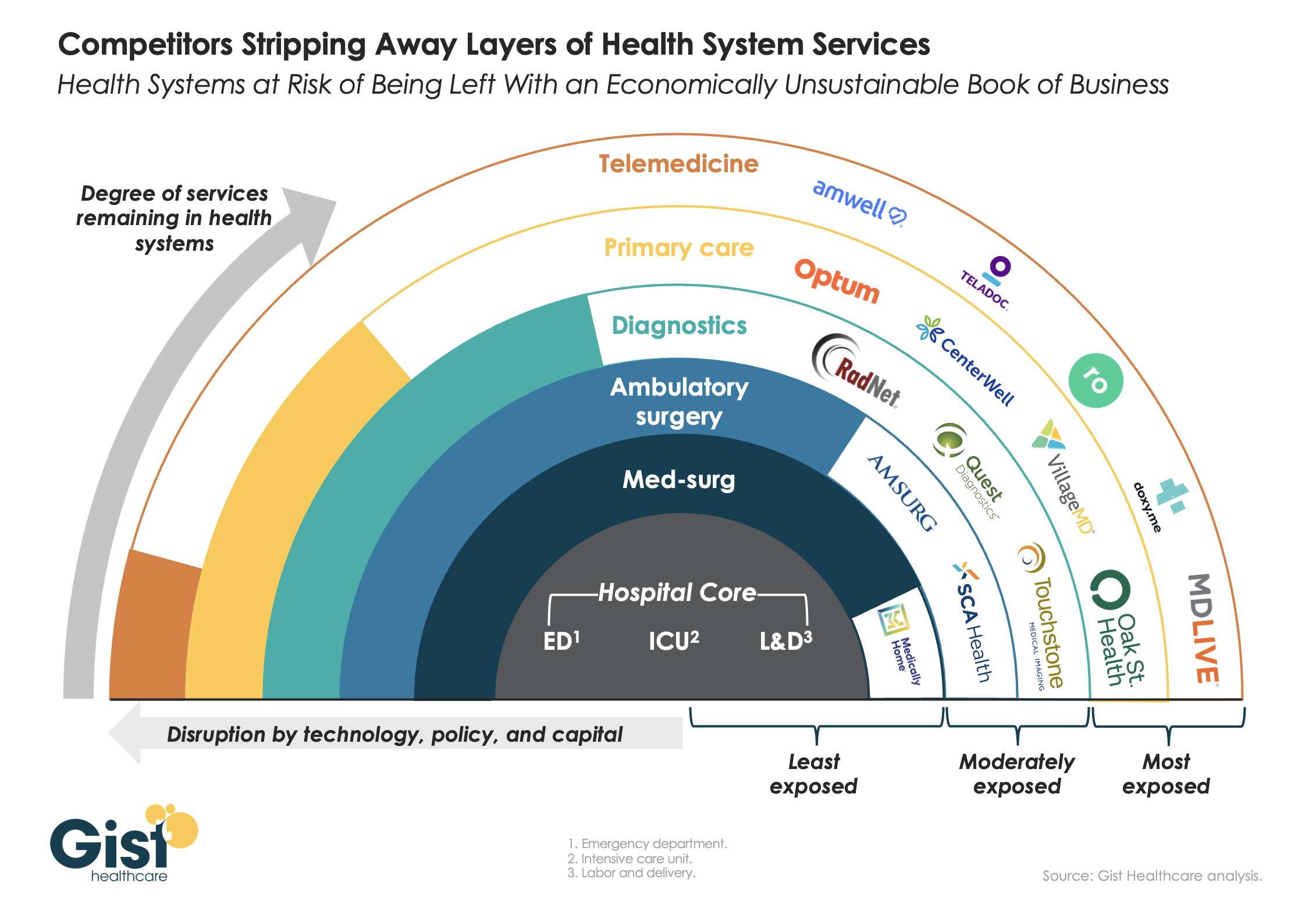

This week’s graphic features our assessment of the many emerging competitive challenges to traditional health systems.

Beyond inflation and high labor costs, health systems are struggling because competitors—ranging from vertically integrated payers to PE-backed physician groups—are effectively stripping away profitable services and moving them to lower-cost care sites. The tandem forces of technological advancement, policy changes, and capital investment have unlocked the ability of disruptors to enter market segments once considered safely within health system control.

