Kaiser Permanente built on 2023’s strong start with $2.08 billion of net income during the quarter ended June 30, bringing its midyear total to about $3.29 billion, the integrated system announced late Friday.

Operating income was also strong at $741 million (2.9% margin) and raised the organization’s six-month performance to $974 million (1.9% margin).

The numbers are both a sequential improvement and a stark turnaround from 2022. By the midpoint of that year, Kaiser Permanente was reporting a $1.3 billion net loss for the quarter and an $89 million operating gain (0.4% margin). Across 2022’s first half, the system had been down a total of $2.26 billion and added just $17 million from operations (0.0% margin).

The Oakland, California-based nonprofit is likely safe from repeating the nearly $4.5 billion net loss and $1.3 billion operating loss of full-year 2022.

Leadership, however, noted that the integrated system historically sees higher operating margins during the first half of the year “due in part to the annual enrollment cycle and seasonal care.”

“Our second-quarter financial results reflect operational improvements that, together with our ongoing expense reduction efforts, will help us face additional financial pressures in the second half of the year,” Kathy Lancaster, executive vice president and chief financial officer at Kaiser Permanente, said in a release. “The process of building our financial performance back to pre-pandemic levels requires that we continue to redesign our cost structure to support investments in our facilities, technology and people while staying competitive in a dynamic healthcare marketplace.”

Kaiser Permanente reported $25.17 billion in operating revenues for the second quarter, a 7.2% increase year over year. Operating expenses increased 4.5% year-over-year to $24.42 billion.

“Like all health systems, Kaiser Permanente is experiencing ongoing cost headwinds and volatility driven by inflation, labor shortages, and the lingering effects of the pandemic on access to care and service,” the system wrote in a release.

Kaiser Permanente’s membership has increased by more than 81,000 members since the start of the year and sits at almost 12.7 million as of June 30. The organization noted that it has kicked off an outreach campaign for Medicaid members “to ensure they have critical enrollment information as states go through the mandated process of eligibility redetermination.”

The largest impact on Kaiser Permanente’s bottom line came from investments. Owing to “favorable financial market conditions,” the organization recorded $1.34 billion in “other income and expense,” nearly a full reversal of the $1.39 billion loss on the same line item it’d logged during the same period last year.

The system’s capital spending reached $824 million for the quarter, which was up from $789 million during the second quarter of 2022 but a pullback from the first quarter of 2023’s $930 million.

“The post-pandemic financial pressures have led many in the industry to cut back on care and service,” CEO Greg Adams said in an accompanying statement. “At Kaiser Permanente, we remain focused on improving access and affordability for our patients, members and communities, which requires continued investment in care and coverage. … I want to thank all employees and physicians for turning the disruptions and challenges of the past three years into opportunities to make our healthcare system stronger and more equitable, with improved outcomes for all.”

Kaiser Permanente is the largest nonprofit health system in the country by revenue with more than $95 billion in annual revenues. As of June 30, it spanned 39 hospitals, 622 medical offices and 43 clinics in addition to its millions of covered health plan members.

Earlier in the year the system highlighted efforts to trim administrative and discretionary spending as well as a workforce push that improved clinical hiring by 15% year over year. It is in the midst of negotiating a new labor contract covering 85,000 unionized healthcare workers who are seeking workforce development investments and higher staffing levels across clinical settings.

The organization is also working toward its high-profile acquisition of fellow integrated nonprofit Geisinger Health, which Kaiser Permanente said would be the first step toward a cross-country value-based care organization called Risant Health.

In January 2023, the Rockefeller Institute published a three-part blog series on trends to watch in healthcare in 2023. The series covered broad issues related to the healthcare workforce, economy, and health policy, and highlighted internal industry changes and trends in service delivery, quality, and equity.

Here, we provide a recap and mid-year update on those trends.

The Public Health Emergency:

In January, we anticipated the COVID-19 federal public health emergency (PHE) would end at some point during the year and its ending would impact the industry by rolling back flexibilities and programs that were temporarily put in place to combat the pandemic. The end of the PHE, while not a “trend” per se, held significant potential to alter the trajectory of trends in healthcare coverage, access, and care delivery that were occurring during the pandemic.

Mid-year Update: As predicted, the PHE was not renewed and ended on May 11, 2023. The most notable impact of the non-renewal of the PHE was the end of continuous Medicaid public health insurance coverage. The Kaiser Family Foundation’s Medicaid Enrollment Tracker shows that, as of July 5, 2023, 1,652,000 Medicaid enrollees were disenrolled by the District of Columbia and 28 states reporting data. For context, this means that 39% of people with a completed renewal were disenrolled in reporting states, though disenrollment rates varied significantly across those states from 16 percent in Virginia to 75 percent in South Carolina. The eligibility redetermination process that can lead to a potential disenrollment is being conducted differently in each state with some states moving quickly to make redeterminations and others doing the process more deliberately over the course of the year with a clear intent to avoid shedding people from the Medicaid program because of an inability to submit administrative paperwork.

The process for eligibility renewals will continue to play out over the course of the next year since states have until mid-2024 to update all Medicaid enrollees’ eligibility status. Also notable are some changes made under the purview of the PHE that persist despite the emergency’s conclusion. For example, access to COVID-19 vaccinations and certain COVID-19 treatments generally have not been affected. Some telehealth flexibilities that were allowed under the PHE are also staying in effect, at least until the end of 2024.

Healthcare Workforce Shortages:

Prior to the pandemic, larger demographic trends in society were already impacting the supply of the healthcare workforce. The number of people aging and needing healthcare services was growing while the number of people available to provide care was not keeping pace thus creating a long-term healthcare workforce shortage.

Mid-year Update:The workforce shortage continues. As outlined in a May 23rd Becker’s Hospital Review article, several sources point to a continued shortage. They include a report that says the US could see a deficit of 200,000 to 450,000 registered nurses by 2025. Within the next five years, another report also projects a shortage of more than 3.2 million lower-wage healthcare workers, such as medical assistants, home health aides, and nursing assistants. As a result, some healthcare providers are becoming more creative in their efforts to counteract the workforce shortage: creating alumni networks from which to recruit or providing other benefits to their workforce, such as housing or educational assistance. Policymakers can help counteract the negative impacts of the workforce shortage through a variety of strategies. With the shortage expected to continue, it will be important to enact additional policies that bolster the workforce.

Price Inflation:

As we noted, price inflation was significant in 2022 but was not unique to the health sector.Inflation was particularly exacerbated by the re-opening of the economy after the pandemic, the continued war in Ukraine, and supply chain challenges.

Mid-year Update: Prices for many consumer goods and services increased faster than usual, with overall inflation reaching a four-decade high in mid-2022. The Bureau of Labor Statistics (BLS) reported inflation rates have slowed, with overall prices growing by 6 percent in February 2023 compared to the previous year. Interestingly, prices for medical care increased only 2.3 percent. Similarly, BLS reported that the average price of health care in the United States increased by 0.7 percent in the 12 months ending May 2023, following a previous increase of 1.1 percent. The slower price growth in healthcare compared to other sectors of the economy is highly unusual,[i] and while inflation is not easily influenced by state-level policymakers’ actions alone, the trend is still worth monitoring to better understand the impacts on healthcare access and quality. As of early July, the latest predictions from PwC are that healthcare costs will rise 7% in 2024.

