Saturday, Congress voted overwhelming (House 335-91, Senate 88-9) to keep the government funded until Nov. 17 at 2023 levels. No surprise. Congress is supposed to pass all 12 appropriations bills before the start of each fiscal year but has done that 4 times since 1970—the last in 1997. So, while this chess game plays out, the health system will soldier on against growing recognition it needs fixing.

In Wednesday night’s debate, GOP Presidential aspirant Nicki Haley was asked what she would do to address the spike in personal bankruptcies due to medical debt. Her reply:

“We will break all of it [down], from the insurance company, to the hospitals, to the doctors’ offices, to the PBMs [pharmacy benefit managers], to the pharmaceutical companies. We will make it all transparent because when you do that, you will realize that’s what the problem is…we need to bring competition back into the healthcare space by eliminating certificate of need systems… Once we give the patient the ability to decide their healthcare, deciding which plan they want, that is when we will see magic happen, but we’re going to have to make every part of the industry open up and show us where their warts are because they all have them”

It’s a sentiment widely held across partisan aisles and in varied degrees among taxpayers, employers and beyond. It’s a system flaw and each sector is complicit.

What seems improbable is a solution that rises above the politics of healthcare where who wins and loses is more important than the solutions themselves.

Perhaps as improbable as the European team’s dominating performance in the 44th Ryder Cup Championship played in Rome last week especially given pre-tournament hype about the US team.

While in Rome last week, I queried hotel employees, restaurant and coffee shop owners, taxi drivers and locals at the tournament about the Italian health system. I saw no outdoor signage for hospitals and clinics nor TV ads for prescriptions and OTC remedies. Its pharmacies, clinics and hospitals are non-descript, modest and understated. Yet groups like the World Health Organization (WHO) and the Organization for Economic Cooperation Development (OECD) rank Servizio Sanitario Nazionale (SSN), the national system authorized in December 1978, in the top 10 in the world (The WHO ranks it second overall behind France).

“It covers all Italian citizens and legal foreign residents providing a full range of healthcare services with a free choice of providers. The service is free of charge at the point of service and is guided by the principles of universal coverage, solidarity, human dignity, and health. In principle, it serves as Italy’s public healthcare system.” Like U.S. ratings for hospitals, rankings for the Italian system vary but consistently place it in the top 15 based on methodologies comparing access, quality, and affordability.

The U.S., by contrast, ranks only first in certain high-end specialties and last among developed systems in access and affordability.

Like many systems of the world, SSN is governed by a national authority that sets operating principles and objectives administered thru 19 regions and two provinces that deliver health services under an appointed general manager. Each has significant independence and the flexibility to determine its own priorities and goals, and each is capitated based on a federal formula reflecting the unique needs and expected costs for that population’s health.

It is funded throughnational and regional taxes, supplemented by private expenditure and insurance plans and regions are allowed to generate their own additional revenue to meet their needs. 74% of funding is public; 26% is private composed primarily of consumer out-of-pocket costs. By contrast, the U.S. system’s funding is 49% public (Medicare, Medicaid et al), 24% private (employer-based, misc.) and 27% OOP by consumers.

Italians enjoy the 6th highest life expectancy in the world, as well as very low levels of infant mortality. It’s not a perfect system: 10% of the population choose private insurance coverage to get access to care quicker along with dental care and other benefits. Its facilities are older, pharmacies small with limited hours and hospitals non-descript.

But Italians seem satisfied with their system reasoning it a right, not a privilege, and its absence from daily news critiques a non-concern.

Issues confronting its system—like caring for its elderly population in tandem with declining population growth, modernizing its emergency services and improving its preventive health programs are understood but not debilitating in a country one-fifth the size of the U.S. population.

My take:

Italy spends 9% of its overall GDP on its health system; the $4.6 trillion U.S spends 18% in its GDP on healthcare, and outcomes are comparable. Our’s is better known but their’s appears functional and in many ways better.

Should the U.S.copy and paste the Italian system as its own? No. Our societies, social determinants and expectations vary widely. Might the U.S. health system learn from countries like Italy? Yes.

Questions like these merit consideration:

Might the U.S. system perform better if states had more authority and accountability for Medicare, CMS, Veterans’ health et al?

Might global budgets for states be an answer?

Might more spending on public health and social services be the answer to reduced costs and demand?

Might strict primary care gatekeeping be an answer to specialty and hospital care?

Might private insurance be unnecessary to a majority satisfied with a public system?

Might prices for prescription drugs, hospital services and insurance premiums be regulated or advertising limited?

Might employers play an expanded role in the system’s accountability?

Can we afford the system long-term, given other social needs in a changing global market?

Comparisons are constructive for insights to be learned. It’s true in healthcare and professional golf. The European team was better prepared for the Ryder Cup competition. From changes to the format of the matches, to pin placements and second shot distances requiring precision from 180-200 yards out on approach shots: advantage Europe. Still, it was execution as a team that made the difference in its dominating 16 1/2- 11 1/2 win —not the celebrity of any member.

The time to ask and answer tough questions about the sustainability of the U.S. system and chart a path forward. A prepared, selfless effort by a cross-sector Team Healthcare USA is our system’s most urgent need. No single sector has all the answers, and all are at risk of losing.

Team USA lost the Ryder Cup because it was out-performed by Team Europe: its data, preparation and teamwork made the difference.

Today, there is no Team Healthcare USA: each sector has its stars but winning the competition for the health and wellbeing of the U.S. populations requires more.

Studies show healthcare affordability is an issue to voters as medical debt soars (KFF) and public disaffection for the “medical system” (per Gallup, Pew) plummets. But does it really matter to the hospitals, insurers, physicians, drug and device manufacturers and army of advisors and trade groups that control the health system?

Each sector talks about affordability blaming inflation, growing demand, oppressive regulation and each other for higher costs and unwanted attention to the issue.

Each play their victim cards in well-orchestrated ad campaigns targeted to state and federal lawmakers whose votes they hope to buy.

