After filing a lawsuit in May to end its affiliation with Renton, Wash.-based Providence, Hoag Memorial Hospital in Newport Beach, Calif., is alleging it is now the target of retaliation, according to theLos Angeles Times.

Hoag Memorial said that Providence removed Hoag Memorial’s three facilities from its website of Southern California locations and terminated Hoag Memorial’s specialists from St. Joseph Heritage Healthcare, a network of medical providers for managed care plans in Southern California. Additionally, Hoag Memorial said that Providence informed Heritage members they would lose access to Hoag’s 13 urgent care centers by Dec. 31.

According to the report, Providence’s notice to patients that Hoag facilities and physicians would be dropped from its network all came in the fall of 2020, amid the COVID-19 pandemic.

“It was the most inappropriate, inexplicable and harsh thing to do to a lot of patients,” Hoag President and CEO Robert Braithwaite told the Los Angeles Times. “Finding a new physician or new specialist is particularly hard on seniors and any patient who has a chronic condition and has established a long-term relationship with an endocrinologist or rheumatologist or cancer doctor.”

Providence told the Los Angeles Times it disagrees that patients have been disadvantaged.

“We are committed to the well-being of our communities and to serving patients with high quality and compassionate care,” a Providence spokesperson told the Los Angeles Times.

Hoag Memorial has been affiliated with Providence, a Catholic health system, since 2016.

Hoag Memorial said the changes all came after the hospital sought to end its affiliation with Providence by filing a lawsuit. Hoag Memorial said in its lawsuit it is seeking to end the affiliation because Providence is undermining local decision-making and Catholic Church restrictions are expanding.

Providence has fought Hoag’s lawsuit to end the affiliation. The health system claims Hoag doesn’t have the right to unilaterally dissolve the affiliation, and its board members don’t have the authority to file the lawsuit. An Orange County Superior Court judge rejected Providence’s argument Feb. 1 and scheduled another court hearing for March.

