Published last week in the Wall Street Journal, this piece predicts that the era of immense profitability for Medicare Advantage (MA) insurers may be drawing to a close.

MA has experienced rapid growth over the past decade, due both to the pace of Baby Boomers aging into Medicare, and the increasing numbers of beneficiaries choosing MA plans. In 2023, MA surpassed 50 percent of total Medicare enrollment.

Payers readily embraced the MA market because they found they could earn gross margins two to three times higher than from a commercial life.

However, as the rate of enrollment growth begins to slow (the last of the Boomers will turn 65 in 2030), competition between payers increases, and government payments become less generous, the MA business—while still profitable—is poised to become less of a jackpot.

The Gist:While MA has been an outsized driver of profits for insurance companies in recent years,the nation’s two largest MA payers, UnitedHealth Group (UHG) and Humana, have been signaling growing concerns to the market.

UHG announced late last month that its 2024 MA enrollment growth will be less than half of its 2023 rate, and Humana has been engaged in merger talks with Cigna.

As the “gold rush” period ends, MA payers will have to earn their keep by better integrating their various care and data assets, and more carefully managing spending for an aging cohort of seniors with increasingly complex needs, both much harder than riding a demographic wave to easy profits.

The nation’s largest for-profit hospital systems by revenue — HCA Healthcare, Community Health Systems, Tenet Healthcare and Universal Health Services —reported mixed results during the third quarter of 2023, despite announcing strong demand for patient services.

With the exception of HCA, each operator reported lower profits in the third quarter compared with the same period last year. Health systems CHS and HCA reported earnings that fell short of Wall Street expectations for revenue.

Major operators posted declining profits in the third quarter compared to the same period in 2022

Q3 net income in millions, by operator

Health System

Profit

Percent Change YOY

Community Health Systems

$−91

−117%

HCA Healthcare

$1,800

59%

Tenet Healthcare

$101

−23%

Universal Health Services

$167

−9%

Admissions rose across the board compared to the same period last year: Same facility equivalent admissions rose4.1% at HCA , 3.7% at CHS and 0.6% at Tenet,and adjusted admissions at acute hospitals rose 6.8% at UHS.

Although the for-profit operators began cost containment strategies earlier this year — recognizing that rising expenses, including costs of salary and wages, were pressuring hospital profitability post-pandemic — expenses also rose, with growth in salaries and benefit costs once again pressuring most operators’ revenue.

Hospital operators faced new challenges this quarter, executives said, including increased physician staffing fees and what hospital executives characterizedas aggressive behavior from payers.

Hospitals highlight rising physician fees

Rising physician fees were a topic of concern on earnings calls this quarter, with executives reporting fees that were 15% to 40% higher compared with the same period last year.

Third-party staffing firms charge hospitals physician fees, a percentage of physicians’ salaries, on top of the salaries themselves. Physician fees are separate but related to contract labor costs, which plagued hospitals during the COVID-19 pandemic as they attempted to stem staffing shortages.

Hospitals typically contract specialty hospitalist roles — like anesthesiologists, radiologists and emergency department physicians — and incur associated staffing costs.

Physician fees at HCA, the country’s largest hospital chain, grew 20% year over year in the third quarter, according to CFO Bill Rutherford.

Physician fees were up by as much as 40% at UHS — making up 7.6% of totaloperating expenses this quarter and surpassing the company’s initial projections for the year,CEOMarc Miller said during an earnings call. Historically, physician fees accounted for about 6% of UHS’ total expenses.

Likewise, Franklin, Tennessee-based CHS attributed some of its third-quarter losses to “increased rates for outsourced medical specialists,” according to a release on the operator’s earnings.

Tenet CEO Saum Sutaria noted that physician fee expenses were up 15% year over year, but said on an earnings call that the operator had spied rising physician fees during the pandemic, and had begun efforts to contain costs — including restructuring staffing contracts and in-sourcing critical physician services.

As a result, physician fee costs at Tenet had remained “relatively flat” from the second quarter to the third quarter this year, according to the Sutaria.

Physician fee increases may be a delayed consequence of the No Surprises Act, which went into effect in January of last year, experts say.

On an earnings call, UHS CFO Steve Filton said “the industry has largely had to reset itself” in wake of the law. Tenet and CHS executives echoed the sentiment, noting that the law had disrupted staffing firms’ business models and complicated payment processes.

The No Surprises Act prevents patients who unknowingly receive out-of-network care at an in-network facility from being stuck with unexpectedbills. However, the act has had unintended ripple effects, experts say.

Staffing firms and hospitals allege that the arbitration process created to resolve disputes between providers and insurers is unbalanced and incentivizes insurers to withhold reimbursement for care. In an August survey, over half of doctors reported insurers have either ignored decisions made by arbitrators or declined to pay claims in full.

In other cases, a backlog prevents claims from being adjudicated at all. Last year, the CMS found the federal arbitration process had only reached a payment determination in 15% of cases. Federal regulators have been forced to pause and restart the arbitration process multiple times in the wake of federal court decisions challenging arbitration methodology.

