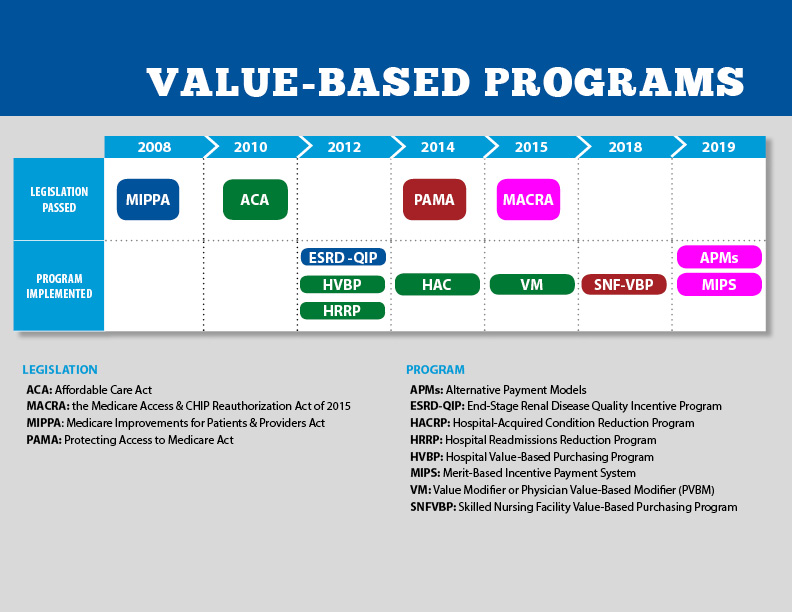

A commentary piece in Health Affairs argues that CMS’s value-based payment (VBP) initiatives have not reached their full potential because they fail to take into account conflicting market dynamics.

The authors argue that VBP models won’t take hold unless CMS both increases the “carrots”, or positive incentives, that market dominant providers receive to support true care transformation, and sharpens the “sticks” by requiring participation in accountable care organization (ACO) models, decreasing the attractiveness of fee-for-service (FFS) payments, and banning anti-competitive commercial deals that discourage steering referrals toward lower-cost providers.

The Gist: To date, CMS’s VBP efforts have largely fallen short of their two primary objectives: transforming care at scale across the country, and generating meaningful savings for the federal government.

With more and more seniors choosing Medicare Advantage (MA) each year, the federal government clearly views MA as the primary vehicle to control Medicare cost growth in the future—although savings will ultimately hinge on CMS cutting payments to insurers in the future.

Over time, continuing to foster the growth of MA may prove more successful than overcoming the myriad complications of FFS-based VBP programs.

The agency’s end goal for Medicare Advantage is to match CMS’ vision for its programs as a whole, with an emphasis on health equity.

On Wednesday, the Centers for Medicare and Medicaid Services released proposed payment policy changes for Medicare Advantage and Part D drug programs in 2023 that are meant to create more choices and provide affordable options for consumers.

The Calendar Year 2023 Advance Notice for Medicare Advantage and Part D plans is open to public comment for 30 days. This year, CMS is soliciting input through a health equity lens on the approach to some future potential changes.

The agency’s end goal for Medicare Advantage is to match CMS’ vision for its programs as a whole, which Administrator Chiquita Brooks-LaSure said is “to advance health equity; drive comprehensive, person-centered care; and promote affordability and the sustainability of the Medicare program.”

CMS is proposing an effective growth rate of 4.75% and an overall expected average change in revenue of 7.98%, following a 4.08% revenue increase planned for 2022.

WHAT’S THE IMPACT?

CMS is requesting input on a potential change to the MA and Part D Star Ratings that would take into account how well each plan advances health equity.

The agency is also requesting comment on including a quality measure in MA and Part D Star Ratings that would assess how often plans are screening for common health-related social needs, such as food insecurity, housing insecurity and transportation problems.

The Health Equity Index has been tasked with creating more transparency on how MA plans care for disadvantaged beneficiaries.