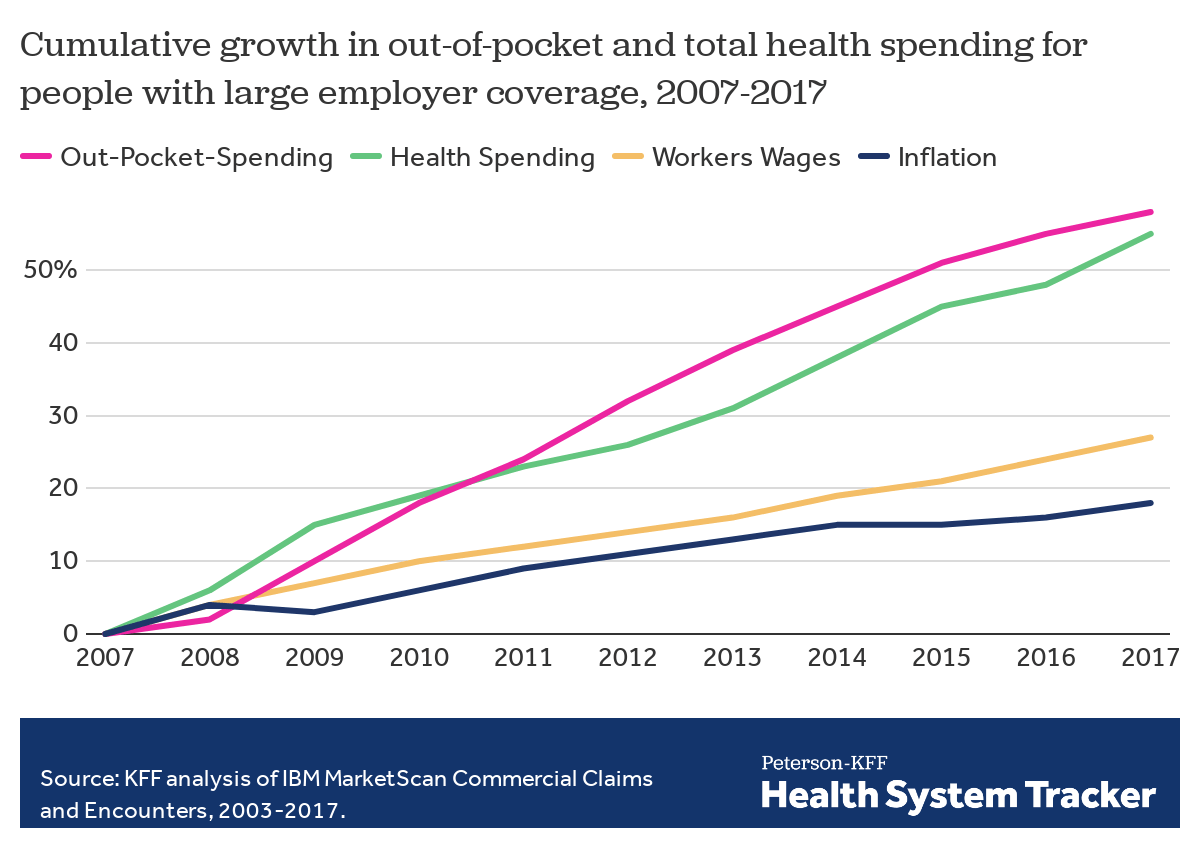

Employers — including companies, state governments and universities — purchase health care on behalf of roughly 150 million Americans. The cost of that care has continued to climb for both businesses and their workers.

For many years, employers saw wasteful care as the primary driver of their rising costs. They made benefits changes like adding wellness programs and raising deductibles to reduce unnecessary care, but costs continued to rise. Now, driven by a combination of new research and changing market forces — especially hospital consolidation — more employers see prices as their primary problem.

By amassing and analyzing employers’ claims data in innovative ways, academics and researchers at organizations like the Health Care Cost Institute (HCCI) and RAND have helped illuminate for employers two key truths about the hospital-based health care they purchase:

1) PRICES VARY WIDELY FOR THE SAME SERVICES

Data show that providers charge private payers very different prices for the exact same services — even within the same geographic area.

For example, HCCI found the price of a C-section delivery in the San Francisco Bay Area varies between hospitals by as much as:$24,107

Data show that hospitals charge employers and private insurers, on average, roughly twice what they charge Medicare for the exact same services. A recent RAND study analyzed more than 3,000 hospitals’ prices and found the most expensive facility in the country charged employers:4.1xMedicare

Hospitals claim this price difference is necessary because public payers like Medicare do not pay enough. However, there is a wide gap between the amount hospitals lose on Medicare (around -9% for inpatient care) and the amount more they charge employers compared to Medicare (200% or more).

Employer Efforts

A small but growing group of companies, public employers (like state governments and universities) and unions is using new data and tactics to tackle these high prices. (Learn more about who’s leading this work, how and why by listening to our full podcast episode in the player above.)

Note that the employers leading this charge tend to be large and self-funded, meaning they shoulder the risk for the insurance they provide employees, giving them extra flexibility and motivation to purchase health care differently. The approaches they are taking include:

Steering Employees

Some employers are implementing so-called tiered networks, where employees pay more if they want to continue seeing certain, more expensive providers. Others are trying to strongly steer employees to particular hospitals, sometimes know as centers of excellence, where employers have made special deals for particular services.

Purdue University, for example, covers travel and lodging and offers a $500 stipend to employees that get hip or knee replacements done at one Indiana hospital.

Negotiating New Deals

There is a movement among some employers to renegotiate hospital deals using Medicare rates as the baseline — since they are transparent and account for hospitals’ unique attributes like location and patient mix — as opposed to negotiating down from charges set by hospitals, which are seen by many as opaque and arbitrary. Other employers are pressuring their insurance carriers to renegotiate the contracts they have with hospitals.

In 2016, the Montana state employee health plan, led by Marilyn Bartlett, got all of the state’s hospitals to agree to a payment rate based on a multiple of Medicare. They saved more than $30 million in just three years. Bartlett is now advising other states trying to follow her playbook.

In 2020, several large Indiana employers urged insurance carrier Anthem to renegotiate their contract with Parkview Health, a hospital system RAND researchers identified as one of the most expensive in the country. After months of tense back-and-forth, the pair reached a five-year deal expected to save Anthem customers $700 million.

Legislating, Regulating, Litigating

Some employer coalitions are advocating for more intervention by policymakers to cap health care prices or at least make them more transparent. States like Colorado and Indiana have passed price transparency legislation, and new federal rules now require more hospital price transparency on a national level. Advocates expect strong industry opposition to stiffer measures, like price caps, which recently failed in the Montana legislature.

Other advocates are calling for more scrutiny by state and federal officials of hospital mergers and other anticompetitive practices. Some employers and unions have even resorted to suing hospitals like Sutter Health in California.