Each considers aggregate health spending—projected to increase at 5.4%/year through 2031 vs. 4.6% GDP growth—a value relative to the health and wellbeing of the population. And each thinks its strategies to address affordability are adequate and the public’s concern understandable but ill-informed.

As the House reconvenes this week joining the Senate in negotiating a resolution to the potential federal budget default October 1, the question facing national and state lawmakers is simple: is the juice worth the squeeze?

Is the US health system deserving of its significance as the fastest-growing component of the total US economy (18.3% of total GDP today projected to be 19.6% in 2031), its largest private sector employer and mainstay for private investors?

Does it deserve the legal concessions made to its incumbents vis a vis patent approvals, tax exemptions for hospitals and employers, authorized monopolies and oligopolies that enable its strongest to survive and weaker to disappear?

Does it merit its oversized role, given competing priorities emerging in our society—AI and technology, climate changes, income, public health erosion, education system failure, racial inequity, crime and global tension with China, Russia and others.

In the last 2 weeks, influential Republicans leaders (Burgess, Cassidy) announced plans to tackle health costs and the role AI will play in the future of the system. Last Tuesday, CMS announced its latest pilot program to tackle spending: the States Advancing All-Payer Health Equity Approaches and Development Model (AHEAD Model) is a total cost of care budgeting program to roll out in 8 states starting in 2026. The Presidential campaigns are voicing frustration with the system and the spotlight on its business practices intensifying.

So, is affordability to the federal government likely to get more attention?

Yes. Is affordability on state radars as legislatures juggle funding for Medicaid, public health and other programs?

Yes, but on a program by program, non-system basis.

Is affordability front and center in CMS value agenda including the new models like its AHEAD model announced last week? Not really.

CMS has focused more on pushing hospitals and physicians to participate than engaging consumers. Is affordability for those most threatened—low and middle income households with high deductible insurance, the uninsured and under-insured, those with an expensive medical condition—front of mind? Every minute of every day.

Per CMS, out-of-pocket spending increased 4.3% in 2022 (down from 10.4% in 2021) and “is expected to accelerate to 5.2%, in part related to faster health care price growth. During 2025–31, average out-of-pocket spending growth is projected to be 4.1% per year.” But these data are misleading. It’s dramatically higher for certain populations and even those with attractive employer-sponsored health benefits worry about unexpected household medical bills.

So, affordability is a tricky issue that’s front of mind to 40% of the population today and more tomorrow.

Legislation that limits surprise medical bills, requires drug, hospital and insurer price transparency, expands scope of practice opportunities for mid-level professionals, avails consumers of telehealth services, restricts aggressive patient debt collection policies and others has done little to assuage affordability issues for consumers.

Ditto CMS’ value agenda which is more about reducing Medicare spending through shared savings programs with hospitals and physicians than improving affordability for consumers. That’s why outsiders like Walmart, Best Buy and others see opportunity: they think patients (aka members, enrollees, end users) deserve affordability solutions more than lip service.

Affordability to consumers is the most formidable challenge facing the US healthcare industry–more than burnout, operating margins, reimbursement or alternative payment models. Today, it is not taken seriously by insiders. If it was, evidence would be readily available and compelling. But it’s not.

Last Monday, four U.S. Senators took aim at the tax exemption enjoyed by not-for-profit (NFP) hospitals in a letter to the IRS demanding detailed accounting for community benefits and increased agency oversight of NFP hospitals that fall short.

Last Tuesday, the Elevance Health Policy Institute released a study concluding that the consolidation of hospitals into multi-hospital systems (for-profit/not-for-profit) results in higher prices without commensurate improvement in patient care quality. “

Friday, Kaiser Health News Editor in Chief Elizabeth Rosenthal took aim at Ballad Health which operates in TN and VA “…which has generously contributed to performing arts and athletic centers as well as school bands. But…skimped on health care — closing intensive care units and reducing the number of nurses per ward — and demanded higher prices from insurers and patients.”

And also last week, the Pharmaceuticals’ Manufacturers Association released its annual study of hospital mark-ups for the top 20 prescription drugs used on hospitals asserting a direct connection between hospital mark-ups (which ranged from 234% to 724%) and increasing medical debt hitting households.

(Excerpts from these are included in the “Quotables” section that follows).

It was not a good week for hospitals, especially not-for-profit hospitals.

In reality, the storm cloud that has gathered over not-for-profit health hospitals in recent months has been buoyed in large measure by well-funded critiques by Arnold Ventures,Lown Institute, West Health, Patient Rights Advocate and others. Providence, Ascension, Bon Secours and now Ballad have been criticized for inadequate community benefits, excessive CEO compensation, aggressive patient debt collection policies and price gauging attributed to hospital consolidation.

This cloud has drawn attention from lawmakers: in NC, the State Treasurer Dale Folwell has called out the state’s 8 major NFP systems for inadequate community benefit and excess CEO compensation.

In Indiana, State Senator Travis Holdman is accusing the state’s NFP hospitals of “hoarding cash” and threatening that “if not-for-profit hospitals aren’t willing to use their tax-exempt status for the benefit of our communities, public policy on this matter can always be changed.” And now an influential quartet of U.S. Senators is pledging action to complement with anti-hospital consolidation efforts in the FTC leveraging its a team of 40 hospital deal investigators.

In response last week, the American Hospital Association called out health insurer consolidation as a major contributor to high prices and,

in a US News and World Report Op Ed August 8, challenged that “Health insurance should be a bridge to medical care, not a barrier.

Yet too many commercial health insurance policies often delay, disrupt and deny medically necessary care to patients,” noting that consumer medical debt is directly linked to insurer’ benefits that increase consumer exposure to out of pocket costs.

My take:

It’s clear that not-for-profit hospitals pose a unique target for detractors: they operate more than half of all U.S. hospitals and directly employ more than a third of U.S. physicians.

But ownership status (private not-for-profit, for-profit investor owned or government-owned) per se seems to matter less than the availability of facilities and services when they’re needed.

And the public’s opinion about the business of running hospitals is relatively uninformed beyond their anecdotal use experiences that shape their perceptions. Thus, claims by not-for-profit hospital officials that their finances are teetering on insolvency fall on deaf ears, especially in communities where cranes hover above their patient towers and their brands are ubiquitous.

