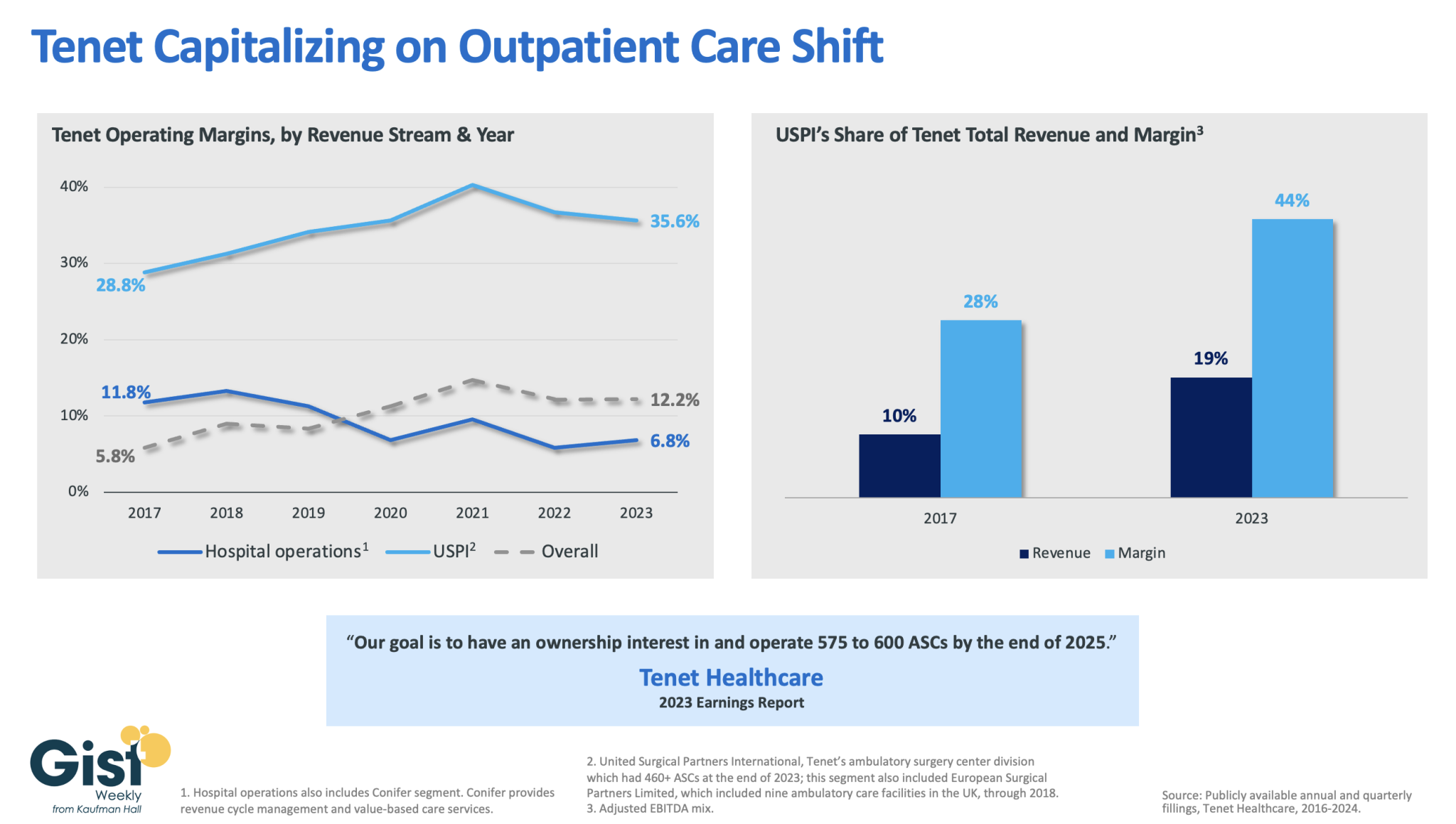

In this week’s graphic, we dive into recently released data on Tenet Healthcare’s 2023 financial performance. While the for-profit healthcare services company’s annual margin on hospital operations has declined since 2017, its overall profitability has more than doubled, thanks to strong performances from its ambulatory surgery center (ASC) chain,

United Surgical Partners International (USPI), which has consistently posted margins above 30 percent. Despite bringing in less than one fifth of Tenet’s total revenue, USPI is now responsible for almost half of Tenet’s overall margin.

Tenet has pursued this growth aggressively since buying USPI in 2015, swelling its ASC footprint from 249 locations in 2015 to more than 460 in 2023, with plans to increase that number to nearly 600 by the end of next year.

Tenet appears to be doubling down on its strategy of pursuing high-margin services over high-revenue services, especially as outpatient volumes are expected to far surpass growth in hospital-based care over the next decade.

Two newly published investigative reports, by the intrepid reporters at STAT News and The American Prospect, pull the curtains back a little more on the astonishing number of recent acquisitions UnitedHealth has made as it moves deeper and deeper into health care delivery, enabling it to grab ever-increasing chunks of our premium and tax dollars to reward its shareholders.

That’s a strategic move that allows the company to steer more seniors to facilities it owns, boosting revenues it gets from the government and padding its bottom line.

The bigger a company gets, the less it has to disclose about the acquisitions it makes in any easily obtainable way. That’s because publicly-traded companies are only required to immediately inform investors of individual deals that are “material to earnings.”

