This week, all eyes will be on the U.S. Congress as the clock ticks toward a potential government shutdown. Whether lawmakers reach agreement on a continuing resolution to extend funding for30 to 60 days or the government shuts down at midnight this Saturday, it will have direct negative impact on consumer activities and spending in healthcare.

Background:

A shutdown alone is not apocalyptic for consumers: they’ve weathered 20 shutdowns averaging 8 days each since 1976 and recovered productivity shortfalls within 3-6 months. What’s complicating and most problematic for healthcare is its concurrence with equally threatening events and trends inside and outside healthcare:

The resumption of Student Loan debt payments starting in October 1 impacting 900,000 Americans– 90% say they can’t!

The probability the Federal Reserve will increase its federal borrowing rate by 25 basis points to 5.50 thus increasing interest costs and consumer prices.

The slowdown in GDP growth and increase in fuel costs projected by economists and regulators.

Increased workforce-management tension resulting in strikes, walkouts and slowdowns in labor-intense settings like auto manufacturing, nursing homes and hospitals.

Medical inflation: technological advancements, increased demand, rising drug prices, expensive medical equipment, and increased administrative costs are contributors. According to the U.S. Bureau of Labor Statistics, prices for medical care are 5,274.47% higher in 2023 vs. 1935 (a $52,744.67 difference in value). Between 1935 and 2023, medical care experienced an average inflation rate of 4.63% per year, but in that period, working-age consumers who are privately insured paid a disproportionate and growing share projected to exceed 10% in 2023.

The health system’s economics are partially protected from shutdowns since funding for the Medicare and Medicaid is somewhat protected. That’s the status quo.

But the confluence of growing bipartisan Congressional antipathy toward the industry vis a vis regulatory reforms (i.e. price transparency, site neutral payments, DOJ-FTC consolidation constraints et al), high profile congressional investigations (i.e. PBMs and drug prices, role of private equity ownership), administrative orders from the White House and Governors (i.e.medical debt, value initiatives, organ procurement et al) and negative publicity challenging community benefits, CEO compensation and fraudulent activities erode the industry’s good will and expose it to unprecedented consumer risks.

Evidence in support of this assessment is substantial as illustrated in the sections that follow. There are no easy solutions. The U.S. health industry status quo is a B2B2P2C (business to business to physician to consumer) industry in which most decisions impacting what consumers ultimately spend for healthcare products and services are made for them, not by them. The direct costs associated with supply chain, technologies, facilities and R&D are closely guarded secrets. Indirect costs, administrative overhead, off balance sheet activities, partnerships and alliances even more.

What’s clear is that every sector in healthcare will be subject to scrutiny through an uncomfortable lens—the consumer. Prices matter. Service matters. Integrity matters. Transparency matters. Ownership matters. Purpose matters. And whether accurate or not, fair or not, comfortable or not, information accessible to consumers is readily accessible.

The shutdown over the debt limit might happen or be diverted. What will not be diverted is growing discontent with the medical system that the majority of consumers believe wasteful, expensive and self-serving. How the status quo is impacted is anyone’s guess, but it’s a good bet its future is not a cut-and-paste version of its past.

Saturday, Congress voted overwhelming (House 335-91, Senate 88-9) to keep the government funded until Nov. 17 at 2023 levels. No surprise. Congress is supposed to pass all 12 appropriations bills before the start of each fiscal year but has done that 4 times since 1970—the last in 1997. So, while this chess game plays out, the health system will soldier on against growing recognition it needs fixing.

In Wednesday night’s debate, GOP Presidential aspirant Nicki Haley was asked what she would do to address the spike in personal bankruptcies due to medical debt. Her reply:

“We will break all of it [down], from the insurance company, to the hospitals, to the doctors’ offices, to the PBMs [pharmacy benefit managers], to the pharmaceutical companies. We will make it all transparent because when you do that, you will realize that’s what the problem is…we need to bring competition back into the healthcare space by eliminating certificate of need systems… Once we give the patient the ability to decide their healthcare, deciding which plan they want, that is when we will see magic happen, but we’re going to have to make every part of the industry open up and show us where their warts are because they all have them”

It’s a sentiment widely held across partisan aisles and in varied degrees among taxpayers, employers and beyond. It’s a system flaw and each sector is complicit.

What seems improbable is a solution that rises above the politics of healthcare where who wins and loses is more important than the solutions themselves.

Perhaps as improbable as the European team’s dominating performance in the 44th Ryder Cup Championship played in Rome last week especially given pre-tournament hype about the US team.