Additionally, CMS is requesting input on considerations for assessing the impact of using sub-state geographic levels of rate setting for enrollees with end-stage renal disease, particularly input regarding the impact of MA payment on care provided to rural and urban underserved populations and how such payment changes may impact health equity.

Other areas in which CMS is soliciting input include a variety of payment updates, a new measure concept to assess whether and how MA plans are transforming care by engaging in value-based models with providers’ and updates to risk-adjustment models to continue to pay appropriately for people enrolled in MA and Part D plans.

Public comments on the Advance Notice must be submitted by March 4. The Medicare Advantage and Part D payment policies for 2023 will be finalized in the 2023 Rate Announcement, which will be published no later than April 4.

REACTION

The proposed rule has already elicited reaction from various organizations, including Better Medicare Alliance.

“As we continue to review the Advance Notice in further detail, we appreciate that CMS has offered a thoughtful proposal that will help ensure stability for the millions of diverse seniors and individuals with disabilities who count on Medicare Advantage,” Mary Beth Donahue, president and CEO of the Better Medicare Alliance, said, adding that the proposal furthers the shared goal of improving health equity.

“Medicare Advantage has proven its worth for seniors and taxpayers – providing lower costs, meaningful benefits that address social determinants of health, better outcomes and greater efficiencies for the Medicare dollar,” she said. “A stable rate for 2023 ensures this work can continue. On behalf of our 170 Ally organizations and over 600,000 beneficiary advocates, we applaud CMS for putting seniors first by issuing an Advance Notice that protects coverage choices, advances health equity and preserves affordability for beneficiaries.”

AHIP also responded, with President and CEO Matt Eyles pointing out that for 2022 the average Medicare Advantage monthly premium dropped to $19, down more than 10% since 2021.

“We agree that MA plans play an essential role in improving health equity and addressing the social determinants of health that impact millions of seniors and people with disabilities,” he said. “We support CMS soliciting input on ways to advance these important goals.

“Medicare Advantage enjoys strong bipartisan support because it provides America’s seniors and people with disabilities with access to affordable, high-quality healthcare services,” said Eyles. “We will continue to review the 2023 rate notice and look forward to providing constructive feedback to CMS during the comment period.”

THE LARGER TREND

CMS’ Advance Notice follows a recent congressional letter in which 346 bipartisan members of Congress declared support for Medicare Advantage and urged the agency “to provide a stable rate and policy environment” for the program in 2023.

A December 2021 Morning Consult poll showed that 94% of Medicare Advantage beneficiaries are satisfied with their coverage, while 93% believe that protecting MA should be a priority of the Biden administration.

Large insurers Humana and Cigna, along with “insurtech” startups Bright Health and Alignment Healthcare, all lowered expectations for their MA membership growth after missing 2022 enrollment targets. The companies blamed fierce competition for the nation’s estimated 29.5M MA lives, and highlighted a focus on diversifying revenue through other business arms like healthcare delivery and service sales.

The Gist: Insurers’ missed expectations are leading some to question whether the MA market is beginning to weaken, but these concerns are overblown, with last fall’s enrollment affected by the pandemic, which hindered brokers’ ability to reach seniors.

Some MA-focused startups are finding challenges in their attempts to scale, and their stock prices will continue to retreat from the lofty valuations that drove their public offerings.

Insurers still have plenty of running room to grow their MA books of business, but will face increasing scrutiny of their ability to manage patients and control costs for the aging population.

We recently caught up with a health system chief clinical officer, who brought up some recent news about CVS. “I was really disappointed to hear that they’re going to start employing doctors,” he shared, referring to the company’s announcement earlier this month that it would begin to hire physicians to staff primary care practices in some stores. He said that as his system considered partnerships with payers and retailers, CVS stood out as less threatening compared to UnitedHealth Group and Humana, who both directly employ thousands of doctors: “Since they didn’t employ doctors, we saw CVS HealthHUBs as complementary access points, rather than directly competing for our patients.”

