For many providers, 2023 provided a return to profitability (albeit at modest levels) following the devastating operating and investment losses experienced in 2022.Kaufman Hall’s National Hospital Flash Report data illustrated generally improving operating margins throughout the year, leveling off at 2.0% in November on a year-to-date basis.

This level of performance is commendable given 2022 and early 2023 margins, although it is still well below the 3% to 4% range which we believe is needed for long-term sustainability in the not-for-profit healthcare world. We may well have reached a point of stability with respect to operating performance, but at a lower level.

The question for hospital and health system leaders is whether this level of operating stability provides sustainability?

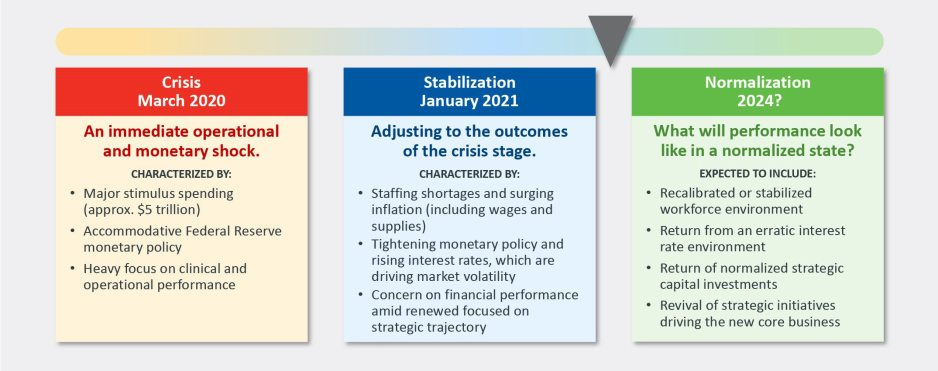

From stabilization to normalization

Since the pandemic began in 2020, the progress of recovery has been viewed over three phases: crisis, stabilization, and normalization. In last year’s outlook, we noted that we were in the midst of a potentially multi-year stabilization phase, which would continue to be marked with volatility—including ongoing labor market dislocations, inflationary pressures, and restrictive monetary policies. As we enter 2024, there are signs that we are now at the bridge between stabilization and normalization (Figure 1).

Figure 1: The Three Phases of Recovery from the Covid Pandemic

“The question for hospital and health system leaders is whether that level of stability provides sustainability?”

These signs include evidence that the first two indicators for normalization—a recalibrated or stabilized workforce environment and a return from an erratic interest rate environment—are coming into place. In our 2023 State of Healthcare Performance Improvement survey, respondents indicated that the spike in contract labor utilization that has been a dominant factor in operating expense increases was subsiding. Sixty percent of respondents said that utilization of contract labor was decreasing, and 36% said it was holding steady. Only 4% noted an increase in contract labor usage. Overall employee cost inflation seems to be subsiding as well: for all three labor categories in our survey (clinical, administrative, and support services), more organizations were able to hold salary increases to the 0% – 5% range in 2023 than in 2022.

There is good news on the interest rate front as well. After a series of rate increases in 2023, the Federal Reserve has held steady the last six months and has signaled rate cuts in 2024. Inflation has cooled markedly (albeit not yet at target levels), and employment rates have held steady. The Fed may have achieved a “soft landing” that satisfies its dual mandate of stable prices and maximum sustainable employment. Borrowing costs for not-for-profit hospital issuers have declined nearly 100 basis points in the last two months and we are expecting a return to more normal issuance levels in the first half of 2024.

There are other indications of normalization, including in the rating agencies’ outlooks for 2024. Regardless of the headline, all saw significant improvement in healthcare performance 2023.

The final answer to the question of whether the healthcare industry is entering the normalization phase likely will hinge on the last two indicators. Will we see a return of normalized strategic capital investments, and will we see a revival of strategic initiatives driving the core business (perhaps newly imagined)?

In effect, are health care systems simply surviving or are they thriving?

Looking forward, several factors could either bolster or undermine healthcare leaders’ confidence and willingness to resume a more normal level of investment in both capital needs and strategic growth. These include:

Politics and the 2024 elections. When North Carolina—a state that has traditionally leaned “red”—decided to opt into the Affordable Care Act’s (ACA’s) Medicaid expansion in 2023, it seemed that political debates over the ACA might be in the rearview mirror. But last November, former president Trump—currently the leading candidate for the Republican presidential nomination after strong wins in the Iowa caucuses and New Hampshire primary—indicated his intent to replace the ACA with something else. President Biden is now making protection and expansion of the ACA a key part of his 2024 campaign. What had appeared to be a settled issue may be a significant point of contention in the 2024 presidential election and beyond.

Although we do not anticipate any significant healthcare-related legislation in advance of the 2024 elections, healthcare leaders should be prepared for renewed attention to the costs of government-funded healthcare programs leading up to and following the elections. The national debt has increased rapidly over the past 20 years, tripling from $11 trillion in 2003 to $33 trillion in 2023. If the deficit and national debt become an important issue in the election, a move toward a balanced budget—akin to the Balanced Budget Act of 1997—post election could lead to further cuts to Medicare and Medicaid.

Temporary relief payments. Health systems continue to receive one-time cash infusions through the 340B settlement, Federal Emergency Management Agency (FEMA) payments and other governmental programs. Approximately 1,600 hospitals have or will be receiving a lump-sum payment to compensate them for a change in the Department of Health & Human Services’ (HHS’s) reimbursement rates for the 340B program from 2018 to 2022, which was ruled unlawful by the Supreme Court in a 2022 decision. The total amount to be distributed is approximately $9 billion and began hitting bank accounts in January 2024.

But what the right hand giveth, the left hand taketh away. Budget neutrality requirements will force HHS to recoup this offset—amounting to approximately $7.8 billion—which it will do by reducing payments for non-drug items and services to all Outpatient Prospective Payment System (OPPS) providers by 0.5% until the offset has been fully recouped, beginning in calendar year 2026. HHS estimates that this process will take approximately 16 years. Is this a harbinger of lower payments on other key governmental programs?

Many hospitals also continue to receive Covid-related payments from FEMA for expenses occurred during the pandemic. In addition, state supplemental payments—especially under Medicaid managed care and fee-for-service programs—are providing some relief. The Centers for Medicare & Medicaid Services has issued a proposed rule, however, that would limit states’ use of provider-based funding sources, such as provider taxes, and cap the rate of growth for state-directed payments.

As all of these payment programs dry up over the next few years, hospitals will need to replace the revenue and/or get leaner on the expense side in order to maintain today’s level of performance.

The hollowing of the commercial health insurance market. Our colleague, Joyjit Saha Choudhury, recently published a blog on the hollowing of the commercial health insurance market, driven by long-term concerns over the affordability of healthcare. While volumes have been recovering to pre-pandemic levels, this hollowing threatens the loss of the most profitable volumes and will pressure hospitals and health systems to create and deliver value, compete for inclusion in narrow networks, and develop more direct relationships with the employer community.

Related, the growing penetration of Medicare Advantage plans is reducing the number of traditional Medicare beneficiaries. Many CFOs report that these programs can be the most difficult with which to work given their high denial rates and required pre-authorization rates. A new rule requiring insurers to streamline prior authorizations for Medicare Advantage, Medicaid, and Affordable Care Act plans may help alleviate this issue; however, it will be incumbent upon management teams to stay ahead of them. Aging demographics are also reducing the percentage of commercially insured patients for many hospitals and health systems, further exacerbating the problem. This combination of fewer commercial patients (who often subsidize governmental patients) and more pressure on receiving the duly owed commercial revenue threatens to be an ongoing headache for management teams.