Although the act went into effect more than a year ago, many hospitals are just now feeling the strain, saidLoren Adler, associate director at the Brookings Institute’s Schaeffer Initiative on Health Policy.

That’s because most insurers, hospitals and medical groups operate on three-year contracts, according to Adler. Staffing firms, which have struggled since the No Surprises Act was enacted, have passed on costs to hospitals as contracts come up for negotiation and insurers charge firms higher rates.

In the face of rising costs, some hospitals may opt to follow Tenet and CHS and in-source physicians — either to retain contracts with physicians who worked with firms that have folded or because the passing of the No Surprises Act makes outsourcing less attractive.

CHS hired 500 physicians from staffing firm American Physician Partners after the company collapsed in July. CFO Kevin Hammons said on an earnings call that hiring the physicians had saved CHS “approximately $4 million sequentially compared to the subsidy payments previously paid” to the staffing firm.

However, in-sourcing may not be an effective cost containment strategy for all operators. HCA reported it was hemorrhaging money following its first-quarter majority stake purchase of staffing firm Valesco, which brought about 5,000 physicians onto its payroll. HCA CEO Sam Hazen said the system expects to lose $50 million per quarter on the venture through 2024, citing low payments as the primary issue.

Payer problems

Hospital executives also tied quarterly losses to aggressive behavior from insurers during third-quarter earnings calls.

UHS executives said payers were improperly denying high volumes of claims and disrupting payments to its hospitals, with UHS’ Miller characterizing insurers as “increasingly aggressive” during the third quarter. Though insurers had reduced their number of claims audits, denials and patient status changes during the early stages of the pandemic, payers were increasing denials and reviews, according to UHS’ Filton.

Tenet’s Sutaria said that claims denials were “excessive and inappropriate” during a third-quarter earnings call, adding that the hospital system was working to push back on the volume of claims denials.

Their number one strategy is to provide “excellent documentation” to refute denials quickly, Sutaria said.

Still, excessive claims denials can drive up administrative costs for hospitals, according to Matthew Bates, managing director at Kaufman Hall.

“That denial creates a lot more work, because now I have to deal with that bill two, three, four times to get through the denial process,” Bates said. “It starts to rapidly eat into the operating margins… [becoming] both a cashflow problem and an administrative costs burden.”

Executives across the four for-profit operators said they planned to negotiate with insurers to receive more favorable rates and limit the number of denials in subsequent quarters.

HCA’s Hazen said that it was important for HCA to maintain its in-network status with insurers “to avoid the surprise billing and that [independent dispute resolution] process,” but that it would work with its payers to get “reasonable rates” going forward.

Here are 68 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings, Moody’s Investors Service and S&P Global in 2023.

AdventHealth has an “AA” rating and stable outlook with Fitch. The rating reflects the Altamonte Springs, Fla.-based system’s strong financial profile, characterized by still-adequate liquidity and moderate leverage, typically strong and highly predictable profitability, Fitch said.

Advocate Aurora Health has an “AA” rating and stable outlook with Fitch. The Downers Grove, Ill.- and Milwaukee-based system’s rating reflects a very strong financial profile in the context of an already sound market position and geographic reach that was enhanced after merging with Charlotte, N.C.-based Atrium Health, Fitch said.

AnMed Health has an “AA-” rating and stable outlook with Fitch. The Anderson, S.C.-based system has maintained strong performance through the COVID-19 pandemic and current labor market pressures, Fitch said.

AtlantiCare has an “AA-” rating and stable outlook with Fitch. The Atlantic City, N.J.-based system has a strong balance sheet with solid liquidity position and low debt burden, Fitch said.

Atrium Health has an “AA-” rating and stable outlook with S&P Global. The Charlotte, N.C.-based system’s rating reflects a robust financial profile, growing geographic diversity and expectations that management will continue to deploy capital with discipline.

Banner Health has an “AA-” and stable outlook with Fitch. The Phoenix-based system’s rating highlights the strength of its core hospital delivery system and growth of its insurance division, Fitch said.

BayCare Health System has an “AA” rating and stable outlook with Fitch. The Tampa, Fla.-based system’s rating reflects its excellent financial profile supported by its leading market position in a four-county area and the ability to sustain a solid operating outlook in the face of inflationary sector headwinds, Fitch said.

Bayhealth has an “AA” rating and stable outlook with Fitch. The rating reflects the strength of the Dover, Del.-based system’s market positions and the stability of its financial profile, Fitch said.

Beacon Health System has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of the South Bend, Ind.-based system’s balance sheet, the rating agency said.

Berkshire Health has an “AA-” rating and stable outlook with Fitch. The Pittsfield, Mass.-based system has a strong financial profile, solid liquidity and modest leverage, according to Fitch.

Bryan Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Lincoln, Neb., system’s leading and growing market position as a regional referral center with strong expense flexibility and cash flow, Fitch said.

