When Jeff Goldsmith and Ian Morrison talk, people listen (apologies to E.F. Hutton…Goldsmith and Morrison are old enough to get that reference, anyway). These two lions of health policy and strategy came together recently to pen an editorial in Health Affairs examining the impact of large integrated health systems on the nation’s response to COVID-19. Morrison and Goldsmith admit to often finding themselves on opposite sides of consolidation issue, but looking back over the past year, both agree the scale systems have built over decades has been foundational to their effective and rapid response to the pandemic, which they rate as “better than just about any other element of our society”.

Larger health systems were able to mobilize the resources to secure protective gear as supplies dwindled.They responded at a speed many would have thought impossible, doubling ICU capacity in a matter of days, and shifting care to telemedicine, implementing their five-year digital strategies during the last two weeks of March.

This kind of innovation would have been impossible without the investments in IT and electronic records enabled by scale—butsystems also exhibited an impressive degree of “systemness”, making important decisions quickly, and mobilizing across regional footprints. Given the financial stresses experienced by smaller providers, consolidation is sure to increase. And the Biden healthcare team will likely bring more scrutiny to health system mergers.

Morrison and Goldsmith urge regulators to reconsider the role of health systems. The government should continue to pursue truly anticompetitive behavior that raises employer and consumer prices. But lawmakers should focus less on the sheer size of health systems and rather on their behavior, considering the potential societal impact a combined system might deliver—and creating policy that takes into account the role health systems have played in bolstering our public health infrastructure.

On Thursday, President Biden signed the American Rescue Plan (ARP) Act of 2021 into law, committing nearly$1.9T of federal spending to boost the nation’s recovery from the coronavirus pandemic. In addition to direct payments to American families, extension of unemployment benefits, several anti-poverty measures, and aid to state and local governments, the plan also contains several key healthcare measures.

Approved by Congress on a near party-line vote using the budget reconciliation process, the law includes thebroadest expansion of the 2010 Affordable Care Act (ACA) to date. It extends subsidies for upper-middle income individuals to purchase coverage on the Obamacare exchanges, caps premiumsfor those higher earners at a substantially lower level, and boosts subsidies for those at the lower end of the income scale.

The Congressional Budget Office (CBO) estimates that expanded ACA subsidies in the ARPwill result in 2.5M more Americans gaining coverage in the next two years. Fully subsidized COBRA coverage for workers who lost their jobs due to COVID is also extended through the end of September, which the CBO estimates will benefit an additional 2M unemployed Americans.

The ARP also puts in place new support for Medicaid, enhancing coverage for home-based care, maternity services, and COVID testing and vaccination, and providing new incentives for the 12 states which haven’t yet expanded Medicaid eligibility under the ACA to do so. In addition to the ACA’s 90 percent match for those states’ Medicaid expansion populations, the lucky dozen will also receive a 5 percent bump to federal matching for the rest of their Medicaid populations should they choose to expand.

Three policy changes of keen interest to providers were left out of the final version of the bill. First, while a special relief fund of $8.5B was created for rural providers, there was no additional allocation of relief funds for hospitals and other providers, similar to the $178B allocated by the CARES Act, despite initial proposals of up to $35B in additional funding. (Around $25B of the initial round of provider relief is still unspent.) Second, the ARPdid not extend or alter the repayment schedule for advance payments to providers made last year, in spite of industry pressure to implement more favorable repayment conditions. Finally, the new law does not extend last year’s pause on sequester-related cuts to Medicare reimbursement, although the House is expected to consider a separate measure to address that issue next week.

Notably, the coverage-related provisions of the ARP are only temporary, lasting through September of next year. That sets up the 2022 midterm elections as yet another campaign cycle dominated by promises to uphold and protect the Affordable Care Act—by then a 12-year-old law bolstered by this week’s COVID recovery legislation.

Many of the Center for Medicare and Medicaid Innovation’s value-based care payment models are undergoing a review, according to the Centers for Medicare & Medicaid Services (CMS).

