Cartoon – Just Two on the Front Lines Who Checkout Hundreds of People a Day

Another 3.8 million Americans filed for unemployment last week, bringing the total of out-of-work Americans to more than 30 million since the outbreak unfolded.

That presents an opportunity for insurers like Molina that are primarily positioned in Medicaid and Affordable Care Act exchange lines of business. Medicaid coverage is based on income and reserved for low-income Americans and the marketplace, or exchanges, tie coverage to income and financial help for those with incomes below a certain threshold.

Although its membership is likely to swell due to current economic conditions, Molina CEO Joe Zubretsky cautioned investors Friday by saying, “by how much we do not yet know.”

Zubretsky said Medicaid has proven it’s a stress-tested model that works in both robust economies and those in a recession.

So far, through April 27, 950 of Molina’s members have been hospitalized with COVID-19, a small fraction of Molina’s 3.4 million membership base. The average length of stay was about 10 days for these members, but they have not been able to assess the costs per episode yet, executives said Friday.

Its plans in Washington, California and Michigan were most affected. However, its Michigan plans have experienced the highest number of cases.

By business line, Medicare members have experienced the highest percentage of COVID-19 diagnoses followed by Medicaid and marketplace members, in line with reports of the disease disproportionately affecting older Americans.

Molina also said it had entered into a definitive agreement to acquire Magellan Complete Care for $820 million in cash. The deal is expected to close in the first quarter of 2021. The deal gives Molina about 155,000 more members. Last year, Magellan generated more than $2.7 billion in revenue, according to Molina.

Magellan operates in six states, three of which would be new for Molina, including Arizona, Virginia and Massachusetts.

Several large employer groups this week refused to sign on to funding requests they consider a “handout” for hospitals and insurers, according to three people close to the process.

The big picture: Coronavirus spending bills are sharpening tensions between the employers that fund a significant portion of the country’s health care system and the hospitals, doctors and insurers that operate it, Bob reports.

Driving the news: The industry’s most recent request — written primarily by the large hospital and health insurance lobbying groups — focused on a few items for the next coronavirus legislation:

Between the lines: Employers know they get charged a lot more for health care services compared with public insurers, but many weren’t keen about urging Congress to “set up a government program to pay commercial reimbursements,” said an executive at a trade group that represents large corporations.

The other side: Several health care groups that signed the letter dismissed the idea of any disagreement with employers.

As the novel coronavirus pandemic brought business to a halt, the pain rippled outward, blowing up sector after sector. According to a detailed analysis of unemployment claims, no industry was left untouched.

After that first chaotic week of lockdowns mid-March, as officials scrambled to slow the spread of the deadliest pandemic in more than a century, restaurants and theaters saw job losses slow while losses in other sectors, such as construction and supply-chain work, accelerated. Now, it appears the economic upheaval is hitting professional and public-sector jobs that some once regarded as safe.

The Labor Department doesn’t release jobless claims by industry. So, building on the work of economist Ben Zipperer and his colleagues at the Economic Policy Institute, we analyzed industry-specific new unemployment-benefit claims from 14 states that publish them. (For a full list, see the charts below.)

For that, we need to focus in on the weekly changes in jobless claims to distinguish between industries where claims are falling and those where claims are steady or increasing. The data can also help us estimate how the labor market will change in coming months.

(Highest week-to-week change included: accommodation and food services; arts entertainment and recreation; hairdressers, auto mechanics and laundry workers)

The first week of closures slammed headfirst into industries that require the most face-to-face customer contact — America’s hospitality sector. More than 7 percent of all restaurant, hotel and bar workers filed for unemployment in this first week alone.

For public officials looking to enforce social distancing, bars, hotels and movie theaters were obvious targets: They’re discretionary spending and require significant human interaction. Another category, which the government calls “other services” but is primarily made up of hairdressers, auto mechanics and laundry workers, also suffered swift and significant losses.

The number of newly unemployed filers in all these high-contact industries fell off in subsequent weeks, but they remain the biggest casualties of the crisis. And unemployment claims probably understate the pain of lower-earning Americans. Low-wage workers often don’t qualify for benefits because they haven’t spent enough time on the job, or aren’t being paid enough, Zipperer said.

