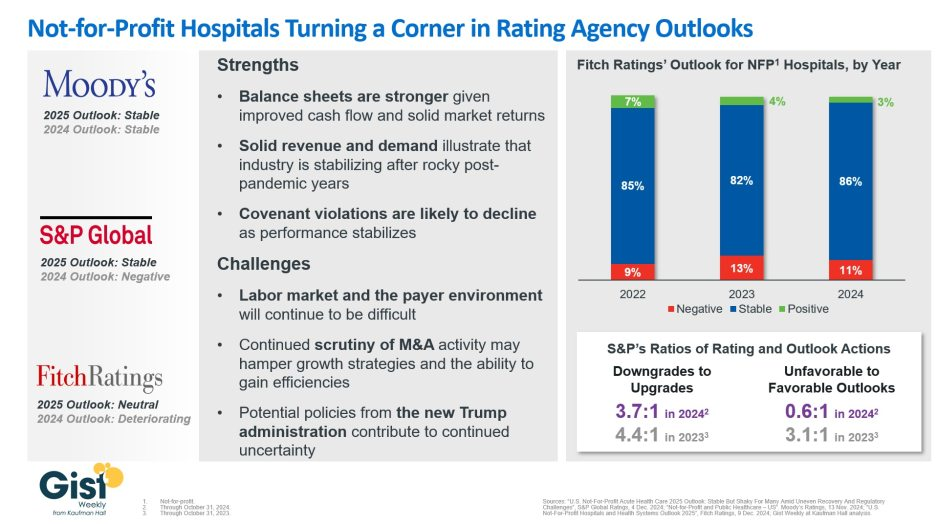

In late 2023, S&P Global and Fitch Ratings viewed the not-for-profit (NFP) hospital sector as negative or deteriorating, reflecting the difficult financial position many were in following the pandemic.

In recent weeks, S&P and Fitch upgraded their 2025 sector outlook for NFP hospitals to stable and neutral respectively, joining Moody’s Ratings, which held stable from last year.

This week’s graphic illustrates the rating agencies’ latest views on NFP hospitals, which point to a promising but uneven recovery for the industry.

Overall, the reports detail that stronger balance sheets, solid revenues, and improved demand have reduced the likelihood of covenant violations and strengthened NFP hospitals’ positions.

However, challenges persist that could impede further progress. The labor market, payer environment, antitrust enforcement, and a new administration all present complications for the continued recovery of NFP hospitals. Nonetheless, the reports indicate significant improvement for the industry since the post-pandemic ratings downturn.

Fitch’s report noted that the share of NFP hospitals with a stable outlook has reached a three-year high. Meanwhile, S&P reported that there are now almost twice as many NFP hospitals with favorable outlooks compared to unfavorable ones, a dramatic flip from 2023, which had a 3.1:1 ratio of unfavorable to favorable outlooks.

These ratings changes reflect the hard work put in by NFP hospitals across the country to improve their financial performance and find new ways to serve their communities sustainably.

However, the recovery remains “shaky” and incomplete, and hospitals still face a long road ahead as they reconfigure to a new normal.

Claim denials are increasing, especially in Medicare Advantage, and it’s affecting hospital’s revenue cycles and patient care.

“We definitely are seeing an increase in denials,” said Sherri Liebl, executive director of Revenue Cycle, CentraCare Health, a large multispecialty system in Minnesota. CareCare has two acute care hospitals, seven Critical Access Hospitals and 30 standalone clinics, many of them in rural areas.

CentraCare reported a positive margin this year, but in no way realizes the profits of insurers, especially the national insurers where Liebl is having the most difficulty with claims.

CentraCare’s goal in its cost to collect – not all-around denials – is to be at 2%. The health system is closer to 7% on its cost to collect.

“The cost for our organization is exorbitant,” Lieble said.

Much of the blame for denials is falling to artificial intelligence being used in algorithms to deny claims.

UnitedHealthcare has been sued in a class action lawsuit that alleges the insurer unlawfully used an artificial intelligence algorithm to deny rehabilitative care to sick Medicare Advantage patients.

Cigna has also been suedfor allegedly using algorithms to deny claims. The lawsuit claims the Cigna PXDX algorithm enables automatic denials for treatments that do not match preset criteria, evading the legally required individual physician review process.