Ongoing impact of the Baby Boom generation. Despite the good news on inflation—and indications that the Fed may begin lowering interest rates in 2024—the economy is by no means out of the woods yet. The Baby Boom generation, which holds more than 50% of the wealth in the U.S. and is seemingly price agnostic, still has many years of spending ahead, in healthcare and general purchasing. This will likely continue to pressure inflation, especially in the healthcare sector, where demand will continue to grow. As the generation starts to shrink, the resulting wealth transfer will be the largest ever in our country’s history and have profound (and unforeseen) consequences on the overall economy and healthcare in general.

In sum, these other factors will continue to affect the sector (both positively and negatively) and require health system management teams to navigate an everchanging world. While many signs point toward short-term relief, the longer-term challenges persist. Improvements in the short term may, however, provide the opportunity to reposition organizations for the future.

How hospitals and health systems should respond

Healthcare leaders should view ongoing uncertainty in the political and economic climate as a tailwind as much as a headwind. This uncertainty, in other words, should be a motivation to put in place strategies that will buffer healthcare organizations from potential bumps in the road ahead. Setting balance sheet strategy should be a part of an organization’s planning process.

How an organization sets that strategy, measures its performance, and makes improvements will set apart top-performing organizations.

Although heightened debt issuance early in 2024 signals a return for many systems to a climate of investment, there is still limited energy around strategy and debt conversations in many boardrooms, especially in those organizations where financial improvement continues to lag. The last two years have illustrated that hospitals and health systems will not be able to cut their way to profitability. Lackluster performance cannot and will not improve without some level of strategic change, whether it is through market share gains, payer mix shift, or operational improvements. This strategic change requires investment and investment requires capital. Capital can be obtained in many forms—whether through growth in capital reserves, improved cash flow, or new debt issuance—but is essential for change. Reengaging in conversations about strategy and growth should be an imperative in 2024 and will require reexamining how that growth is funded.

Healthcare leaders should engage their partners as they continue or refocus on:

Changing the conversation from debt capacity to capital capacity. Management teams need to determine what they can afford to spend on capital if the new normal of cash flow will be constrained going forward. Capital capacity is and should be agnostic to the source of that capital, such as debt, cash flow from operations, or liquidity reserves. Healthcare leaders must focus on what they can spend, before deciding how to fund that spending. The conversation will need to balance investment for the future with maintaining key credit metrics in the short term.

Conducting a capitalization analysis. Separate but related to the previous entry, how much leverage should your organization have relative to its overall capitalization? Ostensibly, many organizations have been paying principal while curtailing borrowing needs, so capitalization may have improved. While that may be the case, many organizations have depleted reserves and/or experienced investment losses that have reduced capitalization. Understanding where the organization stands is an essential next step.

Evaluating surplus return. Consider surplus return as investment income net of interest expense. Organizations should evaluate their ability to reliably generate both operating cash flow and net surplus. How an organization’s balance sheet is positioned to generate returns and manage risk will be a critical success factor.

Focusing on the metrics that matter. These include operating cashflow margin, cash to debt, debt to revenue, and days cash on hand. As key metrics for rating analysts and investors continue to evolve, management teams need to make sure they are focused on the correct numbers. The discussion should be dually focused on ensuring adequate-to-ample headroom to basic financial covenants as well as a comparison to key medians and peers. Strong financial planning will address how these metrics can be improved over time through synergies, growth, and diversification strategies.

Although it has been a difficult few years, hospitals and health systems seem to have moved onto a more stable footing over the last twelve months. In order to build upon the upward trajectory, now is the time to harness strategy, planning, and investment to move organizations from stability to sustainability.

A new perspective on how technology, transformation efforts, and other changes have affected payers, health systems, healthcare services and technology, and pharmacy services.

The acute strain from labor shortages, inflation, and endemic COVID-19 on the healthcare industry’s financial health in 2022 is easing. Much of the improvement is the result of transformation efforts undertaken over the last year or two by healthcare delivery players, with healthcare payers acting more recently. Even so, health-system margins are lagging behind their financial performance relative to prepandemic levels. Skilled nursing and long-term-care profit pools continue to weaken. Eligibility redeterminations in a strong employment economy have hurt payers’ financial performance in the Medicaid segment. But Medicare Advantage and individual segment economics have held up well for payers.

As we look to 2027, the growth of the managed care duals population (individuals who qualify for both Medicaid and Medicare) presents one of the most substantial opportunities for payers. On the healthcare delivery side, financial performance will continue to rebound as transformation efforts, M&A, and revenue diversification bear fruit. Powered by adoption of technology, healthcare services and technology (HST) businesses, particularly those that offer measurable near-term improvements for their customers, will continue to grow, as will pharmacy services players, especially those with a focus on specialty pharmacy.

Below, we provide a perspective on how these changes have affected payers, health systems, healthcare services and technology, and pharmacy services, and what to expect in 2024 and beyond.

The fastest growth in healthcare may occur in several segments

We estimate that healthcare profit pools will grow at a 7 percent CAGR, from $583 billion in 2022 to $819 billion in 2027. Profit pools continued under pressure in 2023 due to high inflation rates and labor shortages; however, we expect a recovery beginning in 2024, spurred by margin and cost optimization and reimbursement-rate increases.

Several segments can expect higher growth in profit pools:

Within payer, Medicare Advantage, spurred by the rapid increase in the duals population; the group business, due to recovery of margins post-COVID-19 pandemic; and individual

Within health systems, outpatient care settings such as physician offices and ambulatory surgery centers, driven by site-of-care shifts

Within HST, the software and platforms businesses (for example, patient engagement and clinical decision support)

Within pharmacy services, with specialty pharmacy continuing to experience rapid growth

On the other hand, some segments will continue to see slow growth, including general acute care and post-acute care within health systems, and Medicaid within payers (Exhibit 1).

Several factors will likely influence shifts in profit pools. Two of these are:

Change in payer mix. Enrollment in Medicare Advantage, and particularly the duals population, will continue to grow. Medicare Advantage enrollment has grown historically by 9 percent annually from 2019 to 2022; however, we estimate the growth rate will reduce to 5 percent annually from 2022 to 2027, in line with the latest Centers for Medicare & Medicaid Services (CMS) enrollment data.1 Finally, the duals population enrolled in managed care is estimated to grow at more than a 9 percent CAGR from 2022 through 2027.

We also estimate commercial segment profit pools to rebound as EBITDA margins likely return to historical averages by 2027. Growth is likely to be partially offset by enrollment changes in the segment, prompted by a shift from fully insured to self-insured businesses that could accelerate as employers seek to cut costs if the economy slows. Individual segment profit pools are estimated to expand at a 27 percent CAGR from 2022 to 2027 as enrollment rises, propelled by enhanced subsidies, Medicaid redeterminations, and other potential favorable factors (for example, employer conversions through the Individual Coverage Health Reimbursement Arrangement offered by the Affordable Care Act); EBITDA margins are estimated to improve from 2 percent in 2022 to 5 to 7 percent in 2027. On the other hand, Medicaid enrollment could decline by about ten million lives over the next five years based on our estimates, given recent legislation allowing states to begin eligibility redeterminations (which were paused during the federal public health emergency declared at the start of the COVID-19 pandemic2).

Accelerating value-based care (VBC). Based on our estimates, 90 million lives will be in VBC models by 2027, from 43 million in 2022. This expansion will be fueled by an increase in commercial VBC adoption, greater penetration of Medicare Advantage, and the Medicare Shared Savings Program (MSSP) model in Medicare fee-for-service. Also, substantial growth is expected in the specialty VBC model, where penetration in areas like orthopedics and nephrology could more than double in the next five years.

