Welcome to Friday’s Health 202, where today we have a special spotlight on the pandemic two years in.

🚨 The federal government is about to be funded. The Senate sent the long-term spending bill to President Biden’s desk last night after months of intense negotiations.

Two years since the WHO declared a pandemic, what health-care system changes are here to stay?

Nurses screened patients at a drive-through testing site in March 2020. (Win McNamee/Getty Images)

Exactly two years ago, the World Health Organizationdeclared the coronavirus a pandemic and much of American life began grinding to a halt.

That’s when the health-care system, which has never been known for its quickness, sped up. The industry was forced to adapt, delivering virtual care and services outside of hospitals on the fly. Yet, the years-long pandemic has exposed decades-old cracks in the system, and galvanized efforts to fix them.

Today, as coronavirus cases plummet and President Biden says Americans can begin resuming their normal lives, we explore how the pandemic could fundamentally alter the health-care system for good. What changes are here to stay — and what barriers are standing in the way?

A telehealth boom

What happened: Telehealth services skyrocketed as doctors’ offices limited in-person visits amid the pandemic. The official declaration of a public health emergency eased long-standing restrictions on these virtual services, vastly expanding Medicare coverage.

But will it stick? Some of these changes go away whenever the Biden administration decides not to renew the public health emergency (PHE). The government funding bill passed yesterday extends key services roughly five months after the PHE ends, such as letting those on Medicare access telehealth services even if they live outside a rural area.

But some lobbyists and lawmakers are pushing hard to make such changes permanent. Though the issue is bipartisan and popular, it could be challenging to pass unless the measures are attached to a must-pass piece of legislation.

“Even just talking to colleagues, I used to have to spend three or four minutes while they were trying desperately not to stare at their phone and explain to them what telehealth was … remote patient monitoring, originating sites, and all this wonky stuff,”said Sen. Brian Schatz (D-Hawaii), a longtime proponent of telehealth.

“Now I can go up to them and say, ‘So telehealth is great, right?’ And they say, ‘yes, it is.’ ”

A new spotlight on in-home care

What happened: The infectious virus tore through nursing homes, where often fragile residents share rooms and depend on caregivers for daily tasks. Ultimately, nearly 152,000 residents died from covid-19.

The devastation has sparked a rethinking of where older adults live and how they get the services they need — particularly inside their own homes.

“That is clearly what people prefer,” said Gail Wilensky, an economist at Project HOPE who directed the Medicare and Medicaid programs under President George H.W. Bush. “The challenge is whether or not it’s economically feasible to have that happen.”

More money, please: Finding in-home care — and paying for it — is still a struggle for many Americans. Meanwhile, many states have lengthy waitlists for such services under Medicaid.

Experts say an infusion of federal funds is needed to give seniors and those with disabilities more options for care outside of nursing homes and assisted-living facilities.

For instance, Biden’s massive social spending bill included tens of billions of dollars for such services. But the effort has languished on Capitol Hill, making it unclear when and whether additional investments will come.

A reckoning on racial disparities

What happened: Hispanic, Black, and American Indian and Alaska Native people are about twice as likely to die from covid-19 than White people. That’s according to age-adjusted data from a recent Kaiser Family Foundation report.

In short, the coronavirus exposed the glaring inequities in the health-care system.

“The first thing to deal with any problem is awareness,” said Georges Benjamin, the executive director of the American Public Health Association. “Nobody can say that they’re not aware of it anymore, that it doesn’t exist.”

But will change come? Health experts say they hope the country has reached a tipping point in the last two years. And yet, any real systemic change will likely take time. But, Benjamin said, it can start with increasing the number of practitioners from diverse communities, making office practices more welcoming and understanding biases.

We need to, as a matter of course, ask ourselves who’s advantaged and who’s disadvantaged” when crafting new initiatives, like drive-through testing sites, Benjamin said. “And then how do we create systems so that the people that are disadvantaged have the same opportunity.”

A lot of communication in the workplace is conducted electronically. However, it is essential for hospital and health system leaders to have face-to-face conversations with employees in some situations.

Becker’s asked healthcare executives to share the interactions they prioritize when they’re in person at their organizations. Many expressed their preference for the deeper connections in-person interactions allow, citing inspiration and team building as reasons to facilitate face-to-face communication. Below are their responses:

Russell F. Cox. President and CEO of Norton Healthcare (Louisville, Ky.): Healthcare, by its very nature, requires in-person interactions.

With the onset of the COVID-19 pandemic, we made a quick and successful shift to virtual visits for the safety of our patients and providers. This enabled patients with a variety of time and transportation constraints to receive convenient care from a trusted provider. However, telemedicine will never completely replace in-person visits, and the opportunity for our patients and community to interact in-person with our patient care providers is very important to me, and to our team.

And, although the pandemic created the need for virtual meetings, I have always prioritized in-person interactions and meetings with all team members. Whether that be rounding in our hospitals and facilities, holding in-person meetings, celebrating employee accomplishments or milestones, or dropping by one of our community vaccine or testing centers — web meetings will never replace what can be accomplished face to face. It became even more important to interact in person with our caregivers and employees during the pandemic. It was important to show my support for their hard work and extraordinary sacrifices during this time. I’m thankful that with the vaccine, more in-person events, with proper safety precautions, are resuming.

Our motto has been and continues to be: Stay safe. Keep the faith.

Jim Dunn, PhD. Executive Vice President and Chief People and Culture Officer of Atrium Health (Charlotte, N.C.): Recognition is part of our organizational DNA, and in-person delivery is an essential component of that — especially as we continue working through the COVID-19 pandemic. One thing our teammates love is the “Surprise Patrol,” which we employ for some of our most special and meaningful awards, such as our annual Pinnacle Award — the highest award given by our organization to those who best exemplify our Culture Commitments: Belong, Work as One, Trust, Innovate and Excellence. Executives, leaders, teammates and loved ones come together to celebrate honorees with balloons, cupcakes, cheers and even a few happy tears. Our honorees are shocked, uplifted and proud to be recognized in-person for their outstanding accomplishments, and our “Surprise Patrol” participants are honored to be a part of such a special moment. Whether we’re celebrating small wins, personal successes, birthdays or prestigious awards, in-person recognition — where and when possible — is a vital part of the teammate experience and culture at Atrium Health.