Demand for hospital services is increasing and shifting, wage and supply costs (including prescription drugs) are soaring, and resources are limited for most.

The size, scale and CEO compensation for the biggest not-for-profit health systems pale in comparison to their counterparts in health insurance and prescription drug manufacturing or even the biggest investor-owned health system, HCA…but that’s not the point.

NFPs are being challenged to demonstrate they merit the tax-exempt treatment they enjoy unlike their investor-owned and public hospital competitors and that’s been a moving target.

Thus, the methodology for consistently defining and accounting for community benefits needs attention. That would be a good start but alone it will not solve the more fundamental issue: what’s the future for the U.S. health system, what role do players including hospitals and others need to play, and how should it be structured and funded?

The issues facing the U.S. health industry are complex. The role hospitals will play is also uncertain. If, as polls indicate, the majority of Americans prefer a private health system that features competition, transparency, affordability and equitable access, the remedy will require input from every major healthcare sector including employers, public health, private capital and regulators alongside others.

It will require less from DC policy wonks and sanctimonious talking heads and more from frontline efforts and privately-backed innovators in communities, companies and in not-for-profit health systems that take community benefit seriously.

No sector owns the franchise for certainty about the future of U.S. healthcare nor its moral high ground. That includes not-for-profit hospitals.

The darkening cloud that hovers over not-for-profit health systems needs attention, but not alone, despite efforts to suggest otherwise.

Clarifying the community-benefit standard is a start, but not enough.

Are NFP hospitals a problem? Some are, most aren’t but all are impacted by the darkening cloud.

Last Friday, the Centers for Medicare and Medicaid Services (CMS) announced that it will begin phasing in major Medicare Advantage (MA) risk-adjustment changes over a three-year period, slower than previously anticipated. Thanks to this delay in full implementation, MA plans will see an average 3.3 percent payment increase in 2024, up from the one percent projected in the earlier draft notice.

CMS also finalized regulations this week that aim to limit MA prior authorizations and denials by requiring that coverage decisions align with traditional Medicare.

The Gist: After CMS began proposing changes to MA payment formulas last year, aimed at reining in pervasive abuses and fraud,

the insurance industry responded with a $13M marketing blitz to oppose the changes.

The ads, one of which aired during the Super Bowl, tied Medicare Advantage “cuts” to the time-tested “Hands Off My Medicare” messaging directed at seniors.

With MA enrollment projected to overtake traditional Medicare this year,the federal government finds itself walking a tightrope in clamping down on overpayments to MA plans, given that any reductions will impact a growing number of seniors.

The AHA has previously noted the third party observers who demonstrate a tenuous grasp of the data and rules regarding federal hospital transparency requirements. Now, some of those same entities with deep pockets and an apparent vendetta against hospitals and health systems have turned their attention toward the broader financial challenges facing the field. The results, as described in a recent Health Affairs blog, are as expected — a complete misunderstanding of current economic realities.

The three most egregious suggestions in this piece are that hospitals are seeking some kind of bailout from the federal government, employers and patients; that investment losses are the most problematic aspect of hospital financing; and that hospitals’ analyses of their financial situation are dishonest.

We debunk these in turn.

Hospitals are seeking fair compensation, not a government bailout. The authors state that hospitals are asking “constituents to foot the bill for hospitals’ investment losses.” This is patently false. Indeed, if you read the request we made to Congress cited in their blog, hospitals and health systems are simply asking to get paid for the care they deliver or to lower unnecessary administrative costs. This includes asking Medicare to pay for the days hospitals care for patients who are otherwise ready for discharge. Increasingly, this has occurred because there is no space in the next site of care or the patient’s insurer has delayed the authorization for that care. Keeping someone in a hospital bed for days, if not weeks, requires skilled labor, supplies and basic infrastructure costs. This doesn’t even account for the impact on a patient’s health for not being in the most appropriate care setting. Today, hospitals are not paid for these days. Asking for fair compensation is not a bailout; it is a basic responsibility of any purchaser.

While investment income may be down, hospitals and health systems have faced massive expense increases in the last year. The authors note that patient care revenue was up “by just below 1 percent in relative terms from 2021 to 2022,” suggesting that implies a positive financial trend. However, hospital total expenses were up 7% in 2022 over 2021, and were up by even more, 20%, when compared to pre-pandemic levels, according to Kaufman Hall. And it’s not just the AHA and Kaufman Hall saying this either: in its 2023 outlook, credit rating agency Moody’s noted that “margins will remain constrained by high expenses.” Hospitals should not need to rely on investment income for operations. However, many have been forced into this situation by substantial underpayments from their largest payers (Medicare and Medicaid), which even the Medicare Payment Advisory Commission (MedPAC), an independent advisor to Congress, has acknowledged. MedPAC’s most recent report showed a negative 8.3% Medicare operating margin. Hospitals and health systems are experiencing run-away increases in the supplies, labor and technology needed to care for patients. At the same time, commercial insurance companies are increasing their use of policies that can cause dangerous delays in care for patients, result in undue burden on health care providers and add billions of dollars in unnecessary costs to the health care system.

Hospitals and health systems are committed to an honest examination of the facts. The authors imply that the studies documenting hospitals’ financial distress are biased. They note that certain studies conducted by Kaufman Hall are based on proprietary data and therefore “challenging to draw general inferences.” They then go on to cherry-pick metrics from specific non-profit health care systems voluntarily released financial disclosures to make general claims about “the primary driver of hospitals’ financial strain.” The authors and their financial backers clearly seem to have a preconceived narrative, and ignore all the other realities that hospital and health system leaders are confronting every day to ensure access to care and programs for the patients and communities they serve.

It is imperative to acknowledge financial challenges facing hospitals and health systems today. Too much is at stake for the patients and communities that depend upon hospitals and health systems to be there, ready to care.

I have been both a frontline officer and a staff officer at a health system. I started a solo practice in 1977 and cared for my rheumatology, internal medicine and geriatrics patients in inpatient and outpatient settings. After 23 years in my solo practice, I served 18 years as President and CEO of a profitable, CMS 5-star, 715-bed, two-hospital healthcare system.

