-related deaths and the stories that go along with the disease. That’s a lot of stuff to unpack.”

The pandemic has been especially challenging for female health providers, who compose 77% of health care workers with direct patient contact. “The pandemic exacerbated gender inequities in formal and informal work, and in the distribution of home responsibilities, and increased the risk of unemployment and domestic violence,” an international group of experts wrote in the Lancet. “While trying to fulfill their professional responsibilities, women had to meet their families’ needs, including childcare, home schooling, care for older people, and home care.”

For one female doctor from the Bay Area who responded to the CHCF survey, the extra burdens of the pandemic have been unrelenting: “Having to work more, lack of safe, affordable, available childcare while I’m working. As a single mother, working 15 hours straight, then having to care for my daughter when I get home. Just exhausted with no days off. So many Zoom meetings all day long. Miss my family and friends.”

It is unclear how the pandemic will affect the health care workforce in the long term. For now, the damage “can be measured in part by a surge of early retirements and the desperation of community hospitals struggling to hire enough workers to keep their emergency rooms running,” Andrew Jacobs reported in the New York Times.

One of the early retirements Jacobs cited was Sheetal Khedkar Rao, MD, a 42-year-old internist in suburban Chicago. Last October, she decided to stop practicing medicineafter “the emotional burden and moral injury became too much to bear,” she said. Two of the main factors driving her decision were a 30% pay cut to compensate for the decline in revenue from primary care visits and the need to spend more time at home after her two preteen children switched to remote learning.

“Everyone says doctors are heroes and they put us on a pedestal, but we also have kids and aging parents to worry about,” Rao said.

Working Through Unremitting Sickness and Death

In addition to the psychological burden, health care providers must cope with a harsh physical toll. People of color account for most COVID-19 cases and deaths among health care workers, according to a KFF issue brief. Some studies show that health care workers of color “are more likely to report reuse of or inadequate access to [personal protective equipment] and to work in clinical settings with greater exposure to patients with COVID-19.”

“Lost on the Frontline,” a collaboration of Kaiser Health News and the Guardian, has counted more than 3,400 deaths among US health care workers from COVID-19. Eighty-six percent of the workers who died were under age 60, and nurses accounted for roughly one-third of the deaths.

“Lost on the Frontline” provides the most comprehensive picture available of health care worker deaths, because the US still lacks a uniform system to collect COVID-19 morbidity and mortality data among health care workers. A year into the project, the federal government has decided to take action. Officials at the US Department of Health and Human Services cited the project when asking the National Academies of Sciences, Engineering, and Medicine for a rapid expert consultation to understand the causes of deaths among health care workers during the pandemic.

The National Academies’ report, published December 10, recommends the “adoption and use of a uniform national framework for collecting, recording, and reporting mortality and morbidity data” along with the development of national reporting standards for a core set of morbidity impacts, including mental well-being and psychological effects related to working through public health crises. Some health care experts said the data gathering could be modeled on the federal government’s World Trade Center Health Program, which provides no-cost medical monitoring and treatment for workers who responded to the 9/11 terrorist attacks 20 years ago.

“We have a great obligation to people who put their lives on the line for the nation,” Victor J. Dzau, MD, president of the National Academy of Medicine, told Jacobs.