Declining Margins at Hospitals:

Previous analysis by the consulting firm Kaufman Hall predicted that more than half of all hospitals would have negative margins at the end of 2022. As we noted, this was due to such factors as higher-than-normal expenses for staff, supplies, and pharmaceuticals and lower revenues.

Mid-year Update: The latest report from Kaufman Hall offers data that shows a reversal in this trend for the first part of 2023. May was the third consecutive month in which hospital margins were positive after operating in the red for most of 2022. The return to normal is largely driven by revenues that are more in line with pre-pandemic levels. With revenues returning to more normal levels, expenses will be particularly important to watch for the remainder of 2023. If hospital expenses continue to outweigh revenues, policymakers may need to evaluate the financial health of providers and the potential impact that may have on access to services for patients.

Private Equity in Healthcare:

We predicted that private equity (PE) would continue to grow in healthcare, pointing to a PwC consulting report that indicated that PE companies still had plenty of “dry powder,” or money, to invest in 2023.

Mid-year Update:There has been a slowdown in private equity deals over the last year. But it is notable that there were still 200 private equity deals in healthcare in the first quarter of 2023, according to PitchBook’s healthcare services report released in May 2023. While lower than the year before, this is still considered active when compared to pre-pandemic PE dealmaking. Because of the waning of the pandemic and stability returning to the healthcare sector, it is more likely that PE deals stabilize in 2023. And some industry predictions indicate that dealmaking will bounce back further in the second half of 2023. As noted in our previous blog, it will be important to monitor the proliferation of PE in healthcare and determine its impact on healthcare markets, care delivery, innovation, and quality.

Consolidations:

Like many other industries, consolidations of all sorts have been happening in healthcare. The consolidations are both vertical—combining two or more stages of production normally operated by separate companies into one company, such as when hospitals or insurers employ physicians and/or acquire physician practices or other entities like pharmacies—and horizontal—combining organizations that provide the same or similar services, such as hospitals acquiring hospitals.

Mid-year Update: Consolidations of all sorts of healthcare entities continued in 2023 with some of the biggest potential consolidations yet. Those include the proposed merger of two major bi-coastal health system providers: Geisinger, based in Pennsylvania, and Kaiser, based in California. Although the deal must still go through regulatory approval, if completed, the two systems will create a nonprofit that will look to add five or six more systems nationally over the next five years. Other notable consolidations include the finalization of tech-giant Amazon’s purchase of One Medical, a primary care network. And Optum, one of the largest conglomerates that is a subsidiary of United Health Group, increased its net revenue growth by 25% to $54.1 billion in the first quarter of 2023, primarily due to more patients visiting OptumHealth clinics and growth in OptumRx pharmacy scripts processed. Optum’s growth is likely to continue in 2023 as they expect to add another 10,000 physicians. Case in point, in February of this year, Optum paid an undisclosed sum for Crystal Run Healthcare, a network of nearly 400 providers in New York. A goal of consolidation has been better coordination of patient care for improved outcomes and value. Results have been mixed and it is therefore an important trend for policymakers and researchers to monitor and to ensure the impacts are positive.

Alternate Payment Models:

Alternate payment models (APMs) in healthcare have been expanding especially since enactment of the Patient Protection and Affordable Care Act in 2010. They are primarily being developed by the Center for Medicare and Medicaid Innovation (CMMI) which has driven payment policy (including APMs) in the two big government healthcare programs: Medicaid and Medicare. There have been several iterations of APMs—over 50 models—but the one common theme is that all of them generally seek to reward better care.

Mid-year Update: Since the start of 2023, the most notable expansion of the trend toward more alternate payment models was CMMI’s introduction of a new primary care-focused APM called Making Care Primary. In addition to this model, it is expected that the Centers for Medicaid and Medicare Services (CMS), which oversees the operation of these two large public health insurance programs, will introduce more new payment models in 2023, including one that allows states to manage the total cost of care in a given region. This may take various forms, including something akin to Maryland’s global budget, which is used statewide. Since the total cost of care model has yet to be officially revealed, this trend and the emergence of any new developments is worth watching in the second half of 2023. Policymakers can learn from these various payment models and use them to inform the plans implemented in their own state or region in order to improve healthcare.

Attention to Health Equity:

A notable aspect of the pandemic was the disparate impact it had on people of color and other marginalized groups. In response, policymakers and providers began paying more attention to the underlying cause of these disparities. In 2021, President Joe Biden signed an executive order to focus federal resources and attention on reducing health disparities.

Mid-year Update: Increased attention to health equity in healthcare has continued. Ernst and Young, an international consulting group, released its first-ever report on the state of health equity in the United States, which involved a survey of over 500 providers to begin tracking their methods for, and progress in, addressing health disparities. More recently, in June 2023, The Joint Commission on the Accreditation of Healthcare Organizations (JCAHO) announced that it will be adding a certification program for healthcare organizations specifically targeted towards improving health equity. While attention to equity has grown, what will be interesting to watch in the second half of 2023 is the degree to which such efforts are having an impact on actually reducing disparities. Understanding the impacts of various interventions can help policymakers expand efforts that are effective.

Digital TeleHealth Delivery Expansion:

The use of digital health expanded dramatically from 2020 to 2022 as social distancing practices were adopted and telehealth options became more widely available. As noted in our blog series, digital health “includes mobile health (mHealth), health information technology (IT), wearable devices, telehealth and telemedicine, and personalized medicine.” It also includes, “mobile medical apps and software that support the clinical decisions doctors make every day to do artificial intelligence and machine learning.”

Mid-year Update: At the end of 2022 and the start of 2023, the ability to infuse capital to drive the expansion of digital health seemed tenuous, in part due to the collapse of Silicon Valley Bank (SVB). As noted by the publication Pitchbook and CB Insights, venture capital funding in the digital health space totaled $7.5 billion in 2022, a 57 percent year-over-year drop. Although the fast pace of investment in digital health may have slowed since its explosion during the pandemic, the expansion of digital health continues. Our January blog suggested that areas such as behavioral health, care at home, and maternal health were areas to watch. In 2023, digital access is expanding in other areas, such as in-home urgent primary care to allow for the treatment of complex injuries and illnesses with the goal of reducing emergency department visits. And other important digital health deals are still occurring: health tech startup Florence picked up Zipnosis from Bright Health to expand its virtual care capabilities. And with the launch of consumer-facing tech products, such as Chat GPT and Apple Vision Pro in the first half of 2023, additional opportunities for applying such technologies in healthcare may fuel further expansion of digital health. Policies that are developed in the future may want to support the growth of such innovation, while also being mindful to monitor the potential impacts on care.

Expansion of Non-Traditional Providers:

In January, we noted an emergence of companies in healthcare whose genesis was something other than healthcare. The blog pointed to examples of how companies such as Walgreens, CVS, and Amazon were expanding their offerings in healthcare.