Employer Challenges

Employers face a few key barriers to purchasing health care in different and more efficient ways:

Provider Power

Hospitals tend to have much more market power than individual employers, and that power has grown in recent years, enabling them to raise prices. Even very large employers have geographically dispersed workforces, making it hard to exert much leverage over any given hospital. Some employers have tried forming purchasing coalitions to pool their buying power, but they face tricky organizational dynamics and laws that prohibit collusion.

Sophistication

Employers can attempt to lower prices by renegotiating contracts with hospitals or tailoring provider networks, but the work is complicated and rife with tradeoffs. Few employers are sophisticated enough, for example, to assess a provider’s quality or to structure hospital payments in new ways.Employers looking for insurers to help them have limited options, as that industry has also become highly consolidated.

Employee Blowback

Employers say they primarily provide benefits to recruit and retain happy and healthy employees. Many are reluctant to risk upsetting employees by cutting out expensive providers or redesigning benefits in other ways. A recent KFF survey found just 4% of employers had dropped a hospital in order to cut costs.

The Tradeoffs

Employers play a unique role in the United States health care system, and in the lives of the 150 million Americans who get insurance through work. For years, critics have questioned the wisdom of an employer-based health care system, and massive job losses created by the pandemic have reinforced those doubts for many.

Assuming employers do continue to purchase insurance on behalf of millions of Americans, though, focusing on lowering the prices they pay is one promising path to lowering total costs. However, as noted above, hospitals have expressed concern over the financial pressures they may face under these new deals. Complex benefit design strategies, like narrow or tiered networks, also run the risk of harming employees, who may make suboptimal choices or experience cost surprises. Finally, these strategies do not necessarily address other drivers of high costs including drug prices and wasteful care.

The federal government has penalized 774 hospitals for having the highest rates of patient infections or other potentially avoidable medical complications.Those hospitals, which include some of the nation’s marquee medical centers, will lose 1% of their Medicare payments over 12 months.

The penalties, based on patients who stayed in the hospitals anytime between mid-2017 and 2019, before the pandemic, are not related to covid-19. They were levied under a program created by the Affordable Care Act that uses the threat of losing Medicare money to motivate hospitals to protect patients from harm.

On any given day, one in every 31 hospital patients has an infection that was contracted during their stay, according to the Centers for Disease Control and Prevention. Infections and other complications can prolong hospital stays, complicate treatments and, in the worst instances, kill patients.

“Although significant progress has been made in preventing some healthcare-associated infection types, there is much more work to be done,” the CDC says.

Now in its seventh year, the Hospital-Acquired Condition Reduction Program has been greeted with disapproval and resignation by hospitals, which argue that penalties are meted out arbitrarily. Under the law, Medicare each year must punish the quarter of general care hospitals with the highest rates of patient safety issues. The government assesses the rates of infections, blood clots, sepsis cases, bedsores, hip fractures and other complications that occur in hospitals and might have been prevented. The total penalty amount is based on how much Medicare pays each hospital during the federal fiscal year — from last October through September.

Hospitals can be punished even if they have improved over past years — and some have. At times, the difference in infection and complication rates between the hospitals that get punished and those that escape punishment is negligible, but the requirement to penalize one-quarter of hospitals is unbending under the law. Akin Demehin, director of policy at the American Hospital Association, said the penalties were “a game of chance” based on “badly flawed” measures.

Some hospitals insist they received penalties because they were more thorough than others in finding and reporting infections and other complications to the federal Centers for Medicare & Medicaid Services and the CDC.

“The all-or-none penalty is unlike any other in Medicare’s programs,” said Dr. Karl Bilimoria, vice president for quality at Northwestern Medicine, whose flagship Northwestern Memorial Hospital in Chicago was penalized this year. He said Northwestern takes the penalty seriously because of the amount of money at stake, “but, at the same time, we know that we will have some trouble with some of the measures because we do a really good job identifying” complications.

Other renowned hospitals penalized this year include Ronald Reagan UCLA Medical Center and Cedars-Sinai Medical Center in Los Angeles; UCSF Medical Center in San Francisco; Beth Israel Deaconess Medical Center and Tufts Medical Center in Boston; NewYork-Presbyterian Hospital in New York; UPMC Presbyterian Shadyside in Pittsburgh; and Vanderbilt University Medical Center in Nashville, Tennessee.

There were 2,430 hospitals not penalized because their patient complication rates were not among the top quarter. An additional 2,057 hospitals were automatically excluded from the program, either because they solely served children, veterans or psychiatric patients, or because they have special status as a “critical access hospital” for lack of nearby alternatives for people needing inpatient care.

