The Federal Trade Commission and the Justice Department are seeking comments on ways merger guidelines should be updated, and physicians are raising concerns about private equity-backed buyouts of provider practices.

The FTC and the Justice Department announced in January that they’re seeking to revamp merger guidelines for businesses. Comments on how to “modernize the merger guidelines to better detect and prevent anticompetitive deals,” can be submitted to the agencies through April 21.

Comments are pouring in from physicians. Many of the comments are anonymous, but the commenters self-identify as physicians.

The physicians’ top concern are private equity-backed buyouts, according to an analysis by Law360. They’re also concerned by the profit-first attitude of healthcare and consolidation in the industry, according to the report.

The comments are coming in as private equity firms continue to buy up physician practices.

Private equity firms acquired 59 physician practices in 2013, and that number increased to 136 practices by 2016, according to a research letter published in JAMA.

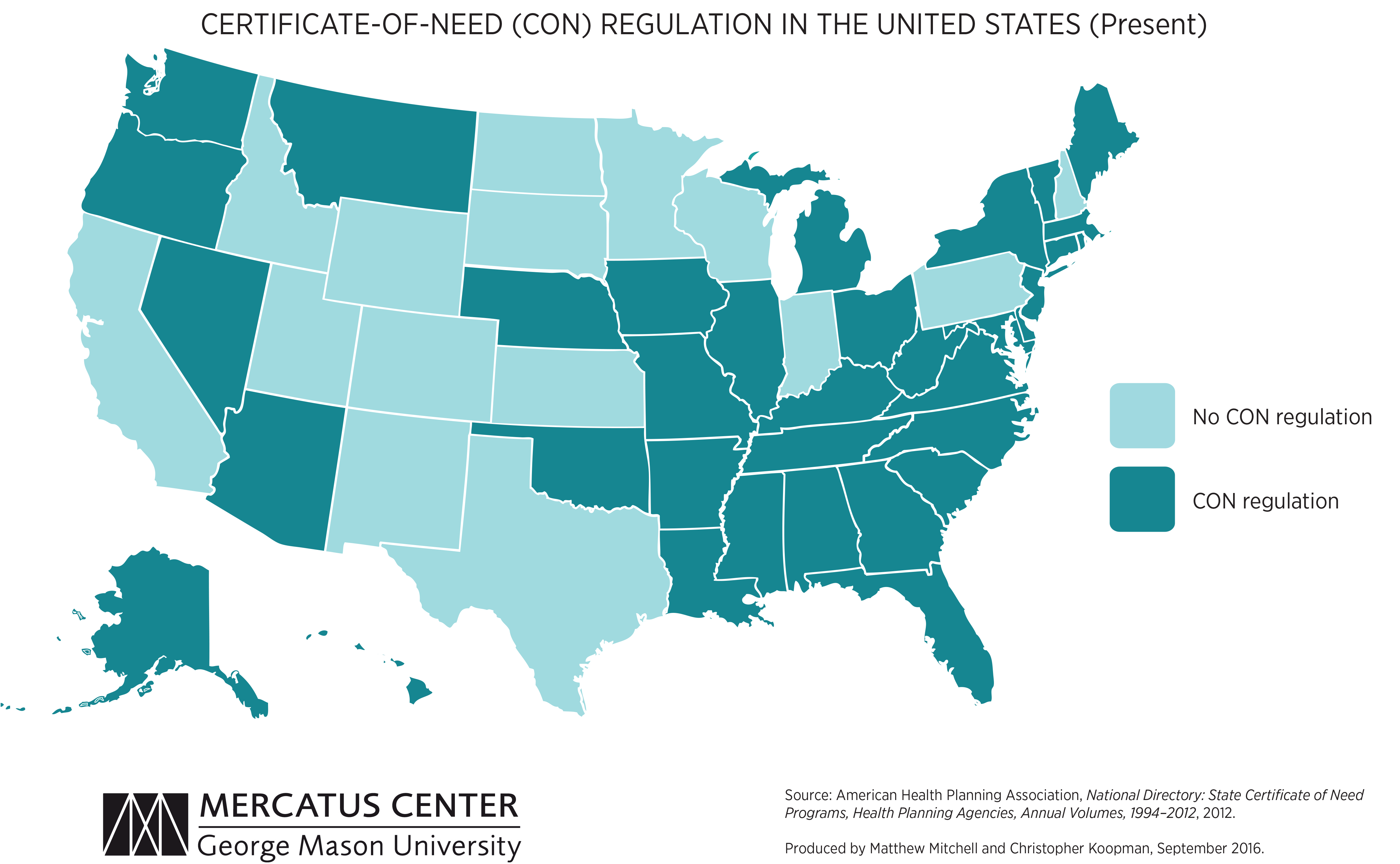

We’re picking up on a growing concern among health system leaders that many states with “certificate of need” (CON) laws in effect are on the cusp of repealing them. CON laws, currently in place in 35 states and the District of Columbia, require organizations that want to construct new or expand existing healthcare facilities to demonstrate community need for the additional capacity, and to obtain approval from state regulatory agencies. While the intent of these laws is to prevent duplicative capacity, reduce unnecessary utilization, and control cost growth, critics claim that CON requirements reduce competition—and free market-minded state legislators, particularly in the South and Midwest, have made them a target.

One of our member systems located in a state where repeal is being debated asked us to facilitate a scenario planning session around CON repeal with system and physician leaders. Executives predicted that key specialty physician groups would quickly move to build their own ambulatory surgery centers, accelerating shift of surgical volume away from the hospital.

The opportunity to expand outpatient procedure and long-term care capacity would also fuel investment from private equity, which have already been picking up in the market. An out-of-market health system might look to build microhospitals, or even a full-service inpatient facility, which would be even more disruptive.