A Cigna Healthcare spokesperson said the vast majority of claims reviewed through PXDX are automatically paid, and that the PXDX process does not involve algorithms, AI or machine learning, but a simple sorting technology that has been used for more than a decade to match up codes. Claims declined for payment via PXDX represent less than 1% of the total volume of claims, the spokesperson said.

Industry consultant Adam Hjerpe, who formerly worked for UnitedHealth Group, said there’s nothing new about payers using artificial intelligence. AI has been used for 20 years in robotic processes, statements in Excel and algorithms, he said.

Everybody is working with good intent, Hjerpe said. There are reasonable controls in place to avoid fraud and abuse.

Claims are being denied for missing information, or for the information being out of sequence, or for the claim giving an incomplete picture of the care.

“We don’t want care delayed,” he said.

Nobody wins in claims denials, said Susan Taylor, Pega’s vice president of Healthcare and Life Sciences.

While payers save money in the short-term, in the long-term, the best arrangement is to have payers and providers work together to prevent denials, said Taylor, who has worked in healthcare for more than 25 years, starting on the health system side before moving into IT.

“There are more claims of note being denied,” Taylor said. “If you look at the ecosystem, there are a lot of opportunities for error.”

The solution is building an agility layer to streamline workflows throughout the revenue cycle, from initial claim submission to the complex denials processing stage.

WHY THIS MATTERS

Liebl said that denials have increased over the past two years and that there’s also been an uptick in payer audits months after payment has been made.

Insurers want justification for why CentraCare should keep its payments, and this is especially true for Medicare Advantage claims, she said.

One insurer said the claim didn’t meet inpatient criteria and downgraded the claim to an observation patient.

“We have a pretty good success rate as far as being able to justify we did the right care,” Liebl said.

Asked what’s driving the higher denial rates Lieble said, “Everybody wants to keep margins and expand their business. I think it comes down to profit margins, trying to keep profit margins high; we’re just trying to stay afloat.”

To combat denials and work with payers, CentraCare founded a joint operating committee to have successful partnerships. They’ve been more successful with the local Minnesota plans than the national plans, but Liebl is optimistic, she said.

“I am hopeful we can create partnerships …” she said. “Some of the denials we receive are against their payer policy. We need to be able to hold payers accountable.”

Larger health systems have a little more clout, and CentraCare is able to partner with other health systems through the Minnesota Hospital Association.

What’s being lost in all this is the patient, Liebl said. Sometimes a patient is getting a bill up to a year after a procedure.

“Sometimes the patient focus is lost when we work through some of this,” she said.

“They keep our money longer,” Liebl said. “They hold our money hostage. We have denials sitting out there for 300 days. It’s a lot of administrative burden on our part. We’ve spent a lot of money just to get the money in the door. Finally when that claim has been resolved, it’s a year later. No one wins? I think there is some winning going on one side.”

In an era of significant medical debt, rising healthcare costs and delayed treatments, our current healthcare system is ripe for solutions that alleviate the burden of paying patient bills.

Enter embedded finance. While not a new concept by any stretch – it has long existed in retail – fintechs and traditional banks are determined to give patients more options and a fundamentally better experience in the way they pay for healthcare services. In doing so, a financially strained domestic healthcare system stands to benefit from increased cash flow, improved health equity and optimized patient engagement.

Simply put, embedded finance is the integration of financial services – such as payment, lending, banking and insurance features – into another company’s normal service or products. We have all undoubtedly come across these offerings in our daily lives as consumers. Think private label credit cards with retail chains or airlines, digital wallet purchase options at the Amazon checkout, a buynow-pay-later (BNPL) plan from Affirm or Klarna, or insurance obtained from a car rental.

The goal of embedded finance:

is to improve a user’s experience by accessing financial services without leaving a brand’s platform. By layering application programming interface (API)-driven fintech or banking capabilities on top of a website or mobile app for, say, a hospital patient portal, the bundled solution allows the user to stay on one website or application to complete a financial transaction. Doing so removes friction in the experience and delivers a breadth of contextual information that a provider or payer can use to prompt further action on the patient’s medical journey.

