Newport Beach, Calif.-based Hoag is spending $1 billion on a project that will add two specialty hospitals and expand its Sand Canyon Medical Center in Irvine, The Orange County Register reported Nov. 14.

Once completed, the project will have added between 1,000 to 1,500 employees, many of whom have specialized jobs and training, according to the report.

The specialty hospitals — which will focus on women’s health, digestive illnesses and cancer — will have inpatient and outpatient facilities. Operating rooms will be housed in a new building, and pharmacy and labs in another. The project will feature six new buildings, including 155 inpatient beds, eight operating rooms and 120,000 square feet of outpatient facilities.

Construction is expected to be completed by 2025.

In 2025, the city is also expected to see the opening of UC Irvine’s $1.3 billion medical complex with a full-service hospital. Earlier this year, City of Hope opened an outpatient cancer center and is now building an adjacent cancer-focused hospital, which is also set to open in 2025.

Providence, a 51-hospital system headquartered in Renton, Wash., ended the first nine months of 2022 with an operating loss of $1.1 billion, according to financial documents released Nov. 14.

The system said in a Nov. 11 news release that its third quarter financial results showed the “ongoing impact of inflation, the national healthcare labor shortage, delayed reimbursement from payers, global supply chain disruptions and financial market weakness.”

For the nine months ended Sept. 30, Providence’s operating revenues were $19.6 billion on a pro forma basis, up from $18.8 billion during the same period last year, according to the report. The pro forma results exclude the operations of Newport Beach, Calif.-based Hoag Hospital. Providence and Hoag ended their affiliation in January.

Operating expenses over the first nine months of the year were $20.7 billion, a 7 percent increase over the same period in 2021 on a pro forma basis. This includes a 9 percent increase in salary and benefits due to the cost of agency staff, overtime and wage increases, according to the release. It also includes a 6 percent increase in supply costs, driven by an 8 percent increase in pharmaceutical spending.

Providence said financial market weakness and volatility drove investment losses of $1.4 billion for the first nine months of 2022, bringing the system’s unrestricted cash and investments to $9.1 billion.

“Healthcare delivery systems across the country face unprecedented challenges, and Providence has not been immune,” Providence President and CEO Rod Hochman, MD, said in the release. “However, just as we have for more than 165 years, we will continue to be here to meet the health care needs of our communities. While we still have a journey ahead of us, we are moving in the right direction and are beginning to see signs of renewal this quarter. My deepest gratitude to the caregivers of Providence for continuing to focus on the Mission and serving those in need, especially those who are most vulnerable, with excellence and compassion.”

Even as new omicron strains take over, Covid is no longer driving a majority of patients into the hospital. Still, doctors worry the virus could re-emerge as immunity wanes.

As the flu and RSV (respiratory syncytial virus) have spread rapidly this fall — inundating and overwhelming hospitals and their staff across the country — Covid has not.

In fact, Covid-related deaths and hospitalizations have fallen in recent months,despite the emergence of new omicron subvariants that evade immunity from previous infections and vaccination.

According to NBC News data, Covid deaths have fallen consistently since Aug. 31, when the seven-day average of daily Covid deaths was at 571. A month later, on Sept. 30, the number fell to 475. By Halloween, 365 were dying per day, on average, from Covid.

As of Nov. 14, the number had fallen to 316.

This week, the Centers for Disease Control and Prevention is expected to release new data on Covid-related mortality, finding that death rates began to decline in March 2022.

The overall hopeful sign of declining deaths could indicate yet another new Covid phase, doctors suggest. Fewer people sick enough to be hospitalized with Covid means that fewer people are dying of the illness.

The average number of Covid hospitalizations per day has decreased by 27.9% since Aug. 28, according to NBC News data.

Even better, Covid, it seems, is no longer sending a majority of patients into intensive care units.

“There has not been an increase in patients admitted to the hospital specific for Covid-related disease,” said Dr. Hugh Cassiere, director of critical care services at Sandra Atlas Bass Heart Hospital at North Shore University Hospital, part of Northwell Health in New York City.

Patients in his ICU with Covid were admitted with unrelated medical issues, and were subsequently found to be Covid-positive, Cassiere said.

“Not to say that it’s gone, but Covid has become a coincidental disease,” he said.

