Cartoon – Medicare Co-Payment Explained

https://us.newschant.com/business/dr-philip-lee-is-dead-at-96-engineered-introduction-of-medicare/

Dr. Philip R. Lee, who as a number one federal well being official and fighter for social justice below President Lyndon B. Johnson wielded authorities Medicare money as a cudgel to desegregate the nation’s hospitals within the Sixties, died on Oct. 27 in a hospital in Manhattan. He was 96.

The trigger was coronary heart arrhythmia, his spouse, Dr. Roz Lasker, mentioned.

From his workplace at the Department of Health, Education and Welfare, because the assistant secretary for well being and scientific affairs from 1965 to 1969, Dr. Lee engineered the introduction of Medicare, which was established for older Americans in 1965, one 12 months after Johnson had bulldozed his landmark civil-rights invoice via Congress.

“To Phil, Medicare wasn’t just a ‘big law’ expanding coverage; it was a vehicle to address racial and economic injustice,” his nephew Peter Lee, the manager director of Covered California, which runs the state’s well being care market below the Affordable Care Act, was quoted as saying in a tribute by the University of California, San Francisco. Dr. Lee was the college’s chancellor from 1969 to 1972, after leaving the Johnson administration.

Dr. Lee’s use of Medicare funding to desegregate hospitals “changed the economic lives of millions of seniors,” Mr. Lee added.

Provisions within the Medicare laws subjected 7,000 hospitals nationwide to guidelines barring discrimination towards sufferers on the premise of race, creed or nationwide origin. The regulation required equal remedy throughout the board — from medical and nursing care to mattress assignments and cafeteria and restroom privileges — and barred discrimination in hiring, coaching or promotion.

Before the regulation took impact in 1966, fewer than half the hospitals within the nation met the desegregation commonplace and fewer than 25 p.c did within the South.

“I remember during one of my visits,” Dr. Lee instructed the journal of the American Society on Aging in 2015, “a cardiologist at Georgia Baptist Hospital told me, ‘Well, you know, Dr. Lee, if I put a nigger in with one of my white patients, it would kill the patient. My patient would die of a heart attack.’”

By February 1967, a 12 months or much less after many of the regulation’s provisions had taken impact, 95 p.c of hospitals have been compliant, Dr. Lee mentioned.

“He was largely responsible for that effort,” mentioned Professor David Barton Smith of Drexel University and writer of “The Power to Heal: Civil Rights, Medicare and the Struggle to Transform America’s Health System” (2016).

Dr. Lee hailed from a household of physicians — his father and 4 siblings have been medical doctors — and whereas working within the Palo Alto Medical Clinic (now the Palo Alto Medical Foundation), which his father based, he noticed firsthand the consequences on the poor and the aged of insufficient well being care and the shortage of insurance coverage protection.

As early as 1961, he was a guide on growing older to the Santa Clara Department of Welfare in California, and as a member of the American Medical Association and a Republican at the time, he defied each the A.M.A. and his celebration in testifying earlier than Congress on behalf of a precursor to Medicare that might have helped pay for hospital and nursing dwelling care via Social Security for sufferers over 65.

Dr. Lee was branded a socialist and a Communist (irrespective of that he had served as a physician within the Korean War).

In 1987, after main the University of California, San Francisco, and heading well being coverage and analysis packages there as a professor of social drugs, he additional riled fellow physicians when, as chairman of Congressional fee, he really helpful a standardized nationwide restrict on how a lot medical doctors enrolled within the Medicare program, with an enormous pool of sufferers obtainable to them, might cost above a set schedule.

He was referred to as again to Washington in 1993, once more to be an assistant secretary, this time of the renamed Department of Health and Human Services below the Clinton administration. Serving till 1997, he suggested the White House on its in the end failed effort on well being care reform.

In 2015 he endorsed the Obama administration’s Affordable Care Act and steered that the nation might go even additional in guaranteeing common well being care.

“In 1967, President Johnson said we would continue to work until equality of treatment is the rule,” Dr. Lee wrote in Generations: Journal of the American Society on Aging. “By making Medicare an option for all Americans, the kind of care I receive could be available to everyone.”

Philip Randolph Lee was born in San Francisco on April 17, 1924, to Dr. Russell Van Arsdale Lee, who had lobbied for nationwide medical insurance as a member of a fee appointed by President Harry S. Truman, and Dorothy (Womack) Lee, an newbie musician.

His curiosity in drugs, he instructed Stanford Medicine Magazine in 2004, “began with house calls with my dad from the age of 6 or 7.”

He earned his bachelor’s and medical levels at Stanford University in 1945 and 1948. As a member of the Naval Reserve, he was on lively responsibility as a physician at the top of World War II and once more from 1949 to 1951, through the Inchon invasion in Korea. He obtained a grasp of science diploma from the University of Minnesota in 1955 and had fellowships at the Rusk Institute of Rehabilitation Medicine in New York and the Mayo Clinic.

“Phil moved from clinical medicine to health policy and then devoted his life to addressing issues at the nexus of civil rights, social justice and health,” Dr. Lasker, his spouse, mentioned in an e-mail.

His distinguished function in shaping Medicare and different federal well being insurance policies was preceded by a stint, 1963-65, as director of well being for the Agency for International Development. As chancellor of the University of California, San Francisco, he was credited with rising racial variety amongst its workers, college and pupil physique.