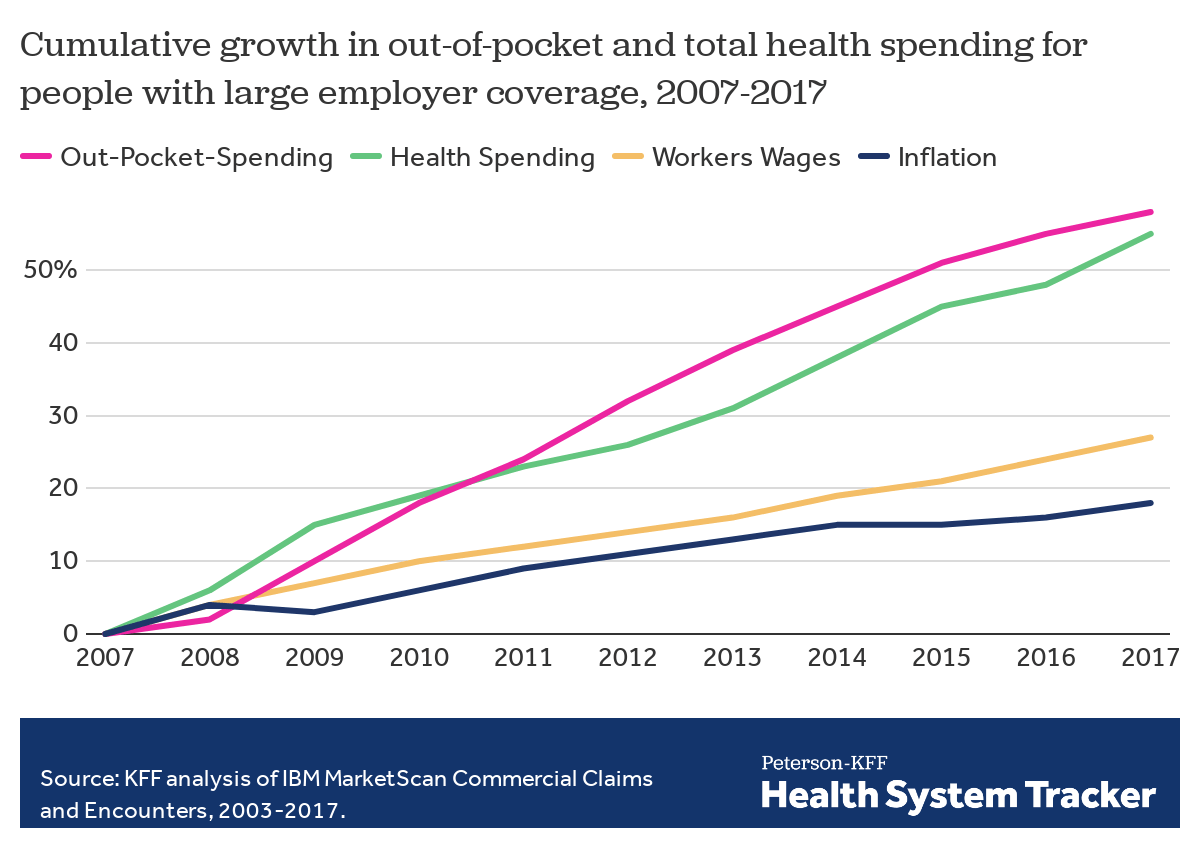

Employers — including companies, state governments and universities — purchase health care on behalf of roughly 150 million Americans. The cost of that care has continued to climb for both businesses and their workers.

For many years, employers saw wasteful care as the primary driver of their rising costs. They made benefits changes like adding wellness programs and raising deductibles to reduce unnecessary care, but costs continued to rise. Now, driven by a combination of new research and changing market forces — especially hospital consolidation — more employers see prices as their primary problem.

By amassing and analyzing employers’ claims data in innovative ways, academics and researchers at organizations like the Health Care Cost Institute (HCCI) and RAND have helped illuminate for employers two key truths about the hospital-based health care they purchase:

1) PRICES VARY WIDELY FOR THE SAME SERVICES

Data show that providers charge private payers very different prices for the exact same services — even within the same geographic area.

For example, HCCI found the price of a C-section delivery in the San Francisco Bay Area varies between hospitals by as much as:$24,107

Data show that hospitals charge employers and private insurers, on average, roughly twice what they charge Medicare for the exact same services. A recent RAND study analyzed more than 3,000 hospitals’ prices and found the most expensive facility in the country charged employers:4.1xMedicare

Hospitals claim this price difference is necessary because public payers like Medicare do not pay enough. However, there is a wide gap between the amount hospitals lose on Medicare (around -9% for inpatient care) and the amount more they charge employers compared to Medicare (200% or more).

Employer Efforts

A small but growing group of companies, public employers (like state governments and universities) and unions is using new data and tactics to tackle these high prices. (Learn more about who’s leading this work, how and why by listening to our full podcast episode in the player above.)

Note that the employers leading this charge tend to be large and self-funded, meaning they shoulder the risk for the insurance they provide employees, giving them extra flexibility and motivation to purchase health care differently. The approaches they are taking include:

Steering Employees

Some employers are implementing so-called tiered networks, where employees pay more if they want to continue seeing certain, more expensive providers. Others are trying to strongly steer employees to particular hospitals, sometimes know as centers of excellence, where employers have made special deals for particular services.

