The beleaguered digital health company announced on Monday that its previously proposed arrangement to go private via a deal with Swiss-based neurotechnology company MindMaze will not happen, offering no further details. That deal was arranged by AlbaCore Capital Group, which had secured a loan for Babylon in May to implement the transaction.

Babylon said that it will now exit its core US businesses, which consist mostly of value-based agreements with health plans, and will continue to seek a buyer for its Meritage Medical Network, a California-based independent practice association (IPA) comprised of approximately 1,800 physicians.

Babylon said it may have to file for bankruptcy if it can’t secure additional funding or reach another deal to divest.

The Gist:Babylon isone of the starkest digital health “boom-and-bust” stories thus far. Despite the fact that the company overpromised and under-delivered in both the US and abroad, it was able to raise—and then lose—billions of dollars in just a few short years after going public in October 2021 via a special purpose acquisition corporation (SPAC) merger. It remains to be seen who will buy Babylon’s attractive IPA asset. Presumablyinsurers, retailers, health systems and other players are evaluating a purchase, either to enter or expand their provider footprint into Northern and Central California.

Value-based healthcare, the holy grail of American medicine, has three parts: excellent clinical quality, convenient access and affordability for all.

And as with the holy grail of medieval legend, the quest for value-based care has been filled with failure.

In the 20th century, U.S. medical groups and hospital systems could—at best—achieve two elements of value-based care, but always at the sacrifice of the third. Until recently, American medicine lacked the clinical knowhow, technology and operational excellence to accomplish all three, simultaneously. We now have the tools. The only thing missing is “system-ness.”

What Is System-ness?

System-ness is the effective and efficient coordination of healthcare’s many parts: outpatient and inpatient, primary and specialty care, financing and care delivery, prevention and treatment.

By bringing these disparate pieces together within a well-functioning system, healthcare providers have the opportunity to maximize clinical outcomes, weed out waste, lower overall costs and provide greater levels of convenience and access.

Who Are The Search Parties?

In the future, system-ness will be the variable that determines whether healthcare transformation is led by (a) incumbent health systems like Kaiser Permanente and Geisinger Health or (b) the retail giants like Amazon, CVS and Walmart. The latter group has become an ever-growing threat in the healthcare arms race, quickly amassing their own (though still modest) systems of care through billion-dollar acquisitions.

Although both the incumbents and new entrants will struggle to implement value-based care on a national scale, the victor stands to earn hundreds of billions of dollars in added revenue and tens of billions in profits.

To better understand the power of system-ness, and the challenges all organizations will face in providing it, here are three examples of value-based-care solutions implemented successfully by Kaiser Permanente.

1. Preventing Problems, Managing Disease

Research demonstrates that preventive medicine and early intervention reduce heart attacks, strokes and cancer. Yet our nation falls far short in these areas when compared to its global peers.

One example is hypertension, the leading cause of strokes and a major contributor to heart attacks. With help from doctors, nearly all patients can keep high blood pressure under control. Yet, nationally, hypertension is controlled only 60% of the time.

We see similarly poor rates of performance when it comes to prevention and screening for cancers of the colon, breast and lung.

Undoing these troubling trends requires system-ness. In Kaiser Permanente, 90% of patients had their blood pressure controlled and were screened for cancer. Getting there required a comprehensive electronic health record, a willingness for every doctor (regardless of specialty) to focus on prevention, leadership that communicated the value of prevention and a salary structure that rewarded group excellence.

2. Continuous Care, Without Interruption

Most doctors’ offices are open Monday to Friday during normal business hours—only one-fourth of the time that a medical problem might occur.

At night and on weekends, patients have no choice but to visit ERs. There, they often wait hours for care, surrounded by people with communicable diseases. Their non-emergent problems generate bills 12-times higher than if they’d waited to be seen in a doctor’s office.

There’s a better way. In large-enough medical groups, hundreds of clinicians can provide round-the-clock care on a rotating, virtual basis—using video to assess patients and make evidence-based recommendations.

This approach, pioneered by physicians in the Mid-Atlantic Permanente Medical group, solved the patient’s problem immediately 70% of the time without a trip to the ER and, for the other 30%, enabled coordination of medical care with the ER staff.

3. Specialized Medicine, Immediate Attention

When a primary care physician needs added expertise (from a dermatologist, urologist or orthopedist), it’s usually the responsibility of the patient to make their own specialty appointments, check with insurance for coverage and provide their medical records.

This takes hours or days to coordinate and can delay care by weeks, resulting in avoidable complications.

But in a well-structured system, there’s no need to wait. Using telehealth tools at Kaiser Permanente, primary care doctors can connect instantly with dozens of different specialists—often while the patient is still in the exam room. Once connected, the specialist evaluates the patient and provides immediate expertise.

This way, care is not only faster and less expensive, but also better coordinated. Data from within Kaiser Permanente show that these virtual consultations resolve the patient’s problem 40% of the time without having to schedule another appointment. For the other 60%, the diagnostic process can begin immediately.

The Foundations For System-ness

Few organizations in the U.S. can or do offer these system-based improvements. Doing so requires skilled physician leadership, a shift in the financial model and a willingness to accept risk.

In fact, most organizations across the U.S. that claim to operate “value-based” systems actually rely on doctors who are scattered across the community, disconnected from each other and paid on the basis of volume (fee-for-service) rather than value (capitation).

As a result, patient care is fragmented and uncoordinated, leading to repeated tests and ineffective treatments, thus increasing medical costs and compromising medical outcomes.

Value-based care (superior quality, access and affordability) requires teams of clinicians working together as one—all paid on a capitated basis.

Without capitation, dermatologists will insist on seeing every patient in their office where they can bill insurance five-times more than with a tele-dermatology visit. And gastroenterology specialists will insist that all patients have colonoscopy rather than recommending low-risk patients do a safe, convenient, at-home colon cancer screening (called a fecal immunochemical test or “FIT”) at 5% of the cost.

In these cases, individual doctors don’t consciously make care inconvenient for patients. Rather, it is the only choice they have when working in a fee-for-service payment model. Ultimately, system-ness is best achieved when health systems are integrated, prepaid, tech-enabled and physician-led.

Amazon, CVS, Walmart Know About Systems

These three companies are global leaders in “system-ness,” at least in retail. Combined, they have a market cap of $1.88 trillion, employ 3.4 million Americans and are looking to take a slice of U.S. healthcare’s $4.3 trillion annual expenditures.

Already, they manage complex order-entry and fulfillment systems. They use technology to streamline everything from customer service to supply-chain management. They are led through a clear and effective reporting structure.

In terms of competing for healthcare’s holy grail, these are huge competitive advantages compared to today’s uncoordinated, individualized, leaderless healthcare industry.

As retailers vie to bring their system knowhow to American medicine, they are acquiring the pieces needed to compete with the healthcare incumbents. They’ve spent tens of billions of dollars on medical groups that are committed to value-based care (One Medical, Oak Street Health, etc.). They’ve also spent massive sums on home-health companies (Signify) and on pharmacies (PillPak), along with expanding their in-store, at-home and online care options. Many of these care-delivery subsidiaries are focused on Medicare Advantage, the capitated half of Medicare where financial success is dependent on high quality medical care provided at lower cost.

What’s more, all these retailers have a national presence with brick-and mortar facilities in nearly every community in the country—a leg up on nearly every existing health system.