In 2007, the college named its Institute for Health Policy Studies, which he based in 1972, in his honor.

He was additionally lauded for his aggressive function in confronting the AIDS epidemic because the president of the newly-formed Health Commission of the City and County of San Francisco from 1985 to 1989.

The writer of a half-dozen books, Dr. Lee was an early critic of the pharmaceutical trade in “Pills, Profits and Politics” (1974, with Milton Silverman).

In swing states from Georgia to Arizona, the Affordable Care Act — and concerns over protecting preexisting conditions — loom over key races for Congress and the presidency.

“I can’t even believe it’s in jeopardy,” says Noshin Rafieei, a 36-year-old from Phoenix. “The people that are trying to eliminate the protection for individuals such as myself with preexisting conditions, they must not understand what it’s like.”

In 2016, Rafieei was diagnosed with colon cancer. A year later, her doctor discovered it had spread to her liver.

“I was taking oral chemo, morning and night — just imagine that’s your breakfast, essentially, and your dinner,” Rafieei says.

In February, she underwent a liver transplant.

Rafieei does have health insurance now through her employer, but she fears whether her medical history could disqualify her from getting care in the future.

“I had to pray that my insurance would approve of my transplant just in the nick of time,” she says. “I had that Stage 4 label attached to my name and that has dollar signs. Who wants to invest in someone with Stage 4?”

“That is no way to feel,” she adds.

After doing her research, Rafieei says she intends to vote for Joe Biden, who helped get the ACA passed in this first place.

“Health care for me is just the driving factor,” she says.

Even 10 years after the Affordable Care Act locked in a health care protection that Americans now overwhelmingly support — guarantees that insurers cannot deny coverage or charge more based on preexisting medical conditions — voters once again face contradicting campaign promises over which candidate will preserve the law’s legacy.

A majority of Democrats, independents and Republicans say they want their new president to preserve the ACA’s provision that protects as many as 135 million people from potentially being unable to get health care because of their medical history.

President Trump has pledged to keep this in place, even as his administration heads to the U.S Supreme Court the week after Election Day to argue the entire law should be struck down.

“We’ll always protect people with preexisting,” Trump said in the most recent debate. “I’d like to terminate Obamacare, come up with a brand new, beautiful health care.”

And yet the Trump administration has not unveiled a health care plan or identified any specific components it might include. In 2017, the administration joined with congressional Republicans to dismantle the Affordable Care Act, but none of the GOP-backed replacement plans could summon enough votes. The Republicans’ final attempt, a limited “skinny repeal” of parts of the ACA, failed in the Senate because of resistance within their own party.

In an attempt to reassure wary voters, Trump recently signed an executive order that asserts protections for preexisting conditions will stay in place, but legal experts say this has no teeth.

“It’s basically a pinky promise, but it doesn’t have teeth,” says Swapna Reddy, a clinical assistant professor at Arizona State University’s College of Health Solutions. “What is the enforceability? The order really doesn’t have any effect because it can’t regulate the insurance industry.”

Since the 2017 repeal and replace efforts, the health care law has continued to gain popularity.

Public approval is now at an all-time high, but polling shows many Republicans still don’t view the ACA as synonymous with its most popular provision — protections for preexisting conditions.

Democrats hope to change that.

“If you have a preexisting condition — heart disease, diabetes, breast cancer — they are coming for you,” said Biden’s running mate, California Sen. Kamala Harris, during her recent debate with Vice President Pence.

Voters support maintaining ACA’s legal protections

In key swing states, many voters say protecting preexisting conditions is their top health concern.

Rafieei, the Phoenix woman with colon cancer, still often has problems getting her treatments covered. Her insurance has denied medications that help quell the painful side effects of chemotherapy or complications related to her transplant.

“During those chemo days, I’d think, wow, I’m really sick, and I just got off the phone with my pharmacy and they’re denying me something that could possibly help me,” she says.

Because of her transplant, she will be on medication for the rest of her life, and sometimes she even has nightmares about being away and running out of it.

“I will have these panic attacks like, ‘Where’s my medicine? Oh my god, I have to get back to get my medicine?'”

Election season and talk of eliminating the ACA has not given Rafieei much reassurance, though.

“I cannot stomach politics. I am beyond terrified,” she says.

And yet she plans to head to the polls — in person — despite having a compromised immune system.

“It might be a long day. But you know what? I want to fix whatever I can,” she says.

A few days after she votes, she’ll get a coronavirus test and go in for another round of surgery.

A key health issue in political swing states

Rafieei’s home state of Arizona is emblematic of the political contradictions around the health care law.

The Republican-led state reaped the benefits of the ACA. Arizona’s uninsured rate dropped considerably since 2010, in part because it expanded Medicaid.

But the state’s governor also embraced the Republican effort to repeal and replace the law in 2017, and now Arizona’s attorney general is part of the lawsuit that will be heard by the Supreme Court on Nov. 10 that could topple the entire law.

Depending on how the Supreme Court rules, ASU’s Reddy says any meaningful replacement for preexisting conditions would involve Congress and the next president.

“At the moment, we have absolutely no national replacement plan,” she says.

Meanwhile, some states have passed their own laws to maintain protections for preexisting conditions, in the event the ACA is struck down. But Reddy says those vary considerably from state to state.