The statement to Fierce Healthcare comes after CMS quietly updated and delayed several payment models, including pulling a controversial model that ties payments to geographic health outcomes.

“CMS remains steadfast in its commitment to transforming the healthcare system into one that rewards value and care coordination,” the agency said. “The CMS Innovation Center and its alternative payment models help execute that commitment.”

The agency added it hopes to design models that support the adoption of value-based care.

“Many of the CMS Innovation Center’s models are currently under review, and we look forward to providing updates when available,” CMS said.

CMS did not return a request for comment on how many models are under review or which ones are being scrutinized.

The statement comes after CMS has quietly updated the webpages for two payment models to note major changes. The agency made an update to the webpage for the Geographic Direct Contracting Model that said it was currently under review.

A request for applications for the model was posted Jan. 1, and the first performance period was expected to start in 2022 and run through 2024.

The model was intended to improve quality and lower costs for Medicare beneficiaries across a region, and providers in that region can enter into value-based payment arrangements.

Providers can build integrated relationships and invest in population health to better coordinate care, the agency said when the model was released last December.

But the model has gotten pushback from some provider groups. The National Association of Accountable Care Organizations has criticized the model, saying it could confuse patients who may not know whether they are participating in a direct contracting entity.

CMS also quietly pushed back the first performance period for the Kidney Care Choices model, which aims to improve the quality of dialysis care.

The model had an implementation period for 2020 that enabled participants to create the necessary infrastructure for the model, which aims to bundle care from treatment of chronic kidney disease all the way through kidney transplantation and post-transplant care.

Starting Jan. 1, 2021, providers were supposed to start taking on financial accountability including capitated payments.

But CMS posted an update on the webpage for the model, saying the start of the financial performance period will now be Jan. 1, 2022. The agency did not give a reason for the delay.

CMS’ review comes on the heels of a separate analysis conducted under the Trump administration on the value generated by the payment models. The analysis found bundled payment models that gave providers an amount of money for an entire episode of care had mixed results, while global budget models, which give providers a fixed amount for the total number of services given over a certain period of time, were given a more positive review.

It remains unclear whether that analysis is playing any role into the review undertaken by the Biden administration.

The Supreme Court announced Thursday it will no longer hear oral arguments later this month on an appeal over the controversial Medicaid work requirements program in New Hampshire and Arkansas.

Legal experts say the move likely means the case won’t be heard this term and possibly may not be heard at all, especially with the Biden administration signaling a different approach to work requirements.

“By taking the cases off the docket, the court is signaling that it won’t hear them this term and probably that it’ll never hear them at all,” University of Michigan Law Professor Nicholas Bagley told Fierce Healthcare.

A major question mark,though, is whether the court will vacate the decisions by several appellate courts that upheld lower court rulings that the programs should be struck down.

“If the Supreme Court is not going to vacate the D.C. Circuit ruling, that means the decision on the books is one that clearly explains why work requirements are not permitted under the Medicaid statute,” said Rachel Sachs, associate professor of law at Washington University, in an interview with Fierce Healthcare.

She added that it is unlikely for the case to come back and “extremely unlikely that this issue will return in the near future.”

The Biden administration asked the court back in February to cancel the oral arguments originally scheduled for March 29. The administration said in a filing that allowing the requirements to take effect won’t promote the objectives of Medicaid to extend health insurance to low-income people.

President Joe Biden’s Department of Justice called for the court to vacate judgments of appeals courts and remand the case back to the Department of Health and Human Services so it can finish a review of all the waivers.

Arkansas Attorney General Leslie Rutledge said in a statement back in February that the legal filing seeking the delay was a “politically motivated stunt designed to avoid a Supreme Court decision upholding a program that encourages personal responsibility while still providing healthcare coverage for those seeking gainful employment.”

Arkansas’ work requirements program was installed in 2018 and led to approximately 18,000 people losing Medicaid coverage before the program was struck down by a federal judge.

Appellate courts upheld judgments from lower courts that New Hampshire and Arkansas’ programs did not meet the objectives of the Medicaid program. The states appealed to the Supreme Court, which agreed to hear the cases late last year.