Mid-year Update:Non-traditional entities continue to expand in the healthcare space. Notable examples include the recent acquisitions and expansions made by CVS. One of these expansions is being done through its affiliation with the insurance company, Aetna. Through Aetna, CVS has entered the insurance exchange market in four more states in 2023, in addition to the 12 states in which it already operates. CVS also closed a deal in the first half of 2023 to acquire Oak Street Health for over $10 billion. And, in March 2023, CVS announced it had officially acquired Signify Health, a digital telehealth company that enables more care to occur in-home. As noted earlier, Amazon officially completed its deal to acquire OneMedical and United Health Group is working on expanding its use of value-based care through a partnership with Walmart. Monitoring the impact of these emerging companies in healthcare will be important for policymakers that have historically only focused on more traditional providers, such as hospitals. These non-traditional entrants, in many cases, are large organizations with substantial resources and their impact may be just as significant if not greater than traditional providers.

Conclusion

These trends merit close attention in the second half of 2023. As healthcare takes on new shapes, the implications for those in the sector and all who depend on it will be huge. In addition, there are important implications for state and federal policymakers who will need to consider how these trends impact access, affordability, and quality of health care, so they can determine whether and how government might help to accelerate beneficial innovations, invest in promising trends, prevent or reverse harmful trends, and monitor the impacts on consumers.

Mountain View, Calif.-based El Camino Health ended the first quarter with an impressive operating margin of 10.2 percent when many health systems saw their margins hover above zero or fall into the red. The system’s revenue for the quarter totaled $131,290.

For the nine months ended March 31, the two-hospital system posted an operating gain of $141.4 million on revenue of just over $1 billion.

However, like most health systems, El Camino’s expenses are substantially higher than the same period last year, increasing 10.6 percent year over year for the nine months ending March 31, 2023, to $881.9 million.

The system is making a conscious effort to march down labor costs while also placing a significant emphasis on retention. In June, El Camino agreed a deal to increase pay for nurses by 16 percent over three years.

“Like nearly all hospitals, our nursing staff comprises the largest part of our workforce. With the recruitment of a single nurse estimated to be nearly $60,000, our primary strategy to reduce labor costs is to focus on decreasing turnover,” El Camino CEO Dan Woods told Becker’s.

“Our turnover rate for nurses is just about 8 percent while the turnover rate nationally is still running at 22 percent.”

In March, the system also received a credit rating upgrade from Moody’s, which noted the system’s “superlative cash metrics and operating performance.” Fitch Ratings also revised El Camino’s outlook to positive in February, noting that the system has a history of generating double-digit operating EBITDA margins, driven by a solid market position that features strong demographics and a very healthy payer mix.

So far, 2023 is shaping up to be a slightly better year for hospital performance, but it comes on the heels of unprecedented financial difficulties for the sector.

In the graphic above, we evaluated nearly 30 years of historical data from Kaufman Hall and the American Hospital Association to provide a broader perspective on hospital operating margins over time. 2020 and 2022 have been the only years in which a majority of hospitals—53 percent—posted a negative operating margin.

During the most comparable periods of recent economic hardship, the “dot-com bubble burst” of the late 1990s and the 2009 Great Recession, the share of hospitals with negative operating margins amounted to only 42 and 32 percent, respectively.

With this context, hospitals’ current financial distress is more severe than anything we’ve seen in the past three decades.

Healthcare is clearly no longer recession-proof: a four percent operating margin—the level needed for health systems to not only sustain operations but also invest in growth—feels even more elusive as labor costs remain high, surgical care continues to shift to outpatient settings, the second half of the Baby-Boom generation ages into Medicare, and deep-pocketed competitors compete for profitable services.

Here is a summary of recent credit downgrades and outlook revisions for hospitals and health systems.

The downgrades and downward revisions reflect continued operating challenges many nonprofit systems are facing, with multiyear recovery processes expected.

Downgrades:

Yale New Haven (Conn.) Health: Operating weakness and elevated debt contributed to the downgrade of bonds held by Yale New Haven (Conn.) Health, Moody’s said May 5. The bond rating slipped from “Aa3” to “A1,” and the outlook was revised to stable from negative.

The system saw a second downgrade as its default rating and that on a series of bonds were revised one notch to “A+” from “AA-” amid continued operating woes, Fitch said June 28.

Not only have there been three straight years of such challenges, but the operating environment continues to cast a pall into the second quarter of the current fiscal year, Fitch said.

UC Health (Cincinnati): The system was downgraded on a series of bonds, Moody’s said May 10.

The move, which involved a lowering from a “Baa2” to “Baa3” grade, refers to such bonds with an overall value of $580 million.

In February, UC Health suffered a similar downgrade from “A” to “BBB+” on its overall rating and on some bonds because of what S&P Global termed “significantly escalating losses.”

UNC Southeastern (Lumberton, N.C.): The system, which is now part of the Chapel Hill, N.C.-based UNC Health network, saw its ratings on a series of bonds downgraded to “BB” amid operating losses and sustained weakness in its balance sheet, S&P Global said June 23.

While UNC Southeastern reported an operating loss of $74.8 million in fiscal 2022, such losses have continued into fiscal 2023 with a $15 million loss as of March 31, S&P Global said. The system had earlier been placed on CreditWatch but that was removed with this downgrade.

Butler (Pa.) Health: The system, now merged with Greensburg, Pa.-based Excela Health to form Independence Health System, saw its credit rating downgraded significantly, falling from “A” to “BBB.”

The move reflects continued operating challenges and low patient volumes, Fitch said June 26.

Such operating challenges, including low days of cash on hand, could result in potential default of debt covenants, Fitch warned.

Outlook revisions:

Redeemer Health (Meadowbrook, Pa.): The system had its outlook revised to negative amid “persistent operating losses,” Fitch Ratings said June 14. The health system, anchored by a 260-bed acute care hospital, reported a $37 million operating loss in the nine months ending March 31, Fitch said.

Thomas Jefferson University (Philadelphia): The June 9 downward revision of its outlook, which includes both the health system and the university’s academic sector, was due to sustained operating weakness, S&P Global said.

IU Health (Indianapolis): While it saw ratings affirmed at “AA,” the 16-hospital system had its outlook downgraded amid persistent inflationary pressures and large capital expense, Fitch said May 31.

UofL Health (Louisville, Ky.): Slumping operating income and low days of cash on hand (42.8 as of March 31) contributed to S&P Global revising its outlook for the six-hospital system to negative May 24.

Here are 45 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings, Moody’s Investors Service and S&P Global in 2023.

Note: This is not an exhaustive list. Health system names were compiled from credit rating reports.

1. AdventHealth has an “AA” rating and stable outlook with Fitch. The rating reflects the Altamonte Springs, Fla.-based system’s strong financial profile, characterized by still-adequate liquidity and moderate leverage, typically strong and highly predictable profitability, Fitch said.

2. AnMed Health has an “AA-” rating and stable outlook with Fitch. The Anderson, S.C.-based system has maintained strong performance through the COVID-19 pandemic and current labor market pressures, Fitch said.