From 2015 to 2020, our health system team added 0.6 years of healthy life expectancy for 400,000 folks across the socioeconomic spectrum. We simultaneously decreased healthcare costs 54% for 6,000 colleagues and family members. With our mentoring, four other large, self-insured organizations enjoyed similar measurable results. We wanted to put our healthcare system out of business. Who wants to spend a night in a hospital?

During the frontline part of my career, I had the privilege of “Being in the Room Where It Happens,” be it the examination room at the start of a patient encounter, or at the end of life providing comfort and consoling family. Subsequently, I sat at the head of the table, responsible for most of the hospital care in Southwest Florida. [1]

Many folks commenting on healthcare have never touched a patient nor led a large system. Outside consultants, no matter how competent, have vicarious experience that creates a different perspective.

At this point in my career, I have the luxury of promoting what I believe is in the best interests of patients — prevention and quality outcomes. Keeping folks healthy and changing the healthcare industry’s focus from a “repair shop” mentality to a “prevention program” will save the industry and country from bankruptcy. Avoiding well-meaning but inadvertent suboptimal care by restructuring healthcare delivery avoids misery and saves lives.

RESPONDING TO AN ATTACK

Preemptive reinvention is much wiser than responding to an attack. Unfortunately, few industries embrace prevention. The entire healthcare industry, including health systems, physicians, non-physician caregivers, device manufacturers, pharmaceutical firms, and medical insurers, is stressed because most are experiencing serious profit margin squeeze. Simultaneously the public has ongoing concerns about healthcare costs. While some medical insurance companies enjoyed lavish profits during COVID, most of the industry suffered. Examples abound, and Paul Keckley, considered a dean among long-time observers of the medical field, recently highlighted some striking year-end observations for 2022. [2]

Recent Siege Examples

Transparency is generally good but can and has led to tarnishing the noble profession of caring for others. Namely, once a sector starts bleeding, others come along, exacerbating the exsanguination. Current literature is full of unflattering public articles that seem to self-perpetuate, and I’ve highlighted standout samples below.

The Federal Government is the largest spender in the healthcare industry and therefore the most influential. Not surprisingly, congressional lobbying was intense during the last two weeks of 2022 in a partially successful effort to ameliorate spending cuts for Medicare payments for physicians and hospitals. Lobbying spend by Big Pharma, Blue Cross/Blue Shield, American Hospital Association, and American Medical Association are all in the top ten spenders again. [3, 4, 5] These organizations aren’t lobbying for prevention, they’re lobbying to keep the status quo.

Concern about consistent quality should always be top of mind. “Diagnostic Errors in the Emergency Department: A Systematic Review,” shared by the Agency for Healthcare Research and Quality, compiled 279 studies showing a nearly 6% error rate for the 130 million people who visit an ED yearly. Stroke, heart attack, aortic aneurysm, spinal cord injury, and venous thromboembolism were the most common harms. The defense of diagnostic errors in emergency situations is deemed of secondary importance to stabilizing the patient for subsequent diagnosing. Keeping patients alive trumps everything. Commonly, patient ED presentations are not clear-cut with both false positive and negative findings. Retrospectively, what was obscure can become obvious. [6, 7]

Spending mirrors motivations. The Wall Street Journal article “Many Hospitals Get Big Drug Discounts. That Doesn’t Mean Markdowns for Patients” lays out how the savings from a decades-old federal program that offers big drug discounts to hospitals generally stay with the hospitals. Hospitals can chose to sell the prescriptions to patients and their insurers for much more than the discounted price. Originally the legislation was designed for resource-challenged communities, but now some hospitals in these programs are profiting from wealthy folks paying normal prices and the hospitals keeping the difference. [8]

“Hundreds of Hospitals Sue Patients or Threaten Their Credit, a KHN Investigation Finds. Does Yours?” Medical debt is a large and growing problem for both patients and providers. Healthcare systems employ collection agencies that typically assess and screen a patient’s ability to pay. If the credit agency determines a patient has resources and has avoided paying his/her debt, the health system send those bills to a collection agency. Most often legitimately impoverished folks are left alone, but about two-thirds of patients who could pay but lack adequate medical insurance face lawsuits and other legal actions attempting to collect payment including garnishing wages or placing liens on property. [9]

“Hospital Monopolies Are Destroying Health Care Value,” written by Rep. Victoria Spartz (R-Ind.) in The Hill, includes a statement attributed to Adam Smith’s The Wealth of Nations, “that the law which facilitates consolidation ends in a conspiracy against the public to raise prices.” The country has seen over 1,500 hospital mergers in the past twenty years — an example of horizontal consolidation. Hospitals also consolidate vertically by acquiring physician practices. As of January 2022, 74 percent of physicians work directly for hospitals, healthcare systems, other physicians, or corporate entities, causing not only the loss of independent physicians but also tighter control of pricing and financial issues. [10] The healthcare industry is an attractive target to examine. Everyone has had meaningful healthcare experiences, many have had expensive and impactful experiences. Although patients do not typically understand the complexity of providing a diagnosis, treatment, and prognosis, the care receiver may compare the experience to less-complex interactions outside healthcare that are customer centric and more satisfying.

PROFIT-MARGIN SQUEEZE

Both nonprofit and for-profit hospitals must publish financial statements. Three major bond rating agencies (Fitch Ratings, Moody’s Investors Service, and S & P Global Ratings) and other respected observers like KaufmanHall, collate, review, and analyze this publicly available information and rate health systems’ financial stability.

One measure of healthcare system’s financial strength is operating margin, the amount of profit or loss from caring for patients. In January of 2023 the median, or middle value, of hospital operating margin index was -1.0%, which is an improvement from January 2022 but still lags 2021 and 2020.