For example, Arizona’s law, passed just earlier this year, only prevents insurers from outright denying coverage — consumers with preexisting conditions can be charged more.

“We are in this season of chaos around the Affordable Care Act,” says Reddy. “From a consumer perspective, it’s really hard to decipher all these details.”

As in the congressional midterm election of 2018, Democrats are hammering away at Republican’s track record on preexisting conditions and the ACA.

In Arizona, Mark Kelly, the Democratic candidate running for Senate, has run ads and used every opportunity to remind voters of Republican Sen. Martha McSally’s votes to repeal the law.

In Georgia, Democratic challenger Jon Ossoff has taken a similar approach.

“Can you look down the camera and tell the people of this state why you voted four times to allow insurance companies to deny us health care coverage because we may suffer from diabetes or heart disease or have cancer in remission?” Ossoff said during a debate with his opponent, Republican Sen. David Purdue.

Republicans have often tried to skirt health care as a major issue this election cycle because there isn’t the same political advantage to pushing the repeal and replace argument, says Mark Peterson, a professor of public policy, political science and law at UCLA.

“It’s political suicide, there doesn’t seem to be any real political advantage anymore,” says Peterson.

But the timing of the Supreme Court case — exactly a week after election day — has somewhat obscured the issue for voters.

Republicans have chipped away at the health care law by reducing the individual mandate — the provision requiring consumers to purchase insurance — to zero dollars.

The premise of the Supreme Court case is that the ACA no longer qualifies as a tax because of this change in the penalty.

“It is an extraordinary stretch, even among many conservative legal scholars, to say that the entire law is predicated on the existence of an enforced individual mandate,” says Peterson.

The court could rule in a very limited way that does not disrupt the entire law or protections for preexisting conditions, he says.

Like many issues this election, Peterson says there is a big disconnect between what voters in the two parties believe is at stake with the ACA.

“Not everybody, particularly Republicans, associates the ACA with protecting preexisting conditions,” he says. “But it is pretty striking that overwhelmingly Democrats and Independents do — and a number of Republicans — that’s enough to give a significant national supermajority.”

https://mailchi.mp/burroughshealthcare/april-16-3240709?e=7d3f834d2f

Less than three months from now, either Donald Trump will begin his second term as President, or Joe Biden will begin his first. What the U.S. healthcare system on that date and moving forward could be starkly different depending on who is sworn in.

The policy differences between the two men are essentially on opposite poles. If fully enacted, Trump’s policies could potentially cause tens of millions of Americans to lose their healthcare coverage. Biden’s policies would likely provide healthcare access to tens of millions more Americans compared to today.

In November, the U.S. Supreme Court will hear arguments in a case called California v. Texas. It stems from the 2017 tax bill that zeroed out the penalty individuals paid if they did not obtain health insurance. The argument put forth by the 20 Republican state attorney generals in that case is if the individual mandate no longer has taxing power, the entire law should be declared unconstitutional based upon a lack of severability of the entire law.

Many legal scholars have noted that this case is premised on a shaky argument. But with a 6-3 majority of conservative justices now on the high court, many bets are off as to the ACA’s survival. And President Trump just said in an interview with “60 Minutes” he fervently hoped the ACA is eliminated. He put forth no alternatives to the ACA in that interview.

Should the ACA be declared unconstitutional, health insurance for some 23 million people would be imperiled. That includes some 12 million Americans who are eligible for Medicaid under the ACA’s expanded income guidelines, and another 11 million who purchase insurance on the state and federal health insurance exchanges – roughly 85% of whom receive premium subsidies that make it more affordable. Moreover, another 14 million Americans who are estimated to have lost their employer-based health plans during the COVID-19 pandemic may not have another place to turn for coverage.

Before the ACA case, the Trump administration also promoted so-called “off-exchange” health plans, and health sharing ministries. The first is often a form of short-term health insurance, the second operates as a cooperative serving those of the same religious stripe. Both offer health coverage that is potentially cheaper that what is offered on the exchanges, but both also tend to cap it at low dollar levels. Many also bar applicants for a variety of claims, such as for maternity or cancer care, or if they have pre-existing medical conditions – practices prohibited for ACA plans.

Should Trump be re-elected and the ACA survives constitutional muster, expect to see many states apply for more waivers from that law. Georgia just received approval to modestly expand Medicaid eligibility, primarily for those poor already working 80 hours or more a month. The state is also on the cusp of being able to opt out of the healthcare.gov exchange entirely and have consumers work directly with insurance brokers to purchase coverage. However, there is nothing in the pending waiver to prevent those brokers from offering stripped-down coverage without the ACA protections that the Trump administration is already promoting.

There could also be more block grants to states for their Medicaid budgets, which most experts have concluded would reduce the number of enrollees in that program.

If Biden is elected and both incoming houses of Congress are also Democratic, the entire Supreme Court case can be mooted simply by reattaching a financial penalty to the individual mandate. That hasn’t been mentioned at all during the campaign, presumably because Biden does not want to discuss what would essentially be a promise to raise taxes. But it is the most direct way to skirt the risk of an adverse Supreme Court decision.

Biden’s campaign has also put forth numerous proposals to enlarge the ACA and the Medicare program. They include expanded premium subsidies for individuals and families to purchase coverage, and a public health plan option – which would allow those who live in the states that have yet to expand Medicaid to obtain coverage. Biden has also proposed a buy-in to Medicare at age 60.