Robert Gardner. CEO of Banner Ironwood Medical Center (Queen Creek, Ariz.) and Banner Goldfield Medical Center (Apache Junction, Ariz.): Over the past few years in particular, I’ve spent some time reflecting on the differences between motivation and inspiration. More often than not, it seems like leaders don’t know the differences and often confuse the two as being synonymous or interchangeable. Put in overly simplified terms, I see motivation as being the metaphorical carrot or the stick. We can motivate with reward (aka the carrot) and with discipline (aka the stick), and both are used frequently in life. Motivation tends to be more surface level. However, inspiration is something much deeper, more intimate, and therefore much more complex. Inspiration is getting to a point of genuinely desiring to change, do more, be better, etc.

For me, knowing the differences is critical when it comes to prioritizing being in person in the workplace. Virtual meetings, emails, newsletters and other forms of electronic communication can work incredibly well when it comes to items of motivation; and believe me, there are plenty of these items. However, when it comes time to inspire the team, I heavily prioritize these meetings to take place in person. Items that fall into this category will be mission-critical initiatives and overall reminders on living our mission, purpose values, etc. It’s so ironic to me that despite the increasing complexity, regulation, bureaucracy and proverbial red tape that healthcare has become famous for, that an inspirational dose of simplicity has more effect on change than any other bestseller leadership book on how to motivate performance through some sort of complicated multistep process.

Brian Koppy. Chief Financial Officer of Cano Health (Miami): As a rapidly growing primary care provider, we have found that face-to-face interactions at our offices are as essential as they are in our medical centers. Our providers provide the best care when they see patients in person because it builds lifelong bonds that improve patient outcomes. In our offices, our team members feel more connected and integrated into the Cano Health family when we are together, both formally and informally. This, of course, does not mean we do not have a flexible work environment, which we do. It simply means our priority is on the employee benefits and outcomes that come from working in the office.

At the beginning of the pandemic, we moved many corporate employees to remote work and moved about 95 percent of our patient interactions to televisits. That did not last long, however. Within a month or two, our employees were asking to come back to the office. Our medical centers never closed their doors, and our visits rapidly returned to mostly in person.

It’s the seemingly inconsequential daily interactions that often have the greatest impact on a company’s employees and their connection to the mission, values and culture of the organization. The quick stop-ins to someone’s workstation, the chance hallway encounters, the team lunches — these are so important in developing relationships and, in turn, maximizing efficiency. Employees who know and personally interact with each other work better together. They discuss ideas, they strategize freely, and they execute on the company’s goals together and more effectively.

At Cano Health, our high-touch approach to primary care is key to our success. And we believe that daily face-to-face interactions among employees are equally important to create a rewarding experience for our employees, but also expanding Cano Health’s services across the country.

Christopher O’Connor. President and incoming CEO of Yale New Haven (Conn.) Health:We are prioritizing one-on-one meetings and small groups. With our vaccination mandate, we feel it is critical to have that in-person contact and fill that void that video can’t replicate. This is a relationship business, and spending the time to build and nurture those relationships is critical.

Thomas J. Senker. President of MedStar Montgomery Medical Center (Olney, Md.): Before and especially during the pandemic our priority has been the well-being and engagement of our front-line staff and essential personnel. And while in-person activities have been limited, our executive team makes regular rounds visiting each unit, expressing gratitude, providing snacks and refreshments, and sharing important hospital updates directly. We believe these face-to-face interactions are critical opportunities to gain feedback and focus on areas of improvement across different areas of MedStar Montgomery Medical Center’s operations.