Dr. Vin Gupta, a pulmonologist and an affiliate faculty member at the University of Washington in Seattle, attributes the decline in deaths and severe Covid cases to a level of “baked-in immunity,” including vaccination, prior infection or a combination of the two.

While Covid-related hospitalizations are not currently increasing, Gupta warns that they could during the winter as immunity, especially from previous infection, diminishes.

“If you had Covid, say six to four months ago, you’re going to have less protection against hospitalization than if you were vaccinated,” Gupta said. “The duration and the robustness of protection wanes a lot more quickly if all you rely on is natural immunity.”

With that in mind, data from the Institute for Health Metrics and Evaluation, a research center within the University of Washington, suggest that Covid hospitalizations and deaths could tick up again in “mid-January at the earliest,” said Gupta, a medical analyst for NBC News and MSNBC.

Despite the encouraging decline in Covid deaths, another school of thought suggests that Covid has simply morphed into a new kind of fatal illness.

“Before everyone was vaccinated or had been infected, 80 or 90% of Covid looked exactly same. They had terrible pneumonia. They were in the ICU on respiratory support,” said Dr. Jeremy Faust, an emergency medicine physician at Brigham and Women’s Hospital and an instructor at Harvard Medical School in Boston.

Now, he said, “Covid deaths don’t all look the same.” While “baked-in immunity” may keep the most severe cases at a minimum, it is clear that Covid can wreak havoc on the body long after the infection has cleared.

“Somebody could have Covid and have a heart attack, and the primary cause of death is listed as a heart attack because that’s what really brought them to the hospital,” Faust said.

But, he added, “we’ll never know to what degree Covid triggered that heart attack.”

South Dakota-based Sanford Health and Minnesota-based Fairview Health Services unveiled plans Tuesday to merge and form a 58-hospital juggernaut serving rural and urban patients across the Midwest.

The nonprofits have signed a nonbinding letter of intent as they proceed with due diligence and regulatory antitrust reviews, they said in a press release. Each would maintain their own regional presence, leadership and regional boards but operate as a single integrated system under Sanford Health’s banner.

The organizations said they anticipate closing their deal sometime next year.

“Our organizations are united by a shared commitment to advance the health and well-being of our communities,” Sanford Health President and CEO Bill Gassen said in the release. “As a combined system, we can do more to expand access to complex and highly specialized care, utilize innovative technology and provide a broader range of virtual services, unlock greater research capabilities and transform the care delivery experience to ensure every patient receives the best care no matter where they live.”

Gassen is teed up to serve as the president and CEO of the new entity should the merger go through, while Fairview CEO James Hereford would serve as co-CEO for one year following the deal’s close.

Headquarted in Sioux Falls, Sanford Health describes itself as the country’s largest rural health system with nearly 48,000 employees, 47 medical centers, 224 clinics and hundreds of other facilities. It serves over 1 million patients and 220,000 health plan members, according to its website, and each year logs 5.2 million outpatient or clinic visits, nearly 83,000 admissions, about 128,000 surgeries and procedures and roughly 195,000 emergency department visits.

Minneapolis-based Fairview Health Services employs 31,000 people across 11 hospitals as well as dozens of clinics, pharmacies and other facilities. It boasts a network of over 5,000 doctors after merging a few years back with fellow Twin Cities system HealthEast and due to partnerships with University of Minnesota Health specialists.

The two systems said their planned merger will improve care quality, outcomes, patient experience and health equity across their patient populations. New efficiencies will also help the systems offer more affordable care, they noted, while their workforces will benefit from stronger recruitment and advancement opportunities.

“With Sanford Health, Fairview Health Services has found a partner that shares our Midwestern values and our commitment to affordable, accessible and equitable care delivery,” Hereford said in the release. “Our complementary capabilities mean that together, we are uniquely positioned to improve clinical outcomes, develop new care delivery models, expand opportunities for employees and clinicians across our broader operational footprint, and apply our combined resources to positively impact the well-being of our patients and communities today and for decades to come.”

Sanford and Fairview’s news lands about six months after Advocate Aurora Health and Atrium Health announced their own nonprofit megamerger. That deal continues to move through the necessary regulatory hurdles and, if closed, would yield a 67-hospital with strong presences in the nearby Chicago and Milwaukee markets.