VBC models are undergoing changes as CMS updates its risk adjustment methodology and as models continue to expand beyond primary care to other specialties (for example, nephrology, oncology, and orthopedics). We expect established models that offer improvements in cost and quality to continue to thrive. The transformation of VBC business models in response to pressures from the current changes could likely deliver outsized improvement in cost and quality outcomes. The penetration of VBC business models is likely to lead to shifts in health delivery profit pools, from acute-care settings to other sites of care such as ambulatory surgical centers, physician offices, and home settings.

Payers: Government segments are expected to be 65 percent larger than commercial segments by 2027

In 2022, overall payer profit pools were $60 billion. Looking ahead, we estimate EBITDA to grow to $78 billion by 2027, a 5 percent CAGR, as the market recovers and approaches historical trends. Drivers are likely to be margin recovery of the commercial segment, inflation-driven incremental premium rate rises, and increased participation in managed care by the duals population. This is likely to be partially offset by margin compression in Medicare Advantage due to regulatory pressures (for example, risk adjustment, decline in the Stars bonus, and technical updates) and membership decline in Medicaid resulting from the expiration of the public health emergency.

We estimate increased labor costs and administrative expenses to reduce payer EBITDA by about 60 basis points in 2023. In addition, health systems are likely to push for reimbursement rate increases (up to about 350 to 400 basis-point incremental rate increases from 2023 to 2027 for the commercial segment and about 200 to 250 basis points for the government segment), according to McKinsey analysis and interviews with external experts.3

Our estimates also suggest that the mix of payer profit pools is likely to shift further toward the government segment (Exhibit 2). Overall, the profit pools for this segment are estimated to be about 65 percent greater than the commercial segment by 2027 ($36 billion compared with $21 billion). This shift would be a result of increasing Medicare Advantage penetration, estimated to reach 52 percent in 2027, and likely continued growth in the duals segment, expanding EBITDA from $7 billion in 2022 to $12 billion in 2027.

Profit pools for the commercial segment declined from $18 billion in 2019 to $15 billion in 2022. We now estimate the commercial segment’s EBITDA margins to regain historical levels by 2027, and profit pools to reach $21 billion, growing at a 7 percent CAGR from 2022 to 2027. Within this segment, a shift from fully insured to self-insured businesses could accelerate in the event of an economic slowdown, which prompts employers to pay greater attention to costs. The fully insured group enrollment could drop from 50 million in 2022 to 46 million in 2027, while the self-insured segment could increase from 108 million to 113 million during the same period.

Health systems: Transformation efforts help accelerate EBITDA recovery

In 2023, health-system profit pools continued to face substantial pressure due to inflation and labor shortages. Estimated growth was less than 5 percent from 2022 to 2023, remaining below prepandemic levels. Health systems have undertaken major transformation and cost containment efforts, particularly within the labor force, helping EBITDA margins recover by up to 100 basis points; some of this recovery was also volume-driven.

Looking ahead, we estimate an 11 percent CAGR from 2023 to 2027, or total EBITDA of $366 billion by 2027 (Exhibit 3). This reflects a rebound from below the long-term historical average in 2023, spurred by transformation efforts and potentially higher reimbursement rates. We anticipate that health systems will likely seek reimbursement increases in the high single digits or higher upon contract renewals (or more than 300 basis points above previous levels) in response to cost inflation in recent years.

Measures to tackle rising costs include improving labor productivity and the application of technological innovation across both administration and care delivery workflows (for example, further process standardization and outsourcing, increased use of digital care, and early adoption of AI within administrative workflows such as revenue cycle management). Despite these measures, 2027 industry EBITDA margins are estimated to be 50 to 100 basis points lower than in 2019, unless there is material acceleration in performance transformation efforts.

There are some meaningful exceptions to this overall outlook for health systems. Although post-acute-care profit pools could be severely affected by labor shortages (particularly nurses), other sites of care might grow (for example, non-acute and outpatient sites such as physician offices and ambulatory surgery centers). We expect accelerated adoption of VBC to drive growth.

HST profit pools will grow in technology-based segments

HST is estimated to be the fastest-growing sector in healthcare. In 2021, we estimated HST profit pools to be $51 billion. In 2022, according to our estimates, the HST profit pool shrank to $49 billion, reflecting a contracting market, wage inflation pressure, and the drag of fixed-technology investment that had not yet fulfilled its potential. Looking ahead, we estimate a 12 percent CAGR in 2022–27 due to the long-term underlying growth trend and rebound from the pandemic-related decline (Exhibit 4). With the continuing technology adoption in healthcare, the greatest acceleration is likely to happen in software and platforms as well as data and analytics, with 15 percent and 22 percent CAGRs, respectively.

In 2023, we observed an initial recovery in the HST market, supported by lower HST wage pressure and continued adoption of technology by payers and health systems searching for ways to become more efficient (for example, through automation and outsourcing).

Three factors account for the anticipated recovery and growth in HST.First, we expect continued demand from payers and health systems searching to improve efficiency, address labor challenges, and implement new technologies (for example, generative AI). Second, payers and health systems are likely to accept vendor price increases for solutions delivering measurable improvements. Third, we expect HST companies to make operational changes that will improve HST efficiency through better technology deployment and automation across services.

Pharmacy services will continue to grow

The pharmacy market has undergone major changes in recent years, including the impact of the COVID-19 pandemic, the establishment of partnerships across the value chain, and an evolving regulatory environment. Total pharmacy dispensing revenue continues to increase, growing by 9 percent to $550 billion in 2022,4 with projections of a 5 percent CAGR, reaching $700 billion in 2027.5Specialty pharmacy is one of the fastest growing subsegments within pharmacy services and accounts for 40 percent of prescription revenue6; this subsegment is expected to reach nearly 50 percent of prescription revenue in 2027 (Exhibit 5). We attribute its 8 percent CAGR in revenue growth to increases in utilization and pricing as well as the continued expansion of pipeline therapies (for example, cell and gene therapies and oncology and rare disease therapies) and expect that the revenue growth will be partially offset by reimbursement pressures, specialty generics, and increased adoption of biosimilars. Specialty pharmacy dispensers are also facing an evolving landscape with increased manufacturer contract pharmacy pressures related to the 340B Drug Pricing Program. With restrictions related to size and location of contract pharmacies that covered entities can use, the specialty pharmacy subsegment has seen accelerated investment in hospital-owned pharmacies.

Retail and mail pharmacies continue to face margin pressure and a contraction of profit pools due to reimbursement pressure, labor shortages, inflation, and a plateauing of generic dispensing rates.7Many chains have recently announced8 efforts to rationalize store footprints while continuing to augment additional services, including the provision of healthcare services.

Over the past year, there has also been increased attention to broad-population drugs such as GLP-1s (indicated for diabetes and obesity). The number of patients meeting clinical eligibility criteria for these drugs is among the largest of any new drug class in the past 20 to 30 years. The increased focus on these drugs has amplified conversations about care and coverage decisions, including considerations around demonstrated adherence to therapy, utilization management measures, and prescriber access points (for example, digital and telehealth services). As we look ahead, patient affordability, cost containment, and predictability of spending will likely remain key themes in the sector.The Inflation Reduction Act is poised to change the Medicare prescription Part D benefit, with a focus on reducing beneficiary out-of-pocket spending, negotiating prices for select drugs, and incentivizing better management of high-cost drugs. These changes, coupled with increased attention to broad-population drugs and the potential of high-cost therapies (such as cell and gene therapies), have set the stage for a shift in care and financing models.

The US healthcare industry faced demanding conditions in 2023, including continuing high inflation rates, labor shortages, and endemic COVID-19. However, the industry has adapted. We expect accelerated improvement efforts to help the industry address its challenges in 2024 and beyond, leading to an eventual return to historical-average profit margins.

This discussion was recorded on November 16, 2023. This transcript has been edited for clarity.

