As the economic situation has worsened over the past few months, we’ve been working with several health systems to recalibrate strategy. For many, the anticipated “post-COVID recovery” period has turned into a struggle to reverse declining (often negative) margins, while still scrambling to address mounting workforce shortages. All this amid continued pressure from disruptive competitors and ever-rising consumer expectations.

In the graphic above, we’ve pulled together some of the most important changes we believe health systems need to make. These range from improvements to the operating model (shifting to a team-based approach to staffing, greater use of automation where appropriate, and moving to asset-light capital strategies) to transformations of the clinical model (moving care into lower-cost outpatient and community settings, integrating virtual care into clinical delivery, and creating tighter alignment with key physicians).

In general, the goal is to deliver lower-cost care in less expensive settings, using less expensive staff.

But those cost-saving strategies will need to be coupled with a new go-to-market approach, including new payment models that reward systems for shifting away from high-cost (and highly reimbursed) care models.

Employers and consumers will expect more solution-based offerings, which integrate care across the continuum into coherent bundles of service. This will require a more deliberate focus on service line strategies, moving away from a fragmented, inpatient-centric model.

Contracting approaches must align payment with this shift, changing incentives to reward coordinated, cost-effective, outcomes-driven care.

A key insight from our discussions with health system leaders: short-term cost-cutting initiatives to “stop the bleed” won’t suffice—instead, more permanent solutions will be required that address not only the core operating model, but also the approach to revenue generation.

The post-COVID environment is turning out to be a lot tougher than many had expected, to say the least.

The digital platform is designed to provide consumers with a coordinated healthcare experience across care settings. It’s being sold to Aetna’s fully insured and self-insured plan sponsors, as well as CVS Caremark clients, and is due to go live next year. According to CVS Health, the new offering “enables consumers to choose care when and where they want,” whether that’s virtually, in a retail setting (including at a MinuteClinic or HealthHUB), or through at-home services.

Patients will have access to primary care, on-demand care, medication management, chronic condition management, and mental health services, as well as help in identifying other in-network care providers.

The Gist: CVS Health has been working to integrate its retail clinics, care delivery assets, and health insurance business. This new virtual-first care platform is aimed at coordinating care and experience across the portfolio, and streamlining how individuals access the range of services available to them.

CVS is not alone in focusing here: UnitedHealth Group, Cigna, and others have announced virtual-first health plans with a similar value proposition. Any payer or provider who aims to own the consumer relationship must field a similar digital care platform that streamlines and coordinates service offerings, lest they find themselves in a market where many patients turn first to CVS and other disruptors for their care needs.

Hospital systems can employ artificial intelligence to reduce the types of health inequities that have made communities of color more vulnerable to COVID-19, the leader of one of the nation’s largest health systems says.

“At Northwell Health, New York’s largest health system, we know health disparities will only grow worse if we don’t move more quickly to identify and correct them,” Michael Dowling, president and CEO of New Hyde Park-based Northwell Health, wrote in a May 11 news release with Tom Manning, chair of Ascertain, an AI venture between Northwell and Aegis Ventures. “To do that, we have turned to AI to disrupt this future.”

For instance, health systems can utilize AI to forecast which expectant mothers could benefit from early intervention and specialized care to treat preeclampsia, a pregnancy complication characterized by high blood pressure that affects Black women at three times the rate of white women, the executives wrote.

Organizations can also use health screenings and predictive models to determine which patients are most likely to develop chronic health conditions such as obesity, diabetes and hypertension, the men wrote. In addition, systems should diligently research AI health care applications, such as the National Institutes of Health’s All of Us initiative, which seeks to obtain health data from a representative sample of the U.S. population.

Dowling and Manning noted that health systems must also commit to high standards of data integrity outlined by the U.S. Food and Drug Administration and apply the Hippocratic oath to AI to make sure it does not widen health inequities.

The explosion of apps, wearables, and other health tech solutions targeted at employers has overwhelmed and frustrated many HR executives who make decisions about employee health benefits. At a recent convening of health insurance brokers we participated in, several bemoaned the challenge of helping their clients understand which solutions might bring real value.

