Mississippi, one of the country’s poorest and least healthy states, could soon become the next to expand Medicaid.

Why it matters:

It’s one of several GOP-dominated states that have seriously discussed Medicaid expansion this year, a sign that opposition to the Affordable Care Act coverage program may be softening among some holdouts 10 years after it became available.

A new House speaker who strongly backs expansion and growing fears that the state’s rural hospitals can’t survive without it have kept up momentum in Mississippi’s legislature this year.

As many as 200,000 low-income adults could gain coverage if lawmakers clinch a deal in the closing weeks of the Mississippi session.

State of play:

Mississippi’s House and Senate this week began hashing out differences between two very different plans passed by each chamber.

The House bill is the traditional ACA expansion, extending coverage to adults earning 138% of the federal poverty level, or about $21,000.

The Senate’s version, which leaders have dubbed “lite” expansion, covers people earning up to the poverty line and wouldn’t bring in the more generous federal support available for full expansion.

Both plans include a work requirement, but only the House version would still allow expansion to take effect without it. The Biden administration opposes work rules, but former President Trump could revive them in a second term.

Zoom out:

State lawmakers in Alabama and Georgia gave serious consideration to Medicaid expansion this year, though they ultimately dropped it. Kansas’ Gov. Laura Kelly, a Democrat, is trying again to expand Medicaid, but the GOP-run legislature remains opposed.

Shuttering rural hospitals and an acknowledgementthat the ACA is unlikely to be repealedhave made Republicans more willing to take a closer look at expansion, Politico reported earlier this year.

The fact that the extra federal funding from the ACA expansion could lift state budgets as pandemic aid dries up has also piqued states’ interest, said Joan Alker, executive director of the Georgetown University Center on Children and Families.

Zoom in:

Mississippi’s expansion effort has advanced further than other states this year largely becausenew House Speaker Jason White has made it a priority. Lt. Gov. Delbert Hosemann, who presides over the Senate, has also pushed the issue.

“We see an unhealthy population that’s uncovered. And we see this as the best way” to insure them, White told Mississippi Today this week.

“I just think it’s time for us to realize that there’s not something else coming down the pipe.”

The state’s crumbling health infrastructure has also made expansion more urgent, said Democratic state Sen. Rod Hickman. More than 40% of the state’s 74 rural hospitals are at risk of closing, a report last summer found.

“The dire need of our hospital systems and the state finally recognizing that Medicaid expansion could assist in those issues is what has kind of brought that to the forefront,” he told Axios.

Yes, but:

Republican Gov. Tate Reeves has reportedly pledged to oppose any Medicaid expansion deal that may emerge before the legislature adjourns in early May,so lawmakers would likely need a veto-proof majority to approve an expansion.

Austin Barbour, a Republican strategist who works in Mississippi politics, said he expects lawmakers will reach a deal.

But if they don’t, “I know this will be an issue that’ll pop right back up next session,” he said.

Health system operating margins improved in 2023 after a tumultuous 2022. Increased revenue from rebounding patient volumes helped offset the high costs of labor and supplies for many systems, but some continue to face challenges turning a financial corner.

In a Feb. 21 analysis, Kaufman Hall noted that too many hospitals are losing money but high-performing hospitals are faring far better, “effectively pulling away from the pack.”

Average operating margins have see-sawed over the last 12 months, from a -1.2% low in February 2023 to 5.5% highs in June and December. In February, average operating margins dropped to 3.96% before the Change Healthcare data breach, which has impacted claims processing.

Here are 42 health systems ranked by operating margins in their most recent financial results.

Editor’s note: The following financial results are for the 12 months ending Dec. 31, 2023, unless otherwise stated.

Revenue: $20.55 billion Expenses: $18.31 billion Operating income/loss: $2.5 billion (*Includes grant income and equity in earnings of unconsolidated affiliates) Operating margin: 12.2%

*Results for the first six months ending Dec. 31 Revenue: $2.1 billion Expenses: $2 billion Operating income/loss: $22.9 million Operating margin: 1.1%

