The Trump administration is moving into its second 100 days facing conditions more problematic than its first 100. For healthcare, this period will define the industry’s near-term future as changes in three domains unfold:

- The Economy: The economy is volatile and consumer confidence is waning. The impact of tariffs on U.S. prices remains an unknown and escalating tension between the Ukraine and Russia, Israel and Palestine, Pakistan and India are worrisome. Household debt is mounting as student loans, medical debt and housing costs imperil financial security for more than half of U.S. households. The 3 major stock indices remain in the red YTD, prospects for a recession are high and investors are increasingly cautious. Net impact on healthcare organizations and public programs: negative, especially those without strong balance sheets and access to affordable private capital.

- The Courts: Recent opinions by the Supreme Court and District Courts suggest a willingness to challenge the administration’s Executive Orders on immigrant deportation and due process, threats and funding cuts aimed at law firms and universities considered “woke” and layoffs initiated by DOGE and more. Court challenges will slow the administration’s agenda and create uncertainty in workplaces. Net impact: negative. Uncertainty paralyses planning and operations in every public and private healthcare organization.

- The Public Mood: The afterglow of the election has dissipated and the public’s mood has shifted from guarded optimism to anxiety and despair. The public’s uncertain about tariffs and worried about household expenses. Net impact: negative. Healthcare affordability and prices are major concerns to consumers: the majority (76%) think the system is more concerned about profitability than patient care (Jarrard).

Current events in these areas portend headwinds for most public and private healthcare organizations where attention in the next 100 days will be focused in these areas:

- Oversight: New rules, programmatic priorities, key personnel appointments and re-organization in HHS, CMS, the FDA and VA: RFKJ’s MAHA plans and Commission appointees, Oz’ affinity for Medicare Advantage predisposition toward value-based care and Makary’s overhaul of the FDA’s drug oversight process will be “on the table” in the next 100 days.

- Funding: Healthcare funding in the FY 2026 federal budget. The GOP-controlled House and Senate can pass a budget with minimal support from Dem’s that reflects a serious effort to reduce the federal debt ($37 trillion/123% of GDP– up from $20 trillion in 2017). Healthcare cuts expected to be significant though rumored massive cuts to Medicaid unlikely.

- States: State healthcare referenda and executive actions: states are evaluating price controls on drugs and hospitals, reparations from insurers for delays and prior-authorizations, scope of practice restrictions and more. Topping the watchlist in most states is Medicaid funding and potential fallout from discontinued ACA marketplace subsidies factored into the FY 2026 budget being finalized by the GOP-led Congress in DC.

- SCOTUS: Supreme Court decisions will be handed down or before June 30 when SCOTUS’ 2024 term ends including Braidwood Management v. Becerra which will determine whether the Affordable Care Act’s requirement that private insurers cover preventive services without cost-sharing will continue. The court will also opine to the authority of the HHS secretary to appoint members of the U.S. Preventive Services Task Force. The potential impact of these decisions on coverage, insurance premiums and access to preventive health services is pervasive.

- Financial markets: Capital markets are in a watchful waiting mode as US trade policy unfolds, inflation fluctuates, the fed’s interest rate determination is disclosed and consumer spending reacts. Private investing in healthcare remains opportunistic though deal flow is shifting and risk thresholds tightening.

- Polls: Polls draw the attention of media and elected officials. They influence how organizations prioritize advocacy strategies, address consumer complaints and concerns and manage reputations. As reflected in numerous national polls, trust in the system and its key players—insurers, hospitals, drug companies—is at a historic low.

Each sector in U.S. healthcare will be impacted differently: Three face the strongest headwinds:

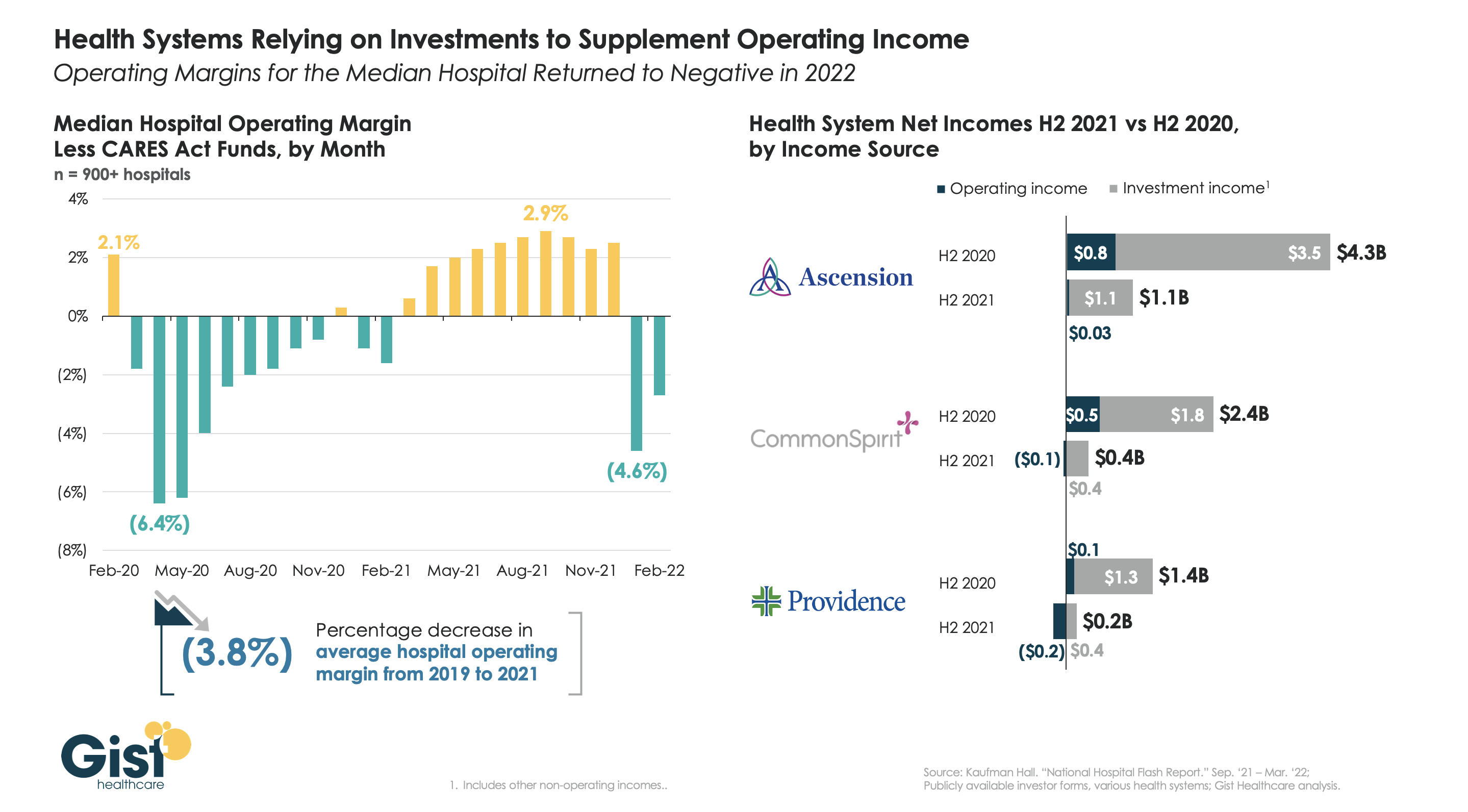

- Hospitals: Hospitals face enormous financial challenges, especially not-for-profits, safety net, rural and veteran’s hospitals. Last week’s unfavorable SCOTUS decision against hospitals alleging DSH under-payments will cost $1 billion per year. Congressional adoption of site neutral payment policy could cost $15 billion/year. Drug prices, labor costs, insurer payment cuts and red-tape will negate operating margins and lower investment income knee-capping growth and innovation plans. Complicating matters, employed physicians will demand higher pay and more control. And Congressional budget-creators believe the sector’s 31% share of total healthcare spending makes it ripe for cuts attributable to “waste, fraud and abuse”.

- Insurers: Medicare Advantage (which enjoys support by key administrators including CMS’ Mehmet Oz) has become a lightening rod of insurer criticism alongside prior authorization policies that restrict care. Coverage remains key to household financial security but insurers are seen as barriers to rather than facilitators of evidence-based cost-effective care. And the concentration of power in corporate titans (United, Humana, Cigna, CVS, Centene and others) is viewed with skepticism.

- Public Health: Public health is not a priority in the U.S. health system despite recognition that social determinants account for 70% of the system’s $5 trillion spending. Most programs are funded by state and local governments with federal support limited. Public health is not seen as an investment and, in some settings treated with disdain as welfare or waste. As Mayors and Governors develop plans for the rest of 2025 and through 2026, public health cuts will be likely as federal co-funding becomes scarce.

The next 100 days will define the national agenda for the mid-term election in November 2026, reflect the solidarity of the MAGA movement and show the impact of tariffs on inflation, consumer prices and the public’s mood.

Healthcare leaders will be watching closely. All will be impacted.