Robert D. Glatter, MD: Welcome. I’m Dr Robert Glatter, medical advisor for Medscape Emergency Medicine. Joining me today is Dr Brian Miller, a hospitalist with Johns Hopkins University School of Medicine and a health policy expert, to discuss the current and renewed interest in physician-owned hospitals.

Welcome, Dr Miller. It’s a pleasure to have you join me today.

Brian J. Miller, MD, MBA, MPH: Thank you for having me.

History and Controversies Surrounding Physician-Owned Hospitals

Miller: Thank you. I should note that my views are my own and don’t represent those of Hopkins or the American Enterprise Institute, where I’m a nonresident fellow nor the Medicare Payment Advisory Commission, of which I’m a Commissioner.

The story about physician-owned hospitals is an interesting one. Hospitals turned into health systems in the 1980s and 1990s, and physicians started to shift purely from an independent model into a more organized group practice or employed model. Physicians realized that they wanted an alternative operating arrangement. You want a choice of how you practice and what your employment is. And as community hospitals started to buy physicians and also establish their own physician groups de novo, physicians opened physician-owned hospitals.

Physician-owned hospitals fell into a couple of buckets. One is what we call community hospitals, or what the antitrust lawyers would call general acute care hospitals: those offering emergency room (ER) services, labor and delivery, primary care, general surgery — the whole regular gamut, except that some of the owners were physicians.

The other half of the marketplace ended up being specialty hospitals: those built around a specific medical specialty and series of procedures and chronic care. For example, cardiac hospitals often do CABG, TAVR, maybe abdominal aortic aneurysm (triple A) repairs, and they have cardiology clinics, cath labs, a cardiac intensive care unit (ICU), ER, etc. There were also orthopedic surgical specialty hospitals, which were sort of like an ambulatory surgery center (ASC) plus several beds. Then there were general surgical specialty hospitals. At one point, there were some women’s health–focused specialty hospitals.

The hospital industry, of course, as you can understand, didn’t exactly like this. They had a series of concerns about what we would historically call cherry-picking or lemon-dropping of patients. They were worried that physician-owned facilities didn’t want to serve public payer patients, and there was a whole series of reports and investigations.

Around the time the Affordable Care Act passed, the hospital industry had many concerns about physician-owned specialty hospitals, and there was a moratorium as part of the 2003 Medicare Modernization Act. As part of the bargaining over the hospital industry support for the Affordable Care Act, they traded their support for, among other things, their number one priority, which is a statutory prohibition on new or expanded physician-owned hospitals from participating in Medicare. That included both physician-owned community hospitals and physician-owned specialty hospitals.

Glatter: I guess the main interest is that, when physicians have an ownership or a stake in the hospital, this is what the Stark laws obviously were aimed at. That was part of the impetus to prevent physicians from referring patients where they had an ownership stake. Certainly, hospitals can be owned by attorneys and nonprofit organizations, and certainly, ASCs can be owned by physicians. There is an ongoing issue in terms of physicians not being able to have an ownership stake. In terms of equity ownership, we know that certain other models allow this, but basically, it sounds like this is an issue with Medicare. That seems to be the crux of it, correct?

Miller: Yes. I would also add that it’s interesting when we look at other professions. When we look at lawyers, nonlawyers are actually not allowed to own an equity stake in a law practice. In many other professions, you either have corporate ownership or professional ownership, or the alternative is you have only professional ownership.I would say the hospital industry is one of the few areas where professional ownership not only is not allowed, but also is statutorily prohibited functionally through the Medicare program.

Unveiling the Dynamics of Hospital Ownership

Glatter: A recent study done by two PhDs looked at 2019 data on 20 of the most expensive diagnosis-related groups (DRGs). It examined the cost savings, and we’re talking over $1 billion in expenditures when you look at the data from general acute care hospitals vs physician-owned hospitals. This is what appears to me to be a key driver of the push to loosen restrictions on physician-owned hospitals. Isn’t that correct?

Miller: I would say that’s one of many components. There’s more history to this issue. I remember sitting at a think tank talking to someone several years ago about hospital consolidation as an issue. We went through the usual levers that us policy wonks go through. We talked about antitrust enforcement, certificate of need, rising hospital costs from consolidation, lower quality (or at least no quality gains, as shown by a New England Journal of Medicine study), and decrements in patient experience that result from the diseconomies of scale. They sort of pooh-poohed many of the policy ideas. They basically said that there was no hope for hospital consolidation as an issue.

Well, what about physician ownership? I started with my research team to comb through the literature and found a variety of studies — some of which were sort of entertaining, because they’d do things like study physician-owned specialty hospitals, nonprofit-owned specialty hospitals, and for-profit specialty hospitals and compare them with nonprofit or for-profit community hospitals, and then say physician-owned hospitals that were specialty were bad.

They mixed ownership and service markets right there in so many ways, I’m not sure where to start. My team did a systematic review of around 30 years of research, looking at the evidence base in this space. We found a couple of things.

We found that physician-owned community hospitals did not have a cost or quality difference, meaning that there was no definitive evidence that the physician-owned community hospitals were cheaper based on historical evidence, which was very old. That means there’s not specific harm from them. When you permit market entry for community hospitals, that promotes competition, which results in lower prices and higher quality.

Then we also looked at the specialty hospital markets — surgical specialty hospitals, orthopedic surgical specialty hospitals, and cardiac hospitals. We noted for cardiac hospitals, there wasn’t clear evidence about cost savings, but there was definitive evidence of higher quality, from things like 30-day mortality for significant procedures like treatment of acute MI, triple A repair, stuff like that.

For orthopedic surgical specialty hospitals, we noted lower costs and higher quality, which again fits with operationally what we would know. If you have a facility that’s doing 20 total hips a day, you’re creating a focused factory. Just like if you think about it for interventional cardiology, your boards have a minimum number of procedures that you have to do to stay certified because we know about the volume-quality relationship.

Then we looked at general surgical specialty hospitals. There wasn’t enough evidence to make a conclusive thought about costs, and there was a clear trend toward higher quality. I would say this recent study is important, but there is a whole bunch of other literature out there, too.

Exploring the Scope of Emergency Care in Physician-Owned Hospitals

One thing I want to bring up — and this is an important issue — is that the risk for patients has been talked about by the American Hospital Association and the Federation of American Hospitals, in terms of limited or no emergency services at such physician-owned hospitals and having to call 911 when patients need emergent care or stabilization. That’s been the rebuttal, along with an Office of Inspector General (OIG) report from 2008. Almost, I guess, three quarters of the patients that needed emergent care got this at publicly funded hospitals.

Miller: I’m familiar with the argument about emergency care. If you actually go and look at it, it differs by specialty market. Physician-owned community hospitals have ERs because that’s how they get their business. If you are running a hospital medicine floor, a general surgical specialty floor, you have a labor delivery unit, a primary care clinic, and a cardiology clinic. You have all the things that all the other hospitals have. The physician-owned community hospitals almost uniformly have an ER.

When you look at the physician-owned specialty hospitals, it’s a little more granular. If you look at the cardiac hospitals, they have ERs. They also have cardiac ICUs, operating rooms, etc. The area where the hospital industry had concerns — which I think is valid to point out — is that physician-owned orthopedic surgical specialty hospitals don’t have ERs. But this makes sense because of what that hospital functionally is: a factory for whatever the scope of procedures is, be it joint replacements or shoulder arthroscopy. The orthopedic surgical specialty hospital is like an ASC plus several hospital beds. Many of those did not have ERs because clinically it didn’t make sense.

What’s interesting, though, is that the hospital industry also operates specialty hospitals. If you go into many of the large systems, they have cardiac specialty hospitals and cancer specialty hospitals. I would say that some of them have ERs, as they appropriately should, and some of those specialty hospitals do not. They might have a community hospital down the street that’s part of that health system that has an ER, but some of the specialty hospitals don’t necessarily have a dedicated ER.

