More than a year after launching an in-house travel staffing agency, UPMC is adding a new regional approach to the effort.

Maribeth McLaughlin, MPM, BSN, RN, chief nursing executive for the Pittsburgh-based health system, told Becker’s the approach provides a new option for nurses and surgical technologists who desire to travel.

“Our overall travel program, when you travel for us, you travel across our hospitals in New York, Maryland and Pennsylvania,” she said. “And now we are launching a regional travel strategy where some staff can choose to travel only within certain regions.”

UPMC initially announced in December 2021 that it had created UPMC Travel Staffing, a new in-house travel staffing agency to address a nursing shortage and to attract and retain workers.

Through the agency, nurses and surgical technologists earn $85 an hour and $63 an hour, respectively, in addition to a $2,880 stipend at the beginning of each six-week assignment.

Ms. McLaughlin said the rate is lower — about $60 an hour — for those who opt for the regional approach.

As of June 1, UPMC has hired more than 700 staff into the in-house travel staffing agency, with 60 percent of those workers being external hires, according to Ms. McLaughlin. And there have been fewer workers leaving UPMC to go to other travel agencies.

“One of my goals since I’ve taken this role is to really look at building in as many flexible programs as I could for staff,” said Ms. McLaughlin, who has served in her current role since August 2022. “I think as we came out of the pandemic, it’s clear to me that work-life harmony means something different to staff today than it maybe meant when I was a young staff nurse years ago, and that we need to have as much flexibility and as many different programs as we can.”

She said UPMC Travel Staffing has delivered this flexibility and allowed the health system to cancel about 90 contracts with external travel agencies. Additionally, some external travelers have now moved into UPMC’s in-house agency. Ms. McLaughlin expects more to join the in-house agency now that UPMC has launched the regional approach.

“We’re launching a win-back program where we’re going out and trying to see some of the people who we know we lost and see if they’re interested in coming back closer to home and traveling closer to home,” she explained.

Still, she acknowledged some of the challenges along the way.

“Our IT department built us an app to be able to manage all of this because, as you can imagine, we have external travel, internal travelers, core staff and at times it could get a little confusing,” said Ms. McLaughlin. “So we’ve been able to build that to be able to figure out the best ways to assign the staff where the greatest needs are.”

Another challenge she noted is that shifts for workers from external travel agencies are often 12 weeks, while shifts with UPMC Travel Staffing are six weeks. She said this is a purposeful move because those in UPMC Travel Staffing receive benefits and are considered UPMC employees, rather than receiving an hourly rate.

“Overall, it’s been a really successful program for us because it’s allowed us to look at things in a different way,” said Ms. McLaughlin. “It’s a central function. It’s not something we did and farmed out to every hospital to administer themselves. We did it as a system and as a core, which I also think is important.”

Now, she said she’s excited about the new regional approach and the opportunities it presents for recruiting and retention.

“We’re growing our own students, we’re bringing in all these students, and we’re not saying, ‘You have to just work here.’ We’re saying, ‘You can work for us at UPMC, and here are all the options. You can even be a traveler with us,'” she said.

As the nation’s leading provider of retail healthcare, CVS Health partners with hospitals and health systems in many local markets.

The health systems assist providers at CVS MinuteClinic locations and accept referrals from patients needing a higher level of care. Here are CVS’ clinical affiliates, according to its website:

More than a year after the regulation went into effect, compliance with the hospital price transparency rule remains low, as hospitals are hesitant to invest in necessary software and resources.

The Centers for Medicare and Medicaid Services (CMS) established the hospital price transparency rule to help individuals know the cost of a hospital item or service before receiving it.

CMS proposed the price transparency rule in the 2020 Medicare Outpatient Prospective Payment System (OPPS) and Ambulatory Surgical Center (ASC) Payment System Proposed Rule. The rule came in response to rising healthcare costs. Policymakers implemented regulations that give consumers more control over what they pay for healthcare services.

The rule went into effect on January 1, 2021, but hospitals have been slow to comply with the regulation. Without consistent compliance from hospitals and health systems, the rule does little to protect consumers from high healthcare prices.

WHAT IS THE PRICE TRANSPARENCY RULE?

The price transparency rule requires hospitals to publish the costs of their items and services on a publicly available website in two ways.

First, hospitals must have a single machine-readable digital file with standard charges for all their items and services. Standard charges include gross charges, discounted cash prices, payer-specific negotiated chargers, and de-identified minimum and maximum negotiated charges.

Hospitals must also display standard charges of at least 300 shoppable services that consumers can schedule in advance. That information must be displayed in a consumer-friendly format that includes plain language descriptions. Hospitals should also group the services with related ancillary services.