Who Will Win—And Why?

Trying to pick the victor in the battle to transform American medicine at this point is like selecting the winner of a heavy-weight championship boxing match after three evenly matched rounds. Intangibles like stamina, courage and willingness to absorb pain have yet to be tested.

In The Innovator’s Dilemma, the late Clayton Christensen examined historical battles between incumbent organizations and new entrants. After analyzing dozens of industries, he concluded new entrants routinely become the victors because the incumbents move too slowly and fail to embrace the need for major change.

And from that perspective, if I had to wager, I’d put my money on the retail giants.

But there’s an even more worrisome potential outcome: neither those inside nor outside of healthcare will make the necessary investments or accept the risk of leading systemic change. As a result, the movement toward value-based healthcare will stall and die.

In that context, purchasers of healthcare (businesses, the government and patients) will encounter a difficult reality: over the next eight years, medical costs will nearly double, creating an unaffordable and unsustainable scenario. As a result, our nation will likely experience reduced medical coverage, increased rationing, ever-longer delays for care and a growth in health disparities.

If that day arrives, our country will regret its inaction.

For decades, research studies and news stories have concluded the American system is ineffective,

too expensive and falling further behind its international peers in important measures of performance: life expectancy, chronic-disease management and incidence of medical error.

As patients and healthcare professionals search for viable alternatives to the status quo, a recent mega-merger is raising new questions about the future of medicine.

In April, Kaiser Permanente acquired Geisinger Health under the banner of newly formed Risant Health. With more than 185 years of combined care-delivery experience, Kaiser and Geisinger have long been held up as role models of the value-based care movement.

Eyeing the development, many speculated whether this deal will (a) ignite widespread healthcare transformation or (b) prove to be a desperate attempt at relevance (Kaiser) or survival (Geisinger).

Whether incumbents like Kaiser Permanente and Geisinger can lead a national healthcare transformation or are displaced by new entrants will depend largely on whether they can deliver value-based care on a national scale.

In Search Of Healthcare’s Holy Grail

Value-based care—the simultaneous provision of high quality, convenient and affordable medical care—has long been the aim of leading health systems like Kaiser, Geisinger, Mayo Clinic, Cleveland Clinic and dozens more.

But results to-date have often failed to match the vision.

The need for value-based care is urgent. That’s because U.S. health and economic problems are expected to get worse, not better, over the next decade. According to federal governmental actuaries, healthcare expenditures will rise from $4.2 trillion today to $7.2 trillion by 2031. At that time, these costs are predicted to consume an estimated 19.6% of the U.S. Gross Domestic Product.

Put simply: The U.S. will nearly double the cost of medical care without dramatically improving the health of the nation.

For decades, health policy experts have pointed out the inefficiencies in medical care delivery. Research has estimated that inappropriate tests and ineffective procedures account for more than 30% of all money spent on American medical care.

This combination of troubling economics and untapped opportunity explain why value-based care has become medicine’s holy grail. What’s uncertain is whether the transformation in healthcare delivery and financing will be led from inside or outside the healthcare system.

Where The Health-System Hopes Hang

For years, Kaiser Permanente has led the nation in clinical quality and patient outcomes based on independent, third-party research via the National Committee for Quality Assurance (NCQA) and Medicare Star ratings. Similarly, Geisinger was praised by President Obama for delivering high-quality care at a cost well below the national average.

And yet, these organizations, and many other highly regarded national and regional health systems, are extremely vulnerable to disruption, especially when their strategy and operational decisions fail to align.

Kaiser, for its part, has struggled with growth while Geisinger’s care-delivery strategy has proven unsuccessful in recent years. Failed expansion efforts forced KP to exit multiple U.S. markets, including New York, North Carolina, Kansas and Texas. More recently, several of its existing regions have failed to grow market share and weakened financially.

Meanwhile, Geisinger has fallen on hard times after decades of market domination. As Bob Herman reported in STAT News: “Failed acquisitions, antitrust scrutiny, leadership changes, growing competition from local players, and a pandemic that temporarily upended how patients got care have forced Geisinger to abandon its independence. The system is coming off a year in which it lost $240 million from its patient care and insurance operations.”

Putting the pieces together, I believe the Kaiser-Geisinger deal represents an industry undergoing massive change as health systems face intensifying pressure from insurers and a growing threat from retailers like Amazon, CVS and Walmart. This upcoming battle over the future of value-based care represents a classic conflict between incumbents and new entrants.

Can The World’s Largest Companies Disrupt U.S. Healthcare?

Retail giants, including Amazon, Walmart and CVS, are among the nation’s 10 largest companies based on annual revenue.

They have a broad geographic presence and strong relationships with almost all self-funded businesses. Nearly all have acquired the necessary healthcare pieces—including clinicians, home-health services, pharmacies, insurance arms and electronic medical record systems—to replace the current medical system.

And yet, while these companies expand into medical care and financing, their core businesses are struggling, resulting in announced store closures and layoffs. As newcomers to the healthcare market, they have been forced to pay premium dollars to acquire parts of the delivery system. All have a steep learning curve ahead of them.

The Challenge Of Healthcare Transformation

American medicine is a conglomerate of monopolies(insurers, hospitals, drug companies and private-equity-owned medical practices). Each works to maximize its own revenue and profit. All are unwilling to innovate in ways that benefit patients when doing so comes at the sacrifice of financial performance.

One problem stands at the center of America’s soaring healthcare costs: the way doctors, hospitals and drug companies are paid.

The dominant payment methodology in the United States, fee-for-service, rewards healthcare providers for charging higher prices and increasing the number (and complexity) of services offered—even when they provide no added value.

The message to doctors and hospitals is clear: The more you do, and the greater market control you have, the higher your income and profit. This is the antithesis of value-based care.

The alternative to fee-for-service payments, capitation, involves paying a single, up-front sum to the providers of care (doctors and hospitals) to cover the total annual cost for a population of patients. This model, unlike fee-for-service, rewards effectiveness and efficiency. Capitation creates incentives to prevent disease, reduce complications from chronic illness, and diminish the inefficiencies and redundancies present in care delivery. Capitated health systems that can prevent heart attacks, strokes and cancer better than others are more successful financially as a result.

However, it’s harder than it sounds to translate what’s best for patients into everyday decisions and actions. It’s one thing to accept a capitated payment with the intent to implement value-based care. It’s another to put in place the complex operational improvements needed for success. Here are the roadblocks that Kaiser-Geisinger will face, followed by those the retail giants will encounter.

3 Challenges For Kaiser-Geisinger:

Involving Clinical Experts. Kaiser Permanente is a two-part organization and when the insurance half (Kaiser) decided to acquire Geisinger, it did so without input or involvement from the half of the organization responsible for care-delivery (Permanente). This spells trouble for Geisinger, which must navigate a complex turnaround without the operational expertise or processes from Permanente that, in the past, helped Kaiser Permanente grow market share and lead the nation in clinical quality.

Going All In. To meet the healthcare needs of most its patients, Geisinger relies on community doctors who are paid on a fee-for-service basis. Generally, the fee-for-service model is predicated on the assumption that higher quality and greater convenience require higher prices and increased costs. With Geisinger’s distributed model, it’ll be very difficult to deliver consistent, value-based care.