A survey released Tuesday by Zipperer and his colleague Elise Gould implies unemployment numbers may be significantly worse than government statistics show. For every 10 people who successfully applied for unemployment benefits during the crisis, they show, another three or four couldn’t get through the overloaded system, and two more didn’t even apply because the system is too difficult.

(Highest week-to-week change included: manufacturing; construction; retail)

By the second week, the shutdown moved from businesses where the primary danger is interacting with customers to those, like construction and manufacturing, that require in-person interaction with large crews of colleagues.

On March 26, for example, Spokane, Wash.-area custom-cabinet maker Huntwood Industries, laid off around 500 employees, according to Thomas Clouse of the Spokesman-Review. As a manufacturer whose sales depend on the construction industry, it was hit doubly hard by the shutdowns.

“It is a scary time,” Amy Ohms, 37, told Clouse. “It’s kind of unfair. I think construction is essential. There is a lot of uncertainty.”

Manufacturers were among the first publicly traded companies to note travel and supply-chain risks related to the coronavirus outbreak in China in financial filings, according to a separate analysis by Oxford researchers Fabian Stephany and Fabian Braesemann and collaborators in Berlin. By March, manufacturers were noting domestic production issues.

Their analysis also shows that, in the middle of March, concern about the coronavirus and its disease, covid-19, from retail corporations eclipsed that of manufacturers. Indeed, retail struggled mightily in the second week of the crisis. More workers were told to stay home, and folks realized foot traffic was often incompatible with social distancing.

The retail sector wasn’t hit as quickly or as forcefully as food services or entertainment, presumably because the sector includes grocery stores and others who employ workers who were deemed essential.

(Highest week-to-week change included: wholesale trade; retail trade; administrative and waste management)

In the third week, the pain worked its way up the supply chain, as wholesale trade — a sector that includes some sales representatives, truck drivers and freight laborers — got slammed.

In theory, the lockdowns created near-perfect trucking conditions: traffic vanished, diesel keeps getting cheaper and the roads are safer than they have been in decades. Only one problem: There’s not much to haul right now.

Don Hayden, president of Louisville trucking firm M&M Cartage, feared he would have to lay off about 70 percent of his 400 employees — drivers, mechanics and office staff — in early April. Orders from his customers in heavy manufacturing evaporated.

But, just in time, he got a Payroll Protection Program loan through his local bank. He was shocked at how rapidly his loan was approved and the money arrived, and he said the Treasury Department had done an outstanding job.

“We’re good through May and into June,” he said. “We have a good workforce. We’re proud of them. We sure would like to retain them.”

At this point in the crisis, the focus shifted from huge, industry-eviscerating swings in jobless numbers to gradual weekly trends that help us guess where the jobless claims will settle in the weeks and months to come.

As industries fall like dominoes, policymakers need to realize the damage isn’t contained to a few specific sectors, said University of Tennessee economist Marianne Wanamaker, a former member of Trump’s Council of Economic Advisers.

She said there may be a temptation to extend benefits for difficult-to-reopen industries such as food service and hospitality, but “it doesn’t comport with the data because the damage is so widespread. It’s not fair to say, ‘Hotel and restaurant workers, you get these really generous packages and everybody else has to go back to work.’ ”

(Highest week-to-week change included: management; finance and insurance; public administration)

White-collar industries have been shedding jobs since mid-March, albeit at a much lower rate than lower-income sectors. But as losses in low-income sectors subsided, white-collar jobless claims stayed flat or even intensified. By week four, categories that contain managers, bookkeepers, insurance agents and bank tellers saw some of the worst weekly trends of any sector.

On April 9, the online review site Yelp laid off 1,000 workers and furloughed 1,100 more (about a third of its workforce) as traffic on the site plunged while businesses were locked down.

“The physical distancing measures and shelter-in-place orders, while critical to flatten the curve, have dealt a devastating blow to the local businesses that are core to our mission,” CEO Jeremy Stoppelman wrote at the time.

Jane Oates, president of the employment-focused nonprofit organization WorkingNation, used to oversee the Labor Department wing that coordinates unemployment claims and training. “The big difference between coronavirus and the Great Recession is that this has completely stopped the economy across so many sectors,” she said.

During the Great Recession, she and her team had the luxury of flooding support into areas that were being hit hardest in a particular week or month. They went from state to state and industry to industry, putting out fires as they arose.