CON repeal wasn’t all downside, however; the team identified adjacent markets they would look to enter as well. The takeaway from our exercise: in addition to the traditional response of flexing lobbying influence to shape legislative change, the system must begin to deliver solutions to consumers that are comprehensive, convenient, and competitively priced—the kind of offerings that might flood the market if CON laws were lifted.

We recently shared an updated perspective on the independent physician landscape. Notably absent from this map, but an important player in this space, are entities, like health plans, private equity, and health systems, who partially or wholly fund some independent physician groups.

We intentionally left these funders off the map because they don’t work in a uniform way with all physician groups. The reality is that funders have their handprints all over this map—and just knowing what type of funder you’re working with doesn’t necessarily tell you how they work with physician groups.

Funders work across the physician landscape because they recognize two things:

First, in order to play in today’s physician market, funders need to be flexible in how they work with physicians in order to appeal to the wide variety of groups and build a bigger market presence.

Second, building or buying these physician group archetypes outright is not the only way to work with them. Many funders instead opt to invest in them—either through dollars or resources.

Key funders to watch

There are three key funders we track the closest: private equity, health plans, and health systems. Below are brief overviews of how they commonly work with independent groups and our predictions for where you might see them go next.

Private equity (PE): Consistent approach with still to be proven outcomes

The goal of PE firms is to make money on their investments. To do this, these firms buy shares of practices in order to have partial ownership. In return, physician groups get the capital they need to make investments—investments that in theory drive profits for both the physician shareholders and the PE investors. Unlike other funders, PE is rarely associated with full acquisition.

Two of the places we’ve seen the most private equity investment are in consolidation of specialty practices (usually at the national level) or value-based care investments in primary care practices (across all archetypes).

Private equity is gaining traction as a physician group partner because they often try to preserve some degree of physician autonomy and they’ve learned to nuance their investments and pitches based on the group they’re seeking to work with.

We predict: PE will continue to back the full range of archetypes on this map—investing in both independent groups directly and the national archetypes.