One shared, “For the past few years, it’s felt like ‘App-apalooza’ out there. CHROs [chief human resource officers] get pitches for new apps every day…there are literally thousands out there saying they’ll reduce costs and improve employee health, but it’s next to impossible to tell which ones of them actually work.”

Brokers expressed surprise at how little evidence, or in some cases, actual patient and client experience, some health tech companies brought to the table: “We have startups coming to our clients talking about their millions of dollars in funding, but when you dig into what they’re actually doing, not only can they not show outcomes data, you find out they’ve only worked with a few dozen patients!”

But among the sea of apps purporting to manage any and every employee health need, from chronic disease to fertility to sleep quality, brokers reported their clients were finding value in a few distinct areas.

Technology-based mental health solutions received high marks for increasing access to care, with the prediction that “tele-behavioral health could become a standard part of most benefits packages very quickly”.

More surprisingly, employers shared positive feedback on the impact of virtual physical therapy solutions: “I was skeptical that it would work, but people like being able to rehab at home. And not only is it cheaper, we’re seeing higher adherence rates.”

But even the best apps are often challenged by a lack of connectivity to the rest of a patient’s healthcare. The technologies that will have the greatest staying power will be those that not only deliver results, but are able to move beyond point solutions to become part of an integrated care experience, meaningfully connected to other providers involved in a patient’s care.