While health systems’ most-exposed services, like telemedicine and primary care, were never key revenue sources (although they are key referral drivers), there are now more competitors than ever providing diagnostics and ambulatory surgery, which health systems have relied on to maintain their margins.

Moving forward, traditional systems run the risk of being “crammed down” into a smaller portfolio of (largely unprofitable) services: the emergency department, intensive care unit, and labor and delivery.

Health systems cannot support their operations by solely providing these core services, yet this is the future many will face if they don’temulate the strategies of disruptors by embracing the site-of-care shift, prioritizing high-margin procedures, rethinking care delivery within the hospital, and implementing lower-cost care models that enable them to compete on price.

After signing a letter of intent in late May, St. Louis, MO-based BJC HealthCare and Kansas City, MO-based Saint Luke’s Health System announced on Wednesday that they have signed a definitive merger agreement, having received the necessary regulatory approvals.

Based on opposite sides of the “Show-Me State,” the systems’ markets do not directly overlap. The merger, expected to close on Jan. 1, 2024, will create a $10B revenue, 28-hospital system spanning Missouri, southern Illinois, and eastern Kansas. The two systems plan to retain their respective brands and will be dually headquartered in St. Louis and Kansas City.

The Gist: BJC and Saint Luke’s are following in the footsteps of other recent mergers involving large health systems with no geographic overlap, which regulators have allowed to move forward. However, recent history shows there’s more to closing a deal than just passing regulatory muster.

Both the Sanford-Fairview and UnityPoint-Presbyterian mergers were called off earlier this year for non-regulatory reasons, including the concerns of local stakeholders.

Given the difficult financial environment and the growing threat of vertically integrated payers, health systems looking to pursue scale strategies must ensure they will actually realize the promise these combinations may hold.

Does hospital ownership matter? According to a study published last week in Health Affairs Scholar, NOT MUCH. That’s a problem for not-for-profit hospitals who claim otherwise.

58% of U.S. hospitals are not-for-profit hospitals; the rest are public (19%) or investor-owned (24%). In recent months, not-for-profit systems have faced growing antagonism from regulators and critics who challenge the worthwhileness of their tax exemptions and reasonableness of the compensation paid their top executives.

The lion’s share of this negative attention is directed at large, not-for-profit hospital system operators. Case in point: last week, Banner Health (AZ) joined the ranks of high-profile operators taken to task in the Arizona Republic for their CEO’s compensation contrasting it to not-for-profit sectors in which compensation is considerably lower.

Unflattering attention to NFP hospitals, especially the big-name systems, is unlikely to subside in the near-term. U.S. healthcare has become a winner-take-all battleground increasingly dominated by large-scale, investor-owned interests in hospitals, medical groups, insurance, retail health in pursuit of a piece of the $4.6 trillion pie.

The moral high ground once the domain of not-for-profit hospitals is shaky.

The NYU study examined whether hospital ownership influenced decisions made by consumers: they found “Fewer than one-third of respondents (29.5%) indicated that hospital status had ever been relevant to them in making decisions about where to seek care…significantly more important to respondents who indicated the lowest health literacy—74.7% of whom answered the key question affirmatively—than it was for people who indicated high health literacy, of whom only 18.3% found hospital ownership status to be relevant…also considerably more relevant for people working in health care than for those who did not work in health care (61.0% vs 24.5%)…

We found little evidence that hospital nonprofit status influenced Americans’ decisions about where to seek care. Ownership status was relevant for fewer than 30% of respondents and preference was greatest overall for public hospitals. Only 30–45% of respondents could correctly identify the ownership status of nationally recognized hospitals, and fewer than 30% could identify their local hospitals.

These findings suggest that contract failure does not currently provide a justification of nonprofit hospitals’ value; further scrutiny of tax exemption for nonprofit hospitals is warranted.”

Are NFP hospitals concerned? YES. It’s reality as systems address near term operational challenges and long-term questions about their strategies.

Last weekend, I facilitated the 4th Annual Chief Strategy Officers Roundtable in Austin TX sponsored by Lumeris. The group consisted of senior-level strategists from 11 not-for-profit systems and one for-profit. In one session, each reacted to 50 future state scenarios in terms of “likelihood” and “disruptive impact” in the NEAR term (3-5 years) and LONG TERM (8-10 years) using a 1 to 10 scale with 10 HI.