The penalties were not distributed evenly across states, according to a KHN analysis of Medicare data that included all categories of hospitals. Half of Rhode Island’s hospitals were penalized, as were 30% of Nevada’s.

All of Delaware’s hospitals escaped punishment.Medicare excludes all Maryland hospitals from the program because it pays them through a different arrangement than in other states.

Over the course of the program, 1,978 hospitals have been penalized at least once, KHN’s analysis found. Of those, 1,360 hospitals have been punished multiple times and 77 hospitals have been penalized in all seven years, including UPMC Presbyterian Shadyside.

The Medicare Payment Advisory Commission, which reports to Congress, said in a 2019 report that “it is important to drive quality improvement by tying infection rates to payment.” But the commission criticized the program’s use of a “tournament” model comparing hospitals to one another. Instead, it recommended fixed targets that let hospitals know what is expected of them and that don’t artificially limit how many hospitals can succeed.

Although federal officials have altered other ACA-created penalty programs in response to hospital complaints and independent critiques — such as one focused on patient readmissions — they have not made substantial changes to this program because the key elements are embedded in the statute and would require a change by Congress.

Boston’s Beth Israel Deaconess said in a statement that “we employ a broad range of patient care quality efforts and use reports such as those from the Centers for Medicare & Medicaid Services to identify and address opportunities for improvement.”

UCSF Health said its hospital has made “significant improvements” since the period Medicare measured in assessing the penalty.

“UCSF Health believes that many of the measures listed in the report are meaningful to patients, and are also valid standards for health systems to improve upon,” the hospital-health system said in a statement to KHN. “Some of the categories, however, are not risk-adjusted, which results in misleading and inaccurate comparisons.”

Cedars-Sinai said the penalty program disproportionally punishes academic medical centers due to the “high acuity and complexity” of their patients, details that aren’t captured in the Medicare billing data.

“These claims data were not designed for this purpose and are typically not specific enough to reflect the nuances of complex clinical care,” the hospital said. “Cedars-Sinai continually tracks and monitors rates of complications and infections, and updates processes to improve the care we deliver to our patients.”

As COVID-19 cases surged last fall, non-COVID-19 hospital admissions fell substantially, particularly in the Midwest and West, according to a new analysis by the Kaiser Family Foundation of 2020 inpatient admission data from electronic medical records through Dec. 5.

The analysis also highlights admission trends by age and sex, and found that patients 65 and over — those most at risk of complications from the novel coronavirus — delayed care at greater rates than those under 65 again in the fall. Still, the discrepancy between visits based on age was more pronounced in the spring.

On average, males and females had almost identical admission patterns throughout the entire year. Though looking at the raw numbers, women’s total admissions trended above their male counterparts, which researchers attributed to childbirth.

Dive Insight:

The latest analysis from the think tank provides a fuller picture of how the COVID-19 pandemic influenced admission trends throughout 2020.

Overall, total admissions bottomed out in April and March but have remained near normal, or above 90% of expected admissions since June, according to electronic medical record data from the Epic Health Research Network, which pools information from 20 million patients across 97 hospitals in the U.S.

However, while total admissions — which includes those sick with COVID-19 — remained near normal, the pattern differed when zeroing in on non-COVID-19 admissions, or those admitted who did not have the virus.

Non-COVID-19 admissions started to fall againin November and by Dec. 5 they fell to 80% of expected volume, which is likely to put financial pressure on hospitals, particularly those with smaller reserves of cash on hand, Kaiser noted.

The decline was steepest in the Midwest and West, dropping to about 76% of expected volume between early November and December.

Researchers fear the drop in non-COVD-19 admissions may have long-term consequences.

“The levels of non-COVID-19 admissions seen in the fall of 2020 suggest that people may be delaying care in ways that could be harmful to their long-term health,” according to the study.

Insurers observed similar patterns of depressed volume in the fourth quarter.

Humana, which largely covers seniors in Medicare plans, noted non-COVID-19 volume dropped the last two months of the quarter after previously returning to near normal. It led Humana to report a loss in the fourth quarter as COVID-19 testing and treatment accelerated. Centene, which reported a Q4 loss, echoed a similar pattern.

With nearly 30% of workers now having a high deductible health plan and a typical family being responsible for on average the first $8,000 of costs, consumers are increasingly weighing care versus cost. Historically, with a small copay, you would conveniently take care of an ailment without shopping around, but with the average person now bearing the brunt of the initial costs, wouldn’t you want to know how much a service costs and what other providers are charging before you “buy” the service?

