MedPAC’s recommendation that acute care hospitals don’t need a significant increase in 2024 Medicare rates is “totally insufficient and out of touch with reality,” according to the American Hospital Association.

“This view is one-sided, inaccurate and misleading,” Ashley Thompson, AHA’s senior vice president of public policy analysis and development, wrote in a March 23 blog post. “After years of once-in-a-lifetime events in the form of a global pandemic and record inflation, hospitals across the country are struggling to continue to fulfill their mission to care for their patients and communities.”

In its annual March report to Congress, MedPAC recommended an update to hospital payment rates of “current law plus 1 percent,” which the AHA says is not enough for many hospitals to keep their doors open.

The commission found that most indicators of sufficient Medicare rates for providers were positive or improved in 2021, though it acknowledged that hospitals saw more volatile cost increases in 2022 compared to years prior. Hospital margins were also lower last year than in 2021, according to preliminary data, driven in part by providers facing higher than expected costs and capacity and staffing challenges.

The report also said that its 2024 payment recommendations “may not be sufficient” to sustain some safety-net hospitals with a low number of commercially insured patients, and proposed $2 billion in add-on payments.

Across the U.S., a total of 631 rural hospitals — or about 30 percent of all rural hospitals — are at risk of closing in the immediate or near future.

MedPAC’s recommendations for 2024 differ from how some health economists have recently described hospitals’ finances. In January, hospitals had a median operating margin of -1 percent according to Kaufman Hall, a finding that arrived on the heels of 2022 being named the worst financial year for hospitals since the start of the COVID-19 pandemic.

“It is also important to realize that MedPAC’s report and data has limitations,” Ms. Thompson wrote, referring to a misalignment in the calendar year MedPAC chose to analyze and how hospitals can differ in how they report their individual financial earnings.

MedPAC said its report reflects 2021 data, preliminary data from 2022, and projections for 2023, along with recent inflation rates.

“…cost reports are filed for hospitals’ own specific fiscal years, and because surges, relief payments, and eventual expense increases happened at different times for different hospitals, these calculated margins don’t necessarily provide a fully accurate picture of the financial reality in 2021,” Ms. Thompson wrote.

The AHA stressed that hospitals’ finances in 2023 face much different challenges compared to 2021, when the industry was more supported by strong investment returns and federal pandemic relief.

“The fact that massive numbers of hospitals are not currently closing due to financial pressures should be seen as positive for patients and communities,” Ms. Thompson said. “Instead, some observers seem to be disappointed that more hospitals are not failing financially.”

A detailed response from the AHA to the MedPAC report is available here.

As the U.S. prepares to end the COVID-19 public health emergency, hospitals are facing a major cut in Medicare payments used to treat patients diagnosed with the disease.

Since January 2020, hospitals nationwide have received a 20 percent increase in the Medicare payment rate through the hospital inpatient prospective payment system to treat COVID-19 patients — that policy ends May 11.

The sunsetting of the three-year policy is a key concern for the AHA because of its financial implication for hospitals already struggling with increased labor costs and inflation.

From January 2020 to November 2021, payments for the 1 million traditional Medicare patients hospitalized with COVID-19 totaled $23.4 billion, or more than $24,000 per patient, according to lobbying and law firm Brownstein.

The end of the policy also has the potential to increase medical costs for patients hospitalized with COVID-19. If patients must pay higher costs for COVID-19-related services, they may be less inclined to get tested or even seek treatment.

“It means there will be less testing in this country, and likely less treatment because not everyone can afford it,” Jose Figueroa, MD, assistant professor of health policy and management at the Harvard T.H. Chan School of Public Health, told Time Jan. 31. “Will this change the trajectory of the pandemic? It’s something we are going to have to watch.”

As of Feb. 8, the nation’s seven-day COVID-19 case average was 40,404, a 1 percent decrease from the previous week’s average. The rate of decrease has slowed in the last two weeks — the CDC’s last weekly report published Feb. 3 reported a 6.7 percent drop in cases.

The seven-day hospitalization average for Feb. 1-7 was 3,665, a 6.2 percent decrease from the previous week’s average and down from an 8.4 percent drop in cases a week prior.

Last week the Biden Administration announced that the federal COVID public health emergency (PHE) will expire on May 11. While the recent Omnibus law will lessen the impact, the graphic above highlights several important provisions for providers which are currently set to end with the PHE.