As CVS has integrated with Aetna, the company is aiming to expand its use of retail care sites to manage cost of care for beneficiaries. CEO Karen Lynch recently described plans to build a more expansive “super-clinic” platform targeted toward seniors, that will offer expanded diagnostics, chronic disease management, mental health and wellness, and a smaller retail footprint. The company hopes that these community-based care sites will boost Aetna’s Medicare Advantage (MA) enrollment, and it sees primary care physicians as central to that strategy.

It’s not surprising that CVS has decided to get into the physician business, as its primary retail pharmacy competitors have already moved in that direction. Last month, Walgreens announced a $5.2B investment to take a majority stake in VillageMD, with an eye to opening of 1,000 “Village Medical at Walgreens” primary care practices over the next five years. And while Walmart’s rollout of its Walmart Health clinics has been slower than initially announced, its expanded clinics, led by primary care doctors and featuring an expanded service profile including mental health, vision and dental care, have been well received by consumers. In many ways employing doctors makes more sense for CVS, given that the company has looked to expand into more complex care management, including home dialysis, drug infusion and post-operative care. And unlike Walmart or Walgreens, CVS already bears risk for nearly 3M Aetna MA members—and can immediately capture the cost savings from care management and directing patients to lower-cost servicesin its stores.

But does this latest move make CVS a greater competitive threat to health systems and physician groups? In the war for talent, yes. Retailer and insurer expansion into primary care will surely amp up competition for primary care physicians, as it already has for nurse practitioners. Having its own primary care doctors may make CVS more effective in managing care costs, but the company’s ultimate strategy remains unchanged: use its retail primary care sites to keep MA beneficiaries out of the hospital and other high-cost care settings.

Partnerships with CVS and other retailers and insurers present an opportunity for health systems to increase access points and expand their risk portfolios. But it’s likely that these types of partnerships are time-limited. In a consumer-driven healthcare market, answering the question of “Whose patient is it?” will be increasingly difficult, as both parties look to build long-term loyalty with consumers.

Oak Street Health, a value-based primary care network for adults on Medicare, is facing a Department of Justice inquiry into its relationships with third-party marketing agents and its provision of free transportation for members.

The DOJ is investigating whether Oak Street violated the False Claims Act, per a regulatory filing published Monday. On a call with investors Tuesday, management declined to provide additional information into the government’s request, saying it was too early to know for sure what exactly the agency is investigating but that they’re working to comply.

Otherwise, the provider had a generally solid third quarter with better-than-expected revenue and well-controlled medical costs, analysts said. Oak Street increased its full-year 2021 guidance following the results, which beat Wall Street expectations with topline revenue of $389 million, up 78% year over year and a quarterly record for the company.

Dive Insight:

The federal government is increasingly cracking down on alleged fraud, especially in the Medicare Advantage program. In privately run MA plans, CMS pays companies on a per-member basis, then adjusts payments based on the acuity or severity of their member’s health status, as supported by provider data like diagnostic codes. Generally, the sicker the member, the higher the plan’s reimbursement.

That’s led to allegations of plans hiking risk scores to overinflate members’ health needs, resulting in higher payments from CMS. Watchdogs have been finding higher incidence of fraud and abuse as the MA program becomes more popular, growing to cover more than 40% of all Medicare beneficiaries.

Oak Street isn’t a traditional plan itself, but enters into full-risk contracts with Medicare Advantage plans, and via CMS’ direct contracting program, in which it assumes full responsibility for patients’ medical expenses in exchange for a fixed per-member, per-month payment. The Chicago-based company is the latest target of a federal inquiry into whether it violated the False Claims Act.

According to the primary care company, the DOJ sent a civil investigative demand on Nov. 1 asking for information about Oak Street’s relationships with third-party marketers and transportation partners.

Oak Street does provide patients transportation to appointments when they need it and has various ways for finding new patients, including community partnerships, but it’s unclear what the DOJ is specifically investigating, CEO Mike Pykosz told investors.

“We have had no meaningful conversations with the government,” Pykosz said. “I’m not really sure what the link is.”

The CEO noted it’s not unusual for such inquiries to take months to resolve, particularly in the hyper-regulated healthcare industry, but said he wouldn’t speculate further.