The Labor Department can’t address individual problems like that during the coronavirus recession, she said, because everybody’s getting shellacked simultaneously.

(Highest week-to-week change included: oil, gas and mining; utilities; public administration)

In the week ending April 18, the most recent for which we have data, we can no longer avoid one of the most ominous trends in the entire analysis: a rise in public-sector layoffs. Utilities, public administration and education services — all of which have close implicit or explicit ties to state and local government, were among the worst-faring sectors on a weekly basis.

To stem the tide of what could be millions of job losses and furloughs, the National League of Cities is pushing for a $250 billion bailout of cities throughout the country, colleague Tony Romm reports.

In Broomfield, Colo., a Denver-area suburb of about 70,000 residents, 235 city and county employees were furloughed on April 22, according to Jennifer Rios in the Broomfield Enterprise.

“The impact of the COVID-19 coronavirus is more significant than any of us could have ever expected for our well-being, as well as our municipal financial stability,” Rios reports that officials wrote in a letter to furloughed employees.“

State and local governments are typically required to balance their budgets. Now that they’re staring down the barrel of a huge tax-revenue shortfall, “these revenue losses are going to cause government budgets to fall and they’re going to lay people off,” Zipperer said.

“You’re seeing the beginnings of a big contraction in the public sector,” he said. “That’s going to be the next huge thing.”

The public sector used to be the bulwark that kept the economy going while the private sector pulled back during a recession, Zipperer said. “Over the last couple of recessions, the public sector hasn’t played that traditional role,” Zipperer said. “As a result, we’ve seen steeper recessions and slower recoveries.”

With an eye on replacing the Affordable Care Act, the Trump administration took one particularly critical action in October 2017. It discontinued cost-sharing reduction subsidy payments to health insurers participating in the ACA marketplaces.

But the response to those cuts was likely not what President Trump expected. State insurance commissioners and insurers used them to make marketplace health plans more affordable.

Premium decreases were large – so large that 4.2 million potential enrollees had the option to purchase a marketplace plan for free in 2019.

These changes made us wonder: Did President Trump’s effort to sabotage the Affordable Care Act backfire? I’m a health economist at the University of Pittsburgh. Along with my colleague David Anderson, a policy expert on the Affordable Care Act, we tried to answer that question shortly after the payment cuts. We discovered that more than 200,000 people, using the Healthcare.gov platform in 2019, gained insurance in 37 states due to the Trump administration’s actions. This finding may even be more important now as massive unemployment from the coronavirus pandemic leads to huge losses of employer-based insurance coverage – and ultimately more people enrolling in the marketplaces.

People who sign up for a plan in the Health Insurance Marketplaces may qualify for two types of subsidies. The first type is the advanced premium tax credit, which reduces the premium paid by the enrollee; lower-income enrollees receive larger premium tax credits. The second type is the cost-sharing reduction subsidy, which decrease deductibles and co-pays.

Premium tax credits may be applied to any marketplace plan, though they’re based on silver plan premiums, which cover 70% of an average enrollee’s health care expenses. Cost-sharing reduction subsidies can only be applied to silver plans; that means qualifying enrollees in less generous bronze plans and more generous gold plans don’t benefit from reduced deductibles and co-pays provided by these subsidies.

When Trump ended those payments, marketplace insurers were suddenly in a bind. They are legally required to provide cost-sharing reduction subsidies to enrollees whether or not the federal government was paying. The expectation: marketplace insurers, forced to make up the lost revenue, would either increase premiums or exit the marketplaces altogether. And Obamacare would implode.

But that’s not what happened. Why did the plans become more affordable? Insurers increased only the premiums of their silver plans. That approach – known as silver loading – did two things. First, the cost of silver plan premiums rose drastically. Second, premium tax credits increased along with premiums. So those enrollees receiving premium tax credits saw no increase in the premiums of their silver plans.

At the same time, non-silver plans became cheaper. Many bronze plans, already costing less, became so cheap they were free after applying premium tax credit subsidies. Lower-income enrollees benefited the most.

In 2019, 4.2 million enrollees could enter the marketplace for free through a zero-dollar bronze plan, largely due to silver loading. Without those zero-premium plans, our analysis showed more than 200,000 lower-income marketplace enrollees would have gone uninsured.