The Centers for Medicare and Medicaid Services (CMS) will no longer provide hospitals with a 20 percent inpatient payment boost for treating traditional Medicare patients hospitalized with COVID. The cost of COVID testing and treatments will shift from the federal government to consumers as private and public insurers can charge for tests and care, while the uninsured will bear the full costs of COVID vaccines and treatment.

Medicare’s current flexibilities around skilled nursing facility (SNF) admissions will end, as it reinstates the three-day prior hospitalization rule for SNF transfers, and ceases paying for SNF stays beyond 100 days.

The end of the PHE also means that providers willno longer be able to prescribe controlled substances virtually, without an initial in-person evaluation. This is especially significant given the volume of mental health and substance abuse treatment that shifted to telehealth across the course of the pandemic.

While the Drug Enforcement Agency has been working on regulations to address this, a proposed rule has not yet been released. Together, these changes amount tolower payments for health systems, COVID cost exposure for patients, and fewer flexibilities for providers managing care, even as thousands of patients are still being hospitalized with COVID each week.

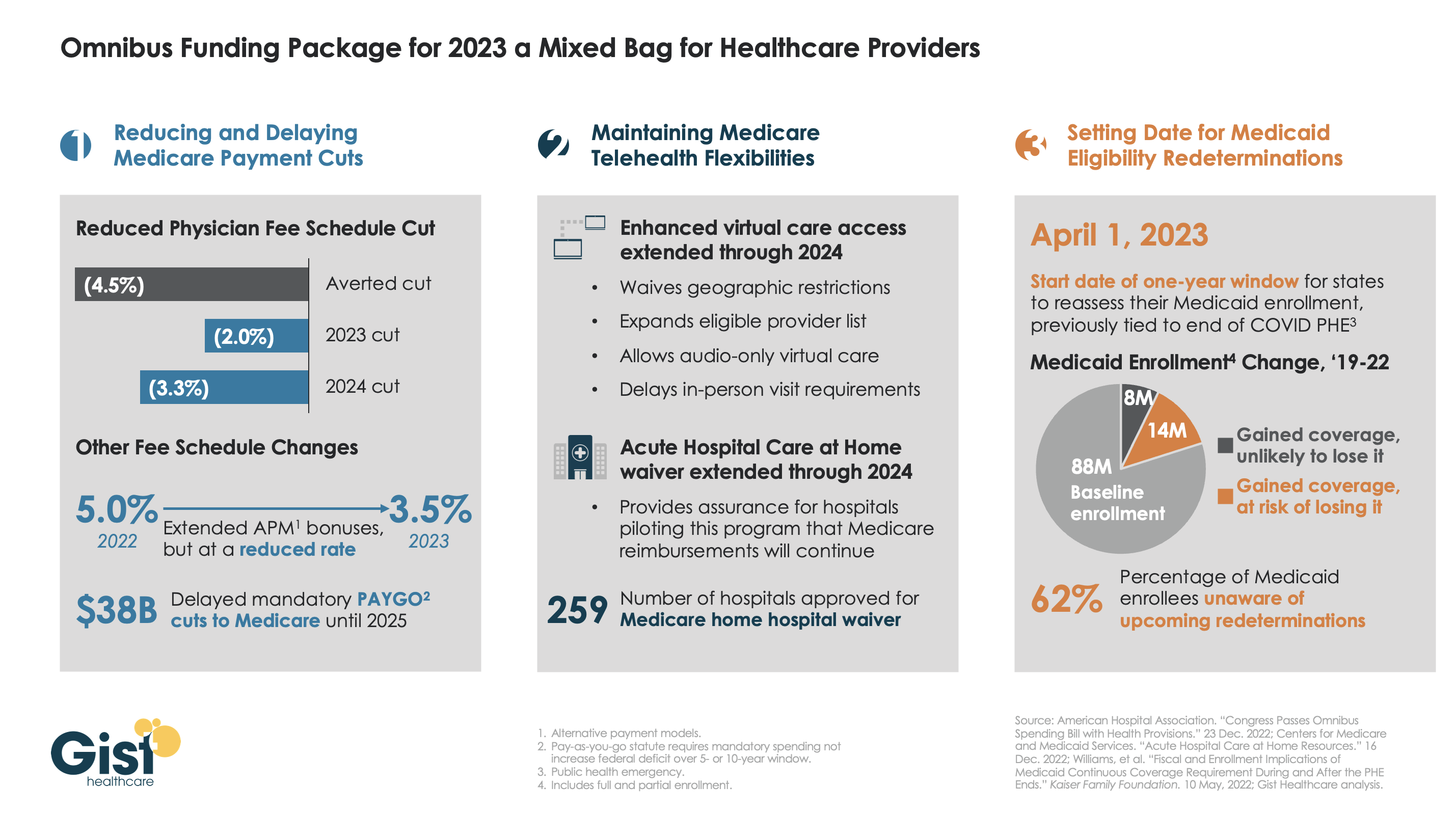

Late last week, President Biden signed a $1.7T spending package to fund the federal government through next September. While around half the funds are dedicated to defense, some important healthcare items made it into the bill, including a reduction in planned Medicare physician pay cuts and a two-year postponement of the $38B Medicare spending cut required by the PAYGO sequester.

The law also decoupled several measures from the end of the federal COVID public health emergency (PHE), setting April 1st as the start date for states to begin Medicaid eligibility redeterminations, and extending Medicare’s telehealth flexibilities and the Acute Hospital Care at Home waiver program through the end of 2024. For more details on these changes, see our graphic below.

The Gist: Medical groups were hoping for more of a reprieve from the Medicare physician fee schedule cuts, but Congress proved unwilling to address concerns over rising practice costs. We’re relieved that Medicare’s new telehealth and hospital at home policies will continue beyond the PHE, given the early interest we’ve seen from the provider community in embracing these new, more consumer-friendly care models.

Once the new Congress finally gets underway, we’re expecting this to be an uneventful two years for federal healthcare legislation, with the emphasis of health policy likely to shift toward states, federal agency rulemaking, and judicial activity.

Hospitals in the United States are on track for their worst financial year in decades. According to a recent report, median hospital operating margins were cumulatively negative through the first eight months of 2022. For context, in 2020, despite unprecedented losses during the initial months of COVID-19, hospitals still reported median eight-month operating margins of 2 percent—although these were in large part buoyed by federal aid from the Coronavirus Aid, Relief, and Economic Security (CARES) Act.