A material amount, as Investopedia explains, “can signify any sum or figure worth mentioning, as in account balances, financial statements, shareholder reports, or conference calls. If something is not a material amount, it is considered too insignificant or trivial to mention.”

UnitedHealth’s long string of acquisitions in recent years has catapulted the company to the #5 spot on the Fortune 500 list of American companies, based on revenue. Only Walmart, Exxon Mobile, Amazon and Apple are bigger.

That rapid growth means that fewer and fewer of UnitedHealth’s acquisitions reach the threshold of requiring prominent disclosure to shareholders.

It was only through a close review of UnitedHealth’s latest annual report to investors and other financial documents that STAT was able to see what the company hides from most of us. As Herman noted:

UnitedHealth Group is so big that it doesn’t have to publicly announce a vast majority of its acquisitions. But a STAT analysis of company financial documents shows the health care conglomerate quietly acquired dozens of outpatient facilities in 2023, with a particular focus on surgery centers.

And it’s not adding random surgery centers, either. There seems to be an explicit strategy: Many of UnitedHealth’s new centers sit in geographic areas where the company is the biggest Medicare Advantage player, based on the latest insurance market share data. That overlap reinforces how UnitedHealth is looking to funnel more of its insurance members toward providers that it owns, with the overarching goal of capturing more profit.

As an example, STAT said it stumbled upon an entry–”buried within UnitedHealth’s annual report”–that revealed the company’s previously undisclosed December acquisition of National Cardiovascular Partners, which operates 21 cardiac cath and vascular labs. Not coincidentally, NCP’s facilities are “in places like Phoenix and large metro areas in Texas where UnitedHealth has the biggest MA market share.”

Tkacik wrote that last Thursday, UnitedHealthcare applied for an emergency exemption that would fast-track its takeover of a medical practice in Corvallis, Oregon, which is facing the prospect of closing its doors because of the financial crunch caused by the hack. As Tkacik explained, the hack interrupted the flow of information from Change Healthcare’s claims processing systems that enables physicians, hospitals, and other health care providers to get paid.

Perversely, UnitedHealth is telling Oregon regulators that the best solution is to allow the company’s proposed acquisition of the medical practice to go forward.

Tkacik reported that:

Although the specific reason for the exemption request is redacted from the publicly posted version of the application, a clinic insider says the “emergency” is the same one that has plunged thousands of other health providers across the nation into a terrifying cash crunch…

The situation underscores the perverse state of affairs in which UnitedHealth, which comprises some 2,642 separate companies that collectively raked in $371.6 billion last year, has arguably profited from the desperation that the hacking of its Change computer systems in late February has inflicted upon the health care system.

An estimated half of all health care transactions are processed or somehow otherwise touched by Change, a rollup of dozens of health care technology firms that provide 137 software applications that have been affected by the outage.

Tkacid added that “Every dollar in revenue that has disappeared from hospitals, medical practices, and pharmacies in the aftermath of the outage corresponds to an extra dollar sitting in the coffers of the nation’s health insurers, so UnitedHealth, which pays out roughly $662 million in medical claims each day, is presumably sitting on a mountain of unexpected cash.”