Erik Swanson, SVP at KaufmanHall, says 2022,

“Is shaping up to be one of the worst financial years on record for hospitals. Expense pressures — particularly with the cost of labor — outpaced revenues and drove poor performance. While emergency department visits and operating room minutes increased slightly, hospitals struggled to discharge patients due to internal staffing shortages and shortages at post-acute facilities,” [11]

Another force exacerbating health system finance is the competent, if relatively new retailers (CVS, Walmart, Walgreens, and others) that provide routine outpatient care affordably. Ninety percent of Americans live within ten miles of a Walmart and 50% visit weekly. CVS and Walgreens enjoy similar penetration. Profit-margin squeeze, combined with new convenient options to obtain routine care locally, will continue disrupting legacy healthcare systems.

Providers generate profits when patients access care. Additionally, “easy” profitable outpatient care can and has switched to telemedicine. Kaiser-Permanente (KP), even before the pandemic, provided about 50% of the system’s care through virtual visits. Insurance companies profit when services are provided efficiently or when members don’t use services. KP has the enviable position of being both the provider and payor for their members. The balance between KP’s insurance company and provider company favors efficient use of limited resources. Since COVID, 80% of all KP’s visits are virtual, a fact that decreases overhead, resulting in improved profit margins. [12]

On the other hand, KP does feel the profit-margin squeeze because labor costs have risen. To avoid a nurse labor strike, KP gave 21,000 nurses and nurse practitioners a 22.5% raise over four years. KP’s most recent quarter reported a net loss of $1.5B, possibly due to increased overhead. [13]

The public, governmental agencies, and some healthcare leaders are searching for a more efficient system with better outcomes

at a lower cost. Our nation cannot continue to spend the most money of any developed nation and have the worst outcomes. In a globally competitive world, limited resources must go to effective healthcare, balanced with education, infrastructure, the environment, and other societal needs. A new healthcare model could satisfy all these desires and needs.

Even iconic giants are starting to feel the pain of recent annual losses in the billions. Ascension Health, Cleveland Clinic, Jefferson Health, Massachusetts General Hospital, ProMedica, Providence, UPMC, and many others have gone from stable and sustainable to stressed and uncertain. Mayo Clinic had been a notable exception, but recently even this esteemed system’s profit dropped by more than 50% in 2022 with higher wage and supply costs up, according to this Modern Healthcare summary. [14]

The alarming point is even the big multigenerational health system leaders who believed they had fortress balance sheets are struggling. Those systems with decades of financial success and esteemed reputations are in jeopardy. Changing leadership doesn’t change the new environment.

Nonprofit healthcare systems’ income typically comes from three sources — operations, namely caring for patients in ways that are now evolving as noted above; investments, which are inherently risky evidence by this past year’s record losses; and philanthropy, which remains fickle particularly when other investment returns disappoint potential donors. For-profit healthcare systems don’t have the luxury of philanthropic support but typically are more efficient with scale and scope.

The most stable and predictable source of revenue in the past was from patient care. As the healthcare industry’s cost to society continues to increase above 20% of the GDP, most medically self-insured employers and other payors will search for efficiencies. Like it or not, persistently negative profit margins will transform healthcare.

Demand for nurses, physicians, and support folks is increasing, with many shortages looming near term. Labor costs and burnout have become pressing stresses, but more efficient delivery of care and better tools can ameliorate the stress somewhat. If structural process and technology tools can improve productivity per employee, the long-term supply of clinicians may keep up. Additionally, a decreased demand for care resulting from an effective prevention strategy also could help.

Most other successful industries work hard to produce products or services with fewer people. Remember what the industrial revolution did for America by increasing the productivity of each person in the early 1900s. Thereafter, manufacturing needed fewer employees.

PATIENTS’ NEEDS AND DESIRES

Patients want to live a long, happy and healthy life. The best way to do this is to avoid illness, which patients can do with prevention because 80% of disease is self-inflicted. When prevention fails, or the 20% of unstoppable episodic illness kicks in, patients should seek the best care.

The choice of the “best care” should not necessarily rest just on convenience but rather objective outcomes. Closest to home may be important for take-out food, but not healthcare.

Care typically can be divided into three categories — acute, urgent, and elective. Common examples of acute care include childbirth, heart attack, stroke, major trauma, overdoses, ruptured major blood vessel, and similar immediate, life-threatening conditions. Urgent intervention examples include an acute abdomen, gall bladder inflammation, appendicitis, severe undiagnosed pain and other conditions that typically have positive outcomes even with a modest delay of a few hours.

Most every other condition can be cared for in an appropriate timeframe that allows for a car trip of a few hours. These illnesses can range in severity from benign that typically resolve on their own to serious, which are life-threatening if left undiagnosed and untreated. Musculoskeletal aches are benign while cancer is life-threatening if not identified and treated.

Getting the right diagnosis and treatment for both benign and malignant conditions is crucial but we’re not even near perfect for either. That’s unsettling.

In a 2017 study,

“Mayo Clinic reports that as many as 88 percent of those patients [who travel to Mayo] go home [after getting a second opinion] with a new or refined diagnosis — changing their care plan and potentially their lives. Conversely, only 12 percent receive confirmation that the original diagnosis was complete and correct. In 21 percent of the cases, the diagnosis was completely changed; and 66 percent of patients received a refined or redefined diagnosis. There were no significant differences between provider types [physician and non-physician caregivers].” [15]

The frequency of significant mis- or refined-diagnosis and treatment should send chills up your spine. With healthcare we are not talking about trivial concerns like a bad meal at a restaurant, we are discussing life-threatening risks. Making an initial, correct first decision has a tremendous influence on your outcome.

Sleeping in your own bed is nice but secondary to obtaining the best outcome possible, even if car or plane travel are necessary. For urgent and elective diagnosis/treatment, travel may be a

good option. Acute illness usually doesn’t permit a few hours of grace, although a surprising number of stroke and heart attack victims delay treatment through denial or overnight timing. But even most of these delayed, recognized illnesses usually survive. And urgent and elective care gives the patient the luxury of some time to get to a location that delivers proven, objective outcomes, not necessarily the one closest to home.