Cape Cod Healthcare has an “AA-” and stable outlook with Fitch. The Hyannis, Mass.-based system’s rating reflects a dominant market position in its service area and historically solid operating results, the rating agency said.

Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area, Fitch said.

CaroMont Health has an “AA-” rating and stable outlook with S&P Global. The Gastonia, N.C.-based system has a healthy financial profile and robust market share in a competitive region.

CentraCare has an “AA-” rating and stable outlook with Fitch. The St. Cloud, Minn.-based system has a leading market position, and its management’s focus on addressing workforce pressures, patient access and capacity constraints will improve operating margins over the medium term, Fitch said.

Children’s Health System of Texas has an “AA” and stable outlook with Fitch. The Dallas-based system’s rating reflects its solid operating performance in 2022, resulting from inpatient, outpatient and surgical volume growth, as well as one-time support from pandemic-era stimulus funding, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The Minneapolis-based system’s broad reach within the region continues to support long-term sustainability as a market leader and preferred provider for children’s health care, Fitch said.

Concord (N.H.) Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of Concord’s leverage and liquidity assessment and Fitch’s assessment that two recently acquired hospitals will be strategically and financially accretive.

Cone Health has an “AA” rating and stable outlook with Fitch. The rating reflects the expectation that the Greensboro, N.C.-based system will gradually return to stronger results in the medium term, the rating agency said.

Cottage Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Santa Barbara, Calif.-based system’s leading market position and broad reach in a service area that exhibits modest population growth but consistently high demand for acute care services, Fitch said.

Deaconess Health System has an “AA” rating and stable outlook with Fitch. The Evansville, Ind.-based system demonstrated operating cost flexibility through the pandemic and recent labor and inflationary pressure, Fitch said.

Duke University Health System has an “AA-” rating and stable outlook with Fitch. Fitch projects the Durham, N.C.-based system will benefit from the integration of the former Private Diagnostic Clinic and from North Carolina’s recently enacted Medicaid expansion and Healthcare Access and Stabilization Program.

El Camino Health has an “AA-” rating and stable outlook with Fitch. The Mountain View, Calif.-based system has a history of generating double-digit operating EBITDA margins, driven by a solid market position that features strong demographics and a very healthy payer mix, Fitch said.

Franciscan Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Mishawaka, Ind.-based system’s strong and stable balance sheet, favorable payer mix, and leading or near leading market share in its service areas, Fitch said.

Froedtert Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s maintenance of a strong, albeit compressed, operating performance and a robust liquidity position, Fitch said.

Geisinger has an “AA-” credit rating and stable outlook with S&P. The Danville, Pa.-based system enjoys strong integration and value-based care experience, the ratings agency said.

Hackensack Meridian Health has an “AA-” rating and stable outlook with Fitch. The Edison, N.J.-based system’s rating is supported by its strong presence in its large and demographically favorable market, Fitch said.

Harris Health System has an “AA” rating and stable outlook with Fitch. The Houston-based system has a “very strong” revenue defensibility, primarily based on the district’s significant taxing margin that provides support for operations and debt service, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by a leading market position in its immediate area and very strong financial profile, Fitch said.

Intermountain Health has an “Aa1” rating and stable outlook with Moody’s. The Salt Lake City-based system’s rating is reflected by its distinctly leading market position in Utah and strong absolute and relative cash levels, Moody’s said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The Mullica Hill, N.J.-based system’s rating reflects its leading market position in a stable service area and a large medical staff supported by a growing residency program, Fitch said.

IU Health has an “AA” rating and stable outlook with Fitch. The Indianapolis-based system has a long track record of strong operating margins and an overall credit profile that is supported by a strong balance sheet, the rating agency said.

Lucile Packard Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the Palo Alto, Calif.-based hospital’s role as a nationally known, leading children’s hospital, Fitch said. It also benefits from resilient clinical volumes and a solid market position, as well as its relationship with Stanford University and Stanford Health Care.

Kaiser Permanente has an “AA-” and stable outlook with Fitch. The Oakland, Calif.-based system’s rating is driven by a strong financial profile, which is maintained despite a challenging operating environment in fiscal year 2022.

Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The Rochester, Minn.-based system’s credit profile characterized by its excellent reputations for clinical services, research and education, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The Grand Blanc, Mich.-based system has a leading market position over a broad service area covering much of Michigan and a track-record of profitability despite sector-wide market challenges in recent years, Fitch said.

McLeod Regional Medical Center has an “AA-” rating and stable outlook with Fitch. The rating reflects the Florence, S.C.-based system’s very strong financial profile assessment, historically strong operating EBITDA margins and its solid market position, Fitch said.

MemorialCare has an “AA-” rating and stable outlook with Fitch. The rating reflects the Fountain Valley, Calif.-based system’s strong financial profile and excellent leverage metrics despite its weaker operating performance, Fitch said.