The implications for embedded finance in healthcare are vast and benefit every stakeholder across the revenue cycle value chain:

Patients: Flexibility and convenience to better structure and plan bill payment while receiving greater access to financial options and additional services that improve the care experience such as reminders and health tracking

Providers: Faster and higher rates of collections coupled with ongoing patient dialogue that cements loyalty, affords clinicians the opportunity to suggest customized treatment options, and improves revenue composition and potential valuation

Payers: More efficient claims processing cycle, automated processes and improved data security

The burden of patient bills and increasing medical costs are not new to our system. Yet there has been a confluence of fundamental changes that make embedded finance particularly attractive in healthcare going forward, including increased smartphone usage and Internet penetration, COVID19 adoption of fintech products across healthcare settings, rising inflation rates that reduce a patient’s ability to pay and the adoption of mobile-based apps among younger, digitally native consumers and lower income patients.

These tailwinds support a massive addressable market as healthcare is expected to comprise approximately 23% of a U.S. embedded finance industry set to exceed $230 billion by 2025, or a 10x increase from $23 billion in 2020.

Significant attention and capital investment are accelerating the rise of embedded finance in healthcare.

Punctuated by attractive elements at the intersection of technology, financial services and healthcare sectors, nimble fintech companies and large financial institutions alike are competing for market presence. For example, pioneering healthcare-focused fintech PayZen closed $220 million in fresh capital in late 20223, while banks such as Wells Fargo and Synchrony have launched the popular medical-focused credit cards Health Advantage and CareCredit, respectively. Cain Brothers’ parent company, KeyBank, has also advanced an embedded strategy to provide healthcare digital innovation at scale and enhance patient experiences by acquiring XUP Payments in 2021. The resulting U.S. landscape for healthcare embedded finance is one that is evolving rapidly and that we are monitoring closely for investment and eventual M&A consolidation.

With expanding options around the type of medical care received and where it is received, we expect the financial tools at a patient’s disposal to garner significant attention in the years to come.

Embedded finance is a leading solution positioned to improve health equity and the financial well-being of millions of patients across the U.S., as well as fuel sector growth. Just as we’re accustomed now to buying pretty much anything with a few clicks, so too will embedded finance become a ubiquitous part of the healthcare landscape.

The bill is coming due for federal loans given to hospitals early in the COVID-19 pandemic, adding to their financial woes, Oregon Public Broadcastingreported May 28.

The Medicare Accelerated and Advance Payment program offered hospitals short-term interest- free loans, according to the report. These loans are coming due as hospitals’ costs are rising quickly and revenue from patient stays and surgeries is growing more slowly.

The idea behind the program was that hospitals would be able to pay back the advance once the pandemic passed and operations returned to normal, according to the report. Hospitals are still dealing with the effects of the pandemic, but the federal government wants to recoup the money to keep Medicare funded.

In March 2021, HHS began recovering those cash advances by paying hospitals 25 percent less for Medicare reimbursement claims, according to the report. Earlier this year, HHS began paying hospitals 50 percent less for reimbursement claims.

Hospitals lobbied for the loans to be forgiven, but were unsuccessful, according to the report.

Kennett Square, Pa.-based Genesis Healthcare, one of the largest post-acute care providers in the U.S., warned that bankruptcy is possible if its financial losses continue.

“The virus continues to have a significant adverse impact on the company’s revenues and expenses, particularly in hard-hit Mid Atlantic and Northeastern markets,” Genesis CEO George V. Hager Jr., said in a Nov. 9 earnings release.

Mr. Hager said government stimulus funds the company received in the third quarter of this year fell nearly $60 million short of the company’s COVID-19 costs and lost revenue.

Genesis said it has taken several steps to help offset the financial damage linked to the pandemic, including delaying payment of a portion of payroll taxes incurred through December.

But the company warned that bankruptcy is possible if its financial losses continue.

“Even if the company receives additional funding support from government sources and/or is able to execute successfully all of its these plans and initiatives, given the unpredictable nature of, and the operating challenges presented by, the COVID-19 virus, the company’s operating plans and resulting cash flows, along with its cash and cash equivalents and other sources of liquidity. may not be sufficient to fund operations for the 12-month period following the date the financial statements are issued,” Genesis said. “Such events or circumstances could force the company to seek reorganization under the U.S. Bankruptcy Code.”