From these data and the discussion that followed, there’s consensus that the U.S. healthcare market is unlikely to change dramatically long-term, their short-term conditions will be tougher and their challenges unique.

‘Near-term cost containment is a priority. Hospitals are here-to-stay, but operating them will be harder.’

‘Increased scale and growth are necessary imperatives for their systems.’

‘Hospital systems will compete in a market wherein private capital and investor ownership will play a growing role, insurers will be hostile and value will the primary focus of cost-reduction by purchasers and policymakers.’

‘Distinctions betweennot-for-profit and for-profit hospitals are significant.’

‘Conditions for hospitals will be tougher as insurers play a stronger hand in shaping the future.’

Given the NYU study findings (above) concluding NFP ownership has marginal impact on hospital choices made by consumers, it’s understandable NFPs are anxious.

My take:

The issues facing not-for-profit hospitals in the U.S. are unique and complex. Per the commentary of the CSOs, their market conditions are daunting and major changes in their structure, funding and regulation unlikely.

That means lack of public understanding of their unique role is a conundrum.

Paul

PS: Issues about CEO compensation in healthcare are touchy and often unfair.

In every major NFP system, comp is set by the Independent Board Compensation Committee with outside consultative counsel. The vast majority of these CEOs aren’t in the job for the money joining their workforce in pursuit of the unique higher calling afforded service leaders in NFP healthcare.

Costco is now offering members online health checkups for as low as $29.

The retailer is offering the new service in partnership with Sesame, a direct-to-consumer health care marketplace that connects medical providers nationwide with consumers.

Sesame, in a release, said Costco members beginning Monday can book health care visits directly through their memberships in all 50 states.

The New York-based company said its platform doesn’t accept health insurance because it primarily caters to uninsured Americans and those with high-deductible plans who prefer to pay cash for their health care. It said its model helps keep prices of services low for its users.

The services listed on Costco Pharmacy’s homepage, include virtual primary care visits for $29, health checkups (a standard lab panel and a virtual follow-up consultation with a provider) for just $72 and online mental health visits for $79.

“Quality, great value, and low price are what the Costco brand is known for,” David Goldhill, Sesame’s co-founder and CEO, said in a statement. “When it comes to health care, Sesame also delivers high quality and great value – and a low price that will be appreciated by Costco Members when it comes to their own care.”

Amazon, in August, announced that its virtual clinic was now also available nationwide. Amazon Clinic launched last November offering 24/7 access to third-party health-care providers directly on Amazon’s website and mobile app.

Amazon customers, through the clinic, can access telehealth treatment for dozens of common conditions, such as pink eye, urinary tract infections and hair loss, the retailer said.

Other retailers, including CVS to Walgreens to Walmart, have made similar moves.

Amazon announced that it has expanded its direct-to-consumer virtual care platform to all 50 states and the District of Columbia. Amazon Clinic, which the e-commerce giant launched in 32 states last November, connects consumers to third-party clinicians via Amazon’s website or mobile app. Through video call or message-based visits (the latter of which are only available in some states), it offers diagnosis and treatment for a range of low-acuity, common health conditions like pink eye and sinus infections. The clinic features flat, upfront cash pricing, and doesn’t currently accept insurance. On the provider side, Amazon is partnering with telehealth companies Wheel, SteadyMD, Curai Health, and Hello Alpha.

The Gist: This is the kind of venture at which Amazon excels: creating a marketplace convenient for buyers and sellers (patients and telemedicine providers, respectively), pricing it competitively to pursue scale over margins, and upselling customers by pairing care with Amazon’s other products or services (like Amazon Pharmacy).

We’ll be watching for how Amazon builds on this service, and whether it connects Amazon Clinic to its Prime membership and One Medical assets. In the meantime, in addition to its consumer-focused offerings,Amazon is also simultaneously expanding its enterprise workflow offerings through its AWS for Health division, recently launching HealthScribe and HealthImaging.

As first half 2023 financial results are reported and many prepare for a busy last half, strategic planning for healthcare services providers and insurers point to 4 issues requiring attention in every boardroom and C suite:

Private equity maturity wall:

The last half of 2023 (and into 2024) is a buyer’s market for global PE investments in healthcare services: 40% of PE investments in hospitals, medical groups and insurtech will hit their maturity wall in the next 12 months. Valuations of companies in these portfolios are below their targeted range; limited partner’ investing in PE funds is down 28% from pre-pandemic peak while fund raising by large, publicly traded, global funds dominate fund raising lifting PE dry powder to a record $3.7 trillion going into the last half of 2023.