Inspired Leadership. Major improvements in care delivery require skilled leadership with the authority to drive clinical change. In Kaiser Permanente, that comes through the medical group and its physician CEO. In Geisinger’s hybrid model, independent doctors have no direct oversight or central accountability structure. Although Risant Health could be an engine for value-based medical care, it’s more likely to serve the role of a “holding company,” capable of recommending operational improvements but incapable of driving meaningful change.

3 Challenges For The Retail Giants:

More Medical Offerings. Amazon, Walmart and CVS are successfully acquiring primary care (and associated telehealth) services. But competing with leading health systems will require a more wholistic, system-based approach to keep medical care affordable. This won’t be easy. To avoid ineffective, expensive specialty and hospital services, they will need to hire their own specialists to consult with their primary care doctors. And they will have to establish centers of excellence to provide heart surgery, cancer treatment, orthopedic care and more with industry-leading outcomes. But to meet the day-to-day and emergent needs of patients, they also will have to establish contracts with specialists and hospitals in every community they serve.

Capitalizing On Capitation. Already, the retail giants have acquired organizations well-versed in delivering patient care through Medicare Advantage, a capitated alternative to traditional (fee-for-service) Medicare plans. It’s a good start. But the retailers must do more than dip a toe in value-based care models. They must find ways to gain sufficient experience with capitation and translate that success into value-based contracts with self-funded businesses, which insure tens of millions of patients.

Defining Leadership. Without an effective and proven clinical leadership structure, the retail giants will be no more effective than their mainstream competitors when it comes to implementing improvements and shifting the culture of medicine to one that is customer- and service-focused.

Be they incumbents or new entrants, every contender will hit a wall if they cling to today’s failing care delivery model. The secret ingredient, which most lack and all will need to embrace in the future, is system-ness.

For all of the hype surrounding value-based care, fragmentation and fee-for-service are far more common in American healthcare today than integration and capitation.

Part two of this article will focus on how these different organizations—one set inside and one set outside of medicine—can make the leap forward with system-ness. And, in the end, you’ll see who is most likely to emerge victorious.

Physician income has not kept pace with inflation and administrative costs prompting 70% to leave private practice. Half are now employed by hospitals and another 20% by private equity-backed practice managers. Both trends began before the pandemic in response to tougher financial conditions for physicians across all specialties. While hospitals held their own at the sector level, physicians lost ground. Per CMS’ NHE analysis, from 2000 to 2021:

Spending in hospitals increased from 30.4% of total spending to 31.4%

Spending for prescription drugs was essentially unchanged from 8.95% to8.88%

Public health spending. increased slightly from 3.2% of total spending to 4.4%.

But spending for physician services shrank from 21.1% to 15.6%.

In tandem with the erosion of finances for medical practices, investments in medical practices by private equity grew. Per Pitchbook, there have been 874 practice acquisitions by PE/Venture backed sponsors in the last 12 years with 20 in the first half of this year alone. Most of these are small ($7.53 million/transaction) and most involve a tuck-in to an existing PE backed platform (i.e., Privia, Sheridan, et al). Rightfully, physicians point out that while hospitals and drug companies have protected their piece of the health care pie successfully for 20 years while physicians have lost ground.

Physicians are not happy and burnout is pervasive. The employment of physicians in hospital and private equity settings has not made life happier for physicians. Per Medscape’s most recent assessment, burnout increased to 53% in 2022–up from 47% in 2021 and 26% since 2018. More than one in five physicians (22%) reported experiencing depression—up from 15% since 2018. They’re anxious about the future and increasingly sensitive to compensation comparisons with professions that require less training and earn more. They’re suspicious of consultants, lawyers and bankers whose experience is limited but fees inexplicably high They’re incensed by executive compensation in hospitals, drug companies, and health insurer settings they deem overpaid and overhyped. And they resent execs in for-profit and private equity companies who achieve astronomical wealth via their stock-option packages earned on the backs of the physicians they control.

The realities are these:

Physicians lack a strong voice. The American Medical Association’s membership includes less than a third of active-practice physicians. It is increasingly under-fire for under-representing primary and preventive health providers in its government-authorized monopoly on coding, its lobbying efforts against scope of practice expansion for APNs and pharmacists, its opposition to medical training innovations that could significantly improve the readiness and effectiveness of the physician workforce and more. The AMA’s influence is strong on a shrinking number of issues and increasingly resonate out of touch on issues that resonate with voters and lawmakers (expanded scope of practice for nurses and pharmacists, price and outcome transparency, et al).

Physicians operate in a buyers’ market but behave like it’s a sellers’ market. Physicians are trained to think of themselves as the hub of a system in which what they say determines what everyone else does…including patients. They are conditioned in medical school, residency and practice to be self-centered and resist efforts via data, clinical practice redesign or even “value-based incentives” to change their behaviors. They despise the notions of price transparency, cost effectiveness and outcome-based comparisons to their peers while calling for more accountability from hospitals, insurers and drug companies. They discount notions of consumerism and self-care and believe report cards over-rate patient experiences since medical practice is uniquely complicated.

Most live in a buyers’ market mentality unwilling/unable to see the sellers’ market healthcare has become. Otherwise, price transparency would be prevalent, operating hours and support services more conducive to the needs of patients and digital investments to maintain connectivity significant…but most don’t.

My take:

The U.S. economy will be testy for the 12 months: bringing down inflation will require interest rate hikes. Unemployment will increase slightly, wage inflation will slow, and the 2024 election cycle will draw unwelcome attention to healthcare spending and its affordability as root causes of growing financial insecurity in American households.

Given this backdrop, the profession of medicine faces a tipping point: become an integral part of the system’s solution or a vestige of its past. That solution should address medicine’s role in…

Addressing affordability for households and patients and the direct role it plays.

Integrating generative AI into more accurate diagnostics and more accessible, efficient treatment methods.

Embracing transparency about medical services pricing, costs, outcomes, business relationships and conflicts of interest.

Creating care plans around individualized social determinants of health and distinctions in populations.

Streamlining medical training toward competency-based lifelong learning, data-driven technology support, a team-based delivery and ‘whole person’ orientation to individuals.

Accepting full accountability for their effectiveness in reducing unnecessary costs and spending, increasing equitable access and engaging consumers in self-care.

How value-based and alternative payment models figure into this is anyone’s guess. Some physician organizations (AAPG, NAACO, et al) are all-in for expansion of these while others note their lackluster results to date. And physician calls for a replacement to RVU-based conversion-factor will grow louder as Congress revisits MACRA and how Medicare pays physicians.

These are important and require urgent attention, but they do not elevate the profession to its rightful place at the center of system transformation.

I hold the profession of medicine in high regard. I respect and trust my physicians—Ben, Ben and Blake are trusted friends in my personal journey to health. But their profession as a whole appears stuck in the past and unable to play a central role in the health system transformation. Until and unless new physician leaders with fresh thinking about the entire system step up, the profession’s role will continue to erode.

Playing the victim card and blame game against Medicare, hospitals, insurers, drug companies and everyone else they deem unworthy will not solve the health system’s problems.

I believe conditions are right for physicians to seize the moral high ground and lead the needed reset of the health system but most aren’t ready.

Two important reports released last Wednesday point to a disconnect in how policymakers are managing the U.S. economy and how the health economy fits.

Report One: The Federal Reserve Open Market Meeting

At its meeting last week, the Governors of the Federal Open Market Committee (FOMC) voted unanimously to keep the target range for the federal funds rate at 5% to 5.25%–the first time since last March that the Fed has concluded a policy meeting without raising interest rates.