What we’ll be watching:

What will happen to the handful of major PE investments in the independent physician group space that will be reaching their 5-7 year mark

What level of physician autonomy will PE firms continue to preserve as PE gains stronger footholds in the physician landscape

Health plans: The most eager to transform (incrementally)

Health plans are often predominantly associated with a single physician archetype for a given plan. For example, when you think about UnitedHealthcare, you might think of their sister company, OptumCare, and an aggregation strategy. Or, you might think of Blues plans most commonly as service partners.

However, when you dig deeper, the story is much more nuanced. Plans and their parent companies like UnitedHealth Group do often aggregate practices, but they also sell and integrate services via service partner models. And several Blues plans are now building practices from the ground up. To top it off, some plans are even adopting an investment strategy like Anthem with Privia.

Perhaps more than any other funder, health plans often adopt a range of strategies to develop their physician strategy and maintain their existing networks. And even cases where plans aren’t funding entities themselves, they’re thinking of new ways to work with the growing range of physician groups.

We predict: Health plans will move away from a uniform approach to physician practice partnership and towards more multifaceted approaches to appeal to a wide range of providers.

What we’ll be watching:

Will health plans diversify their suite of approaches based on the groups they’re pursuing

Will health plans tailor their value proposition for each partnership approach

Health systems: Playing catch up to evolve

We often tend to think about health systems as aggregators—they buy independent physician groups and add them to their employed medical groups. But we’re seeing two physician market shifts that are causing health systems to move away from a one-size-fits-all approach.

One, the remaining independent groups are growing in size and, two, they are less willing to be acquired. On top of that, as private equity firms and payers continue to diversify their strategies, health systems must adapt to keep pace—or risk being seen as the least attractive partner.

As a result, more health systems are telling us about their new approaches to physician partnerships, like starting an MSO to act as a service partner or convening coalitions between themselves and independent groups.

We predict: Health systems will face increasing pressure to diversify how they are operating with physician groups. Similar to health plans, we expect to see a pivot away from an aggregation-only approach. To learn more, read our take on how health systems and independent groups should think about partnership.

What we’ll be watching:

How quickly will health systems stand up additional partnership approaches

Will health systems in markets where they’re the dominant partner proactively adjust their partnership approach versus wait for the market to shift first

Your checklist to work successfully with today’s physician groups

As you evaluate your partnership strategy, here’s our starter list of questions to ask yourself:

Clarify your partnership goals:

What are my organization’s goals for physician partnership broadly?

What are the archetypes I currently fund or partner with?

Do these archetypes serve my organization’s stated goals?

Identify the right partnership approaches for your organization

What new archetypes should I build or work with to advance my organization’s goals and target new physician groups?

Do I need to build this archetype myself or is it better to fund one that exists?

If funding, should I wholly own or invest in the archetype?

Define your value proposition to physicians

Have I adjusted my value proposition for each of the archetypes I fund or partner with?

Am I clearly articulating my value proposition in a way that speaks to physicians’ needs and wants?

Does my value proposition align with what I’m actually delivering? For example, if I say I’m preserving autonomy, how am I doing that?

How does my value proposition compare and compete with others in the market?

Map out the power dynamics of the archetypes you want to work with

Who has the ultimate decision-making power in the organization? (Hint: Decision-making power gets more diffuse as you move from right to left, national chain to service partner.)

Who are the key stakeholders who influence decision-making?

There’s been a lot of hand wringing over the ongoing feeding frenzy among private equity (PE) firms for physician practice acquisition, which has caused health system executives everywhere to worry about the displacement effect on physician engagement strategies (not to mention the inflationary impact on practice valuations).

While we’ve long believed that PE firms are not long-term owners of practices, instead playing a roll-up function that will ultimately end in broader aggregation by vertically-integrated insurance companies, a recent conversation with one system CEO reframed the phenomenon in a way we hadn’t thought of before. It’s all about ademographic shift, she argued.