The recent, historically poor financial performance is the result of significant pressures on multiple fronts. Labor shortages and supply-chain disruptions have fueled a dramatic rise in expenses, which, due to the annually fixed nature of payment rates, hospitals have thus far been unable to pass through to payers. At the same time, diminished patient volumes—especially in more profitable service lines—have constrained revenues, and declining markets have generated substantial investment losses.

While it’s tempting to view these challenges as transient shocks, a rapid recovery seems unlikely for a number of reasons. Thus, hospitals will be forced to take aggressive cost-cutting measures to stabilize balance sheets. For some, this will include department or service line closures; for others, closing altogether. As these scenarios unfold, ultimately, the costs will be borne by patients, in one form or another.

Hospitals Face A Difficult Road To Financial Recovery

There are several factors that suggest hospital margins will face continued headwinds in the coming years. First, the primary driver of rising hospital expenses is a shortage of labor—in particular, nursing labor—which will likely worsen in the future. Since the start of the pandemic, hospitals have lost a total of 105,000 employees, and nursing vacancieshave more than doubled. In response, hospitals have relied on expensive contract nurses and extended overtime hours, resulting in surging wage costs. While this issue was exacerbated by the pandemic, the national nursing shortage is a decades-old problem that—with a substantial portion of the labor force approaching retirement and an insufficient supply of new nurses to replace them—is projected to reach 450,000 by 2025.

Second, while payment rates will eventually adjust to rising costs, this is likely to occur slowly and unevenly. Medicare rates, which are adjusted annually based on an inflation projection, are already set to undershoot hospital costs. Given that Medicare doesn’t issue retrospective corrections, this underadjustment will become baked into Medicare prices for the foreseeable future, widening the gap between costs and payments.

This leaves commercial payers to make up the difference. Commercial rates are typically negotiated in three- to five-year contract cycles, so hospitals on the early side of a new contract may be forced to wait until renegotiation for more substantial pricing adjustments. “Negotiation” is also the operative term here, as payers are under no obligation to offset rising costs. Instead, it is likely that the speed and degree of price adjustments will be dictated by provider market share, leaving smaller hospitals at a further disadvantage. This trend was exemplified during the 2008 financial crisis, in which only the most prestigious hospitals were able to significantly adjust pricing in response to historic investment losses.