Hospitals may offer an online price estimator tool instead of publishing standard charges for the most common shoppable services. According to CMS, the price estimator tool must provide estimates for as many of the 70 CMS-specified shoppable services that the hospital offers and any additional shoppable services to reach a total of 300 services.

In addition, the tool must allow consumers to receive an estimate of the amount they will have to pay for a given service. Hospitals must display the price estimator tool on their websites and make it accessible to the public for free. Consumers also need to be able to access the tool without creating a user account.

CMS established an enforcement plan to ensure hospitals comply with the price transparency rule. The agency planned to evaluate complaints made by individuals or entities, review analyses of noncompliance, and audit hospital websites. However, more than one year after the regulation went into effect, hospitals are still not complying with the price transparency rule.

PRICE TRANSPARENCY RULE COMPLIANCE

The price transparency regulation received immediate pushback from hospital and provider groups. Before the policy went into effect, the American Hospital Association (AHA) sued HHS over the rule, stating that it would confuse consumers and increase prices.

The Kaiser Family Foundation (KFF) analyzed data from the two largest hospitals in each state and the District of Columbia and found similar trends. For example, 80 percent of the hospitals provided gross charge information on a price estimator tool and a machine-readable file, but only 35 of the 102 hospitals displayed payer-specific negotiated rates.

According to an Insights analysis from Xtelligent Healthcare Media, hospital networks frequently had inaccessible machine-readable files and shoppable services. In addition, many hospitals required patients to provide personally identifiable information in exchange for pricing data and had machine-readable files that lacked the required charges.

PatientRightsAdvocate.org has been tracking hospital compliance with the price transparency rule since May 2021. Between May and July, the organization found that out of 500 randomly selected US hospitals, only 5.6 percent were compliant with the rule.

Under the 2022 Medicare OPPS rule, CMS shared the penalties for not complying with the price transparency rule. Hospitals with less than 30 beds would receive penalties of $300 per day, while hospitals with 31 or more beds would receive a $10 per bed per day penalty, with a maximum daily fine of $5,500.

However, hospitals have not received any penalties for noncompliance as of February 2022. CMS has sent around 345 warning notices to noncompliant hospitals since the rule went into effect, the agency told Becker’s Hospital Review.

The threat of financial penalties does not seem to be enough to ensure compliance, though.

Shortly after the rule took effect, noncompliant hospitals said they were not fully complying due to resource constraints and a limited understanding of the rule. Some hospitals also mentioned that they were waiting to see how their competitors responded to the rule before achieving compliance.

More than one year later, in April 2022, financial leaders expressed similar concerns regarding compliance. Revenue cycle leaders told KLAS that a top barrier to achieving compliance was the confusing and complex regulations included in the rule.

Price transparency compliance also requires significant investment in software and outside resources, the KLAS report noted. As hospitals and health systems struggle financially due to the COVID-19 pandemic, investing in price transparency software may not be a top priority.

In addition, revenue cycle leaders reported experiencing difficulties with the software used to publish machine-readable files and a master list of prices online.

Until CMS starts delivering monetary penalties for noncompliance or adjusts the regulation to reduce the financial burden for health systems, hospital compliance with the price transparency rule will likely remain slim.