In the U.S. healthcare services market, conditions favor well-capitalized big players—global private equity funds and large cap aggregators (i.e., Optum, CVS, Goldman Sachs, Blackstone et al) who have $1 trillion to invest in deals that enhance their platforms. Deals done via special purpose acquisition corporations (SPACS) and smaller PE funds in physicians, hospitals, ambulatory services and others are especially vulnerable. (see Bain and Pitchbook citations below). Addressing the growing role of large-cap PE and strategic investors as partners, collaborators, competitors or disruptors is table stakes for most organizations recognizing they have the wind at their backs.

Consolidation muscle by DOJ and FTC:

Healthcare is in the crosshair of the FTC and DOJ, especially hospitals and health insurers. Hospital markets have become increasingly concentrated: only 12% of the 306 Hospital Referral Regions is considered unconcentrated vs. 23% in 2008. In the 384 insurance markets, 23% are unconcentrated, down from 35% in 2020. Wages for healthcare workers are lower, prices for consumers are higher and choices fewer in concentrated markets prompting stricter guidelines announced last week by the oversight agencies. Big hospitals and big insurers are vulnerable to intensified scrutiny. (See Regulatory Action section below).

Defamatory attacks on nonprofit health systems:

In the past 3 years, private, not-for-profit multi-hospital systems have been targeted for excess profits, inadequate charity care and executive compensation. Labor unions (i.e., SEIU) and privately funded foundations (i.e., West, Arnold Venture, Lown Institute) have joined national health insurers in claims that NFP systems are price gaugers undeserving of the federal, state and local tax exemptions they enjoy. It comes at a time when faith in the U.S. health system is at a modern-day low (Gallup), healthcare access and affordability concerns among consumers are growing and hospital price transparency still lagging (36% are fully compliant with the 2021 Executive Order).

Notably, over the last 20 years, NFP hospitals have become less dominant as a share of all hospitals (61% in 2002 vs. 58% last year) while investor-owned hospitals have shown dramatic growth (from 15% in 2002 to 24% last year). Thus, the majority of local NFP hospitals have joined systems creating prominent brands and market dominance in most regions. But polling indicates many of these brands is more closely associated with “big business” than “not-for-profit health” so they’re soft targets for critics. It is likely unflattering attention to large, NFP systems will increase in the next 12 months prompting state and federal regulatory actions and erosion of public support. (See New England Journal citation in Quotables below)

Campaign 2024 healthcare rhetoric:

Republican candidates will claim healthcare is not affordable and blame Democrats. Democrats will counter that the Affordable Care Act’s expanded coverage and the Biden administration’s attack on drug prices (vis a vis the Inflation Reduction Act) illustrate their active attention to healthcare in contrast to the GOP’s less specific posturing.

Campaigns in both parties will call for increased regulation of hospitals, prescription drug manufacturers, health insurers and PBMs. All will cast the health industry as a cesspool for greed and corruption, decry its performance on equitable access, affordability, price transparency and improvements in the public’s health and herald its frontline workers (nurses, physicians et al) as innocent victims of a system run amuck.

To date, 16 candidates (12 R, 3 D, 1 I) have announced they’re candidates for the White House while campaigns for state and local office are also ramping up in 46 states where local, state and national elections are synced. Healthcare will figure prominently in all. In campaign season, healthcare is especially vulnerable to misinformation and hyper-attention to its bad actors. Until November 5, 2024, that’s reality.

My take:

These issues frame the near-term context for strategic planning in every sector of U.S. healthcare. They do not define the long-term destination of the system nor roles key sectors and organizations will play. That’s unknown.

What’s known for sure is that AI will modify up to 70% of the tasks in health delivery and financing and disrupt its workforce.

Black Swans like the pandemic will prompt attention to gaps in service delivery and inequities in access.

People will be sick, injured, die and be born.

And the economics of healthcare will force uncomfortable discussions about its value and performance.

In the U.S. system, attention to regulatory issues is a necessary investment by organizations in every state and at the federal level. Details about these efforts is readily accessible on websites for each organization’s trade group. They’re the rule changes, laws and administrative actions to which all are attentive. They’re today’s issues.