Memorial Sloan-Kettering Cancer Center has an “AA” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the New York City-based system’s national and international reputation as a premier cancer hospital will continue to support growth in its leading and increasing market share for its specialty services.

Midland (Texas) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Midland’s exceptional market position and limited competition for acute-care services and growing outpatient services, Fitch said.

Monument Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Rapid City, S.D.-based system’s dominant inpatient market share and excellent market position across its geographically broad service area, Fitch said.

Munson Healthcare has an “AA” rating and stable outlook with Fitch. The rating reflects the strength of the Traverse City, Mich.-based system’s market position and its leverage and liquidity profiles.

MyMichigan Health has an “AA-” rating and stable outlook with Fitch. The Midland-based system reflects the system’s market position as the largest provider of acute care services and its leading market position in a sizable geographic area covering 25 counties in mid and northern Michigan, the rating agency said.

North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The Tupelo-based system’s rating reflects its very strong cash position and strong market position, Fitch said.

NewYork-Presbyterian Hospital has an “AA” rating and stable outlook with Fitch. The rating reflects the New York City-based system’s market position as one of New York’s major academic healthcare systems with a reputation that extends beyond the region, Fitch said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The Winston-Salem, N.C.-based system has a highly competitive market share in three separate North Carolina markets, Fitch said, including a leading position in Winston-Salem (46.8 percent) and second only to Atrium Health in the Charlotte area.

NYC Health + Hospitals has an “AA-” rating with Fitch. The New York City system is the largest municipal health system in the country, serving more than 1 million New Yorkers annually in more than 70 patient locations across the city, including 11 hospitals, and employs more than 43,000 people.

OhioHealth has an “AA+” rating and stable outlook with Fitch. The Columbus-based system has an exceptionally strong credit profile, very favorable leverage metrics and reliably strong profitability, Fitch said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The system’s upgrade from “A+” reflects the continued strength of the health system’s operating performance, growth in unrestricted liquidity and excellent market position in a demographically favorable market, Fitch said.

Phoenix Children’s Hospital has an “AA-” and stable outlook with Fitch. The rating reflects its position as a distinct leading provider of pediatric health services in a growing primary service area, Fitch said.

The Queen’s Health System has an “AA” rating and stable outlook with Fitch. The Honolulu-based system’s rating reflects its leading state-wide market position, historically strong operating performance and diverse revenue streams, the rating agency said.

Rush System for Health has an “AA-” and stable outlook with Fitch. The Chicago-based system has a strong financial profile despite ongoing labor issues and inflationary pressures, Fitch said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The Cape Girardeau, Mo.-based system enjoys robust operational performance and a strong local market share as well as manageable capital plans, Fitch said.

Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The system has a “very strong” financial profile and a leading market share position, Fitch said.

Sanford Health has an “AA-” rating and stable outlook with Fitch. The Sioux Falls, S.D.-based system rating reflects its leading inpatient market share positions in multiple markets and strong overall financial profile, the rating agency said.

Stanford Health Care has an “AA” rating and stable outlook with Fitch. The Palo Alto, Calif.-based system’s rating is supported by its extensive clinical reach in the greater San Francisco and Central Valley regions and nationwide/worldwide destination position for extremely high-acuity services, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system has a strong financial profile, multi-state presence and scale, with solid revenue diversity, Fitch said.

St. Clair Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Pittsburgh-based system’s strong financial profile assessment, solid market position and historically strong operating performance, the rating agency said.

St. Tammany Parish Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the Covington, La.-based system’s strong operating risk assessment and very strong financial profile supported by consistently robust operating cash flows, Fitch said.

Texas Medical Center has an “AA-” rating and stable outlook with Fitch. The rating reflects the Houston-based system’s profitable service enterprise, its long and collaborative relationship with strong university, nonprofit and medical industry partners, and sizable financial reserve levels, Fitch said.

TriHealth has an “AA-” rating and stable outlook with Fitch. The Cincinnati-based system’s rating reflects its broad reach, high-acuity services and stable market position in a highly fragmented and competitive market, Fitch said.

UChicago Medicine has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s broad and growing reach for high-acuity services and the considerable benefits it receives from its high degree of integration with the University of Chicago, Fitch said.

UCHealth has an “AA” rating and stable outlook with Fitch. The Aurora, Colo.-based system’s margins are expected to remain robust, and the operating risk assessment remains strong, Fitch said.

University of Kansas Health System has an “AA-” rating and stable outlook with S&P Global. The Kansas City-based system has a solid market presence, good financial profile and solid management team, though some balance sheet figures remain relatively weak to peers, the rating agency said.

Virtua Health has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Marlton, N.J.-based system’s leading market position in a stable service area and the successful integration of the Lourdes Health System, Fitch said.

VHC Health has an”AA-” rating and stable outlook with Fitch. The Arlington-based system has demonstrated strong operating cost flexibility, growth in high acuity service lines and an expanding outpatient footprint, Fitch said.