I agree, that’s a valid concern. I would say, though, the question is, what are the scope of services in that hospital? Is an ER required? Community hospitals should have ERs. It makes sense also for a cardiac hospital to have one. If you’re running a total joint replacement factory, it might not make clinical sense.

Glatter: The patients who are treated at that hospital, if they do have emergent conditions, need to have board-certified emergency physicians treating them, in my view because I’m an ER physician. Having surgeons that are not emergency physicians staff a department at a specialty orthopedic hospital or, say, a cancer hospital is not acceptable from my standpoint. That’s my opinion and recommendation, coming from emergency medicine.

Miller: I would say that anesthesiologists are actually highly qualified in critical care. The question is about clinical decompensation; if you’re doing a procedure, you have an anesthesiologist right there who is capable of critical care. The function of the ER is to either serve as a window into the hospital for patient volume or to serve as a referral for emergent complaints.

Glatter: An anesthesiologist — I’ll take issue with that — does not have the training of an emergency physician in terms of scope of practice.

Miller: My anesthesiology colleagues would probably disagree for managing an emergency during an operating room case.

Glatter: Fair enough, but I think in the general sense. The other issue is that, in terms of emergent responses to patients that decompensate, when you have to transfer a patient, that violates Medicare requirements. How is that even a valid issue or argument if you’re going to have to transfer a patient from your specialty hospital? That happens. Again, I know that you’re saying these hospitals are completely independent and can function, stabilize patients, and treat emergencies, but that’s not the reality across the country, in my opinion.

Miller: I don’t think that’s the case for the physician-owned specialty cardiac hospitals, for starters. Many of those have ICUs in addition to operating rooms as a matter of routine in addition to ERs. I don’t think that’s the case for physician-owned community hospitals, which have ERs, ICUs, medicine floors, and surgical floors. Physician-owned community hospitals are around half the market. Of that remaining market, a significant percentage are cardiac hospitals. If you’re taking an issue with orthopedic surgical specialty hospitals, that’s a clinical operational question that can and should be answered.

I’d also posit that the nonprofit and for-profit hospital industries also operate specialty hospitals. Any of these questions, we shouldn’t just be asking about physician-owned facilities; we should be asking about them across ownership types, because we’re talking about scope of service and quality and safety. The ownership in that case doesn’t matter. The broader question is, are orthopedic surgical specialty hospitals owned by physicians, tax-exempt hospitals, or tax-paying hospitals? Is that a valid clinical business model? Is it safe? Does it meet Medicare conditions of participation? I would say that’s what that question is, because other ownership models do operate those facilities.

Glatter: You make some valid points, and I do agree on some of them. I think that, ultimately, these models of care, and certainly cost and quality, are issues. Again, it goes back to being able, in my opinion, to provide emergent care, which seems to me a very important issue.

Miller: I agree that providing emergent care is an issue. It’s an issue in any site of care. The hospital industry posits that all hospital outpatient departments (HOPDs) have emergent care. I can tell you, having worked in HOPDs (I’ve trained in them during residency), the response if something emergent happens is to either call 911 or wheel the patient down to the ER in a wheelchair or stretcher. I think that these hospital claims about emergency care coverage —these are important questions, but we should be asking them across all clinical settings and say what is the appropriate scope of care provided? What is the appropriate level of acuity and ability to provide emergent or critical care? That’s an important question regardless of ownership model across the entire industry.

Deeper Dive Into Data on Physician-Owned Hospitals

Glatter: We need to really focus on that. I’ll agree with you on that.

There was a March 2023 report from Dobson | DaVanzo. It showed that physician-owned hospitals had lower Medicaid, dual-eligible, and uncompensated care and charity care discharges than full-service acute care hospitals. Physician-owned hospitals had less than half the proportion of Medicaid discharges compared with non–physician-owned hospitals. They were also less likely to care for dual-eligible patients overall compared with non–physician-owned hospitals.

In addition, when COVID hit, the physician-owned hospitals overall — and again, there may be exceptions — were not equipped to handle these patient surges in the acute setting of a public health emergency. There was a hospital in Texas that did pivot that I’m aware of — Renaissance Hospital, which ramped up a long-term care facility to become a COVID hospital — but I think that’s the exception. I think this report raises some valid concerns; I’ll let you rebut that.

Miller: A couple of things. One, I am not aware that there’s any clear market evidence or a systematic study that shows that physician-owned hospitals had trouble responding to COVID. I don’t think that assertion has been proven. The study was funded by the hospital industry. First of all, it was not a peer-reviewed study; it was funded by an industry that paid a consulting firm. It doesn’t mean that we still shouldn’t read it, but that brings bias into question. The joke in Washington is, pick your favorite statistician or economist, and they can say what you want and have a battle of economists and statisticians.

For example, in that study, they didn’t include the entire ownership universe of physician-owned hospitals. If we go to the peer-reviewed literature, there’s a great 2015 BMJ paper showing that the Medicaid payer mix is actually the same between physician-owned hospitals vs not. The mix of patients by ethnicity — for example, think about African American patients — was the same. I would be more inclined to believe the peer-reviewed literature in BMJ as opposed to an industry-funded study that was not peer-reviewed and not independent and has methodological questions.

Glatter: Those data are 8 years old, so I’d like to see more recent data. It would be interesting, just as a follow-up to that, to see where the needle has moved — if it has, for that matter — in terms of Medicaid patients that you’re referring to.

Miller: I tend to be skeptical of all industry research, regardless of who published it, because they have an economic incentive. If they’re selecting certain age groups or excluding certain hospitals, that makes you wonder about the validity of the study. Your job as an industry-funded researcher is that, essentially, you’re being paid to look for an answer. It’s not necessarily an honest evaluation of the data.

Glatter: I want to bring up another point about the Hospital Readmissions Reduction Program (HRRP) and the data on how physician-owned hospitals compared with acute care hospitals that are non–physician-owned and have you comment on that. The Dobson | DaVanzo study called into question that physician-owned hospitals treat fewer patients who are dual-eligible, which we know.

Miller: I don’t think we do know that.

Glatter: There are data that point to that, again, looking at the studies.

Miller: I’m saying that’s a single study funded by industry as opposed to an independent, academic, peer-reviewed literature paper. That would be like saying, during the debate of the Inflation Reduction Act (IRA), that you should read the pharmaceutical industries research but take any of it at pure face value as factual. Yes, we should read it. Yes, we should evaluate it on its own merits. I think, again, appropriately, you need to be concerned when people have an economic incentive.

The question about the HRRP I’m going to take a little broader, because I think that program is unfair to the industry overall. There are many factors that drive hospital readmission. Whether Mrs Smith went home and ate potato chips and then took her Lasix, that’s very much outside of the hospital industry’s control, and there’s some evidence that the HRRP increases mortality in some patient populations.

In terms of a quality metric, it’s unfair to the industry. I think we took an operating process, internal metric for the hospital industry, turned it into a quality metric, and attached it to a financial bonus, which is an inappropriate policy decision.

Rethinking Ownership Models and Empowering Clinicians

Glatter: I agree with you on that. One thing I do want to bring up is that whether the physician-owned hospitals are subject to many of the quality measures that full-service, acute care hospitals are. That really is, I think, a broader context.

Miller: Fifty-five percent of physician-owned hospitals are full-service community hospitals, so I would say at least half the market is 100% subject to that.

Glatter: If only 50% are, that’s already an issue.