While in Rome last week, I queried hotel employees, restaurant and coffee shop owners, taxi drivers and locals at the tournament about the Italian health system. I saw no outdoor signage for hospitals and clinics nor TV ads for prescriptions and OTC remedies. Its pharmacies, clinics and hospitals are non-descript, modest and understated. Yet groups like the World Health Organization (WHO) and the Organization for Economic Cooperation Development (OECD) rank Servizio Sanitario Nazionale (SSN), the national system authorized in December 1978, in the top 10 in the world (The WHO ranks it second overall behind France).

“It covers all Italian citizens and legal foreign residents providing a full range of healthcare services with a free choice of providers. The service is free of charge at the point of service and is guided by the principles of universal coverage, solidarity, human dignity, and health. In principle, it serves as Italy’s public healthcare system.” Like U.S. ratings for hospitals, rankings for the Italian system vary but consistently place it in the top 15 based on methodologies comparing access, quality, and affordability.

The U.S., by contrast, ranks only first in certain high-end specialties and last among developed systems in access and affordability.

Like many systems of the world, SSN is governed by a national authority that sets operating principles and objectives administered thru 19 regions and two provinces that deliver health services under an appointed general manager. Each has significant independence and the flexibility to determine its own priorities and goals, and each is capitated based on a federal formula reflecting the unique needs and expected costs for that population’s health.

It is funded throughnational and regional taxes, supplemented by private expenditure and insurance plans and regions are allowed to generate their own additional revenue to meet their needs. 74% of funding is public; 26% is private composed primarily of consumer out-of-pocket costs. By contrast, the U.S. system’s funding is 49% public (Medicare, Medicaid et al), 24% private (employer-based, misc.) and 27% OOP by consumers.

Italians enjoy the 6th highest life expectancy in the world, as well as very low levels of infant mortality. It’s not a perfect system: 10% of the population choose private insurance coverage to get access to care quicker along with dental care and other benefits. Its facilities are older, pharmacies small with limited hours and hospitals non-descript.

But Italians seem satisfied with their system reasoning it a right, not a privilege, and its absence from daily news critiques a non-concern.

Issues confronting its system—like caring for its elderly population in tandem with declining population growth, modernizing its emergency services and improving its preventive health programs are understood but not debilitating in a country one-fifth the size of the U.S. population.

My take:

Italy spends 9% of its overall GDP on its health system; the $4.6 trillion U.S spends 18% in its GDP on healthcare, and outcomes are comparable. Our’s is better known but their’s appears functional and in many ways better.

Should the U.S.copy and paste the Italian system as its own? No. Our societies, social determinants and expectations vary widely. Might the U.S. health system learn from countries like Italy? Yes.

Questions like these merit consideration:

Might the U.S. system perform better if states had more authority and accountability for Medicare, CMS, Veterans’ health et al?

Might global budgets for states be an answer?

Might more spending on public health and social services be the answer to reduced costs and demand?

Might strict primary care gatekeeping be an answer to specialty and hospital care?

Might private insurance be unnecessary to a majority satisfied with a public system?

Might prices for prescription drugs, hospital services and insurance premiums be regulated or advertising limited?

Might employers play an expanded role in the system’s accountability?

Can we afford the system long-term, given other social needs in a changing global market?

Comparisons are constructive for insights to be learned. It’s true in healthcare and professional golf. The European team was better prepared for the Ryder Cup competition. From changes to the format of the matches, to pin placements and second shot distances requiring precision from 180-200 yards out on approach shots: advantage Europe. Still, it was execution as a team that made the difference in its dominating 16 1/2- 11 1/2 win —not the celebrity of any member.

The time to ask and answer tough questions about the sustainability of the U.S. system and chart a path forward. A prepared, selfless effort by a cross-sector Team Healthcare USA is our system’s most urgent need. No single sector has all the answers, and all are at risk of losing.

Team USA lost the Ryder Cup because it was out-performed by Team Europe: its data, preparation and teamwork made the difference.

Today, there is no Team Healthcare USA: each sector has its stars but winning the competition for the health and wellbeing of the U.S. populations requires more.

Two pioneers of mRNA research — the technology that helped the world tame the virus behind the Covid-19 pandemic — won the 2023 Nobel Prize in medicine or physiology on Monday.