WellSpan Health has an “Aa3” rating and stable outlook with Moody’s. The York, Pa.-based system has a distinctly leading market position across several contiguous counties in central Pennsylvania, and management’s financial stewardship and savings initiatives will continue to support sound operating cash flow margins when compared to peers, Moody’s said.

Willis-Knighton Health System has an “AA-” rating and stable outlook with Fitch. The Shreveport, La.-based system has a “dominant inpatient market position” and is well positioned to manage operating pressures, Fitch said.

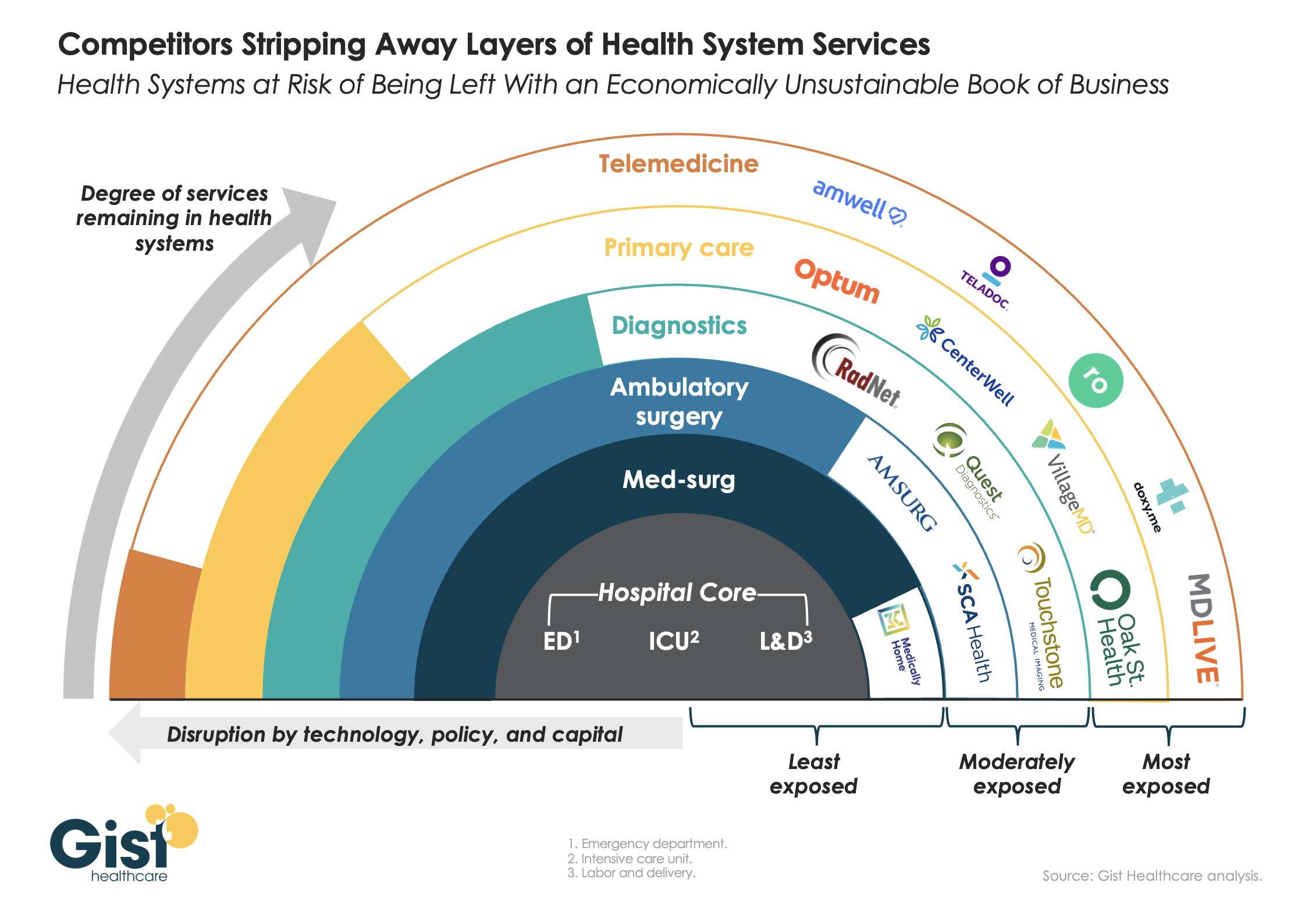

This week’s graphic features our assessment of the many emerging competitive challenges to traditional health systems.

Beyond inflation and high labor costs, health systems are struggling because competitors—ranging from vertically integrated payers to PE-backed physician groups—are effectively stripping away profitable services and moving them to lower-cost care sites. The tandem forces of technological advancement, policy changes, and capital investment have unlocked the ability of disruptors to enter market segments once considered safely within health system control.

While health systems’ most-exposed services, like telemedicine and primary care, were never key revenue sources (although they are key referral drivers), there are now more competitors than ever providing diagnostics and ambulatory surgery, which health systems have relied on to maintain their margins.