A civil investigative demand is a form of administrative subpoena, and doesn’t denote any regulatory or legal action itself. However, it is used by the government to kick off investigating potential False Claims violations, and determine whether there’s sufficient evidence to warrant filing an action, according to the National Law Review.

Penalties for violating the act could range from $11,655 to $23,331 per violation, plus triple damages. Total penalties have resulted recently in some significant payouts from MA participants. Notably, in late August, integrated health system Sutter Health agreed to pay $90 million to settle whistleblower allegations of risk adjustment fraud, in the largest False Claims Act settlement against a hospital system in the MA program.

Analysts noted the inquiry, while in early stages, is a point of concern for Oak Street’s future stock performance.

“This creates a new potential risk factor that we are unlikely to get clarity on for some time,” SVB Leerink analyst Whit Mayo wrote in a note.

Oak Street, which also provides services to patients with a range of insurance options, had an otherwise solid quarter, eclipsing $1 billion of year-to-date revenue for the first time in the company’s history.

The highly infectious delta variant did contribute to higher expenses, as it has with other providers.

Oak Street reported $15 million in costs from COVID-19 admissions in the first half of the year, and another $10 million in the third quarter. COVID-19-related expenses surged in the latter half of August and continued into September, but tailed off early into the fourth quarter, CFO Tim Cook said.

The majority of Oak Street’s patients are in northern U.S. markets, however, which experienced coronavirus surges last year during the winter as more people stayed indoors.

“We will see what happens in November and December,” Cook said. “While COVID costs are going to be lower in Q4, unfortunately we’re not in a world where they’re going to be zero.”

In the quarter, the primary care provider’s medical claims expense doubled year over year to almost $310 million. Oak Street’s medical loss ratio of 82.2% was lower than analysts expected, though management said they expected it to be higher in the fourth quarter.

Pykosz and Cook called out medical costs from new patients brought in during 2021 as a system-wide stressor.

Because diagnoses from 2020 claims are used to determine 2021 risk scores, fewer claims last year could mean lower risk scores and lower payments for plans this year. Oak Street’s patients, especially older adults in low-income communities, used fewer services last year during COVID-19, which resulted in lower revenues this year even as costs expanded.

Management said they expected to get back on track in 2022 as patients new to Oak Street this year will contribute to higher reimbursement next year, closing the current medical-cost gap between tenured and new patients.

“This is certainly an outlier year from every other year we’ve had results,” Pykosz said.

Oak Street, which was founded in 2012 and went public in August 2020 at a $9 billion valuation, reported a net loss of almost $110 million in the quarter, compared to a loss of $59 million at the same time last year.

Oak Street continued expanding its membership and network in the quarter, reporting 69% at-risk patient growth and opening 15 new centers in seven new markets.

But Pykosz pointed to Oak Street’s exclusive relationship with senior group AARP and its acquisition of specialty telehealth provider RubiconMD as differentiators, while noting there’s room for a number of players in the space.

“At this point we don’t feel there’s a lot of pressure or competitive dynamics pressuring our performance,” Pykosz said.

In the third quarter, Oak Street served 100,500 risk-based patients, representing 76% of its total patient base. The company expects at-risk patient volume to grow to between 111,500 and 113,500 patients this year.

Enrollment in Medicare Advantage plans is increasing rapidly, and many insurers are expanding their MA offerings in a bid to grab larger portions of the market share. Medicare Advantage touts itself as having certain advantages over traditional Medicare, such as fitness benefits, coverage for hearing aids and eyeglasses, and limits on out-of-pocket spending.

This begs the question: Are enrollees in the two versions of Medicare fundamentally different, and what are their experiences like in terms of satisfaction?

New analysis from the Commonwealth Fund found that Medicare Advantage enrollees do not differ significantly from beneficiaries in traditional Medicare in terms of their age, race, income, chronic conditions, satisfaction with care, or access to care, after excluding Special Needs Plan (SNP) enrollees.

