Peter Drucker, the hall of fame management guru, once famously said that the hardest business organization to run in America was a hospital. If that comment was true so many years ago, imagine what Drucker would have to say about the difficulty of hospital management right now.

Hospital financial performance suffered significantly in 2022 and recovery during 2023 has been quite slow. This trend suggests the question,

“What steps are hospital C-suites taking to recover pre-Covid financial stability?”

Erik Swanson manages all analyses for our monthly Kaufman Hall Flash Report and he and I speculated that an industry-wide hospital recovery could not be achieved without reductions in force across the hospital ecosystem. Some research on our part determined that no official organization tracks hospital layoffs over time but we wondered if we could use our Flash Report data, which is provided to us by Syntellis Performance Solutions, to reach an informed conclusion.

What we were able to do was prepare three types of charts, as follows:

The first chart measures net employee percentage change by month. This chart shows whether overall hospital employment is increasing or decreasing over time and by how much.

The second chart attempts to establish the median turnover for hospitals over an annual period and then measure the deviation from that turnover rate. A greater deviation from what might be termed “normal turnover” suggests that an increasing number of hospitals are using reductions in force to more quickly reduce the cost of doing business.

The third chart shows average FTEs per occupied bed on a comparative basis looking at month-to-month and year-to-year statistics.

The first chart, Net Employee Percentage Change by Month, begins at January 1, 2018, and continues to March 1, 2023 (Figure 1). Overall additions to hospital employment remained generally positive through January 1, 2020. Overall hospital employment then went generally negative from March 2020 (the onset of Covid restrictions) to March 2022. The reductions in hospital employees during this period were likely the result of the “great resignation” during the worst of the Covid pandemic. But then, from July 2022 to March 2023, overall hospital employees demonstrated by the Flash Report dropped dramatically with an overall 2% decrease at the March 2023 date. This statistic suggests more than simply increased hospital turnover, but rather a formal layoff process initiated across many hospital organizations, along with aggressive management of contract labor.

Figure 1: Net Employee Percentage Change by Month

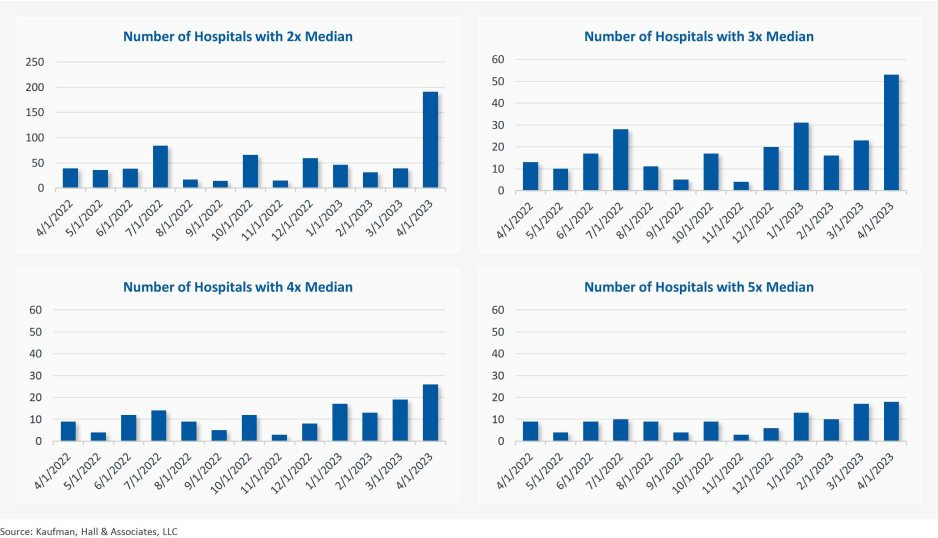

The second chart demonstrates the deviation from expected turnover at levels of 2x, 3x, 4x, and 5x by number of hospitals (Figure 2). No matter which measure you examine, the deviation of employees from expected turnover spiked significantly in April 2023 and even more so in May 2023. This again suggests the aggressive management of labor costs that likely could not occur without the intentional reduction of actual positions and/or the cost of these positions.

Figure 2: Number of Hospitals with Deviations from Expected Turnover at 2x, 3x, 4x, and 5x the Median

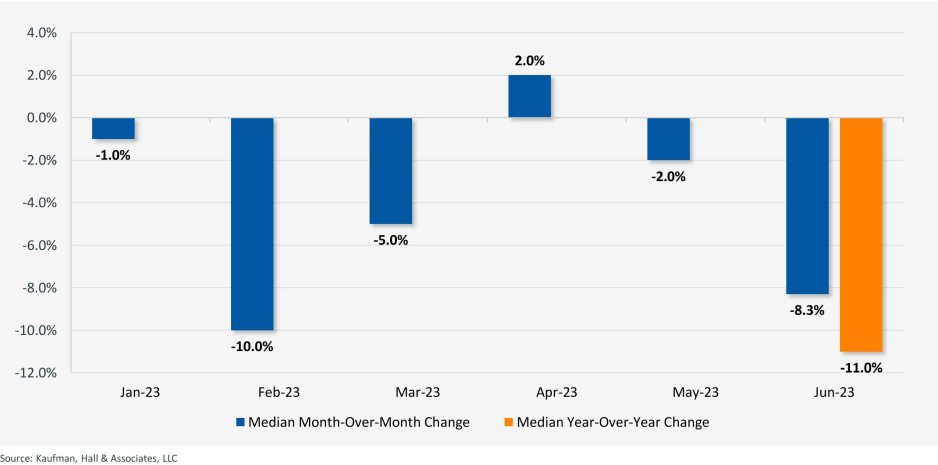

The last chart provides a remarkable set of observations (Figure 3). FTEs per adjusted occupied bed (AOB) declined by 8.3% between June 2023 and July 2023. The year-over-year variation for July 2023 was a decline of 11.01%. Our data further reveals that the FTE per AOB statistic has declined in five of the past six months on a month-over-month basis.