Moving forward, traditional systems run the risk of being “crammed down” into a smaller portfolio of (largely unprofitable) services: the emergency department, intensive care unit, and labor and delivery.

Health systems cannot support their operations by solely providing these core services, yet this is the future many will face if they don’temulate the strategies of disruptors by embracing the site-of-care shift, prioritizing high-margin procedures, rethinking care delivery within the hospital, and implementing lower-cost care models that enable them to compete on price.

West Reading, Pa.-based Tower Health continues to make progress on its performance improvement plan as its operating margin for the three months ended Sept. 30 rose to -4.2% from -8% during the same period in 2022. Its operating cash flow margin also increased from -0.9% to 2.3%.

During the first quarter of fiscal 2024, the three months ending Sept. 30, revenue decreased 2.9% year over year to $457.4 million. Expenses decreased 6.4% to $476.5 million.

Tower’s operating loss for the period was $19.1 million, compared with a loss of $37.6 million for the prior-year period.

As of Sept. 30, total balance sheet unrestricted cash and board-designated investment funds for capital improvements totalled $154 million — a decrease of $54 million from June 30, 2023. The main factors for the decrease were $15 million of debt service payments, physician incentive compensation payments of $9 million, capital expenditures of $6 million, negative changes in working capital of $32 million, partially offset by EBITDA of $10 million.

Total days of cash on hand for the system was 30 on Sept. 30.

After including the performance of its investment portfolio and other nonoperating items, the health system ended the three-month period with a net loss of $20.9 million, compared with a net loss of $37.6 million for the same period in 2022.