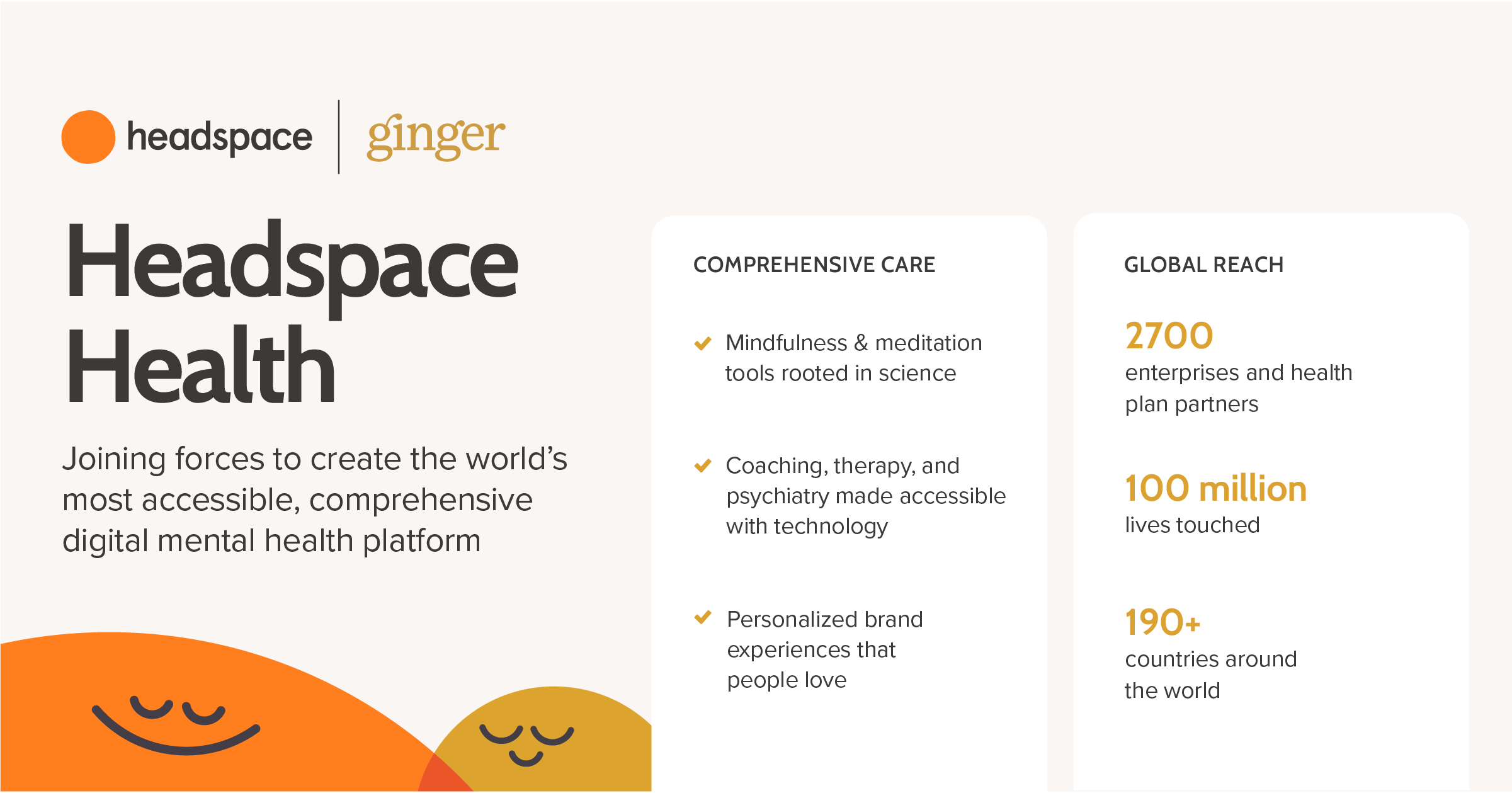

Two of the best-known companies in the virtual mental health space announced plans to merge this week, creating a $3B player poised to dominate this fast-growing segment of healthcare demand.

Headspace, a direct-to-consumer provider of app-based “mindfulness” meditation programs, will combine with Ginger, which sells text- and video-based coaching and therapy services to employers and insurers. Between them, the two companies claim to serve over 100M users worldwide.

Headspace is best known as a consumer-focused app, while Ginger largely serves business and payer clients. The combined company, to be called Headspace Health, will surely look to consolidate offerings into a comprehensive mental health service for employees, targeting a benefits market that is rapidly becoming overwhelmed with startup providers of virtual point solutions.

Behavioral health telemedicine utilization skyrocketed during last year’s COVID surge, and has been the one area of virtual care not to fall back to earth since—we’ve learned that virtual is often a superior approach for many mental health services.

Two questions arose in our minds after the Headspace/Ginger merger was announced. First, does the combined company bring a broad enough value proposition to overcome employer frustration with a highly fragmented market, or will the new Headspace Health eventually need to be part of a larger insurer platform to capture the opportunity in front of it? And second, does “mindfulness” even work?

The academic evidence is decidedly mixed, but the popularity of Headspace and other meditation apps, especially among Millennial consumers, might make that question moot. The mindfulness “wrapper” on more traditional mental health services may prove to be very popular with employees, and could become a must-have element of employers’ benefit packages.

Telehealth claim lines as a percentage of all medical claims dropped 13% in April, marking the third straight month of declines, according to new data from nonprofit Fair Health.

The dip was greater than the drop of 5.1% in March, but not as large as the decrease of almost 16% in February. However, overall utilization remains significantly higher than pre-COVID-19 levels.

The decline appears to be driven by a rebound in in-person services, researchers said. Mental health conditions bucked the trend, however, as the percentage of telehealth claim lines associated with mental conditions — the No. 1 telehealth diagnosis — continued to rise nationally and in every U.S. region.

Dive Insight:

The coronavirus spurred an unprecedented increase in telehealth utilization early last year. But early data from 2021 suggests demand is slowing as vaccinations ramp up and COVID-19 cases decrease across the U.S.

Fair Health has used its database of over 33 billion private claims records to analyze the monthly evolution of telehealth since May last year. Telehealth usage peaked among the privately insured population last April, before easing through September and re-accelerating starting in October, as the coronavirus found a renewed foothold in the U.S.

In January, virtual care claims made up 7% of all medical claim lines, but that fell to 5.9% in February, 5.6% in March and just 4.9% in April, suggesting a steady deceleration in telehealth demand.

The deceleration in April was seen in all U.S. regions, but was particularly pronounced in the South, Fair Health said, which saw a 12.2% decrease in virtual care claims.

The trend doesn’t bode well for the ballooning virtual care sector, which has enjoyed historic levels of funding during COVID-19. Just halfway through the year, 2021 has already blown past 2020’s record for digital health funding, with a whopping $14.7 billion. This latest data suggests dampening utilization could throw cold water on the red-hot marketplace.

And policymakers are still mulling how many telehealth flexibilities should be allowed after the public health emergency expires, expected at the end of this year. Virtual care enjoys broad support on both sides of the aisle and the Biden administration’s top health policy regulators, including CMS administrator Chiquita Brooks-LaSure, have said they support permanently adopting virtual care coverage waivers, but returned restrictions on telehealth access could also stymie use.

Fair Health also found that nationally, mental health conditions increased from 57% from all telehealth claims in March to 59% in April. That month, psychotherapeutic/psychiatric codes jumped nationally as a percentage of telehealth procedure codes, while evaluation and management codes dropped, suggesting a continued need for virtual access to mental health services, which can be some of the rarest and most expensive medical services to find in one’s own geographic area.

Also in April, acute respiratory diseases and infections increased as a percentage of claim lines nationally, and in the Midwest and South, while general signs and symptoms joined the top five telehealth diagnoses in the West. Both trends suggest a return to non-COVID-19 respiratory conditions, like colds and bronchitis, and more ‘normal’ conditions like stomach viruses, researchers said.

As we shared recently, post-pandemic healthcare volume is not returning evenly. While outpatient volume is rebounding quickly, other settings remain sluggish, especially the emergency department. We partnered with healthcare data analytics company Stratasan to take a closer look at ED volume decline. As shown in the graphic above, nationally, ED visits were down 27 percent in 2020, compared to 2019. ED-only volume (cases that started and ended in the ED) took a large hit across last year, down nearly a third from 2019. We expect that a portion of this ED-only volume will never fully recover to pre-COVID levels, with patient demand permanently shifting to lower-acuity care settings, including virtual, and some patients avoiding care altogether for minor ailments as they learn to “live with” problems like back pain.

ED-to-observation volume saw the greatest decline in 2020, likely as a result both of patients avoiding the ED, and presenting in the ED sicker, meeting the criteria for inpatient admission. However,ED-to-inpatient volume, which fell only seven percent in 2020, has been returning. In the second half of 2020, the ED-to-inpatient admission rate was 20 to 30 percent higher than the pre-COVID baseline. Across all three categories of ED volume, pediatrics saw steeper declines compared to adult cases. While some further ED volume rebound is anticipated, health systems should expect that fewer, but sicker, patients will be the new normal for hospital emergency departments.

Fewer low-acuity patients utilizing high-cost emergency care is good news from a public health perspective, but health systems must bolster other access channels like urgent care and telemedicine to ensure patients have convenient access for emergent care needs.