Court rulings have also struck down programs in other states including Kentucky and Michigan. Kentucky pulled its program in 2019 after a Democrat was elected governor.

Arkansas and New Hampshire’s attorneys general did not return requests for comment on the Supreme Court’s decision Thursday.

Wealthy nations — including the U.S., the U.K. and the EU — have vaccinated their citizens at a rate of one person per second over the last month, while most developing countries still haven’t administered a single shot, according to the People’s Vaccine Alliance.

Why it matters:As higher-income countries aim to achieve herd immunity in a matter of months, most of the world’s vulnerable people will remain unprotected.

Experts say that mutations that may arise while the virus spreads could be a danger to us all, vaccinated or not.

The big picture: Even though more vaccines will arrive in developing nations soon, only 3% of people in those countries are likely to be vaccinated by mid-2021.

At best, only a fifth of their population will be vaccinated by the end of the year, per the People’s Vaccine Alliance.

What we’re watching: Three dozen countries have bought several times the amount of vaccine that they’ll need to vaccinate their entire population.

The U.S. alone has ordered more than a billion extra doses, Science Magazine reports. Global health leaders are saying it’s time to figure out where all of these excess doses will go.

“Over the next year or two, U.S. surplus doses and those from other countries could add up to enough to immunize everyone in the many poorer nations that lack any secured COVID-19 vaccine,” Science writes.

In their recent Health Affairs paper, Sungchul Park and coauthors examine rates of switching from Medicare Advantage (MA) to traditional Medicare by patient characteristics. MA plans are the private insurance alternative to traditional fee-for-service Medicare overseen by the Centers for Medicare and Medicaid Services. While enrollment in MA has doubled over the past decade, Park and coauthors find that the needs of certain enrollees are not being met by MA plans.

Park and coauthors report that rural enrollees switch from MA to traditional Medicare at an adjusted annual rate of 10.5 percent, significantly higher than metropolitan residents, who switch at a rate of 5.0 percent.

This phenomenon was more pronounced among those who required the use of costly services such as facility stays or hospitalizations, those who had poor self-reported health, and individuals who reported lower satisfaction with their access to care.

The COVID-19 pandemic has accelerated the pace of artificial intelligence adoption, and healthcare leaders are confident AI can help solve some of today’s toughest challenges, including COVID-19 tracking and vaccines.

The majority of healthcare and life sciences executives (82%) want to see their organizations more aggressively adopt AI technology, according to a new survey from KPMG, an audit, tax and advisory services firm.

Healthcare and life sciences (56%) business leaders report that AI initiatives have delivered more value than expected for their organizations. However, life sciences companies seem to be struggling to select the best AI technologies, according to 73% of executives.

As the U.S. continues to navigate the pandemic, life sciences business leaders are overwhelmingly confident in AI’s ability to monitor the spread of COVID-19 cases (94%), help with vaccine development (90%) and aid vaccine distribution (90%).

KPMG’s AI survey is based on feedback from 950 business or IT decision-makers across seven industries, with 100 respondents each from healthcare and life sciences companies.

Despite the optimism about the potential for AI, executives across industries believe more controls are needed and overwhelmingly believe the government has a role to play in regulating AI technology. The majority of life sciences (86%) and healthcare (84%) executives say the government should be involved in regulating AI technology.

And executives across industries are optimistic about the new administration in Washington, D.C., with the majority believing the Biden administration will do more to help advance the adoption of AI in the enterprise.

“We are seeing very high levels of support this year across all industries for more AI regulation. One reason for this may be that, as the technology advances very quickly, insiders want to avoid AI becoming the ‘Wild Wild West.’ Additionally, a more robust regulatory environment may help facilitate commerce. It can help remove unintended barriers that may be the result of other laws or regulations, or due to lack of maturity of legal and technical standards,” said Rob Dwyer, principal, advisory at KPMG, specializing in technology in government.

Healthcare and pharma companies seem to be more bullish on AI than other industries are.