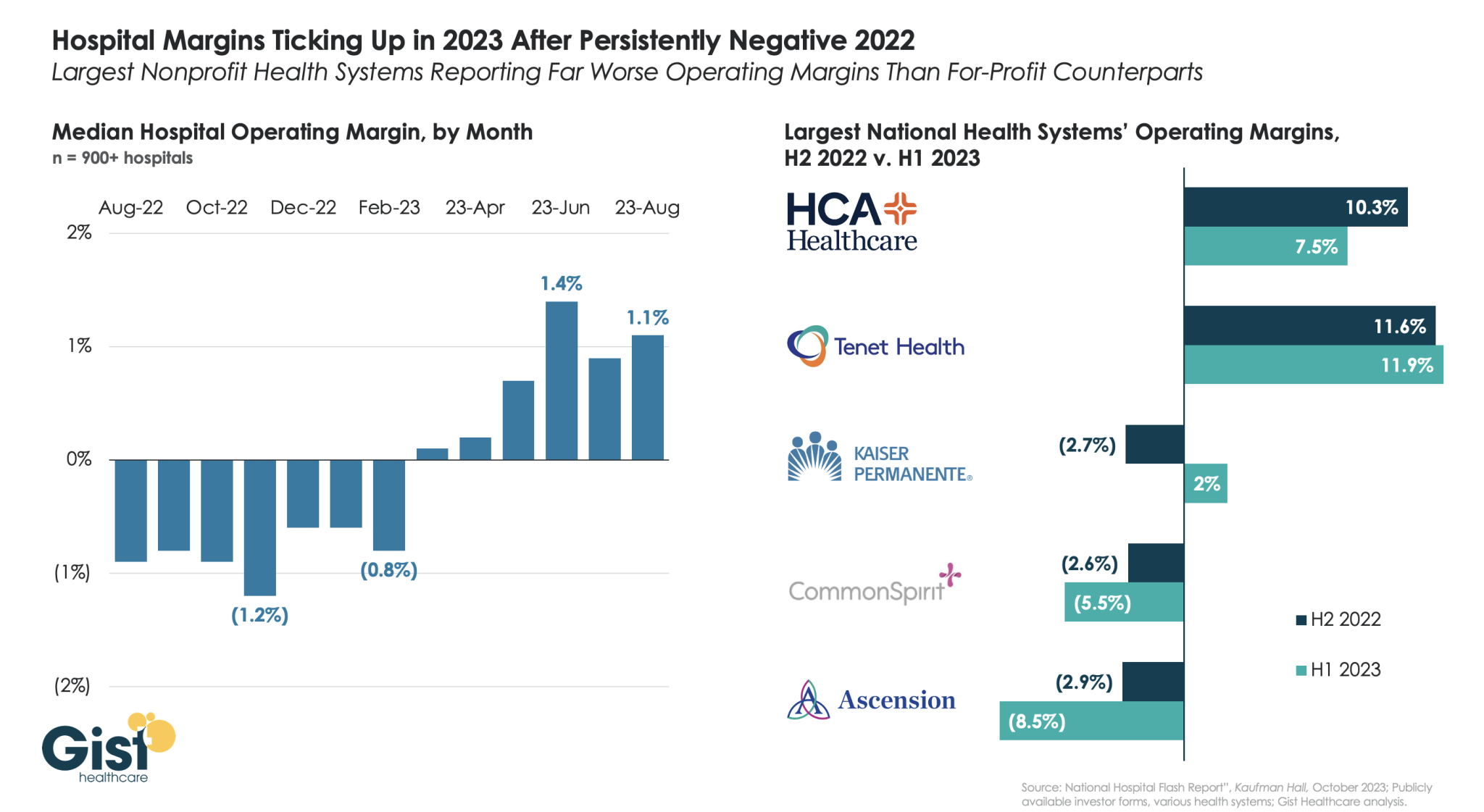

While hospitals’ overall performance declined slightly in September compared to the previous month, the median Kaufman Hall Calendar Year-To-Date Operating Margin Index reflecting actual margins was 1.4% in September. This slight increase was due to the historical variation in the performance of hospitals across 2023.

Volume decreased across the board, but data indicate improvement in the overall financial picture compared to 2022.

Using data from Kaufman Hall’s latest National Hospital Flash Report and publicly available investor reports for some of the nation’s largest health systems, the graphic below takes stock of the state of health system margins.

After the median hospital delivered negative operating margins for twelve-straight months, 2023 has made for a positive but slim year so far, with margins hovering around one percent. Amid this breakeven environment, fortunes have diverged between nonprofit and for-profit health systems.

The largest for-profit systems, HCA Healthcare and Tenet Healthcare, posted operating margins of around 10 percent between July 2022 and June 2023, while the three largest nonprofit systems, Kaiser Permanente, CommonSpirit Health, and Ascension, suffered net losses.

Although Kaiser Permanente’s margin bounced back in the first half of this year, CommonSpirit and Ascension’s margins continued to decline, more than doubling the operating losses of the prior six months.

One key to the recent success of the largest for-profit systems is their diversification away from inpatient care.

Case in point: almost half of Tenet’s profits in 2023 have come from its ambulatory division, driven by its United Surgical Partners International (USPI) ambulatory surgery center network, which has posted 40 percent margins over the past several quarters.

Hospitals and health systems are seeing some signs of stabilization in 2023 following an extremely difficult year in 2022. Workforce-related challenges persist, however, keeping costs high and contributing to issues with patient access to care. The percentage of respondents who report that they have run at less than full capacity at some time over the past year because of staffing shortages, for example, remains at 66%, unchanged from last year’s State of Healthcare Performance Improvement report. A solid majority of respondents (63%) are struggling to meet demand within their physician enterprise, with patient concerns or complaints about access to physician clinics increasing at approximately one-third (32%) of respondent organizations.

Most organizations are pursuing multiple strategies to recruit and retain staff. They recognize, however, that this is an issue that will take years to resolve—especially with respect to nursing staff—as an older generation of talent moves toward retirement and current educational pipelines fail to generate an adequate flow of new talent. One bright spot is utilization of contract labor, which is decreasing at almost two-thirds (60%) of respondent organizations.

Many of the organizations we interviewed have recovered from a year of negative or breakeven operating margins. But most foresee a slow climb back to the 3% to 4% operating margins that help ensure long-term sustainability, with adequate resources to make needed investments for the future. Difficulties with financial performance are reflected in the relatively high percentage of respondents (24%) who report that their organization has faced challenges with respect to debt covenants over the past year, and the even higher percentage (34%) who foresee challenges over the coming year. Interviews confirmed that some of these challenges were “near misses,” not an actual breach of covenants, but hitting key metrics such as days cash on hand and debt service coverage ratios remains a concern.

As in last year’s survey, an increased rate of claims denials has had the most significant impact on revenue cycle over the past year. Interviewees confirm that this is an issue across health plans, but it seems particularly acute in markets with a higher penetration of Medicare Advantage plans. A significant percentage of respondents also report a lower percentage of commercially insured patients (52%), an increase in bad debt and uncompensated care (50%), and a higher percentage of Medicaid patients (47%).

Supply chain issues are concentrated largely in distribution delays and raw product and sourcing availability. These issues are sometimes connected when difficulties sourcing raw materials result in distribution delays. The most common measures organizations are taking to mitigate these issues are defining approved vendor product substitutes (82%) and increasing inventory levels (57%). Also, as care delivery continues to migrate to outpatient settings, organizations are working to standardize supplies across their non-acute settings and align acute and non-acute ordering to the extent possible to secure volume discounts.