3. Atrium Health has an “AA-” and stable outlook with S&P Global. The Charlotte, N.C.-based system’s rating reflects a robust financial profile, growing geographic diversity and expectations that management will continue to deploy capital with discipline.

4. Banner Health has an “AA-” and stable outlook with Fitch. The Phoenix-based system’s rating highlights the strength of its core hospital delivery system and growth of its insurance division, Fitch said.

5. BayCare Health System has an “AA” rating and stable outlook with Fitch. The Tampa, Fla.-based system’s rating reflects its excellent financial profile supported by its leading market position in a four-county area and the ability to sustain a solid operating outlook in the face of inflationary sector headwinds, Fitch said.

6. Beacon Health System has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of the South Bend, Ind.-based system’s balance sheet, the rating agency said.

7. Berkshire Health has an “AA-” rating and stable outlook with Fitch. The Pittsfield, Mass.-based system has a strong financial profile, solid liquidity and modest leverage, according to Fitch.

8. Cape Cod Healthcare has an “AA-” and stable outlook with Fitch. The Hyannis, Mass.-based system’s rating reflects a dominant market position in its service area and historically solid operating results, the rating agency said.

9. Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area, Fitch said.

10.CaroMont Health has an “AA-” rating and stable outlook with S&P Global. The Gastonia, N.C.-based system has a healthy financial profile and robust market share in a competitive region.

11. CentraCare has an “AA-” rating and stable outlook with Fitch. The St. Cloud, Minn.-based system has a leading market position, and its management’s focus on addressing workforce pressures, patient access and capacity constraints will improve operating margins over the medium term, Fitch said.

12. Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The Minneapolis-based system’s broad reach within the region continues to support long-term sustainability as a market leader and preferred provider for children’s health care, Fitch said.

13. Concord (N.H.) Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of Concord’s leverage and liquidity assessment and Fitch’s assessment that two recently acquired hospitals will be strategically and financially accretive.

14. Cone Health has an “AA” rating and stable outlook with Fitch. The rating reflects the expectation that the Greensboro, N.C.-based system will gradually return to stronger results in the medium term, the rating agency said.

15. Cottage Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Santa Barbara, Calif.-based system’s leading market position and broad reach in a service area that exhibits modest population growth but consistently high demand for acute care services, Fitch said.

16. El Camino Health has an “AA-” rating and stable outlook with Fitch. The Mountain View, Calif.-based system has a history of generating double-digit operating EBITDA margins, driven by a solid market position that features strong demographics and a very healthy payer mix, Fitch said.

17. Froedtert Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s maintenance of a strong, albeit compressed, operating performance and a robust liquidity position, Fitch said.

18. Hackensack Meridian Health has an “AA-” rating and stable outlook with Fitch. The Edison, N.J.-based system’s rating is supported by its strong presence in its large and demographically favorable market, Fitch said.

19. Harris Health System has an “AA” rating and stable outlook with Fitch. The Houston-based system has a “very strong” revenue defensibility, primarily based on the district’s significant taxing margin that provides support for operations and debt service, Fitch said.

20. Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by a leading market position in its immediate area and very strong financial profile, Fitch said.

21. IU Health has an “AA” rating and stable outlook with Fitch. The Indianapolis-based system has a long track record of strong operating margins and an overall credit profile that is supported by a strong balance sheet, the rating agency said.

22. Inspira Health has an “AA-” rating and stable outlook with Fitch. The Mullica Hill, N.J.-based system’s rating reflects its leading market position in a stable service area and a large medical staff supported by a growing residency program, Fitch said.

23. Lucile Packard Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the Palo Alto, Calif.-based hospital’s role as a nationally known, leading children’s hospital, Fitch said. It also benefits from resilient clinical volumes and a solid market position, as well as its relationship with Stanford University and Stanford Health Care.

24. Kaiser Permanente has an “AA-” and stable outlook with Fitch. The Oakland, Calif.-based system’s rating is driven by a strong financial profile, which is maintained despite a challenging operating environment in fiscal year 2022.

25. Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The Rochester, Minn.-based system’s credit profile characterized by its excellent reputations for clinical services, research and education, Moody’s said.

26. McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The Grand Blanc, Mich.-based system has a leading market position over a broad service area covering much of Michigan and a track-record of profitability despite sector-wide market challenges in recent years, Fitch said.

27. MemorialCare has an “AA-” rating and stable outlook with Fitch. The rating reflects the Fountain Valley, Calif.-based system’s strong financial profile and excellent leverage metrics despite its weaker operating performance, Fitch said.

28. Memorial Sloan-Kettering Cancer Center has an “AA” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the New York City-based system’s national and international reputation as a premier cancer hospital will continue to support growth in its leading and increasing market share for its specialty services.

29. Midland (Texas) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Midland’s exceptional market position and limited competition for acute-care services and growing outpatient services, Fitch said.

30. Munson Healthcare has an “AA” rating and stable outlook with Fitch. The rating reflects the strength of the Traverse City, Mich.-based system’s market position and its leverage and liquidity profiles.

31. North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The Tupelo-based system’s rating reflects its very strong cash position and strong market position, Fitch said.

32. Novant Health has an “AA-” rating and stable outlook with Fitch. The Winston-Salem, N.C.-based system has a highly competitive market share in three separate North Carolina markets, Fitch said, including a leading position in Winston-Salem (46.8 percent) and second only to Atrium Health in the Charlotte area.

33. NYC Health + Hospitals has an “AA-” rating with Fitch. The New York City system is the largest municipal health system in the country, serving more than 1 million New Yorkers annually in more than 70 patient locations across the city, including 11 hospitals, and employs more than 43,000 people.

34. Orlando (Fla.) Health has an “AA-” and stable outlook with Fitch. The system’s upgrade from “A+” reflects the continued strength of the health system’s operating performance, growth in unrestricted liquidity and excellent market position in a demographically favorable market, Fitch said.

35. The Queen’s Health System has an “AA” rating and stable outlook with Fitch. The Honolulu-based system’s rating reflects its leading state-wide market position, historically strong operating performance and diverse revenue streams, the rating agency said.

36. Rush System for Health has an “AA-” and stable outlook with Fitch. The Chicago-based system has a strong financial profile despite ongoing labor issues and inflationary pressures, Fitch said.

37. Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The Cape Girardeau, Mo.-based system enjoys robust operational performance and a strong local market share as well as manageable capital plans, Fitch said.

38. Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The system has a “very strong” financial profile and a leading market share position, Fitch said.

39. Stanford Health Care has an “AA” rating and stable outlook with Fitch. The Palo Alto, Calif.-based system’s rating is supported by its extensive clinical reach in the greater San Francisco and Central Valley regions and nationwide/worldwide destination position for extremely high-acuity services, Fitch said.

40. SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system has a strong financial profile, multi-state presence and scale, with solid revenue diversity, Fitch said.

41. St. Clair Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Pittsburgh-based system’s strong financial profile assessment, solid market position and historically strong operating performance, the rating agency said.

42. UCHealth has an “AA” rating and stable outlook with Fitch. The Aurora, Colo.-based system’s margins are expected to remain robust, and the operating risk assessment remains strong, Fitch said.