Another 60,000 would have gained insurance had California and New Jersey eliminated regulations that prohibited zero premium plans — and if Indiana, Mississippi and West Virginia had adopted silver loading. Many more likely got coverage in states not included in our study.

All this is clearly not what the Trump administration had in mind when it cut subsidy payments. Other changes to the marketplaces probably masked some coverage gains that occurred. Notably, cuts in the public outreach for Healthcare.gov, along with the elimination of the individual mandate, decreased enrollment. But the popularity of zero premium plans resulting from silver loading likely stopped much of the damage – and Trump’s attempt to destabilize the marketplaces.

Now states can take advantage of the attractiveness of zero premium plans to increase health coverage through the marketplaces. One way: States requiring marketplace insurers to provide extra benefits – again, like California and New Jersey – can pick up the small tab for those extras. For example, California enrollees pay for abortion coverage through a one-dollar monthly premium surcharge. This is not covered by premium tax credits. By shifting premiums from even one dollar to zero dollars, our estimates indicate enrollment would increase by approximately 13% among those with lower incomes.

Another way: States without silver loading should adopt it. This is not a partisan issue. Conservative states – or at least, GOP-controlled states like Alabama, Wyoming and Florida – have silver-loaded. State governments pay nothing, revenue for insurers is increased, and most critically, lower-income Americans are provided with affordable health insurance. Put simply, there’s no downside for states.

The Trump administration is prevented from restricting silver loading through 2021. However, a forthcoming Supreme Court case, Texas v. Azar, may yet repeal the entire ACA. If the court’s conservative majority rules in favor of the GOP plaintiffs, they will put affordable health insurance out of reach for the 11.4 million Americans that purchased health insurance in the marketplaces. They will also eliminate Medicaid coverage for an additional 16.9 million Americans.

If the case succeeds, the uninsured rate could easily surpass levels not seen since the height of the Great Recession. And for millions of Americans, access to health insurance – desperately needed, particularly during the COVID-19 pandemic – will be eliminated.

On the heels of worse-than-anticipated first-quarter GDP data, investors got additional economic data Thursday to reflect the ongoing damage being done to the U.S. economy as a result of the COVID-19 pandemic.