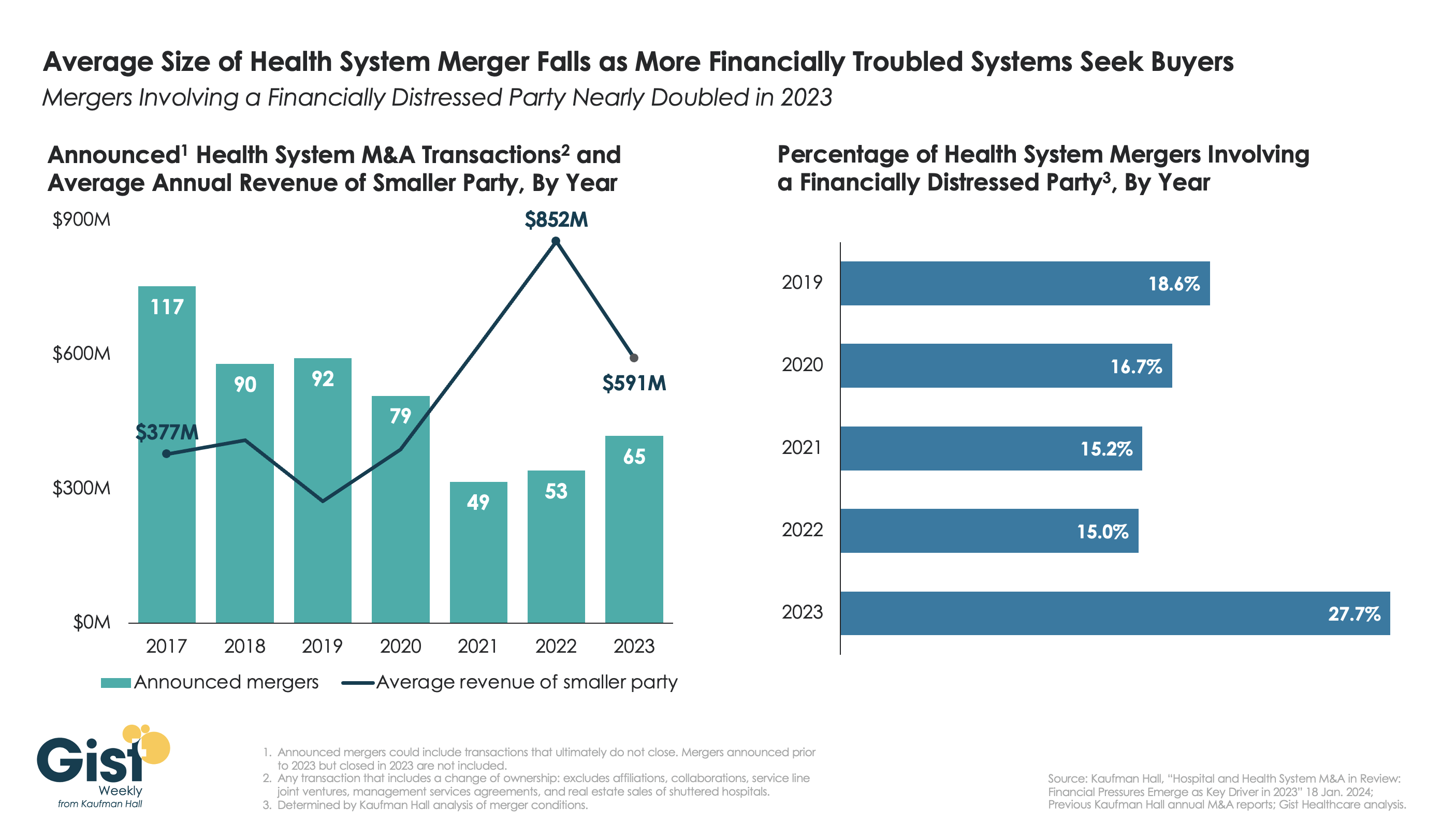

This week’s graphic highlights data from Kaufman Hall’s recently released 2023 Hospital and Health System M&A Report on the current dynamics in health system mergers and acquisitions (M&A) activity.

After a slowdown during the pandemic, 2023 saw an uptick in M&A activity with 65 announced transactions, the most since 2020. Continuing the trend of the past two years, the number of announced “mega mergers,” in which the smaller party had at least $1B in annual revenue, represented more than a tenth of total announced transactions.

However, the average size of mergers fell in 2023, as financial distress emerged as a key driver of M&A activity. The percent of mergers involving a financially distressed party spiked to nearly 28 percent in 2023, almost double the level seen in prior years.

CARES Act funding had buoyed some health systems’ balance sheets through the pandemic, but with the end of federal aid, more systems needed to seek shelter through scale.

With the median hospital operating margin still barely hitting two percent, we anticipate this heightened level M&A activity to continue in 2024 as health systems search for stronger partners that can help them stabilize financially.

On Sunday, Miami, FL-based Cano Health, a Medicare Advantage (MA)-focused primary care clinic operator, filed for bankruptcy protection to reorganize and convert around $1B of secured debt into new debt.

The company, which went public in 2020 via a SPAC deal worth over $4B, has now been delisted from the New York Stock Exchange. After posting a $270M loss in Q2 of 2023, Cano began laying off employees, divesting assets, and seeking a buyer. As of Q3 2023, it managed the care of over 300K members, including nearly 200K in Medicare capitation arrangements, at its 126 medical centers.

The Gist:

Like Babylon Health before it, another “tech-enabled” member of the early-COVID healthcare SPAC wave is facing hard times. While the low interest rate-fueled trend of splashy public offerings was not limitedto healthcare, several prominent primary care innovators and “insurtechs” from this wave have struggled, adding further evidence to the adages that healthcare is both hard and difficult to disrupt.

Given that Cano sold its senior-focused clinics in Texas and Nevada to Humana’s CenterWell last fall, Cano may draw interest from other organizations looking to expand their MA footprints.

If you’re a U.S. health industry watcher, it would appear the $4.5 trillion system is under fire at every corner.

Pressures to lower costs, increase accessibility and affordability to all populations, disclose prices and demonstrate value are hitting every sector. Complicating matters, state and federal legislators are challenging ‘business as usual’ seeking ways to spend tax dollars more wisely with surprisingly strong bipartisan support on many issues. No sector faces these challenges more intensely than hospitals.