Finally, economic uncertainty and the threat of recession will create continued disruptions in patient volumes, particularly with elective procedures. Although health care has historically been referred to as “recession-proof,” the growing prevalence of high-deductible health plans (HDHPs) and more aggressive cost-sharing mechanisms have left patients more exposed to health care costs and more likely to weigh these costs against other household expenditures when budgets get tight. While this consumerist response is not new—research on previous recessions has identified direct correlations between economic strength and surgical volumes—the degree of cost exposure for patients is historically high. Since 2008, enrollment in HDHPs has increased nearly four-fold, now representing 28 percent of all employer-sponsored enrollments. There’s evidence that this exposure is already impacting patient decisions. Recently, one in five adults reported delaying or forgoing treatment in response to general inflation.

Taken together, these factors suggest that the current financial pressures are unlikely to resolve in the short term. As losses mount and cash reserves dwindle, hospitals will ultimately need to cut costs to stem the bleeding—which presents both challenges and opportunities.

Direct And Indirect Consequences For Cost, Quality, And Access To Care

Inevitably, as rising costs become baked into commercial pricing, patients will face dramatic premium hikes. As discussed above, this process is likely to occur slowly over the next few years. In the meantime, the current challenges and the manner in which hospitals respond will have lasting implications on quality and access to care, particularly among the most vulnerable populations.

Likely Effects On Patient Experience And Quality Of Care

Insufficient staffing has already created substantial bottlenecks in outpatient and acute-care facilities, resulting in increased wait times, delayed procedures, and, in extreme cases, hospitals diverting patients altogether. During the Omicron surge, 52 of 62 hospitals in Los Angeles, California, were reportedly diverting patients due to insufficient beds and staffing.

The challenges with nursing labor will have direct consequences for clinical quality. Persistent nursing shortages will force hospitals to increase patient loads and expand overtime hours, measures that have been repeatedly linked to longer hospital stays, more clinical errors, and worse patient outcomes. Additionally, the wave of experienced nurses exiting the workforce will accelerate an already growing divide between average nursing experience and the complexity of care they are asked to provide. This trend, referred to as the “Experience-Complexity Gap,” will only worsen in the coming years as a significant portion of the nursing workforce reaches retirement age. In addition to the clinical quality implications, the exodus of experienced nurses—many of whom serve in crucial nurse educator and mentorship roles—also has feedback effects on the training and supply of new nurses.

Staffing impacts on quality of care are not limited to clinical staff. During the initial months of the pandemic, hospitals laid off or furloughed hundreds of thousands of nonclinical staff, a common target for short-term payroll reductions. While these staff do not directly impact patient care (or billed charges), they can have a significant impact on patient experience and satisfaction. Additionally, downsizing support staff can negatively impact physician productivity and time spent with patients, which can have downstream effects on cost and quality of care.

Disproportionate Impacts On Underserved Communities

Reduced access to care will be felt most acutely in rural regions. A recent report found that more than 30 percent of rural hospitals were at risk of closure within the next six years, placing the affected communities—statistically older, sicker, and poorer than average—at higher risk for adverse health outcomes. When rural hospitals close, local residents are forced to travel more than 20 miles further to access inpatient or emergency care. For patients with life-threatening conditions, this increased travel has been linked to a 5–10 percent increase in risk of mortality.

Rural closures also have downstream effects that further deteriorate patient use and access to care. Rural hospitals often employ the majority of local physicians, many of whom leave the community when these facilities close. Access to complex specialty care and diagnostic testing is also diminished, as many of these services are provided by vendors or provider groups within hospital facilities. Thus, when rural hospitals close, the surrounding communities lose access to the entire care continuum. As a result, individuals within these communities are more likely to forgo treatment, testing, or routine preventive services, further exacerbating existing health disparities.

In areas not affected by hospital closures, access will be more selectively impacted. After the 2008 financial crisis, the most common cost-shifting response from hospitals was to reduce unprofitable service offerings. Historically, these measures have disproportionately impacted minority and low-income patients, as they tend to include services with high Medicaid populations (for example, psychiatric and addiction care) and crucial services such as obstetrics and trauma care, which are already underprovided in these communities. Since 2020, dozens of hospitals, both urban and rural, have closed or suspended maternity care. Similar to closure of rural hospitals, these closures have downstream effects on local access to physicians or other health services.