Figure 3: Median Change in FTEs per Adjusted Occupied Bed by Month

The conclusion here is that the return of the hospital industry to pre-Covid financial results has been no walk in the park. 2022 was, of course, a dismal financial year for the hospital industry. And while 2023 has shown improvement, the usual management steps to recovery have been only moderately effective. The data and analysis above demonstrate that C-suites across America are moving to stronger measures to assure the financial survivability and competitiveness of their organizations.

There is no revenue solve here, or at least not in the current environment: costs must come down and they must come down materially. From the sense and the trend of the data it would seem that hospital executive teams get the joke.

Value-based healthcare, the holy grail of American medicine, has three parts: excellent clinical quality, convenient access and affordability for all.

And as with the holy grail of medieval legend, the quest for value-based care has been filled with failure.

In the 20th century, U.S. medical groups and hospital systems could—at best—achieve two elements of value-based care, but always at the sacrifice of the third. Until recently, American medicine lacked the clinical knowhow, technology and operational excellence to accomplish all three, simultaneously. We now have the tools. The only thing missing is “system-ness.”

What Is System-ness?

System-ness is the effective and efficient coordination of healthcare’s many parts: outpatient and inpatient, primary and specialty care, financing and care delivery, prevention and treatment.

By bringing these disparate pieces together within a well-functioning system, healthcare providers have the opportunity to maximize clinical outcomes, weed out waste, lower overall costs and provide greater levels of convenience and access.

Who Are The Search Parties?

In the future, system-ness will be the variable that determines whether healthcare transformation is led by (a) incumbent health systems like Kaiser Permanente and Geisinger Health or (b) the retail giants like Amazon, CVS and Walmart. The latter group has become an ever-growing threat in the healthcare arms race, quickly amassing their own (though still modest) systems of care through billion-dollar acquisitions.

Although both the incumbents and new entrants will struggle to implement value-based care on a national scale, the victor stands to earn hundreds of billions of dollars in added revenue and tens of billions in profits.

To better understand the power of system-ness, and the challenges all organizations will face in providing it, here are three examples of value-based-care solutions implemented successfully by Kaiser Permanente.

1. Preventing Problems, Managing Disease

Research demonstrates that preventive medicine and early intervention reduce heart attacks, strokes and cancer. Yet our nation falls far short in these areas when compared to its global peers.

One example is hypertension, the leading cause of strokes and a major contributor to heart attacks. With help from doctors, nearly all patients can keep high blood pressure under control. Yet, nationally, hypertension is controlled only 60% of the time.

We see similarly poor rates of performance when it comes to prevention and screening for cancers of the colon, breast and lung.

Undoing these troubling trends requires system-ness. In Kaiser Permanente, 90% of patients had their blood pressure controlled and were screened for cancer. Getting there required a comprehensive electronic health record, a willingness for every doctor (regardless of specialty) to focus on prevention, leadership that communicated the value of prevention and a salary structure that rewarded group excellence.

2. Continuous Care, Without Interruption

Most doctors’ offices are open Monday to Friday during normal business hours—only one-fourth of the time that a medical problem might occur.

At night and on weekends, patients have no choice but to visit ERs. There, they often wait hours for care, surrounded by people with communicable diseases. Their non-emergent problems generate bills 12-times higher than if they’d waited to be seen in a doctor’s office.

There’s a better way. In large-enough medical groups, hundreds of clinicians can provide round-the-clock care on a rotating, virtual basis—using video to assess patients and make evidence-based recommendations.

This approach, pioneered by physicians in the Mid-Atlantic Permanente Medical group, solved the patient’s problem immediately 70% of the time without a trip to the ER and, for the other 30%, enabled coordination of medical care with the ER staff.

3. Specialized Medicine, Immediate Attention

When a primary care physician needs added expertise (from a dermatologist, urologist or orthopedist), it’s usually the responsibility of the patient to make their own specialty appointments, check with insurance for coverage and provide their medical records.

This takes hours or days to coordinate and can delay care by weeks, resulting in avoidable complications.

But in a well-structured system, there’s no need to wait. Using telehealth tools at Kaiser Permanente, primary care doctors can connect instantly with dozens of different specialists—often while the patient is still in the exam room. Once connected, the specialist evaluates the patient and provides immediate expertise.

This way, care is not only faster and less expensive, but also better coordinated. Data from within Kaiser Permanente show that these virtual consultations resolve the patient’s problem 40% of the time without having to schedule another appointment. For the other 60%, the diagnostic process can begin immediately.

The Foundations For System-ness

Few organizations in the U.S. can or do offer these system-based improvements. Doing so requires skilled physician leadership, a shift in the financial model and a willingness to accept risk.