Purdue University, for example, covers travel and lodging and offers a $500 stipend to employees that get hip or knee replacements done at one Indiana hospital.

Negotiating New Deals

There is a movement among some employers to renegotiate hospital deals using Medicare rates as the baseline — since they are transparent and account for hospitals’ unique attributes like location and patient mix — as opposed to negotiating down from charges set by hospitals, which are seen by many as opaque and arbitrary. Other employers are pressuring their insurance carriers to renegotiate the contracts they have with hospitals.

In 2016, the Montana state employee health plan, led by Marilyn Bartlett, got all of the state’s hospitals to agree to a payment rate based on a multiple of Medicare. They saved more than $30 million in just three years. Bartlett is now advising other states trying to follow her playbook.

In 2020, several large Indiana employers urged insurance carrier Anthem to renegotiate their contract with Parkview Health, a hospital system RAND researchers identified as one of the most expensive in the country. After months of tense back-and-forth, the pair reached a five-year deal expected to save Anthem customers $700 million.

Legislating, Regulating, Litigating

Some employer coalitions are advocating for more intervention by policymakers to cap health care prices or at least make them more transparent. States like Colorado and Indiana have passed price transparency legislation, and new federal rules now require more hospital price transparency on a national level. Advocates expect strong industry opposition to stiffer measures, like price caps, which recently failed in the Montana legislature.

Other advocates are calling for more scrutiny by state and federal officials of hospital mergers and other anticompetitive practices. Some employers and unions have even resorted to suing hospitals like Sutter Health in California.

Employer Challenges

Employers face a few key barriers to purchasing health care in different and more efficient ways:

Provider Power

Hospitals tend to have much more market power than individual employers, and that power has grown in recent years, enabling them to raise prices. Even very large employers have geographically dispersed workforces, making it hard to exert much leverage over any given hospital. Some employers have tried forming purchasing coalitions to pool their buying power, but they face tricky organizational dynamics and laws that prohibit collusion.

Sophistication

Employers can attempt to lower prices by renegotiating contracts with hospitals or tailoring provider networks, but the work is complicated and rife with tradeoffs. Few employers are sophisticated enough, for example, to assess a provider’s quality or to structure hospital payments in new ways.Employers looking for insurers to help them have limited options, as that industry has also become highly consolidated.

Employee Blowback

Employers say they primarily provide benefits to recruit and retain happy and healthy employees. Many are reluctant to risk upsetting employees by cutting out expensive providers or redesigning benefits in other ways. A recent KFF survey found just 4% of employers had dropped a hospital in order to cut costs.

The Tradeoffs

Employers play a unique role in the United States health care system, and in the lives of the 150 million Americans who get insurance through work. For years, critics have questioned the wisdom of an employer-based health care system, and massive job losses created by the pandemic have reinforced those doubts for many.

Assuming employers do continue to purchase insurance on behalf of millions of Americans, though, focusing on lowering the prices they pay is one promising path to lowering total costs. However, as noted above, hospitals have expressed concern over the financial pressures they may face under these new deals. Complex benefit design strategies, like narrow or tiered networks, also run the risk of harming employees, who may make suboptimal choices or experience cost surprises. Finally, these strategies do not necessarily address other drivers of high costs including drug prices and wasteful care.

The complexity of Medicare Advantage (MA) physician networks has been well-documented, but the payment regulations that underlie these plans remain opaque, even to experts. If an MA plan enrollee sees an out-of-network doctor, how much should she expect to pay?

The answer, like much of the American healthcare system, is complicated. We’ve consulted experts and scoured nearly inscrutable government documents to try to find it. In this post we try to explain what we’ve learned in a much more accessible way.

Medicare Advantage Basics

Medicare Advantage is the private insurance alternative to traditional Medicare (TM), comprised largely of HMO and PPO options. One-third of the 60+ million Americans covered by Medicare are enrolled in MA plans. These plans, subsidized by the government, are governed by Medicare rules, but, within certain limits, are able to set their own premiums, deductibles, and service payment schedules each year.