Measuring quality in healthcare has traditionally been difficult for the average patient. Roadside billboards, commercials, displays at major sporting events, fancy logos, name changes and image building campaigns do not relate to quality. Confusingly, some heavily advertised metrics rely on a combination of subjective reputational and lagging objective measures. Most consumers don’t know enough about the sources of information to understand which ratings are meaningful to outcomes.

Arguably, hospital quality star ratings created by the Centers for Medicare and Medicaid Services (CMS) are the best information for potential patients to rate hospital mortality, safety, readmission, patient experience, and timely/effective care. These five categories combine 47 of the more than 100 measures CMS publicly reports. [16]

A 2017 JAMA article by lead author Dr. Ashish Jha said:

“Found that a higher CMS star rating was associated with lower patient mortality and readmissions. It is reassuring that patients can use the star ratings in guiding their health care seeking decisions given that hospitals with more stars not only offer a better experience of care, but also have lower mortality and readmissions.”

The study included only Medicare patients who typically are over 65, and the differences were most apparent at the extremes, nevertheless,

“These findings should be encouraging for policymakers and consumers; choosing 5-star hospitals does not seem to lead to worse outcomes and in fact may be driving patients to better institutions.” [17]

Developing more 5-star hospitals is not only better and safer for patients but also will save resources by avoiding expensive complications and suffering.

As a patient, doing your homework before you have an urgent or elective need can change your outcome for the better. Driving a

couple of hours to a CMS 5-star hospital or flying to a specialty hospital for an elective procedure could make a difference.

Business case studies have noted that hospitals with a focus on a specific condition deliver improved outcomes while becoming more efficient. [18] Similarly, specialty surgical areas within general hospitals have also been effective in improving quality while reducing costs. Mayo Clinic demonstrated this with its cardiac surgery department. [19] A similar example is Shouldice Hospital near Toronto, a focused factory specializing in hernia repairs. In the last 75 years, the Shouldice team has completed four hundred thousand hernia repairs, mostly performed under local anesthesia with the patient walking to and from the operating room. [20] [21]

THE BOTTOM LINE

The Mayo Brother’s quote, “The patient’s needs come first,” is more relevant today than when first articulated over a century ago. Driving treatment into distinct categories of acute, urgent, and elective, with subsequent directing care to the appropriate facilities, improves the entire care process for the patient. The saved resources can fund prevention and decrease the need for future care. The healthcare industry’s focus has been on sickness,

not prevention. The virtuous cycle’s flywheel effect of distinct categories for care and embracing prevention of illness will decrease misery and lower the percentage of GDP devoted to healthcare.

Editor’s note: This is a multi-part series on reinventing the healthcare industry. Part 2 addresses physicians, non-physician caregivers, and communities’ responses to the coming transformation.

The pharmaceutical industry is on the verge of defeating a major Democratic proposal that would allow the federal government to negotiate drug prices.

Speaker Nancy Pelosi (D-Calif.) can afford only three defections when the House votes on a sweeping $3.5 trillion spending package, but Reps. Scott Peters (D-Calif.), Kurt Schrader (D-Ore.) and Kathleen Rice (D-N.Y.) last week voted to block the drug pricing bill from advancing out of the Energy and Commerce Committee. Rep. Stephanie Murphy (D-Fla.) voted against advancing the tax portion of the legislation in the House Ways and Means Committee.

All told, the number of House Democrats who have concerns about the drug pricing bill is in the double digits, and several Democrats in the 50-50 Senate would not vote for the measure in its current form, according to industry lobbyists.

The holdouts mark a sharp contrast to just two years ago, when every House Democrat voted for the same drug pricing bill, underscoring the inroads pharmaceutical manufacturers have made with the caucus on a measure that would narrow corporate profit margins.

“The House markups on health care demonstrate there are real concerns with Speaker Pelosi’s extreme drug pricing plan and those concerns are shared by thoughtful lawmakers on both sides of the aisle,” the Pharmaceutical Research and Manufacturers of America (PhRMA), the industry’s top trade group, said in a statement following the committee votes.

The reversal follows the industry’s multimillion-dollar ad campaigns opposing the bill, timely political donations and an extensive lobbying effort stressing drugmakers’ success in swiftly developing lifesaving COVID-19 vaccines.

The bill at the center of the fight, H.R. 3, would allow Medicare to negotiate the price of prescription drugs by tying them to the lower prices paid by other high-income countries. The measure is projected to free up around $700 billion through the money it saves on drug purchases — covering a big chunk of the Democrats’ $3.5 trillion spending plan.

Drugmakers say the measure would reduce innovation, pointing to a Congressional Budget Office estimate that found it would lead to nearly 60 fewer new drugs over the next three decades.

Peters and other Democrats have proposed an alternative bill that would limit price negotiation to a fraction of the prescription drugs included in H.R. 3, focusing instead on drugs like insulin, the diabetes treatment that has seen its price rise dramatically over the last decade. The alternative measure also would set a yearly out-of-pocket spending limit for lower-income Medicare recipients.

The proposal foreshadows a less aggressive drug pricing compromise that uneasy Senate Democrats are more likely to get behind.

“You’re going to see something pass, but it probably won’t be H.R. 3,” said a lobbyist who represents pharmaceutical companies.

Pharmaceutical manufacturers oppose any efforts to control the price of prescription drugs, but the alternative bill is more favorable to the industry than the broader Democratic bill.

“Any kind of artificial price controls will have an impact on both new scientific investment as well as access to medicines,” said Rich Masters, chief public affairs and advocacy officer at the Biotechnology Innovation Organization, a trade group that represents pharmaceutical giants such as Sanofi, Merck and Johnson & Johnson.

“We appreciate the focus on patient out of pocket costs, which we know is a critical component to any reform efforts and something that BIO and our member companies have long supported,” he added.

Progressive lawmakers, who have long bemoaned rising drug prices, blasted the three House Democrats who voted to block H.R. 3, saying they succumbed to industry donations and lobbying efforts.

“What the pharmaceutical industry has done, year after year, is pour huge amounts of money into lobbying and campaign contributions … the result is that they can raise their prices to any level they want,” Sen. Bernie Sanders (I-Vt.) said in a video message Friday.