In 2022 (the latest year for NHE data from CMS), hospitals accounted for 30.4% of total spending ($1.35 trillion. While total healthcare spending increased 4.1% that year, hospital spending was up 2.2%–less than physician services (+2.7%), prescription drugs (+8.4%), private insurance (+5.9%) and the overall inflation rate (+6.5%) and only slightly less than the overall economy (GDP +1.9%). Operating margins were negative (-.3%) because operating costs increased more than revenues (+7.7% vs. 6.5%) creating deficits for most. Hardest hit: the safety net, rural hospitals and those that operate in markets with challenging economic conditions.

In 2023, the hospital outlook improved. Pre-Covid utilization levels were restored. Workforce tensions eased somewhat. And many not-for-profits and investor-owned operators who had invested their cash flows in equities saw their non-operating income hit record levels as the S&P 500 gained 26.29% for the year.

In 2024, the S&P is up 5.15% YTD but most hospital operators are uncertain about the future, even some that appear to have weathered the pandemic storm better than others. A sense of frustration and despair is felt widely across the sector, especially in critical access, rural, safety net, public and small community hospitals where long-term survival is in question.

The cynicism felt by hospitals is rooted in four conflicts in which many believe hospitals are losing ground:

Hospitals vs. Insurers:

Insurers believe hospitals are inefficient and wasteful, and their business models afford them the role of deciding how much they’ll pay hospitals and when based on data they keep private. They change their rules annually to meet their financial needs. Longer-term contracts are out of the question. They have the upper hand on hospitals.

Hospitals take financial risks for facilities, technologies, workforce and therapies necessary to care. Their direct costs are driven by inflationary pressures in their wage and supply chains outside their control and indirect costs from regulatory compliance and administrative overhead, Demand is soaring. Hospital balance sheets are eroding while insurers are doubling down on hospital reimbursement cuts to offset shortfalls they anticipate from Medicare Advantage. Their finances and long-term sustainability are primarily controlled by insurers. They have minimal latitude to modify workforces, technology and clinical practices annually in response to insurer requirements.

Hospitals vs. the Drug Procurement Establishment:

Drug manufacturers enjoy patent protections and regulatory apparatus that discourage competition and enable near-total price elasticity. They operate thru a labyrinth of manufacturers, wholesalers, distributors and dispensers in which their therapies gain market access through monopolies created to fend-off competition. They protect themselves in the U.S. market through well-funded advocacy and tight relationships with middlemen (GPOs, PBMs) and it’s understandable: the global market for prescription drugs is worth $1.6 trillion, the US represents 27% but only 4% of the world population.

And ownership of the 3 major PBMs that control 80% of drug benefits by insurers assures the drug establishment will be protected.

Prescription drugs are the third biggest expense in hospitals after payroll and med/surg supplies. They’re a major source of unexpected out-of-pocket cost to patients and unanticipated costs to hospitals, especially cancer therapies. And hospitals (other than academic hospitals that do applied research) are relegated to customers though every patient uses their products.

Prescription drug cost escalation is a threat to the solvency and affordability of hospital care in every community.

Hospitals vs. the FTC, DOJ and State Officials:

Hospital consolidation has been a staple in hospital sustainability and growth strategies. It’s a major focus of regulator attention. Horizontal consolidation has enabled hospitals to share operating costs thru shared services and concentrate clinical programs for better outcomes. Vertical consolidation has enabled hospitals to diversify as a hedge against declining inpatient demand: today, 200+ sponsor health insurance plans, 60% employ physicians directly and the majority offer long-term, senior care and/or post-acute services. But regulators like the FTC think hospital consolidation has been harmful to consumers and third-party data has shown promised cost-savings to consumers are not realized.

Federal regulators are also scrutinizing the tax exemptions afforded not-for-profit hospitals, their investment strategies, the roles of private equity in hospital prices and quality and executive compensation among other concerns. And in many states, elected officials are building their statewide campaigns around reining in “out of control” hospitals and so on.

Bottom line: Hospitals are prime targets for regulators.

Hospitals vs. Congress:

Influential members in key House and Senate Committees are now investigating regulatory changes that could protect rural and safety net hospitals while cutting payments to the rest. In key Committees (Senate HELP and Finance, House Energy and Commerce, Budget), hospitals are a target. Example: The Lower Cost, More Transparency Act passed in the the House December 11, 2023. It includes price transparency requirements for hospitals and PBMs, site-neutral payments, additional funding for rural and community health among more. The American Hospital Association objected noting “The AHA supports the elimination of the Medicaid disproportionate share hospital (DSH) reductions for two years. However, hospitals and health systems strongly oppose efforts to include permanent site-neutral payment cuts in this bill. In addition, the AHA has concerns about the added regulatory burdens on hospitals and health systems from the sections to codify the Hospital Price Transparency Rule and to establish unique identifiers for off-campus hospital outpatient departments (HOPDs).” Nonetheless, hospitals appear to be fighting an uphill battle in Congress.

Hospitals have other problems:

Threats from retail health mega-companies are disruptive. The public’s trust in hospitals has been fractured. Lenders are becoming more cautious in their term sheets. And the hospital workforce—especially its doctors and nurses—is disgruntled. But the four conflicts above seem most important to the future for hospitals.