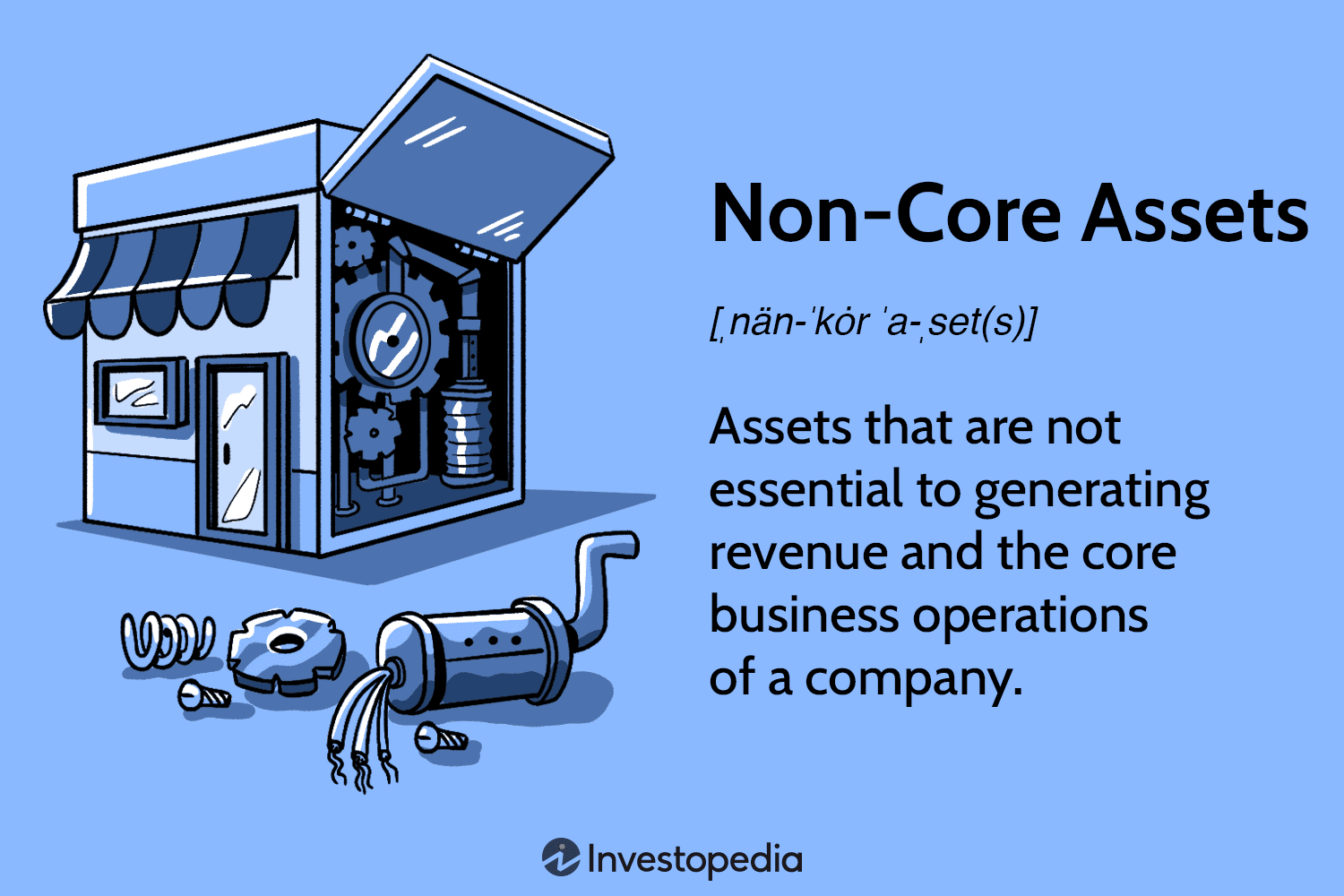

Inflation, labor pressures, and general economic uncertainty have created significant financial strain for hospitals in the wake of the COVID pandemic. Compressed operating margins and weakened liquidity have left many hospitals in a precarious economic situation, with some entities deciding to delay or even cancel planned capital expenditures or capital raising. Given these tumultuous times, hospital entities could look to the realm of the higher education sector for a playbook on how to leverage non-core assets to unlock significant unrealized value and strengthen financial positions, in the form of public-private partnerships.

These structures, also known as P3s, involve collaborative agreements between public entities, like hospitals, and private sector partners who possess the expertise to unlock the value of non-core assets. A special purpose vehicle (SPV) is created, with the sole purpose of delivering the responsibilities outlined under the project agreement. The SPV is typically owned by equity members. The private sector would be responsible for raising debt to finance the project, which is secured by the obligations of the project agreement (and would be non-recourse to the hospital). Of note, the SPV undergoes the rating process, not the hospital entity. Even more importantly, the hospital retains ownership of the asset while benefiting from the expertise and resources of the private sector.

Hospitals can utilize P3s to capitalize on already-built assets, in what is known as a “brownfield” structure. A brownfield structure would typically result in an upfront payment to the hospital in exchange for the right of a private entity to operate the asset for an agreed-upon term. These upfront payments can range from tens of millions to hundreds of millions of dollars.

Alternatively, hospitals can engage in “greenfield” structures where the underlying asset is either not yet built or needs significant capital investment. Greenfield structures typically do not result in an upfront payment to the hospital entity. Instead, (in the example of a new build) private partners would typically design, build, finance, operate and maintain the asset. The hospital still retains ownership of the underlying asset at the completion of the agreed upon term.

P3 structures can be individually tailored to suit the unique needs of the hospital entity, and the resulting benefits are multifaceted. Financially, hospitals can increase liquidity, lower operating expenses, increase debt capacity, and create headroom for financial covenants. These partnerships provide a means to raise funds without directly accessing the capital markets or undergoing the rating process. Upfront payments represent unrestricted funds and can be used as the hospital entity sees fit to further its core mission. Operationally, infrastructure P3s offer hospitals the opportunity to address deferred maintenance needs, which may have accumulated over time. Immediate capital expenditure on infrastructure facilities can enhance reliability and efficiency and contribute to meeting carbon reduction or sustainability goals. Furthermore, these structures provide a means for the hospital to transfer a meaningful amount of risk to private partners via operation and maintenance agreements.