The pharmaceutical industry spent $171 million on lobbying through the first half of the year, more than any other industry, to deploy nearly 1,500 lobbyists, according to money-in-politics watchdog OpenSecrets. That’s up from around $160 million at the same point last year, when the industry broke its own lobbying spending record.

Peters announced his opposition to Pelosi’s drug pricing proposal in May and shortly after was showered with donations from pharmaceutical industry executives and lobbyists, STAT News reported.

Peters is the No. 1 House recipient of pharmaceutical industry donations this year, bringing in $88,550 from pharmaceutical executives and PACs, according to OpenSecrets. Over his congressional career, Peters has received in excess of $860,000 from drugmakers, more than any other private industry.

The California Democrat told The Hill last week that accusations of his vote being guided by donations are “flat wrong” and noted that his San Diego congressional district employs roughly 27,000 pharmaceutical industry workers consisting mostly of researchers.

“It’s always going to be the attack because it’s simple and it’s easier than engaging on the merits,” he said.

Schrader received nearly $615,000 from the industry. He inherited a fortune from his grandfather, a former top executive at Pfizer, and had between $50,000 and $100,000 invested in Pfizer, in addition to other pharmaceutical holdings as of last year, according to his most recent annual financial disclosure.

Schrader tweeted last week that he is “committed to lowering prescription drug costs,” while arguing that the House bill would not pass the Senate in its current form.

Rep. Lou Correa (D-Calif.) another supporter of Peters’s more industry friendly bill, received an influx of pharmaceutical donations in recent months, including a $2,000 check from Pfizer’s PAC in mid-August, according to Federal Election Commission filings.

In meetings with lawmakers, lobbyists have argued that now is not the time to go after drugmakers, which developed highly effective COVID-19 vaccines and are developing booster shots and other treatments to fight the virus.

The U.S. Chamber of Commerce, which represents several major pharmaceutical manufacturers, said last month that Democratic drug pricing efforts will leave the U.S. “unprepared for the next public health crisis.”

PhRMA last week launched a seven-figure ad campaign to oppose H.R. 3. That’s after pharmaceutical groups and conservative organizations bankrolled by drugmakers spent $18 million on ads attacking the proposal through late August, according to an analysis from Patients for Affordable Drugs, a group that launched its own ads backing H.R. 3 last week.

The ad buys are meant to sway both lawmakers and the general public. A June Kaiser Family Foundation poll found that 90 percent of Americans approve of the drug pricing measure, but that support dropped to 32 percent when they were told that the proposal “could lead to less research and development of new drugs.”

With a $56,000-a-year price tag, Biogen’s newly approved Alzheimer’s drug Aduhelm is dovetailing into the debate on Capitol Hill over how to lower prescription drug prices.

Why it matters:Democrats may be positioning themselves to push policy measures that assign value to drugs and then price them accordingly — a huge potential blow to the pharmaceutical industry.

To truly address its launch price, policymakers have to grapple with big questions the U.S. system currently avoids: How should we determine the value of a drug, and who gets to make that decision?

President Biden proposed giving an independent review board the power to determine the Medicare rate for new drugs that don’t have any competition.

Democrats’ most prominent drug legislation is a House bill that gives Medicare the power to negotiate drug prices.

Sen. Ron Wyden, the chairman of the Senate Finance Committee, recently called out Aduhelm by name in a document outlining the principles that will guide the Senate’s drug pricing bill, a hint that the Senate’s legislation will take a different direction than the House’s.

The bottom line:“Any kind of process for valuing new drugs like Aduhelm take you immediately into the controversial quagmire of how to quantify improvements in quality of life for people,” said KFF’s Larry Levitt.