The survey found half of business leaders in industrial manufacturing, retail and tech say AI is moving faster than it should in their industry. Concerns about the speed of AI adoption are particularly pronounced among small companies (63%), business leaders with high AI knowledge (51%) and Gen Z and millennial business leaders (51%).

“Leaders are experiencing COVID-19 whiplash, with AI adoption skyrocketing as a result of the pandemic. But many say it’s moving too fast. That’s probably because of current debate surrounding the ethics, governance and regulation of AI. Many business leaders do not have a view into what their organizations are doing to control and govern AI and may fear risks are developing,” Traci Gusher, principal of artificial intelligence at KPMG, said in a statement.

Future AI investment

Healthcare organizations are ramping up their investments in AI in response to the COVID-19 pandemic. In a Deloitte survey, nearly 3 in 4 healthcare organizations said they expect to increase their AI funding, with executives citing making processes more efficient as the top outcome they are trying to achieve with AI.

Healthcare executives say current AI investments at their organizations have focused on electronic health record (EHR) management and diagnosis.

To date, the technology has proved its value in reducing errors and improving medical outcomes for patients, according to executives. Around 40% of healthcare executives said AI technology has helped with patient engagement and also to improve clinical quality. About a third of executives said AI has improved administrative efficiency. Only 18% said the technology helped uncover new revenue opportunities.

But AI investments will shift over the next two years to prioritize telemedicine (38%), robotic tasks such as process automation (37%) and delivery of patient care (36%), the survey found. Clinical trials and diagnosis rounded out the top five investment areas.

At life sciences companies, AI is primarily deployed during the drug development process to improve record-keeping and the application process, the survey found. Companies also have leveraged AI to help with clinical trial site selection.

Moving forward, pharmaceutical companies will likely focus their AI investments on discovering new revenue opportunities in the next two years, a pivot from their current strategy focusing on increasing profitability of existing products, according to the survey. About half of life sciences executives say their organizations plan to leverage AI to reduce administrative costs, analyze patient data and accelerate clinical trials.

Industry stakeholders are taking steps to advance the use of AI and machine learning in healthcare.

The Consumer Technology Association (CTA) created a working group two years ago to develop some standardization on definitions and characteristics of healthcare AI. Last year, the CTA working group developed a standard that creates a common language so industry stakeholders can better understand AI technologies. A group also recently developed a new standard to advance trust in AI solutions.

On the regulatory front, the U.S. Food and Drug Administration (FDA) last month released its first AI and machine learning action plan, a multistep approach designed to advance the agency’s management of advanced medical software. The action plan aims to force manufacturers to be more rigorous in their evaluations, according to the FDA.