43. University of Kansas Health System has an “AA-” rating and stable outlook with S&P Global. The Kansas City-based system has a solid market presence, good financial profile and solid management team, though some balance sheet figures remain relatively weak to peers, the rating agency said.

44. WellSpan Health has an “Aa3” rating and stable outlook with Moody’s. The York, Pa.-based system has a distinctly leading market position across several contiguous counties in central Pennsylvania, and management’s financial stewardship and savings initiatives will continue to support sound operating cash flow margins when compared to peers, Moody’s said.

45. Willis-Knighton Health System has an “AA-” rating and stable outlook with Fitch. The Shreveport, La.-based system has a “dominant inpatient market position” and is well positioned to manage operating pressures, Fitch said.

A number of hospitals and health systems are trimming their workforces or jobs due to financial and operational challenges.

Below are workforce reduction efforts or job eliminations that were announced within the past year and/or take effect later in 2023.

Editor’s Note: This webpage was updated June 30 and will continue to be updated.

1. Coral Gables-based Baptist Health South Florida is offering its executives at the director level and above a “one-time opportunity” to apply for voluntary separation, according to a June 29 Miami Herald report. Decisions on buyout applications will be made during the summer.

2. MultiCare Health System, a 12-hospital organization based in Tacoma, Wash., will lay off 229 employees, or about 1 percent of its 23,000 staff members, including about two dozen leaders, as part of cost-cutting efforts, the health system said June 29. The layoffs primarily affect support departments, such as marketing, IT and finance.

3. Greensburg, Pa.-based Independence Health System laid off 53 employees and has cut 226 positions — including resignations, retirements and elimination of vacant positions — since January, The Butler Eagle reported June 28. The 226 reductions began at the executive level, with 13 manager positions terminated in March.

4. Billings (Mont.) Clinic will lay off workers as part of a restructuring plan to address financial and operational headwinds in today’s healthcare environment, the organization confirmed. The layoffs are expected to affect approximately 27 or fewer positions.

5. Melbourne, Fla.-based Health First is eliminating some positions and leaving open ones vacant, Florida Today reported June 21. Seventeen jobs will be cut and 36 will be left unfilled, according to Paula Just, the health system’s chief experience officer.

6. Pittsburgh-based Highmark Health laid off 118 employees on June 21, including two from Allegheny Health Network, a spokesperson for the health system told Becker’s. The layoffs follow the health system’s cutbacks in March and April, according to the Pittsburgh Business Times. Highmark laid off 141 workers earlier this year.

7. Vibra Hospital of Western Massachusetts, a long-term-acute care hospital in Springfield, will lay off 87 employees by Aug. 15 ahead of the facility’s planned closure. About 30 patients will be relocated to Baystate Health’s Valley Springs Behavioral Health Hospital in Holyoke, Mass., which will open in August.

8. Cortez, Colo.-based Southwest Memorial Hospital laid off nine people to help ensure the hospital is staffed appropriately, and create financial stability for the future, a spokesperson confirmed to Becker’s. The spokesperson, Chuck Krupa, said the layoffs occurred June 14 and included administrative workers. No bedside care positions were affected.

9. Henry Mayo Newhall Hospital in Valencia, Calif., is making “a little over 100” layoffs amid financial challenges, spokesperson Patrick Moody confirmed to Becker’s. Mr. Moody said the layoffs affect workers “in a wide range of hospital departments.” This includes some management-level employees. The hospital, which has about 1,800 employees total, is not providing specific numbers for specific job titles or departments.

10. Dartmouth Health is laying off 75 workers and eliminating 100 job vacancies. The layoffs came after the Lebanon, N.H.-based health system implemented a performance improvement plan in November.

11. Seattle Children’s is eliminating 135 leader roles, citing financial challenges. The management restructuring and reduction affects 1.5 percent of employees across the organization.

12. White Rock (Texas) Medical Center laid off 30 workers across 28 departments. The layoffs include clinical and administrative roles.

13. Jackson, Miss.-based St. Dominic Health Services is laying off 157 workers and ending behavioral health services. The reduction represents 5.5 percent of the hospital’s workforce.

14. Danville, Pa.-based Geisinger laid off 47 employees from its IT department. The reduction is part of a restructuring plan to offset high labor and supply costs.

15. Cascade Behavioral Health Hospital in Tukwila, Wash., is winding down operations and laying off 288 employees. The 137-bed psychiatric facility is slated to close by July 31.

16. Cambridge (Mass.) Health Alliance is laying off 69 employees, reducing the hours of 15 others and eliminating 170 open positions, according to The Boston Globe. The reductions are primarily in management, administrative and support areas, a health system spokesperson told Becker’s.

17. Wenatchee, Wash.-based Confluence Health has eliminated its chief operating officer amid restructuring efforts and financial pressures, the health system confirmed to Becker’s May 16.

18. Conemaugh Memorial Medical Center, a Duke LifePoint hospital in Johnstown, Pa., has laid off less than 1 percent of its workforce, the hospital confirmed to Becker’s May 15.

19. Community Health Network, a nonprofit health system based in Indianapolis, plans to cut an unspecified number of jobs as it restructures its workforce and makes organizational changes. The health system confirmed the job cuts in a statement shared with Becker’s on May 11. It did not say how many jobs would be cut or which positions would be affected.

20. New Orleans-based Ochsner Health eliminated 770 positions, or about 2 percent of its workforce, on May 11. This is the largest layoff to date for the health system.

21. Cedars-Sinai Medical Center eliminated the positions of 131 employees and cut about two dozen other jobs at related Cedars-Sinai facilities, a spokesperson confirmed via a statement shared with Becker’s May 7. The Los Angeles-based organization said reductions represent less than 1 percent of the workforce and apply to management and non-management roles primarily in non-patient care jobs.

22. Rochester (N.Y.) Regional Health is eliminating about 60 positions. A statement from RRH said the changes affect less than one-half percent of the system population, mostly in nonclinical and management positions.

23. Memorial Health System laid off fewer than 90 people, or less than 2 percent of its workforce.The Gulfport, Miss.-based health system said May 2 that most of the affected positions are nonclinical or management roles, and the majority do not involve direct patient care.

24. Monument Health laid off at least 80 employees, or about 2 percent of its workforce. The Rapid City, S.D.-based system said positions are primarily corporate service roles and will not affect patient services. Unfilled corporate service positions were also eliminated.

25. Habersham Medical Center in Demorest, Ga., laid off four executives. The layoffs are part of cost-cutting measures before the hospital joins Gainesville-based Northeast Georgia Health System in July, nowhaberbasham.com reported April 27.

26. Scripps Health is eliminating 70 administrative roles, according to WARN documents filed by the San Diego-based health system in March. The layoffs take effect May 8 and affect corporate positions in San Diego and La Jolla, Calif.

27. Trinity Health Mid-Atlantic, part of Livonia, Mich.-based Trinity Health, eliminated fewer than 40 positions, a spokesperson confirmed to Becker’s April 24. The layoffs represent 0.5 percent of the health system’s approximately 7,000-person workforce.