In its statement by Chairman Powell, the central bank left open the possibility of additional rate hikes this year which means interest rates could hit 5.6% before trending slightly lower in 2024.

In conjunction with the (FOMC) meeting, meeting participants submitted projections of the most likely outcomes for each year from 2023 to 2025 and over the longer run:

Median

2023

2024

2025

Longer Run

Longer Run Range

% Change in GDP

1.1

1.1

1.8

1.8

1.6-2.5

Unemployment rate &

4.1

4.5

4.5

4.0

3.6-4.4

PCE Inflation rate

3.2

2.5

2.1

2.0

2.0

Core PCE Inflation

3.9

2.6

2.2

*

*

*Longer-run projections for core PCE inflation are not collected.

Notes re: the Fed’s projections based on these indicators:

The GDP (a measure of economic growth) is expected to increase 1% more this year than anticipated in its March 2023 analysis while estimates for 2024 were lowered just slightly by 0.1%. Economic growth will continue but at a slower pace.

The unemployment rate is expected to increase to 4.1% by the end of 2023, a smaller rise in joblessness than the previous estimate of 4.5%. (As of May, the unemployment rate was 3.7%). Unemployment is returning to normalcy impacting the labor supply and wages.

inflation: as measured by the Personal Consumption Expenditures index, will be 3.2% at the end of 2023 vs. 3.3% they previously projected. By the end of 2024, it expects inflation will be 2.5% reaching 2.1% at the end of 2025. Its 2.0% target is within reach on or after 2025 barring unforeseen circumstances.

Core inflation projections, which excludes energy and food prices, increased: the Fed now anticipates 3.9% by the end of 2023–0.3% above the March estimate. Price concerns will continue among consumers.

Based on these projections, two conclusions about nation’s monetary policy may be deduced the Fed’s report and discussion:

The Fed is cautiously optimistic about the U.S. economy in for the near term (through 2025) while acknowledging uncertainty exists.

Interest rates will continue to increase but at a slower rate than 2022 making borrowing and operating costs higher and creditworthiness might also be under more pressure.

Report Two: CMS

On the same day as the Fed meeting, the actuaries at the Centers for Medicare and Medicaid Services (CMS) released their projections for overall U.S. national healthcare spending for the next several years:

“CMS projects that over 2022-2031, average annual growth in NHE (5.4%) will outpace average annual growth in gross domestic product (GDP) (4.6%), resulting in an increase in the health spending share of GDP from 18.3% in 2021 to 19.6% in 2031. The insured percentage of the population is projected to have reached a historic high of 92.3% in 2022 (due to high Medicaid enrollment and gains in Marketplace coverage). It is expected to remain at that rate through 2023. Given the expiration of the Medicaid continuous enrollment condition on March 31, 2023 and the resumption of Medicaid redeterminations, Medicaid enrollment is projected to fall over 2023-2025, most notably in 2024, with an expected net loss in enrollment of 8 million beneficiaries. If current law provisions in the Affordable Care Act are allowed to expire at the end of 2025, the insured share of the population is projected to be 91.2%. In 2031, the insured share of the population is projected to be 90.5%, similar to pre-pandemic levels.”

The report includes CMS’ assumptions for 4 major payer categories:

Medicare Part D: Several provisions from the Inflation Reduction Act (IRA) are expected to result in out-of-pocket savings for individuals enrolled in Medicare Part D. These provisions have notable effects on the growth rates for total out-of-pocket spending for prescription drugs, which are projected to decline by 5.9% in 2024, 4.2% in 2025, and 0.2% in 2026.

Medicare: Average annual expenditure growth of 7.5% is projected for Medicare over 2022-2031. In 2022, the combination of fee-for-service beneficiaries utilizing emergent hospital care at lower rates and the reinstatement of payment rate cuts associated with the Medicare Sequester Relief Act of 2022 resulted in slower Medicare spending growth of 4.8% (down from 8.4% in 2021).

Medicaid: On average, over 2022-2031, Medicaid expenditures are projected to grow by 5.0%. With the end of the continuous enrollment condition in 2023, Medicaid enrollment is projected to decline over 2023-2025, with most of the net loss in enrollment (8 million) occurring in 2024 as states resume annual Medicaid redeterminations. Medicaid enrollment is expected to increase and average less than 1% through 2031, with average expenditure growth of 5.6% over 2025-2031.

Private Health Insurance: Over 2022-2031, private health insurance spending growth is projected to average 5.4%. Despite faster growth in private health insurance enrollment in 2022 (led by increases in Marketplace enrollment related to the American Rescue Plan Act’s subsidies), private health insurance expenditures are expected to have risen 3.0% (compared to 5.8% in 2021) due to lower utilization growth, especially for hospital services.

And for the 3 major recipient/payee categories:

Hospitals: Over 2022-2031, hospital spending growth is expected to average 5.8% annually. In 2023, faster growth in hospital utilization rates and accelerating growth in hospital prices (related to economy wide inflation and rising labor costs) are expected to lead to faster hospital spending growth of 9.3%. For 2025-2031, hospital spending trends are expected to normalize (with projected average annual growth of 6.1%) as there is a transition away from pandemic public health emergency funding impacts on spending.

Physicians and Clinical Services: Growth in physician and clinical services spending is projected to average 5.3% over 2022-2031. An expected deceleration in growth in 2022, to 2.4% from 5.6% in 2021, reflects slowing growth in the use of services following the pandemic-driven rebound in use in 2021. For 2025-2031, average spending growth for physician and clinical services is projected to be 5.7%, with an expectation that average Medicare spending growth (8.1%) for these services will exceed that of average Private Health Insurance growth (4.6%) partly as a result of comparatively faster growth in Medicare enrollment.

Prescription Drugs: Total expenditures for retail prescription drugs are projected to grow at an average annual rate of 4.6% over 2022-2031. For 2025-2031, total spending growth on prescription drugs is projected to average 4.8%, reflecting the net effects of key IRA provisions: Part D benefit enhancements (putting upward pressure on Medicare spending growth) and price negotiations/inflation rebates (putting downward pressure on Medicare and out-of-pocket spending growth).

Thus, CMS Actuaries believe spending for healthcare will be considerably higher than the growth of the overall economy (GDP) and inflation and become 19.6% of the total US economy in 2031. And it also projects that the economy will absorb annual spending increases for hospitals (5.8%) physician and clinical services (5.3%) and prescription drugs (4.6%).

My take:

Side-by-side, these reports present a curious projection for the U.S. economy through 2031: the overall economy will return to a slightly lower-level pre-pandemic normalcy and the healthcare industry will play a bigger role despite pushback from budget hawks preferring lower government spending and employers and consumers frustrated by high health prices today.

They also point to two obvious near-term problems:

1-The Federal Reserve pays inadequate attention to the healthcare economy. In Chairman Powell’s press conference following release of the FOMC report, there was no comment relating healthcare demand or spending to the broader economy nor a question from any of the 20 press corps relating healthcare to the overall economy. In his opening statement (below), Chairman Powell reiterated the Fed’s focus on prices and called out food, housing and transportation specifically but no mention of healthcare prices and costs which are equivalent or more stressful to household financial security:

“Good afternoon. My colleagues and I remain squarely focused on our dual mandate to promote maximum employment and stable prices for the American people…My colleagues and I are acutely aware that high inflation imposes hardship as it erodes purchasing power, especially for those least able to meet the higher costs of essentials like food, housing, and transportation. We are highly attentive to the risks that high inflation poses to both sides of our mandate, and we are strongly committed to returning inflation to our 2% objective.”