Critically, they also determine their own network extent, choosing which physicians are in- or out-of-network. Apart from cost sharing or deductibles, the cost of care from providers that are in-network is covered by the plan. However, if an enrollee seeks care from a provider who is outside of their plan’s network, what the cost is and who bears it is much more complex.

Provider Types

To understand the MA (and enrollee) payment-to-provider pipeline, we first need to understand the types of providers that exist within the Medicare system.

Participating providers, which constitute about 97% of all physicians in the U.S., accept Medicare Fee-For-Service (FFS) rates for full payment of their services. These are the rates paid by TM. These doctors are subject to the fee schedules and regulations established by Medicare and MA plans.

Non-participating providers(about 2% of practicing physicians) can accept FFS Medicare rates for full payment if they wish (a.k.a., “take assignment”), but they generally don’t do so. When they don’t take assignment on a particular case, these providers are not limited to charging FFS rates.

Opt-out providersdon’t accept Medicare FFS payment under any circumstances. These providers, constituting only 1% of practicing physicians, can set their own charges for services and require payment directly from the patient. (Many psychiatrists fall into this category: they make up 42% of all opt-out providers. This is particularly concerning in light of studies suggesting increased rates of anxiety and depression among adults as a result of the COVID-19 pandemic).

How Out-of-Network Doctors are Paid

So, if an MA beneficiary goes to see an out-of-network doctor, by whom does the doctor get paid and how much? At the most basic level, when a Medicare Advantage HMO member willingly seeks care from an out-of-network provider, the member assumes full liability for payment.That is, neither the HMO plan nor TM will pay for services when an MA member goes out-of-network.

The price that the provider can charge for these services, though, varies, and must be disclosed to the patient before any services are administered. If the provider is participating with Medicare (in the sense defined above), they charge the patient no more than the standard Medicare FFS rate for their services. Non-participating providers that do not take assignment on the claim are limited to charging the beneficiary 115% of the Medicare FFS amount, the “limiting charge.” (Some states further restrict this. In New York State, for instance, the maximum is 105% of Medicare FFS payment.) In these cases, the provider charges the patient directly, and they are responsible for the entire amount (See Figure 1.)

Alternatively, if the provider has opted-out of Medicare, there are no limits to what they can charge for their services.The provider and patient enter into a private contract; the patient agrees to pay the full amount, out of pocket, for all services.

MA PPO plans operate slightly differently. By nature of the PPO plan, there are built-in benefits covering visits to out-of-network physicians (usually at the expense of higher annual deductibles and co-insurance compared to HMO plans). Like with HMO enrollees, an out-of-network Medicare-participating physician will charge the PPO enrollee no more than the standard FFS rate for their services. The PPO plan will then reimburse the enrollee 100% of this rate, less coinsurance. (SeeFigure 2.)

In contrast, a non-participating physician that does not take assignment is limited to charging a PPO enrollee 115% of the Medicare FFS amount, which can be further limited by state regulations. In this case, the PPO enrollee is also reimbursed by their plan up to 100% (less coinsurance) of the FFS amount for their visit. Again, opt-out physicians are exempt from these regulations and must enter private contracts with patients.

Figure 2: MA PPO Out-of-Network Payments

Some Caveats

There are two major caveats to these payment schemes (with many more nuanced and less-frequent exceptions detailed here). First, if a beneficiary seeks urgent or emergent care (as defined by Medicare) and the provider happens to be out-of-network for the MA plan (regardless of HMO/PPO status), the plan must cover the services at their established in-network emergency services rates.

The second caveat is in regard to the declared public health emergency due to COVID-19 (set to expire in April 2021, but likely to be extended). MA plans are currently required to cover all out-of-network services from providers that contract with Medicare (i.e., all but opt-out providers) and charge beneficiaries no more than the plan-established in-network rates for these services. This is being mandated by CMS to compensate for practice closures and other difficulties of finding in-network care as a result of the pandemic.

Conclusion

Outside of the pandemic and emergency situations, knowing how much you’ll need to pay for out-of-network services as a MA enrollee depends on a multitude of factors. Though the vast majority of American physicians contract with Medicare, the intersection of insurer-engineered physician networks and the complex MA payment system could lead to significant unexpected costs to the patient.