In fact, most organizations across the U.S. that claim to operate “value-based” systems actually rely on doctors who are scattered across the community, disconnected from each other and paid on the basis of volume (fee-for-service) rather than value (capitation).

As a result, patient care is fragmented and uncoordinated, leading to repeated tests and ineffective treatments, thus increasing medical costs and compromising medical outcomes.

Value-based care (superior quality, access and affordability) requires teams of clinicians working together as one—all paid on a capitated basis.

Without capitation, dermatologists will insist on seeing every patient in their office where they can bill insurance five-times more than with a tele-dermatology visit. And gastroenterology specialists will insist that all patients have colonoscopy rather than recommending low-risk patients do a safe, convenient, at-home colon cancer screening (called a fecal immunochemical test or “FIT”) at 5% of the cost.

In these cases, individual doctors don’t consciously make care inconvenient for patients. Rather, it is the only choice they have when working in a fee-for-service payment model. Ultimately, system-ness is best achieved when health systems are integrated, prepaid, tech-enabled and physician-led.

Amazon, CVS, Walmart Know About Systems

These three companies are global leaders in “system-ness,” at least in retail. Combined, they have a market cap of $1.88 trillion, employ 3.4 million Americans and are looking to take a slice of U.S. healthcare’s $4.3 trillion annual expenditures.

Already, they manage complex order-entry and fulfillment systems. They use technology to streamline everything from customer service to supply-chain management. They are led through a clear and effective reporting structure.

In terms of competing for healthcare’s holy grail, these are huge competitive advantages compared to today’s uncoordinated, individualized, leaderless healthcare industry.

As retailers vie to bring their system knowhow to American medicine, they are acquiring the pieces needed to compete with the healthcare incumbents. They’ve spent tens of billions of dollars on medical groups that are committed to value-based care (One Medical, Oak Street Health, etc.). They’ve also spent massive sums on home-health companies (Signify) and on pharmacies (PillPak), along with expanding their in-store, at-home and online care options. Many of these care-delivery subsidiaries are focused on Medicare Advantage, the capitated half of Medicare where financial success is dependent on high quality medical care provided at lower cost.

What’s more, all these retailers have a national presence with brick-and mortar facilities in nearly every community in the country—a leg up on nearly every existing health system.

Who Will Win—And Why?

Trying to pick the victor in the battle to transform American medicine at this point is like selecting the winner of a heavy-weight championship boxing match after three evenly matched rounds. Intangibles like stamina, courage and willingness to absorb pain have yet to be tested.

In The Innovator’s Dilemma, the late Clayton Christensen examined historical battles between incumbent organizations and new entrants. After analyzing dozens of industries, he concluded new entrants routinely become the victors because the incumbents move too slowly and fail to embrace the need for major change.

And from that perspective, if I had to wager, I’d put my money on the retail giants.

But there’s an even more worrisome potential outcome: neither those inside nor outside of healthcare will make the necessary investments or accept the risk of leading systemic change. As a result, the movement toward value-based healthcare will stall and die.

In that context, purchasers of healthcare (businesses, the government and patients) will encounter a difficult reality: over the next eight years, medical costs will nearly double, creating an unaffordable and unsustainable scenario. As a result, our nation will likely experience reduced medical coverage, increased rationing, ever-longer delays for care and a growth in health disparities.

If that day arrives, our country will regret its inaction.

In behavioral economics, the sunk cost fallacy describes the tendency to carry on with a project or investment past the point where cold logic would suggest it is not working out. Given human nature, the existence of the sunk cost fallacy is not surprising. The more resources—time, money, emotions—we devote to an effort, the more we want it to succeed, especially when the cause is an important one.

Under normal circumstances, the sunk cost fallacy might qualify as an interesting but not especially important economic theory. But at the moment, given that 2022 will likely be the worst financial year for hospitals since 2008 and given that the hospital revenue/expense relationship seems to be entirely broken, there is little that is theoretical about the sunk cost fallacy. Instead, the sunk cost fallacy becomes one of the most important action ideas in the hospital industry’s absolutely necessary financial recovery.

Historically, cases of the sunk cost fallacy can be relatively easy to spot. However, in real time, cases can be hard to identify and even harder to act on. For hospital organizations that are subsidizing underperforming assets, identifying and acting on these cases is now essential to the financial health of most hospital enterprises.

For example, perhaps the asset that isunderperforming is a hospital acquired by a health system. (Although this same concept could apply to a service line or a related service such as a skilled nursing facility, ambulatory surgery center, or imaging center.) The costs associated with integrating an acquired hospital into a health system are typically significant. And chances are, if the hospital was struggling prior to the acquisition, the purchaser made substantial capital investments to improve the performance.

As time goes on, if the financial performance of the entity in question continues to fall short, hospital executives may be reluctant to divest the asset because of their heavy investment in it.

This understandable tendency can lead the acquiring organization to throw good money after bad. After all, even when an asset is underperforming, it can’t be allowed to deteriorate. In the case of hospitals, that’s not just a matter of keeping weeds from sprouting in the parking lot. The health system often winds up supporting an underperforming hospital with both working capital and physical capital, which compounds the losses.

And the costs don’t stop there, because other assets in the system are supporting the underperforming asset. This de facto cross-subsidy has been commonplace in hospital organizations for decades. Such a cross subsidy was probably never sustainable, but it is even less so in the current challenging financial environment.