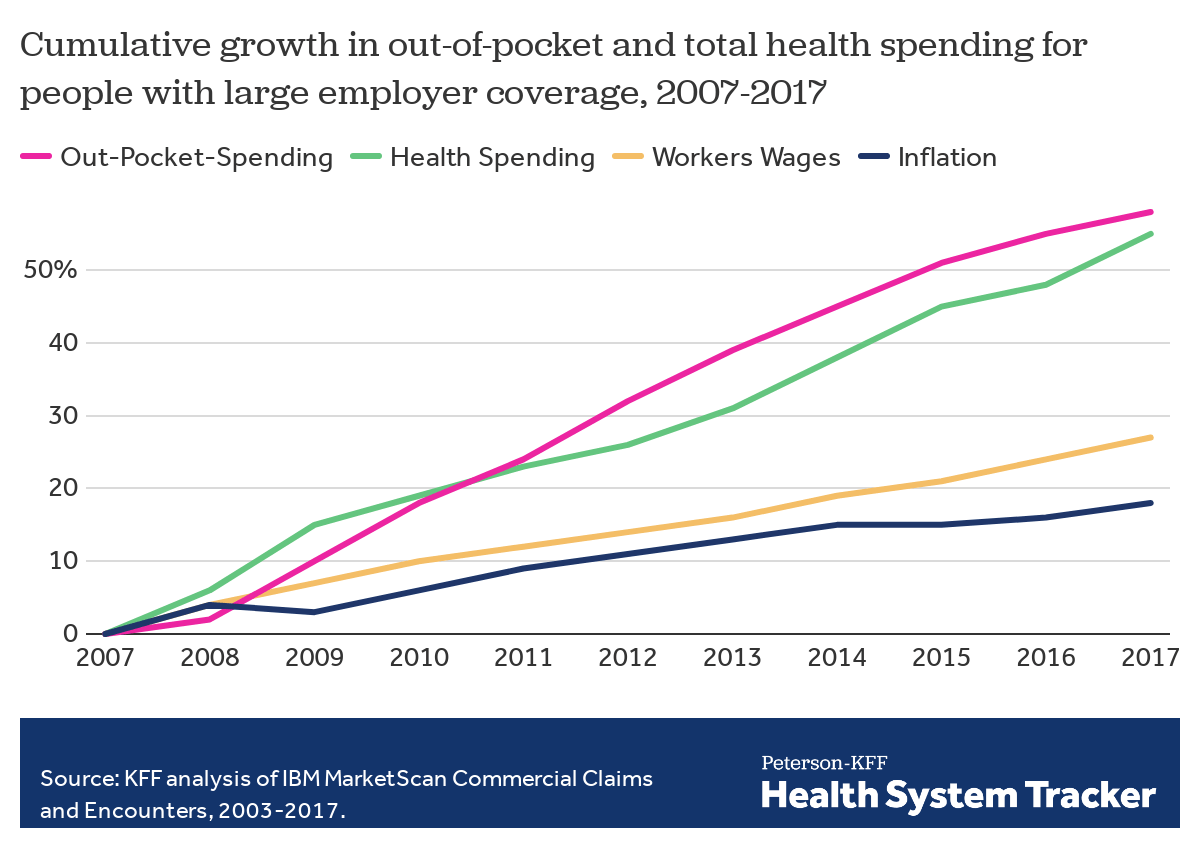

Employers — including companies, state governments and universities — purchase health care on behalf of roughly 150 million Americans. The cost of that care has continued to climb for both businesses and their workers.

For many years, employers saw wasteful care as the primary driver of their rising costs. They made benefits changes like adding wellness programs and raising deductibles to reduce unnecessary care, but costs continued to rise. Now, driven by a combination of new research and changing market forces — especially hospital consolidation — more employers see prices as their primary problem.

By amassing and analyzing employers’ claims data in innovative ways, academics and researchers at organizations like the Health Care Cost Institute (HCCI) and RAND have helped illuminate for employers two key truths about the hospital-based health care they purchase:

1) PRICES VARY WIDELY FOR THE SAME SERVICES

Data show that providers charge private payers very different prices for the exact same services — even within the same geographic area.

For example, HCCI found the price of a C-section delivery in the San Francisco Bay Area varies between hospitals by as much as:$24,107

Data show that hospitals charge employers and private insurers, on average, roughly twice what they charge Medicare for the exact same services. A recent RAND study analyzed more than 3,000 hospitals’ prices and found the most expensive facility in the country charged employers:4.1xMedicare

Hospitals claim this price difference is necessary because public payers like Medicare do not pay enough. However, there is a wide gap between the amount hospitals lose on Medicare (around -9% for inpatient care) and the amount more they charge employers compared to Medicare (200% or more).

Employer Efforts

A small but growing group of companies, public employers (like state governments and universities) and unions is using new data and tactics to tackle these high prices. (Learn more about who’s leading this work, how and why by listening to our full podcast episode in the player above.)

Note that the employers leading this charge tend to be large and self-funded, meaning they shoulder the risk for the insurance they provide employees, giving them extra flexibility and motivation to purchase health care differently. The approaches they are taking include:

Steering Employees

Some employers are implementing so-called tiered networks, where employees pay more if they want to continue seeing certain, more expensive providers. Others are trying to strongly steer employees to particular hospitals, sometimes know as centers of excellence, where employers have made special deals for particular services.

Purdue University, for example, covers travel and lodging and offers a $500 stipend to employees that get hip or knee replacements done at one Indiana hospital.