However, conflict resolution on these is problematic because opinions about hospitals inside and outside the sector are strongly held and remedy proposals vary widely across hospital tribes—not-for profits, investor-owned, public, safety nets, rural, specialty and others.

Nonetheless, conflict resolution on these issues must be pursued if hospitals are to be effective, affordable and accessible contributors and/or hubs for community health systems in the future. The risks of inaction for society, the communities served and the 5.48 million (NAICS Bureau of Labor 622) employed in the sector cannot be overstated. The likelihood they can be resolved without the addition of new voices and fresh solutions is unlikely.

PS: In the sections that follow, citations illustrate the gist of today’s major message: hospitals are under attack—some deserved, some not. It’s a tough business climate for all of them requiring fresh ideas from a broad set of stakeholders.

PS If you’ve been following the travails of Mission Hospital, Asheville NC—its sale to HCA Healthcare in 2019 under a cloud of suspicion and now its “immediate jeopardy” warning from CMS alleging safety and quality concerns—accountability falls squarely on its Board of Directors. I read the asset purchase agreement between HCA and Mission: it sets forth the principles of operating post-acquisition but does not specify measurable ways patient safety, outcomes, staffing levels and program quality will be defined. It does not appear HCA is in violation with the terms of the APA, but irreparable damage has been done and the community has lost confidence in the new Mission to operate in its best interest. Sadly, evidence shows the process was flawed, disclosures by key parties were incomplete and the hospital’s Board is sworn to secrecy preventing a full investigation.

The lessons are 2 for every hospital:

Boards must be prepared vis a vis education, objective data and independent counsel to carry out their fiduciary responsibility to their communities and key stakeholders. And the business of running hospitals is complex, easily prone to over-simplification and misinformation but highly important and visible in communities where they operate.

Business relationships, price transparency, board performance, executive compensation et al can no longer to treated as private arrangements.

On Monday, Fitch Ratings, the New York City-based credit rating agency, released a report predicting that the US not-for-profit hospital sector will see average operating margins reset in the one-to-two percent range, rather than returning to historical levels of above three percent.

Following disruptions from the pandemic that saw utilization drop and operating costs rise, hospitals have seen a slower-than-expected recovery.

But, according to Fitch, these rebased margins are unlikely to lead to widespread credit downgrades as most hospitals still carry robust balance sheets and have curtailed capital spending in response.

The Gist:As labor costs stabilize and volumes return, the median hospital has been able to maintain a positive operating margin for the past ten months.

But nonprofit hospitals are in a transitory period, one with both continued challenges—including labor costs that rebased at a higher rate and ongoing capital restraints—and opportunities—including the increase in outpatient demand, which has driven hospital outpatient revenue up over 40 percent from 2020 levels.

While the future margin outlook for individual hospitals will depend on factors that vary greatly across markets, organizations that thrive in this new era will be the ones willing to pivot, take risks, and invest heavily in outpatient services.

The physician-led healthcare network formed to save hospitals from financial distress. Now, hospitals in its own portfolio need bailing out after years of alleged mismanagement.

Steward Health Care formed over a decade ago when a private equity firm and a CEO looking to disrupt a regional healthcare environment teamed up to save six Boston-based hospitals from the brink of financial collapse. Since that time, Steward has expanded from a handful of facilities to become the largest physician-led for-profit healthcare network in the country, operating 33 community hospitals in eight states, according to its own corporate site.

However, Steward has also found itself once again on the precipice of failure.

Steward’s ongoing issues in Massachusetts have played out in regional media outlets in recent weeks. Massachusetts Gov. Maura Healey warned there would be no bailout for Steward in an interview on WBUR’s Radio Boston.

The Massachusetts Department of Public Health said it is investigating concerns raised about Steward facilities and began conducting daily site inspections at some Steward sites to ensure patient safety beginning Jan. 31.

However, the tide may have begun to change. Steward executives said on Feb. 2 they had secured a deal to stabilize operations and keep Massachusetts hospitals open — for now. Steward will receive bridge financing under the deal and consider transferring ownership of one or more hospitals to other companies, a Steward spokesperson confirmed to Healthcare Dive on Feb. 7.

While politicians welcomed the news, some say Steward’s long term outlook in the state is uncertain. Other politicians sought answers for how a prominent system could seemingly implode overnight.

“I am cautiously optimistic at this point that [Steward] will be able to remain open, because it’s really critical they do,” said Brockton City Councilor Phil Griffin. “But they owe a lot of people a lot of money, so we’ll see.”

However, the business model wasn’t immediately a financial success. Steward didn’t turn a profit between 2011 and 2014, according to a 2015 monitoring report from the Massachusetts attorney general. Instead, Steward’s debt increased from $326 million in 2011 to $413 million at the end of the 2014 fiscal year, while total liabilities ballooned to $1.4 billion in the same period as Steward engaged in real estate sale and leaseback plays.

Under the 2010 deal, Steward agreed to assume Caritas’ debt and carry out $400 million in capital expenditures over four years to upgrade the hospitals’ infrastructure. However, that capital expenditure could come in part from financial engineering, such as monetizing Steward’s own assets, according to Zirui Song, associate professor of health care policy and medicine at the Harvard Medical School who has studied private equity’s impact on healthcare since 2019.