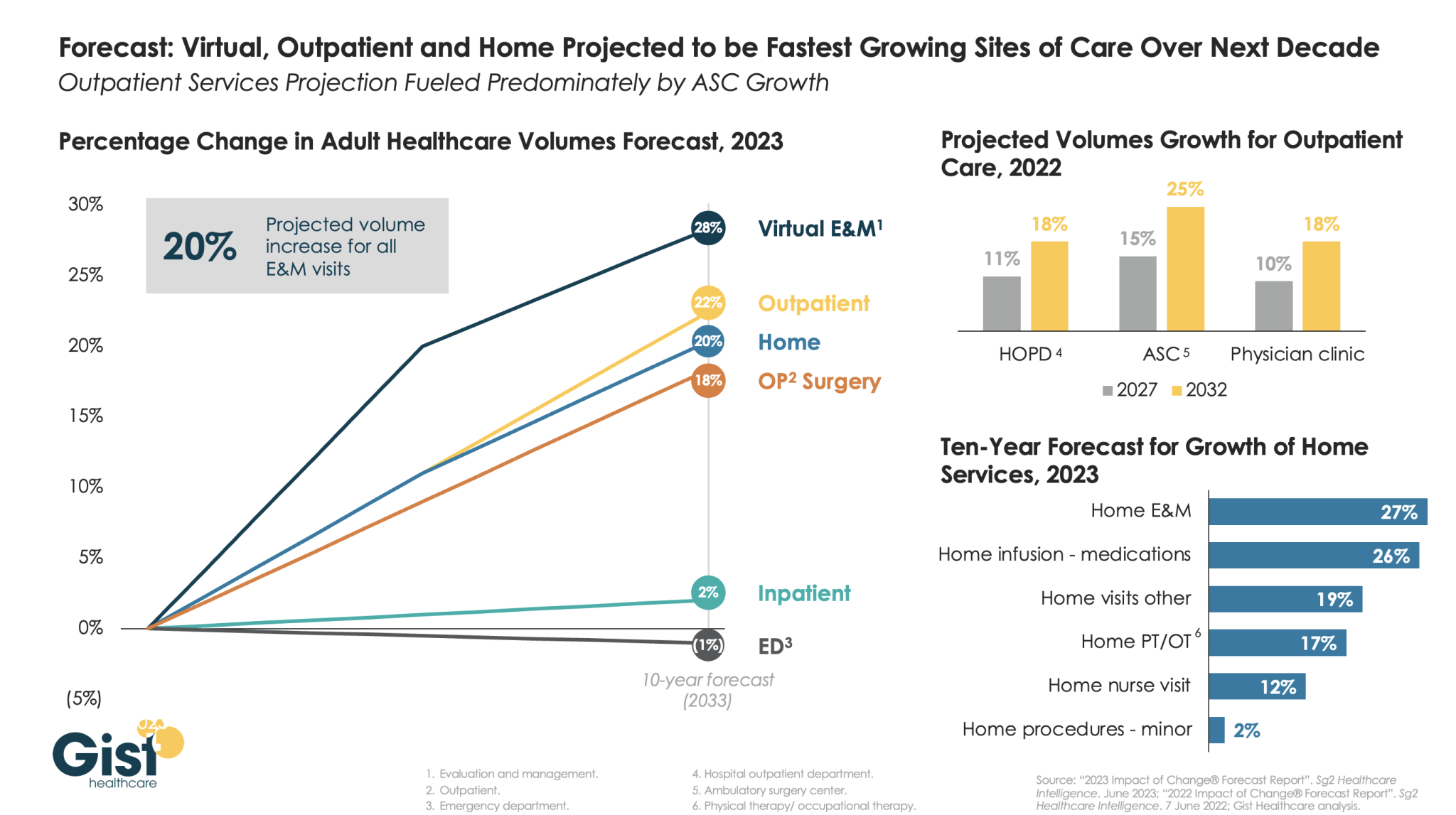

The pandemic accelerated the outpatient shift, which had been progressing steadily for decades, into a new gear, as safety-minded consumers avoided inpatient settings.

Using the latest forecasting data from strategic healthcare consulting firm Sg2, the graphic above illustrates how the outpatient shift will continue to accelerate in the coming years. With each projected to grow by 20 percent or more, outpatient, virtual, and home-based care services will continue far outpace growth in hospital-based care over the next decade.

Ambulatory surgery centers (ASCs) will be at the center of this care shift, reflected by a projected 25 percent rise in ASC volumes by 2032.

The breadth of care available at home will also expand as care delivery technology improves. With the population becoming older and sicker, higher incidence of chronic disease will be met by a rapid expansion of home evaluation and management services (E&M),reflecting a shift away from hospitals and doctors’ offices as hubs for complex care management.

Instead, the patients still coming to hospitals will present with increasingly acute conditions, driving up demand for resource-intensive critical care, as broader inpatient volume remains relatively flat.

CMS proposes in the Outpatient Prospective Payment (OPPS) rule to increase Medicare outpatient payments by 2.8 percent next year while bolstering hospital price transparency enforcement.

The OPPS rule states that payment rates for hospitals that meet applicable quality reporting requirements will increase in 2024 based on the projected market basket percentage increase of 3.0 percent, less 0.2 percentage points for the productivity adjustment.

Meanwhile, ambulatory surgical centers (ASCs) would also see a 2.8 percent increase in payment rates next year under the proposed ASC rule that was released alongside the OPPS rule.

CMS also proposes to continue using the productivity-adjusted hospital market basket update to ASC payment system rates for another two years despite plans to shift away from the system as hospital procedures shift to ASC settings. But disruptions to care patterns during the COVID-19 pandemic have prompted CMS to extend the application of the hospital market basket update.

The OPPS and ASC proposed rules also include a new benefit category for Medicare beneficiaries who require more frequent services than individual outpatient therapy visits but less intensive services than a partial hospitalization program. The benefit would be the Intensive Outpatient Program and include its own payment and program requirements for services across various settings, including hospital outpatient departments, community mental health centers, and federally qualified health centers.

Starting next year, CMS also proposes establishing payment for intensive outpatient program services as part of Opioid Treatment Programs. These intensive behavioral health services are available for individuals with mental health conditions and substance use disorders.

Other payment policies proposed in the rule include an update to Medicare payment rates for partial hospitalization program services, remote mental health services, and OPPS and ASC dental services, as well as changes to community mental health center Conditions of Participation (CoPs). The proposed rule also contains updates to the 340B payment rate, which CMS proposed to remedy via previous rulemaking to return improper payments to eligible hospitals.

“This proposed rule reflects CMS’ commitment to ensure Medicare is comprehensive in its ability to address patient needs, filling gaps in the health care system including behavioral health,” Meena Seshamani, MD, Deputy Administrator and Director for CMS’ Center for Medicare, said in a statement. “Through these proposals, we will ensure people get timely access to quality care in their communities, leading to improved outcomes and better health.”

HOSPITAL PRICE TRANSPARENCY CHANGES ON HORIZON

In addition to payment updates, the OPPS proposed rule also includes extensive updates to hospital price transparency requirements to increase compliance and enforcement.

Previous OPPS rules have required hospitals to make standard charges, including payer-specific negotiated rates, available to the public in a machine-readable file on their websites and through a more patient-friendly list of shoppable services. Hospitals face financial penalties of up to $2 million if they do not comply with the requirements.

However, a recent website assessment conducted by CMS found that about 70 percent of hospitals were fully meeting display criteria for the machine-readable file, 27 percent were partially meeting display criteria, and just 3 percent failed to post any required pricing data online by the fall of 2022. The rates improved from a previous compliance assessment in early 2021 when 30 percent of hospitals did not publish the required pricing data.