The estimates are that an expanded ACA and other Biden plans could net another 20 to 25 million Americans healthcare coverage. That would leave fewer than 10 million – 2% to 3% of the population – without access to coverage. It would probably be as close to universal healthcare as the United States could get given its current political realities.

The two different approaches will either lead to a country where virtually everyone has access to healthcare coverage and services, or one where 50 million or more people could potentially be uninsured. It’s a shift that could impact a minimum of 45 million people – and that’s not even counting those who lost their coverage during the current public health crisis.

Elections have consequences. Less than three months from now, this one will determine whether the U.S. healthcare system will take one consequential path over another.

https://interimcfo.wordpress.com/2020/10/22/are-you-ready-for-price-transparency/

Abstract: This article focuses on the correct strategic response to the impending implementation of price transparency on New Year’s Day of next year.

I have stated before that I have multiple articles in process at any given time. Some of them have been ‘in process’ for years because newer topics sometimes rise to the queue’s top. Price transparency is an example of such a case. I have a friend who is developing AI-enabled solutions to help organizations respond to price transparency government diktats. Few people beyond healthcare CFOs, healthcare financial consultants, and accountants have any useful understanding of how convoluted hospital pricing has become due to decades of ill-conceived government policy for the most part.

Another problem is endless confusion over terms. People frequently interchange the terms ‘price’, ‘cost’, ‘payment’, and ‘reimbursement’ in situations where the polar opposite is true on the other side of the issue. In other words, ‘cost’ to a payor is price or reimbursement to a provider.

Anyway, my friend’s questions finally inspired me to go to the Federal Register, acquire the final rule, and begin the process of learning where government is headed with these regulations. There are probably at least fifty diatribe angles I could launch into over the final rule, but I will confine my rant to only a couple of points.

First, the final draft of the rule is ‘only’ 331 pages long. The three-column final rule in the Federal Register is ‘only’ 83 pages long. That pales compared to Obamacare that is over 1,200 pages long, so by government standards, this is but a trifle of regulation.

Secondly, some parts of the final rule are actually funny. For example, CMS estimates that the average hospital will spend only 150 staff hours in the first and 46 staff hours in subsequent years complying with price transparency requirements. Is it constitutional for government to compel private enterprises to disclose the terms of what they thought were private contracts? Apparently so. Once government breaks this ice, will any agreement of any type ever be private?

As I have discussed price transparency with healthcare leaders, I sense that leaders are currently focused on technical compliance with the regulations. With COVID on their plate simultaneously, they have little capacity to take on strategic financial planning.

The final rule lays out in excruciating detail what providers face complying with the regulation. Reading the comments and responses is equally entertaining. CMS repeatedly says something to the effect; we heard your concern, and we’re proceeding as planned anyway. Litigation brought by the AHA and others has to date been unsuccessful in slowing stopping the price transparency snowball that is now most of the way down the mountain.

So, what are you supposed to do? The CFO and CIO will work, possibly with consultants’ assistance, to prepare the organization’s data release. Soon after the release occurs, expect the defecation to hit the rotary oscillator. The press will call out organizations with high prices, and the rancor over learning what some systems have been able to get from third-party payors will be entertaining, to say the least. Many people believe that one of the primary motivators of the massive consolidation occurring in the healthcare industry is the market leverage exerted by growing systems on third-party payors to obtain otherwise unachievable reimbursement rates.

Regardless of the course of action following price releases in January, the intended and most likely result of this initiative is to drive prices to a lower common denominator. A lot of people think Medicare rates will become that benchmark. There are two significant issues that I did not see addressed in the pricing rule that will have the effect of transferring substantial risk to providers.

The first is that there will be little if any provision for recognition of complications, comorbidities, and hospital-acquired conditions that can dramatically impact the cost of care in a given diagnosis.

The second is the elephant in the room. The current pricing system has developed over time to facilitate cross-subsidization among payors. There is a reason that commercial rates are so high that has nothing to do with the cost of providing care. I have stated before that, government has turned the entire healthcare industry into a taxing authority to extract tax from commercial payors for the benefit of government payors that routinely reimburse providers below the cost of providing care. It has been entertaining to watch the reaction of Boards of Directors when they first realize that the healthcare system has been forced by government into a wealth redistribution mechanism.

So, what happens as providers lose the ability to cross-subsidize the cost of care? Very few hospitals (<10%) are profitable on Medicare, and it is doubtful that any hospital is breaking even on services provided to Medicaid patients. In my experience, hospital reimbursement for self-pay patients is less than 5% of charges. If the prices hospitals realize for services start falling and they lose the current ability to cross-subsidize the cost of care . . . . . well, you don’t need an MBA to understand the likely outcome.

What to do? If (when) prices start falling and providers lose pricing leverage, the only place to turn is operating expense. Hospitals that have failed to undertake serious, highly focused, and robust operating cost reduction programs that yield quantifiable results may not have a very bright future. If your organization is not in the bottom quartile of operating cost compared to its peer group and part of your mission is to remain independent, you must be losing sleep. In a recent article related to COVID Response, I argued that the time has come to get after clinical process variance that is the source of most of the high cost, waste, and abuse in the healthcare system. For most organizations, the days of sourcing cheaper supplies and sending nurses home early are, for the most part, over as there is little if any juice remaining in that lemon.