Both groups reported waiting more than a month for physician office visits, while similar shares of Medicare Advantage and traditional Medicare enrollees report that their out-of-pocket costs make it difficult to obtain care.

Ultimately, MA and traditional Medicare are serving similar populations, with beneficiaries having comparable healthcare experiences. The care management services provided by Medicare Advantage plans appear to neither impede access to care nor reduce concerns about costs.

WHAT’S THE IMPACT?

Beneficiaries weigh a number of trade-offs when deciding whether to enroll in Medicare Advantage plans or traditional Medicare. Unlike the latter, MA plans are required to place limits on enrollees’ out-of-pocket spending and to maintain provider networks. The plans also can provide benefits not covered by traditional Medicare, such as eyeglasses, fitness benefits and hearing aids.

Medicare Advantage plans are intended to manage and coordinate beneficiaries’ care. Some MA plans specialize in care for people with diabetes and other common chronic conditions, including Special Needs Plans. SNPs also focus on people who are eligible for both Medicare and Medicaid and on those who require an institutional level of care.

Traditional Medicare and MA enrollees have historically had different characteristics, with MA enrollees somewhat healthier. Black and Hispanic beneficiaries and those with lower incomes have tended to enroll in MA plans at higher rates than others, while traditional Medicare has historically performed better on beneficiary-reported metrics, such as provider access, ease of getting needed care, and overall care experience.

The Commonwealth Fund found that, after excluding beneficiaries in SNPs, beneficiaries enrolled in traditional Medicare do not differ significantly from MA enrollees on age, income, or receipt of a Part D low-income subsidy (LIS), which helps low-income individuals pay for prescription drugs. But beneficiaries in traditional Medicare are significantly more likely than MA enrollees to reside in a metropolitan area and more likely to live in a long-term-care or residential facility.

Beneficiaries in SNPs are different. Given the eligibility criteria for these plans, it’s not surprising that enrollees tend to have significantly lower incomes and a greater likelihood of receiving Medicaid benefits or LIS than other Medicare beneficiaries.

Enrollment in SNPs for people who require an institutional level of care has been growing rapidly, leading to a similar share of SNP enrollees and beneficiaries in traditional Medicare living in a long-term-care facility.

There are some areas in which Medicare Advantage plans appear to perform better than traditional Medicare. In particular, MA enrollees are more likely than those in traditional Medicare to have a treatment plan, to have someone who reviews their prescriptions, to have someone they can contact for help, and to receive a response to a health query relatively quickly.

By providing this additional help, Medicare Advantage plans are making it easier for enrollees to get the help they need to manage their healthcare conditions, the report found. Medicare experts have suggested providing a similar service to beneficiaries in traditional Medicare through care coordinators.

The results also raise questions about whether Medicare Advantage plans are receiving appropriate payments. MedPAC estimates that plans are paid 4% more than it would cost to cover similar people in traditional Medicare.

On the one hand, Medicare Advantage plans seem to be providing services that help their enrollees manage their care, and this added care management could be of significant value to both plan enrollees and the Medicare program. On the other hand, rates of hospitalizations and emergency room visits are similar for beneficiaries in Medicare Advantage plans and traditional Medicare. This calls into question the impact of the added services on healthcare use, spending and outcomes.

THE LARGER TREND

Insurers are expanding their Medicare Advantage offerings at a decent clip, with Humana announcing last week it would debut a new Medicare Advantage PPO plan in 37 rural counties in North Carolina in response to market demand in the eastern part of the state.

Just last week, UnitedHealthcare, which already has significant market control with its MA plans, said it will strengthen its foothold in the space by expanding its MA plans in 2022, adding a potential 3.1 million members and reaching 94% of Medicare-eligible consumers in the U.S.

And for the third straight year, health insurer Cigna is expanding its Medicare Advantage plans, growing into 108 new counties and three new states – Connecticut, Oregon and Washington – which will increase its geographic presence by nearly 30%.

Centene is also getting in on the act, expanding MA into 327 new counties and three new states: Massachusetts, Nebraska and Oklahoma. In all, this represents a 26% expansion of Centene’s MA footprint, with the offering available to a potential 48 million beneficiaries across 36 states.