However, the latest OPPS rule aims to increase compliance by altering enforcement actions. For example, the rule would allow CMS to require an authorized hospital official to certify the accuracy and completeness of the data in the machine-readable file. Hospitals may also have to submit additional documentation to determine hospital compliance and an acknowledgment of receipt of the warning notice if CMS deems them out of compliance.

If CMS has to take action to address noncompliance, CMS may also notify the hospital’s health system leadership of the issue and work with the health system to address compliance issues across its system.

Finally, CMS proposes to publicize a hospital’s assessment of compliance, any compliance actions taken against a hospital, and notifications sent to health system leadership.

Additionally, the OPPS rule would update hospital price transparency requirements, requiring hospitals to display the required pricing data using a CMS template versus any machine-readable file format. Pricing data would also have to be encoded in a CSV or JSON format using a CMS template layout and other specified technical instructions.

CMS aims to increase machine-readable file accessibility by proposing a requirement to place a “footer” at the bottom of a hospital’s homepage that links to the webpage with the pricing data. Hospitals would also have to ensure that a .txt file is included in the root folder of the publicly available website chosen by the hospital for posting its machine-readable format.

Healthcare stakeholders can comment on the OPPS and ASC proposed rules through September 11th. CMS expects to release the final rules in November.

Health systems are ramping up investments in ambulatory surgery centers and forming joint ventures with outpatient partners to accelerate the development of new centers. The trend is picking up steam as complex procedures increasingly move to ASCs, which are steadily growing as the preferred site of service for physicians, patients and payers.

Tenet Healthcare, one of the largest for-profit health systems in the country, has been paying close attention to outpatient migration for years and has cemented itself as the leader in the ASC space. It now operates more than 445 ASCs — the most of any health system — and 24 surgical hospitals, according to its first-quarter earnings report.

United Surgical Partners International, Tenet’s ASC company, strengthened its footing in the ASC market after its $1.2 billion acquisition of Towson, Md.-based SurgCenter Development and its more than 90 ASCs in December 2021. Over the next several years, USPI will inject more than $250 million into ASC mergers and acquisitions and work with SurgCenter to develop at least 50 more ASCs, according to terms of the transaction.

The SurgCenter acquisition was completed shortly after Tenet sold five Florida hospitals to Dallas-based Steward Health Care for $1.1 billion. In 2022, Tenet also acquired Dallas-based Baylor Scott & White Health’s 5 percent equity position in USPI to own 100 percent of the company’s voting shares and paid $78 million to acquire ownership of eight Compass Surgical Partners ASCs.

These ASC investments and hospital sales make it clear that CEO Saum Sutaria, MD, sees surgery centers to become Tenet’s main growth driver in the coming years. Dr. Sutaria has described USPI as the company’s “gem for the future,” and aims to have 575 to 600 ASCs by the end of 2025.

While Tenet continues to increase its ASC market share, its closest competitor is Deerfield, Ill.-based SCA Health, which UnitedHealth Group’s Optum acquired for $2.3 billion several years ago.

SCA has more than 320 ASCs, but has expanded its focus on value-based care under Optum and is doubling down on supporting physicians across the specialty care continuum rather than operating as an ASC company “singularly focused on partnering with surgeons in their ASCs,” SCA CEO Caitlin Zulla told Becker’s.

While Tenet may operate the most ASCs among health systems, it lags behind Optum in terms of the number of physicians it employs. Optum is now affiliated with more than 70,000 physicians, making it the largest employer of physicians in the country, and is continuing to add to that through mergers and acquisitions.

Nashville, Tenn.-based HCA Healthcare, another for-profit system, employs or is affiliated with more than 47,000 physicians, but is also ramping up its surgery center portfolio. HCA comprises 2,300 ambulatory care facilities, including more than 150 ASCs, freestanding emergency rooms, urgent care centers and physician clinics, according to its first-quarter earnings report.

Like Tenet and Optum, HCA is heavily focused on expanding its outpatient portfolio. The company ended 2021 with 125 ASCs, four more than it had at the end of 2020, and added more than 25 ASCs last year. It is focused on both developing and acquiring surgery centers in the coming years.

The other big ASC operators include Nashville, Tenn.-based AmSurg, with more than 250 surgery centers, and Brentwood, Tenn.-based Surgery Partners, with more than 120 centers. Surgery Partners spent about $250 million on ASCs acquisitions last year and recently signed collaboration agreements with two large health systems —- Salt Lake City-based Intermountain Health and Columbus-based OhioHealth.

Oakland, Calif.-based Kaiser Permanente has 62 freestanding ASCs and outpatient surgery departments on its hospital campuses, a spokesperson for the health system told Becker’s.

As care continues to shift to lower cost ambulatory surgery centers (ASCs), the graphic above looks at recent growth and consolidation in the ASC market.

From 2012 to 2022, the five largest operators increased their collective ownership of ASC facilities from 17 to 21 percent, and were responsible for over 50 percent of total facility growth in that period.

While physicians still fully own over half of the nation’s ASCs, the national chains tend to run larger, multispecialty facilities responsible for an outsized proportion of procedures and revenue.

The likes of Tenet, Optum, and HCA are betting big on ASCs, banking on projections that the market will grow by over 60 percent in the next seven years.

