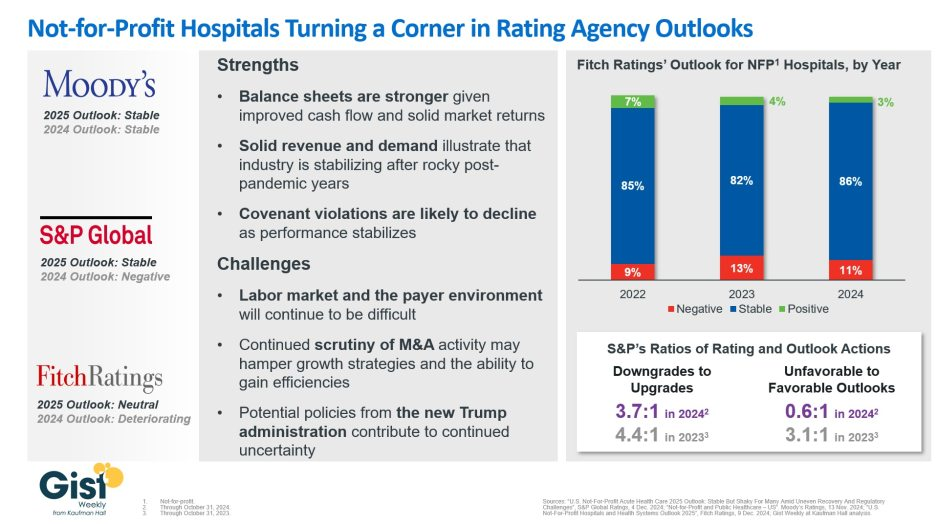

In late 2023, S&P Global and Fitch Ratings viewed the not-for-profit (NFP) hospital sector as negative or deteriorating, reflecting the difficult financial position many were in following the pandemic.

In recent weeks, S&P and Fitch upgraded their 2025 sector outlook for NFP hospitals to stable and neutral respectively, joining Moody’s Ratings, which held stable from last year.

This week’s graphic illustrates the rating agencies’ latest views on NFP hospitals, which point to a promising but uneven recovery for the industry.

Overall, the reports detail that stronger balance sheets, solid revenues, and improved demand have reduced the likelihood of covenant violations and strengthened NFP hospitals’ positions.

However, challenges persist that could impede further progress. The labor market, payer environment, antitrust enforcement, and a new administration all present complications for the continued recovery of NFP hospitals. Nonetheless, the reports indicate significant improvement for the industry since the post-pandemic ratings downturn.

Fitch’s report noted that the share of NFP hospitals with a stable outlook has reached a three-year high. Meanwhile, S&P reported that there are now almost twice as many NFP hospitals with favorable outlooks compared to unfavorable ones, a dramatic flip from 2023, which had a 3.1:1 ratio of unfavorable to favorable outlooks.

These ratings changes reflect the hard work put in by NFP hospitals across the country to improve their financial performance and find new ways to serve their communities sustainably.

However, the recovery remains “shaky” and incomplete, and hospitals still face a long road ahead as they reconfigure to a new normal.

Health systems have a big challenge: rising costs and reimbursement that doesn’t keep up with inflation. The amount spent on healthcare annually continues to rise while outcomes aren’t meaningfully better.

Some people outside of the industry wonder: Why doesn’t healthcare just act more like other businesses?

“There seems to be a widely held belief that healthcare providers respond the same as all other businesses that face rising costs,” said Cliff Megerian, MD, CEO of University Hospitals in Cleveland. “That is absolutely not true. Unlike other businesses, hospitals and health systems cannot simply adjust prices in response to inflation due to pre-negotiated rates and government mandated pay structures. Instead, we are continually innovating approaches to population health, efficiency and cost management, ensuring that we maintain delivery of high quality care to our patients.”

Nonprofit hospitals are also responsible for serving all patients regardless of ability to pay, and University Hospitals is among the health systems distinguished as a best regional hospital for equitable access to care by U.S. News & World Report.

“This commitment necessitates additional efforts to ensure equitable access to healthcare services, which inherently also changes our payer mix by design,” said Dr. Megerian. “Serving an under-resourced patient base, including a significant number of Medicaid, underinsured and uninsured individuals, requires us to balance financial constraints with our ethical obligations to provide the highest quality care to everyone.”

Hospitals need adequate reimbursement to continue providing services while also staffing the hospital appropriately. Many hospitals and health systems have been in tense negotiations with insurers in the last 24 months for increased pay rates to cover rising costs.

“Without appropriate adjustments, nonprofit healthcare providers may struggle to maintain the high standards of care that patients deserve, especially when serving vulnerable populations,” said Dr. Megerian. “Ensuring fair reimbursement rates supports our nonprofit industry’s aim to deliver equitable, high quality healthcare to all while preserving the integrity of our health systems.”

Industry outsiders often seek free market dynamics in healthcare as the “fix” for an expensive and complicated system. But leaving healthcare up to the normal ebbs and flows of businesses would exclude a large portion of the population from services. Competition may lead to service cuts and hospital closures as well, which devastates communities.