Cerberus did not contribute equity into Steward after making its initial investment of $245.9 million, according to the December 2015 monitoring report. Meanwhile, according to reporting at the time, de la Torre wanted to expand Steward. Steward was on its own to raise funds.

Such deals are typically short-sighted, Song explained. When hospitals sell their property, they voluntarily forfeit their most valuable assets and tend to be saddled with high rent payments.

Healthcare Dive spoke with four workers across Steward’s portfolio who said Steward’s emphasis on the bottom line negatively impacted the company’s operations for years.

Terra Ciurro worked in the emergency department at Steward Health Care-owned Odessa Regional Medical Center in January 2022 as a travel nurse. She recalled researching Steward and being attracted to the fact the company was physician owned.

“I remember thinking, ‘That’s all I need to know. Surely, doctors will have their heart in the right place,’” Ciurro said. “But yeah — that’s not the experience I had at all.”

The emergency department was “shabby, rundown and ill-equipped,” and management didn’t fix broken equipment that could have been hazardous, she said. Nine weeks into her 13-week contract and three hours before Ciurro was scheduled to work, Ciurro said her staffing agency called to cut her contract unceremoniously short. Steward hadn’t paid its bills in six months, and the agency was pulling its nurses, she said she was told.

In Massachusetts, Katie Murphy, president of the Massachusetts Nurses Association, which represents more than 3,000 registered nurses and healthcare professionals who work in eight Steward hospitals, said there were “signals” that Steward facilities had been on the brink of collapse for “well over a year.”

Steward hospitals are often “significantly” short staffed and lack supplies from the basics, like dressings, to advanced operating room equipment, said Murphy. While most hospitals in the region got a handle on staffing and supply shortages in the aftermath of the COVID pandemic, at Steward hospitals shortages “continued to accelerate,” Murphy said.

A review of Steward’s finances by BDO USA, a tax and advisory firm contracted last summer by the health system itself to demonstrate it was solvent enough to construct a new hospital in Massachusetts, showed Steward had a liquidity problem. The health system had few reserves on hand last year to pay down its debts owed to vendors, possibly contributing to the shortages. The operator carried only 10.2 days of cash on hand in 2023. In comparison, most healthy nonprofit hospital systems carried 150 days of cash on hand or more in 2022, according to KFF.

One former finance employee, who worked for Steward beginning around 2018, said that the books were routinely left unbalanced during her tenure. Each month, she made a list of outstanding bills to determine who must be paid and who “we can get away with holding off” and paying later.

Food, pharmaceuticals and staff were always paid, while all other vendors were placed on an “escalation list,” she said. Her team prioritized paying vendors that had placed Steward on a credit hold.

The worker permanently soured on Steward when she said operating room staff had to “make do” without a piece of a crash cart — which is used in the event of a heart attack, stroke or trauma.

She stopped referring friends to Steward facilities, telling them “Don’t go — if you can go anywhere else, don’t go [to Steward], because there’s no telling if they’ll have the supplies needed to treat you.”

Away from regulatory review

Massachusetts officials maintain that it hasn’t been easy to see what was happening inside Steward.

Steward is legally required to submit financial data to the MA Center for Health Information and Analysis (CHIA) and to the Massachusetts Registration of Provider Organizations Program (MA-RPO Program), according to a spokesperson from the Health Policy Commission, which analyzes the reported data. Under the latter requirement, Steward is supposed to provide “a comprehensive financial statement, including information on parent entities and corporate affiliates as applicable.”

However, Steward fought the requirements. During Stuart Altman’s tenure as the chair of the Commission from 2012 to 2022, Altman told Healthcare Dive that the for-profit never submitted documents, despite CHIA levying fines against Steward for non-compliance. Steward even sued CHIA and HPC for relief against the reporting obligations.

Steward is currently appealing a superior court decision and order from June 2023 that required it to comply with the financial reporting requirements and produce audited financial reports that cover the full health system, Mickey O’Neill, communications director for the HPC told Healthcare Dive. As of Feb. 6, Steward’s non-compliance remained ongoing, O’Neill said.

Without direct insight into Steward’s finances, the state was operating at a disadvantage, said John McDonough, professor of the practice of public health at The Harvard T.H. Chan School of Public Health. He added that some regulators saw a crisis coming generally, “but the timing was hard to predict.”

Altman gives his team even more of a pass for not spotting the Steward problem.

“There was no indication while I was there that Steward was in deep trouble,” Altman said. Although Steward was the only hospital system that failed to report financial data to the HPC, that alone had not raised red flags for him. “[CEO] Ralph [de la Torre] was just a very contrarian guy. He didn’t do a lot of things.”

Song and his co-author, Sneha Kannan, a clinical research fellow at Harvard Medical School, are hopeful that in the future, regulatory agencies can make better use of the data they collect annually to track changes in healthcare performance over time. They can potentially identify problem operators before they become crises.

“State legislators, even national legislators, are not in the habit of comparing hospitals’ performances on [quality] measures to themselves over time — they compare to hospitals’ regional partners,” Kannan said. “Legislators, Medicare, [and] CMS has access to that information.”

However, although there’s interest from regulators in scrutinizing healthcare quality more closely — particularly when private equity gets involved — a streamlined approach to analyzing such data is still a “ways off,” according to the pair. For now, all parties interviewed for this piece agreed that the best way to avoid being caught off guard by a failing system was to know how such implosions could occur.