Miller: Cardiac specialty hospitals — which, as I said, nonprofit and for-profit hospital chains also operate — are also subject to the appropriate quality measures, readmissions, etc. Just because we don’t necessarily have the best quality measurement in the system in the country, it doesn’t mean that we shouldn’t allow care specialization. As I’d point out, if we’re concerned about specialty hospitals, the concern shouldn’t just be about physician-owned specialty hospitals; it should be about specialty hospitals by and large. Many health systems run cardiac specialty hospitals, cancer specialty hospitals, and orthopedic specialty hospitals. If we’re going to have a discussion about concerns there, it should be about the entire industry of specialty hospitals.

I think specialty hospitals serve an important role in society, allowing for specialization and exploiting in a positive way the volume-quality relationship. Whether those are owned by a for-profit publicly traded company, a tax-exempt facility, or physicians, I think that is an important way to have innovation and care delivery because frankly, we haven’t had much innovation in care delivery. Much of what we do in terms of how we practice clinically hasn’t really changed in the 50 years since my late father graduated from medical school. We still have rounds, we’re still taking notes, we’re still operating in the same way. Many processes are manual. We don’t have the mass production and mass customization of care that we need.

When you have a focused factory, it allows you to design care in a way that drives up quality, not just for the average patient but also the patients at the tail ends, because you have time to focus on that specific service line and that specific patient population.

Physician-owned community hospitals offer an important opportunity for a different employment model. I remember going to the dermatologist and the dermatologist was depressed, shuffling around the room, sad, and I asked him why. He said he didn’t really like his employer, and I said, “Why don’t you pick another one?” He’s like, “There are only two large health systems I can work for. They all have the same clinical practice environment and functionally the same value.”

Physicians are increasingly burned out. They face monopsony power in who purchases their labor. They have little control. They don’t want to go through five committees, seven administrators, and attend 25 meetings just to change a single small process in clinical operations. If you’re an owner operator, you have a much better ability to do it.

Frankly, when many facilities do well now, when they do well clinically and do well financially, who benefits? The hospital administration and the hospital executives. The doctors aren’t benefiting. The nurses aren’t benefiting. The CNA is not benefiting. The secretary is not benefiting. The custodian is not benefiting. Shouldn’t the workers have a right to own and operate the business and do well when the business does well serving the community? That puts me in the weird space of agreeing with both conservatives and progressives.

Glatter: I agree with you. I think an ownership stake is always attractive. It helps with retention of employed persons. There’s no question that, when they have a stake, when they have skin in the game, they feel more empowered. I will not argue with you about that.

Miller: We don’t have business models where workers have that option in healthcare. Like the National Academy of Medicine said, one of the key drivers of burnout is the externalization of the locus of control over clinical practice, and the current business operating models guarantee an externalization of the locus of control over clinical practice.

If you actually look at the recent American Medical Association (AMA) meeting, there was a resolution to ban the corporate practice of medicine. They wanted to go more toward the legal professions model where only physicians can own and operate care delivery.

Miller: It’s not just doctors. I think nurses want a better lifestyle. The nurses are treated as interchangeable lines on a spreadsheet. The nurses are an integral part of our clinical team. Why don’t we work together as a clinical unit to build a better delivery system? What better way to do that than to have clinicians in charge of it, right?

My favorite bakery that’s about 30 minutes away is owned by a baker. It is not owned by a large tax-exempt corporation. It’s owned by an owner operator who takes pride in their work. I think that is something that the profession would do well to return to. When I was a resident, one of my colleagues was already planning their retirement. That’s how depressed they were.

I went into medicine to actually care for patients. I think that we can make the world a better place for our patients. What that means is not only treating them with drugs and devices, but also creating a delivery system where they don’t have to wander from lobby to lobby in a 200,000 square-foot facility, wait in line for hours on end, get bills 6 months later, and fill out endless paper forms over and over again.

All of these basic processes in healthcare delivery that are broken could have and should have been fixed — and have been fixed in almost every other industry. I had to replace one of my car tires because I had a flat tire. The local tire shop has an app, and it sends me SMS text messages telling me when my appointment is and when my car is ready. We have solved all of these problems in many other businesses.

We have not solved them in healthcare delivery because, one, we have massive monopolies that are raising prices, have lower quality, and deliver a crappy patient experience, and we have also subjugated the clinical worker into a corporate automaton. We are functionally drones. We don’t have the agency and the authority to improve clinical operations anymore. It’s really depressing, and we should have that option again.

I trust my doctor. I trust the nurses that I work with, and I would like them to help make clinical decisions in a financially responsible and a sensible operational manner. We need to empower our workforce in order to do that so we can recapture the value of what it means to be a clinician again.

The current model of corporate employment: massive scale, more administrators, more processes, more emails, more meetings, more PowerPoint decks, more federal subsidies. The hospital industry has choices. It can improve clinical operations. It can show up in Washington and lobby for increased subsidies. It can invest in the market and not pay taxes for the tax-exempt facilities. Obviously, it makes the logical choices as an economic actor to show up, lobby for increased subsidies, and then also invest in the stock market.

Improving clinical operations is hard. It hasn’t happened. The Bureau of Labor Statistics shows that the private community hospital industry has had flat labor productivity growth, on average, for the past 25 years, and for some years it even declined. This is totally atypical across the economy.

We have failed our clinicians, and most importantly, we have failed our patients. I’ve been sick. My relatives have been sick, waiting hours, not able to get appointments, and redoing forms. It’s a total disaster. It’s time and reasonable to try an alternative ownership and operating model. There are obviously problems. The problems can and should be addressed, but it doesn’t mean that we should have a statutory prohibition on professionals owning and operating their own business.

Glatter: There was a report that $500 million was saved by limiting or banning or putting a moratorium on physician-owned hospitals by the Congressional Budget Office.

The CBO is not transparent about what its assumptions are or its analysis and methods. As a researcher, we have to publish our information. It has to go through peer review. I want to know what goes into that $500 million figure — what the assumptions are and what the model is. It’s hard to comment without knowing how they came up with it.

Glatter: The points you make are very valid. Physicians and nurses want a better lifestyle.

Miller: It’s not even a better lifestyle. It’s about having a say in how clinical operations work and helping make them better. We want the delivery system to work better. This is an opportunity for us to do so.

Glatter: That translates into technology: obviously, generative artificial intelligence (AI) coming into the forefront, as we know, and changing care delivery models as you’re referring to, which is going to happen. It’s going to be a slow process. I think that the evolution is happening and will happen, as you accurately described.

Miller: The other thing that’s different now vs 20 years ago is that managed care is here, there, and everywhere, as Dr Seuss would say. You have utilization review and prior authorization, which I’ve experienced as a patient and a physician, and boy, is it not a fun process. There’s a large amount of friction that needs to be improved. If we’re worried about induced demand or inappropriate utilization, we have managed care right there to help police bad behavior.

Reforming Healthcare Systems and Restoring Patient-Centric Focus

Glatter: If you were to come up with, say, three bullet points of how we can work our way out of this current morass of where our healthcare systems exist, where do you see the solutions or how can we make and effect change?

Miller: I’d say there are a couple of things. One is, let business models compete fairly on an equal playing field. Let the physician-owned hospital compete with the tax-exempt hospital and the nonprofit hospital. Put them on an equal playing field. We have things like 340B, which favors tax-exempt hospitals. For-profit or tax-paying hospitals are not able to participate in that. That doesn’t make any sense just from a public policy perspective. Tax-paying hospitals and physician-owned hospitals pay taxes on investments, but tax-exempt hospitals don’t. I think, in public policy, we need to equalize the playing field between business models. Let the best business model win.

The other thing we need to do is to encourage the adoption of technology. The physician will eventually be an arbiter of tech-driven or AI-driven tools. In fact, at some point, the standard of care might be to use those tools. Not using those tools would be seen as negligence. If you think about placing a jugular or central venous catheter, to not use ultrasound would be considered insane. Thirty years ago, to use ultrasound would be considered novel. I think technology and AI will get us to that point of helping make care more efficient and more customized.