The Centers for Medicare and Medicaid Services said in late September that the average premium for Medicare Advantage plans will be lower in 2022 at $19 per month, compared with $21.22 in 2021. However, Part D coverage is rising to $33 per month, compared with $31.47 in 2021.

Enrollment in MA continues to increase, CMS said. In 2022, it’s projected to reach 29.5 million people, compared with 26.9 million enrolled in a Medicare Advantage plan in 2021.

The healthcare industry is now at the peak of the long-awaited transition of the Baby Boom generation into Medicare. The “greying” of the Boomers will continue to bring a rapid influx of new Medicare beneficiaries, but this is just the beginning of a protracted period of growth for the program, with the number of Medicare-eligible Americans increasing by more than 50 percent over the next three decades.

Using data from the US Census Bureau, the graphic above shows how the generational makeup of the Medicare population will change across time. The next decade will bring the fastest growth, as the latter half of the Baby Boom generation turns 65. Over that time, the Medicare-eligible population will increase by almost a third. Gen X will begin to age into Medicare in 2029. (Go ahead, take a minute. It hurts.) While fewer in number, Gen X beneficiaries, combined with the longer lifespan of Baby Boomers, will bring no respite from Medicare growth, with enrollment still increasing 11 percent between 2030 and 2040.

As the country looks at a prolonged period of Medicare cost growth, we’ll be counting on a ballooning workforce of Millennials and Gen Z youngsters—each part of generations even larger than the Baby Boom—to continue to fund the Medicare trust across the next 25 years, when the first Millennials will receive their Medicare cards. (See how it feels?)

The Centers for Medicare & Medicaid Services (CMS) issued its final payment rule for inpatient hospitals for FY22 this week, giving providers a 2.5 percent pay increase, and implementing a number of other regulatory changes. Of particular note, the rule puts in place a requirement for hospitals and long-term care providers to report on COVID vaccination rates among their workers, amid growing calls for healthcare organizations to mandate vaccines.

The final rule will also extend additional payments to hospitals for delivering COVID care until the end of the public health emergency is declared.

On top of a number of changes to quality reporting programs aimed at reducing the adverse impact of the pandemic on hospital metrics, CMS also used the final inpatient rule to begin acting on the Biden administration’s stated desire of improving health equity by adding a maternal morbidity measure to hospital quality reporting requirements.

The measure will require hospitals to report whether they participate in initiatives to improve perinatal health, an area in which unequal treatment has led to disproportionately adverse outcomes for women of color. In what will surely be welcome news for hospitals, CMS will no longer require disclosure of the contract terms providers strike with Medicare Advantage insurers, which was a key provision of Trump-era transparency regulations.

Nevertheless, based on earlier proposed changes to physician and outpatient surgery payment rules, and the President’s recent executive order on competition policy, we’d anticipate the Biden administration will continue to boost efforts to increase transparency of provider pricing.

First things first, however: there’s a pandemic to get through, and this final inpatient payment rule should largely come as good news to hospitals who are increasingly feeling the strain of a fourth surge of COVID cases.

Senate Democrats announced a compromise budget framework to fund President Biden’s social spending plans to the tune of $3.5T, including substantial money for some of the administration’s key healthcare priorities. The framework sends instructions to several Senate committees, including the Budget and Finance panels, to craft legislative language around the central components of the deal, with the goal of passing a spending package before next month’s recess.

Many specifics remain to be ironed out in negotiations among the party’s progressive and moderate camps, but some of the main elements of the deal became clear this week. The plan includes extending theenhanced subsidies for purchasing individual coverage on the healthcare marketplaces, which were implemented earlier this year as part of the American Rescue Plan Act. It would also seek to close the so-called “Medicaid coverage gap”, by providing new coverage options for low-income adults in states that did not expand Medicaid under the Affordable Care Act (ACA).