If, as a leader, you do not have a plan that gets you to break-even on Medicare within the next 12-18 months, you had better have a plan B, something like tuning up your CV. I can help you with your response to price transparency, working on your CV, or helping manage your next career transition as the case may turn out. I am as close as your phone. Best of luck.

Contact me to discuss any questions or observations you might have about these articles, leadership, transitions, or interim services. I might have an idea or two that might be valuable to you. An observation from my experience is that we need better leadership at every level in organizations. Some of my feedback comes from people demonstrating interest in advancing their careers and inspiring content to address those inquiries.

The easiest way to keep abreast of this blog is to become a follower. You are then notified of all updates as they occur. To become a follower, click the “Following” bubble that usually appears near each web page’s bottom.

I encourage you to use the comment section at the bottom of each article to provide feedback and stimulate discussion. I welcome input and feedback that will help me to improve the quality and relevance of this work.

This article is an original work. I copyright this material with reproduction prohibited without attribution. I note and provide links to supporting documentation for non-original material. If you choose to link any of my articles, I’d appreciate a notification.

If you would like to discuss any of this content, provide private feedback or ask questions, I may be reached at ras2@me.com.

https://www.commonwealthfund.org/blog/2020/uncertain-future-medicare-trust-fund

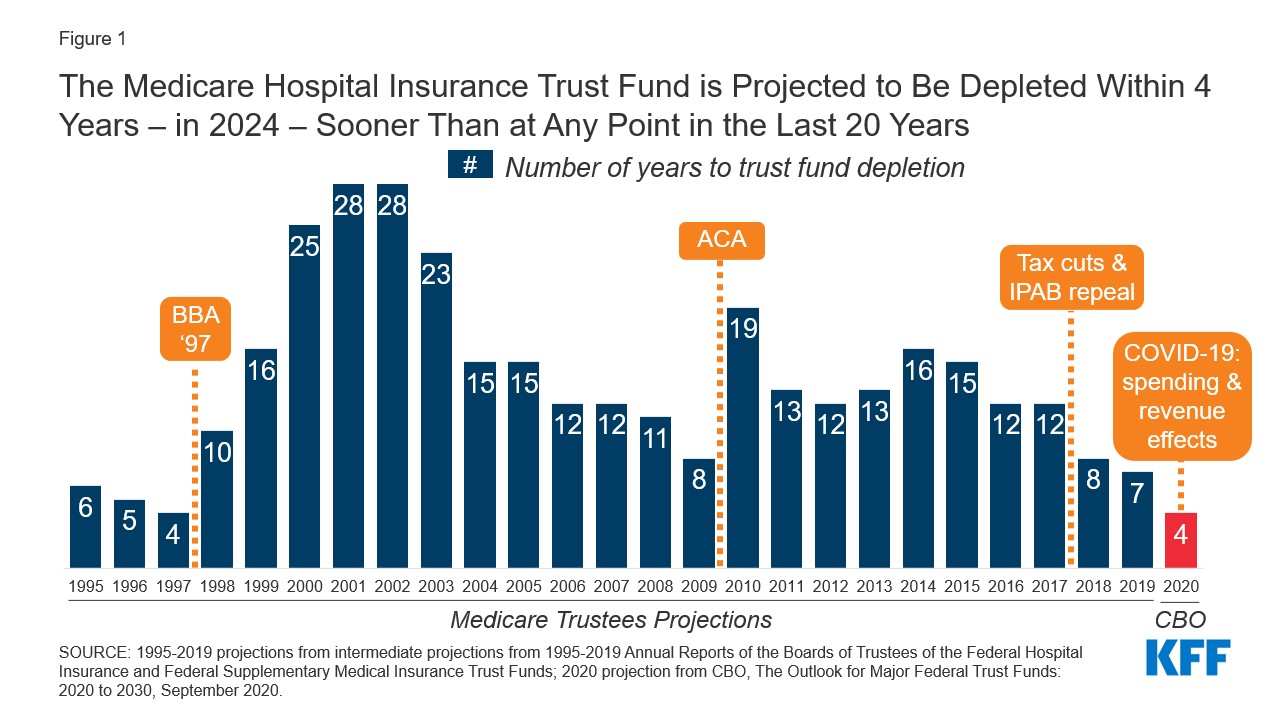

The COVID-19 pandemic has increased pressures on an already-stressed public health care financing system. This is especially evident when it comes to the financial health of Medicare’s Hospital Insurance (HI) Trust Fund, which finances health care services related to hospital, skilled nursing facility, and hospice stays for Medicare beneficiaries.

In April, using pre-COVID-19 data, the Trustees of Social Security and Medicare projected that the HI Trust Fund would become insolvent in 2026 — meaning that Medicare Part A claims submitted by providers would not be fully reimbursed. The Congressional Budget Office (CBO) made a similar projection when it issued its March 2020 baseline projections. In a September 2020 report, the CBO projected that the date of insolvency had moved up to 2024.

The pandemic has disrupted economic activity in the United States in several ways: a large and rapid rise in unemployment substantially reduced payments to the Trust Fund from payroll taxes, and hospitals experienced unprecedented financial stress from lost revenues because of a dramatic drop in admissions and procedures, along with new costs arising from the pandemic. One way that Congress provided relief to address these economic shocks was to make advance payments. Between $65 billion and $92 billion in advance payments were made to Medicare Part A providers that draw upon the HI Trust Fund. This increased claims on the Trust Fund in 2020 and lowers them for 2021 — assuming they are paid back in 2021. Together these economic dynamics create a situation that requires quick action to prevent insolvency; the margin for error is small.