“A misconception is that the marketplace and utilization of competitive business model will fix all that ails the American healthcare system,”

said Scot Nygaard, MD, COO of Lee Health in Ft. Myers and Cape Coral, Fla.

“Is healthcare really a marketplace, in which the forces of competition will solve for many of the complex problems we face, such as healthcare disparities, cost effective care, more uniform and predictive quality and safety outcomes, mental health access, professional caregiver workforce supply?”

Without comprehensive reform at the state or federal level, many health systems have been left to make small changes hoping to yield different results. But, Dr. Nygaard said, the “evidence year after year suggests that this approach is not successful and yet we fear major reform despite the outcomes.”

The dearth of outside companies trying to enter the healthcare space hasn’t helped. People now expect healthcare providers to function like Amazon or Walmart without understanding the unique complexities of the industry.

“Unlike retail, healthcare involves navigating intricate regulations, providing deeply personal patient interactions and building sustained trust,” said Andreia de Lima, MD, chief medical officer of Cayuga Health System in Ithaca, N.Y. “Even giants like Walmart found it challenging to make primary care profitable due to high operating costs and complex reimbursement systems. Success in healthcare requires more than efficiency; it demands a deep understanding of patient care, ethical standards and the unpredictable nature of human health.”

So what can be done?

Tracea Saraliev, a board member for Dominican Hospital Santa Cruz (Calif.) and PIH Health said leaders need to increase efforts to simplify and improve healthcare economics.

“Despite increased ownership of healthcare by consumers, the economics of healthcare remain largely misunderstood,” said Ms. Saraliev. “For example, consumers erroneously believe that they always pay less for care with health insurance. However, a patient can pay more for healthcare with insurance than without as a result of the negotiated arrangements hospitals have with insurance companies and the deductibles of their policy.”

There is also a variation in cost based on the provider, and even with financial transparency it’s a challenge to provide an accurate assessment for the cost of care before services. Global pricing and other value-based care methods streamline the price, but healthcare providers need great data to benefit from the arrangements.

Based on payer mix, geographic location and contracted reimbursement rates, some health systems are able to thrive while others struggle to stay afloat. The variation mystifies some people outside of the industry.

“Healthcare economics very much remains paradoxical to even the most savvy of consumers,” said Ms. Saraliev.

Last Thursday, Seattle-based Providence Health System announced it is refunding nearly $21 million in medical bills paid by low-income residents of Washington and erasing $137 million more in outstanding debt for others. Other systems are likely to follow as pressure con mounts on large, not-for-profit systems to modify their business practices in sensitive areas like patient debt collection, price transparency, executive compensation, investment activities and others.

Not-for profit systems control the majority of the 2,987 nongovernment not-for-profit community hospitals in the U.S. Some lawmakers think it’s time to revisit to revisit the tax exemption. It has the attention of the American Hospital Association which lists “protecting not-for-profit hospitals’ the tax-exempt status” among its 15 Advocacy Priorities in 2024 (it was not on their list in 2023).

Background: Per a recent monograph in Health Affairs: “The Internal Revenue Service (IRS) uses the Community Benefit Standard (CBS), a set of 10 holistically analyzed metrics, to assess whether nonprofit hospitals benefit community health sufficiently to justify their tax-exempt status. Nonprofit hospitals risk losing their tax exemption if assessed as underinvesting in improving community health. This exemption from federal, state, and local property taxes amounts to roughly $25 billion annually.

However, accumulating evidence shows that many nonprofit hospitals’ investments in community health meet the letter, but not the spirit, of the CBS.

Indeed, a 2021 study showed that for every $100 in total expenses nonprofit hospitals spend just $2.30 on charity care (a key component of community benefit)—substantially less than the $3.80 of every $100 spent by for-profit hospitals. A 2022 study looked at the cost of caring for Medicaid patients that goes unreimbursed and is therefore borne by the hospital (another key component of community benefit); the researchers found that nonprofit hospitals spend no more than for-profit hospitals ($2.50 of every $100 of total expense).”

In its most recent study, the AHA found the value of CBS well-in-excess of the tax exemption by a factor of 9:1. But antagonism toward the big NFP systems has continued to mount and feelings are intense…

Insurers think NFP systems exist to gain leverage in markets & states over insurers in contract negotiations and network design. They’ll garner support from sympathetic employers and lawmakers, federal anti-consolidation and price transparency rulings and in the court of public opinion where frustration with the system is high.

State officials see the mega- NFP systems as monopolies that don’t deserve their tax exemptions while the state’s public health, mental health and social services programs struggle.

Some federal lawmakers think the NFP systems are out of control requiring closer scrutiny and less latitude. They think the tax exemption qualifiers should be re-defined, scrutinized more aggressively and restricted.

Well-publicized investments by NFP systems in private equity backed ventures has lent to criticism among labor unions and special interests that allege systems have abandoned community health for Wall Street shareholders.

Investor-owned multi-hospital operators believe the tax exemption is an unfair advantage to NFPs while touting studies showing their own charity care equivalent or higher.

Other key NFP and public sector hospital cohorts cry foul: Independent hospitals, academic medical centers, safety-net (aka ‘essential’) hospitals, rural health clinics & hospitals, children’s hospitals, rural health providers, public health providers et al think they get less because the big NFPs get more.