“If there’s a lesson from [Steward],” McDonough ventured, “it is that the entire state health system and state government need to be much more wary of all for-profits.”

Companies grappling with liquidity concerns are looking to cut costs and streamline operations, according to a new survey.

Dive Brief:

Over three-quarters of healthcare chief financial officers expect to see profitability increases in 2024, according to a recent survey from advisory firm BDO USA. However, to become profitable, many organizations say they will have to reduce investments in underperforming service lines, or pursue mergers and acquisitions.

More than 40% of respondents said theywill decrease investments in primary care and behavioral health services in 2024, citing disruptions from retail players. They will shift funds to home care, ambulatory services and telehealth that provide higher returns, according to the report.

Nearly three-quarters of healthcare CFOs plan to pursue some type of M&A deal in the year ahead, despite possible regulatory threats.

Dive Insight:

Though inflationary pressures have eased since the height of the COVID-19 pandemic, healthcare CFOs remain cognizant of managing costs amid liquidity concerns, according to the report.

The firmpolled 100 healthcare CFOs serving hospitals, medical groups, outpatient services, academic centers and home health providers with revenues from $250 million to $3 billion or more in October 2023.

Just over a third of organizations surveyed carried more than 60 days of cash on hand. In comparison, a recent analysis from KFF found that financially strong health systems carried at least 150 days of cash on hand in 2022.

Liquidity is a concern for CFOs given high rates of bond and loan covenant violations over the past year. More than half of organizations violated such agreements in 2023, while 41% are concerned they will in 2024, according to the report.

To remain solvent, 44% of CFOs expect to have more strategic conversations about their economic resiliency in 2024, exploring external partnerships, options for service line adjustments and investments in workforce and technology optimization.

Most organizations are interested in exploring sales, according to the report. Financially struggling organizations are among the most likely to consider deals. Nearly one in three organizations that violated their bond or loan covenants in 2023 are planning a carve-out or divestiture this year. Organizations with less than 30 days of cash on hand are also likely to consider carve-outs.

Organizations will also turn to automation to cut costs. Ninety-eight percent of organizations surveyed had pilotedgenerative AI tools in a bid to alleviate resource and cost constraints, according to the consultancy.

“Healthcare leaders believe AI will be essential to helping clinicians operate at the top of their licenses, focusing their time on patient care and interaction over administrative or repetitive tasks,” authors wrote. Nearly one in three CFOs plan to leverage automation and AI in the next 12 months.

However, CFOs are keeping an eye on the risks. As more data flows through their organizations, they are increasingly concerned about cybersecurity. More than half of executives surveyed said data breaches are a bigger risk in 2024 compared to 2023.

Saltzer Health, a Meridian, ID-based multispecialty group with over 100 providers that’s been owned by Intermountain Health since 2020, shared this week that it will shut down if it cannot find a buyer within the next two months, due to its ongoing financial and economic challenges. Beyond the rising costs of care that have plagued provider organizations across the country, Saltzer leaders pointed to a lack of progress around contracts and market relationships in its Boise, ID service area as contributing factors. The group announced that it’s in active negotiations with other healthcare companies potentially interested in purchasing some of its assets, and is optimistic it can avoid full closure.

Saltzer has experienced several ownership changes in recent years: Intermountain bought the group from development firm Ball Ventures Ahlquist in 2020, which had purchased it from Change Healthcare in 2019. Change acquired it two years prior after a Federal Trade Commission (FTC) challenge led to Saltzer’s divestment from St. Luke’s Health System.

The Gist: It’s notable that Intermountain appears uninterested in continuing to grow its presence as a provider in the Boise market, suggesting the system is opting to instead focus its resources on faster growing markets like Denver, which it unlocked through its purchase of SCL Health in 2022.

Given that the FTC previously signaled opposition to Saltzer’s acquisition by a local health system, and a dominant regional integrated delivery system is no longer interested in the group, a nontraditional buyer—like a vertically integrated payer—may use this as an opportunity to enter the Treasure Valley and attempt to steal market share from Intermountain’s Select Health insurance arm.

Earlier this month, leaders from more than 400 organizations descended on San Francisco for J.P. Morgan‘s 42nd annual healthcare conference to discuss some of the biggest issues in healthcare today. Here’s how Advisory Board experts are thinking about Modern Healthcare’s 10 biggest takeaways — and our top resources for each insight.

How we’re thinking about the top 10 takeaways from JPM’s annual healthcare conference

Following the conference, Modern Healthcare provided a breakdown of the top-of-mind issues attendees discussed.

Here’s how our experts are thinking about the top 10 takeaways from the conference — and the resources they recommend for each insight.

1. Ambulatory care provides a growth opportunity for some health systems

By Elizabeth Orr, Vidal Seegobin, and Paul Trigonoplos

At the conference, many health system leaders said they are evaluating growth opportunities for outpatient services.

However, results from our Strategic Planner’s Survey suggest only the biggest systems are investing in building new ambulatory facilities. That data, alongside the high cost of borrowing and the trifurcation of credit that Fitch is predicting, suggests that only a select group of health systems are currently poised to leverage ambulatory care as a growth opportunity.