2-Congress is reticent to make substantive changes in Medicare and other healthcare programs despite its significance in the U.S. economy. It’s politically risky. In the June 2 Congressional standoff to lift the $31.4 debt ceiling, cuts to Medicare and Social Security were specifically EXCLUDED. Medicare is 12% of mandated spending in the 2022 federal budget and is expected to grow from a rate of 4.8% in 2022 to 8% in 2023—good news for investors in Medicare Advantage but concerning to consumers and employers facing higher prices as a result.

Even simplifying the Medicare program to replace its complicated Parts A, B, C, and D programs or addressing over-payments to Medicare Advantage plans (in 2022, $25 billion per MedPAC and $75 billion per USC) is politically tricky. It’s safer for elected officials to support price transparency (hospitals, drugs & insurers) and espouse replacing fee for service payments with “value” than step back and address the bigger issue: how should the health system be structured and financed to achieve lower costs and better health…not just for seniors or other groups but everyone.

These two realities contribute to the disconnect between the Fed and CMS. Looking back 20 years across 4 Presidencies, two economic downturns and the pandemic, it’s also clear the health economy’s emergence did not occur overnight as the Fed navigated its monetary policy. Consider:

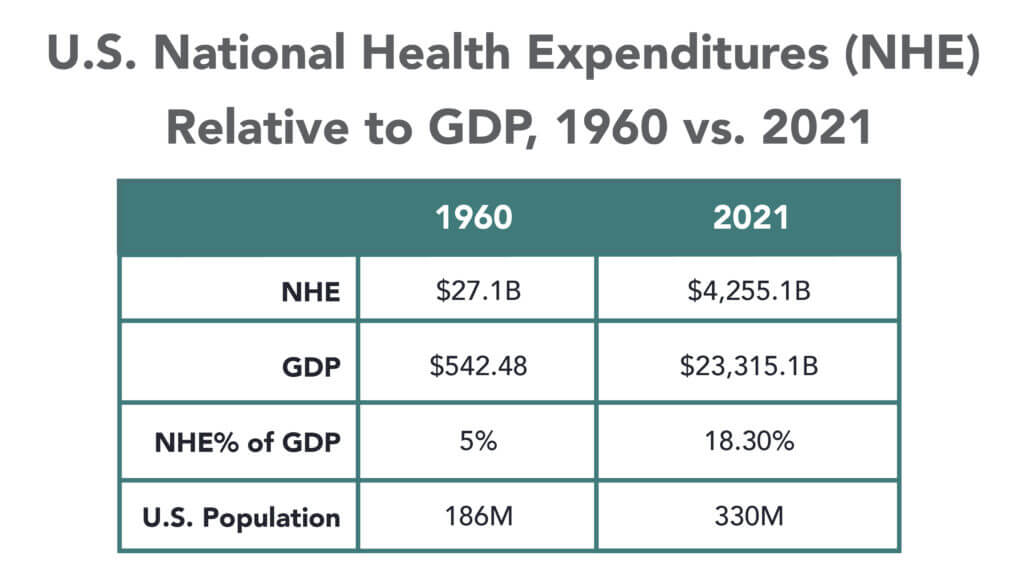

National health expenditures were $1.366 trillion (13.3% of GDP) in 2000 and $4.255 billion in 2021 (18.3% of the GDP). This represents 210% increase in nominal spending and a 37.5% increase in the relative percentage of the nation’s GDP devoted to healthcare. No other sector in the economy has increased as much.

In the same period, the population increased 17% from 282 million to 334 million while per capita healthcare spending increased 166% from $4,845 to $12,914. This disproportionate disconnect between population and health spending growth is attributed by economists to escalating unit costs increases for the pills, facilities, technologies and specialty-provider services we use—their underlying cost escalation notably higher than other industries.

There were notable changes in where dollars were spent: hospitals were unchanged (from $415 billion/30.4% of total spending to $1.323 trillion/31.4% of total spending), physician services shrank (from $288.2 billion/21.1% of total spending to 664.6 billion/15.6% pf total spending), prescription drugs were unchanged (from $122.3 billion/8.95% to $378 billion/8.88% of total spending) and public health increased slightly (from $43 billion/$3.2% of total spending to $187.6 billion/4.4% of total spending).

And striking differences in sources of funding: out of pocket spending shrank from $193.6/14.2% of payments to $433 billion/10.2% % of payments; private insurance shrank from $441 billion/32.3% of payments to $1.21 trillion/28.4% of total payments; Medicare grew from $224.8 billion/16.5% of payments to $900.8 billion/21.2% of payments; Medicaid + CHIP grew from $203.4 billion/14.9% to $756.2 billion/17.8% of payments; and Veterans Health grew from $19.1 billion/1.4% of payments to $106.0 billion/2.5% of payments.

Thus, if these trends continue…

Aggregate payments to providers from government programs will play a bigger role and payments from privately insured individuals and companies will play a lesser role.

Hospital price increases will exceed price increases for physician services and prescription drugs.

Spending for healthcare will (continue to) exceed overall economic growth requiring additional funding from taxpayers, employers and consumers AND/OR increased dependence on private investments that require shareholder return AND/OR a massive restructure of the entire system to address its structure and financing.

What’s clear from these reports is the enormity of the health economy today and tomorrow, the lack of adequate attention and Congressional Action to address its sustainability and the range of unintended, negative consequences on households and every other industry if left unattended. It’s illustrative of the disconnect between the Fed and CMS: one assumes it controls the money supply while delegating to the other spending and policies independent of broader societal issues and concerns.

The health economy needs fresh attention from inside and outside the industry. Its impact includes not only the wellbeing of its workforce and services provided its users. It includes its direct impact on household financial security, community health and the economic potential of other industries who get less because healthcare gets more.

Securing the long-term sustainability of the U.S. economy and its role in world affairs cannot be appropriately addressed unless its health economy is more directly integrated and scrutinized. That might be uncomfortable for insiders but necessary for the greater good. Recognition of the disconnect between the Fed and CMS is a start!

On October 1, 1908, Ford produced the first Model T automobile. More than 60 years later, this affordable, mass produced, gasoline-powered car was still the top-selling automobile of all time. The Model T was geared to the broadest possible market, produced with the most efficient methods, and used the most modern technology—core elements of Ford’s business strategy and corporate DNA.

On April 25, 2018, almost 100 years later, Ford announced that it would stop making all U.S. internal-combustion sedans except the Mustang.

The world had changed. The Taurus, Fusion, and Fiesta were hardly exciting the imaginations of car-buyers. Ford no longer produced its U.S. cars efficiently enough to return a suitable profit. And the internal combustion technology was far from modern, with electronic vehicles widely seen as the future of automobiles.

Ford’s core strategy, and many of its accompanying products, had aged out. But not all was doom and gloom; Ford was doing big and profitable business in its line of pickups, SUVs, and -utility vehicles, led by the popular F-150.