Negotiating New Deals

There is a movement among some employers to renegotiate hospital deals using Medicare rates as the baseline — since they are transparent and account for hospitals’ unique attributes like location and patient mix — as opposed to negotiating down from charges set by hospitals, which are seen by many as opaque and arbitrary. Other employers are pressuring their insurance carriers to renegotiate the contracts they have with hospitals.

In 2016, the Montana state employee health plan, led by Marilyn Bartlett, got all of the state’s hospitals to agree to a payment rate based on a multiple of Medicare. They saved more than $30 million in just three years. Bartlett is now advising other states trying to follow her playbook.

In 2020, several large Indiana employers urged insurance carrier Anthem to renegotiate their contract with Parkview Health, a hospital system RAND researchers identified as one of the most expensive in the country. After months of tense back-and-forth, the pair reached a five-year deal expected to save Anthem customers $700 million.

Legislating, Regulating, Litigating

Some employer coalitions are advocating for more intervention by policymakers to cap health care prices or at least make them more transparent. States like Colorado and Indiana have passed price transparency legislation, and new federal rules now require more hospital price transparency on a national level. Advocates expect strong industry opposition to stiffer measures, like price caps, which recently failed in the Montana legislature.

Other advocates are calling for more scrutiny by state and federal officials of hospital mergers and other anticompetitive practices. Some employers and unions have even resorted to suing hospitals like Sutter Health in California.

Employer Challenges

Employers face a few key barriers to purchasing health care in different and more efficient ways:

Provider Power

Hospitals tend to have much more market power than individual employers, and that power has grown in recent years, enabling them to raise prices. Even very large employers have geographically dispersed workforces, making it hard to exert much leverage over any given hospital. Some employers have tried forming purchasing coalitions to pool their buying power, but they face tricky organizational dynamics and laws that prohibit collusion.

Sophistication

Employers can attempt to lower prices by renegotiating contracts with hospitals or tailoring provider networks, but the work is complicated and rife with tradeoffs. Few employers are sophisticated enough, for example, to assess a provider’s quality or to structure hospital payments in new ways.Employers looking for insurers to help them have limited options, as that industry has also become highly consolidated.

Employee Blowback

Employers say they primarily provide benefits to recruit and retain happy and healthy employees. Many are reluctant to risk upsetting employees by cutting out expensive providers or redesigning benefits in other ways. A recent KFF survey found just 4% of employers had dropped a hospital in order to cut costs.

The Tradeoffs

Employers play a unique role in the United States health care system, and in the lives of the 150 million Americans who get insurance through work. For years, critics have questioned the wisdom of an employer-based health care system, and massive job losses created by the pandemic have reinforced those doubts for many.

Assuming employers do continue to purchase insurance on behalf of millions of Americans, though, focusing on lowering the prices they pay is one promising path to lowering total costs. However, as noted above, hospitals have expressed concern over the financial pressures they may face under these new deals. Complex benefit design strategies, like narrow or tiered networks, also run the risk of harming employees, who may make suboptimal choices or experience cost surprises. Finally, these strategies do not necessarily address other drivers of high costs including drug prices and wasteful care.

The complexity of Medicare Advantage (MA) physician networks has been well-documented, but the payment regulations that underlie these plans remain opaque, even to experts. If an MA plan enrollee sees an out-of-network doctor, how much should she expect to pay?

The answer, like much of the American healthcare system, is complicated. We’ve consulted experts and scoured nearly inscrutable government documents to try to find it. In this post we try to explain what we’ve learned in a much more accessible way.

Medicare Advantage Basics

Medicare Advantage is the private insurance alternative to traditional Medicare (TM), comprised largely of HMO and PPO options. One-third of the 60+ million Americans covered by Medicare are enrolled in MA plans. These plans, subsidized by the government, are governed by Medicare rules, but, within certain limits, are able to set their own premiums, deductibles, and service payment schedules each year.

Critically, they also determine their own network extent, choosing which physicians are in- or out-of-network. Apart from cost sharing or deductibles, the cost of care from providers that are in-network is covered by the plan. However, if an enrollee seeks care from a provider who is outside of their plan’s network, what the cost is and who bears it is much more complex.

