The U.S. economy expanded at a 2.6% annual rate in the third quarter, ending the streak of back-to-back contractions that raised fears the country had entered a recession.

Why it matters: Gross domestic product got a boost from trade dynamics, but the underlying details — including weaker housing and decelerating consumer spending — point to an economy that’s slowing.

The first estimate of GDP, released by the Commerce Department on Thursday, will be revised in the coming months as the government gets more complete data.

The report comes on the heels of negative GDP growth during the first half of the year. In the January through March period, the economy contracted at a 1.6% annual rate. In the second quarter, the economy shrank at a 0.6% annualized pace.

Between the lines: The latest GDP report is among the final major economic data releases before the midterm elections, where voters have ranked the economy as a critical issue.

The labor market is solid, with the unemployment rate at the lowest level in over 50 years. But soaring inflation has eaten away at Americans’ wage gains.

The backdrop: The Federal Reserve is trying to engineer an economic slowdown in a bid to crush high inflation. It has swiftly raised borrowing costs five times this year, with another big increase likely ahead at its upcoming policy meeting next week.

What they’re saying: “For months, doomsayers have been arguing that the US economy is in a recession and Congressional Republicans have been rooting for a downturn,” President Biden said in a statement. “But today we got further evidence that our economic recovery is continuing to power forward.”

As everyone in our industry knows, sluggish volumes amid persistently rising costs, especially for labor, have sent health system margins into a downward spiral across 2022. Using the latest data from consultancy Kaufman Hall, the graphic above shows that by the end of this year, employed labor expenses will have increased more than all non-labor costs combined.

While contract labor usage, namely travel nursing, is declining, the constant battle for nursing talent means travel nurses are still a significant expense at many hospitals. Through the first six months of this year, over half of hospitals reported a negative operating margin, and the median hospital operating margin has dropped over 100 percent from 2019.

Larger health systems are not faring better: all five of the large, multi-regional, not-for-profit systems we’ve highlighted below saw their operating margins tumble this year, with drops ranging from three points (Kaiser Permanente) to nearly seven points (CommonSpirit Health and Providence).

While these unfavorable cost trends have been building throughout COVID, health systems now have neither federal relief nor returns from a thriving stock market to help stabilize their deteriorating financial outlooks.

Health system boards will tolerate negative margins in the short-term (especially given that many have months’ worth of days cash on hand), but if this situation persists into 2023, pressure for service cuts, layoffs, and restructuring will mount quickly.

The jobs of young professionals in several white-collar industries are particularly vulnerable as companies scale back hiring plans, pull job listings and lay off workers.

Sixty-five percent of employers see a recession coming and many are taking steps to prepare, according to a survey by Principal Financial Group. If there is a recession, white-collar industries are likely the most vulnerable, said William Lee, PhD, chief economist at the Milken Institute, according to Bloomberg.

“The entry-level white-collar guy is going to have to watch out. That’s going to be the surprise in this downturn,” Dr. Lee said, according to Newsweek.

A Challenger, Gray and Christmas survey revealed companies are preparing for a recession by reducing business travel, laying off staff and implementing hiring freezes.

Many industries, including technology, banking and business services, have staffing numbers that are far above pre-pandemic levels, and the layoffs have already begun, according to Bloomberg. Social media platform Snap, Netflix and Re/Max Holdings are a few of the companies that have recently announced staff reductions.

While Advocate Aurora Health’s year-to-date operating income sits at $51.2 million, $666 million in investment declines weigh heavy on its bruised bottom line.

Following a tight first quarter, Advocate Aurora Health managed to grow its operating margin but still landed negative due to $400 million in investment losses during the quarter ended June 30, according to financial filings.

The 27-hospital nonprofit—which pending regulatory review slated to merge with Atrium Health in one of the year’s biggest hospital transactions—reported a $48.7 million operating income during its second fiscal quarter of 2022 (1.7% margin).

This is up from the $2.5 million (0.3% margin) it scraped out earlier this year but well below the $213.7 million (6.5% margin) of Q2 2021.

Revenues for the quarter increased 1.5% year over year to more than $3.5 billion. While patient service revenue and other revenue both grew by tens of millions, capitation revenue declined slightly due to a shift in overall membership mix and a 6.1% dip in capitated lives, the system wrote in its filing.

Discharge volumes fell 7.7% year over year during the most recent quarter, as did home care visits by 7.6%. The system saw increases compared to the previous year among its observation cases (11.6%), hospital outpatient visits (2.1%) and physician visits (7.1%).