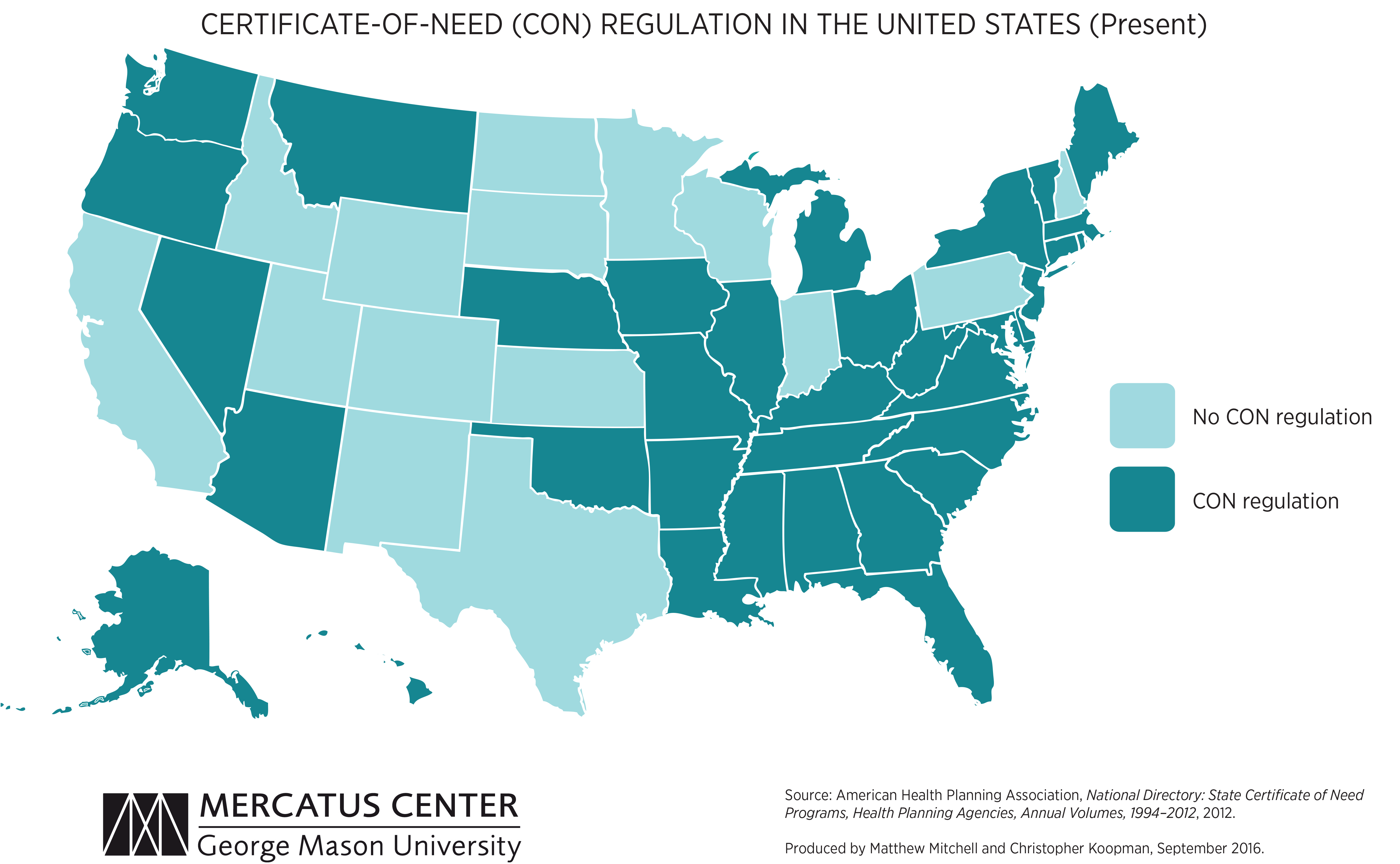

We’re picking up on a growing concern among health system leaders that many states with “certificate of need” (CON) laws in effect are on the cusp of repealing them. CON laws, currently in place in 35 states and the District of Columbia, require organizations that want to construct new or expand existing healthcare facilities to demonstrate community need for the additional capacity, and to obtain approval from state regulatory agencies. While the intent of these laws is to prevent duplicative capacity, reduce unnecessary utilization, and control cost growth, critics claim that CON requirements reduce competition—and free market-minded state legislators, particularly in the South and Midwest, have made them a target.

One of our member systems located in a state where repeal is being debated asked us to facilitate a scenario planning session around CON repeal with system and physician leaders. Executives predicted that key specialty physician groups would quickly move to build their own ambulatory surgery centers, accelerating shift of surgical volume away from the hospital.

The opportunity to expand outpatient procedure and long-term care capacity would also fuel investment from private equity, which have already been picking up in the market. An out-of-market health system might look to build microhospitals, or even a full-service inpatient facility, which would be even more disruptive.

CON repeal wasn’t all downside, however; the team identified adjacent markets they would look to enter as well. The takeaway from our exercise: in addition to the traditional response of flexing lobbying influence to shape legislative change, the system must begin to deliver solutions to consumers that are comprehensive, convenient, and competitively priced—the kind of offerings that might flood the market if CON laws were lifted.

Insurers, retailers, and other healthcare companies vastly exceed health system scale, dwarfing even the largest hospital systems. The graphic above illustrates how the largest “mega-systems” lag other healthcare industry giants, in terms of gross annual revenue.

Amazon and Walmart, retail behemoths that continue to elbow into the healthcare space, posted 2021 revenue that more than quintuples that of the largest health system, Kaiser Permanente. The largest health systems reported increased year-over-year revenue in 2021, largely driven by higher volumes, as elective procedures recovered from the previous year’s dip.

However, according to a recent Kaufman Hall report, while health systems, on average, grew topline revenue by 15 percent year-over-year, they face rising expenses, and have yet to return to pre-pandemic operating margins.

Meanwhile, the larger companies depicted above, including Walmart, Amazon, CVS Health, and UnitedHealth Group, are emerging from the pandemic in a position of financial strength, and continue to double down on vertical integration strategies, configuring an array of healthcare assets into platform businesses focused on delivering value directly to consumers.

The Mark Cuban Cost Plus Drug Co. launched its online pharmacy in January, offering low-cost versions of high-cost generic drugs. And it all started with a cold email.

Alex Oshmyansky, MD, PhD, fired off an email to Mr. Cuban with a simple subject line: “Cold pitch.” The then 33-year-old radiologist told Mr. Cuban about work he was doing in Denver with a compounding pharmacy and the business plan behind a company he founded in 2018, Osh’s Affordable Pharmaceuticals.