For years, various colleges and universities have adopted the P3 model, which is emerging as a viable solution for hospitals as well. Examples of recent structures in the higher education sector include:

Fresno State University, which partnered with Meridiam (an infrastructure private equity fund) and Noresco (a design builder) to deliver a new central utility plant. The 30-year agreement involved long-term routine and major maintenance obligations from the operator, with provisions for key performance indicators and performance deductions inserted to protect the university. Fresno State is not required to begin making availability payments until construction is completed.

The Ohio State University, which secured a $483 million upfront payment in exchange for the right of a private party to operate and maintain its parking infrastructure. The university used the influx of capital to hire key faculty members and to invest in their endowment.

The University of Toledo, which received an approximately $60 million upfront payment in exchange for a 35-year lease and concession agreement to a private operator. The private team will be responsible for operating and maintaining the university’s parking facilities throughout the term of the agreement.

Ultimately, healthcare entities can learn from the successful implementation of infrastructure P3 structures in the higher education sector. The experiences of Fresno State, The Ohio State University, and the University of Toledo (among others) serve as compelling examples of the transformative potential of P3s in the healthcare sector. By unlocking the true value of non-core assets through partnerships with the private sector, hospitals can reinforce their financial stability, meet sustainability goals, reduce risk, and shift valuable focus back to the core mission of providing high-quality healthcare services.

Author’s note: Implementing P3 structures requires careful consideration and expert guidance. Given the complex nature of these partnerships, hospitals can greatly benefit from the support of experienced advisors to navigate the intricacies of the process. KeyBank and Cain Brothers specialize in guiding entities through P3 initiatives, providing valuable expertise and insight. For additional information, please refer to a recording of our recent webinar and associated summary, which can be accessed here: https://www.key.com/businesses-institutions/business-expertise/articles/public-private-partnerships-can-unlock-hospitals-hiddenvalue.html

Despite a reasonably solid third quarter, Trinity Health is still operating at a loss in its 2023 fiscal year, according to a new filing.

The health system’s fiscal year began July 1, 2022, with the latest figures covering the first nine months. Its latest operating loss shrank to $263.1 million from the prior six months’ $298 million loss. Fiscal year 2023 operating revenue currently stands at $15.9 billion, up from the same period last year.

The nonprofit health system attributed its operating revenue growth to several acquisitions (MercyOne, North Ottawa Community Health System, Genesis Health System), which collectively added $1 billion of operating revenue. Net income for the last nine months was $856.3 million, compared to $43 million in the same period the prior year.

Though inpatient volumes are stabilizing to “a new normal,” management wrote in the latest filing, most of Trinity’s revenue comes from outpatient and other non-patient revenue. Operating expenses rose $1.1 billion compared to the same period in fiscal year 2022, mostly driven by the acquisitions.

Nonoperating income was $1.2 billion during the first nine months of fiscal year 2023, up from $264.6 million in the first six months. This hike was driven partly by a $629.3 million increase in investment returns.

The health system’s operating margin was 1.6%, per the latest filing, compared to 0.1% during the same period a year ago. Margins were affected by expenses outpacing revenue, primarily driven by premium labor rates and inflation impacting supplies as well as a $137 million reduction in CARES Act grant funding.

Trinity reports $10.2 billion in unrestricted cash and investments, including 180 days cash on hand compared to 211 days in fiscal year 2022, in its latest filing.

Trinity is focused on diversifying its business by shifting to ambulatory, home health, PACE, urgent care, specialty pharmacy and telehealth. The filing also noted the recent launch of a new care delivery model dubbed TogetherTeam, involving on-site and virtual nurses, that is expected to be implemented systemwide by the end of its 2024 fiscal year.

Salaries, wages and employee benefit costs rose 2.2%, offset by a reduction of $54.6 million in executive compensation and $39.7 million more pharmacy rebates than in the same period in fiscal year 2022. Same-facility contract labor costs decreased more than 40% to $193.9 million, reflecting “unprecedented” pandemic-related costs during the third quarter in 2022.

Trinity “continues to use strong cost controls over contract labor and other operational spending as colleague investment and utilization of its FirstChoice internal staffing agency promotes labor stabilization,” management wrote.

Trinity Health spans 88 acute care hospitals and hundreds of other care locations in 26 states and purports to have the second-largest Medicare PACE (Program of All-inclusive Care for the Elderly) program in the country. It provided services to 1.3 million people and reported a community benefit and charity of $1.4 billion in fiscal year 2022.

BJC HealthCare of St. Louis and Saint Luke’s Health System of Kansas City are exploring a merger that would yield a 28-hospital, $10 billion, integrated, academic health system, the nonprofits announced Wednesday.