New investments would be made in home- and community-based services for long-term care, along the lines of the $400B proposed in President Biden’s American Families Plan. And the budget deal envisions expanding benefits in the Medicare program to include dental, vision, and hearing services. Given the budgetary concerns of moderate Democratic lawmakers like Sen. Joe Manchin (WV), one critical question will be how the $3.5T deal will be paid for. One likely source of funding for the deal will be reforming the way Medicare purchases prescription drugs, making that long-time Democratic policy objective a probable part of any final package.

Notably absent from the healthcare spending proposals: lowering the eligibility age for Medicare from 65 to 60. No final decision has been reached on whether to incorporate such a move; rather, the question will be sent to the Senate Finance Committee for consideration. Given the urgency of passing as much of the Biden administration’s legislative agenda as possible before the midterm campaign season begins in earnest, we think it’s unlikely that Democrats will be willing to cross the Rubicon of Medicare expansion at this point.

The prospect of having to gain support from all 50 Democratic senators—as zero Republicans are expected to support the package—will likely temper any appetite for picking a fight with the influential hospital and physician industries, which have strongly opposed Medicare expansion.

One longer-term implication of the apparent decision to favor expansion of Medicare benefits over lowering the Medicare eligibility age now:a richer package of services in traditional Medicare might make Medicare Advantage (MA) a less attractive alternative for potential enrollees and could undermine any future efforts to create an “MA buy-in” for coverage expansion.

Expect lobbying and negotiations to reach a furious pace over the next several weeks, as lawmakers work out the final details of the $3.5T spending plan.

Medicare Advantage (MA) focused companies, like Oak Street Health (14x revenues), Cano Health (11x revenues), and Iora Health (announced sale to One Medical at 7x revenues), reflect valuation multiples that appear irrational to many market observers. Multiples may be exuberant, but they are not necessarily irrational.

One reason for high valuations across the healthcare sector is the large pools of capital from institutional public investors, retail investors and private equity that are seeking returns higher than the low single digit bond yields currently available. Private equity alone has hundreds of billions in investable funds seeking opportunities in healthcare. As a result of this abundance of capital chasing deals, there is a premium attached to the scarcity of available companies with proven business models and strong growth prospects.

Valuations of companies that rely on Medicare and Medicaid reimbursement have traditionally been discounted for the risk associated with a change in government reimbursement policy. This “bop the mole” risk reflects the market’s assessment that when a particular healthcare sector becomes “too profitable,” the risk increases that CMS will adjust policy and reimbursement rates in that sector to drive down profitability.

However, there appears to be consensus among both political parties that MA is the right policy to help manage the rise in overall Medicare costs and, thus, incentives for MA growth can be expected to continue. This factor combined with strong demographic growth in the overall senior population means investors apply premiums to companies in the MA space compared to traditional providers.

Large pools of available capital, scarcity value, lower perceived sector risk and overall growth in the senior population are all factors that drive higher valuations for the MA disrupters.However, these factors pale in comparison the underlying economic driver for these companies. Taking full risk for MA enrollees and dramatically reducing hospital utilization, while improving health status, is core to their business model. These companies target and often achieve reduced hospital utilization by 30% or more for their assigned MA enrollees.

In 2019, the average Medicare days per 1,000 in the U.S. was 1,190. With about $14,700 per Medicare discharge and a 4.5 ALOS, the average cost per Medicare day is approximately $3,200. At the U.S. average 1,190 Medicare hospital days per thousand, if MA hospital utilization is decreased by 25%, the net hospital revenue per 1,000 MA

enrollees is reduced by about $960,000. If one of the MA disrupters has, for example, 50,000 MA lives in a market, the decrease in hospital revenues for that MA population would be about $48 million. This does not include the associated physician fees and other costs in the care continuum. That same $48 million + in the coffers of the risk-taking MA disrupters allows them deliver comprehensive array of supportive services including addressing social determinants of health. These services then further reduce utilization and improves overall health status, creating a virtuous circle. This is very profitable.

MA is only the beginning. When successful MA businesses expand beyond MA, and they will, disruption across the healthcare economy will be profound and painful for the incumbents. The market is rationally exuberant about that prospect.