“I asked him a simple question, because this was when the whole pharma bro thing was going down,” Mr. Cuban said on NPR podcast The Limits, referring to convicted felon Martin Shkreli. “I was like, ‘Look, if this guy can jack up the prices 750 percent for lifesaving medicines, can we go the opposite direction? Can we cut the pricing? Are there inefficiencies in this industry that really allow us to do it and really make a difference?'”

Dr. Oshmyansky answered yes. Their weekly email correspondence continued for months. The Mark Cuban Cost Plus Drug Co. was quietly founded in May 2020, and Dr. Oshmyansky now serves as its CEO. The company is organized as a public-benefit corporation, meaning it is for-profit but claims its social mission of improving public health is just as important as the bottom line.

“We basically created a vertically integrated manufacturing company that will start with generic drugs,” Mr. Cuban told NPR. A major component of the strategy is to bypass pharmacy benefit managers, which Mr. Cuban likens to bouncers at a club.

“They’re the ones who say, ‘Hey, I’m controlling access to all the big insurance companies. If you want this insurance company to sell your drug, you’ve got to pay the cover charge. All these drugs pay the cover charge to these PBMs through rebates, and because they’re paying the cover charges, the prices are jacked up,” Mr. Cuban told NPR. “We said we’re going to create our own PBM, we’re going to work directly with the manufacturers, and we’re not going to charge the cover charge.”

The Mark Cuban Cost Plus Drug Co. marks the prices of its drugs up 15 percent, charges a $3 pharmacy fee to pay the pharmacists it works with, and a fee for shipping. “That’s it,” Mr. Cuban said on NPR. “There’s no other added costs. The manufacturers love what we’re doing for that reason.”

Others have set out before to disrupt pharma the way Mr. Cuban and Dr. Oshmyansky intend, but their downfall is cooperating or giving in to the PBMs, the entrepreneur noted.

“People always ask, well why didn’t somebody do this before? The reality is there’s so much money there, it’s hard not to be greedy,” Mr. Cuban said on the podcast. “If you get to any scale at all, those PBMs will start throwing money at you and saying, ‘Look, just play the game.’”

Mr. Cuban has indicated he has no intention to play the game.

“I could make a fortune from this,” Mr. Cuban told Texas Monthlylast fall. “But I won’t. I’ve got enough money. I’d rather f— up the drug industry in every way possible.”

Amazon Care, which contracts with employers, will now deliver its virtual care services nationwide. It also plans to expand its hybrid service offering—in which care is delivered by nurses dispatched to employees’ homes—to more than 20 new cities this year, including San Francisco, Miami, Chicago, and New York City. The company also announced it has secured new contracts with its subsidiary Whole Foods Market, as well as Hilton Hotels, semiconductor manufacturing company Silicon Labs, and staffing and recruiting firm TrueBlue.

The Gist: Amazon Care is looking to differentiate itself with a virtual-first, asset-light, hybrid service offering. But given the slow-moving and complex nature of employee health benefit contracting, Amazon’s recent moves could displace employer-facing point solutions, but present less of a threat to incumbent providers, instead offering a partnership opportunity for downstream care.

Ultimately, Amazon could combine its care delivery offerings with its pharmacy and diagnostics businesses to launch a robust direct-to-consumer offering—should the company find healthcare a lucrative and manageable market.

CVS Health announced it has struck a deal with Medable, a decentralized clinical trial software company, incorporating its offerings into MinuteClinics to help reach more patients for late-stage clinical trials. With over 40 percent of Americans living near a CVS pharmacy, CVS says it can help gather data and manage patients at MinuteClinic locations, and through its home infusion service, Coram. CVS has already cut its teeth in the clinical research space by conducting COVID-19 vaccine and treatment trials and testing home dialysis machines, and said it plans to engage 10M patients and open up to 150 community research sites this year.

The Gist: With this deal, CVS Health joins companies like Verily, Alphabet’s life sciences subsidiary, in taking advantage of patient appetite for clinical trials without regularly traveling to a research center, which became difficult during the pandemic.