The duration of the pandemic and the timing and size of an economic recovery remain highly uncertain. While unemployment has declined notably, from 14.7 percent in April to 8.4 percent in August, new spikes in COVID-19 cases across the country continue to dampen economic activity. The recent jobs report also suggested a slowing of employment recovery. Further, there is great uncertainty about the timing, availability, and effectiveness of a potential vaccine. As a result, we are quite unsure when payroll tax revenues will recover or to what degree hospital finances will recover.

The Federal Reserve Bank of St. Louis recently underscored the uncertainty when it issued the following assessment:

“The COVID-19 pandemic — like all pandemics — will come to an end. Of course, nobody knows when that will be. No one also knows whether there will be subsequent waves of the virus that trigger a nationwide resumption of strict social distancing protocols or whether a proven vaccine allows a swift return to pre-COVID norms. Thus, the trajectory of the recovery is the key unknown at this point.”

Together these forces create policy tensions. It is important to continue to support hospitals and nursing homes whose revenues have not yet recovered, and those that continue to incur unusual costs because they are still carrying heavy financial burdens stemming from COVID-19. At the same time state and federal health care financing programs are under extreme financial stress.

Recent legislation negotiated between Congress and the Trump administration would permit hospitals to request an extension for repaying advance payment loans and also reduce the interest rate. Together, these provisions recognize the continued financial stress and provide relief but also introduce new uncertainty. That is, by lengthening the repayment period and reducing the costs of carrying the loans it becomes less certain when they will be paid back in full and returned to the Trust Fund, making the solvency date of the Trust Fund less certain (as specified further in Centers for Medicare and Medicaid Services guidance). In addition, this assumes that the full amounts of the loan will be paid back.

The timing of the COVID-19 pandemic has been especially unfortunate in terms of maintaining the Medicare HI Trust Fund’s solvency. The Trustees issued a warning that action was needed when insolvency was estimated to occur in 2026; it has now been pushed up to 2024. One way to address the uncertainty would be to make a fund transfer from general revenues to the Trust Fund in the amount of the outstanding loans, thereby removing any additional uncertainty around timing of repayment. This could help mitigate risks in a world with highly uncertain economic and epidemiological forecasts but would risk further increasing federal spending during an economic downturn.

https://www.commonwealthfund.org/blog/2020/health-care-2020-presidential-election-whats-stake

As the presidential election draws near, we reflect on the meaningful differences in health policy priorities and platforms between the two candidates, which we’ve described more fully in our recent blog series.

While similarities exist in some areas — most notably prescription drug pricing and proposals to control health care costs — the most striking differences between the positions taken by President Donald Trump and those of former Vice President Joe Biden are on safeguarding access to affordable health care coverage, advancing health equity for those who have been historically disadvantaged by the current system, and managing the novel coronavirus pandemic.

The importance of maintaining or expanding access to affordable health care in the midst of a pandemic cannot be understated. Going into the crisis, 30 million Americans lacked health coverage, with many more potentially at risk as a result of the current economic downturn. And even for many with coverage, costs are a barrier to receiving care. Moreover, despite efforts by Congress and the Trump administration to ease the financial burden of COVID-19 testing and treatment, many people remain concerned about costs; examples of charges for COVID-related medical expenses are not uncommon.

In this context, President Trump’s efforts to repeal the Affordable Care Act (ACA) is the most important signal of his position on health care. The administration’s legal challenge of the law will be considered by the Supreme Court this fall. With no Trump proposal for a replacement to the ACA, if the Court strikes the law in its entirety or in part, many voters cannot be certain that their health coverage will be secure. By undermining the ACA — the vast law that protects Americans with preexisting health conditions and makes health coverage more affordable through a system of premium subsidies and cost-sharing assistance — the president has put coverage for millions at risk.

Trump issued an executive order to preserve preexisting condition protections. If the ACA remains intact, the order is redundant. But if the ACA is repealed by the Court, the order is meaningless because it lacks the legal underpinning and legislative framework to take effect.

In contrast, Vice President Biden has proposed expanding coverage through the ACA by adding a public option, enhancing subsidies to make health care more affordable, filling the gap for low-income families living in states that did not expand Medicaid, and giving people with employer health plans the option to enroll in marketplace coverage and take advantage of premium subsidies. For sure, if Biden is elected, many policy details must be ironed out; passing legislation in a deeply divided Congress is never easy. Despite these challenges, Biden proposes expanding health coverage rather than revoking it.

Just as COVID-19 has exposed gaps in health coverage and affordability, it also has highlighted the poor health outcomes stemming from racial and ethnic inequities in the U.S. health system. Communities of color — Black, Hispanic, and American Indian and Alaska Native people — have higher rates of COVID cases, hospitalizations, and deaths compared to white people. These disparities are a result of myriad factors, many of which are deeply rooted in structural racism. The candidates’ plans to address health disparities and advance health equity set them apart.