Genesis ended the third quarter of this year with a net loss of $62.8 million, compared to net income of $46.1 million in the same period a year earlier.

The financial challenges caused by the COVID-19 pandemic have forced hundreds of hospitals across the nation to furlough, lay off or reduce pay for workers, and others have had to scale back services or close.

Lower patient volumes, canceled elective procedures and higher expenses tied to the pandemic have created a cash crunch for hospitals. U.S. hospitals are estimated to lose more than $323 billion this year, according to a report from the American Hospital Association. The total includes $120.5 billion in financial losses the AHA predicts hospitals will see from July to December.

Hospitals are taking a number of steps to offset financial damage. Executives, clinicians and other staff are taking pay cuts, capital projects are being put on hold, and some employees are losing their jobs. More than 260 hospitals and health systems furloughed workers this year and dozens of others have implemented layoffs.

Below are 11 hospitals and health systems that announced layoffs since Sept. 1, most of which were attributed to financial strain caused by the pandemic.

1. NorthBay Healthcare, a nonprofit health system based in Fairfield, Calif., is laying off 31 of its 2,863 employees as part of its pandemic recovery plan, the system announced Nov. 2.

2. Minneapolis-based Children’s Minnesota is laying off 150 employees, or about 3 percent of its workforce. Children’s Minnesota cited several reasons for the layoffs, including the financial hit from the COVID-19 pandemic. Affected employees will end their employment either Dec. 31 or March 31.

3. Brattleboro Retreat, a psychiatric and addiction treatment hospital in Vermont, notified 85 employees in late October that they would be laid off within 60 days.

4. Citing a need to offset financial losses, Minneapolis-basedM Health Fairview said it plans to downsize its hospital and clinic operations. As a result of the changes, 900 employees, about 3 percent of its 34,000-person workforce, will be laid off.

5. Lake Charles (La.) Memorial Health Systemlaid off 205 workers, or about 8 percent of its workforce, as a result of damage sustained from Hurricane Laura. The health system laid off employees at Moss Memorial Health Clinic and the Archer Institute, two facilities in Lake Charles that sustained damage from the hurricane.

6. Burlington, Mass.-based Wellforce laid off 232 employees as a result of operating losses linked to the COVID-19 pandemic. The health system, comprising Tufts Medical Center, Lowell General Hospital and MelroseWakefield Healthcare,experienced a drastic drop in patient volume earlier this year due to the suspension of outpatient visits and elective surgeries. In the nine months ended June 30, the health system reported a $32.2 million operating loss.

7. Baptist Health Floyd in New Albany, Ind., part of Louisville, Ky.-based Baptist Health, eliminated 36 positions. The hospital said the cuts, which primarily affected administrative and nonclinical roles, are due to restructuring that is “necessary to meet financial challenges compounded by COVID-19.”

8. Cincinnati-based UC Health laid off about 100 employees. The job cuts affected both clinical and non-clinical staff. A spokesperson for the health system said no physicians were laid off.

9. Mercy Iowa City(Iowa) announced in September that it will lay off 29 employees to address financial strain tied to the COVID-19 pandemic.

10. Springfield, Ill.-based Memorial Health Systemlaid off 143 employees, or about 1.5 percent of the five-hospital system’s workforce. The health system cited financial pressures tied to the pandemic as the reason for the layoffs.

11. Watertown, N.Y.-based Samaritan Healthannounced Sept. 8 that it laid off 51 employees and will make other cost-cutting moves to offset financial stress tied to the COVID-19 pandemic.

Here are nine hospitals and health systems with strong operational metrics and solid financial positions, according to reports from Fitch Ratings, Moody’s Investors Service and S&P Global Ratings.

1. St. Louis-based Ascension has an “AA+” rating and stable outlook with Fitch. The system has a strong financial profile and a significant presence in several key markets, Fitch said. The credit rating agency expects Ascension will continue to produce healthy operating margins.

2. Phoenix-based Banner Health has an “AA-” rating and stable outlook with Fitch and S&P. Banner’s financial profile is strong, even taking into consideration the market volatility that occurred in the first quarter of this year, Fitch said. The credit rating agency expects the system to continue to improve operating margins and to generate cash flow sufficient to sustain strong key financial metrics.