28. PeaceHealth eliminated 251 caregiver roles across multiple locations. The Vancouver, Wash.-based health system said affected roles include 121 from Shared Services, which supports its 16,000 caregivers in Washington, Oregon and Alaska.

29. Toledo, Ohio-based ProMedica plans to lay off 26 skilled nursing support staff. The layoffs, effective in June, affect 20 employees who work remotely across the U.S, and six who work at the ProMedica Summit Center in Toledo, according to a Worker Adjustment and Retraining Notification filed April 18. Most affected positions support sales, marketing and administrative functions for the skilled nursing facilities, Promecia told Becker’s.

30. Northern Inyo Healthcare District, which operates a 25-bed critical access hospital in Bishop, Calif., anticipates eliminating about 15 positions, or less than 4 percent of its 460-member workforce, by April 21, a spokesperson confirmed to Becker’s. The layoffs include nonclinical roles within support and administration, according to a news release. No further details were provided about specific positions affected.

31. West Reading, Pa.-based Tower Health is eliminating 100 full-time equivalent positions. The move will affect 45 individuals, according to an April 13 news release the health system shared with Becker’s. The other 55 positions are either recently vacated or involve individuals who plan to retire in the coming weeks and months.

32. Grand Forks, N.D.-based Altru Health is trimming its executive team as its new hospital project moves forward. The health system is trimming its executive team from nine to six and incentivizing 34 other employees to take early retirement.

33. Tacoma, Wash.-based Virginia Mason Franciscan Health laid off nearly 400 employees, most of whom are in non-patient-facing roles. The job cuts affected less than 2 percent of the health system’s 19,000-plus workforce.

34. Katherine Shaw Bethea Hospital in Dixon, Ill., will lay off 20 employees, citing financial headwinds affecting health organizations across the U.S. It will also leave other positions unfilled to reduce expenses amid rising labor and supply costs and reductions in payments by insurance plans. Affected employees largely work in administrative support areas and not direct patient care.

35. Danbury, Conn.-based Nuvance Health will close a 100-bed rehabilitation facility in Rhinebeck, N.Y., resulting in 102 layoffs. The layoffs are effective April 12, according to the Daily Freeman.

36. Charleston, S.C.-based MUSC Health University Medical Center laid off an unspecified number of employees from its Midlands hospitals in the Columbia, S.C. area. Division President Terry Gunn also resigned after the facilities missed budget expectations by $40 million in the first six months of the fiscal year, The Post and Courier reported March 30.

37. Winston-Salem, N.C.-based Novant Health laid off about 50 workers, including C-level executives, the health system confirmed to Becker’s March 29. The layoffs affected Jesse Cureton, the health system’s executive vice president and chief consumer officer since 2013; Angela Yochem, its executive vice president and chief transformation and digital officer since 2020; and Paula Dean Kranz, vice president of innovation enablement and executive director of the Novant Health Innovation Labs.

38. Penn Medicine Lancaster (Pa.) General Health eliminated fewer than 65 jobs, or less than 1 percent of its workforce of about 9,700, the health system confirmed to Becker’s March 30. The layoffs include support, administrative and executive roles, and COVID-19-related support staff, spokesperson John Lines said, according to lancasteronline.com. Mr. Lines did not provide a specific number of affected workers.

39. McLaren St. Luke’s Hospital in Maumee, Ohio, will lay off 743 workers, including 239 registered nurses, when it permanently closes this spring. Other affected roles include physical therapists, radiology technicians, respiratory therapists, pharmacists and pharmacy support staff, and nursing assistants. The hospital’s COO is also affected, and a spokesperson for McLaren Health Care told Becker’s other senior leadership roles are also affected.

40. Bellevue, Wash.-based Overlake Medical Center and Clinics laid off administrative staff, the health system confirmed to the Puget Sound Business Journal. The layoffs, which occurred earlier this year, included 30 workers across Overlake’s human resources, information technology and finance departments, a spokesperson said, according to the publication. This represents about 6 percent of the organization’s administrative workforce. Overlake’s website says it employs more than 3,000 people total.

41. Columbia-based University of Missouri Health Care is eliminating five hospital leadership positions across the organization, spokesperson Eric Maze confirmed to Becker’s March 20. Mr. Maze did not specify which roles are being eliminated saying that the organization won’t address individual personnel actions. According to MU Health Care, the move is a result of restructuring “to better support patients and the future healthcare needs of Missourians.”

42. Greensboro, N.C.-based Cone Health eliminated 68 senior-level jobs. The job eliminations occurred Feb. 21, Cone Health COO Mandy Eaton told The Alamance News. Of the 68 positions eliminated, 21 were filled. Affected employees were offered severance packages.

43. The newly merged Greensburg, Pa.-based organization made up of Excela Health and Butler Health System eliminated 13 filled managerial jobs. The affected employees and positions are from across both sides of the new organization, Tom Chakurda, spokesperson for the Excela-Butler enterprise, confirmed to Becker’s. The positions were in various support functions unrelated to direct patient care.

44. Crozer Health, a four-hospital system based in Upland, Pa., is laying off roughly 215 employees amid financial challenges. The system announced the layoffs March 15 as part of its “operational restructuring plan” that “focuses on removing duplication in administrative oversight and discontinuing underutilized services.” Affected employees represent about 4 percent of the organization’s workforce.

45. Philadelphia-based Penn Medicine is eliminating administrative positions. The change is part of a reorganization plan to save the health system $40 million annually, the Philadelphia Business Journal reported March 13. Kevin Mahoney, CEO of the University of Pennsylvania Health System, told Penn Medicine’s 49,000 employees last week that changes include the elimination of a “small number of administrative positions which no longer align with our key objectives,” according to the publication. The memo did not indicate the exact number of positions that were eliminated.

46. Sovah Health, part of Brentwood, Tenn.-based Lifepoint Health, eliminated the COO positions at its Danville and Martinsville, Va., campuses. The responsibilities of both COO roles will now be spread across members of the existing administrative team.

47. Valley Health, a six-hospital health system based in Winchester, Va., eliminated 31 administrative positions. The job cuts are part of the consolidation of the organization’s leadership team and administrative roles.

48. Marshfield (Wis.) Clinic Health System said it would lay off 346 employees, representing less than 3 percent of its employee base.

50. Roseville, Calif.-based Adventist Health plans to go from seven networks of care to five systemwide to reduce costs and strengthen operations. The reorganization will result in job cuts, including reducing administration by more than $100 million.

51. Arcata, Calif.-based Mad River Community Hospital is cutting 27 jobs as it suspends home health services.

52. Hutchinson (Kan.) Regional Medical Center laid off 85 employees, a move tied to challenges in today’s healthcare environment.

53. Oklahoma City-based OU Health eliminated about 100 positions as part of an organizational redesign to complete the integration from its 2021 merger.

54. Memorial Sloan Kettering Cancer Center announced it would lay off to reduce costs amid widespread hospital financial challenges. The layoffs are spread across 14 sites in New York City, and equate to about 1.8 percent of Memorial Sloan’s 22,500 workforce.