CMS believes“consumers should be able to know, long before they open a medical bill, roughly how much a hospital will charge for items and services it provides.” Cue the hospital price transparency rule that just went into effect January 1, 2021. Hospitals are now required to post their standard charges, including the rates they negotiate with insurers, and the discounted price a hospital is willing to accept directly from a patient if paid in cash. As a consumer, the intent is to make it “easier to shop and compare prices across hospitals and estimate the cost of care before going to the hospital.”

There are a few different angles to analyze here:

Are hospitals following the rules?

Each hospital must post online a comprehensive machine readable file with all items and services, including gross charges, actual negotiated prices with insurers, and the cash price for patients who are uninsured. Additionally, hospitals must post the costs for 300 common “shoppable” services in a “consumer-friendly format.” Some hospitals and health systems have done a good job at posting these prices in a digestible format, like the Cleveland Clinic or Sutter Health, but others have posted complicated spreadsheets, relied on online cost estimator tools, or simply not posted them at all. An analysis from consulting firm ADVI of the top 20 largest hospitals in the U.S. found that not all of them appeared to completely comply with this mandate. In some instances, data was not able to be downloaded in a useable format, others did not post the DRG or service codes, and the variability in the terms/categories used simply created difficulty in comparing pricing information across hospitals. CMS has stated that a failure to comply with the rules could result in a fine of up to $300 per day. As with most new rules, there are growing pains, and hospitals will likely get better at this over time, assuming the data is being used for its original intent.

Is this helpful to consumers?

Consumers will able to see the variation in prices for the exact same service or procedure between hospitals and get an estimate of what they will be charged before getting the care. But how likely is the average person to go to their hospital’s website, look at a price, and change their decision about where to get care? In addition, awareness of these price transparency tools is still low among consumers. Frankly, it is competitors and insurers that have been first in line to review the data. Looking through a number of hospital websites, and even certain state agency sites that have done a good job at summarizing the costs, like Florida Health Price Finder, the price transparency tools are helpful, but appear to be much more suited for relatively standardized services that can be scheduled in advance, like a knee replacement. It’s highly unlikely you will be telling your ambulance driver what hospital to go to based on cost while in cardiac arrest…Plus, it’s all still confusing – even physicians have shared their bewilderment, when trying to decipher and compare pricing. Conceptually, price transparency should be beneficial to consumers, but it will take time; and it will need to involve not just the hospitals posting rates, but the outpatient care facilities as well. Knowing what you will pay before you decide to go to a physician’s office or a clinic or an urgent care or an ED will hopefully help drive consumers to make more educated decisions in the future.

Will this ultimately drive down costs?

I sure hope so. Revealing actual negotiated prices between hospitals and insurers should push the more expensive hospitals in the area to reduce prices, especially if consumers start using the other hospitals, instead. However, it could also have an inverse effect, with lower cost hospitals insisting on a payment increase from insurers; thereby driving up costs. In the end, as has historically been the case, the market power of certain providers will likely dictate the direction of costs in a given region. That is, until both price AND quality become fully transparent and the consumer is armed with the tools to shop for the best care at the lowest cost – consumerism here we come.

We spend a lot of our time helping health system executives craft and communicate enterprise-level strategy: entering new markets or businesses, developing new services, responding to competitive threats, exploring partnership opportunities. Strategy is about the “what” and “when”—what moves are we going to make, and when is the right time to make them?Answering those questions requires an understanding of industry and market forces, organizational capabilities, and consumer needs. But there’s another important component that often goes missing in the rush to get to the “how” of strategy execution: the “why”.

Yet understanding why we’re pursuing one path and not another is critical for aligning stakeholders: physicians, operators, and (importantly) the board. Joan Didion famously wrote that “we tell ourselves stories in order to live”, and we’d agree; the “why” is about storytelling. What’s the strategic narrative, or story, that frames our intended actions? Making sure that everyone involved—including our patients and consumers—has a clear understanding of why we’re opening a new facility, or launching a new service, or entering into a new partnership, is a key to success.

It’s about sharing the vision of our desired role as a system, and the part we see ourselves playing in improving healthcare. We’re sometimes criticized for spending so much time on “framing” and drawing “pretty graphics”, but we’ve come to believe that the ability to succinctly and compellingly describe the “why” of strategy is as important as coming up with the vision in the first place.And then, of course, delivering on the “why”—a job made easier if all involved are clear on just what it is.