Hardly one month into 2021, the pressing priorities facing healthcare leaders are abundantly clear.

First, we will be living in a world preoccupied by COVID-19 and vaccination for many months to come. Remember: this is a marathon, not a sprint. And the stark reality is that the vaccination rollout will continue well into the summer, if not longer, while at the same time we continue to care for hundreds of thousands of Americans sickened by the virus. Despite the challenges we face now and in the coming months in treating the disease and vaccinating a U.S. population of 330 million, none of us should doubt that we will prevail. Despite the federal government’s missteps over the past year in managing and responding to this unprecedented public health crisis, historians will recognize the critical role of the nation’s healthcare community in enabling us to conquer this once-in-a-generation pandemic.

While there has been an overwhelming public demand for the vaccine during the past couple of weeks, there remains some skepticism within the communities we serve, including some of the most-vulnerable populations, so healthcare leaders will find themselves spending time and energy communicating the safety and efficacy of vaccines to those who may be hesitant. This is a good thing. It is our responsibility to share facts, further public education and influence public policy.COVID-19 has enhanced public trust in healthcare professionals, and we can maintain that trust if we keep our focus on the right things — namely, how we improve the health of our communities.

And as healthcare leaders diligently balance this work, we also have a great opportunity to reimagine what our hospitals and health systems can be as we emerge from the most trying year of our professional lifetimes. How do you want your hospital or system organized? What kind of structural changes are needed to achieve the desired results? What do you really want to focus on? Amid the pressing priorities and urgent decision-making needed to survive, it is easy to overlook the great reimagination period in front of us. The key is to forget what we were like before COVID-19 and reflect upon what we want to be after.

These changes won’t occur overnight. We’ll need patience, but here are my thoughts on five key questions we need to answer to get the right results.

1. How do you enhance productivity and become more efficient? Throughout 2021, most systems will be in recovery mode from COVID’s financial bruises. Hospitals saw double-digit declines in inpatient and outpatient volumes in 2020, and total losses for hospitals and health systems nationwide were estimated to total at least $323 billion. While federal relief offset some of our losses, most of us still took a major financial hit. As we move forward, we must reorganize to operate as efficiently as possible. Does reorganization sound daunting? If so, remember the amount of reorganization we mustered to work effectively in the early days of the pandemic. When faced with no alternative, healthcare moved heaven and earth to fulfill its mission. Crises bring with them great clarity. It’s up to leaders to keep that clarity as this tragic, exhausting and frustrating crisis gradually fades.

2. How do you accelerate digital care? COVID-19 changed our relationship with technology, personally and professionally. Look at what we accomplished and how connected we remain. We were reminded of how high-quality healthcare can go unhindered by distance, commutes and travel constraints with the right technology and telehealth programs in place. Health system leaders must decide how much of their business can be accommodated through virtual care so their organizations can best offer convenience while increasing access. Oftentimes, these conversations don’t get far before confronting doubts about reimbursement. Remember, policy change must happen before reimbursement catches up. If you wait for reimbursement before implementing progressive telehealth initiatives, you’ll fall behind.

3. How will your organization confront healthcare inequities? In 2020, I pledged that Northwell would redouble its efforts and remain a leader in diversity and inclusion. I am taking this commitment further this year and, with the strength of our diverse workforce, will address healthcare inequities in our surrounding communities head-on. This requires new partnerships, operational changes and renewed commitments from our workforce. We need to look upstream and strengthen our reach into communities that have disparate access to healthcare, education and resources. We must push harder to transcend language barriers, and we need our physicians and medical professionals of color reinforcing key healthcare messages to the diverse communities we serve. COVID-19’s devastating effect on communities of color laid bare long-standing healthcare inequalities. They are no longer an ugly backdrop of American healthcare, but the central plot point that we can change. If more equitable healthcare is not a top priority, you may want to reconsider your mission. We need leaders whose vision, commitment and courage match this moment and the unmistakable challenge in front of us.

4. How will you accommodate the growing portion of your workforce that will be remote?Ten to 15 percent of Northwell’s workforce will continue to work remotely this year. In the past, some managers may have correlated remote work and teams with a decline in productivity. The past year defied that assumption. Leaders now face decisions about what groups can function remotely, what groups must return on-site, and how those who continue to work from afar are overseen and managed. These decisions will affect your organizations’ culture, communications, real estate strategy and more.

5. How do you vigorously hold onto your cultural values amid all of this change? This will remain a test through 2021 and beyond. Culture is the personality of your organization. Like many health systems and hospitals, much of Northwell’s culture of connectedness, awareness, respect and empathy was built through face-to-face interaction and relationships where we continually reinforced the organization’s mission, vision and values. With so many employees now working remotely, how can we continue to bring out the best in all of our people? We will work to answer that question every day. The work you put in to restore, strengthen and revitalize your culture this year will go a long way toward cementing how your employees, patients and community come to see your organization for years to come. Don’t underestimate the power of these seemingly simple decisions.

While we’ve been through hell and back over the past year, I’m convinced that the healthcare community can continue to strengthen the public trust and admiration we’ve built during this pandemic. However, as we slowly round the corner on COVID-19, our future success will hinge on what we as healthcare organizations do now to confront the questions above and others head-on. It won’t be quick or easy and progress will be a jagged line. Let’s resist the temptation to return to what healthcare was and instead work toward building what healthcare can be. After the crisis of a lifetime, here’s our opportunity of a lifetime. We can all be part of it.

The annual J.P. Morgan Healthcare Conference is one of the best ways to diagnose the financial condition of the healthcare industry. Every January, every key stakeholder — providers, payers, pharmaceutical companies, tech companies, medical device and supply companies as well as bankers, venture capital and private equity firms — comes together in one exam room, even when it is virtual, for their annual check-up. But as we all know, this January is unlike any other as this past year has been unlike any other year.

You would have to go back to the banking crisis of 2008 to find a similar moment from an economic perspective. At the time, we were asking, “Are banks too big to fail?” The concern behind the question was that if they did fail, the economic chaos that would follow would lead to a collapse with the consumer ultimately picking up the tab. The rest is history.

Healthcare is “Too Vital to Fail”

2020 was historic in too many ways to count. But in a year when healthcare providers faced the worst financial crisis in the history of healthcare, the headline is that they are still standing. And what they proved is that in contrast to banks in 2008 that were seen by many as “too big to fail,” healthcare providers in 2020 proved that they were “too vital to fail.”