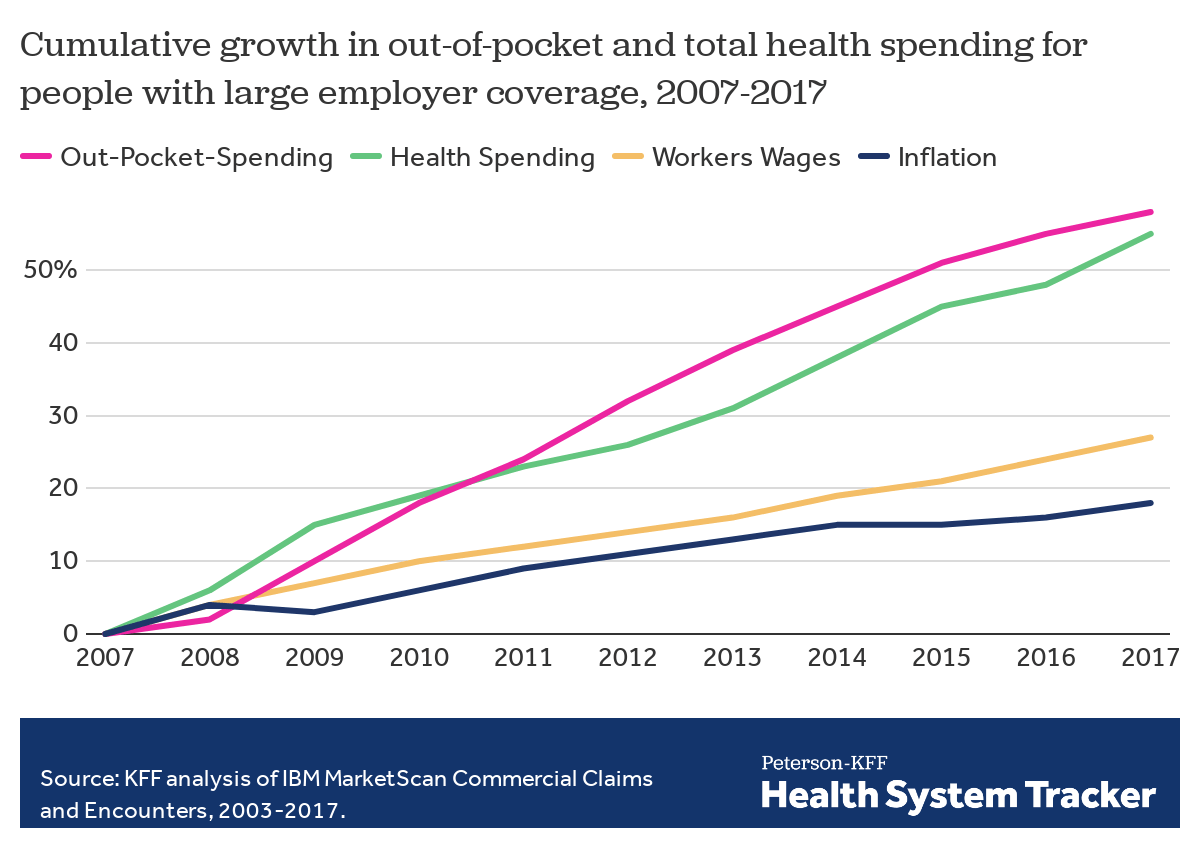

Employers — including companies, state governments and universities — purchase health care on behalf of roughly 150 million Americans. The cost of that care has continued to climb for both businesses and their workers.

For many years, employers saw wasteful care as the primary driver of their rising costs. They made benefits changes like adding wellness programs and raising deductibles to reduce unnecessary care, but costs continued to rise. Now, driven by a combination of new research and changing market forces — especially hospital consolidation — more employers see prices as their primary problem.

By amassing and analyzing employers’ claims data in innovative ways, academics and researchers at organizations like the Health Care Cost Institute (HCCI) and RAND have helped illuminate for employers two key truths about the hospital-based health care they purchase:

1) PRICES VARY WIDELY FOR THE SAME SERVICES

Data show that providers charge private payers very different prices for the exact same services — even within the same geographic area.

For example, HCCI found the price of a C-section delivery in the San Francisco Bay Area varies between hospitals by as much as:$24,107

Data show that hospitals charge employers and private insurers, on average, roughly twice what they charge Medicare for the exact same services. A recent RAND study analyzed more than 3,000 hospitals’ prices and found the most expensive facility in the country charged employers:4.1xMedicare

Hospitals claim this price difference is necessary because public payers like Medicare do not pay enough. However, there is a wide gap between the amount hospitals lose on Medicare (around -9% for inpatient care) and the amount more they charge employers compared to Medicare (200% or more).

Employer Efforts

A small but growing group of companies, public employers (like state governments and universities) and unions is using new data and tactics to tackle these high prices. (Learn more about who’s leading this work, how and why by listening to our full podcast episode in the player above.)

Note that the employers leading this charge tend to be large and self-funded, meaning they shoulder the risk for the insurance they provide employees, giving them extra flexibility and motivation to purchase health care differently. The approaches they are taking include:

Steering Employees

Some employers are implementing so-called tiered networks, where employees pay more if they want to continue seeing certain, more expensive providers. Others are trying to strongly steer employees to particular hospitals, sometimes know as centers of excellence, where employers have made special deals for particular services.

Purdue University, for example, covers travel and lodging and offers a $500 stipend to employees that get hip or knee replacements done at one Indiana hospital.

Negotiating New Deals

There is a movement among some employers to renegotiate hospital deals using Medicare rates as the baseline — since they are transparent and account for hospitals’ unique attributes like location and patient mix — as opposed to negotiating down from charges set by hospitals, which are seen by many as opaque and arbitrary. Other employers are pressuring their insurance carriers to renegotiate the contracts they have with hospitals.

In 2016, the Montana state employee health plan, led by Marilyn Bartlett, got all of the state’s hospitals to agree to a payment rate based on a multiple of Medicare. They saved more than $30 million in just three years. Bartlett is now advising other states trying to follow her playbook.

In 2020, several large Indiana employers urged insurance carrier Anthem to renegotiate their contract with Parkview Health, a hospital system RAND researchers identified as one of the most expensive in the country. After months of tense back-and-forth, the pair reached a five-year deal expected to save Anthem customers $700 million.

Legislating, Regulating, Litigating

Some employer coalitions are advocating for more intervention by policymakers to cap health care prices or at least make them more transparent. States like Colorado and Indiana have passed price transparency legislation, and new federal rules now require more hospital price transparency on a national level. Advocates expect strong industry opposition to stiffer measures, like price caps, which recently failed in the Montana legislature.

Other advocates are calling for more scrutiny by state and federal officials of hospital mergers and other anticompetitive practices. Some employers and unions have even resorted to suing hospitals like Sutter Health in California.

Employer Challenges

Employers face a few key barriers to purchasing health care in different and more efficient ways:

Provider Power

Hospitals tend to have much more market power than individual employers, and that power has grown in recent years, enabling them to raise prices. Even very large employers have geographically dispersed workforces, making it hard to exert much leverage over any given hospital. Some employers have tried forming purchasing coalitions to pool their buying power, but they face tricky organizational dynamics and laws that prohibit collusion.

Sophistication

Employers can attempt to lower prices by renegotiating contracts with hospitals or tailoring provider networks, but the work is complicated and rife with tradeoffs. Few employers are sophisticated enough, for example, to assess a provider’s quality or to structure hospital payments in new ways.Employers looking for insurers to help them have limited options, as that industry has also become highly consolidated.

Employee Blowback

Employers say they primarily provide benefits to recruit and retain happy and healthy employees. Many are reluctant to risk upsetting employees by cutting out expensive providers or redesigning benefits in other ways. A recent KFF survey found just 4% of employers had dropped a hospital in order to cut costs.

The Tradeoffs

Employers play a unique role in the United States health care system, and in the lives of the 150 million Americans who get insurance through work. For years, critics have questioned the wisdom of an employer-based health care system, and massive job losses created by the pandemic have reinforced those doubts for many.

Assuming employers do continue to purchase insurance on behalf of millions of Americans, though, focusing on lowering the prices they pay is one promising path to lowering total costs. However, as noted above, hospitals have expressed concern over the financial pressures they may face under these new deals. Complex benefit design strategies, like narrow or tiered networks, also run the risk of harming employees, who may make suboptimal choices or experience cost surprises. Finally, these strategies do not necessarily address other drivers of high costs including drug prices and wasteful care.