There’s a generation of Boomer-aged doctors who followed their entrepreneurial calling and started their own practices, and are now nearing retirement age without an obvious path to exit the business. Many didn’t plan for retirement—rather than a 401(k), what they have is equity in the practice they built.

What the PE industry is doing now is basically helping those docs transition out of practice by monetizing their next ten years of income in the form of a lump-sum cash payout. You could have predicted this phenomenon decades ago.

The real question is what happens to the younger generations of doctors left behind, who have another 20 or 30 years of practice ahead of them? Will they want to work in a PE-owned (or insurer-owned) setting, or would they prefer health system employment—or something else entirely?

The answer to that question will determine the shape of physician practice for decades to come…at least until the Millennials start pondering their own retirement.

The number of independent physician practices continued to decline nationwide as health systems, payers, and investors accelerated their physician acquisition and employment strategies during the pandemic.

The graphic above highlights recent analysis from consulting firm Avalere Health and the nonprofit Physicians Advocacy Institute, finding that nearly half of physician practices are now owned by hospital or corporate entities, meaning insurers, disruptors, or other investor-owned companies.

This increase has been driven mainly by a surge in the number of corporate-owned practices, which has grown over 50 percent across the last two years. (Researchers said they were unable to accurately break down corporate employers more specifically, and that the study likelyundercounts the number of practices owned by private equity firms, given the lack of transparency in that segment.)

It’s no surprise that we’re seeing an uptick in physician employment, as about a quarter of physicians surveyed a year ago claimed COVID was making them more likely to sell or partner with other entities, and last year saw independent physicians’ average salary falling below that of hospital-employed physicians.

We expect the move away from private practice will continue throughout this year and beyond, as physicians seek financial stability and access to capital for necessary investments to remain competitive.

A new report from consulting firm Avalere Health and the nonprofit Physicians Advocacy Institute finds that the pandemic accelerated the rise in physician employment, with nearly 70 percent of doctors now employed by a hospital, insurer or investor-owned entity.

Researchers evaluated shifts to employment in the two-year period between January 2019 and January 2021, finding that 48,400 additional doctors left independent practice to join a health system or other company, with the majority of the change occurring during the pandemic. While 38 percent chose employment by a hospital or health system,the majority of newly employed doctors are now employed by a “corporate entity”, including insurers, disruptors and investor-owned companies.

(Researchers said they were unable to accurately break down corporate employers by entity, and that the study likely undercounts the number of physician practices owned by private equity firms, given the lack of transparency in that segment.) Growth rates in the corporate sector dwarfed health system employment, increasing a whopping 38 percent over the past two years, in comparison to a 5 percent increase for hospitals.

We expect this pace will continue throughout this year and beyond, as practices seek ongoing stability and look to manage the exit of retiring partners, enticed by the outsized offers put on the table by investors and payers.

As we reported recently, healthcare M&A hit record highs in the first quarter of 2021—with deal activity in the physician practice space surging 87 percent. The graphic above highlights private equity firms’ increasing investment in the sector over the last five years. Both the number and size of PE-backed healthcare deals have increased substantially from 2015 to 2020, up 39 and 45 percent respectively.

In 2020, physician practices and services comprised nearly a fifth of all transactions, with PE firms driving the majority. One in five physician transactions involvedprimary care practices—a signal that investors are banking on profits to be made in the shift to value-based care models.

Meanwhile, PE firms are still rolling up high-margin specialty practices, with ophthalmology, orthopedics, dermatology, and anesthesiology groups all receiving significant funding in 2020. PE investment in physician practices will likely continue to accelerate, as investors view healthcare as a promising place to deploy readily available capital.

But we remain convinced that private equity investors have little interest in being long-term owners of practices,and will ultimately look for an exit by selling “rolled-up” physician entities to health systems or insurers.