One of the many unique things about the COVID-19 pandemic is we are simultaneously experiencing a health crisis, where healthcare providers are the front line in the battle, and an economic crisis, felt in a big way in healthcare given the unique role hospitals play as the largest employer in most communities. Hospitals and health systems have done the vast majority of testing, treating, monitoring, counseling, educating and vaccinating all while searching for PPE and ventilators, and conducting clinical trials. And that’s just the beginning of the list.

Stop and think about that for a minute. What would we have done without them? Thinking through that question will give you some appreciation for the critical, challenging and central role that healthcare providers have had to play over the past year.

Simply stated, healthcare providers are the heart of healthcare, both clinically (essentially 100 percent of the care) and financially (over 50 percent of the $4 trillion annual spend on U.S. healthcare). Over the last year they stepped up and they stepped in at the moment where we needed them the most. This was despite the fact that, like most businesses, they were experiencing calamitous losses with no assurances of any assistance.

Healthcare is “Pandemic-Proof”

This was absolutely the worst-case scenario and the biggest test possible for our nation’s healthcare delivery system. Patient volume and therefore revenue dropped by over 50 percent when the panic of the pandemic was at its peak, driving over $60 billion in losses per month across hospitals and healthcare providers. At the same time, they were dramatically increasing their expenses with PPE, ventilators and additional staff. This was not heading in a good direction. While failure may not have been seen as an option, it was clearly a possibility.

The CARES Act clearly provided a temporary lifeline, providing funding for our nation’s hospitals to weather the storm. While there are more challenging times ahead, it is now clear that most are going to make it to the other side. The system of care in our country is often criticized, but when faced with perhaps the most challenging moment in the history of healthcare, our nation’s hospitals and health systems stepped up heroically and performed miraculously. The work of our healthcare providers on the front line and those who supported them was and is one thing that we all should be exceptionally proud of and thankful for.In 2020, they proved that not only is our nation’s healthcare system too vital to fail, but also that it is “pandemic proof.”

Listening to Front Line at the 2021 J.P. Morgan Healthcare Conference

There has never been a more important year to listen to the lessons from healthcare providers. They are and were the front line of our fight against COVID-19. If there was a class given about how to deal with a pandemic at an institutional level, this conference is where those lessons were being taught.

This year at the J.P. Morgan Healthcare Conference, CEOs, and CFOs from many of the most prestigious and most well-respected health systems in the world presented including AdventHealth, Advocate Aurora Health, Ascension, Baylor Scott & White Health, CommonSpirit Health, Henry Ford Health System, Intermountain Healthcare, Jefferson Health, Mass General Brigham, Northwell Health, OhioHealth, Prisma Health, ProMedica Health System, Providence, Spectrum Health and SSM Health.

I’ve been in healthcare for 30 years and this is my fifth year of writing up the summary of the non-profit provider track of the conference for Becker’s Healthcare to help share the wisdom of the crowd of provider organizations that share their stories. Clearly, this year was different and not because the presentations were virtual, but because they were inspirational.

What did we learn? The good news is that they have made many changes that have the potential to move healthcare in a much better direction and to get to a better place much faster. So, this year instead of providing you a nugget from each presentation, I am going to take a shot at summarizing what they collectively have in motion to stay vital after COVID.

10 Moves Healthcare Providers are Making to Stay Vital After-COVID

As a leader in healthcare, you will never have a bigger opportunity to drive change than right now. Smart leaders are framing this as essentially “before-COVID (BC)” and “after-COVID (AC)” and using this moment as their burning platform to drive change. Credit to the team at Providence for the acronym, but every CEO talked about this concept. As the saying goes, “never let a good crisis go to waste.” Well, we’ve certainly had a crisis, so here is a list of what the top health systems are doing to ensure that they don’t waste it and that they stay vital after-COVID:

1. Take Care of Your Team and They’ll Take Care of You: In a crisis, you can either come together as a team or fall apart. Clearly there has been a significant and stunning amount of pressure on healthcare providers. Many are fearing that mental health might be our nation’s next pandemic in the near future because they are seeing it right now with their own team. Perhaps one of their biggest lessons from this crisis has been the need to address the mental, physical and spiritual health of both team members as well as providers. They have put programs in place to help and have also built a tremendous amount of trust with their team by, in many cases, not laying off and/or furloughing employees. While they have made cuts in other areas such as benefits, this collective approach proved incredibly beneficial. And the last point here that relates to thinking differently about their team is that similar to other businesses, many health systems are making remote arrangements permanent for certain administrative roles and moving to a flexible approach regarding their team and their space in the future.

2. Focus on Health Equity, Not Just Health Care: This was perhaps the most notable and encouraging change from presentations in past years at J.P. Morgan. I have been going to the conference for over a decade, and I’ve never heard someone mention this term or outline their efforts on “health equity” — this year, nearly everyone did. In the past, they have outlined many wonderful programs on “social determinants of health,” but this year they have seen the disproportionate impact of COVID on low-income communities bringing the ongoing issue of racial disparities in access to care and outcomes to light. As the bedrock of employment in their community, this provides an opportunity to not just provide health care, but also health equity, taking an active role to help make progress on issues like hunger, homelessness, and housing. Many are making significant investments in a number of these and other areas.

3. Take the Lead in Public Health — the Message is the Medicine:One of the greatest failings of COVID, perhaps the greatest lesson learned, is the need for clear and consistent messaging from a public health perspective. That is a role that healthcare providers can and should play. In the pandemic, it represented the greatest opportunity to save lives as the essence of public health is communication — the message is the medicine. A number of health systems stepped into this opportunity to build trust and to build their brand, which are essentially one in the same. Some organizations have created a new role — a Chief Community Health Officer — which is a good way to capture the work that is in motion relative to social determinants of health as well as health equity. Many understand the opportunity here and will take the lead relative to vaccine distribution as clear messaging to build confidence is clearly needed.

4. Make the Home and Everywhere a Venue of Care:A number of presenters stated that “COVID didn’t change our strategy, it accelerated it.” For the most part, they were referring to virtual visits, which increased dramatically now representing around 10 percent of their visits vs. 1 percent before-COVID. One presenter said, “Digital has been tested and perfected during COVID,” but that is only considering the role we see digital playing in this moment. It is clear some organizations have a very narrow tactical lens while others are looking at the opportunity much more strategically. For many, they are looking at a “care anywhere and everywhere” strategy. From a full “hospital in the home” approach to remote monitoring devices, it is clear that your home will be seen as a venue of care and an access point moving forward. The pandemic of 2020 may have sparked a new era of “post-hospital healthcare” — stay tuned.