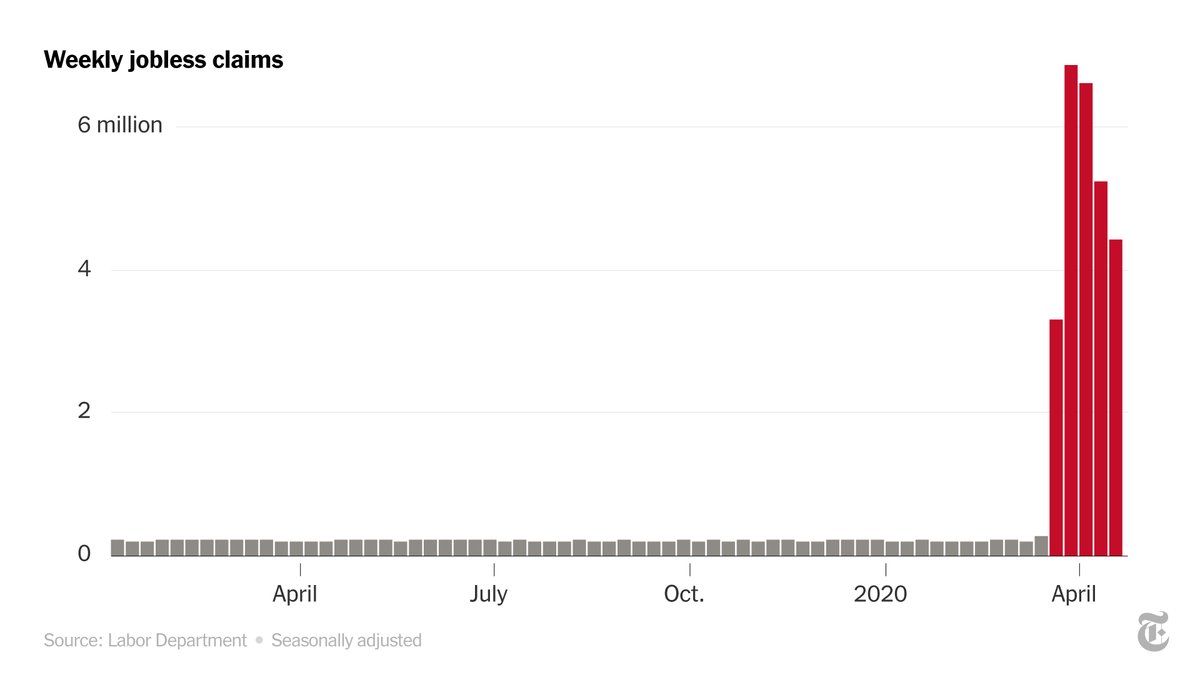

The U.S. Labor Department released its weekly jobless claims figures Thursday morning, and another 3.839 million Americans filed for unemployment benefits during the week ending April 25. Economists were predicting 3.5 million claims for the week, and the prior week’s figure was revised higher to 4.44 million from 4.43 million. In just the previous six weeks, more than 30 million Americans have filed unemployment insurance claims.

Continuing claims, which lags initial jobless claims data by one week, totaled 17.99 million for the week ending April 18. The prior week’s record 15.98 million continuing claims was revised lower to 15.82 million.

“This is the fourth consecutive slowing in the pace of new jobless claims, but it is still horrible and underlines the severe economic consequences of the Covid-19 containment measures,” ING economist James Knightley wrote in a note Thursday.

“The re-opening of some states, including Georgia, Tennessee, South Carolina and Florida, appear to have gone fairly slowly. Consumers remain reluctant to go shopping or visit a restaurant due to lingering COVID-19 fears, while the social distancing restrictions placed on the number of customers allowed in restaurants do not make it economically justifiable for some to open. Evidence so far suggests very little chance of a V-shaped recovery, meaning that unemployment is unlikely to come down anywhere near as quickly as it has been going up,” Knightley added.

Certain states got hit harder than others last week as massive backlogs continued to pile up, and states that implemented shelter-in-place orders later than others saw an increase in claims. For the week ending April 25, Florida saw the highest number of initial jobless claims at an estimated 432,000 on an unadjusted basis, from 507,000 in the prior week. California reported 328,000, down from 528,000 in the previous week. Georgia had an estimated 265,000 and Texas reported 254,000.

While consensus economists anticipate weekly jobless claims will be in the millions in the near term, a continued steady decline is largely expected going forward.

“We expect initial jobless claims to continue to decline on a weekly basis. Many workers affected by closures of nonessential businesses have likely already filed for benefits at this point,” Nomura economist Lewis Alexander wrote in a note April 27. “In addition, the strong demand for Paycheck Protection Program (PPP) loans, part of the CARES Act passed on 27 March, suggests some room for labor market stabilization.”

However, Barclays warned that some recent data indicated that the decline in weekly claims could actually be slower than previously estimated.

“NYC 311 calls in the week ending April 24 were running about 30% higher than a week earlier and support our change in forecast,” Barclays economist Blerina Uruci wrote in a note Wednesday. “In particular, we find it concerning that after declining steadily in recent weeks, the number of calls related to unemployment rose again during the week ending April 24.”

The firm increased its estimate for weekly jobless claims to 4 million from the previously estimated 3.25 million for the week ending April 25. Bank of America also boosted its estimate for claims to 4.1 million from the previously forecast 3.5 million claims.

“Scanning through the local news, we were able to locate information about ten states + DC. We found that claims declined only 2.5% week-to-week NSA [not seasonally adjusted],” Bank of America said in a note Wednesday.

COVID-19 cases recently topped 3.2 million worldwide, according to Johns Hopkins University data. There were more than 1 million cases in the U.S. and 60,000 deaths, as of Thursday morning.

https://www.axios.com/coronavirus-west-virginia-first-case-ac32ce6d-5523-4310-a219-7d1d1dcb6b44.html

The pandemic is a long way from over, and its impact on our daily lives, information ecosystem, politics, cities and health care will last even longer.

The big picture: The novel coronavirus has infected more than 939,000 people and killed over 54,000 in the U.S., Johns Hopkins data shows. More than 105,000 Americans have recovered from the virus as of Sunday.

Lockdown measures: Demonstrators gathered in Florida, Texas and Louisiana Saturday to protest stay-at-home orders designed to protect against the spread of COVID-19, following a week of similar rallies across the U.S.