55. St. Louis-based Ascension completed layoffs in Texas, the health system confirmed in January. A statement shared with Becker’s says the layoffs primarily affected nonclinical support roles. The health system declined to specify to Becker’s the number of employees or positions affected.

57. Chillicothe, Ohio-based Adena Health System announced it would eliminate 69 positions — 1.6 percent of its workforce — and send 340 revenue cycle department employees to Ensemble Health Partners’ payroll in a move aimed to help the health system’s financial stability.

58. Ascension St. Vincent’s Riverside in Jacksonville, Fla., will end maternity care at the hospital, affecting 68 jobs, according to a Workforce Adjustment and Retraining Notification filed with the state Jan. 17. The move will affect 62 registered nurses as well as six other positions.

59. Visalia, Calif.-based Kaweah Health said it aimed to eliminate 94 positions as part of a new strategy to reduce labor costs. The job cuts come in addition to previously announced workforce reductions; the health system already eliminated 90 unfilled positions and lowered its workforce by 106 employees.

60. Oklahoma City-based Integris Health said it would eliminate 200 jobs to curb expenses. The eliminations include 140 caregiver roles and 60 vacant jobs.

61. Toledo, Ohio-based ProMedica announced plans to lay off 262 employees, a move tied to its exit from a skilled-nursing facility joint venture late last year. The layoffs will take effect between March 10 and April 1.

62. Employees at Las Vegas-based Desert Springs Hospital Medical Center were notified of layoffs coming to the facility, which will transition to a freestanding emergency department. There are 970 employees affected. Desert Springs is part of the Valley Health System, a system owned and operated by King of Prussia, Pa.-based Universal Health Services.

63. Philadelphia-based Jefferson Health plans to go from five divisions to three in an effort to flatten management and become more efficient. The reorganization will result in an unspecified number of job cuts, primarily among executives.

64. Pikeville (Ky.) Medical Center said it would lay off 112 employees as it outsources its environmental services department. The 112 layoffs were effective Jan. 1, 2023.

65. Southern Illinois Healthcare, a four-hospital system based in Carbondale, announced it would eliminate or restructure 76 jobs in management and leadership. The 76 positions fall under senior leadership, management and corporate services. Included in that figure are 33 vacant positions, which will not be filled. No positions in patient care are affected.

66. Citing a need to further reduce overhead expenses and support additional investments in patient care and wages, Traverse City, Mich.-based Munson Health said it would eliminate 31 positions and leave another 20 jobs unfilled. All affected positions are in corporate services or management. The layoffs represent less than 1 percent of the health system’s workforce of nearly 8,000.

67. West Reading, Pa.-based Tower Health on Nov. 16 laid off 52 corporate employees as the health system shrinks from six hospitals to four. The layoffs, which are expected to save $15 million a year, account for 13 percent of Tower Health’s corporate management staff.

68. Sioux Falls, S.D.-based Sanford Health announced layoffs affecting an undisclosed number of staff in October, a decision its CEO said was made “to streamline leadership structure and simplify operations” in certain areas. The layoffs primarily affect nonclinical areas.

69. St. Vincent Charity Medical Center in Cleveland closed its inpatient and emergency room care Nov. 11, four days before originally planned — and laid off 978 workers in doing so. After the transition, the Sisters of Charity Health System will offer outpatient behavioral health, urgent care and primary care.

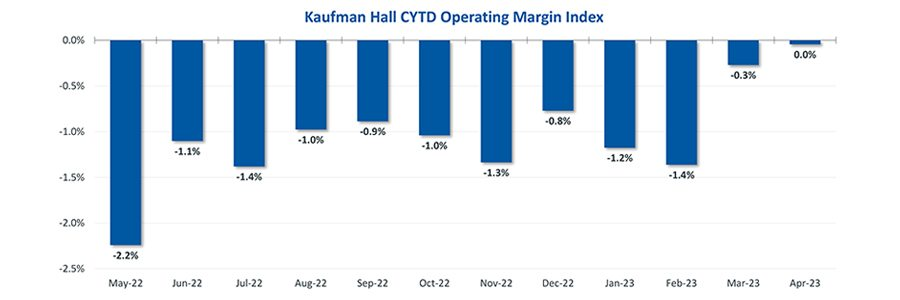

Hospital finances showed signs of stabilizing in May amid slightly improving operating margins, declining expenses and notable increases in outpatient visits.

The median Kaufman Hall Year-To-Date Operating Margin Index reflecting actual margins was 0.3% in May.

The National Hospital Flash Report uses both actual and budget data over the last three years, sampled from more than 900 hospitals on a recurring monthly basis from Syntellis Performance Solutions.

The sample of hospitals for this report is representative of all hospitals in the United States both geographically and by bed size. Additionally, hospitals of all types are represented, from large academic to small critical access. Advanced statistical techniques are used to standardize data, identify and handle outliers, and ensure statistical soundness prior to inclusion in the report.

While this report presents data in the aggregate, Syntellis Performance Solutions also has real-time data down to individual department, jobcode, paytype, and account levels, which can be customized into peer groups for unparalleled comparisons to drive operational decisions and performance improvement initiatives.

Key Takeaways

Hospitals broke even in April. The median operating margin for hospitals was 0% in April, leaving most hospitals with little to no financial wiggle room.

Volumes dropped while lengths of stay increased. Hospital volumes dropped across the board—including inpatient and outpatient. Emergency department volumes were the least affected.

Effects of Medicaid disenrollment could be materializing. Hospitals experienced increases in bad debt and charity care in April. Combined with anemic patient volumes, experts note this data could illustrate the effects of the start of widespread disenrollment from Medicaid following the end of the COVID-19 public health emergency.

Inflation continued to throttle hospital finances. Labor costs jumped in April and the costs of goods and services continued to be well above pre-pandemic levels. Though expenses generally fell in April, revenues declined at a faster rate.

National Non-Operating Results

Key Observations

At their May meeting, the Federal Open Market Committee (FOMC) raised the benchmark borrowing rate another 25 basis points, setting the range to 5.00-5.25% and marking the 10th consecutive hike in the cycle as well as a 16-year high

Fed officials acknowledged discussion of a potential pause in tightening while leaving wiggle room, saying “rates are going to come down” over a long period of time while also warning inflation “continues to run high” and the Fed will be taking a “data-dependent approach”

The consumer price index (CPI) rose 0.4% in April, a 4.9% increase year-over-year, an annual pace of inflation below 5% for the first time in two years

The labor market continued to show resilience in April as U.S. nonfarm payrolls grew by 253,000 and unemployment fell back to a 53-year low of 3.4%

Strong inflation, a robust labor market, continued banking sector woes, and a debt ceiling standoff further complicates credit conditions and may challenge the Fed to stabilize financial markets

Equities in April, as measured by the S&P 500, were up 1.5% in April and 8.6% YTD despite downbeat economic data, reoccurring banking sector fears, and mixed earnings

On October 1, 1908, Ford produced the first Model T automobile. More than 60 years later, this affordable, mass produced, gasoline-powered car was still the top-selling automobile of all time. The Model T was geared to the broadest possible market, produced with the most efficient methods, and used the most modern technology—core elements of Ford’s business strategy and corporate DNA.