This is a transformative period in American healthcare, when hospital organizations are faced with the need to fundamentally reinvent themselves both financially and clinically. The opportunity costs of supporting assets that don’t have an appropriate return are uniquely high in such an environment. This is true whether the underperforming asset is a hospital in a smaller system, multiple hospitals in a larger system, or a service line within a hospital.

The money that is being funneled off to support underperforming assets may be better directed, for example, toward realigning the organization’s portfolio away from inpatient care and toward growth strategies. In some cases, the resources may be needed for more immediate purposes, such as improving cash flow to support mission priorities and avoiding downgrades of the organization’s credit rating.

The underlying principle is straightforward:

When a hospital supports too many low-performing assets, the capital allocation process becomes inefficient. Directing working capital and capital capacity toward assets that are dilutive to long-term financial success means that assets that are historically or potentially accretive don’t receive the resources they need to grow and thrive. The underlying principle is a clear lose-lose.

In the highly challenging current environment, it is especially important for boards and management to recognize the sunk cost fallacy and determine the right size of their hospital organizations—both clinically and financially.

Some leadership teams may determine that their organizations are too big, or too big in the wrong places, and need to be smaller in order to maximize clinical and balance-sheet strength. Other leadership teams may determine that their organizations are not large enough to compete effectively in their fast-changing markets or in a fast-changing economy.

Organizational scale is a strategy that must be carefully managed. A properly sized organization maximizes its chances of financial success in this very difficult inflationary period. Such an organization invests consistently in its best performing assets and reduces cross-subsidies to services and products that have outlived their opportunity for clinical or financial success.

Executives may see academic economic theory as arcane and not especially relevant. However, we have clearly entered a financial moment when paying attention to the sunk cost fallacy will be central to maintaining, or recovering, the financial, clinical, and mission strength of America’s hospitals.

In an era of significant medical debt, rising healthcare costs and delayed treatments, our current healthcare system is ripe for solutions that alleviate the burden of paying patient bills.

Enter embedded finance. While not a new concept by any stretch – it has long existed in retail – fintechs and traditional banks are determined to give patients more options and a fundamentally better experience in the way they pay for healthcare services. In doing so, a financially strained domestic healthcare system stands to benefit from increased cash flow, improved health equity and optimized patient engagement.

Simply put, embedded finance is the integration of financial services – such as payment, lending, banking and insurance features – into another company’s normal service or products. We have all undoubtedly come across these offerings in our daily lives as consumers. Think private label credit cards with retail chains or airlines, digital wallet purchase options at the Amazon checkout, a buynow-pay-later (BNPL) plan from Affirm or Klarna, or insurance obtained from a car rental.

The goal of embedded finance:

is to improve a user’s experience by accessing financial services without leaving a brand’s platform. By layering application programming interface (API)-driven fintech or banking capabilities on top of a website or mobile app for, say, a hospital patient portal, the bundled solution allows the user to stay on one website or application to complete a financial transaction. Doing so removes friction in the experience and delivers a breadth of contextual information that a provider or payer can use to prompt further action on the patient’s medical journey.

The implications for embedded finance in healthcare are vast and benefit every stakeholder across the revenue cycle value chain:

Patients: Flexibility and convenience to better structure and plan bill payment while receiving greater access to financial options and additional services that improve the care experience such as reminders and health tracking

Providers: Faster and higher rates of collections coupled with ongoing patient dialogue that cements loyalty, affords clinicians the opportunity to suggest customized treatment options, and improves revenue composition and potential valuation

Payers: More efficient claims processing cycle, automated processes and improved data security

The burden of patient bills and increasing medical costs are not new to our system. Yet there has been a confluence of fundamental changes that make embedded finance particularly attractive in healthcare going forward, including increased smartphone usage and Internet penetration, COVID19 adoption of fintech products across healthcare settings, rising inflation rates that reduce a patient’s ability to pay and the adoption of mobile-based apps among younger, digitally native consumers and lower income patients.

These tailwinds support a massive addressable market as healthcare is expected to comprise approximately 23% of a U.S. embedded finance industry set to exceed $230 billion by 2025, or a 10x increase from $23 billion in 2020.

Significant attention and capital investment are accelerating the rise of embedded finance in healthcare.

Punctuated by attractive elements at the intersection of technology, financial services and healthcare sectors, nimble fintech companies and large financial institutions alike are competing for market presence. For example, pioneering healthcare-focused fintech PayZen closed $220 million in fresh capital in late 20223, while banks such as Wells Fargo and Synchrony have launched the popular medical-focused credit cards Health Advantage and CareCredit, respectively. Cain Brothers’ parent company, KeyBank, has also advanced an embedded strategy to provide healthcare digital innovation at scale and enhance patient experiences by acquiring XUP Payments in 2021. The resulting U.S. landscape for healthcare embedded finance is one that is evolving rapidly and that we are monitoring closely for investment and eventual M&A consolidation.

With expanding options around the type of medical care received and where it is received, we expect the financial tools at a patient’s disposal to garner significant attention in the years to come.

Embedded finance is a leading solution positioned to improve health equity and the financial well-being of millions of patients across the U.S., as well as fuel sector growth. Just as we’re accustomed now to buying pretty much anything with a few clicks, so too will embedded finance become a ubiquitous part of the healthcare landscape.