The two have signed a nonbinding letter of intent and “are working toward reaching a definitive agreement in the coming months” with a targeted close before the end of the year, they said. The cross-market deal would be subject to regulatory review and other customary closing conditions.

“Together with Saint Luke’s, we have an exciting opportunity to reinforce our commitment to providing extraordinary care to Missourians and our neighboring communities,” BJC HealthCare President and CEO Richard Liekweg said in the announcement. “Amid the rapidly changing health care landscape, this is the right time to build on our established relationship with Saint Luke’s. With an even stronger financial foundation, we will further invest in our teams, advance the use of technologies and data to support our providers and caregivers and improve the health of our communities.”

Both systems are based in Missouri but “serve distinct geographic markets,” they said.

St. Louis-based BJC Healthcare’s footprint is spread across the greater St. Louis, southern Illinois and southeast Missouri regions. It comprises 14 hospitals including two (Barnes-Jewish and St. Louis Children’s) affiliated with Washington University School of Medicine. It also operates multiple health service organizations providing home health, long-term care, workplace health and other offerings.

Kansas City, Missouri-based Saint Luke’s is a faith-based system with 14 hospitals and more than 100 offices throughout western Missouri and parts of Kansas. It also provides home care and hospice, adult and children’s behavioral care and a senior living community.

Should the deal close, both systems would continue to serve their existing markets and maintain their branding. The joined organization would be run from dual headquarters with BJC’s Liekweg as CEO but an initial board chair hailing from Saint Luke’s.

The organizations said their combination will expand the services available to patients and provide an estimated $1 billion in annual community benefits. The arrangement would also fuel clinical and academic research while supporting greater workforce investment.

“Our integrated health system, with complementary expertise and team of world-class physicians and caregivers, will set a new national standard for medical education and research,” Saint Luke’s President and CEO Melinda Estes, M.D., said in the announcement. “Through our decade-long relationship as a member of the BJC Collaborative, we’ve established mutual trust and respect, so the opportunity to come together as a single integrated system that can accelerate innovation to better serve patients is a logical next step.”

Years of health system consolidation have led to increased scrutiny from regulators and lawmakers, who have worried that mergers can harm competition. To date, however, efforts to block announced deals have been limited to situations where the parties are operating in the same geographic markets.

Larger, cross-market deals like BJC and Saint Luke’s have become more common in the past year, potentially due to the opportunity to distribute operational risks with limited regulatory scrutiny, analysts have noted.

Multiple health policy researchers have warned that these deals are relatively understudied and, according to some prior analyses, very rarely translate to the quality and consumer cost savings often touted by health systems.

Pennsylvania unions have filed a complaint with the Department of Justice alleging integrated hospital giant UPMC is abusing its dominant market position to suppress wages and retain workers.

On Thursday, SEIU Healthcare Pennsylvania and a coalition of labor unions filed a 55-page complaint against UPMC, the largest private employer in the state, saying the hospital system’s size has allowed it to stamp out wage growth, “drastically increase” workload and keep workers from departing to other jobs.

The unions are asking federal regulators to investigate UPMC for antitrust violations, citing its dominance of the healthcare market in select regions of Pennsylvania. UPMC denied allegations of wage suppression.

Dive Insight:

The Pittsburgh-based system has seen a rise in labor complaints, according to the unions, as the system has grown into its 41-hospital footprint through a series of mergers and acquisitions. UPMC, which also operates 800 doctors offices and clinics and a handful of health insurance offerings, reported $26 billion in operating revenue last year.

Attempts in the last decade to organize UPMC’s hourly workers have been unsuccessful, according to SEIU.

Matt Yarnell, president of SEIU Healthcare Pennsylvania, called the complaints groundbreaking on a Thursday call with reporters, saying that no entity has ever filed a complaint arguing that mobility restrictions and labor violations are anticompetitive, and in violation of antitrust law.

The complaint alleges that, for every 10% increase in market share, the wages of UPMC workers falls 30 to 57 cents an hour on average. UPMC hospital workers face an average 2% wage gap compared to non-UPMC facilities, according to a study cited in the complaint.

In addition, the labor groups allege that UPMC’s staffing ratios have fallen over the past decade, resulting in its staffing ratios being 19% lower on average compared with non-UPMC care sites as of 2020.

The unions are going after UPMC for being a “monopsony,” or a company that controls buying in a given marketplace, including controlling a large number of jobs. UPMC has some 92,000 workers, according to the complaint, and has cut off avenues of competition through non-compete agreements, in addition to preventing employees from unionizing.

“If, as we believe, UPMC is insulated from competitive market pressures, it will be able to keep workers’ wages and benefits — and patient quality — below competitive levels, while at the same time continually imposing further restraints and abuses on workers to maintain its market dominance,” the complaint states. “Because we believe this conduct is contrary to Section 2 of the Sherman Act, we respectfully urge the Department of Justice to investigate UPMC and take action to halt this conduct.”