Catch up quick: Deborah Birx said Sunday that it “bothers” her that the news cycle is still focused on Trump’s comments about disinfectants possibly treating coronavirus, arguing that “we’re missing the bigger pieces” about how Americans can defeat the virus.

With 4.4 million added last week, the five-week total passed 26 million. The struggle by states to field claims has hampered economic recovery.

Nearly a month after Washington rushed through an emergency package to aid jobless Americans, millions of laid-off workers have still not been able to apply for those benefits — let alone receive them — because of overwhelmed state unemployment systems.

Across the country, states have frantically scrambled to handle a flood of applications and apply a new set of federal rules even as more and more people line up for help. On Thursday, the Labor Department reported that another 4.4 million people filed initial unemployment claims last week, bringing the five-week total to more than 26 million.

“At all levels, it’s eye-watering numbers,” Torsten Slok, chief international economist at Deutsche Bank Securities, said. Nearly one in six American workers has lost a job in recent weeks.

Delays in delivering benefits, though, are as troubling as the sheer magnitude of the figures, he said. Such problems not only create immediate hardships, but also affect the shape of the recovery when the pandemic eases.

Laid-off workers need money quickly so that they can continue to pay rent and credit card bills and buy groceries. If they can’t, Mr. Slok said, the hole that the larger economy has fallen into “gets deeper and deeper, and more difficult to crawl out of.”

Hours after the Labor Department report, the House passed a $484 billion coronavirus relief package to replenish a depleted small-business loan program and fund hospitals and testing. The Senate approved the bill earlier this week.

Even as Congress continues to provide aid, distribution has remained challenging. According to the Labor Department, only 10 states have started making payments under the federal Pandemic Unemployment Assistance program, which extends coverage to freelancers, self-employed workers and part-timers. Most states have not even completed the system needed to start the process.

Ohio, for example, will not start processing claims under the expanded federal eligibility criteria until May 15. Recipients whose state benefits ran out, but who can apply for extended federal benefits, will not begin to have their claims processed until May 1.

Pennsylvania opened its website for residents to file for the federal program a few days ago, but some applicants were mistakenly told that they were ineligible after filling out the forms. The state has given no timetable for when benefits might be paid.

Reports of delays, interruptions and glitches continue to come in from workers who have been unable to get into the system, from others who filed for regular state benefits but have yet to receive them, and from applicants who say they have been unfairly turned down and unable to appeal.

Florida has paid just 17 percent of the claims filed since March 15, according to the state’s Department of Economic Opportunity.

“Speed matters” when it comes to government assistance, said Carl Tannenbaum, chief economist at Northern Trust. Speed can mean the difference between a company’s survival and its failure, or between making a home mortgage payment and facing foreclosure.

There is “a race between policy and a pandemic,” Mr. Tannenbaum said, and in many places, it is clear that the response has been “very uneven.”

Using data reported by the Labor Department for March 14 to April 11, the Economic Policy Institute, a liberal research group, estimated that seven in 10 applicants were receiving benefits. That left seven million other jobless workers who had filed claims but were still waiting for relief.

States manage their own unemployment insurance programs and set the level of benefits and eligibility rules. Now they are responsible for administering federal emergency benefits that provide payments for an additional 13 weeks, cover previously ineligible workers and add $600 to the regular weekly check.

So far, 44 states have begun to send the $600 supplement to jobless workers who qualified under state rules, the Labor Department said. Only two — Kentucky and Minnesota — have extended federal benefits to workers who have used up their state allotment.

With government phones and websites clogged and drop-in centers closed, legal aid lawyers around the country are fielding complaints from people who say they don’t know where else to turn.

“Our office has received thousands of calls,” said John Tirpak, a lawyer with the Unemployment Law Project, a nonprofit group in Washington.

People with disabilities and nonnative English speakers have had particular problems, he said.

Even those able to file initially say they have had trouble getting back into the system as required weekly to recertify their claims.

Colin Harris of Marysville, Wash., got a letter on March 31 from the state’s unemployment insurance office saying he was eligible for benefits after being laid off as a quality inspector at Safran Cabin, an aerospace company. He submitted claims two weeks in a row and heard nothing. When he submitted his next claim, he was told that he had been disqualified. He has tried calling more than 200 times since then, with no luck.