And the physicians, nurses and workforces employed by Big NFP systems are increasingly concerned by systemization that limits their wages, cuts their clinical autonomy and compromises their patients’ health.

My take:

The big picture is this: the growth and prominence of multi-hospital systems mirrors the corporatization in most sectors of the economy: retail, technology, banking, transportation and even public utilities. The trifecta of community stability—schools, churches and hospitals—held out against corporatization, standardization and franchising that overtook the rest. But modernization required capital, the public’s expectations changed as social media uprooted news coverage and regulators left doors open for “new and better” that ceded local control to distant corporate boards.

Along the way, investor-owned hospitals became alternatives to not-for-profits, and loose networks of hospitals that shared purchasing and perhaps religious values gave way to bigger multi-state ownership and obligated groups.

The attention given large NFP hospital systems like Providence and others is not surprising. These brands are ubiquitous. Their deals with private equity and Big Tech are widely chronicled in industry journalism and passed along in unfiltered social media. And their collective financial position seems strong: Moody’s, Fitch, Kaufman Hall and others say utilization has recovered, pandemic recovery is near-complete and, despite lingering concerns about workforce issues, growth in their core businesses plus diversification in new businesses are their foci. (See Hospital Section below).

I believe not-for-profit hospital systems are engines for modernizing health delivery in communities and a lightening rod for critics who think their efforts more self-serving than for the public good.

Most consumers (55%) think they earn their tax exemption but 34% have mixed feelings and 10% disagree. (Keckley Poll November 20, 2023). That’s less than a convincing defense.

That’s why the threat to the tax exemption risk is real, and why every organization must be prepared. Equally important, it’s why AHA, its state associations and allies should advance fresh thinking about ways re-define CBS and hardwire the distinction between organizations that exist for the primary purpose of benefiting their shareholders and those that benefit health and wellbeing in their communities.

PS: Must reading for industry watchers is a new report from by Health Management Associates (HMA) and Leavitt Partners, an HMA company, with support from Arnold Ventures. The 70-page report provides a framework for comparing the increasingly crowned field of 120 entities categorized in 3 groups: Hybrids (6.9 million), Delivery (5.8 million) and Enablers 17.5 million

“At the start of the movement, value-based arrangements primarily involved traditional providers and payers engaging in relatively straight-forward and limited contractual arrangements. In recent years, the industry has expanded organically to include a broader ecosystem of risk-bearing care delivery organizations and provider enablement entities with capabilities and business models aligned with the functions and aims of accountable care…Inclusion criteria for the 120 VBD entities included in this analysis were:

1-Serve traditional Medicare, MA, and/or Medicaid populations. Entities that are focused solely on commercial populations were excluded

2-Operate in population-based, total cost of care APMs—not only bundled payment models.

3- Focus on primary care and/or select specialties that are relevant to total cost of care models (i.e., nephrology, oncology, behavioral health, cardiology, palliative care). Those exclusively focused on specialty areas geared toward episodic models (e.g., MSK) were excluded. –

4-Share accountability for cost and quality outcomes. Business models must be aligned with provider performance in total cost of care arrangements. Vendors that support VBP but do not share accountability for outcomes were excluded.

Jersey City, N.J.-based CarePoint Health and Hudson Regional Hospital in Secaucus, N.J., have signed a letter of intent to combine under a new management company, Hudson Health System, which will incorporate the acute care facilities of both organizations.

Hudson Health System would be a four-hospital system that includes both nonprofit and for-profit hospitals in an innovative new model and continue to be in-network with all major payers.

The transaction is expected to strengthen CarePoint’s financial position and improve patient care and outcomes across the hospitals, according to John Rimmer, CarePoint’s chief medical officer, said in a Jan. 12 news release.

“Hudson County is the most diverse and dynamic community in New Jersey, and its residents deserve nothing less than exceptional care, affordable access, the most advanced specialties and technology, and the highest caliber physicians to serve patients’ needs, especially the underserved communities that rely on our facilities,” said CarePoint President and CEO Achintya Moulick, MD, who will be president and CEO of Hudson Health System. “With adequate state support, I believe we can build a hospital system that will deliver on its core mission.”

The letter of intent is the precursor to a new organizational structure and operating plan that will require approval from the New Jersey State Department of Health. Hudson Health System would be a four-hospital system that includes Hudson Regional, Bayonne Medical Center, Hoboken University Medical Center and Christ Hospital in Jersey City.

“This new system expands our mutual impact far beyond and far sooner than what we could ever have achieved separately,” Hudson Regional CEO Nizar Kifaieh, MD, said. “The possibilities are enormous and will energize the entire medical community to deliver that much more to the patients.”

More details about Hudson Health System are expected to be announced in the coming days.

The U.S. health system has experienced three major shifts since the pandemic that set the stage for its future:

From trust to distrust: Every poll has chronicled the decline in trust and confidence in government: Congress, the Presidency, the FDA and CDC and even the Supreme Court are at all-time lows. Thus, lawmaking about healthcare is met with unusual hostility.