When it comes to her feelings about investing in care delivery startups, it’s a real “mixed bag” for Ulili Onovakpuri, managing partner at Kapor Capital. This is because a lot of them operate on a cash-pay model. She summarized the issue quite succinctly: there’s an incredible amount of innovation happening, but the people who could benefit the most from this type of care will be the last ones to receive it.

Healthcare investors are facing a myriad of care delivery startups seeking their capital. And it’s an interesting time in the care delivery startup space — there’s more and more questions arising about how much scrutiny should be applied to the way these companies are growing, what should be included in their gross margins, and how they should be valued.

When it comes to her feelings about investing in care delivery startups, it’s a real “mixed bag” for Ulili Onovakpuri, managing partner at Kapor Capital. She said so Sunday at Engage at HLTH, a patient engagement summit hosted by MedCity News in Las Vegas.

Healthcare is a stratified experience in the U.S. Onovakpuri drew attention to the fact that this stratification is getting worse with the advent of provider startups that operate on a cash-pay model, such as Sesame and Tia.

These types of cash-pay providers usually offer a simpler healthcare experience compared to the endless bureaucracy and billing confusion patients face in the traditional healthcare system. This can be very attractive to patients — they don’t want to deal with months-long wait times to see a provider, nor do they wish to navigate the Kafkaesque ordeal of trying to understand and pay their healthcare bills.

In Onovakpuri’s view, these cash-pay providers “are good for some” — those who can afford it. But those who lack the means to pay for care outside the traditional healthcare delivery system don’t get to take part in these startups’ care model, regardless of how innovative or convenient it may be.

“If I’m honest, it’s hard for me because I see a lot of great tech every single day, and when I talk to them, I’m like, ‘Wait, this is awesome — how much is this?’ and then I say, ‘Well, we can’t do it because the people that we care the most about can’t afford it.’ And it’s hard, because they’re probably the folks who need it the most,” Onovakpuri said.

She summarized the issue quite succinctly: there’s an incredible amount of innovation happening, but the people who could benefit the most from this type of care will be the last ones to receive it.

“Innovation is great, but it’s another dividing factor we face,” Onovakpuri declared.

Onovakpuri noted another key concern: the fact that many of the country’s most talented physicians are opting to leave their hospitals and health systems to work for cash-pay care delivery startups. She said she can understand why they make this choice (they are understandably fed up with the inefficiency of standard systems), but it still is a problem because it exacerbates hospitals’ labor shortage crisis and makes their patients wait times even longer to receive care.

There’s an old trope among human resources leaders that people don’t quit companies, they quit managers. There’s certainly truth to it. If an employee has a difficult or inattentive boss, they are at much greater risk of leaving for another opportunity. But a “bad” manager is not always someone lacking in the skills necessary to engage employees; sometimes the problem is that their own roles are structured in ways that make it nearly impossible to succeed.

We’ve recently heard stories from leaders at several health systems describing the untenable management scope for many of their mid-level nursing leaders. It’s common to hear that nurse managers have dozens of direct reports, and a few systems reported that some of their managers have well over a hundred individuals reporting to them. With that scope, it’s impossible to develop relationships with everyone on the team, much less be able to customize roles, or provide tailored feedback and support.

For younger workers, the manager relationship is critical for engagement, skill development, and building loyalty.

Given today’s intense margin pressures, it’s tempting to cut clinical managers and increase the span of control for those who remain—but underinvestment here is short-sighted, and will surely exacerbate challenges maintaining critical capacity in the near-term, as well as building the foundation for future growth.