“And that’s still where I am right now,” he said, “unable to talk to somebody to find out what the issue is.” If he had not received a $1,200 stimulus check from the federal government, he said, he would not have been able to make his mortgage payment.

Last week’s tally of new claims was lower than each of the previous three weeks. But millions of additional claims are still expected to stream in from around the country over the next month, while hiring remains piddling.

States are frantically trying to catch up. California, which has processed 2.7 million claims over the last four weeks, opened a second call center on Monday. New York, which has deployed 3,100 people to answer the telephone, said this week that it had reduced the backlog that accumulated by April 8 to 4,305 from 275,000.

Florida had the largest increase in initial claims last week, although the state figures, unlike the national total, are not seasonally adjusted. That increase could be a sign that jobless workers finally got access to the system after delays, but it is impossible to assess how many potential applicants have still failed to get in.

The 10 states that have started making Pandemic Unemployment Assistance payments to workers who would not normally qualify under state guidelines are Alabama, Colorado, Iowa, Kentucky, Louisiana, Massachusetts, Rhode Island, Tennessee, Texas and Utah.

Pain is everywhere, but it is most widespread among the most vulnerable.

In a survey that the Pew Research Center released on Tuesday, 52 percent of low-income households — below $37,500 a year for a family of three — said someone in the household had lost a job because of the coronavirus, compared with 32 percent of upper-income ones (with earnings over $112,600). Forty-two percent of families in the middle have been affected as well.

Those without a college education have taken a disproportionate hit, as have Hispanics and African-Americans, the survey found.

An outsize share of jobless claims have also been filed by women, according to an analysis from the Fuller Project, a nonprofit journalism organization that focuses on women.

Josalyn Taylor, 31, learned that she was out of a job on March 16. “I clocked in at 3 o’clock, and by 3:30 my boss called me and told me we were going to shut down for three weeks,” said Ms. Taylor, an assistant manager at Cicis Pizza in Galveston, Tex. The restaurant has yet to reopen.

Two days later, she applied for unemployment insurance, but she kept receiving a message that a claim was already active for her Social Security number and that she could not file. She has tried to clear up the matter hundreds of times — online, by phone and through the Texas Workforce Commission’s site on Facebook — with no luck.

“I used my stimulus check to pay my light bill, and I’m using that to keep groceries and stuff in the house,” said Ms. Taylor, who is five months pregnant. “But other than that, I don’t have any other income, and I’m almost out of money.”

The first wave of layoffs most heavily whacked the restaurant, travel, personal care, retail and manufacturing industries, but the damage has spread to a much broader range of sectors.

At the online job site Indeed, for example, postings for software development jobs are down nearly 30 percent from last year, while listings for finance and banking openings are down more than 40 percent.

New layoffs are expected to ease over the next couple of months, but the damage to the economy is likely to last much longer. In a matter of weeks, the shutdown has more than erased 10 years of net job gains — more than 19 million jobs.

Health and education are going to revive relatively quickly, said Rick Rieder, chief investment officer for global fixed income at BlackRock, but leisure and hospitality are going to take a lot longer.

“A lot of the people who have been furloughed won’t come back,” he said. “Companies will either close or decide not to take back those workers.”

Over the past decade, the employment landscape has shifted substantially as new types of jobs have appeared and old categories have disappeared. The U.S. economy, Mr. Rieder said, is “going to go through another period of evolution.”

The new weekly total comes on top of 22 million Americans who had sought benefits in previous weeks, a volume that has overwhelmed state systems for processing unemployment claims. Economists estimate the national unemployment rate sits between 15 and 20 percent, much higher than it was during the Great Recession in 2008 and 2009. The unemployment rate at the peak of the Great Depression was about 25 percent.

The new weekly jobless claims figure came in around economists’ predictions, which were expected “to be staggering, but not growing, which is a small mercy,” said Julia Pollak, a labor economist at ZipRecruiter. For comparison, 5.2 million people filed unemployment claims for the week ending April 11.

As the coronavirus began spreading in the United States earlier this year, many businesses rapidly began to close. Hotels, restaurants, and airlines were hit particularly hard, but few businesses were immune from the economic toll. The problems have only worsened each week, as more Americans reduced their spending and more businesses cut workers because income has fallen so sharply.