On April 25, 2018, almost 100 years later, Ford announced that it would stop making all U.S. internal-combustion sedans except the Mustang.

The world had changed. The Taurus, Fusion, and Fiesta were hardly exciting the imaginations of car-buyers. Ford no longer produced its U.S. cars efficiently enough to return a suitable profit. And the internal combustion technology was far from modern, with electronic vehicles widely seen as the future of automobiles.

Ford’s core strategy, and many of its accompanying products, had aged out. But not all was doom and gloom; Ford was doing big and profitable business in its line of pickups, SUVs, and -utility vehicles, led by the popular F-150.

It’s hard to imagine the level of strategic soul-searching and cultural angst that went into making the decision to stop producing the cars that had been the basis of Ford’s history. Yet, change was necessary for survival. At the time, Ford’s then-CEO Jim Hackett said, “We’re going to feed the healthy parts of our business and deal decisively with the areas that destroy value.”

So Ford took several bold steps designed to update—and in many ways upend—its strategy. The company got rid of large chunks of the portfolio that would not be relevant going forward, particularly internal combustion sedans. Ford also reorganized the company into separate divisions for electric and internal combustion vehicles. And Ford pivoted to the future by electrifying its fleet.

Ford did not fully abandon its existing strategies. Rather, it took what was relevant and successful, and added that to the future-focused pivot, placing the F-150 as the lead vehicle in its new electric fleet.

This need for strategic change happens to all large organizations. All organizations, including America’s hospitals and health systems, need to confront the fact that no strategic plan lasts forever.

Over the past 25-30 years, America’s hospitals and health systems based their strategies on the provision of a high-quality clinical care, largely in inpatient settings. Over time, physicians and clinics were brought into the fold to strengthen referral channels, but the strategic focus remained on driving volume to higher-acuity services.

More recently, the longstanding traditional patient-physician-referral relationship began to change. A smarter, internet-savvy, and self-interested patient population was looking for different aspects of service in different situations. In some cases, patients’ priority was convenience. In other cases, their priority was affordability. In other cases, patients began going to great lengths to find the best doctors for high-end care regardless of geographic location. In other cases, patients wanted care as close as their phone.

Around the country, hospitals and health systems have seen these environmental changes and adjusted their strategies, but for the most part only incrementally. The strategic focus remains centered on clinical quality delivered on campus, while convenience, access, value, affordability, efficiency, and many virtual innovations remain on the strategic periphery.

Health system leaders need to ask themselves whether their long-time, traditional strategy is beginning to age out. And if so, what is the “Ford strategy” for America’s health systems?

The questions asked and answered by Ford in the past five years are highly relevant to health system strategic planning at a time of changing demand, economic and clinical uncertainty, and rapid innovation. For example, as you view your organization in its entirety, what must be preserved from the existing structure and operations, and what operations, costs, and strategies must leave? And which competencies and capabilities must be woven into a going-forward structure?

America’s hospitals and health systems have an extremely long history—in some cases, longer than Ford’s. With that history comes a natural tendency to stick with deeply entrenched strategies. Now is the time for health systems to ask themselves, what is our Ford F150? And how do we “electrify” our strategic plan going forward?

A couple of months ago, I got a call from a CEO of a regional health system—a long-time client and one of the smartest and most committed executives I know. This health system lost tens of millions of dollars in fiscal year 2022 and the CEO told me that he had come to the conclusion that he could not solve a problem of this magnitude with the usual and traditional solutions. Pushing the pre-Covid managerial buttons was just not getting the job done.

This organization is fiercely independent. It has been very successful in almost every respect for many years. It has had an effective and stable board and management team over the past 30 to 40 years.

But when the CEO looked at the current situation—economic, social, financial, operational, clinical—he saw that everything has changed and he knew that his healthcare organization needed to change as well. The system would not be able to return to profitability just by doing the same things it would have done five years or 10 years ago. Instead of looking at a small number of factors and making incremental improvements, he wanted to look across the total enterprise all at once. And to look at all aspects of the enterprise with an eye toward organizational renovation.

I said, “So, you want a makeover.”

The CEO is right. In an environment unlike anything any of us have experienced, and in an industry of complex interdependencies, the only way to get back to financial equilibrium is to take a comprehensive, holistic view of our organizations and environments, and to be open to an outcome in which we do things very differently.

In other words, a makeover.

Consider just a few areas that the hospital makeover could and should address:

There’s the REVENUE SIDE: Getting paid for what you are doing and the severity of the patient you are treating—which requires a focus on clinical documentation improvement and core revenue cycle delivery—and looking for any material revenue diversification opportunities.

There is the relationship with payers: Involving a mix of growth, disruption, and optimization strategies to increase payments, grow share of wallet, or develop new revenue streams.

There’s the EXPENSE SIDE: Optimizing workforce performance, focusing on care management and patient throughput, rethinking the shared services infrastructure, and realizing opportunities for savings in administrative services, purchased services, and the supply chain. While these have been historic areas of focus, organizations must move from an episodic to a constant, ongoing approach.

There’s the BALANCE SHEET: Establishing a parallel balance sheet strategy that will create the bridge across the operational makeover by reconfiguring invested assets and capital structure, repositioning the real estate portfolio, and optimizing liquidity management and treasury operations.

There is NETWORK REDESIGN: Ensuring that the services offered across the network are delivered efficiently and that each market and asset is optimized; reducing redundancy, increasing quality, and improving financial performance.

There is a whole concept around PORTFOLIO OPTIMIZATION: Developing a deep understanding of how the various components of your business perform, and how to optimize, scale back, or partner to drive further value and operational performance.

Incrementalism is a long-held business approach in healthcare, and for good reason. Any prominent change has the potential to affect the health of communities and those changes must be considered carefully to ensure that any outcome of those changes is a positive one. Any ill-considered action could have unintended consequences for any of a hospital’s many constituencies.

But today, incrementalism is both unrealistic and insufficient.

Just for starters, healthcare executive teams must recognize that back-office expenses are having a significant and negative impact on the ability of hospitals to make a sufficient operating margin. And also, healthcare executive teams must further realize that the old concept of “all things to all people” is literally bringing parts of the hospital industry toward bankruptcy.

As I described in a previous blog post, healthcare comprises some of the most wicked problems in our society—problems that are complex, that have no clear solution, and for which a solution intended to fix one aspect of a problem may well make other aspects worse.

The very nature of wicked problems argues for the kind of comprehensive approach that the CEO of this organization is taking—not tackling one issue at a time in linear fashion but making a sophisticated assessment of multiple solutions and studying their potential interdependencies, interactions, and intertwined effects.

My colleague Eric Jordahl has noted that “reverting to a 2019 world is not going to happen, which means that restructuring is the only option. . . . Where we are is not sustainable and waiting for a reversion is a rapidly decaying option.”

The very nature of the socioeconomic environment makes doing nothing or taking an incremental approach untenable. It is clearly beyond time for the hospital industry makeover.