3. Cincinnati-based Bon Secours Mercy Health has an “AA-” rating and stable outlook with Fitch. The health system has a good payer mix, a leading position in several of its markets and adequate margins to support its growth, Fitch said. The credit rating agency expects the system to maintain strong operating profitability.

4. Children’s Hospital of Philadelphia has an “Aa2” rating and stable outlook with Moody’s and an “AA” rating and stable outlook with S&P. The hospital has a strong market position and healthy liquidity, Moody’s said. The credit rating agency expects CHOP’s market position and brand equity will support its recovery from disruption caused by COVID-19.

5. Milwaukee-based Children’s Wisconsin has an “Aa3” rating and stable outlook with Moody’s and an “AA” rating and stable outlook with S&P. The health system has strong cash flow margins, Moody’s said. The credit rating agency expects the health system’s financial performance to remain solid, given its commanding market presence and demand for services.

6. Philadelphia-based Main Line Health has an “AA” rating and stable outlook with Fitch. The credit rating agency expects the system’s operations to recover after the COVID-19 pandemic and for it to resume its track record of strong operating cash flow margins.

7. Midland-based MidMichigan Health has an “AA-” rating and stable outlook with Fitch. The system has generated healthy operational levels through fiscal year 2020, and Fitch expects it to continue generating strong cash flow.

8. Columbus, Ohio-based Nationwide Children’s Hospital has an “Aa2” rating and stable outlook with Moody’s. The system has a strong market position in pediatric services in Columbus and the broad central Ohio region, and its advanced research capabilities will support volume recovery from disruption caused by COVID-19, Moody’s said. The credit rating agency expects Nationwide Children’s margins to remain strong and for cost management initiatives and volume recovery to drive improvements.

9. Chicago-based Northwestern Memorial HealthCare has an “Aa2” rating and stable outlook with Moody’s. The health system had strong pre-COVID margins and liquidity, Moody’s said. The credit rating agency expects the system to maintain strong operating cash flow margins.

Fort Myers, Fla.-based Lee Health is freezing salaries for its 13,500 employees next year to help offset financial losses tied to the COVID-19 pandemic, according to the Fort Myers News-Press.

The pay freeze in 2021 will mark the first time in nine years that the publicly operated health system has not given employee raises. Salaries and benefits make up about half of the system’s nearly $2 billion in spending each year, according to the report.

Lee Health is facing a budget deficit for the first time in two decades due to financial strain linked to the pandemic. The salary freeze is one of several steps the system is taking to offset losses and avoid layoffs.

The system has halted most capital projects, and its top executives took pay cuts earlier this year. Lee Health will also reduce the match for employee retirement plans from 5 percent to 4 percent next year, and health plan premiums and copays will also increase, according to the report.

The U.S. Department of Labor (DOL) released its weekly jobless claims report at 8:30 a.m. ET Thursday. Here were the main metrics from the report, compared to Bloomberg estimates:

Initial jobless claims, week ended Sept. 19: 870,000 vs. 840,000 expected, and 866,000 during the prior week

Continuing claims, week ended Sept. 12: 12.580 million vs. 12.275 million expected, and 12.747 million during the prior week

At 870,000, Thursday’s figure represented the fourth consecutive week that new jobless claims came in below the psychologically important 1 million level, but was still high on a historical basis. Nevertheless, the labor market has made strides in recovering from the pandemic-era spike high of nearly 7 million weekly new claims seen in late March.

“While jobless claims under a million for four straight weeks could be considered a positive, we’re staring down a pretty stagnant labor market,” Mike Loewengart, managing director of investment strategy for E-Trade Financial Corporation, said in an email Thursday. “This has been a slow roll to recovery and with no signs of additional stimulus from Washington, jobless Americans will likely continue to exist in limbo. Further, a shaky labor market translates into a skittish consumer, and in the face of a pandemic that seemingly won’t go away without a vaccine, the outlook for the economy certainly comes into question.”

On an unadjusted basis, initial jobless claims rose by a greater margin, or about 28,500, from the previous week to about 824,500. The seasonally adjusted level of new claims rose by 4,000 week on week.

By state, unadjusted claims in California – where joblessness due to the pandemic has compounded with labor market stress due to wildfires – were again the highest in the country at more than 230,000, for an increase of about 4,400 week-over-week. Georgia, New York, New Jersey and Massachusetts also reported significant increases in new claims relative to the rest of the country. Most states reported at least increases in new claims last week.