From big to bigger: The market has consistently rewarded large cap operators, giving advantage to national and global operators in health insurance, information technology and retail health. In response, horizontal consolidation via mergers and acquisitions has enabled hospitals, medical practices, law firms and consultancies to get bigger, attracting increased attention from regulators. Access to private capital and investor confidence is a major differentiator for major players in each sector.

From regulatory tailwinds to headwinds: in the last 3 years, regulators have forced insurers, hospitals and drug companies to disclose prices and change business practices deemed harmful to fair competition and consumer choice. Incumbent-unfriendly scrutiny has increased at both the state and federal levels including notable bipartisan support for industry-opposed legislation. It will continue as healthcare favor appears to have run its course.

Some consider these adverse; others opportunistic; all consider them profound. All concede the long-term destination of the U.S. health system is unknown. Against this backdrop, 2024 is about safe bets.

These 10 themes will be on the agenda for every organization operating in the $4.5 trillion U.S. healthcare market:

Not for profit health: “Not-for-profit” designation is significant in healthcare and increasingly a magnet for unwelcome attention. Not-for-profit hospitals, especially large, diversified multi-hospital systems, will face increased requirements to justify their tax exemptions. Special attention will be directed at non-operating income activities involving partnerships with private equity and incentives used in compensating leaders. Justification for profits will take center stage in 2024 with growing antipathy toward organizations deemed to put profit above all else.

Insurer coverage and business practices: State and federal regulators will impose regulatory constraints on insurer business practices that lend to consumer and small-business affordability issues.

Workforce wellbeing: The pandemic hangover, sustained impact of inflation on consumer prices, increased visibility of executive compensation and heightened public support for the rank-and-file workers and means wellbeing issues must be significant in 2024.

Board effectiveness: The composition, preparedness, compensation and independent judgement of Boards will attract media scrutiny; not-for-profit boards will get special attention in light of 2023 revelations in higher education.

Employer-sponsored health benefits: The cost-effectiveness of employee health benefits coverage will prompt some industries and large, self-insured companies to pursue alternative strategies for attracting and maintaining a productive workforce. Direct contracting, on-site and virtual care will be key elements.

Physician independence: With 20% of physicians in private equity-backed groups, and 50% in hospital employed settings, ‘corporatization’ will encounter stiff resistance from physicians increasingly motivated to activism believing their voices are unheard.

Data driven healthcare: The health industry’s drive toward interoperability and transparency will will force policy changes around data (codes) and platform ownership, intellectual property boundaries, liability et al. Experience-based healthcare will be forcibly constrained by data-driven changes to processes and insights.

Consolidation: The DOJ and FTC will expand their activism against vertical and horizontal consolidation that result in higher costs for consumers. Retrospective analyses of prior deals to square promises and actual results will be necessary.

Public health: State and federal funding for public health programs that integrate with community-based health providers will be prioritized. The inadequacy of public health funding versus the relative adequacy of healthcare’s more lucrative services will be the centerpiece for health reforms.

ACO 2.0: In Campaign 2024, abortion and the Affordable Care Act will be vote-getters for candidates favoring/opposing current policies. Calls to “Fix and Repair” the Affordable Care Act will take center stage as voters’ seek affordability and access remedies.

Every Board and C suite in U.S. healthcare will face these issues in 2024.

Does hospital ownership matter? According to a study published last week in Health Affairs Scholar, NOT MUCH. That’s a problem for not-for-profit hospitals who claim otherwise.

58% of U.S. hospitals are not-for-profit hospitals; the rest are public (19%) or investor-owned (24%). In recent months, not-for-profit systems have faced growing antagonism from regulators and critics who challenge the worthwhileness of their tax exemptions and reasonableness of the compensation paid their top executives.

The lion’s share of this negative attention is directed at large, not-for-profit hospital system operators. Case in point: last week, Banner Health (AZ) joined the ranks of high-profile operators taken to task in the Arizona Republic for their CEO’s compensation contrasting it to not-for-profit sectors in which compensation is considerably lower.

Unflattering attention to NFP hospitals, especially the big-name systems, is unlikely to subside in the near-term. U.S. healthcare has become a winner-take-all battleground increasingly dominated by large-scale, investor-owned interests in hospitals, medical groups, insurance, retail health in pursuit of a piece of the $4.6 trillion pie.

The moral high ground once the domain of not-for-profit hospitals is shaky.

The NYU study examined whether hospital ownership influenced decisions made by consumers: they found “Fewer than one-third of respondents (29.5%) indicated that hospital status had ever been relevant to them in making decisions about where to seek care…significantly more important to respondents who indicated the lowest health literacy—74.7% of whom answered the key question affirmatively—than it was for people who indicated high health literacy, of whom only 18.3% found hospital ownership status to be relevant…also considerably more relevant for people working in health care than for those who did not work in health care (61.0% vs 24.5%)…

We found little evidence that hospital nonprofit status influenced Americans’ decisions about where to seek care. Ownership status was relevant for fewer than 30% of respondents and preference was greatest overall for public hospitals. Only 30–45% of respondents could correctly identify the ownership status of nationally recognized hospitals, and fewer than 30% could identify their local hospitals.