It’s hard to imagine the level of strategic soul-searching and cultural angst that went into making the decision to stop producing the cars that had been the basis of Ford’s history. Yet, change was necessary for survival. At the time, Ford’s then-CEO Jim Hackett said, “We’re going to feed the healthy parts of our business and deal decisively with the areas that destroy value.”

So Ford took several bold steps designed to update—and in many ways upend—its strategy. The company got rid of large chunks of the portfolio that would not be relevant going forward, particularly internal combustion sedans. Ford also reorganized the company into separate divisions for electric and internal combustion vehicles. And Ford pivoted to the future by electrifying its fleet.

Ford did not fully abandon its existing strategies. Rather, it took what was relevant and successful, and added that to the future-focused pivot, placing the F-150 as the lead vehicle in its new electric fleet.

This need for strategic change happens to all large organizations. All organizations, including America’s hospitals and health systems, need to confront the fact that no strategic plan lasts forever.

Over the past 25-30 years, America’s hospitals and health systems based their strategies on the provision of a high-quality clinical care, largely in inpatient settings. Over time, physicians and clinics were brought into the fold to strengthen referral channels, but the strategic focus remained on driving volume to higher-acuity services.

More recently, the longstanding traditional patient-physician-referral relationship began to change. A smarter, internet-savvy, and self-interested patient population was looking for different aspects of service in different situations. In some cases, patients’ priority was convenience. In other cases, their priority was affordability. In other cases, patients began going to great lengths to find the best doctors for high-end care regardless of geographic location. In other cases, patients wanted care as close as their phone.

Around the country, hospitals and health systems have seen these environmental changes and adjusted their strategies, but for the most part only incrementally. The strategic focus remains centered on clinical quality delivered on campus, while convenience, access, value, affordability, efficiency, and many virtual innovations remain on the strategic periphery.

Health system leaders need to ask themselves whether their long-time, traditional strategy is beginning to age out. And if so, what is the “Ford strategy” for America’s health systems?

The questions asked and answered by Ford in the past five years are highly relevant to health system strategic planning at a time of changing demand, economic and clinical uncertainty, and rapid innovation. For example, as you view your organization in its entirety, what must be preserved from the existing structure and operations, and what operations, costs, and strategies must leave? And which competencies and capabilities must be woven into a going-forward structure?

America’s hospitals and health systems have an extremely long history—in some cases, longer than Ford’s. With that history comes a natural tendency to stick with deeply entrenched strategies. Now is the time for health systems to ask themselves, what is our Ford F150? And how do we “electrify” our strategic plan going forward?

On Monday, Minnetonka, MN-based UHG’s Optum division made a $3.3B all-cash offer to acquire Baton Rouge, LA-based Amedisys, one of the country’s largest home health companies.

Optum’s bid came several weeks after Bannockburn, IL-based Option Care Health, a home health company specialized in drug and infusion services, offered to purchase Amedisys in an all-stock transaction valued at $3.6B. Amedisys itself acquired hospital-at-home company Contessa Health for $250M in 2021. While its Board of Directors is now evaluating whether UHG has made a “Superior Proposal”, a UHG acquisition of Amedisys would likely be subject to significant regulatory oversight, as the payer recently closed on its purchase of home health company and Amedisys-competitor LHC Group in a deal that was heavily scrutinized by the Federal Trade Commission.

The Gist: UHG, the nation’s largest health insurer, is on a tear to bring the country’s largest home health providers under its Optum umbrella—and it has the deep pockets to outbid nearly anyone else trying to do the same.

While some questioned the value of an Option Care-Amedisys combination, UHG would get to plug another asset into its scaled continuum of home-based care, allowing it to steer beneficiaries away from high-cost post acute care and continue to increase profitable intercompany eliminations.

If UHG’s bid for Amedisys is accepted, it would also gain its first hospital-at-home asset in Contessa, providing it with the opportunity to fully redirect—and reduce—its inpatient care spend.

At the end of a meeting last week with a health system executive team, the system’s COO asked us a question: “Your concept of a consumer-focused health system centered around treating patients as members describes exactly how we want to relate to our patients, but we’re not sure about the timing. Could you give us a list of the ‘no regrets’ investments you’d recommend for health systems looking to do this?”

We frequently get asked about “no regrets” strategies:

decisions or investments that will be accretive in both the current fee-for-service system as well as a future payment and operational model oriented around consumer value. The idea is understandably appealing for systems concerned about changing their delivery model too quickly in advance of payment change. And there is a long list of strategies that would make a system stronger in both fee-for-service and value: cost reduction, value-driven referral management, and online scheduling, just to name a few.

But as we pointed out, the decision to pursue only the no-regrets moves is a clear signal that the organization’s strategy is still tied to the current payment model.

If the system is truly ready to change, strategy development should start with identifying the most important investments for delivering consumer value. It’s fine to acknowledge that a health system is not yet ready, but we cautioned the team that they should not rely on the external market to provide signals for when they should undertake real change in strategy.

External signals—from payers, competitors, or disruptors—will come too slowly, or perhaps never. At some point, the health system should be prepared to lead innovation, introduce a new model of value to the market, and define and promote the incentives to support it.

Real change will require disruption of parts of the current business and cannot be accomplished with “no-regrets investments” alone.

Academic medicine combines healthcare with higher education, the two sectors of the American economy that have exhibited outsized cost growth during the past 50 years. The result is a stunning disconnection between the business practices of academic medical centers (AMCs) and the supply-demand dynamics reshaping healthcare delivery.

Market, technological and regulatory forces are pushing the healthcare industry to deliver higher-value care that generates better outcomes at lower costs. A parallel movement is shifting resources out of specialty and acute care services into primary, preventive, behavioral health and chronic disease care services. In the process, care delivery is decentralizing and becoming more consumer-centric.

AMCs Double Down

Counter to these trends, academic medicine is doubling down on high-cost, centralized, specialty-focused care delivery. Privilege has its price. Several AMCs — including Mass General Brigham, IU Health, UCSF, Ohio State and UPMC — are undertaking multibillion-dollar expansions of their existing campuses. Collectively, AMCs expect American society to fund their continued growth and profitability irrespective of cost, effectiveness and contribution to health status.

Despite being tax-exempt and having access to a large pool of free labor (residents), AMCs charge the highest treatment prices in most markets. [1] Archaic formulas allocate residency “slots” and lucrative Graduate Medical Education payments (over $20 billion annually) disproportionately into specialty care and more-established AMCs. Given their cushy funding arrangements, it’s no wonder AMCs fight vigorously to maintain an out-of-date status quo.

Legacy practices from the early 1900s still dominate medical education, medical research and clinical care. Like tenured faculty, academic physicians manage their practices with little interference. Clinical deans rule their departments with a free hand. With few exceptions, interdisciplinary coordination is an oxymoron. The result is fragmented care delivery that tolerates duplication, medical error and poor patient service.

Irresistible consumerism confronts immovable institutional inertia. As exhibited by substantial operating losses at many AMCs, their foundations are beginning to crack. [2]

Medicine’s Rise from Poverty to Prosperity

In his 1984 Pulitzer Prize-winning work, Paul Starr chronicles the social transformation of American medicine during the 19th and 20th centuries. Prior to the 1900s, doctors had low social status. Most care took place in the home. Pay was low. The profession lacked professional standards. There were too many quacks. Most doctors lived hand-to-mouth.