Less attention is given the long-term. That focus is often more academic than practical—much the same as Robert Oppenheimer’s early musings about the future of nuclear fusion. But the Manhattan Project produced two bombs (Little Boy and Fat Man) that detonated above the Japanese cities of Hiroshima and Nagasaki in 1945, triggering the end of World War II.

The four issues above should be treated as near and present dangers to the U.S. health system requiring attention in every organization. But responses to these do not define the future of the U.S. system. That’s the Manhattan Project that’s urgently needed in our system.

For decades, research studies and news stories have concluded the American system is ineffective,

too expensive and falling further behind its international peers in important measures of performance: life expectancy, chronic-disease management and incidence of medical error.

As patients and healthcare professionals search for viable alternatives to the status quo, a recent mega-merger is raising new questions about the future of medicine.

In April, Kaiser Permanente acquired Geisinger Health under the banner of newly formed Risant Health. With more than 185 years of combined care-delivery experience, Kaiser and Geisinger have long been held up as role models of the value-based care movement.

Eyeing the development, many speculated whether this deal will (a) ignite widespread healthcare transformation or (b) prove to be a desperate attempt at relevance (Kaiser) or survival (Geisinger).

Whether incumbents like Kaiser Permanente and Geisinger can lead a national healthcare transformation or are displaced by new entrants will depend largely on whether they can deliver value-based care on a national scale.

In Search Of Healthcare’s Holy Grail

Value-based care—the simultaneous provision of high quality, convenient and affordable medical care—has long been the aim of leading health systems like Kaiser, Geisinger, Mayo Clinic, Cleveland Clinic and dozens more.

But results to-date have often failed to match the vision.

The need for value-based care is urgent. That’s because U.S. health and economic problems are expected to get worse, not better, over the next decade. According to federal governmental actuaries, healthcare expenditures will rise from $4.2 trillion today to $7.2 trillion by 2031. At that time, these costs are predicted to consume an estimated 19.6% of the U.S. Gross Domestic Product.

Put simply: The U.S. will nearly double the cost of medical care without dramatically improving the health of the nation.

For decades, health policy experts have pointed out the inefficiencies in medical care delivery. Research has estimated that inappropriate tests and ineffective procedures account for more than 30% of all money spent on American medical care.

This combination of troubling economics and untapped opportunity explain why value-based care has become medicine’s holy grail. What’s uncertain is whether the transformation in healthcare delivery and financing will be led from inside or outside the healthcare system.

Where The Health-System Hopes Hang

For years, Kaiser Permanente has led the nation in clinical quality and patient outcomes based on independent, third-party research via the National Committee for Quality Assurance (NCQA) and Medicare Star ratings. Similarly, Geisinger was praised by President Obama for delivering high-quality care at a cost well below the national average.

And yet, these organizations, and many other highly regarded national and regional health systems, are extremely vulnerable to disruption, especially when their strategy and operational decisions fail to align.

Kaiser, for its part, has struggled with growth while Geisinger’s care-delivery strategy has proven unsuccessful in recent years. Failed expansion efforts forced KP to exit multiple U.S. markets, including New York, North Carolina, Kansas and Texas. More recently, several of its existing regions have failed to grow market share and weakened financially.

Meanwhile, Geisinger has fallen on hard times after decades of market domination. As Bob Herman reported in STAT News: “Failed acquisitions, antitrust scrutiny, leadership changes, growing competition from local players, and a pandemic that temporarily upended how patients got care have forced Geisinger to abandon its independence. The system is coming off a year in which it lost $240 million from its patient care and insurance operations.”

Putting the pieces together, I believe the Kaiser-Geisinger deal represents an industry undergoing massive change as health systems face intensifying pressure from insurers and a growing threat from retailers like Amazon, CVS and Walmart. This upcoming battle over the future of value-based care represents a classic conflict between incumbents and new entrants.

Can The World’s Largest Companies Disrupt U.S. Healthcare?

Retail giants, including Amazon, Walmart and CVS, are among the nation’s 10 largest companies based on annual revenue.

They have a broad geographic presence and strong relationships with almost all self-funded businesses. Nearly all have acquired the necessary healthcare pieces—including clinicians, home-health services, pharmacies, insurance arms and electronic medical record systems—to replace the current medical system.

And yet, while these companies expand into medical care and financing, their core businesses are struggling, resulting in announced store closures and layoffs. As newcomers to the healthcare market, they have been forced to pay premium dollars to acquire parts of the delivery system. All have a steep learning curve ahead of them.