(Though AmSurg’s parent company, Envision Healthcare, filed for bankruptcy, AmSurg is buying Envision’s remaining ASCs to retain its significant foothold in the market.)

While many high-revenue specialties, notably orthopedics and gastroenterology, have already seen a significant shift to ASCs, cardiology is one of the most promising service lines for ASC growth, with some predicting that a third of cardiology procedures will be performed in ambulatory settings in the next few years.

The shift of surgeries from hospitals to ASCs is daunting for health systems, who stand to lose half or more of the revenue from each case—if they’re able keep the procedure within the system.

In the meantime, low-cost ASC operators will continue to add new facilities that deliver high margins to fuel their growth.

As the locus of care continues to shift from inpatient hospitals to outpatient centers, health system executives face a growing conundrum over pricing. The combination of “consumerism” and tougher reimbursement policies raises a question about how aggressively systems should discount services to compete in the ambulatory arena.

Site-neutral payment remains a goal for Medicare, and consumers are increasingly voting with their pocketbooks when it comes to choosing where to have procedures and diagnostics performed. “We know we’re going to have to give on price,” one CEO recently shared with us. “The question is how much, and how soon.”

Should hospitals proactively shift to match prices offered by freestanding centers, or should they try to defend their substantially higher “hospital outpatient department” (HOPD) pricing?

The former choice could help win—or at least keep—business in the system, but at the risk of turning that business into a money-losing proposition.

To compete successfully, hospitals will not only need to lower price, but also lower cost-to-serve—rethinking how operations are run, how overhead is allocated, and how services are staffed and delivered in ambulatory settings.

“We’ve got to get our costs down,” the CEO admitted. “Trying to run an ambulatory business with our traditional hospital cost structure is a recipe for losing money.”

And as a system CFO recently told us, “We can’t just trade good price for bad, for doing the same work. We have to be smart about where to discount services.” The future sustainability of many health systems will hinge on how they navigate this transition to an ambulatory-centric model.

The Medicare Advisory Payment Commission recommends a higher-than-current-law fee-for-service payment update in 2024 for acute care hospitals and positive payment updates for clinicians paid under the physician fee schedule. It recommends reductions in base payment rates for skilled nursing facilities, home health agencies and inpatient rehabilitation facilities.

MedPAC gave Congress recommendations on payment rates in both traditional fee-for-service and Medicare Advantage for 2024, satisfying a legislative mandate comparing per enrollee spending in both programs.

MedPAC estimates that Medicare spends 6% more for MA enrollees than it would spend if those enrollees remained in fee-for-service Medicare.

In their March 2023 Report to the Congress: Medicare Payment Policy, commissioners said they were acutely aware of how providers’ financial status and patterns of Medicare spending varied in 2020 and 2021 due to COVID-19 and were also aware of higher and more volatile cost increases.

However, they’re statutorily charged to evaluate available data to assess whether Medicare payments are sufficient to support the efficient delivery of care and ensure access to care for Medicare’s beneficiaries, commissioners said.

FEE-FOR-SERVICE RATE RECOMMENDATIONS

MedPAC’s payment update recommendations are based on an assessment of payment adequacy, beneficiaries’ access to and use of care, the quality of the care, the supply of providers, and their access to capital, the report said. As well as higher payments for acute care hospitals and clinicians, MedPAC recommends positive rates for outpatient dialysis facilities.

It recommends providing additional resources to acute care hospitals and clinicians who furnish care to Medicare beneficiaries with low incomes. It also recommends a positive payment update in 2024 for hospice providers concurrent with wage adjusting and reducing the hospice aggregate Medicare payment cap by 20%.

It recommends negative updates, which are reductions in base payment rates, for skilled nursing facilities, home health agencies and inpatient rehabilitation facilities.

Acute care

For acute care hospitals paid under the inpatient prospective payment system, commissioners recommend adding $2 billion to current disproportionate share and uncompensated care payments and distributing the entire amount using a commission-developed “Medicare SafetyNet Index” to direct funding to those hospitals that provide care to large shares of low-income Medicare beneficiaries.

This recommendation got pushback from America’s Essential Hospitals.

“We appreciate the Medicare Payment Advisory Commission’s desire to define safety net hospitals for targeted support, but the commission’s Medicare safety net index (MSNI) could have the perverse effect of shifting resources away from hospitals that need support the most,” said SVP of Policy and Advocacy Beth Feldpush. “The MSNI methodology fails to account for all the nation’s safety net hospitals by overlooking uncompensated care and care provided to non-Medicare, low-income patients – especially Medicaid beneficiaries. Any practical definition of a safety net provider must consider the care of Medicaid and uninsured patients, yet the MSNI misses on both counts.”

Feldpush urged policymakers to develop a federal designation of safety net hospitals and to reject the MSNI.

“Further, policymaking for these hospitals should supplement, rather than redistribute, existing Medicare DSH funding, which reflects a congressionally sanctioned, well-established methodology,” she said.

Physicians and clinicians

For clinicians, the commission recommends that Medicare make targeted add-on payments of 15% to primary care clinicians and 5% to all other clinicians for physician fee schedule services provided to low-income Medicare beneficiaries.

The American Medical Association commended MedPAC, but also said that an update tied to just 50% of the Medicare Economic Index would cause physician payment to chronically fall even further behind increases in the cost of providing care. AMA president Dr. Jack Resneck Jr. urged Congress to pass legislation providing for an annual inflation-based payment update.