Overcoming a lack of broader interest in their work and scientific challenges, Katalin Karikó and Drew Weissman made key discoveries about messenger RNA that enabled scientific teams to start developing the tool into therapies, immunizations, and — as the pandemic spread in 2020 — vaccines targeting the SARS-CoV-2 coronavirus. Moderna and the Pfizer-BioNTech partnership unveiled their mRNA-based Covid-19 shots in record time thanks to the foundational work of Karikó and Weissman, helping save millions of lives.

Karikó, a biochemist, and Weissman, an immunologist, performed their world-changing research on the interaction between mRNA and the immune system at the University of Pennsylvania, where Weissman, 64, remains a professor in vaccine research. Karikó, 68, who later went to work at BioNTech, is now a professor at Szeged University in her native Hungary, and is an adjunct professor at Penn’s Perelman School of Medicine.

The duo will receive 11 million Swedish kronor, or just over $1 million. Their names are added to a list of medicine or physiology Nobel winners that prior to this year included 213 men and 12 women.

The award was announced by Thomas Perlmann, secretary general of Nobel Assembly, in Stockholm. Perlmann said he had spoken to both laureates, describing them as grateful and surprised even though the pair has won numerous awards seen as precursors and had been tipped as likely Nobel recipients at some point.

Every year, the committee considers hundreds of nominations from former Nobel laureates, medical school deans, and prominent scientists from fields including microbiology, immunology, and oncology. Members try to identify a discovery that has altered scientists’ understanding of a subject. And according to the criteria laid out in Alfred Nobel’s will, that paradigm-shifting discovery also has to have benefited humankind.

The Nobel committee framed Karikó and Weissman’s work as a prime example of complementary expertise, with Karikó focused on RNA-based therapies and Weissman bringing a deep knowledge about immune responses to vaccines.

But it was not an easy road for the scientists. Karikó encountered rejection after rejection in the 1990s while applying for grants. She was even demoted while working at Penn, as she toiled away on the lower rungs of academia.

But the scientists persisted, and made a monumental discovery published in 2005 based on simply swapping out some of the components of mRNA.

With instructions from DNA, our cells make strands of mRNA that are then “read” to make proteins. The idea underlying an mRNA vaccine then is to take a piece of mRNA from a pathogen and slip it into our bodies. The mRNA will lead to the production of a protein from the virus, which our bodies learn to recognize and fight should we encounter it again in the form of the actual virus.

It’s an idea that goes back to the 1980s, as scientific advances allowed researchers to make mRNA easily in their labs. But there was a problem: The synthetic mRNA not only produced smaller amounts of protein than the natural version in our cells, it also elicited a potentially dangerous inflammatory immune response, and was often destroyed before it could reach target cells.

Karikó and Weissman’s breakthrough focused on how to overcome that problem. mRNA is made up of four nucleosides, or “letters”: A, U, G, and C. But the version our bodies make includes some nucleosides that are chemically modified — something the synthetic version didn’t, at least until Karikó and Weissman came along. They showed that subbing out some of the building blocks for modified versions allowed their strands of mRNA to sneak past the body’s immune defenses.

While the research did not gain wide attention at the time, it did catch the attention of scientists who would go on to found Moderna and BioNTech. And now, nearly 20 years later, billions of doses of mRNA vaccines have been administered.

For now, the only authorized mRNA products are the Covid-19 shots. But academic researchers and companies are exploring the technology as a potential therapeutic platform for an array of diseases and are using it to develop cancer vaccines as well as immunizations against other infectious diseases, from flu to mpox to HIV. An mRNA vaccine is highly adaptable compared to earlier methods, which makes it easier to alter the underlying recipe of the shot to keep up with viral evolution.

As she gained global fame, Karikó has been open about the barriers she encountered in her scientific career, which raised broader issues about the challenges women and immigrants can face in academia. But she’s said she always believed in the potential of her RNA research.

“I thought of going somewhere else, or doing something else,” Karikó told STAT in 2020, recalling the moment she was demoted. “I also thought maybe I’m not good enough, not smart enough. I tried to imagine: Everything is here, and I just have to do better experiments.”

This is Part 2 of a series by Cain Brothers about the first-ever collaboration conference between health systems and private equity (PE) investment firms. Part 1 of this series addressed the conference’s who, what and where. This commentary will focus on the why. We will explore the underlying forces uniting health systems with private equity during this period of unprecedented industry disruption.

Why Health Systems and PE Need Each Other

On June 13 and 14, 2023, Cain Brothers hosted the first-ever collaboration conference between health systems and private equity (PE) investment firms. Timing, market dynamics and opportunity aligned. The conference was an over-the-moon success. Along with its sponsors, Cain Brothers will seek to expand the conference and align initiatives through the coming years.