In response to the allegations, UPMC said it has the highest entry-level pay of any provider in the state, and offers “above-industry” employee benefits. UPMC’s average wage is more than $78,000, Paul Wood, UPMC’s chief communications officer, told Healthcare Dive in a statement.

“There are no other employers of size and scope in the regions UPMC serves that provide good paying jobs at every level and an average wage of this magnitude,” Wood said.

Healthcare workers are increasingly pushing for better working conditions and pay amid the COVID-19 pandemic, as hospitals grapple with recruitment and retention issues driven by burnout and heightened labor costs.

Congressional Republicans and the White House reached a deal over the weekend to raise the debt ceiling that includes healthcare wins for both sides of the aisle, creating a path forward to prevent economic upheaval roughly a week before a potential federal default.

The 99-page agreement released Sunday to suspend the debt ceiling until January 2025 doesn’t include Medicaid work requirements, a key priority for the White House, but it does claw back billions of unspent COVID-19 relief funds.

The bill, which already faces opposition from some hard-right Republicans, could still be halted in Congress. The government could run out of money to meet its payment obligations as early as Monday without a debt ceiling increase, according to the Treasury Department, with a default threatening Medicare and Medicaid reimbursements to states and providers.

What’s in the agreement

The deal claws back roughly $30 billion in unspent pandemic relief fundsfrom dozens of programs under the CMS, National Institutes of Health and Centers for Disease Control and Prevention, among other agencies.

However, the White House did retain money for some COVID priorities. The Biden administration will retain about $5 billion to develop coronavirus vaccines and treatments in Project NextGen, and to cover the cost of those therapies for uninsured people, according to The New York Times.

The deal leaves healthcare-related federal entitlement programs mostly untouched, a key win touted by the White House in its messaging to Democrats. Despite being targeted by Republicans during negotiations, Medicare, Medicaid and the Inflation Reduction Act emerged unscathed.

Medicaid was particularly at risk. Though the final agreement excludes Medicaid work requirements, last month Republicans in the House passed a debt ceiling bill that would have included the controversial policy. Those requirements would have resulted in an estimated 600,000 people being booted from the safety-net insurance coverage, according to the Congressional Budget Office.

“One thing this budget deal suggests: Democrats won’t go along with Republican proposals to cut or impose restrictions on Medicaid,” tweeted Larry Levitt, executive vice president of health policy at the Kaiser Family Foundation.

If passed, however, the deal would enact work rules for people receiving federal food stamps and those on the family welfare benefits program. Veterans and homeless people would be exempt from food stamp work requirements.

Those provisions put food assistance at risk for very low-income older adults, and “will increase hunger and poverty among that group,” nonpartisan think tank the Center on Budget and Policy Priorities said in a statement on the bill.

The agreement also increases funding for the Cost of War Toxic Exposures Fund, created by bipartisan legislation last summer that expanded healthcare and disability benefits for veterans exposed to toxic burn pits.

The House Rules Committee, which includes a number of critics of House Speaker Kevin McCarthy, R-Calif., who spearhead the negotiations for Republicans, will discuss the legislation Tuesday afternoon.

A full House vote on the bill could come as soon as Wednesday. Senate Majority Leader Chuck Schumer, D-N.Y., has said the Senate will immediately move to consider the bill once it leaves the House.

Healthcare’s most recent billion-dollar deal took the industry by surprise, leaving medical experts and hospital leaders grappling to comprehend its implications.

In case you missed it, California-based Kaiser Foundation Health Plan and Hospitals, which make up the insurance and facilities half of Kaiser Permanente, announced the acquisition of Geisinger, a Pennsylvania-based health system once acknowledged by President Obama for delivering “high-quality care.”

Upon regulatory approval, Geisinger will become the first organization to join Risant Health, Kaiser Foundation’s newly created $5 billion subsidiary. According to Kaiser, the aim is to build “a portfolio of likeminded, nonprofit, value-oriented, community-based health systems anchored in their respective communities.”

Having spent 18 years as CEO of The Permanente Medical Group, the half of Kaiser Permanente responsible for the delivery of medical care, I took great interest in the announcement. And I wasn’t alone. My phone rang off the hook for weeks with calls from reporters, policy experts and healthcare executives.

After hundreds of conversations, here are the three most common questions I received about the acquisition—and the implications for doctors, insurers, health-system competitors and patients all over the country.

Question 1: Why did Kaiser acquire Geisinger?

Most callers wanted to know about Kaiser’s motivation, figuring there must’ve been more to the acquisition than the press release indicated. Although I don’t have inside information, I believe they were right. Here’s why:

Kaiser Permanente has a long and ongoing reputation for delivering nation-leading care. The organization has consistently earned the highest quality and patient-satisfaction rankings from the National Committee for Quality Assurance (NCQA), Leapfrog Group, JD Power and Medicare.