Clinical research is a $50B market that has largely revolved around academic medical centers in large urban areas, which could see their dominance of the research business challenged. CVS’s entry into this space could lower the barriers to entry for community health systems to expand into clinical research.

Ultimately, the decentralization of the clinical trials business is a win for patients, especially groups that have historically been under-represented in medical research, including rural and lower-income individuals. They may find participation through a local pharmacy—or even completely virtually from the comfort of their own home—much more accessible, affordable, and convenient.

Massachusetts-based health system Wellforce recently appointed its first ever chief consumer officer, tapping an executive from a well-known sneaker brand.

Christine Madigan joined the health system to lead marketing and consumer engagement, Wellforce announced in January. She comes from New Balance Athletics, where she led the global marketing and brand management organization. Madigan was attracted to what she termed the “challenger brand” because of its nimble innovation strategy and its mission to help people live healthier. “I can’t imagine a more purpose-driven culture than that,” she told Fierce Healthcare.

“As a marketing veteran from consumer products, Christine understands the importance of envisioning and building services around consumer needs. She will be a great asset in improving and modernizing the way consumers engage with the health care industry,” David Storto, Wellforce’s executive vice president and chief strategy and growth officer, said in the announcement.

The move comes amid a rising trend in healthcare: executives sourced from outside the industry, and in particular from consumer brands, to lead innovation strategies. Fierce Healthcare spoke to several, some of whom have been in their roles for years. They agree that while there are many transferrable skills, there is also an advantage to being an outsider.

To Madigan, the core challenge remains the same business to business—understanding who the consumer is and the different ways they engage with one’s brand.

Aaron Martin, chief digital officer at Providence St. Joseph Health, who joined the health system from Amazon in 2016, echoed Madigan. “Bringing the patient focus—what we called at Amazon ‘customer obsession’—to Providence was key,” he told Fierce Healthcare.

Society is bombarded by healthcare marketing messages, Madigan noted. She wants to “drive some simplicity into the process.” While the system is built to provide reactive, acute care, Madigan sees preventive care as just as important. And a crucial part of facilitating that is establishing not only awareness of but trust in a provider. “Every detail matters in what you communicate in an experience,” she said.

And for organizations that don’t innovate, “somebody else is going to disrupt us,” Martin said.

To drive innovation at scale, Martin sees a disciplined strategy as key. At Amazon, that looked like picking an area to impact and measuring the value of closing that gap. Applying that to Providence, Martin worked with the clinical team to discover patients in need of low-acuity care were going to other providers instead of to Providence. So Providence launched ExpressCare, offering virtual appointments to recapture those patients and establish continuity of care.

Like Madigan, Novant’s chief digital and transformation officer Angela Yochem, who has held chief information officer roles at Rent-A-Center and BDP International, believes passive care is not enough to eradicate health inequities. “We’ve optimized for fixing things,” she said of the healthcare system. “I’d like to see the healthcare industry become more engaged continually. We need to understand our patients beyond what their last condition is,” she added, referring to social determinants of health.

“In retail, we used to say that customers shouldn’t have to shop our merchandising organizational chart,” said Prat Vemana, Kaiser Permanente’s chief digital officer, who transitioned in 2019 from chief product and experience officer at The Home Depot. To streamline how patients navigate an already highly fragmented healthcare system, Kaiser starts with the patient and works backward when developing digital experiences.

A challenge in healthcare, Vemana acknowledged, is the lag in data around health outcomes. Whereas in retail, results are immediately visible, healthcare is less straightforward. “We have to develop workarounds to get directional information while waiting to see the results,” he said.

The transformation of the sector won’t happen without diversity of thought and experience, Yochem said. It’s less about hiring from a particular sector and more about hiring from all over. Those people will have seen the potential for consumer engagement and will be able to “apply what we know to be possible,” Yochem said. Without those outsider insights in the insular sector, “you create an echo chamber, because you respond to problems in the same way.”

/cloudfront-us-east-1.images.arcpublishing.com/dmn/TQICJ3WTJZGNXIVCFOVNRM3UPQ.png)