Why Now? Healthcare is Stuck and Needs Solutions

As a society, the U.S. is spending ever-higher amounts of money while its population is getting sicker. A maldistribution of facilities and practitioners creates inequitable access to healthcare services in lower-income communities with the highest levels of chronic disease.

New competitors and business models along with unfavorable macro forces, including high inflation, aging demographics and deteriorating payer mixes, are fundamentally challenging health systems’ status quo business practices.

Governments, particularly the federal government, have become healthcare’s largest payers, funding over 40% of healthcare’s projected $4.7 trillion expenditure in 2023. Individual patients often get lost in the massive payment shuffle between payers and providers.

Meanwhile, governments’ pockets are emptying. As a percentage of GDP, U.S. government debt obligations have grown from 55% in 2001 to 124% currently. With rising interest rates and the commensurate increase in debt service costs, as well as an aging population, there is little to suggest that new funding sources will emerge to fund expansive healthcare expenditures. Scarcity reigns where resources for healthcare providers were once plentiful.

As a consequence, the healthcare industry is entering a period of more fundamental economic limitations. Delaying transformation and expecting society to fund ongoing excess expenditure is not a sustainable long-term strategy. Current economic realities are forcing a dramatic reallocation of resources within the healthcare industry.

The healthcare industry will need to do more with less. Pleading poverty will fall on deaf ears. There will be winners and losers. The nation’s acute care footprint will shrink. For these reasons, health systems are experiencing unprecedented levels of financial distress. Indeed, parts of the system appear on the verge of collapse, particularly in medically underserved rural and urban communities.

More of the same approaches will yield more of the same dismal results. Waking up to this existential challenge, enlightened health systems have become more open to new business models and collaborative partnerships.

Necessity Stimulates Innovation

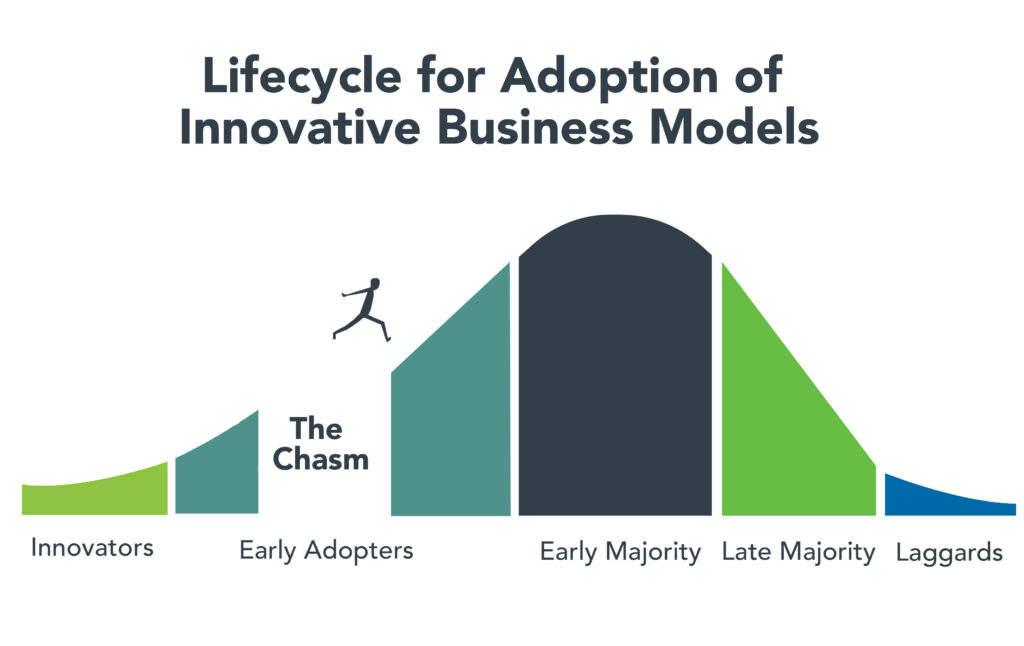

Two disruptive and value-based business models are on the verge of achieving critical mass. They are risk-bearing “payvider” companies (e.g. Kaiser, Oak Street Health and others) and consumer-friendly, digital-savvy delivery platforms (e.g. OneMedical and innumerable point-solution companies).