5. Bury Your Budget and Pivot to Planning:The budget process has been a source of incredible distrust, dissatisfaction and distraction for every health system for decades. The chaos and uncertainty of the pandemic forced every organization to bury their budget last year. With that said, many of the organizations that presented are now making a permanent shift away from a “budget-based culture” where the focus is on hitting a now irrelevant target set that was set six to nine months ago to a “performance-based culture” where the focus is on making progress every day, week, month and quarter. Given that the traditional annual operating budget process has been the core of how health systems have operated, this shift to a rolling forecast and a more dynamic planning process is likely the single most substantial and permanent change in how hospitals and health systems operate due to COVID. In other words, it is arguably a much bigger headline than what’s happened with virtual visits.

6. Get Your M&A Machine in Motion: It was clear from the presentations that activity around acquisitions is going to return, perhaps significantly. These organizations have strong balance sheets and while the strong have gotten stronger during COVID, the weak have in many cases gotten weaker. Many are going to be opportunistic to acquire hospitals, but at the same time they have concluded that they can’t just be a system of care delivery. They are also focused on acquiring and investing in other types of entities as well as forming more robust partnerships to create new revenue streams. Organizations that already had diversified revenue streams in place came through this pandemic the best. Most hospitals are overly reliant on the ED and surgical volume. Trying to drive that volume in a value-based world, with the end of site of service differentials and the inpatient only list, will be an even bigger challenge in the future as new niche players enter the market. As I wrote in the headline of my summary two years ago, “It’s the platform, stupid.” There are better ways to create a financial path forward that involve leveraging their assets — their platform — in new and creative ways.

7. Hey, You, Get into the Cloud:With apologies for wrapping a Rolling Stones song into a conference summary, one of the main things touted during presentations was “the cloud” and their ability to pull clinical, operational and financial dashboards together to monitor the impact of COVID on their organization and organize their actions. Focus over the last decade has been on the clinical (implementing EHRs), but it is now shifting to “digitizing operations” with a focus on finance and operations (planning, cost accounting, ERPs, etc.) as well as advanced analytics and data science capabilities to automate, gather insight, manage and predict. It is clear that the cloud has moved from a curiosity to a necessity for health systems, making this one of the biggest areas of investment for every health system over the next decade.

8. Make Price Transparency a Key Differentiator: One of the great lessons from Amazon (and others) is that you can make a lot of money when you make something easy to buy. While many health systems are skeptical of the value of the price transparency requirements, those that have a deep understanding of both their true cost of care and margins are using this as an opportunity to prove their value and accelerate their strategy to become consumer-centric. While there is certainly a level of risk, no business has ever been unsuccessful because they made their product easier to understand and access. Because healthcare is so opaque, there is an opening for healthcare providers to build trust, which is their main asset, and volume, which is their main source of revenue, by becoming stunningly easy to do business with. This may be tough sledding for some as this isn’t something healthcare providers are known for. To understand this, spend a few minutes on Tesla’s website vs. Ford’s. The concept of making something easy, or hard, to buy will become crystal clear as fast as a battery-driven car can go from zero to 60.

9. Make Care More Affordable:This represents the biggest challenge for hospitals and health systems as they ultimately need to be on the right side of this issue or the trust that they have will disappear and they will remain very vulnerable to outside players. All are investing in advanced cost accounting systems (time-driven costing, physician costing, supply, and drug costing) to truly understand their cost and use that as a basis to price more strategically in the market. Some are dropping prices for shoppable services and using loss leader strategies to build their brand. The incoming Secretary of Health and Human Services has a strong belief regarding the accountability of health systems to be consumer centric. The health systems that understand this are working to get ahead of this issue as it is likely one of their most significant threats (or opportunities) over the next decade. This means getting all care to the right site of care, evaluating every opportunity to improve, and getting serious about eliminating the need for expensive care through building healthy communities. If you’re worried about Wal-Mart or Amazon, this is your secret weapon to keep them on the sideline.

10. Scale = Survival: One of the big lessons here is that the strong got stronger, the weak got weaker. For the strong, many have been able to “snapback” in financial performance because they were resilient. They were able to designate COVID-only facilities, while keeping others running at a higher capacity. To be clear, while most health systems are going to get to the other side and are positioned better than ever, there are many others that will continue to struggle for years to come. According to our data at Strata, we see 25 percent operating at negative margins right now and another 50 percent just above breakeven. They key to survival moving forward, for those that don’t have a captive market, will be scale. If this pandemic proved one thing relative to the future of health systems it is this — scale equals survival.

When Will We Return to Normal?

Based on what the projections that these health systems shared, the “new normal” for health systems for the first half of 2021 will be roughly 95 percent of prior year inpatient volume with a 20 percent year-over-year drop in ED volume and a drop of 10-15 percent in observation visits. So, the pain will continue, but given the adjustments that were already made in 2020, it looks like they will be able to manage through COVID effectively. While there will be a pickup in the second half of 2021, the safe bet is that a “return to normal” pre-COVID volumes likely won’t occur until 2022. And there are some who believe that some of the volume should have never been there to begin with and we might see a permanent shift downward in ED volume as well as in some other areas.

With that said, I’ll steal a quote from Bert Zimmerli, the CFO of Intermountain Healthcare, who said, “Normal wasn’t ever nearly good enough in healthcare.”In that spirit, the goal should be to not return to normal, but rather to use this moment as an opportunity to take the positive changes driven by COVID — from technology to processes to areas of focus to a sense of responsibility — and make them permanent.

Thanking Our “Healthcare Heroes”

We’ll never see another 2020 again, hopefully. With that said, one of the silver linings of the year is everything we learned in healthcare. The most important lesson was this — in healthcare there are literally heroes everywhere. To each of them, I just want to say “thank you” for being there for us when we needed you the most. We should all be writing love letters to those on the front line who risked their lives to save others. Our nation’s healthcare system has taken a lot of criticism through the years from those on the outside, often with a blind eye to how things work in practice vs. in concept. But this year we all got to see first-hand what’s happening inside of healthcare — the heroic work of our healthcare providers and those who support them.

They faced the worst crisis in the history of healthcare. They responded heroically and were there for our families and friends.

They proved that healthcare is too vital to fail. They proved that healthcare is pandemic-proof.