These findings suggest that contract failure does not currently provide a justification of nonprofit hospitals’ value; further scrutiny of tax exemption for nonprofit hospitals is warranted.”

Are NFP hospitals concerned? YES. It’s reality as systems address near term operational challenges and long-term questions about their strategies.

Last weekend, I facilitated the 4th Annual Chief Strategy Officers Roundtable in Austin TX sponsored by Lumeris. The group consisted of senior-level strategists from 11 not-for-profit systems and one for-profit. In one session, each reacted to 50 future state scenarios in terms of “likelihood” and “disruptive impact” in the NEAR term (3-5 years) and LONG TERM (8-10 years) using a 1 to 10 scale with 10 HI.

From these data and the discussion that followed, there’s consensus that the U.S. healthcare market is unlikely to change dramatically long-term, their short-term conditions will be tougher and their challenges unique.

‘Near-term cost containment is a priority. Hospitals are here-to-stay, but operating them will be harder.’

‘Increased scale and growth are necessary imperatives for their systems.’

‘Hospital systems will compete in a market wherein private capital and investor ownership will play a growing role, insurers will be hostile and value will the primary focus of cost-reduction by purchasers and policymakers.’

‘Distinctions betweennot-for-profit and for-profit hospitals are significant.’

‘Conditions for hospitals will be tougher as insurers play a stronger hand in shaping the future.’

Given the NYU study findings (above) concluding NFP ownership has marginal impact on hospital choices made by consumers, it’s understandable NFPs are anxious.

My take:

The issues facing not-for-profit hospitals in the U.S. are unique and complex. Per the commentary of the CSOs, their market conditions are daunting and major changes in their structure, funding and regulation unlikely.

That means lack of public understanding of their unique role is a conundrum.

Paul

PS: Issues about CEO compensation in healthcare are touchy and often unfair.

In every major NFP system, comp is set by the Independent Board Compensation Committee with outside consultative counsel. The vast majority of these CEOs aren’t in the job for the money joining their workforce in pursuit of the unique higher calling afforded service leaders in NFP healthcare.

Last Monday, four U.S. Senators took aim at the tax exemption enjoyed by not-for-profit (NFP) hospitals in a letter to the IRS demanding detailed accounting for community benefits and increased agency oversight of NFP hospitals that fall short.

Last Tuesday, the Elevance Health Policy Institute released a study concluding that the consolidation of hospitals into multi-hospital systems (for-profit/not-for-profit) results in higher prices without commensurate improvement in patient care quality. “

Friday, Kaiser Health News Editor in Chief Elizabeth Rosenthal took aim at Ballad Health which operates in TN and VA “…which has generously contributed to performing arts and athletic centers as well as school bands. But…skimped on health care — closing intensive care units and reducing the number of nurses per ward — and demanded higher prices from insurers and patients.”

And also last week, the Pharmaceuticals’ Manufacturers Association released its annual study of hospital mark-ups for the top 20 prescription drugs used on hospitals asserting a direct connection between hospital mark-ups (which ranged from 234% to 724%) and increasing medical debt hitting households.

(Excerpts from these are included in the “Quotables” section that follows).

It was not a good week for hospitals, especially not-for-profit hospitals.

In reality, the storm cloud that has gathered over not-for-profit health hospitals in recent months has been buoyed in large measure by well-funded critiques by Arnold Ventures,Lown Institute, West Health, Patient Rights Advocate and others. Providence, Ascension, Bon Secours and now Ballad have been criticized for inadequate community benefits, excessive CEO compensation, aggressive patient debt collection policies and price gauging attributed to hospital consolidation.

This cloud has drawn attention from lawmakers: in NC, the State Treasurer Dale Folwell has called out the state’s 8 major NFP systems for inadequate community benefit and excess CEO compensation.

In Indiana, State Senator Travis Holdman is accusing the state’s NFP hospitals of “hoarding cash” and threatening that “if not-for-profit hospitals aren’t willing to use their tax-exempt status for the benefit of our communities, public policy on this matter can always be changed.” And now an influential quartet of U.S. Senators is pledging action to complement with anti-hospital consolidation efforts in the FTC leveraging its a team of 40 hospital deal investigators.

In response last week, the American Hospital Association called out health insurer consolidation as a major contributor to high prices and,

in a US News and World Report Op Ed August 8, challenged that “Health insurance should be a bridge to medical care, not a barrier.

Yet too many commercial health insurance policies often delay, disrupt and deny medically necessary care to patients,” noting that consumer medical debt is directly linked to insurer’ benefits that increase consumer exposure to out of pocket costs.

My take:

It’s clear that not-for-profit hospitals pose a unique target for detractors: they operate more than half of all U.S. hospitals and directly employ more than a third of U.S. physicians.

But ownership status (private not-for-profit, for-profit investor owned or government-owned) per se seems to matter less than the availability of facilities and services when they’re needed.

And the public’s opinion about the business of running hospitals is relatively uninformed beyond their anecdotal use experiences that shape their perceptions. Thus, claims by not-for-profit hospital officials that their finances are teetering on insolvency fall on deaf ears, especially in communities where cranes hover above their patient towers and their brands are ubiquitous.