From time to time the blogging process stimulates a conversation between the author and the audience. This type of conversation occurred after the publication of my recent blog, “The Hospital Makeover—Part 2.” This blog focused entirely on the current problems, financial and otherwise, of the hospital physician employment model. I received responses from CEOs and other C-suite executives and those responses are very much worth adding to the physician employment conversation. Hospital executives have obviously given the physician employment strategy considerable thought.

One CEO noted that, looking back from a business perspective, physician employment was not actually a doctor retention strategy but, in the long run, more of a customer acquisition and customer loyalty strategy.

The tactic was to employ the physician and draw his or her patients into the hospital ecosystem. And by extension, if the patient was loyal to the doctor, then the patient would also be loyal to the hospital. Perhaps this approach was once legitimate but new access models, consumerism, and the healthcare preferences of at least two generations of patients have challenged the strategic validity of this tactic.

The struggle now—and the financial numbers validate that struggle—is that the physician employment model has become extraordinarily expensive and, from observation, does not scale.

Therefore, the relevant business question becomes what are the most efficient and durable customer acquisition and loyalty models now available to hospitals and health systems?

A few more physician employment observations worth sharing:

Primary Care. The physician employment model has generally created a one-size-fits all view of primary care. Consumers, however, want choice. They want 32 flavors, not just vanilla. Alternative primary care models need to match up to fast-changing consumer preferences.

Where Physician Employment Works. In general, the employment model has worked where doctor “shift work” is involved. This includes facility-based specialists such as emergency physicians, anesthesiologists, and hospitalists.

Chronic Care Management. Traditional physician employment models that drive toward doctor-led physical clinics have generally not led to the improved monitoring and treatment of chronic care patient problems. As a result, the chronic care space will likely see significant disruption from virtual and in-home tools.

All in all, the four very smart observations detailed above continue the hospital physician employment conversation. Please feel free to add your thoughts on this or on other topics of hospital management which may be of interest to you. Thanks for reading.

Mountain View, Calif.-based El Camino Health ended the first quarter with an impressive operating margin of 10.2 percent when many health systems saw their margins hover above zero or fall into the red. The system’s revenue for the quarter totaled $131,290.

For the nine months ended March 31, the two-hospital system posted an operating gain of $141.4 million on revenue of just over $1 billion.

However, like most health systems, El Camino’s expenses are substantially higher than the same period last year, increasing 10.6 percent year over year for the nine months ending March 31, 2023, to $881.9 million.

The system is making a conscious effort to march down labor costs while also placing a significant emphasis on retention. In June, El Camino agreed a deal to increase pay for nurses by 16 percent over three years.

“Like nearly all hospitals, our nursing staff comprises the largest part of our workforce. With the recruitment of a single nurse estimated to be nearly $60,000, our primary strategy to reduce labor costs is to focus on decreasing turnover,” El Camino CEO Dan Woods told Becker’s.

“Our turnover rate for nurses is just about 8 percent while the turnover rate nationally is still running at 22 percent.”

In March, the system also received a credit rating upgrade from Moody’s, which noted the system’s “superlative cash metrics and operating performance.” Fitch Ratings also revised El Camino’s outlook to positive in February, noting that the system has a history of generating double-digit operating EBITDA margins, driven by a solid market position that features strong demographics and a very healthy payer mix.

At least 17 health systems announced changes to executive ranks and administration teams in 2023.

The changes come as hospitals continue to grapple with financial challenges, leading some organizations to cut jobs and implement other operational adjustments.

The following changes were announced within the last two months and are summarized below, with links to more comprehensive coverage of the changes.

1. Middletown, N.Y.-based Garnet Healthlaid off 49 employees, including 25 leaders, to offset recent operating losses. The reductions represent 1.13 percent of the organization’s total workforce and $13 million in salaries and benefits.

2. Greensburg, Pa.-based Independence Health Systemlaid off 53 employees and has cut 226 positions — including resignations, retirements and elimination of vacant positions — since January, The Butler Eagle reported June 28. The 226 reductions began at the executive level, with 13 manager positions terminated in March.

3. Coral Gables-based Baptist Health South Florida is offering its executives at the director level and above a “one-time opportunity” to apply for voluntary separation, according to a June 29 Miami Herald report. Decisions on buyout applications will be made during the summer.

4. MultiCare Health System, a 12-hospital organization based in Tacoma, Wash., will lay off 229 employees, or about 1 percent of its 23,000 staff members, including about two dozen leaders, as part of cost-cutting efforts, the health system said June 29. The layoffs primarily affect support departments, such as marketing, IT and finance.

5. Seattle Children’s is eliminating 135 leader roles, citing financial challenges. The management restructuring and reduction affects 1.5 percent of employees across the organization.

6. Bonnie Panlasigui was tapped as the first president of Summa Health System Hospitals.This new role was first announced in October as the Akron, Ohio-based system made 10 changes to its executive team: reshuffling three leaders’ roles, adding three positions and eliminating four.

7. Allentown, Pa.-based Lehigh Valley Health Network named two new regional and hospital presidents. Bob Begliomini, PharmD, was appointed president of Lehigh Valley Hospital-Cedar Crest campus in Allentown, according to a news release shared with Becker’s. He will also lead the health system’s Lehigh region, which includes four hospital campuses. Jim Miller, CRNA, was selected to replace Mr. Begliomini as president of the Muhlenberg hospital. He was also named president of the health system’s Northampton region, which includes three hospitals, Muhlenberg being one of them.