Continuing claims have also trended lower after a peak of nearly 25 million in May, and fell for a second straight week in this week’s report. But these claims, which capture the total number of individuals still receiving unemployment insurance, have not broken below the 12 million mark since before the pandemic took hold of the labor market in mid-March.

Consistently high numbers of individuals have been filing for, and receiving, jobless benefits from regular state programs, and those newly created during the pandemic. The number of individuals claiming benefits in all programs for the week ended September 5 – the latest reported week – fell for the first time following three straight weeks of increases to 26.04 million, from the nearly 29.8 million reported during the prior week.

Of that total, more than 11.5 million comprised individuals receiving Pandemic Unemployment Assistance, which is aimed at self-employed and gig workers who don’t qualify for regular unemployment compensation but have still been impacted by the pandemic.

One of the major downside risks to further improvement in the labor market has been concern that Congress may not soon pass another round of fiscal stimulus aimed at keeping individuals on payrolls during the pandemic. Economists have already said that the end of the last round of augmented federal unemployment benefits in late July has weighed on improvements in joblessness.

“The current picture suggests that growth has slowed sharply in the past three months, and that the labor market is stalling again in the face of rising infections and the sudden ending of federal government support to unemployed people,” Ian Shepherdson, chief economist for Pantheon Macroeconomics, said in a note Wednesday.

The need for more fiscal stimulus to encourage the economy’s ongoing recovery has become a key talking point of policymakers including Federal Reserve Chair Jerome Powell and his colleagues at the central bank. In congressional testimony Tuesday and Wednesday, the Fed leader said further fiscal stimulus is “unequaled” by any other form of support that could be unleashed, with the central bank’s lending facilities having gone largely untouched by Main Street.

“The concept of the [congressionally authorized] Paycheck Protection Program was helpful because for many of those kinds of businesses – those businesses that don’t have cash reserves – the ability to get a forgivable loan if they stay open, if they keep people employed, was sound, and did give them the prospect of staying in business,” Joseph Minarik, The Conference Board chief policy economist and former Office of Management and Budget chief economist, told Yahoo Finance. “The notion that you have businesses that have been weak over the last few months and now have simply had to shut their doors, that’s a real problem, and it is not necessity going to be solved with a loan.”

The House passed a short-term government funding bill that extends the deadline for providers to start repaying Medicare advance payment loans to the end of the COVID-19 public health emergency.

The bill that the House passed late Tuesday is a major win for provider groups who worried they could struggle to repay the Medicare loans starting in August. The bill still has to pass through the GOP-controlled Senate.

The continuing resolution, which funds the federal government through Dec. 11, also lowers the interest rate for payments made under the Medicare Accelerated and Advance Payment Program to 4%, down from 10.25%.

The Centers for Medicare & Medicaid Services (CMS) gave out more than $100 billion in advance payments in March to providers slammed by the pandemic. The payments are essentially loans which CMS recoups by garnishing Medicare payments to providers. That process starts 120 days after the first payment was received.

But the bill would give providers one year before Medicare can claim their payments.

It would also give providers 29 months since the first payment to fully repay the loan amount. Currently, CMS gives providers a year to fully repay.

In addition to the changes to the repayment terms, the bill also delays $4 billion in payment cuts to disproportionate share hospitals that were supposed to go into effect as part of the Affordable Care Act. The cuts will now be delayed until December.

The bill earned plaudits from the hospital industry, which has pressed Congress for help as providers are still struggling with the pandemic and could not afford to have Medicare payments become garnished.

“Our hospitals continue to suffer high costs and revenue losses associated with COVID-19, and they welcome the relief this continuing resolution would provide,” said Bruce Siegel, president and CEO of America’s Essential Hospitals, which represents safety net hospitals.

The Federation of American Hospitals said earlier this week before the House vote that the advance payment program is a “vital lifeline to hospitals and healthcare providers during the pandemic that has enabled hospitals and providers to maintain access to critical patient care. But the ongoing pressures of the current crisis required a revision of the repayment terms.”

The bill, which has approval from the White House, now heads to the Senate. The chamber must reach a decision on the legislation to avoid a government shutdown when funding runs out on Sept. 30.