Demand for hospital services is increasing and shifting, wage and supply costs (including prescription drugs) are soaring, and resources are limited for most.

The size, scale and CEO compensation for the biggest not-for-profit health systems pale in comparison to their counterparts in health insurance and prescription drug manufacturing or even the biggest investor-owned health system, HCA…but that’s not the point.

NFPs are being challenged to demonstrate they merit the tax-exempt treatment they enjoy unlike their investor-owned and public hospital competitors and that’s been a moving target.

Thus, the methodology for consistently defining and accounting for community benefits needs attention. That would be a good start but alone it will not solve the more fundamental issue: what’s the future for the U.S. health system, what role do players including hospitals and others need to play, and how should it be structured and funded?

The issues facing the U.S. health industry are complex. The role hospitals will play is also uncertain. If, as polls indicate, the majority of Americans prefer a private health system that features competition, transparency, affordability and equitable access, the remedy will require input from every major healthcare sector including employers, public health, private capital and regulators alongside others.

It will require less from DC policy wonks and sanctimonious talking heads and more from frontline efforts and privately-backed innovators in communities, companies and in not-for-profit health systems that take community benefit seriously.

No sector owns the franchise for certainty about the future of U.S. healthcare nor its moral high ground. That includes not-for-profit hospitals.

The darkening cloud that hovers over not-for-profit health systems needs attention, but not alone, despite efforts to suggest otherwise.

Clarifying the community-benefit standard is a start, but not enough.

Are NFP hospitals a problem? Some are, most aren’t but all are impacted by the darkening cloud.

A bipartisan quartet of influential senators is tapping tax regulators within the U.S. Treasury for detailed information on nonprofit hospitals’ reported charity care and community investments, the latest in legislators’ increasing scrutiny of tax-exempt hospitals’ business practices.

In a pair of letters (PDF) sent Monday, Sens. Elizabeth Warren, D-Massachusetts, Raphael Warnock, D-Georgia, Bill Cassidy, M.D., R-Louisiana, and Chuck Grassley, R-Iowa, wrote they “are alarmed by reports that despite their tax-exempt status, certain nonprofit hospitals may be taking advantage of this overly broad definition of ‘community benefit’ and engaging in practices that are not in the best interest of the patient.”

They also outlined studies from academic and policy groups highlighting that the tax-exempt status of the nation’s nonprofit hospitals collectively was worth about $28 billion in 2020 and how this tally paled in comparison to the charity care most of those hospitals had provided during that same period.

Such studies have been quickly contested by the hospital lobby, which highlights that charity care is just one component of the broader activities that constitute a nonprofit hospital’s community benefit spending.

However, that ambiguity was squarely in the crosshairs of the legislators who said the long-standing community benefit standard “is arguably insufficient in its current form to guarantee protection and services to the communities hosting these hospitals.”

They cited a 2020 report from the Government Accountability Office that found oversight of nonprofit hospitals’ tax exemptions was “challenging” due to the vague definition of community benefit.

Though the IRS implemented several of the office’s recommendations from the report, “more is required to ensure nonprofit hospitals’ community benefit information is standardized, consistent and easily identifiable.” Included here could be additional updates to Form 990’s Schedule H, where nonprofits detail their community benefits and related activities.

To get a better handle on the agencies’ current oversight, the legislators requested from the IRS and the Treasury’s Tax Exempt & Government Entities Division a laundry list of information related to nonprofits’ tax filings from the last several years, including “a list of the most commonly reported community benefit activities that qualified a nonprofit hospital for tax exemptions in FY2021 and FY2022.”

They also sought lists of the nonprofit hospitals that were flagged, penalized or had their tax-exempt status revoked for violating community benefit standard requirements.

In another letter to the Treasury’s inspector general for tax administration, they asked the auditor to update their upcoming reviews to evaluate existing standards for financial assistance policy and other “practices that reduce unnecessary medical debt from patients who qualify for free or discounted care.”

The lawmakers also asked the inspector general to explore how often nonprofit hospitals bill patients with “gross charges” and to make sure the IRS is doing enough to ensure hospitals are making “’reasonable efforts’ to determine whether individuals are eligible for financial assistance before initiating extraordinary collection actions.”

Both letters from the senators gave the tax regulators 60 days to provide the requested information.

As first half 2023 financial results are reported and many prepare for a busy last half, strategic planning for healthcare services providers and insurers point to 4 issues requiring attention in every boardroom and C suite:

Private equity maturity wall:

The last half of 2023 (and into 2024) is a buyer’s market for global PE investments in healthcare services: 40% of PE investments in hospitals, medical groups and insurtech will hit their maturity wall in the next 12 months. Valuations of companies in these portfolios are below their targeted range; limited partner’ investing in PE funds is down 28% from pre-pandemic peak while fund raising by large, publicly traded, global funds dominate fund raising lifting PE dry powder to a record $3.7 trillion going into the last half of 2023.