The Challenge Of Healthcare Transformation

American medicine is a conglomerate of monopolies(insurers, hospitals, drug companies and private-equity-owned medical practices). Each works to maximize its own revenue and profit. All are unwilling to innovate in ways that benefit patients when doing so comes at the sacrifice of financial performance.

One problem stands at the center of America’s soaring healthcare costs: the way doctors, hospitals and drug companies are paid.

The dominant payment methodology in the United States, fee-for-service, rewards healthcare providers for charging higher prices and increasing the number (and complexity) of services offered—even when they provide no added value.

The message to doctors and hospitals is clear: The more you do, and the greater market control you have, the higher your income and profit. This is the antithesis of value-based care.

The alternative to fee-for-service payments, capitation, involves paying a single, up-front sum to the providers of care (doctors and hospitals) to cover the total annual cost for a population of patients. This model, unlike fee-for-service, rewards effectiveness and efficiency. Capitation creates incentives to prevent disease, reduce complications from chronic illness, and diminish the inefficiencies and redundancies present in care delivery. Capitated health systems that can prevent heart attacks, strokes and cancer better than others are more successful financially as a result.

However, it’s harder than it sounds to translate what’s best for patients into everyday decisions and actions. It’s one thing to accept a capitated payment with the intent to implement value-based care. It’s another to put in place the complex operational improvements needed for success. Here are the roadblocks that Kaiser-Geisinger will face, followed by those the retail giants will encounter.

3 Challenges For Kaiser-Geisinger:

Involving Clinical Experts. Kaiser Permanente is a two-part organization and when the insurance half (Kaiser) decided to acquire Geisinger, it did so without input or involvement from the half of the organization responsible for care-delivery (Permanente). This spells trouble for Geisinger, which must navigate a complex turnaround without the operational expertise or processes from Permanente that, in the past, helped Kaiser Permanente grow market share and lead the nation in clinical quality.

Going All In. To meet the healthcare needs of most its patients, Geisinger relies on community doctors who are paid on a fee-for-service basis. Generally, the fee-for-service model is predicated on the assumption that higher quality and greater convenience require higher prices and increased costs. With Geisinger’s distributed model, it’ll be very difficult to deliver consistent, value-based care.

Inspired Leadership. Major improvements in care delivery require skilled leadership with the authority to drive clinical change. In Kaiser Permanente, that comes through the medical group and its physician CEO. In Geisinger’s hybrid model, independent doctors have no direct oversight or central accountability structure. Although Risant Health could be an engine for value-based medical care, it’s more likely to serve the role of a “holding company,” capable of recommending operational improvements but incapable of driving meaningful change.

3 Challenges For The Retail Giants:

More Medical Offerings. Amazon, Walmart and CVS are successfully acquiring primary care (and associated telehealth) services. But competing with leading health systems will require a more wholistic, system-based approach to keep medical care affordable. This won’t be easy. To avoid ineffective, expensive specialty and hospital services, they will need to hire their own specialists to consult with their primary care doctors. And they will have to establish centers of excellence to provide heart surgery, cancer treatment, orthopedic care and more with industry-leading outcomes. But to meet the day-to-day and emergent needs of patients, they also will have to establish contracts with specialists and hospitals in every community they serve.

Capitalizing On Capitation. Already, the retail giants have acquired organizations well-versed in delivering patient care through Medicare Advantage, a capitated alternative to traditional (fee-for-service) Medicare plans. It’s a good start. But the retailers must do more than dip a toe in value-based care models. They must find ways to gain sufficient experience with capitation and translate that success into value-based contracts with self-funded businesses, which insure tens of millions of patients.

Defining Leadership. Without an effective and proven clinical leadership structure, the retail giants will be no more effective than their mainstream competitors when it comes to implementing improvements and shifting the culture of medicine to one that is customer- and service-focused.

Be they incumbents or new entrants, every contender will hit a wall if they cling to today’s failing care delivery model. The secret ingredient, which most lack and all will need to embrace in the future, is system-ness.

For all of the hype surrounding value-based care, fragmentation and fee-for-service are far more common in American healthcare today than integration and capitation.

Part two of this article will focus on how these different organizations—one set inside and one set outside of medicine—can make the leap forward with system-ness. And, in the end, you’ll see who is most likely to emerge victorious.