Those are the two biggest interventions, I would say. Third, every time we have a conversation in public policy, we need to remember what it is to be a patient. The decision should be driven not around any one industry’s profitability, but what it is to be a patient and how we can make that experience less burdensome, less expensive, or in plain English, suck less.

Glatter: Safety net hospitals and critical access hospitals are part of this discussion that, yes, we want everything to, in an ideal world, function more efficiently and effectively, with less cost and less red tape. The safety net of our nation is struggling.

Miller: I 100% agree. The Cook County hospitals of the world are deserving of our support and, frankly, our gratitude. Facilities like that have huge burdens of patients with Medicaid. We also still have millions of uninsured patients. The neighborhoods that they serve are also poorer. I think facilities like that are deserving of public support.

I also think we need to clearly define what those hospitals are. One of the challenges I’ve realized as I waded into this space is that market definitions of what a service market is for a hospital, its specialty type or what a safety net hospital is need to be more clearly defined because those facilities 100% are deserving of our support. We just need to be clear about what they are.

Regarding critical access hospitals, when you practice in a rural area, you have to think differently about care delivery. I’d say many of the rural systems are highly creative in how they structure clinical operations. Before the public health emergency, during the COVID pandemic, when we had a massive change in telehealth, rural hospitals were using — within the very narrow confines — as much telehealth as they could and should.

Rural hospitals also make greater use of nurse practitioners (NPs) and physician assistants (PAs). For many of the specialty services, I remember, your first call was an NP or a PA because the physician was downstairs doing procedures. They’d come up and assess the patient before the procedure, but most of your consult questions were answered by the NP or PA. I’m not saying that’s the model we should use nationwide, but that rural systems are highly innovative and creative; they’re deserving of our time, attention, and support, and frankly, we can learn from them.

Glatter: I want to thank you for your time and your expertise in this area. We’ll see how the congressional hearings affect the industry as a whole, how the needle moves, and whether the ban or moratorium on physician-owned hospitals continues to exist going forward.

Miller: I appreciate you having me. The hospital industry is one of the most important industries for health care. This is a time of inflection, right? We need to go back to the value of what it means to be a clinician and serve patients. Hospitals need to reorient themselves around that core concern. How do we help support clinicians — doctors, nurses, pharmacists, whomever it is — in serving patients? Hospitals have become too corporate, so I think that this is an expected pushback.

Glatter: Again, I want to thank you for your time. This was a very important discussion. Thank you for your expertise.

Robert D. Glatter, MD, is an assistant professor of emergency medicine at Zucker School of Medicine at Hofstra/Northwell in Hempstead, New York. He is a medical advisor for Medscape and hosts the Hot Topics in EM series.

Brian J. Miller, MD, MBA, MPH, is a hospitalist and an assistant professor of medicine at the Johns Hopkins University School of Medicine. He is also a nonresident fellow at the American Enterprise Institute. From 2014 – 2017, Dr Miller worked at four federal regulatory agencies: Federal Trade Commission (FTC), Federal Communications Commission (FCC), Centers for Medicare & Medicaid Services (CMS), and the Food & Drug Administration (FDA).

Affordable Care Act (ACA) enrollment appears poised to reach record levels once again as signups grew by more than a third of what they were this time last year, a fact the White House is using to continue to draw attention to former President Trump’s threats to try again to repeal the law.

More than 15 million people have signed up for plans in states that use HealthCare.gov, representing a 33 percent increase from last year. The Biden administration estimates 19 million will sign up for plans by the Jan. 16 deadline.

On Dec. 15, the deadline for coverage starting Jan. 1, more than 745,000 people selected a plan through HealthCare.gov — the most in a day in history, the Department of Health and Human Services said.

For 2023 plans, more than 16.3 million people signed up through HealthCare.gov last year, another record. Of those who enrolled for this year, 22 percent were new to the marketplace.

This year’s enrollment had some unusual factors that may have played a part in boosting enrollment. Those who were disenrolled from Medicaid this year during the “unwinding” period were allowed to sign up for ACA plans earlier than normal.

There was also stronger insurer participation in the program this year, providing significantly more options for customers to choose from.

“Thanks to policies I signed into law, millions of Americans are saving hundreds or thousands of dollars on health insurance premiums,” President Biden said on Wednesday.

“Extreme Republicans want to stop these efforts in their tracks,” he added. “At every turn, extreme Republicans continue to side with special interests to keep prescription drug prices high and to deny millions of people health coverage.”

Ten states have uninsured rates below 5 percent. What are they doing right?

Universal health care remains an unrealized dream for the United States. But in some parts of the country, the dream has drawn closer to a reality in the 13 years since the Affordable Care Act passed.

Overall, the number of uninsured Americans has fallen from 46.5 million in 2010, the year President Barack Obama signed his signature health care law, to about 26 million today. The US health system still has plenty of flaws — beyond the 8 percent of the population who are uninsured, far higher than in peer countries, many of the people who technically have health insurance still find it difficult to cover their share of their medical bills. Nevertheless, more people enjoy some financial protection against health care expenses than in any previous period in US history.

The country is inching toward universal coverage. If everybody who qualified for either the ACA’s financial assistance or its Medicaid expansion were successfully enrolled in the program, we would get closer still: More than half of the uninsured are technically eligible for government health care aid.

Particularly in the last few years, it has been the states, using the tools made available by them by the ACA, that have been chipping away most aggressively at the number of uninsured.

Today, 10 states have an uninsured rate below 5 percent — not quite universal coverage, but getting close. Other states may be hovering around the national average, but that still represents a dramatic improvement from the pre-ACA reality: In New Mexico, for instance, 23 percent of its population was uninsured in 2010; now just 8 percent is.

Their success indicates that, even without another major federal health care reform effort, it is possible to reduce the number of uninsured in the United States. If states are more aggressive about using all of the tools available to them under the ACA, the country could continue to bring down the number of uninsured people within its borders.

The law gave states discretion to build upon its basic structure. Many received approval from the federal government to create programs that lower premiums; some also offer state subsidies in addition to the federal assistance to reduce the cost of coverage, including for people who are not eligible for federal aid, such as undocumented immigrants. A few states are even offering new state-run health plans that will compete with private offerings.

I asked several leading health care experts which states stood out to them as having fully weaponized the ACA to reduce the number of uninsured. There was not a single answer.

“I don’t think any state has taken advantage of everything,” said Larry Levitt, executive vice president at the KFF health policy think tank. “No state has put all the pieces together to the full extent available under the ACA.”

But a few stood out for the steps they have taken over the last decade to strive toward universal health care.

Massachusetts (and New Mexico): Streamlined enrollment and state subsidies

Massachusetts has the lowest uninsured rate of any state: Just 2.4 percent of the population lacks coverage. It had a head start: The law provided the model for the ACA itself, with its system of government subsidies for private plans sold on a public marketplace that existed prior to 2010.

But experts say it still deserves credit for the steps it has taken since the Massachusetts model was applied to the rest of the country. Matt Fiedler, a senior fellow with the Brookings Schaeffer Initiative on Health Policy, said two policies stood above any others in expanding coverage: integrating the enrollment process for both Medicaid and ACA marketplace plans and offering state-based assistance on top of the law’s federal subsidies.

Massachusetts was among the first states to do both.

“The former can do a lot to reduce the risk that people lose their coverage when incomes change,” Fiedler told me, “while the latter directly improves affordability and thereby promotes take-up.”