In the U.S. healthcare services market, conditions favor well-capitalized big players—global private equity funds and large cap aggregators (i.e., Optum, CVS, Goldman Sachs, Blackstone et al) who have $1 trillion to invest in deals that enhance their platforms. Deals done via special purpose acquisition corporations (SPACS) and smaller PE funds in physicians, hospitals, ambulatory services and others are especially vulnerable. (see Bain and Pitchbook citations below). Addressing the growing role of large-cap PE and strategic investors as partners, collaborators, competitors or disruptors is table stakes for most organizations recognizing they have the wind at their backs.

Consolidation muscle by DOJ and FTC:

Healthcare is in the crosshair of the FTC and DOJ, especially hospitals and health insurers. Hospital markets have become increasingly concentrated: only 12% of the 306 Hospital Referral Regions is considered unconcentrated vs. 23% in 2008. In the 384 insurance markets, 23% are unconcentrated, down from 35% in 2020. Wages for healthcare workers are lower, prices for consumers are higher and choices fewer in concentrated markets prompting stricter guidelines announced last week by the oversight agencies. Big hospitals and big insurers are vulnerable to intensified scrutiny. (See Regulatory Action section below).

Defamatory attacks on nonprofit health systems:

In the past 3 years, private, not-for-profit multi-hospital systems have been targeted for excess profits, inadequate charity care and executive compensation. Labor unions (i.e., SEIU) and privately funded foundations (i.e., West, Arnold Venture, Lown Institute) have joined national health insurers in claims that NFP systems are price gaugers undeserving of the federal, state and local tax exemptions they enjoy. It comes at a time when faith in the U.S. health system is at a modern-day low (Gallup), healthcare access and affordability concerns among consumers are growing and hospital price transparency still lagging (36% are fully compliant with the 2021 Executive Order).

Notably, over the last 20 years, NFP hospitals have become less dominant as a share of all hospitals (61% in 2002 vs. 58% last year) while investor-owned hospitals have shown dramatic growth (from 15% in 2002 to 24% last year). Thus, the majority of local NFP hospitals have joined systems creating prominent brands and market dominance in most regions. But polling indicates many of these brands is more closely associated with “big business” than “not-for-profit health” so they’re soft targets for critics. It is likely unflattering attention to large, NFP systems will increase in the next 12 months prompting state and federal regulatory actions and erosion of public support. (See New England Journal citation in Quotables below)

Campaign 2024 healthcare rhetoric:

Republican candidates will claim healthcare is not affordable and blame Democrats. Democrats will counter that the Affordable Care Act’s expanded coverage and the Biden administration’s attack on drug prices (vis a vis the Inflation Reduction Act) illustrate their active attention to healthcare in contrast to the GOP’s less specific posturing.

Campaigns in both parties will call for increased regulation of hospitals, prescription drug manufacturers, health insurers and PBMs. All will cast the health industry as a cesspool for greed and corruption, decry its performance on equitable access, affordability, price transparency and improvements in the public’s health and herald its frontline workers (nurses, physicians et al) as innocent victims of a system run amuck.

To date, 16 candidates (12 R, 3 D, 1 I) have announced they’re candidates for the White House while campaigns for state and local office are also ramping up in 46 states where local, state and national elections are synced. Healthcare will figure prominently in all. In campaign season, healthcare is especially vulnerable to misinformation and hyper-attention to its bad actors. Until November 5, 2024, that’s reality.

My take:

These issues frame the near-term context for strategic planning in every sector of U.S. healthcare. They do not define the long-term destination of the system nor roles key sectors and organizations will play. That’s unknown.

What’s known for sure is that AI will modify up to 70% of the tasks in health delivery and financing and disrupt its workforce.

Black Swans like the pandemic will prompt attention to gaps in service delivery and inequities in access.

People will be sick, injured, die and be born.

And the economics of healthcare will force uncomfortable discussions about its value and performance.

In the U.S. system, attention to regulatory issues is a necessary investment by organizations in every state and at the federal level. Details about these efforts is readily accessible on websites for each organization’s trade group. They’re the rule changes, laws and administrative actions to which all are attentive. They’re today’s issues.

Less attention is given the long-term. That focus is often more academic than practical—much the same as Robert Oppenheimer’s early musings about the future of nuclear fusion. But the Manhattan Project produced two bombs (Little Boy and Fat Man) that detonated above the Japanese cities of Hiroshima and Nagasaki in 1945, triggering the end of World War II.

The four issues above should be treated as near and present dangers to the U.S. health system requiring attention in every organization. But responses to these do not define the future of the U.S. system. That’s the Manhattan Project that’s urgently needed in our system.

Last week, 35,000 gathered in Chicago to hear about the future of health information technologies at the HIMSS Global Health Conference & Exhibition where generative AI, smart devices and cybersecurity were prominent themes.

Yesterday, the Annual Meeting of the American Hospital Association convened. Its line-up includes some big names in federal health policy and politics along with some surprising notaries like Chris Wray, Head of the FBI and others. In tandem, a new TV ad campaign launched yesterday by the Coalition to Protect America’s Health Care, of which the AHA is a founding member to pressure Congress to avoid budget cuts to hospitals to “protect care for seniors”.