Provider Types

To understand the MA (and enrollee) payment-to-provider pipeline, we first need to understand the types of providers that exist within the Medicare system.

Participating providers, which constitute about 97% of all physicians in the U.S., accept Medicare Fee-For-Service (FFS) rates for full payment of their services. These are the rates paid by TM. These doctors are subject to the fee schedules and regulations established by Medicare and MA plans.

Non-participating providers(about 2% of practicing physicians) can accept FFS Medicare rates for full payment if they wish (a.k.a., “take assignment”), but they generally don’t do so. When they don’t take assignment on a particular case, these providers are not limited to charging FFS rates.

Opt-out providersdon’t accept Medicare FFS payment under any circumstances. These providers, constituting only 1% of practicing physicians, can set their own charges for services and require payment directly from the patient. (Many psychiatrists fall into this category: they make up 42% of all opt-out providers. This is particularly concerning in light of studies suggesting increased rates of anxiety and depression among adults as a result of the COVID-19 pandemic).

How Out-of-Network Doctors are Paid

So, if an MA beneficiary goes to see an out-of-network doctor, by whom does the doctor get paid and how much? At the most basic level, when a Medicare Advantage HMO member willingly seeks care from an out-of-network provider, the member assumes full liability for payment.That is, neither the HMO plan nor TM will pay for services when an MA member goes out-of-network.

The price that the provider can charge for these services, though, varies, and must be disclosed to the patient before any services are administered. If the provider is participating with Medicare (in the sense defined above), they charge the patient no more than the standard Medicare FFS rate for their services. Non-participating providers that do not take assignment on the claim are limited to charging the beneficiary 115% of the Medicare FFS amount, the “limiting charge.” (Some states further restrict this. In New York State, for instance, the maximum is 105% of Medicare FFS payment.) In these cases, the provider charges the patient directly, and they are responsible for the entire amount (See Figure 1.)

Alternatively, if the provider has opted-out of Medicare, there are no limits to what they can charge for their services.The provider and patient enter into a private contract; the patient agrees to pay the full amount, out of pocket, for all services.

MA PPO plans operate slightly differently. By nature of the PPO plan, there are built-in benefits covering visits to out-of-network physicians (usually at the expense of higher annual deductibles and co-insurance compared to HMO plans). Like with HMO enrollees, an out-of-network Medicare-participating physician will charge the PPO enrollee no more than the standard FFS rate for their services. The PPO plan will then reimburse the enrollee 100% of this rate, less coinsurance. (SeeFigure 2.)

In contrast, a non-participating physician that does not take assignment is limited to charging a PPO enrollee 115% of the Medicare FFS amount, which can be further limited by state regulations. In this case, the PPO enrollee is also reimbursed by their plan up to 100% (less coinsurance) of the FFS amount for their visit. Again, opt-out physicians are exempt from these regulations and must enter private contracts with patients.

Figure 2: MA PPO Out-of-Network Payments

Some Caveats

There are two major caveats to these payment schemes (with many more nuanced and less-frequent exceptions detailed here). First, if a beneficiary seeks urgent or emergent care (as defined by Medicare) and the provider happens to be out-of-network for the MA plan (regardless of HMO/PPO status), the plan must cover the services at their established in-network emergency services rates.

The second caveat is in regard to the declared public health emergency due to COVID-19 (set to expire in April 2021, but likely to be extended). MA plans are currently required to cover all out-of-network services from providers that contract with Medicare (i.e., all but opt-out providers) and charge beneficiaries no more than the plan-established in-network rates for these services. This is being mandated by CMS to compensate for practice closures and other difficulties of finding in-network care as a result of the pandemic.

Conclusion

Outside of the pandemic and emergency situations, knowing how much you’ll need to pay for out-of-network services as a MA enrollee depends on a multitude of factors. Though the vast majority of American physicians contract with Medicare, the intersection of insurer-engineered physician networks and the complex MA payment system could lead to significant unexpected costs to the patient.