And yet, despite a 78-year history, dozens of hospitals and 13 million members across eight states, Kaiser Permanente is still considered a coastal—not national—health system. It maintains a huge market share in California and a strong presence in the Mid-Atlantic states, yet the organization has failed repeatedly to replicate that success in other geographies.

With that context, I see two compelling reasons why the Kaiser Foundation Health Plan and Hospitals wish to become a national brand:

Influence. Elected officials and regulatory bodies often turn to healthcare’s biggest players to set legislative agendas and carve out national policy. At that table, there are a limited number of seats. By shedding its reputation as a “local” health system, Kaiser could earn one.

Survival. In recent years, companies like Amazon, CVS and Walmart have been scooping up organizations that provide primary care, telehealth, home health and specialty care services. These “retail giants” are spending up to $13 billion per acquisition. And they’re consuming already-successful healthcare companies like One Medical, Oak Street Health, Signify, Pill Pack and many others. Like an army preparing for war, these corporate behemoths are amassing the components needed to battle the traditional healthcare incumbents and ultimately oust them entirely.

The Geisinger deal expands Kaiser’s footprint, adding 600,000 patients, 10 hospitals and 100 specialty and primary care clinics. These assets lend gravitas, even though Geisinger also comes with a 2022 operating loss of $239 million.

The lesson to draw from this first question is clear: size matters. The days of solo physicians and stand-alone hospitals are over. Nostalgia for medicine’s folksy, home-spun past is understandable but futile. To survive, healthcare players must get bigger quickly or team up with someone who can. That insight leads to the next question and lesson.

Question 2: How much value will Kaiser give Geisinger?

Almost everyone I’ve spoken with understands Kaiser’s desire for greater national influence, but they’re less sure how this deal will affect Geisinger Health.

Geisinger’s Pennsylvania-based hospitals and clinics have been locked in territorial battles for years with surrounding health systems. More recently, the pandemic, combined with staffing shortages and national inflation, have challenged Geisinger’s clinical performance and eroded its bottom line.

Assuming Kaiser plans to invest roughly $1 billion in each of the four to five health systems it’s planning to acquire, that surge in cash inflow will provide Geisinger with temporary financial safety. But the bigger question is how will Kaiser improve Geisinger’s value-proposition enough to grow its market share?

In public comments, Kaiser leaders spoke of the acquisition as an opportunity for Risant to “improve the health of millions of people by increasing access to value-based care and coverage, and raising the bar for value-based approaches that prioritize patient quality outcomes.”

Many of the experts I spoke with understand Kaiser’s value intent. But they question how Kaiser can could deliver on that promise since The Permanente Medical Group (TPMG) wasn’t involved in the deal.

If, hypothetically, Kaiser and Permanente leaders were to strike a deal to collaborate in the future, TPMG’s physician leaders could bring tremendous knowledge, experience and expertise to the table. Otherwise, I agree with those who’ve expressed doubt that Kaiser, alone, will be able to significantly improve Geisinger’s clinical performance.

Health plans and insurance companies play an important role in financing medical care. They possess rich data on performance and can offer incentives that boost access to higher-quality care. But insurers don’t work directly with individual doctors to coordinate medical care or advance clinical solutions on behalf of patients. And without strong physician leadership, the pace of positive change slows to a crawl. As a example, research conducted within The Permanente Medical Group found that it takes only three years to turn a proven clinical advance into standard practice—that’s nearly six times faster than the national average.

For decades, the secret sauce for Kaiser Permanente has been the cohesive success of its three parts: Kaiser Health Plan, Kaiser Foundation Hospitals and The Permanente Medical Group.

And KP’s results speak for themselves:

90% control of hypertension for members (compared to 60% for the rest of the country)

30% fewer deaths from heart attack and stroke (compared to the rest of the country)

20% fewer deaths from colon cancer

The big lesson: insurance, by itself, doesn’t drive major improvements in medicine. It must be a combined effort between forward-looking insurers and innovative, high-performing clinicians.

But there’s another takeaway here for doctors everywhere: now is the time to join forces with other clinicians in your community. Together, you can collaborate to improve clinical quality. You can augment access and make care more affordable for patients. Simultaneously, this is the time for the insurers and the retail giants to figure out which medical groups can deliver the best care and make the best partners. Neither side will flourish alone. And this leads to a third question and lesson.

Question 3: Will the deal work?

Almost all of my conversations ended with this query. I say it’s too early to tell. But as I look years down the road, one part of the deal, in particular, gives me doubt.