Fourteen of the nation’s largest health systems announced this week that they have joined together to form a new, for-profit data company aimed at aggregating and mining their clinical data. Called Truveta, the company will draw on the de-identified health records of millions of patients from thousands of care sites across 40 states, allowing researchers, physicians, biopharma companies, and others to draw insights aimed at “improving the lives of those they serve.”

Health system participants include the multi-state Catholic systems CommonSpirit Health, Trinity Health, Providence, and Bon Secours Mercy, the for-profit system Tenet Healthcare, and a number of regional systems. The new company will be led by former Microsoft executive Terry Myerson, who has been working on the project since March of last year. As large technology companies like Amazon and Google continue to build out healthcare offerings, and national insurers like UnitedHealth Group and Aetna continue to grow their analytical capabilities based on physician, hospital, and pharmacy encounters, it’s surprising that hospital systems are only now mobilizing in a concerted way to monetize the clinical data they generate.

Like Civica, an earlier health system collaboration around pharmaceutical manufacturing, Truveta’s launch signals that large national and regional systems are waking up to the value of scale they’ve amassed over time, moving beyond pricing leverage to capture other benefits from the size of their clinical operations—and exploring non-merger partnerships to create value from collaboration. There will inevitably be questions about how patient data is used by Truveta and its eventual customers, but we believe the venture holds real promise for harnessing the power of massive clinical datasets to drive improvement in how care is delivered.

Here are 11 health systems and hospitals with strong operational metrics and solid financial positions, according to reports from Fitch Ratings, Moody’s Investors Service and S&P Global Ratings.

1. Morristown, N.J.-based Atlantic Health System has an “Aa3” rating and stable outlook with Moody’s. The credit rating agency expects the health system to continue to generate favorable operating performance and to maintain double-digit operating cash flow margins and solid debt coverage.

2. Charlotte, N.C.-based Atrium Health has an “Aa3” rating and stable outlook with Moody’s and an “AA-” rating and stable outlook with S&P. Atrium and Winston-Salem, N.C.-based Wake Forest Baptist Health merged in October. The addition of the Winston-Salem service area and Wake Forest Baptist’s academic and research programs enhances Atrium’s position within the highly competitive North Carolina healthcare market, S&P said.

3. Dallas-based Baylor Scott & White Health has an “Aa3” rating and stable outlook with Moody’s. The system has strong liquidity and is the largest nonprofit health system in Texas, Moody’s said. The credit rating agency expects Baylor Scott & White Health to continue to benefit from its centralized operating model, proven ability to execute complex strategies and well-developed planning abilities.

4. Pittsfield, Mass.-based Berkshire Health System has an “AA-” rating and stable outlook with Fitch. The health system has improved its liquidity while investing in facilities without increasing its debt load, Fitch said. The credit rating agency expects the system to maintain a strong financial profile.

5. Mishawaka, Ind.-based Franciscan Alliance has an “Aa3” rating and stable outlook with Moody’s. The system has leading positions in key markets and a strong cash position, Moody’s said. The credit rating agency expects the system to sustain double-digit operating cash flow margins.

6. Falls Church, Va.-basedInova Health System has an “Aa2” rating and stable outlook with Moody’s. The system has a strong financial profile, and Moody’s expects Inova’s balance sheet to remain exceptionally strong.

7. Palo Alto, Calif.-based Lucile Packard Children’s Hospital at Stanford has an “AA-” rating and stable outlook with Fitch. The hospital is nationally known, has a strong market position and is one of two key clinical partners of Stanford University, Fitch said.

8. Grand Blanc, Mich.-based McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The health system has a strong financial profile and a leading market position over a broad service area that covers much of Michigan, Fitch said.

9. Winston-Salem, N.C.-based Novant Health has an “AA-” rating and stable outlook with Fitch. The system has strong margins, and each of its markets has met or exceeded budgeted expectations over the past four years, Fitch said.

10. Renton, Wash.-based Providence has an “Aa3” rating and stable outlook with Moody’s. Providence has a large revenue base and a leading market share in most of its markets, according to Moody’s. The credit rating agency expects the system’s operations to improve this year.

11. Livonia, Mich.-based Trinity Health has an “AA-” rating and stable outlook with Fitch. The rating is driven by Trinity’s national size and scale, with significant market presence in several states, Fitch said. The credit rating agency expects the system’s operating margins to improve in the long term.