Survey Highlights

98% of respondents are pursuing one or more recruitment and retention strategies

90%have raised starting salaries or the minimum wage

73%report an increased rate of claims denials

71% are encountering distribution delays in their supply chain

70%are boarding patients in the emergency department or post-anesthesia care unit because of a lack of staffing or bed capacity

66% report that staffing shortages have required their organization to run at less than full capacity at some time over the past year

63% are struggling to meet demand for patient access to their physician enterprise

60% see decreasing utilization of contract labor at their organization

44%report that inpatient volumes remain below pre-pandemic levels

32% say that patients concerns or complaints about access to their physician enterprise are increasing

24%have encountered debt covenant challenges during the past 12 months

None of our respondents believe that their organization has fully optimized its use of the automation technologies in which it has already invested

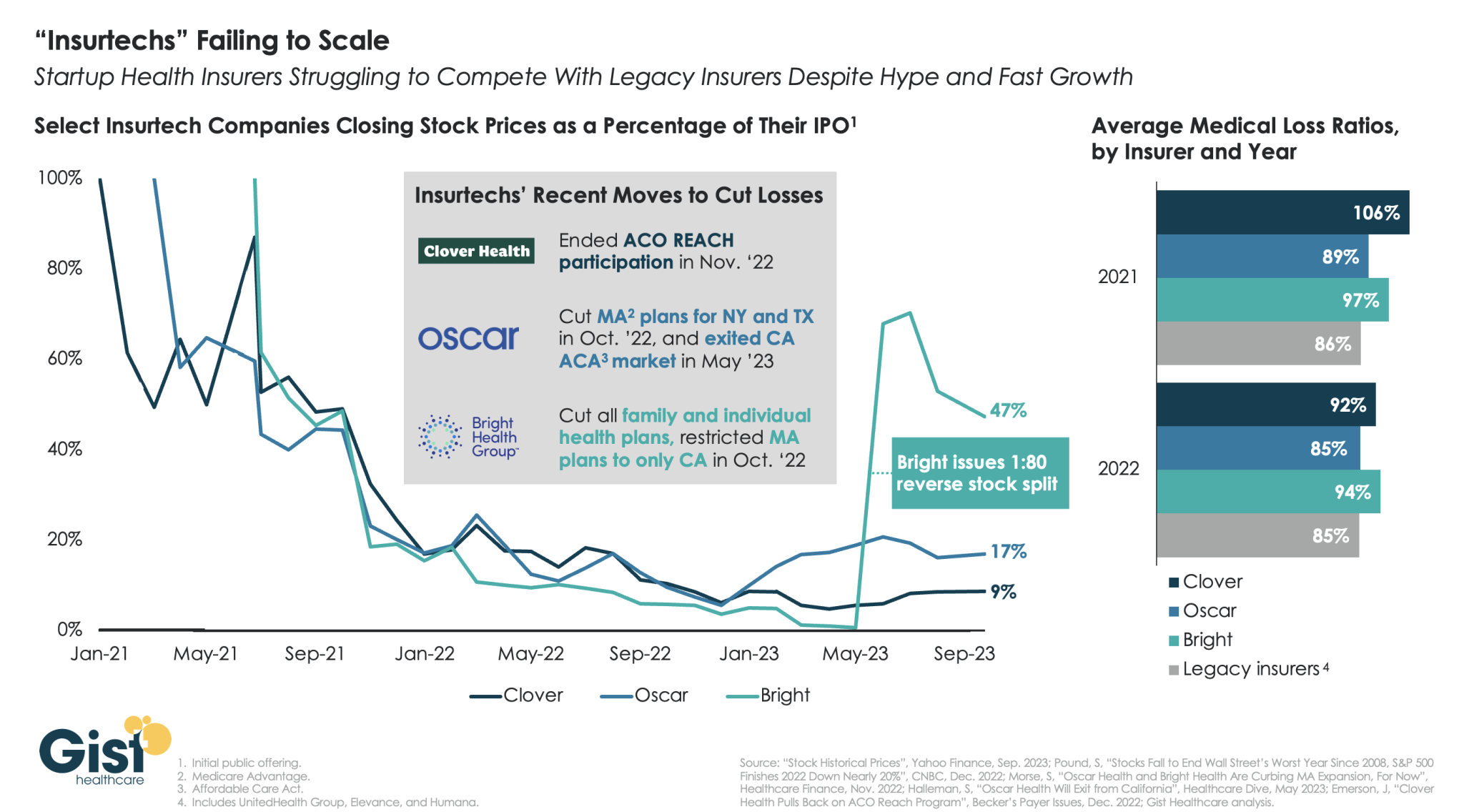

“Insurtechs” Clover Health, Oscar Health, and Bright Health all went public in the midst of the hot equity market of 2021. Investors were excited by the fast growth of these health insurer startups, and their potential to revolutionize an industry dominated by a few large players.

However, the hype has dissipated as financial performance has deteriorated. After growing at all costs during a period of low interest rates, changing market conditions directed investors to demand a pivot to profitability,which the companies have struggled to deliver—twoyears later,none of the three has turned a profit.

Oscar and Bright have cut back their market presence significantly, while Clover has mostly carried on while sustaining high losses. In the last two years, only Oscar has posted a medical loss ratio in line with other major payers, who meanwhile are reporting expectation-beating profits. While Oscar has shown signs of righting the ship since the appointment of former Aetna CEO Mark Bertolini,

the future of these small insurers remains uncertain. As their losses mount and they exit markets, they may become less desirable as acquisition targets for large payers.