MedPAC has long championed a physician payment update tied to the Medicare Economic Index, Resneck said. Physicians have faced the cost of inflation, the COVID-19 pandemic and growing expenses to run medical practices, jeopardizing access to care, particularly in rural and underserved areas.

“Not only have Medicare payments failed to respond adequately, but physicians saw a 2% payment reduction for 2023, creating an additional challenge at a perilous moment,” Resneck said. “As one of the only Medicare providers without an inflationary payment update, physicians have waited a long time for this change. When adjusted for inflation, Medicare physician payment has effectively declined 26% from 2001 to 2023. These increasingly thin or negative operating margins disproportionately affect small, independent, and rural physician practices, as well as those treating low-income or other historically minoritized or marginalized patient communities. Our workforce is at risk just when the health of the nation depends on preserving access to care.”

The AMA and 134 other health organizations wrote to congressional leaders urging for a full inflation-based update to the Medicare Physician Fee Schedule.

MGMA’s SVP of Government Affairs Anders Gilberg said, “Today’s MedPAC report recommends Congress provide an inflationary update to the Medicare base payment rate for physician and other health professional services of 50% of the Medicare Economic Index (MEI), an estimated annual increase of 1.45% for 2024. In the best of times such a nominal increase would not cover annual medical practice cost increases. In the current inflationary environment, it is grossly insufficient.”

MGMA urged Congress to pass legislation to provide an annual inflationary update based on the full MEI.

Ambulatory surgical centers and long-term care hospitals

Previously, the commission considered an annual update recommendation for ambulatory surgical centers (ASCs). However, because Medicare does not require ASCs to submit data on the cost of treating beneficiaries, the commissioners said they had no new significant data to inform an ASC update recommendation for 2024.

Commissioners also previously considered an annual update recommendation for long-term care hospitals (LTCHs). But as the number of cases that qualify for payment under Medicare’s prospective payment system for LTCHs has fallen, they said they have become increasingly concerned about small sample sizes in the analyses of this sector.

“As a result, we will no longer provide an annual payment adequacy analysis for LTCHs but will continue to monitor that sector and provide periodic status reports,” they said in the report.

MEDICARE ADVANTAGE

Commissioners said that overall, indicators point to an increasingly robust MA program. In 2022, the MA program included over 5,200 plan options, enrolled about 29 million Medicare beneficiaries (49% of eligible beneficiaries), and paid MA plans $403 billion (not including Part D drug plan payments).

In 2023, the average Medicare beneficiary has a choice of 41 plans offered by an average of eight organizations. Further, the level of rebates that fund extra benefits reached a record high of about $2,350 per enrollee, on average.

Medicare payments for these extra benefits – which are not covered for beneficiaries in FFS – have more than doubled since 2018. For 2023, the average MA plan bid to provide Medicare Part A and Part B benefits was 17% less than FFS Medicare would be projected to spend for those enrollees.

However, the benefits from MA’s lower cost relative to FFS spending are shared exclusively by the companies sponsoring MA plans and MA enrollees (in the form of extra benefits). The taxpayers and FFS Medicare beneficiaries (who help fund the MA program through Part B premiums) do not realize any savings from MA plan efficiencies.

Medicare should not continue to overpay MA plans, MedPAC said. Over the past few years, the commission has made recommendations to address coding intensity, replace the quality bonus program and establish more equitable benchmarks, which are used to set plan payments, the report said. All of these would stem Medicare’s excess payments to MA plans, helping to preserve Medicare’s solvency and sustainability while maintaining beneficiary access to MA plans and the extra benefits they can provide.

PART D

Medicare’s cost-based reinsurance continues to be the largest and fastest growing component of Part D spending, totaling $52.4 billion, or about 55% of the total, according to the report.

As a result, the financial risk that plans bear, as well as their incentives to control costs, has declined markedly. The value of the average basic benefit that is paid to plans through the capitated direct subsidy has plummeted in recent years.

In 2023, direct subsidy payments averaged less than $2 per member per month, compared with payments of nearly $94 per member, per month, for reinsurance. To help address these issues, in 2020 the commission recommended substantial changes to Part D’s benefit design to limit enrollee out-of-pocket spending; realign plan and manufacturer incentives to help restore the role of risk-based, capitated payments; and eliminate features of the current program that distort market incentives.

In 2022, Congress passed the Inflation Reduction Act, which included numerous policies related to prescription drugs. One such provision is a redesign of the Part D benefit with many similarities to the commission’s recommended changes.

The changes adopted in the IRA will be implemented over the next several years, and are likely to alter the drug-pricing landscape, commissioners said.

Radio Advisory’s Rachel Woods sat down with Optum EVP Dr. Jim Bonnette to discuss the sustainability of modern-day hospitals and why scaling down might be the best strategy for a stable future.

Rachel Woods:When I talk about hospitals of the future, I think it’s very easy for folks to think about something that feels very futuristic, the Jetsons, Star Trek, pick your example here. But you have a very different take when it comes to the hospital, the future, and it’s one that’s perhaps a lot more streamlined than even the hospitals that we have today. Why is that your take?

Jim Bonnette: My concern about hospital future is that when people think about the technology side of it, they forget that there’s no technology that I can name that has lowered health care costs that’s been implemented in a hospital. Everything I can think of has increased costs and I don’t think that’s sustainable for the future.