It turns out it’s not just the kids who aren’t getting snow days this year. This week, we spoke with an executive at a health system hit hard by Wednesday’s Nor’easter, and asked how the system was faring with the expected 18 inches of snowfall. He replied that the medical group was as busy as usual.

With all the work this spring to expand telemedicine capabilities, clinic staff were able to reach out to patients the day before the storm, and proactively convert a majority of scheduled in-person clinic visits to telemedicine. “Normally we would’ve been closed, and most appointments rescheduled for weeks down the road,” he told us. Instead, they were able to keep most of those visits in their scheduled time slot.

“Now that we have a systemwide process for telemedicine, I don’t think we’ll have a reason for the clinic to take a snow day again.” It’s a clear win-win for the system and patients: patient care seamlessly goes on. It’s easy to see the many use cases for the ability to toggle between in-person and virtual visits. A parent is stuck at home with a sick kid, and can’t make her endocrinologist appointment? Moved to virtual! A patient has an unexpected business trip taking him out of town? Don’t cancel, let’s do that follow-up visit via telemedicine.

We’ve been worried about the slowdown in progress made on telemedicine as patients switched back to in-person visits across the summer and fall. The ability to continue patient care during a record-breaking snowstorm is a perfect illustration of why it’s critical not to “backslide” with virtual care: meeting patients where they are, regardless of circumstances, is an essential part of building long-term loyalty and care continuity.

The pandemic put nurses on the front lines of the battle against COVID-19 and caused shifts in the way they provide care.

During this year, nurses have adapted to increased adoption of telehealth and virtual patient monitoring, as well as constantly evolving staffing needs.

These factors — and others, such as the physical and emotional conditions nurses have faced due to the public health crisis — are sure to affect nursing in the years to come. Here, 10 healthcare executives and leaders share their predictions for nursing in the next five years.

Editor’s note: Responses were edited lightly for length and clarity.

Beverly Bokovitz, DNP, RN. Vice President and Chief Nurse Executive of UC Health (Cincinnati): In the next five years, as we continue to encounter a national nursing shortage, I expect to see additional innovative strategies to complement the care provided at the bedside.

One of these strategies will be some type of robot-assisted care. From delivery of medications to answering call lights — and completing simple tasks like needing a blanket or requesting that the heat be adjusted — we will see more electronic solutions. These solutions will allow for a better patient experience and help to exceed the expectations of our patients as customers.

Of course, nothing can take the place of skilled and compassionate bedside care, but many tasks could be automated — and will be — to supplement the professional nursing shortage.

Natalia Cineas, DNP, RN. Senior Vice President and Chief Nurse Executive of NYC Health + Hospitals (New York City): Nurses will continue to play a vital role in addressing the health inequities and social determinants of health among vulnerable populations as the nursing workforce itself becomes more diverse and inclusive. As the largest segment of the healthcare workforce — with some 4 million nurses active in the U.S. — nurses represent the faces of the communities in which they serve. As America becomes a more diverse and inclusive society, so too will the nursing profession become more diverse and inclusive. Currently, industry estimates indicate that between one quarter to one-third of all U.S. nurses identify as a member of a minority group, with between 19 percent and 24 percent of U.S. nurses identifying themselves as Black/African-American; 5 percent to 9 percent identifying themselves as Hispanic; and about 3 percent identifying themselves as Asian. The percentage of minority nurses has been rising steadily for the past two decades and is expected to continue to climb in the coming years.

Blacks and underserved minority populations face numerous genetic, environmental, cultural and socioeconomic factors that account for health disparities, and the impact is particularly visible in the areas of cardiovascular disease, diabetes, pregnancy and childbirth mortality, and cancer outcomes, as well as the enormous toll of the current novel coronavirus global pandemic, where communities of color have been among the hardest hit populations.

In New York City alone, statistics compiled by the city’s health department show Blacks and Hispanics together account for 65 percent of all COVID-19 cases; represented 70 percent of all hospitalizations due to COVID-19; and, sadly, 68 percent of all deaths caused by COVID-19. As demonstrated during this pandemic, in the future, technology such as telehealth and virtual patient monitoring will play a major role in the care of patients. There will be a vast need to address social determinants of health by educating and providing resources to allow utilization of this technology such as using “wearable tech” to monitor ongoing health issues, such as high blood pressure, diabetes, heart conditions and other chronic illnesses.

Ryannon Frederick, MSN, RN. Chief Nursing Officer of Mayo Clinic (Rochester, Minn.):Nursing research will experience extraordinary demand and growth driven by a realization that both complex and unmet patient needs can often be best served by the role of a professional registered nurse. Nurses are uniquely positioned to implement symptom and self-management interventions for patients and their caregivers. Significant disruption in healthcare, including increasing use of technology, will lead to a dramatic shift to understand the role of the RN in improving patient outcomes and implementing interventions using novel approaches. Nursing researchers will provide a scientific body of evidence proving equivalent, if not better, patient care outcomes that can be obtained at a lower cost than traditional models, leading to an even greater demand for the role of the professional nurse in patient care.

Karen Higdon, DNP, RN, Vice President and Chief Nursing Officer of Baptist Health Louisville (Ky.):The value of nursing has never been more apparent. Nurses have led the front line during this pandemic. In the next five years, we must be flexible and creative in establishing new models of care, specifically around roles that support nursing, such as assistant and tech roles. Creating roles with clear role definition, that are attractive and meaningful for nursing support will help build consistent, high-quality models for nursing to lead. This consistency, along with IT capabilities that enhance workflow, will better allow nurses to work at the top of their scope.

Karen Hill, DNP, RN. COO and Chief Nursing Officer of Baptist Health Lexington (Ky.): 2020 was declared the “Year of the Nurse” and this reality has never been more true than realizing the personal and professional sacrifices of nurses in dealing with issues surrounding the pandemic. The next five years will require nursing professionals to be flexible to address new, unknown emerging issues in all settings, to be open to new opportunities for leadership in hospitals, schools and communities and to use technology and telehealth to provide safer care to patients. Nurses need to evaluate our practices and traditions that are value-added and leave behind the task orientation of the past. We need to honor our legacy and create our path.