Systems with limited capital will be well served by considering other ways to reach patients outside the hospital through virtual care, a better digital front door, and partnerships. The efficiency of outpatient operations and how they connect through the care continuum will affect the ROI on ambulatory investments. Buying or building ambulatory facilities does not guarantee dramatic revenue growth, and gaining ambulatory market share does not always yield improved margins.

While physician groups, together with management service organizations, are very good at optimizing care environments to generate margins (and thereby profit), most health systems use ambulatory surgery center development as a defensive market share tactic to keep patients within their system.

This approach leaves margins on the table and doesn’t solve the growth problem in the long term. Each of these ambulatory investments would do well to be evaluated on both their individual profitability and share of wallet.

On January 24 and 25, Advisory Board will convene experts from across the healthcare ecosystem to inventory the predominant growth strategies pursued by major players, explore considerations for specialty care and ambulatory network development, understand volume and site-of-care shifts, and more. Register here to join us for the Redefining Growth Virtual Summit.

Also, check out our resources to help you plan for shifts in patient utilization:

2. Rebounding patient volumes further strain capacity

By Jordan Peterson, Eliza Dailey, and Allyson Paiewonsky

Many health system leaders noted that both inpatient and outpatient volumes have surpassed pre-pandemic levels, placing further strain on workforces.

The rebound in patient volumes, coupled with an overstretched workforce, underscores the need to invest in technology to extend clinician reach, while at the same time doubling down on operational efficiency to help with things like patient access and scheduling.

For leaders looking to leverage technology and boost operational efficiency, we have a number of resources that can help:

3. Health systems aren’t specific on AI strategies

By Paul Trigonoplos and John League

According to Modern Healthcare, nearly all health systems discussed artificial intelligence (AI) at the conference, but few offered detailed implementation plans and expectations.

Over the past year, a big part of the work for Advisory Board’s digital health and health systems research teams has been to help members reframe the fear of missing out (FOMO) that many care delivery organizations have about AI.

We think AI can and will solve problems in healthcare. Every organization should at least be observing AI innovations. But we don’t believe that “the lack of detail on healthcare AI applications may signal that health systems aren’t ready to embrace the relatively untested and unregulated technology,” as Modern Healthcare reported.

The real challenge for many care delivery organizations is dealing with the pace of change — not readiness to embrace or accept it. They aren’t used to having to react to anything as fast-moving as AI’s recent evolution. If their focus for now is on low-hanging fruit, that’s completely understandable. It’s also much more important for these organizations to spend time now linking AI to their strategic goals and building out their governance structures than it is to be first in line with new applications.

Check out our top resources for health systems working to implement AI:

Digital health companies like Teladoc, R1 RCM, Veradigm, and Talkspace all spoke out about their use of generative AI.

This does not surprise us at all. In fact, we would be more surprised if digital health companies were not touting their AI capabilities. Generative AI’s flexibility and ease of use make it an accessible addition to nearly any technology solution.

However, that alone does not necessarily make the solution more valuable or useful. In fact, many organizations would do well to consider how they want to apply new AI solutions and compare those solutions to the ones that they would have used in October 2022 — before ChatGPT’s newest incarnation was unveiled. It may be that other forms of AI, predictive analytics, or robotic process automation are as effective at a better cost.

Again, we believe that AI can and will solve problems in healthcare. We just don’t think it will solve every problem in healthcare, or that every solution benefits from its inclusion.

During the conference, providers criticized insurers for the rate of denials, Modern Healthcare reports.

Denials — along with other utilization management techniques like prior authorization — continue to build tension between payers and providers, with payers emphasizing their importance for ensuring cost effective, appropriate care and providers overwhelmed by both the administrative burden and the impact of denials on their finances.

Many health plans have announced major moves to reduce prior authorizations and CMS recently announced plans to move forward with regulations to streamline the prior authorization process. However, these efforts haven’t significantly impacted providers yet.

In fact, most providers report no decrease in denials or overall administrative burden. A new report found that claims denials increased by 11.99% in the first three quarters of 2023, following similar double digit increases in 2021 and 2022.

Our team is actively researching the root cause of this discrepancy and reasons for the noted increase in denials. Stay tuned for more on improving denials performance — and the broader payer-provider relationship — in upcoming 2024 Advisory Board research.

For now, check out this case study to see how Baptist Health achieved a 0.65% denial write-off rate.

6. Insurers are prioritizing Star Ratings and risk adjustment changes

By Mallory Kirby

Various insurers and providers spoke about “the fallout from star ratings and risk adjustment changes.”

2023 presented organizations focused on MA with significant headwinds. While many insurers prioritized MA growth in recent years, leaders have increased their emphasis on quality and operational excellence to ensure financial sustainability.

With an eye on these headwinds, it makes sense that insurers are upping their game to manage Star Ratings and risk adjustment. While MA growth felt like the priority in years past, this focus on operational excellence to ensure financial sustainability has become a priority.

We’ve already seen litigation from health plans contesting the regulatory changes that impact the bottom line for many MA plans. But with more changes on the horizon — including the introduction of the Health Equity Index as a reward factor for Stars and phasing in of the new Risk Adjustment Data Validation model — plans must prioritize long-term sustainability.