Potential For Productive Cost Reduction And The Need For A Measured Policy Response

Despite the doom-and-gloom scenario presented above, the focus on hospital costs is not entirely negative. Cost-cutting measures will inevitably yield efficiencies in a notoriously inefficient industry. Additionally, not all facility closures negatively impact care. While rural facility closures can have dire consequences in health emergencies, studies have found that outcomes for non-urgent conditions remained similar or actually improved.

Historically, attempts to rein in health care spending have focused on the demand side (that is, use) or on negotiated prices. These measures ignore the impact of hospital costs, which have historically outpaced inflation and contributed directly to rising prices. Thus, the current situation presents a brief window of opportunity in which hospital incentives are aligned with the broader policy goals of lowering costs. Capitalizing on this opportunity will require a careful balancing act from policy makers.

In response to the current challenges, the American Hospital Association has already appealed to Congress to extend federal aid programs created in the CARES Act. While this would help to mitigate losses in the short term, it would also undermine any positive gains in cost efficiency. Instead of a broad-spectrum bailout, policy makers should consider a more targeted approach that supports crucial community and rural services without continuing to fund broader health system inefficiencies.

The establishment of Rural Emergency Hospitals beginning in 2023 represents one such approach to eliminating excess costs while preventing negative patient consequences. This rule provides financial incentives for struggling critical access and rural hospitals to convert to standalone emergency departments instead of outright closing. If effective, this policy would ensure that affected communities maintain crucial access to emergency care while reducing overall costs attributed to low-volume, financially unviable services.

Policies can also help promote efficiencies by improving coverage for digital and telehealth services—long touted as potential solutions to rural health care deserts—or easing regulations to encourage more effective use of mid-level providers.

Conclusion

The financial challenges facing hospitals are substantial and likely to persist in the coming years. As a result, health systems will be forced to take drastic measures to reduce costs and stabilize profit margins. The existing challenges and the manner in which hospitals respond will have long-term implications for cost, quality, and access to care, especially within historically underserved communities. As with any crisis, though, they also present an opportunity to address industrywide inefficiencies. By relying on targeted, evidence-based policies, policy makers can mitigate the negative consequences and allow for a more efficient and effective system to emerge.

Drawing on a report published by the North Carolina State Health Plan for Teachers and State Employees, a recent Kaiser Health News article shines a light on the lack of transparency in financial reporting of not-for-profit hospitals’ community benefit obligations.

The report claims many North Carolina hospitals—including the state’s largest system, Atrium Health—show profits on Medicare patients in their cost report filings, while at the same time claiming sizable unrecouped losses on Medicare patients as a part of their overall community benefit analyses.

The Gist: These kind of reporting discrepancies draw attention to the controversial issue of whether not-for-profit hospitals provide sufficient community benefit to compensate for their tax-exempt status, which was worth nearly $2 billion in 2020 for North Carolina hospitals alone.

Greater transparency around charity care, community benefit, and losses sustained from public payerscould go a long way toward shoring up stakeholder support for not-for-profit institutions at a time when their political goodwill has deteriorated. Hospitals should be proactive on this front, as political leaders increasingly train their sites on high hospital spending in the current tight economic environment.

The court ruling comes after the Supreme Court struck down a nearly 30 percent cut to 340B hospital payments from 2018.

October 04, 2022 – A federal judge has ordered HHS to immediately end the almost 30 percent cut in Medicare drug reimbursement to 340B hospitals.

The decision published last week by judge Rudolph Contreras with the US District Court for the District of Columbia rejected HHS’ plan to restore full payment to hospitals participating in the 340B Drug Pricing Program in 2023.

“HHS should not be allowed to continue its unlawful 340B reimbursements for the remainder of the year just because it promises to fix the problem later,” wrote Contreras.

Hospitals participating in the 340B Drug Pricing Program receive outpatient prescription drugs at a discounted price of up to 50 percent since they treat a disproportionate amount of low-income and vulnerable patients. The 340B Program is designed to enable the safety-net providers to stretch their financial resources. Medicare must also reimburse hospitals for administering covered outpatient drugs.