Today, Geisinger uses a hybrid reimbursement model—blending both “value-based” care payments with traditional “fee-for-service” insurance plans. In addition to offering its own coverage, it contracts with a variety of other insurance companies. Rarely have I seen this scattered approach succeed.

Most healthcare observers understand the inherent flaw in the “fee for service” (FFS) model is also its greatest appeal to providers: the more you do the more you earn. FFS is how nearly all financial transactions take place in America (i.e., provide a service, earn a fee). In medicine, however, this financial model results in frequent over-testing and over-treatment with minimal if any improvement in clinical outcomes, according to researchers.

The “value-based” alternative to FFS involves prepaying for care—a model often referred to as “capitation.” In short, capitation involves a single fee, paid upfront for all the medical care provided to a defined population of patients for one year based on their age and health status. The better an organization at preventing disease and avoiding complications from chronic illness, the greater its success in both clinical quality and affordability.

Within the small world of capitated healthcare payments, there’s an important element that often gets overlooked. It makes a big difference who receives that lump-sum payment.

In the case of Kaiser Permanente, capitated payments are made directly to the medical group and the physicians who are responsible for providing care. In almost every other health system, an insurance company collects capitated payments but then pays the medical providers on a fee-for-service basis. Even though the arrangement is referred to as capitated, the incentives are overwhelmingly tied to the volume of care (not the value of that care).

In a mixed-payment model, doctors and hospitals invariably prioritize the higher paying FFS patients over the capitated ones. When I think about these conflicting incentives, I’m reminded of a prominent medical group in California. It had a main entrance for its fee-for-service patients and a second, smaller one off to the side for capitated patients.

I doubt the time spent with the patient—or the overall care provided—was equal for both groups. When income is based on quantity of care, not quality, clinicians focus more on treating the complications of chronic disease and medical errors rather than preventing them in the first place. Geisinger has walked this tightrope in the past, but as economic pressures mount, I fear doctors will find the two sets of incentives conflicting and difficult to navigate.

The big lesson: as financial pressures mount, the most effective approaches of the past will likely fail in the future. All healthcare organizations will need to make a decision: keep trying to drive volume and prices up through FFS or shift to capitation. Getting caught in the middle is a prescription for failure.

Examining the healthcare acquisitions made by Amazon and CVS, it’s clear these giants have decided to move aggressively toward a model more like Kaiser Permanente’s—one that brings insurance, pharmacy, physicians and sophisticated IT systems under one roof. These companies, along with Walmart, are aggressively marching down a path toward capitation, focusing on Medicare Advantage (the value-based option for Americans 65+) as an entry point.

So far, Geisinger has hedged its bets by maintaining a hybrid revenue stream. I doubt they can do so successfully in the future. That brings us to a final question.

The biggest question remaining

Over the next decade, hospital systems, insurers and retailers will battle for healthcare supremacy. The most recent Kaiser-Geisinger deal reflects an industry that’s undergoing massive change as health systems face intensifying pressure to remain relevant.

The most important issue to resolve is whether these shifts will ultimately help or harm patients. I’m optimistic for a positive outcome.

Whether or not the retail giants displace the incumbents, they will redefine what it takes to win. For all their faults, companies like Amazon and Walmart care a lot about meeting the needs of customers—a mindset rarely found in today’s healthcare world. As these companies grow ever larger, they’ll place consumer-oriented demands on doctors and hospitals. This will require care providers to deliver higher quality care at more affordable prices.

The retailers will only do deals with the best of the best. And they’ll kick the underachievers to the curb. They’ll use their sophisticated IT systems to better coordinate and innovate medical care. Insurers, hospitals and doctors who fail to keep up will be left behind.

Over time, patients will find themselves with far more choices and control than they have today. And I’m optimistic that will be good for the health of our nation.

A decline in COVID-19 funding and sustained expenses issues helped lead St. Louis-based Ascension to a $1.8 billion operating loss in the nine months ending March 31.

The nine-month loss was on revenue of $21.3 billion. In the quarter ending March 31, the 140-hospital system reported an operating loss of $1.4 billion on $6.9 billion in revenue.

Such losses compared with $640 million and $671 million deficits in the nine-month and three-month periods, respectively, ending March 31, 2022.

Expenses for the nine-month period increased 3.7 percent on the previous year to total $22.3 billion.

“The reduction in COVID-19 funding negatively impacted revenue in the current year,” Ascension management said in the filing. “Additionally, challenges to expenses continue to persist resulting from the inflationary environment.”

The operating losses were offset by improved non-operating income in the first three months of 2023 but not over the nine-month period, which saw a net deficit of $1.9 billion.

Ascension, which operates 2,600 sites of care across 19 states and Washington, D.C., had 219 days of cash on hand as of March 31 compared with 259 at the same time last year.