Integrated enrollment means that, for the consumer, they can be directed to either the ACA’s marketplace (where they can use government subsidies to buy private coverage) or to the state Medicaid program through one portal. They enter their information and the state tells them which program they should enroll in. Without that integration, people might have to first apply to Medicaid and then, if they don’t qualify, separately seek out marketplace coverage. The more steps that a person must take to successfully enroll in a health plan, the more likely it is people will fall through the cracks.

The state assistance, meanwhile, both reduces premiums for people and makes it easier for them to afford more generous coverage, with lower out-of-pocket costs when they actually use medical services. Nine states including Massachusetts now have state assistance, with interest picking up in the past few years.

New Mexico, for example, only recently converted to a state-based ACA marketplace and started offering additional aid in 2023. Having already seen some dramatic improvements, it remains to be seen how much more progress the state can make toward universal coverage with that policy in place.

Minnesota and New York: The Basic Health Plan states

The basic structure of the ACA was this: Medicaid expansion for people living in or near poverty and marketplace plans for people with incomes above that. But the law included an option for states to more seamlessly integrate those two populations — and so far, the two states that have taken advantage of it, Minnesota and New York, are also among those states with the lowest uninsured rates. Just 4.3 percent of Minnesotans and 4.9 percent of New Yorkers lack coverage today.

They have both created Basic Health Plans, the product of one of the more obscure provisions of the health care law. This is a state-regulated health insurance plan meant to cover people up to 200 percent of the federal poverty level (about $29,000 for an individual or $50,000 for a family of three). Those are people who may not technically qualify for Medicaid under the ACA but who can still struggle to afford their monthly premiums and out-of-pocket obligations with a marketplace plan.

In both states, the Basic Health Plans offered insurance options with lower premiums and reduced cost-sharing responsibilities than the marketplace coverage that they would otherwise have been left with. In New York, for example, people between 100 percent and 150 percent of the federal poverty level pay no premiums at all, while people between 150 percent and 200 percent pay just $20 per month.

There is good evidence that the approach has increased coverage: In New York, for example, enrollment among people below 200 percent of the poverty level increased by 42 percent when the state adopted its BHP in 2016, compared to what it had been the year before when those people were relegated to conventional marketplace coverage.

State interest in Basic Health Plans has been limited so far, but Minnesota and New York provide a model others could follow. Fiedler said part of the basic plans’ success in those states has been using Medicaid managed-care companies to administer the plan: Those insurers already pay providers lower rates than marketplace plans do and the savings give the states money to reduce premiums and cost-sharing.

Colorado and Washington: Public options and assistance for the undocumented

These states have been inventive in myriad ways. They are both early adopters of a public option, a government health plan that competes with private plans on the marketplace, a policy also being tested in Nevada.

There is another policy that unites them, one that addresses a sizable part of the remaining uninsured nationwide: They both provide some state subsidies to undocumented immigrants.

Most uninsured Americans are already technically eligible for some kind of government assistance, whether Medicaid or marketplace subsidies. But there is a large chunk of people who are not: About 29 percent of the US’s uninsured are ineligible for government aid, among them the people who are in the country undocumented. Those people bear the full cost of their medical bills and may avoid care for that reason (among others, of course).

Starting this year, Washington is allowing undocumented people with incomes that would make them eligible for Medicaid expansion to enroll in that program, and making state subsidies available to people with higher incomes no matter their immigration status. Colorado has set aside a small pool of money annually to provide state aid to about 11,000 undocumented people. (After that threshold is hit, those folks can still enroll in a health plan but they must pay the full price.)

Interest has been robust: Last year, Colorado hit the enrollment limit after about a month. This year, enrollment capped out in just two days, suggesting the state may need to put more money behind the effort.

It is difficult to imagine insurance subsidies for undocumented people nationwide any time soon, given the fraught national politics of immigration. But states are finding ways to make inroads on their own: California has made undocumented people eligible for Medicaid.

Through these and other means, they are helping the US inch toward universal health care.

In the last 2 weeks, the Affordable Care Act (ACA) has been inserted itself in Campaign 2024 by Republican aspirants for the White House:

On Truth Social November 28, former President Trump promised to replace it with something better:“Getting much better Healthcare than Obamacare for the American people will be a priority of the Trump Administration. It is not a matter of cost; it is a matter of HEALTH. America will have one of the best Healthcare Plans anywhere in the world. Right now, it has one of the WORST! I don’t want to terminate Obamacare, I want to REPLACE IT with MUCH BETTER HEALTHCARE. Obamacare Sucks!!!!”

Then, on NBC’s Meet the Press December 3, Florida Governor Ron DeSantis offered “We need to have a healthcare plan that works,” Obamacare hasn’t worked. We are going to replace and supersede with a better plan….a totally different healthcare plan… big institutions that are causing prices to be high: big pharma, big insurance and big government.”

It’s no surprise. Health costs and affordability rank behind the economy as top issues for Republican voters per the latest Kaiser Tracking Poll. And distaste with the status quo is widespread and bipartisan: per the Keckley Poll (October 2023), 70% of Americans including majorities in both parties and age-cohorts under 65 think “the system is fundamentally flawed and needs major change.” To GOP voters, the ACA is to blame.

Background:

The Affordable Care Act (aka Obamacare aka the Patient Protection and Affordable Care Act) was passed into law March 23, 2013. It is the most sweeping and controversial health industry legislation passed by Congress since Lyndon Johnson’s Medicare and Medicaid Act (1965). Opinions about the law haven’t changed much in almost 14 years: when passed in 2010, 46% were favorable toward the law vs. 40% who were opposed. Today, those favorable has increased to 59% while opposition has stayed at 40% (Kaiser Tracking Poll).

Few elected officials and even fewer voters have actually read the law. It’s understandable: 955 pages, 10 major sections (Titles) and a plethora of administrative actions, executive orders, amendments and legal challenges that have followed. It continues to be under-reported in media and misrepresented in campaign rhetoric by both sides. Campaign 2024 seems likely to be more of the same.

In 2009, I facilitated discussions about health reform between the White House Office of Health Reform and the leading private sector players in the system (the American Medical Association, the American Hospital Association, America’s Health Insurance Plans, AdvaMed, PhRMA, and BIO). The impetus for these deliberations was the Obama administration’s directive that systemic reform was necessary with three-aims: reduce cost, increase access via insurance coverage and improve the quality of care provided by a private system. In parallel, key Committees in the House and Senate held hearings ultimately resulting in passage of separate House and Senate versions with the Senate’s becoming the substance of the final legislation. Think tanks on the left (I.e. the Center for American Progress et al.) and on the right (i.e. the Heritage Foundation) weighed in with members of Congress and DC influencers as the legislation morphed. And new ‘coalitions, centers and institutes’ formed to advocate for and against certain ACA provisions on behalf of their members while maintaining a degree of anonymity.

So, as the ACA resurfaces in political discourse in coming months, it’s important it be framed objectively. To that end, 3 major considerations are necessary to have a ‘fair and balanced’ view of the ACA:

1-The ACA was intended as a comprehensive health reform legislative platform. It was designed to be implemented between 2010 and 2019 in a private system prompted by new federal and state policies to address cost, access and quality. It allowed states latitude in implementing certain elements (like Medicaid expansion, healthcare marketplaces) but few exceptions in other areas (i.e.individual and employer mandates to purchase insurance, minimum requirements for qualified health plans, et al). The CBO estimated it would add $1.1 trillion to overall healthcare spending over the decade but pay for itself by reducing demand, administrative red-tape and leveraging better data for decision-making. The law included provisions to…

To improve quality by modernizing of the workforce, creating an Annual Quality Report obligation by HHS, creating the Patient Centered Outcome Research Institute and expanding the the National Quality Forum, adding requirements that approved preventive care be accessible at no cost, expanding community health centers, increasing residency programs in primary care and general surgery, implementing comparative effectiveness assessments to enable clinical transparency and more.