Advocate Aurora’s expenses grew at a faster rate, at 6.7% year over year during the second quarter. The increase was led by a 10.2% jump in salaries, wages and benefits payouts, which the system said was fueled by a blend of higher nurse agency costs, higher merit and premium pay for clinical care and volume-driven demand for more full-time equivalent employees.

The nonprofit saw last year’s investment gains largely upended, recording a $400 million net loss during the quarter compared to the $571.6 million gain of the prior year’s equivalent quarter.

The shortfall dragged Advocate Aurora’s net income to a $347.6 million loss for the quarter. It had logged a $545.6 million gain the previous year.

Looking at six-month numbers, the health system reported $7.1 billion in total revenue and $7 billion in total expenses for an operating income of $51.2 million. Year-to-date investment losses landed at $666 million, bringing the organization to a $600.8 million net loss.

Advocate Aurora was formed in 2018 from the merger of nonprofits Advocate Health Care and Aurora Health Care. It treats 2.6 million unique patients, employs 75,000 people and logged just under $14.1 billion in total revenue across 2021 and a net income of more than $1.8 billion.

Should its merger plans go through, Advocate Aurora and Atrium Health would control 67 hospitals and $27 billion of combined revenues across six states. The deal is anticipated to close before the end of the year, according to the earnings filing.

The system’s latest numbers will come as no surprise in light of similar quarterly reports from Advocate Aurora’s nonprofit contemporaries.

Investment struggles and increased expenses were reported across the board, although not every major system was able to keep operations in the black. Mayo Clinic, Kaiser Permanente and UPMC were among those on the stronger side of the scale while Sutter Health, Mass General Brigham and Providence each reported tens to hundreds of millions in operational losses.

Fitch Ratingswarned last week that these sector-wide challenges are unlikely to vanish during the remainder of the year. As such, the agency has downgraded its outlook for the nonprofit hospital industry from “neutral” to “deteriorating.”

Nonprofit hospitals’ median financial metrics showed improvement last year, but Fitch Ratings is projecting declines for next year and beyond.

The credit rating agency analyzed 2021 audited data and reported that “AA” rated hospital medians showed a 20 percent increase in cash to adjusted debt. “BBB” rated health systems had an 8 percent increase.

“The deceptively strong numerical improvements over prior years’ medians are less a sign of sector resiliency and more a cautionary calm before the storm,” Fitch Ratings senior director Kevin Holloran said in the Aug. 18 report. “Additional expenses, primarily labor, have become part of the permanent fabric of hospital operations, that when combined with ongoing incremental challenges will exert tremendous pressure on providers through calendar 2022 and beyond.”

Fitch predicts hospital medians will flip this time next year due to inflationary pressures, a challenging operational start to 2022 and additional omicron sub-variants.

Fitch also highlighted staffing as a concern for hospital medians.

“We are likely two years before some level of ‘normal’ returns to the sector,” Mr. Holloran said in the report. “For many hospitals, their ‘value journey’ will be on temporary hold until expenses stabilize and become more predictable.”

Citing more severe than expected macro headwinds, Fitch revised its sector outlook for nonprofit hospitals and health systems to “deteriorating” Aug. 16.

Nonprofit hospitals have been hamstrung by labor and broader macro inflationary pressures that “are rendering the sector even more vulnerable to future stress,” Fitch senior director Kevin Holloran said in an Aug. 16 news release. Investment losses have also contributed to a rockier 2022 than anticipated, and operating metrics are down significantly compared to last year.

“While severe volume disruption to operations appears to be waning, elevated expense pressure remains pronounced,” Mr. Holloran said. “Even if macro inflation cools, labor expenses may be reset at a permanently higher level for the rest of 2022, and likely well beyond.”

Many nonprofit hospitals and health systems are expected to violate debt service coverage covenants this year, according to the news release.