Value-based care providers and their investors have the scars and bruises to show for challenging entrenched business practices reliant on fee-for-service (FFS) business models and administrative services only (ASO) contracting. Incumbents have protected their privileged market position well through market leverage and outsized political influence.

Despite market resistance, “payvider” and digital platform companies are emerging from the proverbial “innovators’ chasm.” More early adopters, including those health systems attending the Nashville conference, are embracing value-creating business models. The chart below illustrates the well-trodden path innovation takes to achieve market penetration.

Ironically, during this period of industry disruption, health systems understand they need to deliver greater value to customers to maintain market relevance. It will require great execution and overcoming legacy practices to develop business platforms that incorporate the following value-creating capabilities:

Decentralized care delivery (to make care more accessible and lower cost).

Root-cause treatment of chronic conditions.

Integrated physical and mental healthcare services.

Consistent, high-quality consumer experience.

Coordinated service delivery.

Standardized protocols that improve care quality and outcomes.

A truly patient/customer-centric operating orientation.

It’s not what to do, it’s how to get it done that creates the vexing conundrum. Solutions require collaboration. Platform business models replete with strategic partnerships are emerging. Paraphrasing an African proverb, it’s going to take a village to fix healthcare. That’s why the moment for health systems and PE firms to collaborate is now.

PE to the Rescue?

Private equity has become the dominant investment channel for business growth across industries and nations. According to a recent McKinsey report, PE has more than $11.7 trillion in assets under management globally. This is a massive number that has grown steadily. PE changes markets. It turbocharges productivity. It is a relentless force for value creation.

By investing in a wide spectrum of asset classes, private equity has become a vital source of investment returns for pensions, endowments, sovereign wealth funds and insurance companies. Healthcare, given its size and inefficiencies, is a target-rich environment for PE investment and returns. This explains the PE’s growing interest in working with health systems to develop mutually beneficial, value-creating healthcare enterprises.

Despite reports to the contrary, PE firms must invest for the long term. Unlike the stock market, where investors can buy and sell a stock within a matter of seconds, PE firms do not have that luxury. To generate a return, they must acquire and grow businesses over a period of years to create suitable exit strategies.

Money talks. By definition, all buyers of new companies value their purchase more than the capital required for the acquisition. In making purchase decisions, buyers evaluate businesses’ past performance. They also assess how the new business will perform under their stewardship. PE or PE-backed acquirers also consider which future buyers will be most likely acquire the company after a five-plus year development period.

PE’s investment approach can align well with health systems looking to create sustainable long-term businesses tied to their brands and market positioning. PE firms buy and build companies that attract customers, employees and capital over the long term, far beyond their typical five- to seven-year ownership period. Health systems that partner with PE firms to develop companies are the logical acquirers of those companies if they succeed in the marketplace. In this way, a rising valuation creates value for both health systems and their PE partners.

It is important to note that not all PE are created the same. Like health systems, PE firms differ in size, market orientation, investment theses, experience and partner expectations. Given this inherent diversity, it takes time, effort and a shared commitment to value creation for health systems and PE firms to determine whether to become strategic partners. Not all of these partnerships will succeed, but some will succeed spectacularly.

For health system-PE partnerships to work, the principals must align on strategic objectives, governance, performance targets and reporting guidelines. Trust, honest communication and clear expectations are the key ingredients that enable these partnerships to overcome short-term hurdles on the road to long-term success.

Conclusion: Time to Slay Healthcare’s Dragons

Market corrections are hard. As a nation, the U.S. has invested too heavily in hospital-centric, disease-centric, volume-centric healthcare delivery. The result is a fragmented, high-cost system that fails both consumers and caregivers. The marketplace is working to reallocate resources away from failing business practices and into value-creating enterprises that deliver better care outcomes at lower costs with much less friction.

Progressive health systems and PE firms share the goal of creating better healthcare for more Americans. Cain Brothers is committed to advancing collaboration between health systems and PE-backed companies. In addition to the Nashville conference, the firm has combined its historically separate corporate and non-profit coverage groups to foster idea exchange, expand sector understanding and deliver higher value to clients.

The ability to connect and collaborate effectively with private equity to advance business models will differentiate winning health systems. In a consolidating industry, this differentiation is a prerequisite for sustaining competitiveness. It’s adapt or die time. Health systems that proactively embrace transformation will control their future destiny. Those that fail to do so will lose market relevance.

The future of healthcare is not a zero-sum equation. Markets evolve by creating more complex win-win arrangements that create value for customers. No industry requires restructuring more than healthcare. As a nation and an industry, we have the capacity to fix America’s broken healthcare system. The real question is whether we have the collective will, creativity and resourcefulness to power the transformation. We believe the answer to that question is yes.