8. McLaren St. Luke’s Hospital in Maumee, Ohio, will lay off 743 workers, including 239 registered nurses, when it permanently closes this spring. Other affected roles include physical therapists, radiology technicians, respiratory therapists, pharmacists and pharmacy support staff, and nursing assistants. The hospital’s COO is also affected, and a spokesperson for McLaren Health Care told Becker’s other senior leadership roles are also affected.

9. Habersham Medical Center in Demorest, Ga., laid off four executives. The layoffs were part of cost-cutting measures before the hospital joined Gainesville-based Northeast Georgia Health System.

10. Grand Forks, N.D.-based Altru Health announced it would trim its executive team as its new hospital project moves forward. The health system is trimming its executive team from nine to six and incentivizing 34 other employees to take early retirement.

11. Scripps Healtheliminated 70 administrative roles, according to WARN documents filed by the San Diego-based health system in March. The layoffs took effect May 8 and affect corporate positions in San Diego and La Jolla, Calif.

12. Columbia-based University of Missouri Health Care announced it would eliminate five hospital leadership positions across the organization. According to MU Health Care, the move is a result of restructuring “to better support patients and the future healthcare needs of Missourians.”

13. Winston-Salem, N.C.-based Novant Healthlaid off about 50 workers, including C-level executives, the health system confirmed to Becker’s March 29. The layoffs affected Jesse Cureton, the health system’s executive vice president and chief consumer officer since 2013; Angela Yochem, its executive vice president and chief transformation and digital officer since 2020; and Paula Dean Kranz, vice president of innovation enablement and executive director of the Novant Health Innovation Labs.

14. Philadelphia-based Penn Medicine announced that it would eliminate administrative positions. The change is part of a reorganization plan to save the health system $40 million annually, the Philadelphia Business Journal reported March 13. Kevin Mahoney, CEO of the University of Pennsylvania Health System, told Penn Medicine’s 49,000 employees changes include the elimination of a “small number of administrative positions which no longer align with our key objectives,” according to the publication.

15. Sovah Health, part of Brentwood, Tenn.-based Lifepoint Health, eliminated the COO positions at its Danville and Martinsville, Va., campuses. The responsibilities of both COO roles are now spread across members of the existing administrative team.

16. Valley Health, a six-hospital health system based in Winchester, Va., eliminated 31 administrative positions. The job cuts are part of the consolidation of the organization’s leadership team and administrative roles. They were announced internally on Feb. 28.

17. Roseville, Calif.-based Adventist Healthannounced it would transition from seven networks of care to five systemwide to reduce costs and strengthen operations. Under the reorganization, the health system will have separate networks for Northern California, Central California, Southern California, Oregon and Hawaii. The reorganization will result in job cuts, including reducing administration by more than $100 million.

CMS proposes in the Outpatient Prospective Payment (OPPS) rule to increase Medicare outpatient payments by 2.8 percent next year while bolstering hospital price transparency enforcement.

The OPPS rule states that payment rates for hospitals that meet applicable quality reporting requirements will increase in 2024 based on the projected market basket percentage increase of 3.0 percent, less 0.2 percentage points for the productivity adjustment.

Meanwhile, ambulatory surgical centers (ASCs) would also see a 2.8 percent increase in payment rates next year under the proposed ASC rule that was released alongside the OPPS rule.

CMS also proposes to continue using the productivity-adjusted hospital market basket update to ASC payment system rates for another two years despite plans to shift away from the system as hospital procedures shift to ASC settings. But disruptions to care patterns during the COVID-19 pandemic have prompted CMS to extend the application of the hospital market basket update.

The OPPS and ASC proposed rules also include a new benefit category for Medicare beneficiaries who require more frequent services than individual outpatient therapy visits but less intensive services than a partial hospitalization program. The benefit would be the Intensive Outpatient Program and include its own payment and program requirements for services across various settings, including hospital outpatient departments, community mental health centers, and federally qualified health centers.

Starting next year, CMS also proposes establishing payment for intensive outpatient program services as part of Opioid Treatment Programs. These intensive behavioral health services are available for individuals with mental health conditions and substance use disorders.

Other payment policies proposed in the rule include an update to Medicare payment rates for partial hospitalization program services, remote mental health services, and OPPS and ASC dental services, as well as changes to community mental health center Conditions of Participation (CoPs). The proposed rule also contains updates to the 340B payment rate, which CMS proposed to remedy via previous rulemaking to return improper payments to eligible hospitals.

“This proposed rule reflects CMS’ commitment to ensure Medicare is comprehensive in its ability to address patient needs, filling gaps in the health care system including behavioral health,” Meena Seshamani, MD, Deputy Administrator and Director for CMS’ Center for Medicare, said in a statement. “Through these proposals, we will ensure people get timely access to quality care in their communities, leading to improved outcomes and better health.”

HOSPITAL PRICE TRANSPARENCY CHANGES ON HORIZON

In addition to payment updates, the OPPS proposed rule also includes extensive updates to hospital price transparency requirements to increase compliance and enforcement.

Previous OPPS rules have required hospitals to make standard charges, including payer-specific negotiated rates, available to the public in a machine-readable file on their websites and through a more patient-friendly list of shoppable services. Hospitals face financial penalties of up to $2 million if they do not comply with the requirements.