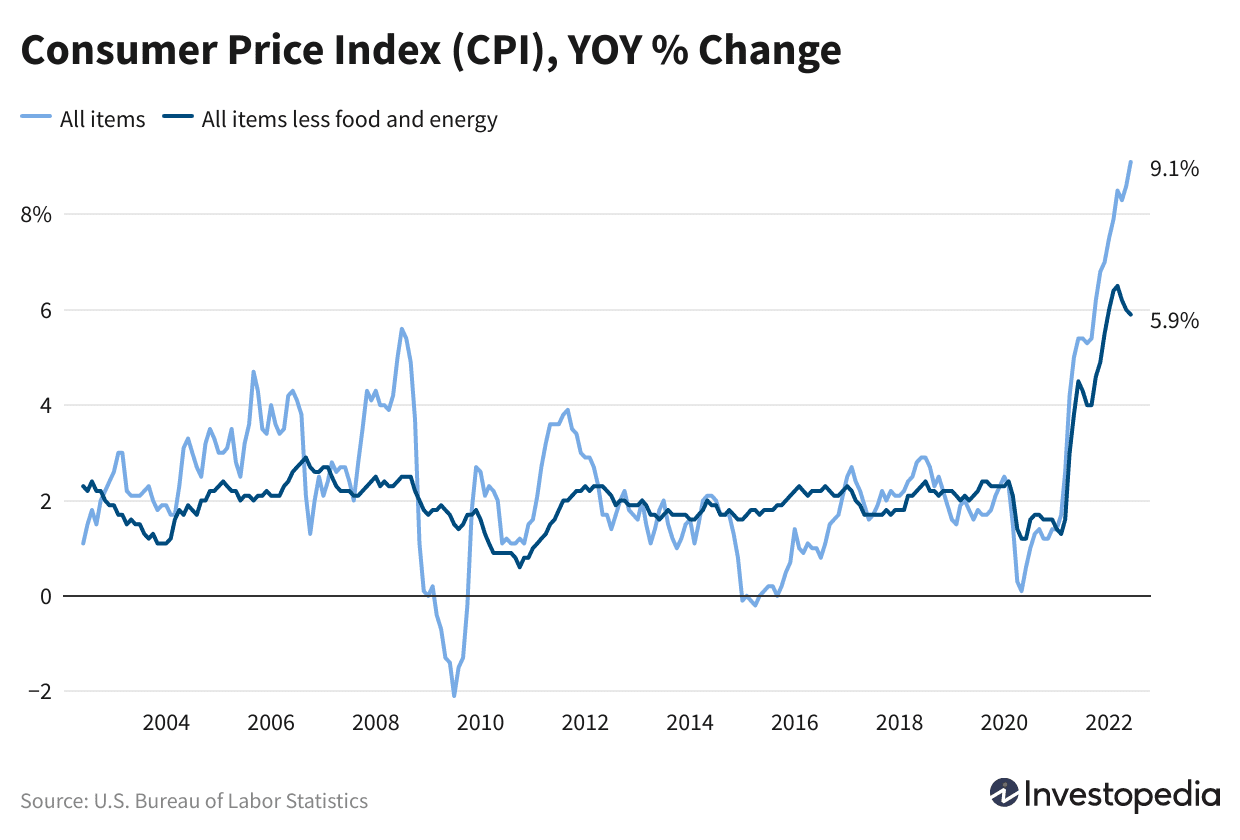

Consumer prices were unchanged in July, as plunging prices for gasoline dragged the Consumer Price Index down to zero. Core inflation, which excludes energy and food, rose only 0.3%, below what analysts expected.

Driving the news: The Labor Department reported that overall consumer prices rose 0% last month, and are up 8.5% over the past year. That compares to a 9.1% year-over-year reported in June.

Why it matters: Falling gasoline prices are clearly giving American consumers some inflation relief, and the broader inflation picture was more favorable in July than economists had expected.

By the numbers: Gasoline prices fell 7.7% in July, dragging down headline inflation. Other items with falling prices included used cars and trucks (-0.4%) and airfares (down 7.8%).

But rents kept rising, a major factor in stubbornly high underlying inflation. Renters faced a 0.7% rise in costs.

What’s next: The Federal Reserve has indicated it intends to keep raising interest rates until there is clear evidence inflation is waning. After two straight months of extremely hot inflation readings, this report will be welcome news.

While for-profit health system giants HCA Healthcare and Tenet Healthcare reported reductions in contract labor usage last quarter, sustained higher labor costs and sluggish demand resulted in both of them, along with Community Health Systems and Universal Health Services, seeing their net income decline in the second quarter.

Like many systems, the for-profit chains seem to have successfully weaned themselves from earlier reliance on expensive temporary nurses, but are facing more structural increases in labor costs as salaries have risen to remain competitive in a very tight labor market.

The Gist: The earnings reports from for-profit companies are a canary in the coal mine for the overall margin performance of the industry. Although investor-owned companies are vastly outnumbered by their not-for-profit peers, they often move more quickly, and with more vigor, to reduce costs in order to meet the earnings expectations of Wall Street investors. They also typically rely more heavily on volume growth—particularly emergency department visits—as a driver of earnings.

If for-profits are now finding it more difficult to pull those levers, we’d expect that the broader universe of nonprofit systems is experiencing even tougher sledding. That’s consistent with what we’re hearing anecdotally from health systems we work with.