The ACA has played a critical role in reducing disparities in access to health care and narrowed the uninsured rate among Black and Hispanic people compared to white people. Medicaid expansion has been key to improving racial equity. Repealing the ACA, as President Trump has sought to do, would reverse these gains. Even beyond repealing the ACA, this administration has pursued policies intended to limit Medicaid eligibility — for example, by permitting states to impose work requirements and other restrictions that would lead to fewer people covered. These measures and others are already having an impact; coverage gains achieved through the ACA have eroded since 2016. Health care for legal immigrants also has declined as a result of policies like the recently finalized “public charge” rule, which seems also to have caused an increase in uninsurance among children. The administration has further revoked ACA antidiscrimination and civil rights protections for LGBTQ people.

In addition to restoring and expanding coverage under the ACA, Vice President Biden has pledged to address health disparities and reinstate antidiscrimination protections. He has a proposal to advance racial equity not just in health care but across the economy. If successful, his plan could address underlying factors contributing to higher rates of COVID-19 cases and deaths among people of color, as well as their higher rates of heart disease, diabetes, and other health conditions tied to social determinants of health.

Finally, the candidates differ deeply in their approaches to the coronavirus pandemic. President Trump has failed to orchestrate a national strategy for combating coronavirus and has routinely undermined accepted public health advice with respect to mask-wearing and social distancing. He has delegated to the states responsibility for controlling the pandemic when it is clear that the virus travels freely across the country, regardless of state borders. Lax states can negate the efforts of those states sacrificing to bring the pandemic under control. Vice President Biden has strongly signaled, though his personal conduct and rhetoric, that he intends more aggressive federal leadership in fighting the virus.

In a recent Commonwealth Fund survey of likely voters, control of the pandemic and covering preexisting conditions were very important factors in choosing a president. In seven battleground states, protections for preexisting conditions outweighed COVID-19 and health costs as the leading health care issue voters are considering. In all 10 battleground states included in the survey, Vice President Biden was viewed as the more likely candidate to address these critical health care issues.

Perhaps since the Civil War, the United States has never faced starker choices in a presidential election. In health and other areas, there are profound differences in the positions of President Trump and former Vice President Biden. Voting this November is literally a matter of life and death for the American people.

Overall approach: Repeal the ACA and replace it with market-driven coverage options aimed at lowering premiums and increasing choice of plans tailored to individual preferences; give states more flexibility in designing coverage options; require more accountability for people with low incomes enrolled in public programs; protect preexisting conditions.

Medicaid: Repeal the ACA Medicaid expansion for adults; provide block grants to states to design their own programs; increase accountability through work requirements.

Individual market and marketplaces: Has promoted weaker regulations on plans that don’t comply with the ACA’s preexisting condition protections and other requirements; elimination of advertising and enrollment assistance during open enrollment; elimination of payments to insurers to offer lower-deductible plans.

Employer coverage: Has promoted weaker regulations on association health plans that don’t comply with the ACA and allowed employers to fund accounts for employees to buy health plans on their own, including products that don’t comply with the ACA.

Overall approach: Protect insurance for people with preexisting conditions by supporting and building on the ACA; expand insurance coverage and reduce consumers’ health care costs by enhancing the ACA’s marketplace subsidies, covering people currently eligible for Medicaid in nonexpansion states, and giving more people in employer plans the option to enroll in marketplace plans with subsidies.

Medicaid: Expand enrollment by allowing eligible people in 12 states without Medicaid expansion to enroll in a public plan through the marketplaces with no premiums; make enrollment easier with autoenrollment.

Individual market and marketplaces: Expand enrollment through enhanced subsidies, greater advertising and enrollment assistance: no one pays more than 8.5 percent of income on marketplace coverage; change the benchmark plan from silver to gold to reduce deductibles and cost-sharing.

Employer coverage: Allows anyone with employer coverage to enroll in a public plan through the marketplaces and be eligible for subsidies.

Medicare: Would allow people ages 60 to 65 to enroll in a Medicare-like heath plan.

Trump: The number of people without health insurance has increased under the president’s watch in part because of policies that have eliminated the promotion and advertising of marketplace open-enrollment periods, enrollment restrictions in Medicaid, and immigration policies that have had a chilling effect on enrollment of legal immigrants and their children. Trump supports a lawsuit now before the Supreme Court that argues for repeal of the ACA, which would eliminate coverage for as many as 20 million people. Says he will come up with a replacement but has yet to do so.

Biden: Has introduced proposals to build on the ACA by covering people in the 12 states that haven’t expanded Medicaid and enhance subsidies for marketplace plans. This would provide new options for people who are currently uninsured and increase coverage over time.

Trump: The ACA currently provides this protection. Trump supports the lawsuit before the Supreme Court that argues for repeal of the ACA and its preexisting conditions provision. Trump issued an executive order that said preexisting conditions are protected, but without the ACA or new legislation the order has no effect and is purely symbolic.

Biden: The vice president pledges to support and build on the ACA, retaining its preexisting condition protections.

Trump: The president eliminated payments to insurers to reimburse them for offering lower-deductible plans in the ACA marketplaces to people with lower incomes, as required by the law. This had the effect of increasing premiums for people not eligible for subsidies. He has promoted the sale of non-ACA-compliant health plans, like short-term plans. These plans have lower premiums for healthy people but screen for preexisting conditions and often provide little cost protection if someone becomes sick. He has loosened regulations for association health plans, although that was turned back under legal challenge. The repeal of the ACA would mean the loss of marketplace subsidies and preexisting-condition protections, making coverage unavailable or unaffordable for people with low and moderate incomes and those with health problems.