On Thursday, the Biden administration issued the first of what is expected to be a series of new regulations aimed at implementing the No Surprises Act, passed by Congress last year and signed into law by President Trump, which bans so-called “surprise billing” by out-of-network providers involved in a patient’s in-network hospital visit.

The interim final rule, which takes effect in 2022, prohibits surprise billing of patients covered by employer-sponsored and individual marketplace plans, requiring providers to give advance warning if out-of-network physicians will be part of a patient’s care, limiting the amount of patient cost-sharing for bills issued by those providers, and prohibiting balance billing of patients for fees in excess of in-network reimbursement amounts.

The rule also establishes a process for determining allowable rates for out-of-network care, involving comparison to prevailing statewide rates or the involvement of a neutral arbitrator, but falls short of specifying a baseline price for arbitrators to use in determining allowable charges. That methodology, along with other details, will be part of future rulemaking, which will be issued later this year.

Of note, the rule does not include a ban on surprise billing forground ambulance services, which were excluded by Congress in the law’s final passage—even though more than half of all ambulance trips result in an out-of-network bill. Expect intense lobbying by industry interests to continue as the details of future rulemaking are worked out, as has been the case since before the law was passed.

While burdensome for patients,surprise billing has become a lucrative business model for some large, investor-owned specialist groups, who will surely look to minimize the law’s impact on their profits.

Medicare Advantage (MA) focused companies, like Oak Street Health (14x revenues), Cano Health (11x revenues), and Iora Health (announced sale to One Medical at 7x revenues), reflect valuation multiples that appear irrational to many market observers. Multiples may be exuberant, but they are not necessarily irrational.

One reason for high valuations across the healthcare sector is the large pools of capital from institutional public investors, retail investors and private equity that are seeking returns higher than the low single digit bond yields currently available. Private equity alone has hundreds of billions in investable funds seeking opportunities in healthcare. As a result of this abundance of capital chasing deals, there is a premium attached to the scarcity of available companies with proven business models and strong growth prospects.

Valuations of companies that rely on Medicare and Medicaid reimbursement have traditionally been discounted for the risk associated with a change in government reimbursement policy. This “bop the mole” risk reflects the market’s assessment that when a particular healthcare sector becomes “too profitable,” the risk increases that CMS will adjust policy and reimbursement rates in that sector to drive down profitability.

However, there appears to be consensus among both political parties that MA is the right policy to help manage the rise in overall Medicare costs and, thus, incentives for MA growth can be expected to continue. This factor combined with strong demographic growth in the overall senior population means investors apply premiums to companies in the MA space compared to traditional providers.

Large pools of available capital, scarcity value, lower perceived sector risk and overall growth in the senior population are all factors that drive higher valuations for the MA disrupters.However, these factors pale in comparison the underlying economic driver for these companies. Taking full risk for MA enrollees and dramatically reducing hospital utilization, while improving health status, is core to their business model. These companies target and often achieve reduced hospital utilization by 30% or more for their assigned MA enrollees.

In 2019, the average Medicare days per 1,000 in the U.S. was 1,190. With about $14,700 per Medicare discharge and a 4.5 ALOS, the average cost per Medicare day is approximately $3,200. At the U.S. average 1,190 Medicare hospital days per thousand, if MA hospital utilization is decreased by 25%, the net hospital revenue per 1,000 MA

enrollees is reduced by about $960,000. If one of the MA disrupters has, for example, 50,000 MA lives in a market, the decrease in hospital revenues for that MA population would be about $48 million. This does not include the associated physician fees and other costs in the care continuum. That same $48 million + in the coffers of the risk-taking MA disrupters allows them deliver comprehensive array of supportive services including addressing social determinants of health. These services then further reduce utilization and improves overall health status, creating a virtuous circle. This is very profitable.

MA is only the beginning. When successful MA businesses expand beyond MA, and they will, disruption across the healthcare economy will be profound and painful for the incumbents. The market is rationally exuberant about that prospect.