However, a recent website assessment conducted by CMS found that about 70 percent of hospitals were fully meeting display criteria for the machine-readable file, 27 percent were partially meeting display criteria, and just 3 percent failed to post any required pricing data online by the fall of 2022. The rates improved from a previous compliance assessment in early 2021 when 30 percent of hospitals did not publish the required pricing data.

However, the latest OPPS rule aims to increase compliance by altering enforcement actions. For example, the rule would allow CMS to require an authorized hospital official to certify the accuracy and completeness of the data in the machine-readable file. Hospitals may also have to submit additional documentation to determine hospital compliance and an acknowledgment of receipt of the warning notice if CMS deems them out of compliance.

If CMS has to take action to address noncompliance, CMS may also notify the hospital’s health system leadership of the issue and work with the health system to address compliance issues across its system.

Finally, CMS proposes to publicize a hospital’s assessment of compliance, any compliance actions taken against a hospital, and notifications sent to health system leadership.

Additionally, the OPPS rule would update hospital price transparency requirements, requiring hospitals to display the required pricing data using a CMS template versus any machine-readable file format. Pricing data would also have to be encoded in a CSV or JSON format using a CMS template layout and other specified technical instructions.

CMS aims to increase machine-readable file accessibility by proposing a requirement to place a “footer” at the bottom of a hospital’s homepage that links to the webpage with the pricing data. Hospitals would also have to ensure that a .txt file is included in the root folder of the publicly available website chosen by the hospital for posting its machine-readable format.

Healthcare stakeholders can comment on the OPPS and ASC proposed rules through September 11th. CMS expects to release the final rules in November.

For decades, research studies and news stories have concluded the American system is ineffective,

too expensive and falling further behind its international peers in important measures of performance: life expectancy, chronic-disease management and incidence of medical error.

As patients and healthcare professionals search for viable alternatives to the status quo, a recent mega-merger is raising new questions about the future of medicine.

In April, Kaiser Permanente acquired Geisinger Health under the banner of newly formed Risant Health. With more than 185 years of combined care-delivery experience, Kaiser and Geisinger have long been held up as role models of the value-based care movement.

Eyeing the development, many speculated whether this deal will (a) ignite widespread healthcare transformation or (b) prove to be a desperate attempt at relevance (Kaiser) or survival (Geisinger).

Whether incumbents like Kaiser Permanente and Geisinger can lead a national healthcare transformation or are displaced by new entrants will depend largely on whether they can deliver value-based care on a national scale.

In Search Of Healthcare’s Holy Grail

Value-based care—the simultaneous provision of high quality, convenient and affordable medical care—has long been the aim of leading health systems like Kaiser, Geisinger, Mayo Clinic, Cleveland Clinic and dozens more.

But results to-date have often failed to match the vision.

The need for value-based care is urgent. That’s because U.S. health and economic problems are expected to get worse, not better, over the next decade. According to federal governmental actuaries, healthcare expenditures will rise from $4.2 trillion today to $7.2 trillion by 2031. At that time, these costs are predicted to consume an estimated 19.6% of the U.S. Gross Domestic Product.

Put simply: The U.S. will nearly double the cost of medical care without dramatically improving the health of the nation.

For decades, health policy experts have pointed out the inefficiencies in medical care delivery. Research has estimated that inappropriate tests and ineffective procedures account for more than 30% of all money spent on American medical care.

This combination of troubling economics and untapped opportunity explain why value-based care has become medicine’s holy grail. What’s uncertain is whether the transformation in healthcare delivery and financing will be led from inside or outside the healthcare system.

Where The Health-System Hopes Hang

For years, Kaiser Permanente has led the nation in clinical quality and patient outcomes based on independent, third-party research via the National Committee for Quality Assurance (NCQA) and Medicare Star ratings. Similarly, Geisinger was praised by President Obama for delivering high-quality care at a cost well below the national average.

And yet, these organizations, and many other highly regarded national and regional health systems, are extremely vulnerable to disruption, especially when their strategy and operational decisions fail to align.

Kaiser, for its part, has struggled with growth while Geisinger’s care-delivery strategy has proven unsuccessful in recent years. Failed expansion efforts forced KP to exit multiple U.S. markets, including New York, North Carolina, Kansas and Texas. More recently, several of its existing regions have failed to grow market share and weakened financially.

Meanwhile, Geisinger has fallen on hard times after decades of market domination. As Bob Herman reported in STAT News: “Failed acquisitions, antitrust scrutiny, leadership changes, growing competition from local players, and a pandemic that temporarily upended how patients got care have forced Geisinger to abandon its independence. The system is coming off a year in which it lost $240 million from its patient care and insurance operations.”

Putting the pieces together, I believe the Kaiser-Geisinger deal represents an industry undergoing massive change as health systems face intensifying pressure from insurers and a growing threat from retailers like Amazon, CVS and Walmart. This upcoming battle over the future of value-based care represents a classic conflict between incumbents and new entrants.

Can The World’s Largest Companies Disrupt U.S. Healthcare?

Retail giants, including Amazon, Walmart and CVS, are among the nation’s 10 largest companies based on annual revenue.

They have a broad geographic presence and strong relationships with almost all self-funded businesses. Nearly all have acquired the necessary healthcare pieces—including clinicians, home-health services, pharmacies, insurance arms and electronic medical record systems—to replace the current medical system.

And yet, while these companies expand into medical care and financing, their core businesses are struggling, resulting in announced store closures and layoffs. As newcomers to the healthcare market, they have been forced to pay premium dollars to acquire parts of the delivery system. All have a steep learning curve ahead of them.