Job openings fell slightly in May as demand for workers remained near record highs, according to data released Wednesday by the Labor Department, even amid growing concerns of a potential recession.

The number of open jobs listed in the U.S. on the final business day of May totaled 11.3 million, dropping from 11.7 million in April after seasonal adjustments. Though job openings fell in May, hires, layoffs and quits stayed roughly even with their April numbers, according to the May Job Openings and Labor Turnover Survey (JOLTS) report.

The JOLTS report showed a labor market still stacked strongly for workers in May, a month when the U.S. added 390,000 jobs and saw the jobless rate hold strong at 3.6 percent. Despite the decline in job openings, there were still almost two open gigs for each unemployed American.

That mismatch can give workers many opportunities to find new jobs with better compensation and career opportunities than their current ones.

“This is not what a recession looks like. The May 2022 JOLTS data obviously lags what’s happening in the labor market presently, but all signs are that it remains strong,” wrote Nick Bunker, research director at Indeed.com, in a Wednesday analysis.

“If the labor market were quickly and suddenly taking a downturn, we would see employers’ demand for new hires drop and their willingness to let workers go increase. For now, we aren’t seeing a sudden move in either direction.”

Businesses hired roughly 6.5 million workers and lost 6 million in May, both in line with April totals. The percentage of the workers who quit their jobs in May fell to 2.8 percent, just 0.1 percentage points from a record high of 2.9 percent set earlier this year.

With ample jobs available and people still eager to leave in search of better work, businesses have avoided laying off employees over fears they could be hard to replace. Roughly 1.4 million workers were laid off in May, slightly higher than April’s total of 1.3 million. But the percentage of the workforce laid off by their employers held even at 0.9 percent, which is below pre-pandemic levels.

“Despite continued headlines about layoffs, particularly in the tech sector, the layoff rate remains low,” Bunker explained. “This is the 15th straight month that the layoff rate has been below its pre-pandemic bottom.”

The steady strength of the U.S. job market helped propel a rapid recovery from the depths of the COVID-19 recession through much of 2020 and 2021. The U.S. is fewer than 1 million new jobs away from replacing the 21 million jobs lost to the onset of the pandemic, and the speed of the pandemic recovery has helped fuel rapid wage growth, particularly for low-earning workers.

Even so, many economists — including Federal Reserve officials — fear the strength of the job market could add further fuel to inflation already at four-decade highs. While steady job gains are good for the economy, the intense competition for workers has made it difficult for many firms to stay adequately staffed and keep up with both higher wage demands and rising prices.

Fed Chairman Jerome Powelland many economists are hopeful that higher interest rates and the fading effects of fiscal stimulus can help reduce job openings — and the pressure they put on wages — without wiping out job gains.

The Fed has boosted its baseline interest rate range by 1.5 percentage points from near-zero levels in January and is expected to hike by another 2 percentage points by the end of the year. Higher interest rates are meant to reduce inflation by slowing the economy enough to force businesses to stop raising prices and wages.

Even so, he has acknowledged it will be difficult for the Fed to avoid slowing down the labor market into a standstill as the central bank boosts interest rates to fight inflation.

“The labor market conditions [Powell] has described as ‘extremely, historically’ tight and ‘unsustainably hot’ persisted in May,” wrote Julia Pollak, chief economist at ZipRecruiter, in a Wednesday analysis.

“Employers are hanging onto the workers they have in a tight labor market where replacing them is unusually costly.”

The June jobs report, set to be released Friday, will give a most recent view into how well the labor market has held up amid Fed rate hikes. Economists expect the U.S. to have added roughly 268,000 jobs last month, according to consensus estimates.

“There will be a time when the US labor market takes a downturn, jobs are shed at a higher rate, and workers stop quitting their jobs. But that time has yet to come. The labor market remains very tight and very hot. That may change, but it hasn’t yet,” Bunker wrote.