HHS reduced the Medicare drug reimbursement rates for 340B hospitals though in 2018, cutting payments by 28.5 percent in an effort to generate about $1.6 billion in savings. Federal officials reasoned that reimbursing 340B hospitals at the same rate as other hospitals creates an incentive for the hospitals to overprescribe the drugs or prescribe more expensive drugs since they receive covered outpatient drugs at a discounted price.

HHS also argued that 340B hospital reimbursement cuts would lower co-payments for Medicare beneficiaries since the amounts are tied to hospital reimbursement rates.

Hospitals and hospital groups, including the American Hospital Association (AHA) Association of American Medical Colleges (AAMC), and American’s Essential Hospitals, sued the federal government over the reduced reimbursement rates.

The case made it all the way to the Supreme Court where, in a major win for hospitals, judges unanimously ruled that HHS should not have reduced payments to certain hospitals in 2018 and 2019 without surveying hospitals to determine average acquisition costs for drugs. HHS had relied on the average price of the drugs to set lower rates.

However, the Supreme Court did not make judgments on 340B hospital reimbursement cuts for 2020 and later years. Following the Supreme Court’s ruling, HHS announced it would reimburse hospitals for administering 340B-covered drugs the same as non-340B drugs starting Jan. 1, 2023.

Hospital groups again challenged HHS policy, asking the courts to immediately halt the unlawful cuts in 2022.

“The AHA appreciates Judge Contreras’ ruling that the Department of Health and Human Services must immediately stop unlawful reimbursement cuts for 2022 for hospitals participating in the 340B drug pricing program. Halting these cuts will help 340B hospitals provide comprehensive health services to their patients and communities,” said Melinda Hatton, AHA’s general counsel and secretary, regarding the most recent court ruling.

“We continue to urge the Administration to promptly reimburse all the hospitals that were affected by these unlawful cuts in previous years and to ensure the remainder of the hospital field is not penalized for their prior unlawful policy, especially as hospitals and health systems continue to deal with rising costs for supplies, equipment, drugs and labor,” Hatton continued in the public statement.

340B Health’s president and CEO Maureen Testoni also called the court ruling “an important victory for 340B hospitals that have been fighting these unlawful cuts for nearly six years.” 340B health advocates safety-net hospitals participating in the drug pricing program.

“The Centers for Medicare & Medicaid Services (CMS) has the clear responsibility to restore the appropriate payments for 340B drugs immediately, and now a federal court has ordered it to do so without delay,” Testoni said.

HHS has not announced a repayment plan for 340B hospitals. Notably, the court ruling also did not cover the AHA’s motion to include reimbursement cuts from 2020 through 2022 in the case, nor AHA’s motion to repay hospitals for the cuts since 2018 without penalizing other hospitals.

Hospitals are forced to absorb inflationary expenses, particularly related to supporting their workforce, AHA says.

The Centers for Medicare and Medicaid Services’ increase in the inpatient payment rate for 2023 is welcome but not enough to offset expenses, according to the American Hospital Association.

CMS set a 4.1% market basket update for 2023 in its final rule released Monday, calling it the highest in the last 25 years. The increase was due to the higher cost in compensation for hospital workers.

The final rule gave inpatient hospitals a 4.3% increase for 2023, as opposed to the 3.2% increase in April’s proposed rule.

WHY THIS MATTERS

CMS used more recent data to calculate the market basket and disproportionate share hospital payments, a move that better reflects inflation and labor and supply cost pressures on hospitals, the AHA said.

“That said, this update still falls short of what hospitals and health systems need to continue to overcome the many challenges that threaten their ability to care for patients and provide essential services for their communities,” said AHA Executive Vice President Stacey Hughes. “This includes the extraordinary inflationary expenses in the cost of caring hospitals are being forced to absorb, particularly related to supporting their workforce while experiencing severe staff shortages.”

The AHA would continue to urge Congress to take action to support the hospital field, including by extending the low-volume adjustment and Medicare-dependent hospital programs, Hughes said.

In late July, Senate and House members urged CMS to increase the inpatient hospital payment.

Premier, which works with hospitals, also said the 4.3% payment update falls short of reflecting the rising labor costs that hospitals have experienced since the onset of the pandemic.

“Coupled with record high inflation, this inadequate payment bump will only exacerbate the intense financial pressure on American hospitals,” said Soumi Saha, senior vice president of Government Affairs for Premier.