Therese Hudson-Jinks, MSN, RN. Chief Nursing Officer and Chief Patient Experience Officer at Tufts Medical Center and Tufts Children’s Hospital (Boston):Over the next five years, I expect that the support and retention of clinical nurses will become the top priority of every CNO and executive team, given nurses’ direct impact on supporting the business of healthcare. This will be particularly critical because there will be a concerning shortage of experienced clinical nurses as a result of advancing technologies increasing complexity in care, additional nurse roles created outside traditional areas, fierce competition for talent between large healthcare systems, aging baby boom workforce retiring at higher rates year over year, and a lack of sufficient numbers of PhD-prepared nurses working in academia and supporting higher enrollments.

I also believe that CNOs will be laser-focused on creating the practice environment that enhances retention of top, talented clinical nurses, and we will put a greater emphasis on the influence of effective nursing leadership in reaching that goal. In addition, I fully expect that nurses will be seen more as individuals with talents and experience than ever before — not just a number on a team, but rather a professional with specific, unique, talents that are highly sought after in competitive markets.

Finally, I anticipate that nursing innovation will blossom, given the exposure of the “innovation/solutionist superpower” within nurses during the pandemic. Philanthropy will grow exponentially in support of nursing innovation as a result.

Carol Koeppel-Olsen, MSN, RN. Vice President of Patient Care Services at Abbott Northwestern Hospital (Minneapolis): During the COVID-19 pandemic nurses have been working in difficult physical and emotional conditions, which may lead to significant turnover after the pandemic resolves. Nurses have a commitment to serving others and will persevere until the crisis is past; however, when conditions improve, many nurses may decide to pursue careers outside acute care settings. A possible turnover, coupled with a service economy that has been devastated, may result in large numbers of former service workers seeking stable jobs in nursing. Hospitals will have to be nimble and creative to onboard an influx of new nurses that are not only new to the profession but new to healthcare. Tactics to onboard these new nurses may include the use of retired RNs as mentors, instructor-model clinical groups in the work setting, job shadowing and aptitude testing to determine the best clinical fit.

Jacalyn Liebowitz, DNP, RN. Senior Vice President and System Chief Nurse Officer of Adventist Health (Roseville, Calif.): Over the next five years, I see nurses providing more hospital-based care in the home using remote technology. Based on that shift, we will see lower-acuity patients move into home-based care, and higher-acuity care in hospitals will increase. With that, hospital beds will be used at a different level. My bold prediction is that we will not need as many beds, but we will need higher acute care in the hospitals.

Nurses will learn differently. As we are seeing now, nurses have not been able to train in the traditional way. They are already using more remote technology to educate, onboard and orient to their roles. It looks and feels vastly different, and nurses need to be comfortable with that.

As for patient care, I think data that can be gleaned from wearable biometrics, and the use of artificial intelligence will help predict patient care on a patient-by-patient basis. Nurses will work with AI as part of their thought process, instead of completely focusing on their own judgment and assessment.

I also believe we are going to face a nursing shortage post-COVID for a few reasons. Due to the emotional and physical toll of responding to a pandemic, some nurses will decide to retire, and another group will leave based on the risks that go hand-in-hand with the profession.

As for patient care, we are going to collaborate differently. There will be more video conferencing regarding collaboration around the patient. And I think in the future we will see that the full continuum of care will include a wellness plan.

Debi Pasley, MSN, RN. Senior Vice President Chief Nursing Officer of Christus Health (Irving, Texas):I believe the demand for nurses will become increasingly visible and newsworthy throughout the pandemic. This could drive increases in salaries and numbers of qualified candidates seeking nursing as a profession in the medium and long term. The shortage will, however, continue to be a factor, leading to more remote work options to both supplement nursing at the bedside and substitute for in-person care.

Denise Ray, RN.Chief Nursing Executive of Piedmont Healthcare (Atlanta): Nursing schools will need to focus on emergency management and critical care training utilizing a team nursing model. While nursing has become very specialty-driven, the pandemic has demonstrated gaps in our ability to adapt as quickly utilizing a team model where nurses lead and direct care teams. By implementing a team model and enhancing education in the areas of emergency management and critical care, nursing can adapt quickly to the ever-changing environment.

Also, communication with patients and families will take on different dimensions with wider use of tele-therapeutic communication. Nurses will be leaders and liaisons in the process, connecting physicians, patients and patient families virtually.Nurses will play a key role in integrating patient family members as true patient care partners— making sure they have the information they need to serve an active caregiving role for their family members during and after hospitalization. We’ll also see more nurses becoming advanced nurse practitioners, playing an expanded role in all healthcare settings.

A quick stop at the local Whole Foods Market recently yielded surprising insights into the dilemma faced by physician practices in the COVID-era telemedicine boom.

The store location opened just last year, part of a brand-new residential and shopping complex designed for busy professionals. It’s larger than the old-style, pre-Amazon era stores, and was designed to integrate Amazon’s online grocery operations into the bricks-and-mortar retail setting. There’s a portion of the store set aside for Amazon “shoppers” to receive and pack online orders for pickup and delivery, along with an expanded array of convenience-food offerings for the app-powered consumer to scan and purchase.

But when COVID hit, the volume of online orders went through the roof, and the store hired a small army of Amazon shoppers (including one of our own adult children who’s on a “gap year”) to keep up with demand. The result has been barely controlled chaos—easily 70 percent of the shoppers in the aisles last weekend were young Amazon employees “shopping” on behalf of online customers. They’re all held to an Amazon-level productivity standard, which makes the pace of their cart-pushing somewhat frantic and erratic. And the discreet area at the front of the store for managing the Amazon orders has become a noisy hub, making entering and exiting the store problematic. Even the “regular” store employees at Whole Foods have begun to complain about the disruption caused by the Amazon fulfillment operation.

It’s acautionary tale for traditional physician practices and other care delivery organizations looking to “integrate” telemedicine into normal operations. Integration sounds great in theory, but in practice raises important questions:

1)What physical space should be set aside for delivering virtual care?

2)Should telemedicine work be done in a separate, centralized location, or in existing clinic space?

3) How does the staffing of clinics need to change to meet the demand for virtual care?

4) How can we flex staffing up and down based on demand for telemedicine?

5)If new staff are required, how will they be incorporated into the existing team—or should they be managed separately?

6)What operational metrics will they be held accountable for, and what impact will those metrics have on other operational goals?

If Amazon, a worldwide leader online, renowned for running tight, precision, productivity-driven operations, is having trouble figuring out physical-virtual integration at the front end of their business, imagine how difficult these challenges will be for healthcare providers. The sooner we start to dig into these issues and find sustainable solutions, the better.