And so looking at how hospitals have to function, I think the things that hospitals do that should no longer be in the hospital need to move out and they need to move out now. I think that there are a large number of procedures that could safely and easily be done in a lower cost setting, in an ASC for example, that is still done in hospitals because we still pay for them that way. I’m not sure that’s going to continue.

Woods: And to be honest, we’ve talked about that shift, I think about the outpatient shift. We’ve been talking about that for several years but you just said the change needs to happen now. Why is the impetus for this change very different today than maybe it was two, three, four, five years ago? Why is this change going to be frankly forced upon hospitals in the very near future, if not already?

Bonnette: Part of the explanation is regarding the issues that have been pushed regarding price transparency. So if employers can see the difference between the charges for an ASC and an HOPD department, which are often quite dramatic, they’re going to be looking to say to their brokers, “Well, what’s the network that involves ASCs and not hospitals?” And that data hasn’t been so easily available in the past, and I think economic times are different now.

We’re not in a hyper growth phase, we’re not where the economy’s performing super at the moment and if interest rates keep going up, things are going to slow down more. So I think employers are going to become more sensitized to prices that they haven’t been in the past. Regardless of the requirements under the Consolidated Appropriations Act, which require employers to know the costs, which they didn’t have to know before. They’re just going to more sensitive to price.

Woods: I completely agree with you by the way, that employers are a key catalyst here and we’ve certainly seen a few very active employers and some that are very passive and I too am interested to see what role they play or do they all take much more of an active role.

And I think some people would be surprised that it’s not necessarily consumers themselves that are the big catalyst for change on where they’re going to get care, how they want to receive care. It’s the employers that are going to be making those decisions as purchasers themselves.

Bonnette: I agree and they’re the ultimate payers. For most commercial insurance employers are the ultimate payers, not the insurance companies. And it’s a cost of care share for patients, but the majority of the money comes from the employers. So it’s basically cutting into their profits.

Woods: We are on the same page, but I’m going to be honest, I’m not sure that all of our listeners are right. We’re talking about why these changes could happen soon, but when I have conversations with folks, they still think about a future of a more consolidated hospital, a more outpatient focused practice is something that is coming but is still far enough in the future that there’s some time to prepare for.

I guess my question is what do you say to that pushback? And are there any inflection points that you’re watching for that would really need to hit for this kind of change to hit all hospitals, to be something that we see across the industry?

Bonnette: So when I look at hospitals in general, I don’t see them as much different than they were 20 years ago. We have talked about this movement for a long time, but hospitals are dragging their feet and realistically it’s because they still get paid the same way until we start thinking about how we pay differently or refuse to pay for certain kinds of things in a hospital setting, the inertia is such that they’re going to keep doing it.

Again, I think the push from employers and most likely the brokers are going to force this change sooner rather than later, but that’s still probably between three and five years because there’s so much inertia in health care.

On the other hand, we are hitting sort of an unsustainable phase of cost. The other thing that people don’t talk about very much that I think is important is there’s only so many dollars that are going to health care.

And if you look at the last 10 years, the growth in pharmaceutical spend has to eat into the dollars available for everybody else. So a pharmaceutical spend is growing much faster than anything else, the dollars are going to come out of somebody’s hide and then next logical target is the hospital.

Woods: And we talked last week about how slim hospital margins are, how many of them are actually negative. And what we didn’t mention that is top of mind for me after we just come out of this election is that there’s actually not a lot of appetite for the government to step in and shore up hospitals.

There’s a lot of feeling that they’ve done their due diligence, they stepped in when they needed to at the beginning of the Covid crisis and they shouldn’t need to again. That kind of savior is probably not their outside of very specific circumstances.

Bonnette: I agree. I think it’s highly unlikely that the government is going to step in to rescue hospitals. And part of that comes from the perception about pricing, which I’m sure Congress gets lots of complaints about the prices from hospitals.

And in addition, you’ll notice that the for-profit hospitals don’t have negative margins. They may not be quite as good as they were before, but they’re not negative, which tells me there’s an operational inefficiency in the not for-profit hospitals that doesn’t exist in the for-profits.

Woods: This is where I wanted to go next. So let’s say that a hospital, a health system decides the new path forward is to become smaller, to become cheaper, to become more streamlined, and to decide what specifically needs to happen in the hospital versus elsewhere in our organization.

Maybe I know where you’re going next, but do you have an example of an organization who has had this success already that we can learn from?

Bonnette: Not in the not-for-profit section, no. In the for-profits, yes, because they have already started moving into ambulatory surgery centers. So Tenet has a huge practice of ambulatory surgery centers. It generates high margins.

So, I used to run ambulatory surgery centers in a for-profit system. And so think about ASCs get paid half as much as a hospital for a procedure, and my margin on that business in those ASCs was 40% to 50%. Whereas in the hospital the margin was about 7% and so even though the total dollars were less, my margin was higher because it’s so much more efficient. And the for-profits already recognize this.

Woods: And I’m guessing you’re going to tell me you want to see not-for-profit hospitals make these moves too? Or is there a different move that they should be making?

Bonnette: No, I think they have to. I think there are things beyond just ASCs though, for example, medical patients who can be treated at home should not be in the hospital. Most not-for-profits lose money on every medical admission.