So far, 2023 is shaping up to be a slightly better year for hospital performance, but it comes on the heels of unprecedented financial difficulties for the sector.

In the graphic above, we evaluated nearly 30 years of historical data from Kaufman Hall and the American Hospital Association to provide a broader perspective on hospital operating margins over time. 2020 and 2022 have been the only years in which a majority of hospitals—53 percent—posted a negative operating margin.

During the most comparable periods of recent economic hardship, the “dot-com bubble burst” of the late 1990s and the 2009 Great Recession, the share of hospitals with negative operating margins amounted to only 42 and 32 percent, respectively.

With this context, hospitals’ current financial distress is more severe than anything we’ve seen in the past three decades.

Healthcare is clearly no longer recession-proof: a four percent operating margin—the level needed for health systems to not only sustain operations but also invest in growth—feels even more elusive as labor costs remain high, surgical care continues to shift to outpatient settings, the second half of the Baby-Boom generation ages into Medicare, and deep-pocketed competitors compete for profitable services.

Health systems are ramping up investments in ambulatory surgery centers and forming joint ventures with outpatient partners to accelerate the development of new centers. The trend is picking up steam as complex procedures increasingly move to ASCs, which are steadily growing as the preferred site of service for physicians, patients and payers.

Tenet Healthcare, one of the largest for-profit health systems in the country, has been paying close attention to outpatient migration for years and has cemented itself as the leader in the ASC space. It now operates more than 445 ASCs — the most of any health system — and 24 surgical hospitals, according to its first-quarter earnings report.

United Surgical Partners International, Tenet’s ASC company, strengthened its footing in the ASC market after its $1.2 billion acquisition of Towson, Md.-based SurgCenter Development and its more than 90 ASCs in December 2021. Over the next several years, USPI will inject more than $250 million into ASC mergers and acquisitions and work with SurgCenter to develop at least 50 more ASCs, according to terms of the transaction.

The SurgCenter acquisition was completed shortly after Tenet sold five Florida hospitals to Dallas-based Steward Health Care for $1.1 billion. In 2022, Tenet also acquired Dallas-based Baylor Scott & White Health’s 5 percent equity position in USPI to own 100 percent of the company’s voting shares and paid $78 million to acquire ownership of eight Compass Surgical Partners ASCs.

These ASC investments and hospital sales make it clear that CEO Saum Sutaria, MD, sees surgery centers to become Tenet’s main growth driver in the coming years. Dr. Sutaria has described USPI as the company’s “gem for the future,” and aims to have 575 to 600 ASCs by the end of 2025.

While Tenet continues to increase its ASC market share, its closest competitor is Deerfield, Ill.-based SCA Health, which UnitedHealth Group’s Optum acquired for $2.3 billion several years ago.

SCA has more than 320 ASCs, but has expanded its focus on value-based care under Optum and is doubling down on supporting physicians across the specialty care continuum rather than operating as an ASC company “singularly focused on partnering with surgeons in their ASCs,” SCA CEO Caitlin Zulla told Becker’s.

While Tenet may operate the most ASCs among health systems, it lags behind Optum in terms of the number of physicians it employs. Optum is now affiliated with more than 70,000 physicians, making it the largest employer of physicians in the country, and is continuing to add to that through mergers and acquisitions.

Nashville, Tenn.-based HCA Healthcare, another for-profit system, employs or is affiliated with more than 47,000 physicians, but is also ramping up its surgery center portfolio. HCA comprises 2,300 ambulatory care facilities, including more than 150 ASCs, freestanding emergency rooms, urgent care centers and physician clinics, according to its first-quarter earnings report.

Like Tenet and Optum, HCA is heavily focused on expanding its outpatient portfolio. The company ended 2021 with 125 ASCs, four more than it had at the end of 2020, and added more than 25 ASCs last year. It is focused on both developing and acquiring surgery centers in the coming years.

The other big ASC operators include Nashville, Tenn.-based AmSurg, with more than 250 surgery centers, and Brentwood, Tenn.-based Surgery Partners, with more than 120 centers. Surgery Partners spent about $250 million on ASCs acquisitions last year and recently signed collaboration agreements with two large health systems —- Salt Lake City-based Intermountain Health and Columbus-based OhioHealth.

Oakland, Calif.-based Kaiser Permanente has 62 freestanding ASCs and outpatient surgery departments on its hospital campuses, a spokesperson for the health system told Becker’s.