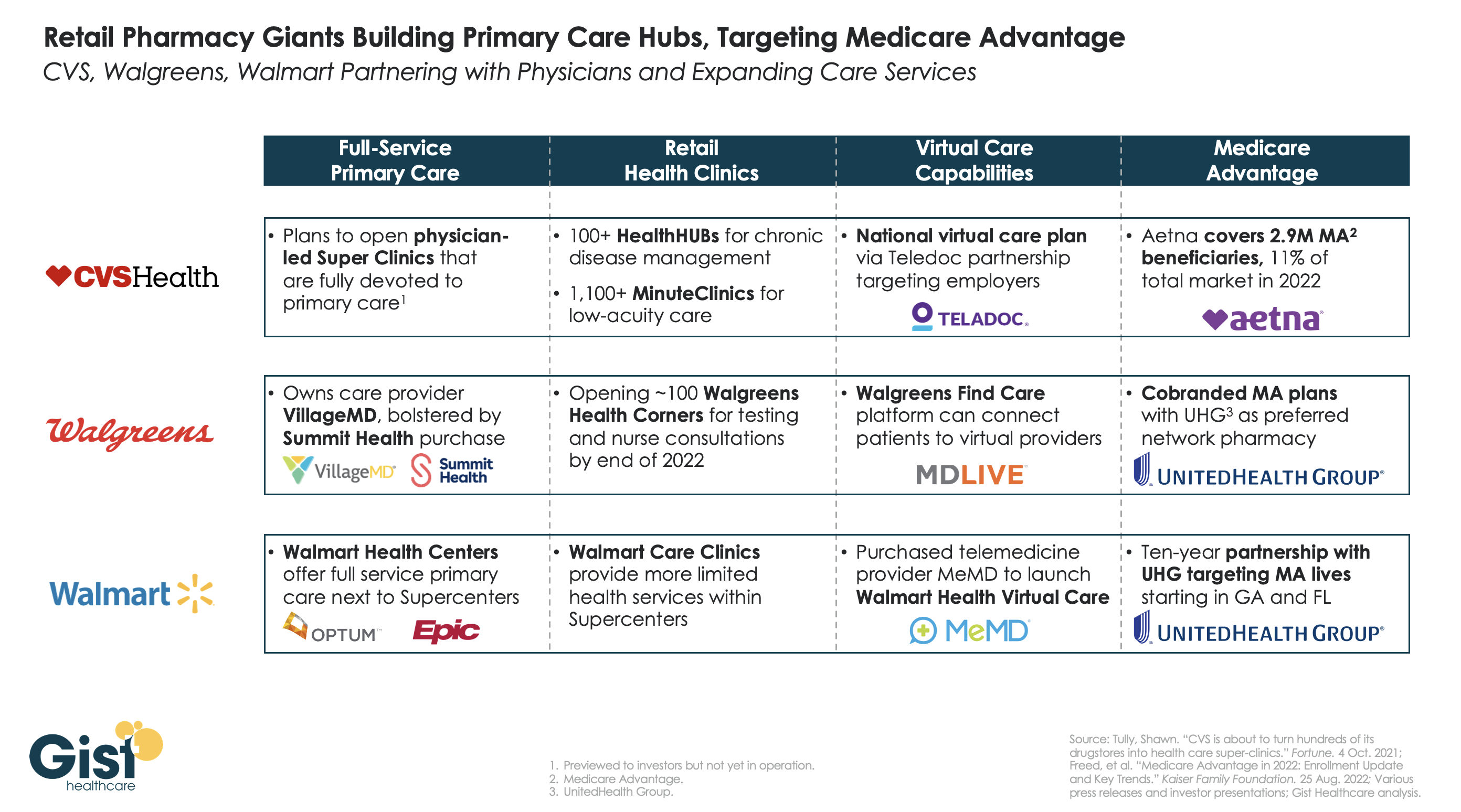

Retailers and insurers are building out their primary care strategies in a bid to become the new front door for patients seeking healthcare services, especially seniors on highly profitable Medicare Advantage (MA) plans. In the graphic above, we examine the capabilities of three of the largest pharmacy chains—CVS Health, Walgreens, and Walmart—to deliver full-service primary care across in-person and virtual settings.

CVS pioneered the pivot to care provision in 2006 with its acquisition of MinuteClinic, which now has over 1,000 locations. The company has further expanded its concept of pairing retail and pharmacy services with primary care by opening over 100 HealthHUBs, which provide an expanded slate of care services. However, CVS lags competitors in the rollout of full-service primary care practices, with its proposed physician-led Super Clinics still stuck in the planning stages.

Walgreens, with its majority stake in VillageMD (on track for 200 co-branded practices by the end of the year) and the recent acquisition of Summit Health (which operates another 370 primary and urgent care clinics) has assembled the most impressive primary care footprint of the three companies.

Walmart, the largest by number of stores but also the newest to healthcare, has opened more than 25 Walmart Health Centers, a step up from earlier experimentation with in-store care clinics, offering more services and partnering with Epic Systems to integrate electronic health records.