Check out our latest MA research for strategies on MA coding accuracy and Star Ratings:

Pharmacy benefit manager (PBM) leaders discussed the ways they are preparing for potential congressional action, including “updating their pricing models and diversifying their revenue streams.”

Healthcare leaders should be prepared for Congress to move forward with PBM regulation in 2024. A final bill will likely include federal reporting requirements, spread pricing bans, and preferred pricing restrictions for PBMs with their own specialty pharmacy. In the short term, these regulations will likely apply to Medicare and Medicaid population benefits only, and not the commercial market.

Congress isn’t the only entity calling for change. Several states passed bills in the last year targeting PBM transparency and pricing structures. The Federal Trade Commission‘s ongoing investigation into select PBMs looks at some of the same practices Congress aims to regulate. PBM commercial clients are also applying pressure. In 2023, Blue Cross Blue Shield of California‘s (BSC) decided to outsource tasks historically performed by their PBM partner. A statement from BSC indicated the change was in part due to a desire for less complexity and more transparency.

Here’s what this means for PBMs:

Transparency is a must

The level of scrutiny on transparency will force the hand of PBMs. They will have to comply with federal and state policy change and likely give something to their commercial partners to stay competitive. We’re already seeing this unfold across some of the largest PBMs. Recently, CVS Caremarkand Express Scripts launched transparent reimbursement and pricing models for participating in-network pharmacies and plan sponsors.

While transparency requirements will be a headache for larger PBMs, they might be a real threat to smaller companies. Some small PBMs highlight transparency as their main value add. As the larger PBMs focus more on transparency, smaller PBMs who rely on transparent offerings to differentiate themselves in a crowded market may lose their main competitive edge.

PBMs will have to try new strategies to boost revenue

PBM practice of guiding prescriptions to their own specialty pharmacy or those providing more competitive pricing is a key strategy for revenue. Stricter regulations on spread pricing and patient steerage will prompt PBMs to look for additional revenue levers.

PBMs are already getting started — with Express Scripts reporting they will cut reimbursement for wholesale brand name drugs by about 10% in 2024. Other PBMs are trying to diversify their business opportunities. For example, CVS Caremark’s has offered a new TrueCost model to their clients for an additional fee. The model determines drug prices based on the net cost of drugs and clearly defined fee structures. We’re also watching growing interest in cross-benefitutilization management programs for specialty drugs. These offerings look across both medical and pharmacy benefits to ensure that the most cost-effective drug is prescribed for patients.

At the conference, retailers such as CVS, Walgreens, and Amazon doubled down on their healthcare services strategies.

Typically, disruptors do not get into care delivery because they think it will be easy. Disruptors get into care delivery because they look at what is currently available and it looks so hard — hard to access, hard to understand, and hard to pay for.

Many established players still view so-called disruptors as problematic, but we believe that most tech companies that move into healthcare are doing what they usually do — they look at incumbent approaches that make it hard for customers and stakeholders to access, understand, and pay for care, and see opportunities to use technology and innovative business models in an attempt to target these pain points.

CVS, Walgreens, and Amazon are pursuing strategies that are intended to make it more convenient for specific populations to get care. If those efforts aren’t clearly profitable, that does not mean that they will fail or that they won’t pressure legacy players to make changes to their own strategies. Other organizations don’t have to copy these disruptors (which is good because most can’t), but they must acknowledge why patient-consumers are attracted to these offerings.

For more information on how disruptors are impacting healthcare, check out these resources:

9. Financial pressures remain for many health systems

By Vidal Seegobin and Marisa Nives

Health systems are recovering from the worst financial year in recent history. While most large health systems presenting at the conference saw their finances improve in 2023, labor challenges and reimbursement pressures remain.

We would be remiss to say that hospitals aren’t working hard to improve their finances. In fact, operating margins in November 2023 broke 2%. But margins below 3% remain a challenge for long-term financial sustainability.

One of the more concerning trends is that margin growth is not tracking with a large rebound in volumes. There are number of culprits: elevated cost structures, increased patient complexity, and a reimbursement structure shifting towards government payers.

For many systems, this means they need to return to mastering the basics: Managing costs, workforce retention, and improving quality of care. While these efforts will help bridge the margin gap, the decoupling of volumes and margins means that growth for health systems can’t center on simply getting bigger to expand volumes.

Maximizing efficiency, improving access, and bending the cost curve will be the main pillars for growth and sustainability in 2024.

To learn more about what health system strategists are prioritizing in 2024, read our recent survey findings.

Also, check out our resources on external partnerships and cost-saving strategies:

During the conference, MA insurers reported seeing a spike in utilization driven by increased doctor’s visits and elective surgeries.

These increased medical expenses are putting more pressure on MA insurers’ margins, which are already facing headwinds due to CMS changes in MA risk-adjustment and Star Ratings calculations.

However, this increased utilization isn’t all bad news for insurers. Part of the increased utilization among seniors can be attributed to more preventive care, such as an uptick in RSV vaccinations.

In UnitedHealth Group‘s* Q4 earnings call, CFO John Rex noted that, “Interest in getting the shot, especially among the senior population, got some people into the doctor’s office when they hadn’t visited in a while,” which led to primary care physicians addressing other care needs. As seniors are referred to specialty care to address these needs, plans need to have strategies in place to better manage their specialist spend.