Paraphrasing Rev. Theodore Parker, the economic arc of the marketplace is long but it bends toward value. Together, health systems and PE firms can power value-creation and transformation more effectively than either sector can do independently. Each needs the other to succeed. Slaying healthcare’s dragons will not be easy but it is doable. It’s going to take a village to fix healthcare.

Costco is now offering members online health checkups for as low as $29.

The retailer is offering the new service in partnership with Sesame, a direct-to-consumer health care marketplace that connects medical providers nationwide with consumers.

Sesame, in a release, said Costco members beginning Monday can book health care visits directly through their memberships in all 50 states.

The New York-based company said its platform doesn’t accept health insurance because it primarily caters to uninsured Americans and those with high-deductible plans who prefer to pay cash for their health care. It said its model helps keep prices of services low for its users.

The services listed on Costco Pharmacy’s homepage, include virtual primary care visits for $29, health checkups (a standard lab panel and a virtual follow-up consultation with a provider) for just $72 and online mental health visits for $79.

“Quality, great value, and low price are what the Costco brand is known for,” David Goldhill, Sesame’s co-founder and CEO, said in a statement. “When it comes to health care, Sesame also delivers high quality and great value – and a low price that will be appreciated by Costco Members when it comes to their own care.”

Amazon, in August, announced that its virtual clinic was now also available nationwide. Amazon Clinic launched last November offering 24/7 access to third-party health-care providers directly on Amazon’s website and mobile app.

Amazon customers, through the clinic, can access telehealth treatment for dozens of common conditions, such as pink eye, urinary tract infections and hair loss, the retailer said.

Other retailers, including CVS to Walgreens to Walmart, have made similar moves.

Were you better off in 2022 than you were in 2017? I was for a lot of reasons. One thing that didn’t change over those five years, though, was my health insurance status. I had health insurance in 2017, and I had health insurance in 2022. And I still have health insurance today.

So do most Americans. In fact, according to the U.S. Census Bureau’s latest report on health insurance coverage in the U.S., 92.1% of us had some form of health insurance in 2022. That’s about 304 million people, per the report.

Conversely, 7.9% of us were uninsured last year. That’s a little more than 25.9 million people. That’s down from 8.3% and about 27.2 million people in 2021.

Some may see the decrease in both the percentage and number of uninsured as good news. And it is. Any time the uninsured figures go down, that’s good.

The bad news is, we’re back where we were in 2017. That’s also when 7.9% of us, or about 25.6 million people, were uninsured. Five years of trying to get more people insured and nothing to show for it.

The number of people with any type of private health insurance (employer-based or direct-purchase) crept up to 216.5 million last year from 216.4 million in 2021. The number of people with any type of public health insurance (Medicare, Medicaid, etc.) rose to 119.1 million last year from 117.1 million in 2021. Both headed in the right direction but too slow to push the uninsured rate significantly down.

If we want to get serious about achieving universal coverage, let’s get serious about it. If we don’t want to get serious about it because most of us already have health insurance, the only useful purpose of the Census Bureau’s annual reports on health insurance is to show us how little we really care.

The hospital workforce is critical to the care process and is most often the largest expense on a hospital or health system’s balance sheet. Even before the pandemic, labor expenses — which include costs associated with recruitment and retention, employee benefits and incentives — accounted for more than 50 percent of hospitals’ total expenses, according to the American Hospital Association.

As a result, a slight increase in labor costs can have a tremendous effect on a hospital or health system’s total expenses and operating margins. Hospitals across the country are focused on managing the premium cost of labor, while recruiting and retaining talent remains a priority, and the cost of supplies and drugs also increases due to inflation.

Here’s how 23 health systems’ labor costs are tracking based on the results of their most recent financial documents.

Note: This is not an exhaustive list. Most of the following health systems’ labor costs are for the three months ending 30, with others for the six months ending June 30 and the 12 months ending June 30 — the most recent periods for which financial data is available. The year-over-year percentage increase/decrease is also included.

21. CommonSpirit Health (Chicago) Salaries and benefits: $18.3 billion (+0.7 percent YOY) *For the 12 months ended June 30 **Merged with Broomfield, Colo. -based SCL Health in April 2022

22. Ascension (St. Louis) Salaries, wages and employee benefits: $14.3 billion (-1.3 percent YOY) *For the 12 months ended June 30