Now, when I worked for a for-profit, I didn’t lose money on every Medicare patient that was a medical patient. We had a 7% margin so it’s doable. Again, it’s efficiency of care delivery and it’s attention to detail, which sometimes in a not-for-profit friends, that just doesn’t happen.

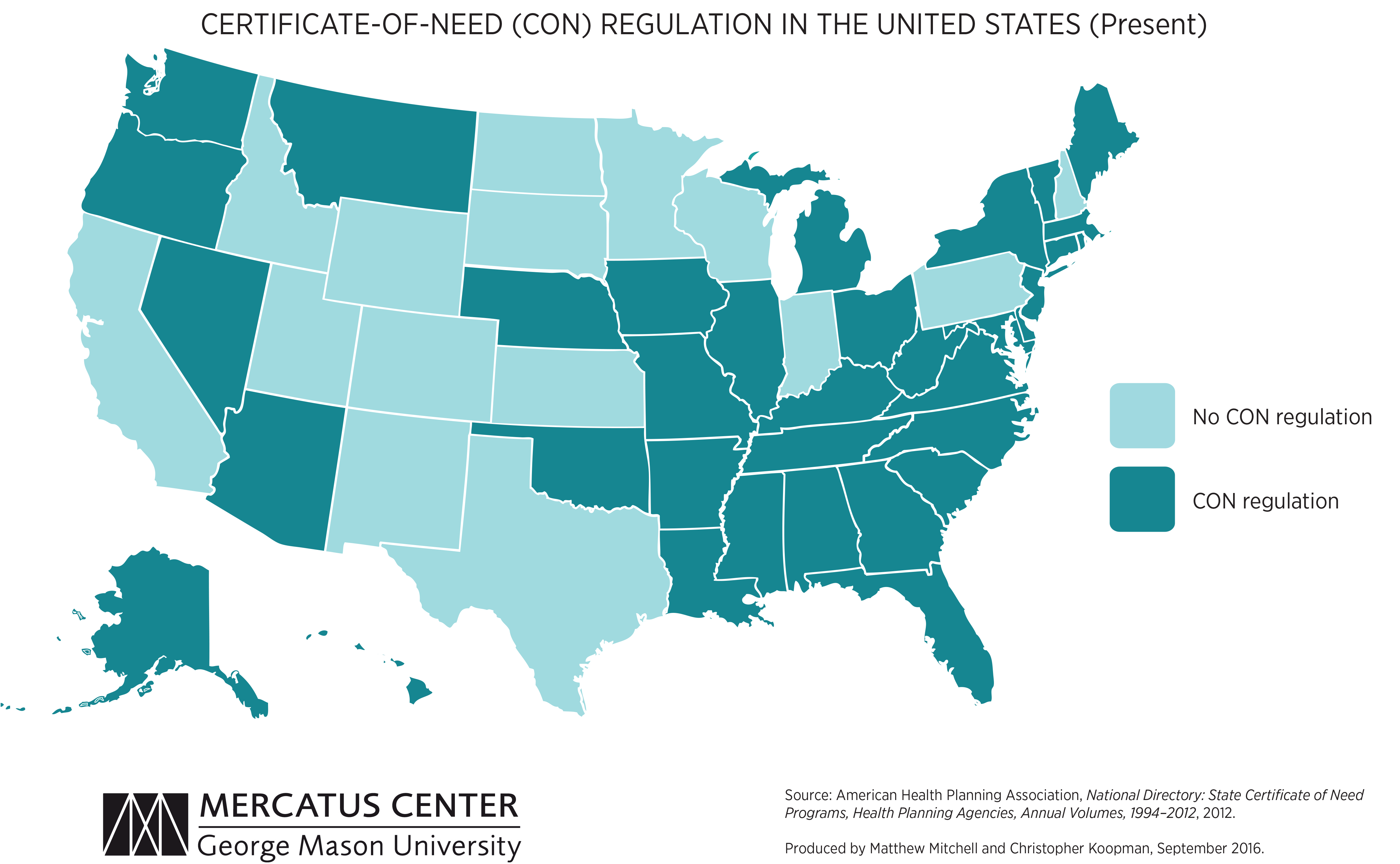

We’re picking up on a growing concern among health system leaders that many states with “certificate of need” (CON) laws in effect are on the cusp of repealing them. CON laws, currently in place in 35 states and the District of Columbia, require organizations that want to construct new or expand existing healthcare facilities to demonstrate community need for the additional capacity, and to obtain approval from state regulatory agencies. While the intent of these laws is to prevent duplicative capacity, reduce unnecessary utilization, and control cost growth, critics claim that CON requirements reduce competition—and free market-minded state legislators, particularly in the South and Midwest, have made them a target.

One of our member systems located in a state where repeal is being debated asked us to facilitate a scenario planning session around CON repeal with system and physician leaders. Executives predicted that key specialty physician groups would quickly move to build their own ambulatory surgery centers, accelerating shift of surgical volume away from the hospital.

The opportunity to expand outpatient procedure and long-term care capacity would also fuel investment from private equity, which have already been picking up in the market. An out-of-market health system might look to build microhospitals, or even a full-service inpatient facility, which would be even more disruptive.

CON repeal wasn’t all downside, however; the team identified adjacent markets they would look to enter as well. The takeaway from our exercise: in addition to the traditional response of flexing lobbying influence to shape legislative change, the system must begin to deliver solutions to consumers that are comprehensive, convenient, and competitively priced—the kind of offerings that might flood the market if CON laws were lifted.