The Challenge Of Healthcare Transformation

American medicine is a conglomerate of monopolies(insurers, hospitals, drug companies and private-equity-owned medical practices). Each works to maximize its own revenue and profit. All are unwilling to innovate in ways that benefit patients when doing so comes at the sacrifice of financial performance.

One problem stands at the center of America’s soaring healthcare costs: the way doctors, hospitals and drug companies are paid.

The dominant payment methodology in the United States, fee-for-service, rewards healthcare providers for charging higher prices and increasing the number (and complexity) of services offered—even when they provide no added value.

The message to doctors and hospitals is clear: The more you do, and the greater market control you have, the higher your income and profit. This is the antithesis of value-based care.

The alternative to fee-for-service payments, capitation, involves paying a single, up-front sum to the providers of care (doctors and hospitals) to cover the total annual cost for a population of patients. This model, unlike fee-for-service, rewards effectiveness and efficiency. Capitation creates incentives to prevent disease, reduce complications from chronic illness, and diminish the inefficiencies and redundancies present in care delivery. Capitated health systems that can prevent heart attacks, strokes and cancer better than others are more successful financially as a result.

However, it’s harder than it sounds to translate what’s best for patients into everyday decisions and actions. It’s one thing to accept a capitated payment with the intent to implement value-based care. It’s another to put in place the complex operational improvements needed for success. Here are the roadblocks that Kaiser-Geisinger will face, followed by those the retail giants will encounter.

3 Challenges For Kaiser-Geisinger:

Involving Clinical Experts. Kaiser Permanente is a two-part organization and when the insurance half (Kaiser) decided to acquire Geisinger, it did so without input or involvement from the half of the organization responsible for care-delivery (Permanente). This spells trouble for Geisinger, which must navigate a complex turnaround without the operational expertise or processes from Permanente that, in the past, helped Kaiser Permanente grow market share and lead the nation in clinical quality.

Going All In. To meet the healthcare needs of most its patients, Geisinger relies on community doctors who are paid on a fee-for-service basis. Generally, the fee-for-service model is predicated on the assumption that higher quality and greater convenience require higher prices and increased costs. With Geisinger’s distributed model, it’ll be very difficult to deliver consistent, value-based care.

Inspired Leadership. Major improvements in care delivery require skilled leadership with the authority to drive clinical change. In Kaiser Permanente, that comes through the medical group and its physician CEO. In Geisinger’s hybrid model, independent doctors have no direct oversight or central accountability structure. Although Risant Health could be an engine for value-based medical care, it’s more likely to serve the role of a “holding company,” capable of recommending operational improvements but incapable of driving meaningful change.

3 Challenges For The Retail Giants:

More Medical Offerings. Amazon, Walmart and CVS are successfully acquiring primary care (and associated telehealth) services. But competing with leading health systems will require a more wholistic, system-based approach to keep medical care affordable. This won’t be easy. To avoid ineffective, expensive specialty and hospital services, they will need to hire their own specialists to consult with their primary care doctors. And they will have to establish centers of excellence to provide heart surgery, cancer treatment, orthopedic care and more with industry-leading outcomes. But to meet the day-to-day and emergent needs of patients, they also will have to establish contracts with specialists and hospitals in every community they serve.

Capitalizing On Capitation. Already, the retail giants have acquired organizations well-versed in delivering patient care through Medicare Advantage, a capitated alternative to traditional (fee-for-service) Medicare plans. It’s a good start. But the retailers must do more than dip a toe in value-based care models. They must find ways to gain sufficient experience with capitation and translate that success into value-based contracts with self-funded businesses, which insure tens of millions of patients.

Defining Leadership. Without an effective and proven clinical leadership structure, the retail giants will be no more effective than their mainstream competitors when it comes to implementing improvements and shifting the culture of medicine to one that is customer- and service-focused.

Be they incumbents or new entrants, every contender will hit a wall if they cling to today’s failing care delivery model. The secret ingredient, which most lack and all will need to embrace in the future, is system-ness.

For all of the hype surrounding value-based care, fragmentation and fee-for-service are far more common in American healthcare today than integration and capitation.

Part two of this article will focus on how these different organizations—one set inside and one set outside of medicine—can make the leap forward with system-ness. And, in the end, you’ll see who is most likely to emerge victorious.

So far, 2023 is shaping up to be a slightly better year for hospital performance, but it comes on the heels of unprecedented financial difficulties for the sector.

In the graphic above, we evaluated nearly 30 years of historical data from Kaufman Hall and the American Hospital Association to provide a broader perspective on hospital operating margins over time. 2020 and 2022 have been the only years in which a majority of hospitals—53 percent—posted a negative operating margin.

During the most comparable periods of recent economic hardship, the “dot-com bubble burst” of the late 1990s and the 2009 Great Recession, the share of hospitals with negative operating margins amounted to only 42 and 32 percent, respectively.

With this context, hospitals’ current financial distress is more severe than anything we’ve seen in the past three decades.

Healthcare is clearly no longer recession-proof: a four percent operating margin—the level needed for health systems to not only sustain operations but also invest in growth—feels even more elusive as labor costs remain high, surgical care continues to shift to outpatient settings, the second half of the Baby-Boom generation ages into Medicare, and deep-pocketed competitors compete for profitable services.