As the century turned, several cultural, economic, scientific and legal developments converged to elevate the profession’s status in American society. Stricter licensing reduced the supply of physicians and closed most existing medical schools. Legislation and legal rulings restricted corporate ownership of medical practices and enshrined physicians’ operating autonomy. Scientific breakthroughs gave medicine more healing power.

Through the decades that followed, the American Medical Association and state medical societies frustrated external attempts to control medical delivery externally and institute national health insurance. They insisted on fee-for-service payment and the absolute right of patients to choose their doctors. These are causal factors underlying healthcare’s skyrocketing cost increases, growing from 5% of the U.S. gross domestic product (GDP) in 1960 to over 18% in 2021.

Academic and community-based physicians have always had a tenuous relationship. Status and prestige accompany academic affiliations. Academic practices require referrals from community physicians but rarely consult with them on treatment protocols. For their part, community physicians marvel at the lack of market awareness exhibited by academic practices. They have tolerated one another to perpetuate collective physician control over healthcare operations.

Incomes and prestige for both community and academic physicians rose as the medical profession limited practitioner supply, established payment guidelines, encouraged specialization, controlled service delivery and socialized capital investment. One hundred years later, the business of healthcare still exhibits these characteristics. Gleaming new medical centers testify to the profession’s success in socializing capital investment and maintaining autonomy over hospital operations.

Entrenched beliefs and behaviors explain why most hospitals, despite their high construction costs, are largely deserted after 4 p.m. and on weekends. They explain the maldistribution of facilities and practitioners. They explain the overdevelopment of specialty care. They explain the underinvestment in preventive care, mental health services and public health.

Value-Focused Backlash Portends Reckoning

These beliefs and behaviors are contributing to AMC’s current economic dislocation. Dependent upon public subsidies and premium treatment payments to maintain financial sustainability, high-cost AMCs are particularly vulnerable to value-based competitors.

The marketplace is attacking inefficient clinical care with tech-savvy, consumer-friendly business models. Care delivery is decentralizing even as many AMCs invest more heavily in campus-based medicine. A market-based reckoning confronts academic medicine.

A visit up north illustrates the general unwillingness of academic physicians to accept market realities and their continued insistence on maintaining full control over the academic medical enterprise. It’s like watching a train wreck occur in slow motion.

Minnesota Madness

After experiencing severe economic distress, the University of Minnesota sold its University of Minnesota Medical Center (UMMC) to Fairview Health in 1997. Fairview currently operates UMMC in partnership with the University of Minnesota Physicians (UMP) under the banner of M Health Fairview.

In September 2022, Sanford Health and Fairview Health signed a letter of intent to merge. The new combined company would bear the Sanford name with its headquarters in Sioux Falls, South Dakota. Despite the opportunity to double its catchment area for specialty referrals, the University and UMP oppose the merger with Sanford. They fear out-of-state ownership could compromise the integrity of UMMC’s operations.

Fairview wants the Sanford merger to help it address massive operating losses resulting, in part, from its contractual arrangements with UMP. Negotiations between the parties have become acrimonious. Amid the turmoil, the University and UMP announced in January 2023 their intention to acquire UMMC from Fairview and build a new state-of-the-art medical center on the University’s Minneapolis campus.

The University has named this proposal “MPact Health Care Innovation.” It calls for the Minnesota state legislature to fund the multibillion-dollar cost of acquiring, building and operating the new medical enterprise. Typical of academic medical practices, UMP expects external sources to pony up the funding to support their high-cost centralized business model while they continue to call the shots.

The arrogance and obliviousness of the University’s proposal is staggering. Minnesota struggles with rising rates of chronic disease and inequitable healthcare access for low-income urban and rural communities. The idea that a massive governmental investment in academic medicine will “bridge the past and future for a healthier Minnesota” as the MPact tagline proclaims is ludicrous.

Out of Touch

Like the rest of the country, Minnesota is experiencing declining life expectancy. Despite spending more than double the average per-capita healthcare cost of other wealthy countries, the United States scores among the worst in health status measures. Spending more on high-end academic medicine won’t change these dismal health outcomes. Spending more on preventive care, health promotion and social determinants of health could.

The real gem in the University of Minnesota’s medical enterprise is its medical school. It has trained 70% of the state’s physicians. It ranks third and fourth nationally in primary care and family medicine. It is advancing a progressive approach to interdisciplinary and multi-professional care.

If the Minnesota state legislature really wants to advance health in Minnesota, it should expand funding for the University’s aligned health schools and community-based programs without funding the acquisition and expansion of the University’s clinical facilities.

No Privilege Without Performance

Our nation must stop enabling academic medicine’s excesses. Funding AMCs’ insatiable appetite for facilities and specialized care delivery is counterproductive. It is time for academic medicine to embrace preventive health, holistic care delivery and affordable care access.

Privilege comes with responsibility. AMCs that resist the pivot to value-based care and healthier communities deserve to lose market relevance.

America has the means to create a healthier society. It requires shifting resources out of healthcare into public health. We must have the will to make community-based health networks a reality. It starts by saying no to needless expansion of acute care facilities.

Healthcare’s most recent billion-dollar deal took the industry by surprise, leaving medical experts and hospital leaders grappling to comprehend its implications.

In case you missed it, California-based Kaiser Foundation Health Plan and Hospitals, which make up the insurance and facilities half of Kaiser Permanente, announced the acquisition of Geisinger, a Pennsylvania-based health system once acknowledged by President Obama for delivering “high-quality care.”

Upon regulatory approval, Geisinger will become the first organization to join Risant Health, Kaiser Foundation’s newly created $5 billion subsidiary. According to Kaiser, the aim is to build “a portfolio of likeminded, nonprofit, value-oriented, community-based health systems anchored in their respective communities.”

Having spent 18 years as CEO of The Permanente Medical Group, the half of Kaiser Permanente responsible for the delivery of medical care, I took great interest in the announcement. And I wasn’t alone. My phone rang off the hook for weeks with calls from reporters, policy experts and healthcare executives.

After hundreds of conversations, here are the three most common questions I received about the acquisition—and the implications for doctors, insurers, health-system competitors and patients all over the country.

Question 1: Why did Kaiser acquire Geisinger?

Most callers wanted to know about Kaiser’s motivation, figuring there must’ve been more to the acquisition than the press release indicated. Although I don’t have inside information, I believe they were right. Here’s why:

Kaiser Permanente has a long and ongoing reputation for delivering nation-leading care. The organization has consistently earned the highest quality and patient-satisfaction rankings from the National Committee for Quality Assurance (NCQA), Leapfrog Group, JD Power and Medicare.

And yet, despite a 78-year history, dozens of hospitals and 13 million members across eight states, Kaiser Permanente is still considered a coastal—not national—health system. It maintains a huge market share in California and a strong presence in the Mid-Atlantic states, yet the organization has failed repeatedly to replicate that success in other geographies.

With that context, I see two compelling reasons why the Kaiser Foundation Health Plan and Hospitals wish to become a national brand:

Influence. Elected officials and regulatory bodies often turn to healthcare’s biggest players to set legislative agendas and carve out national policy. At that table, there are a limited number of seats. By shedding its reputation as a “local” health system, Kaiser could earn one.

Survival. In recent years, companies like Amazon, CVS and Walmart have been scooping up organizations that provide primary care, telehealth, home health and specialty care services. These “retail giants” are spending up to $13 billion per acquisition. And they’re consuming already-successful healthcare companies like One Medical, Oak Street Health, Signify, Pill Pack and many others. Like an army preparing for war, these corporate behemoths are amassing the components needed to battle the traditional healthcare incumbents and ultimately oust them entirely.