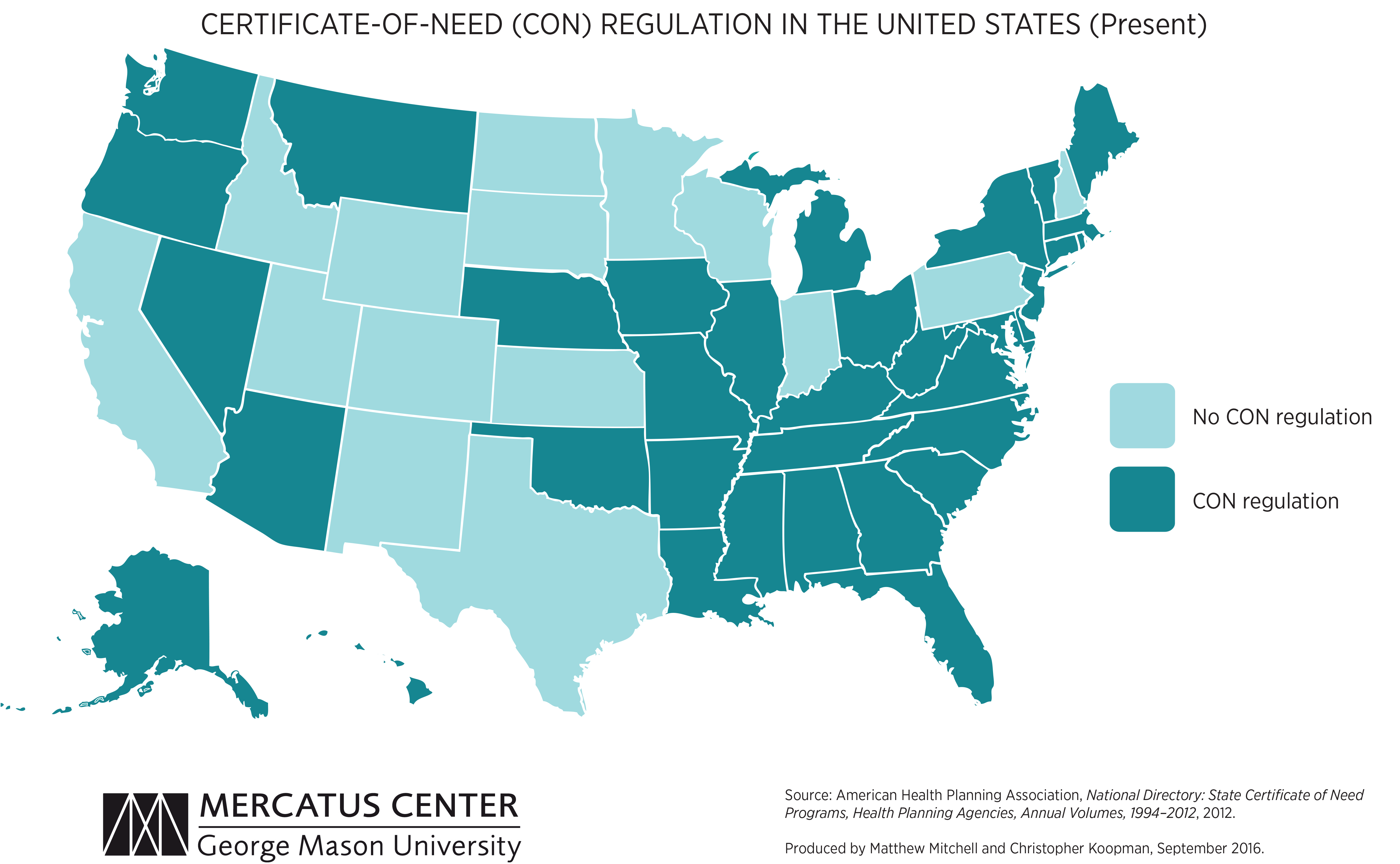

We’re picking up on a growing concern among health system leaders that many states with “certificate of need” (CON) laws in effect are on the cusp of repealing them. CON laws, currently in place in 35 states and the District of Columbia, require organizations that want to construct new or expand existing healthcare facilities to demonstrate community need for the additional capacity, and to obtain approval from state regulatory agencies. While the intent of these laws is to prevent duplicative capacity, reduce unnecessary utilization, and control cost growth, critics claim that CON requirements reduce competition—and free market-minded state legislators, particularly in the South and Midwest, have made them a target.

One of our member systems located in a state where repeal is being debated asked us to facilitate a scenario planning session around CON repeal with system and physician leaders. Executives predicted that key specialty physician groups would quickly move to build their own ambulatory surgery centers, accelerating shift of surgical volume away from the hospital.

The opportunity to expand outpatient procedure and long-term care capacity would also fuel investment from private equity, which have already been picking up in the market. An out-of-market health system might look to build microhospitals, or even a full-service inpatient facility, which would be even more disruptive.

CON repeal wasn’t all downside, however; the team identified adjacent markets they would look to enter as well. The takeaway from our exercise: in addition to the traditional response of flexing lobbying influence to shape legislative change, the system must begin to deliver solutions to consumers that are comprehensive, convenient, and competitively priced—the kind of offerings that might flood the market if CON laws were lifted.