THE LARGER TREND

Recent studies show hospitals remain financially challenged since the COVID-19 pandemic’s effect on revenue and supply chain and labor expenses. Piled onto that has been inflation that has added to soaring expenses.

Hospital margins were up slightly from May to June, but are still significantly lower than pre-pandemic levels, according to a Flash Report from Kaufman Hall.

The effects of the pandemic on the healthcare industry have been profound, resulting in the creation of new business models, according to a report from McKinsey.

Transformational change is necessary as hospitals have been hit hard by eroding margins due to cost inflation and expenses, Fitch found.

Hospitals’ labor costs rose by more than a third from pre-pandemic levels by March 2022, according to a report out Wednesday from Kaufman Hall.

Heightened temporary and traveling labor costs were a main contributor, with contract labor accounting for 11% of hospitals’ total labor expenses in 2022 compared to 2% in 2019, the report found.

Contract nurses’ median hourly wages rose 106% over the period, from $64 an hour to $132 an hour, while employed nurse wages increased 11%, from $35 an hour to $39 an hour, the report found.

Dive Insight:

The new data from Kaufman Hall supports concerns hospital executives expressed while releasing first quarter earnings results, as higher-than expected labor costs spurred some operators, like HCA, to lower their financial full-year guidance.

The ongoing use of contract labor amid shortages driven by heightened turnover was a key factor executives cited for higher costs, and follows the findings from Kaufman Hall’s latest report.

More than a third of nurses surveyed by staffing firm Incredible Health said they plan to leave their current jobs by the end of this year, according to a March report. While burnout is driving them to leave, higher salaries are the top motivating factor for taking other positions, that report found.

Kaufman Hall’s report, which analyzes data from more than 900 hospitals across the country, found hospitals spent $5,494 in labor expenses per adjusted discharge in March compared to $4,009 roughly three years ago.

Costs rose for hospitals in every region, though the South and West experienced the largest increases from pre-pandemic levels as those expenses rose 43% and 42%, respectively.

The West and Northeast/Mid-Atlantic regions saw the highest expenses consistently from 2019 to 2022, according to the report.

“The pandemic made longstanding labor challenges in the healthcare sector much worse, making it far more expensive to care for hospitalized patients over the past two years,” said Erik Swanson, senior vice president of data and analytics at Kaufman Hall.

“Hospitals now face a number of pressures to attract and retain affordable clinical staff, maintain patient safety, deliver quality services and increase their efficiency,” Swanson said.

The report also notes that hospitals are competing with non-hospital employers also pursuing hourly staff, though those companies can pass along wage increases to consumers through higher prices “in a way healthcare organizations cannot,” the report said.

Some hospitals, like HCA Healthcare and Universal Health Services, are looking to raise prices for health plans amid rising nurse salaries, according to reporting from The Wall Street Journal.

Another recent report from group purchasing organization Premier found the CMS underestimated hospital labor spending when making payment adjustments for the 2022 fiscal year, resulting in hospitals receiving only a 2.4% rate increase compared to a 6.5% increase in hospital labor rates.

To match the rates hospitals are now paying staff, an adequate inpatient payment update for fiscal 2023 is needed, that report said.

The CMS proposed its IPPS rule for FY 2023 on April 18 that includes a 3.2% hike to inpatient hospital payments, which provider groups like the American Hospital Association rebuked as “simply unacceptable” considering inflation and rising hospital labor costs.

The American Hospital Association (AHA) is asking Congress for an additional $25B to help hospitals offset high labor costs, largely incurred by the need to rely on travel nurse staffing firms that charge two to three times pre-pandemic rates. The AHA, along with 200 members of Congress, is urging the Federal Trade Commission to investigate the staffing agencies for anti-competitive activity, although the agency has previously declined to do so.

The Gist: The Department of Health and Human Services (HHS) is now releasing$2B in of provider relief dollars from the CARES Act. Beyond that, after nearly two years and $178B of federal support, hospitals shouldn’t count on additional funds from the government, even as costs of labor and supplies continue to rise.

Instead, we’d expect more scrutinyover how the remaining relief dollars are spent. Federal support during the pandemic has masked structural economic flaws in provider economics, and we expect 2022 will be a year of financial reckoning for many hospitals and health systems.