These events bracket what has been a whip-lash week for the U.S. healthcare industry…

Throughout the week, the fate of medication-abortion mifepristone was in suspense ending with a Supreme Court emergency-stay decision late Friday night that defers prohibitions against its use until court challenges are resolved.

At HIMSS last Monday, EHR juggernaut EPIC and Microsoft announced they are expanding their partnership and integrating Microsoft’s Azure Open AI Service into Epic’s EHR software. Epic’s EHR system will be able to run generative AI solutions through Microsoft’s Open AI Azure Service. Microsoft uses Open Ai’s language model GPT-4 capabilities in its Azure cloud solution.

Thursday HHS posted data online showing who owns 6,000 hospices and 11,000 home health agencies that are reimbursed by Medicare.

Bell-weather companies HCA (investor-owned hospitals), Johnson and Johnson (prescription drugs) and Elevance (health insurers) reported strong 1Q profits and raised their guidance to shareholders for year-end performance.

And Monday, House Speaker Kevin McCarthy told an audience at the New York Stock Exchange that Republicans will agree to increase the $31.4 trillion debt-limit if it is accompanied by spending cuts i.e. a requirement that all “able bodied Americans without children” work to receive benefits like Medicaid, re-setting federal spending to 2022 levels and others.

Each of these is newsworthy. The partisan brinksmanship about the debt ceiling is perhaps the most immediately consequential for healthcare because it will draw attention to 2 themes:

Healthcare is profitable for some. Big companies and others with access to capital are advantaged in the current environment. Healthcare is fast-becoming a land of giants: it’s almost there in health insurance (the Big 7 in the US), prescription drugs (36 major players globally), retail drugstores (the Big 5), PBMs (the Big 4) and even the accountancies who monitor their results (the Big 4).

By contrast, the hospital and long-term care sectors sectors remain fragmented though investor-owned systems now own a quarter of operations in both.

Physicians and other clinical service provider sectors (physical therapy, dentistry, et al) are transitioning toward two options—corporatization via private equity roll-ups or hospital employment.

The 1Q earnings reported by HCA, J&J and Elevance last week give credence to beliefs among budget hawks that healthcare is a business that can be lucrative for some and expensive for all. That view aka “Survival of the Fittest” will figure prominently into the debt ceiling debate.

The regulatory environment in which U.S. healthcare operates is hostile because the public thinks it needs more scrutiny. 82% of U.S. adults think the health system puts its profits above all else. The public’s antipathy toward the system feeds regulatory activism toward healthcare.

At a federal level, the debt ceiling debate in Congress will be intense and healthcare cuts a likely by-product of negotiations between hawks and doves.

In addition, government accountants and lawmakers will increase penalties for fraud and compliance suspecting healthcare’s ripe for ill-gotten gain and/or excess. Federal advocacy in each sector will be strained by increasingly significant structural fault-lines between non-profit and for profits, and public health programs that operate on shoestrings below the radar. Two committees of the House (Ways and Means and Energy and Commerce) and two Senate Committee’s) will hold public hearings on issues including not-for-profit hospitals consolidation, price transparency and others with unprecedented Bipartisan support for changes likely “uncomfortable” for industry insiders.

At a state level, matters are even more complicated: states are the gatekeeper for the healthcare system’s future. States will increasingly control the supply and performance criteria for providers and payers. Ballot referenda will address issues reflective of the state’s cultural and political values—abortion rights, public health funding, gun control, provider and prescription drug price controls, and many more.

My take

The upcoming debt ceiling debate comes at a pivotal time for healthcare because it does not enjoy the good will it has in decades past. The pandemic, dysfunctional political system and the struggling economy have taken a toll on public confidence. Long-term planning for the system’s future is subordinated to the near term imperative to control costs in the context of the debt ceiling debate.

The federal debt will hit its ceiling in June. Speaker McCarthy’s ‘Limit, Save, Grow Act’ would return the government’s discretionary spending to fiscal year 2022 levels, cap annual spending growth at 1% for a decade and raise the debt ceiling until March 31, 2024, or until the national debt increases by $1.5 trillion, whichever comes first.

That means healthcare program cuts. That’s why this debt ceiling expansion is more than perfunctory: it’s an important barometer about the system’s future in the U.S. and how it MIGHT evolve:

In 8-10 years, it MIGHT be dominated by fewer players with heightened regulatory constraints.

It MIGHT be funded by higher taxes in exchange for better performance.

It MIGHT be restructured with acute services as a public utility. It might be a B2C industry in which employers play a lesser role and a national platform powered by generative AI and GPT4 enables self-care and interoperability.

It MIGHT be an industry wherein public health and social services programs are seamlessly integrated with non-profit health systems.

It MIGHT be built on the convergence of financing and delivery into regional systems of health.

It MIGHT bifurcate into two systems—one public for the majority and one private for some who can afford it.

It MIGHT replace the trade-off between community benefits and tax exemption.

It MIGHT re-define distinctions between non-profit hospitals and plans with their predicate investor-owned operators, and so on.

No one knows for sure, but everyone accepts the future will NOT be a repeat of the past. And the resolution of the debt ceiling in the next 60 days will set the stage for healthcare for the next decade.