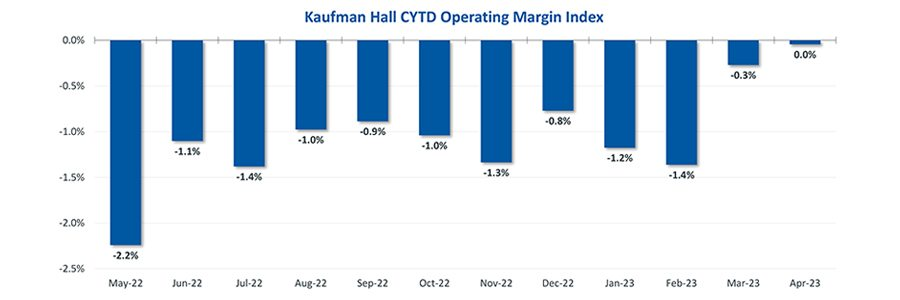

Hospital finances showed signs of stabilizing in May amid slightly improving operating margins, declining expenses and notable increases in outpatient visits.

The median Kaufman Hall Year-To-Date Operating Margin Index reflecting actual margins was 0.3% in May.

The June issue of the National Hospital Flash Report covers these and other key performance metrics.

About the Data

The National Hospital Flash Report uses both actual and budget

data over the last three years, sampled from more than 900 hospitals

on a recurring monthly basis from Syntellis Performance Solutions.

The sample of hospitals for this report is representative of all hospitals in

the United States both geographically and by bed size. Additionally,

hospitals of all types are represented, from large academic to small

critical access. Advanced statistical techniques are used to standardize

data, identify and handle outliers, and ensure statistical soundness prior

to inclusion in the report.

While this report presents data in the aggregate, Syntellis Performance

Solutions also has real-time data down to individual department,

jobcode, paytype, and account levels, which can be customized into peer

groups for unparalleled comparisons to drive operational decisions and

performance improvement initiatives.

Key Takeaways

- Hospitals broke even in April.

The median operating margin for hospitals was 0% in April, leaving most hospitals with little to no

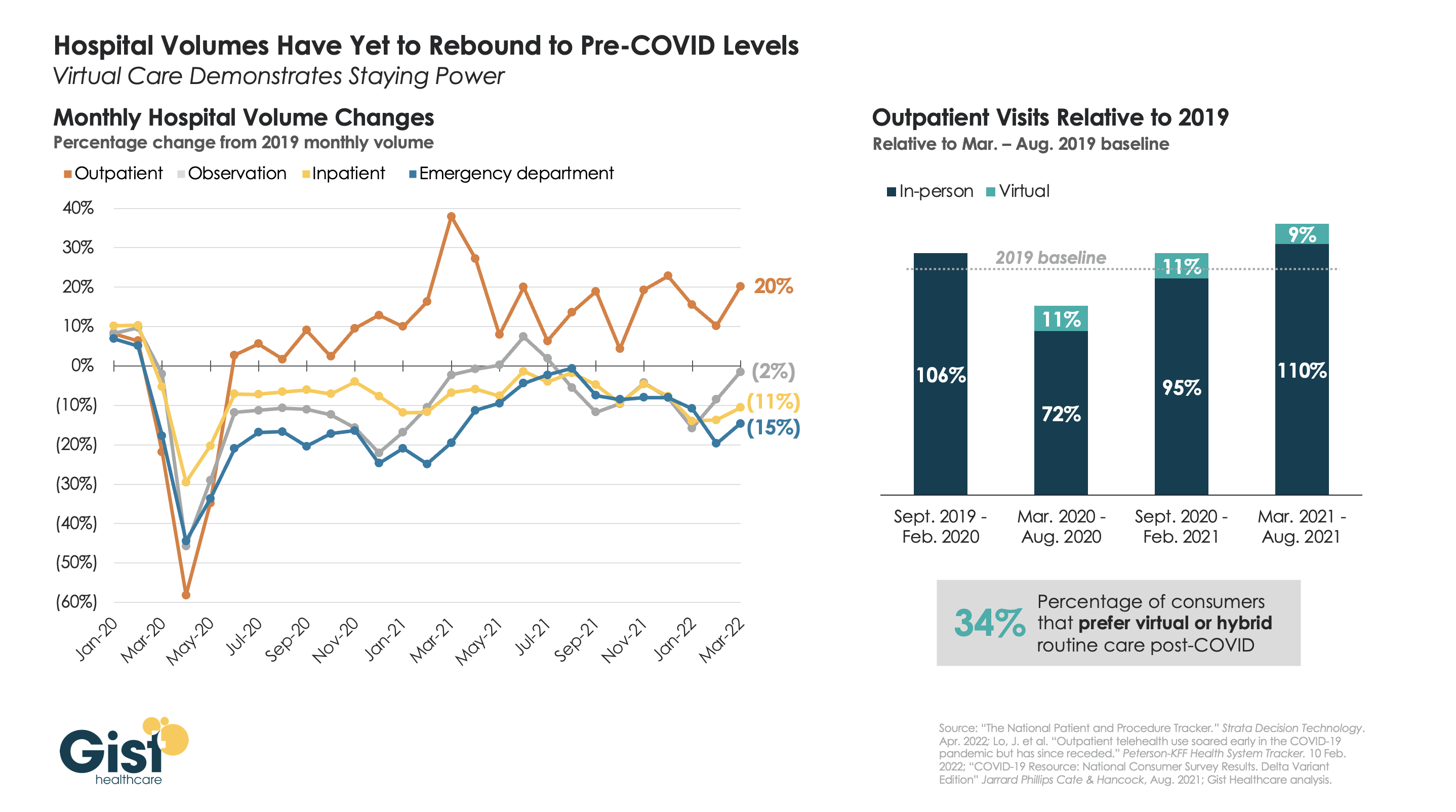

financial wiggle room. - Volumes dropped while lengths of stay increased.

Hospital volumes dropped across the board—including inpatient and outpatient. Emergency department

volumes were the least affected. - Effects of Medicaid disenrollment could be materializing.

Hospitals experienced increases in bad debt and charity care in April. Combined with anemic patient

volumes, experts note this data could illustrate the effects of the start of widespread disenrollment from

Medicaid following the end of the COVID-19 public health emergency. - Inflation continued to throttle hospital finances.

Labor costs jumped in April and the costs of goods and services continued to be well above pre-pandemic

levels. Though expenses generally fell in April, revenues declined at a faster rate.

National Non-Operating Results

Key Observations

At their May meeting, the Federal Open Market Committee (FOMC) raised the

benchmark borrowing rate another 25 basis points, setting the range to 5.00-5.25%

and marking the 10th consecutive hike in the cycle as well as a 16-year high

- Fed officials acknowledged discussion of a potential pause in tightening while

leaving wiggle room, saying “rates are going to come down” over a long period of

time while also warning inflation “continues to run high” and the Fed will be taking

a “data-dependent approach” - The consumer price index (CPI) rose 0.4% in April, a 4.9% increase year-over-year,

an annual pace of inflation below 5% for the first time in two years - The labor market continued to show resilience in April as U.S. nonfarm payrolls

grew by 253,000 and unemployment fell back to a 53-year low of 3.4% - Strong inflation, a robust labor market, continued banking sector woes, and a debt

ceiling standoff further complicates credit conditions and may challenge

the Fed to stabilize financial markets - Equities in April, as measured by the S&P 500, were up 1.5% in April and

8.6% YTD despite downbeat economic data, reoccurring banking sector fears,

and mixed earnings