CVS’s key advantage over its competitors comes from its payer business, having acquired Aetna in 2018, now the fourth-largest MA payer by membership. Walgreens and Walmart have both aligned themselves with UnitedHealth Group (UHG) to participate in MA, with Walmart having struck a ten-year partnership to steer UHG MA beneficiaries to Walmart Health Centers in Florida and Georgia.

While aligning with UHG expands the reach of these retail giants into MA risk, UHG, whose OptumHealth division is by far the largest employer of physicians nationwide, remains the healthcare juggernaut most poised to unseat incumbent providers as the home for consumers’ healthcare needs.

In their latest article scrutinizing the MA program, New York Times reporters Reed Abelson and Margot Sanger-Katz highlight MA marketing practices brought to light in a recent report from the Senate Finance Committee. Complaints to the Centers for Medicare and Medicaid Services (CMS) about MA marketing more than doubled from 2020 to 2021, as agents and brokers took advantage of oversight rules relaxed during the Trump administration. Some of the most egregious alleged abuses include agents switching seniors into new plans without their consent and exploiting individuals with cognitive impairments.

The Gist: Media interest is finally catching up to the building legislative and regulatory pressure on Medicare Advantage. While earlier reporting has highlighted how plans can inflate payments from Medicare, this new story shows how the process of selecting a plan can be fraught for the seniors enrolled.

Plan design is confusing even for industry insiders, so it is no surprise that seniors might find themselves ‘choosing’ plans that omit key providers, or even drug coverage they already rely on, particularly after being badgered or misled by agents and brokers.

Many of the regulatory fixes highlighted in the report can be implemented directly by CMS, but insurers, who remember the managed care backlash of the 90s, shouldn’t wait to tighten the reins on questionable marketing practices, lest they risk losing public support for one of their most lucrative business lines.

In its Q3 earnings call, Oscar Health CEO Mario Schlosser revealed that the “insurtech” has pulled out of the MA market in Texas and New York, leaving it with only one Florida-based plan. Oscar entered the MA business with high hopes in 2020, but counted fewer than 5K MA members in Q3 2022.

Although its Affordable Care Act exchange enrollment has nearly doubled since last year, now covering more than 1M lives, Oscar is still struggling with high medical loss ratios, which have kept it from turning a profit. The company’s stock price is at an all-time low, having declined over 90 percent from its peak, shortly after its 2021 IPO.

The Gist: Like Bright HealthCare before them, Oscar pulling out of MA is another sign that the chance of meaningful disruption from “insurtechs” has nearly vanished. While still privately held, Oscar achieved fame in the early 2010s through catchy marketing that targeted a young, tech-savvy client base, and its move into MA before the pandemic signaled broader ambitions.

Oscar’s travails illustrate just how hard it is to start an insurance company from scratch, even with an intriguing and comprehensive technology platform. The company proved unable to overcome its lack of market power in negotiations with providers, and faced difficulty managing a small, unstable risk pool.

Now that more traditional insurers are improving their mobile tech interfaces and telehealth offerings, the differentiated value Oscar offers to its members has clearly diminished.

Last week, over 1,200 resident physicians and interns at Montefiore Medical Center, one of the largest employers in New York City, with four hospitals in the Bronx, held an organizing vote and requested voluntary recognition of their bargaining unit. The residents organized under the Committee of Interns and Residents, a unit of the Service Employees International Union that claims 22K members and has established unions at five hospitals this year. Roughly seven percent of practicing doctors were unionized as of 2019; that number has grown in the wake of pandemic-induced burnout and industry consolidation. Montefiore Medical Center declined to voluntarily recognize the union and has requested that the union re-form via a secret ballot election.

The Gist: Health system executives may see the possibility of resident unions as another headache amid the ongoing labor crisis, but the drivers of the crisis—burnout, workplace safety concerns, work-life balance, and real-wage erosion—are responsible for the growing appeal of unions for physicians. Fueled by economy-wide stressors, unionization has been growing in nontraditional labor sectors, including among baristas and tech workers, and medical residents may be the next to join that wave.

Health systems worried about resident unionization should address residents’ concerns about working conditions proactively, which may involve reevaluating wages in light of residents’ significant contributions to operational and financial success.