Biden: The vice president’s proposal to enhance marketplace subsidies will cap the amount of premiums people pay at 8.5 percent of income, including people in employer plans who would have the option to enroll in the marketplaces. By linking subsidies to gold plans, deductibles would also fall for those who choose those plans.

Trump: Uninsured rates among Hispanic people have risen under the president’s watch. Repealing the ACA would further eliminate coverage gains made by Hispanics, as well as Black people and Asian Americans, widening racial disparities in coverage and access.

Biden: The vice president’s proposals to expand coverage under the ACA will particularly benefit people of color. This is because people living in the 12 states that have not yet expanded Medicaid are disproportionately Black and Hispanic.

https://www.commonwealthfund.org/blog/2020/introducing-health-care-2020-presidential-election-series

Before each presidential election, the Commonwealth Fund analyzes the major health policy positions of the Democratic and Republican candidates to assist Americans in making informed choices. In 2020, with health care rising to the top of the electorate’s concerns for myriad reasons, this information has never been more important.

In the next week, we will be publishing a series of analyses that compare the positions of President Donald Trump and his challenger, former Vice President Joe Biden, on topics like:

prescription drug policy;

the affordability and availability of health care and insurance, including the issue of preexisting conditions;

questions concerning older adults, like Medicare; how best to control the costs of health care;

addressing mental and behavioral health concerns;

and strategies for advancing health care equity.

In most previous presidential election years, we have had the opportunity to compare fairly well-delineated party and candidate programs. In 2020, President Trump and the Republican party have chosen not to issue any party platform or formal policy positions. Therefore, we have derived our description of President Trump’s program from the policies he espoused, and decisions made during his first term. Vice President Biden’s information comes from his campaign platform.

We hope you find these summaries helpful as you weigh your choices for Election Day.

One of Medicare’s trust funds is expected to run out of money in the next few years, but we’ve heard almost nothing about it on the campaign trail. We explain what would happen, how things got so bad, and what can be done to fix it.

Listen to the full episode below, read the transcript or scroll down for more information.

Click here for more of our 2020 election coverage.https://embed.acast.com/tradeoffs/themedicarecliff/?brandColor=e65a4b

Medicare is a federal health insurance program that covers Americans 65 years or older as well as some Americans with certain disabilities. The federal government spends $800 billion a year — 15% of the overall federal budget — on care for the roughly 60 million Medicare beneficiaries.

Medicare is split into four parts:

Covers inpatient hospital visits, as well as hospice, post-acute care and graduate medical education.

Covers physician and outpatient services.

Also known as Medicare Advantage. Allows beneficiaries to get Part A and B benefits through a private insurer.

Covers prescription drugs.

Medicare Part A comes out of the Hospital Insurance (HI) trust fund, which is primarily funded by a 2.9% payroll tax split evenly between employers and employees.

Parts B and D are funded by the Supplementary Medical Insurance (SMI) trust fund, which is primarily funded by general tax revenues and beneficiary premiums.

Medicare Advantage (or Part C) is supported by set per enrollee payments from the HI and SMI trust funds, as well as additional enrollee premiums in some cases.

For many years, the payroll taxes coming into Medicare Part A exceeded the benefits the program needed to pay out. This has allowed Medicare Part A to build up a reserve in the HI trust fund.

Over time, two main factors have often pushed Part A’s annual benefits payments higher than its tax revenue, forcing Medicare to dip into its reserves:

In April, the Medicare Board of Trustees reported that the Part A trust fund had around $200 billion in reserves and that, barring any changes, it would run out in 2026.

But with significant job losses during the pandemic, far lower levels of payroll taxes are expected to be collected, leading the Congressional Budget Office and the Committee for a Responsible Federal Budget to now estimate the HI trust fund will run out — or become insolvent — in 2024.

If Congress is unable to make any changes before the trust fund runs out, Medicare would effectively be operating paycheck-to-paycheck — only able to use current payroll taxes to pay out claims. The Congressional Budget Office estimates that would only cover about 85% of Part A’s bills, leaving providers likely to receive late and incomplete payments, which could lead them to accept fewer Medicare patients or stop taking them altogether.

Congress has never let Medicare Part A run completely dry. When it has gotten close to exhaustion — most recently in 1997 and 2009 — lawmakers used a combination of three tactics to extend the life of the trust fund.

Congress can lower how much it pays hospitals and other providers for different services. It did this as part of the Balanced Budget Act of 1997 and the Affordable Care Act in 2010. One area that has been mentioned this time around as a potential place to cut are payments to post-acute care facilities.

Congress can increase the amount of money coming into the trust fund. It did this as part of the ACA by adding a 0.9% payroll tax surcharge to people earning more than $200,000 a year.

Congress can also ease the burden on the trust fund by deciding to pay for certain benefits from somewhere other than the HI trust fund. For example, in 1997, Congress moved some home health payments into Medicare Part B, which is funded by general tax revenues and premiums.

While leaders from both parties have suggested similar policies to address Medicare’s financial troubles, any spending cuts or tax increases are likely to be politically difficult and generate opposition. Any fix will also take time to implement, meaning that the next president and Congress will have to act quickly to avoid more abrupt and painful remedies.