Pollack said many businesses quickly “cut to the bone” when they realized how the pandemic would gut sales. Now, many of the new layoffs stem from businesses like news organizations and tech companies that weren’t directly affected by people staying home but are suffering the consequences of vanishing ad revenue and paid subscriptions.

“We see declines across every major industry and state, although the declines hit industries at different times,” Pollak said.

Meanwhile, consumer spending, the engine behind the longest economic expansion in U.S. history, has evaporated. If they’re still operating, many offices are working with skeleton staffs and staring down months of dismal revenue.

The White House and Congress have tried to intervene, but with limited impact so far.

New funding for small businesses in a $2 trillion March emergency spending package quickly dried up in the face of overwhelming demand, prompting the Senate to expand funding by $310 billion on Tuesday. The bill would direct an additional $60 billion to a separate small-business emergency grant and loan program. The House is slated to vote on the measure Thursday afternoon.

Even with all the new government spending, hopes for a sharp economic rebound are fading, overtaken by the public fear of going back to restaurants, movie theaters, schools and gyms. The growing possibility of a “W”-shaped recovery — in which a resurgence of the virus, or a spike in defaults and bankruptcies, triggers another downturn — has analysts reframing what a reopened or rehabilitated economy might look like.

This year defies historical comparison. In 2020, 28.9 million people have filed for unemployment benefits. Halfway through the fourth month of the year, the figure has already eclipsed the full-year totals of every year but 1982 (30.4 million) and 2009 (29.8 million). At this rate, it will overtake both within a week or so.

Less than half of working-age Americans will be earning a wage next month, said James Knightley, ING Chief International Economist.

“In an election year, this means that the call for politicians to reopen the economy is only going to get louder, irrespective of the health advice,” Knightley said.

In five weeks, 9.4 percent of the working-age population has filed for unemployment insurance, said Nick Bunker, Indeed Hiring Lab’s director of economic research. That’s about twice the share of the population that lost a job during the Great Recession. In some states, such as Michigan, about one in four workers has filed an unemployment claim in the past few weeks.

“The numbers detailing the shock to the U.S. labor market are so large, and cover such a short time, that your first reaction is that they’re a typo,” Bunker said.

Employers are also unlikely to be hiring at the same levels they were before the pandemic. As of April 16, job postings on Indeed were down 34 percent compared with last year, Bunker said.

The job losses, like the epidemic itself, haven’t fallen evenly across the country. In three states — Hawaii, Kentucky and Michigan — about 1 in 4 workers have filed for unemployment benefits in the past 5 weeks. In Michigan, plant shutdowns and furloughs have ravaged the manufacturing economy, which had only recently recovered all the jobs it lost in the Great Recession.

On the opposite of the ledger sits South Dakota, where Gov. Kristi L. Noem (R) has resisted calls to lock down the state’s businesses to slow the spread of the coronavirus. Only 6 percent of the state’s labor force has applied for unemployment benefits. It may be a regional trend: Neighboring Wyoming and Nebraska, and nearby Utah, also have unusually low claims numbers.

As part of its sprawling stimulus package, Washington has rolled out relief for millions of households and small businesses struggling to make ends meet. But money for struggling businesses quickly ran dry, and system glitches have prevented $1,200 stimulus checks from reaching some of the neediest.

On Tuesday, the Senate passed a bill to expand the Paycheck Protection Program for small businesses by $310 billion, and flood a separate small-business emergency grant and loan initiative by an additional $60 billion.

Meanwhile, many low-income veterans and Social Security recipients still haven’t received the stimulus money in their bank accounts, while other IRS checks are going to dead people. People who didn’t file tax returns last year or don’t have direct-deposit information may have weeks more to wait.

In the wake of the Great Recession, the number of unemployed — about 15 million — was significantly higher than the number who claimed benefits, and the unemployment rate still peaked at just 10 percent. Economists expect the United States to blow by that figure when April’s jobs data are released on May 8.

Granted, this comes as unemployment eligibility and benefits have been greatly expanded. The government has relied on the unemployment insurance system to deliver relief to out-of-work Americans as it forces millions of businesses to close during temporary stay-at-home orders. The soaring numbers are, for once, a sign of the system working as intended.