The Geisinger deal expands Kaiser’s footprint, adding 600,000 patients, 10 hospitals and 100 specialty and primary care clinics. These assets lend gravitas, even though Geisinger also comes with a 2022 operating loss of $239 million.

The lesson to draw from this first question is clear: size matters. The days of solo physicians and stand-alone hospitals are over. Nostalgia for medicine’s folksy, home-spun past is understandable but futile. To survive, healthcare players must get bigger quickly or team up with someone who can. That insight leads to the next question and lesson.

Question 2: How much value will Kaiser give Geisinger?

Almost everyone I’ve spoken with understands Kaiser’s desire for greater national influence, but they’re less sure how this deal will affect Geisinger Health.

Geisinger’s Pennsylvania-based hospitals and clinics have been locked in territorial battles for years with surrounding health systems. More recently, the pandemic, combined with staffing shortages and national inflation, have challenged Geisinger’s clinical performance and eroded its bottom line.

Assuming Kaiser plans to invest roughly $1 billion in each of the four to five health systems it’s planning to acquire, that surge in cash inflow will provide Geisinger with temporary financial safety. But the bigger question is how will Kaiser improve Geisinger’s value-proposition enough to grow its market share?

In public comments, Kaiser leaders spoke of the acquisition as an opportunity for Risant to “improve the health of millions of people by increasing access to value-based care and coverage, and raising the bar for value-based approaches that prioritize patient quality outcomes.”

Many of the experts I spoke with understand Kaiser’s value intent. But they question how Kaiser can could deliver on that promise since The Permanente Medical Group (TPMG) wasn’t involved in the deal.

If, hypothetically, Kaiser and Permanente leaders were to strike a deal to collaborate in the future, TPMG’s physician leaders could bring tremendous knowledge, experience and expertise to the table. Otherwise, I agree with those who’ve expressed doubt that Kaiser, alone, will be able to significantly improve Geisinger’s clinical performance.

Health plans and insurance companies play an important role in financing medical care. They possess rich data on performance and can offer incentives that boost access to higher-quality care. But insurers don’t work directly with individual doctors to coordinate medical care or advance clinical solutions on behalf of patients. And without strong physician leadership, the pace of positive change slows to a crawl. As a example, research conducted within The Permanente Medical Group found that it takes only three years to turn a proven clinical advance into standard practice—that’s nearly six times faster than the national average.

For decades, the secret sauce for Kaiser Permanente has been the cohesive success of its three parts: Kaiser Health Plan, Kaiser Foundation Hospitals and The Permanente Medical Group.

And KP’s results speak for themselves:

90% control of hypertension for members (compared to 60% for the rest of the country)

30% fewer deaths from heart attack and stroke (compared to the rest of the country)

20% fewer deaths from colon cancer

The big lesson: insurance, by itself, doesn’t drive major improvements in medicine. It must be a combined effort between forward-looking insurers and innovative, high-performing clinicians.

But there’s another takeaway here for doctors everywhere: now is the time to join forces with other clinicians in your community. Together, you can collaborate to improve clinical quality. You can augment access and make care more affordable for patients. Simultaneously, this is the time for the insurers and the retail giants to figure out which medical groups can deliver the best care and make the best partners. Neither side will flourish alone. And this leads to a third question and lesson.

Question 3: Will the deal work?

Almost all of my conversations ended with this query. I say it’s too early to tell. But as I look years down the road, one part of the deal, in particular, gives me doubt.

Today, Geisinger uses a hybrid reimbursement model—blending both “value-based” care payments with traditional “fee-for-service” insurance plans. In addition to offering its own coverage, it contracts with a variety of other insurance companies. Rarely have I seen this scattered approach succeed.

Most healthcare observers understand the inherent flaw in the “fee for service” (FFS) model is also its greatest appeal to providers: the more you do the more you earn. FFS is how nearly all financial transactions take place in America (i.e., provide a service, earn a fee). In medicine, however, this financial model results in frequent over-testing and over-treatment with minimal if any improvement in clinical outcomes, according to researchers.

The “value-based” alternative to FFS involves prepaying for care—a model often referred to as “capitation.” In short, capitation involves a single fee, paid upfront for all the medical care provided to a defined population of patients for one year based on their age and health status. The better an organization at preventing disease and avoiding complications from chronic illness, the greater its success in both clinical quality and affordability.

Within the small world of capitated healthcare payments, there’s an important element that often gets overlooked. It makes a big difference who receives that lump-sum payment.

In the case of Kaiser Permanente, capitated payments are made directly to the medical group and the physicians who are responsible for providing care. In almost every other health system, an insurance company collects capitated payments but then pays the medical providers on a fee-for-service basis. Even though the arrangement is referred to as capitated, the incentives are overwhelmingly tied to the volume of care (not the value of that care).

In a mixed-payment model, doctors and hospitals invariably prioritize the higher paying FFS patients over the capitated ones. When I think about these conflicting incentives, I’m reminded of a prominent medical group in California. It had a main entrance for its fee-for-service patients and a second, smaller one off to the side for capitated patients.

I doubt the time spent with the patient—or the overall care provided—was equal for both groups. When income is based on quantity of care, not quality, clinicians focus more on treating the complications of chronic disease and medical errors rather than preventing them in the first place. Geisinger has walked this tightrope in the past, but as economic pressures mount, I fear doctors will find the two sets of incentives conflicting and difficult to navigate.

The big lesson: as financial pressures mount, the most effective approaches of the past will likely fail in the future. All healthcare organizations will need to make a decision: keep trying to drive volume and prices up through FFS or shift to capitation. Getting caught in the middle is a prescription for failure.

Examining the healthcare acquisitions made by Amazon and CVS, it’s clear these giants have decided to move aggressively toward a model more like Kaiser Permanente’s—one that brings insurance, pharmacy, physicians and sophisticated IT systems under one roof. These companies, along with Walmart, are aggressively marching down a path toward capitation, focusing on Medicare Advantage (the value-based option for Americans 65+) as an entry point.

So far, Geisinger has hedged its bets by maintaining a hybrid revenue stream. I doubt they can do so successfully in the future. That brings us to a final question.

The biggest question remaining

Over the next decade, hospital systems, insurers and retailers will battle for healthcare supremacy. The most recent Kaiser-Geisinger deal reflects an industry that’s undergoing massive change as health systems face intensifying pressure to remain relevant.

The most important issue to resolve is whether these shifts will ultimately help or harm patients. I’m optimistic for a positive outcome.

Whether or not the retail giants displace the incumbents, they will redefine what it takes to win. For all their faults, companies like Amazon and Walmart care a lot about meeting the needs of customers—a mindset rarely found in today’s healthcare world. As these companies grow ever larger, they’ll place consumer-oriented demands on doctors and hospitals. This will require care providers to deliver higher quality care at more affordable prices.

The retailers will only do deals with the best of the best. And they’ll kick the underachievers to the curb. They’ll use their sophisticated IT systems to better coordinate and innovate medical care. Insurers, hospitals and doctors who fail to keep up will be left behind.

Over time, patients will find themselves with far more choices and control than they have today. And I’m optimistic that will be good for the health of our nation.