As the locus of care continues to shift from inpatient hospitals to outpatient centers, health system executives face a growing conundrum over pricing. The combination of “consumerism” and tougher reimbursement policies raises a question about how aggressively systems should discount services to compete in the ambulatory arena.

Site-neutral payment remains a goal for Medicare, and consumers are increasingly voting with their pocketbooks when it comes to choosing where to have procedures and diagnostics performed. “We know we’re going to have to give on price,” one CEO recently shared with us. “The question is how much, and how soon.”

Should hospitals proactively shift to match prices offered by freestanding centers, or should they try to defend their substantially higher “hospital outpatient department” (HOPD) pricing?

The former choice could help win—or at least keep—business in the system, but at the risk of turning that business into a money-losing proposition.

To compete successfully, hospitals will not only need to lower price, but also lower cost-to-serve—rethinking how operations are run, how overhead is allocated, and how services are staffed and delivered in ambulatory settings.

“We’ve got to get our costs down,” the CEO admitted. “Trying to run an ambulatory business with our traditional hospital cost structure is a recipe for losing money.”

And as a system CFO recently told us, “We can’t just trade good price for bad, for doing the same work. We have to be smart about where to discount services.” The future sustainability of many health systems will hinge on how they navigate this transition to an ambulatory-centric model.

Renton, Wash.-based Providence suffered its third credit downgrade in less than three weeks when Moody’s revised a rating on bonds the 51-hospital system holds to “A2” from “A1.”

Such a rating reflects an expectation margins will remain weak in 2023. The outlook is negative.

The move follows similar actions by Fitch Ratings March 17 and S&P Global March 21 amid an anticipated multiyear process of financial recovery.

Capital expenditure for Providence is expected to be restricted after the completion of a couple of major projects this year to effect “margin recovery,” Moody’s said.

Providence reported a $1.7 billion operating loss in 2022.

Tacoma, Wash.-based Virginia Mason Franciscan Health has laid off more than 300 administrative employees, the Puget Sound Business Journal reported April 4.

The job cuts affected less than 2 percent of the health system’s 19,000-plus workforce.

“Like many healthcare providers in the Pacific Northwest, we are experiencing tremendous financial strain caused by a number of factors, including lasting impacts from the COVID-19 pandemic, inflation and labor shortages,” Kelly Campbell, vice president of marketing and communications, told the Journal.

Affected employees will be eligible for career transition assistance, extended benefits and severance programs, according to the report.

Virginia Mason, which includes 10 hospitals and nearly 300 care sites, said it is focused on improving efficiencies and reducing costs in response to financial headwinds.

In 2022, Washington hospitals reported a total net loss of more than $2.7 billion, compared to a $1.2 billion loss in 2021, while their net operating loss was $2.1 billion, up from $742 million in 2021.

“We’re very concerned that access to this specialized care, the highest level of care, and in many cases, the life-saving care is threatened by unsustainable financial losses as hospitals are resorting to extraordinary means to close the gaps in their budgets,” Cassie Sauer, president and CEO of the Washington State Hospital Association, said in a March 21 media briefing.

Jaime King On Consolidation and Competition — The Trials and Triumphs of Health Care Antitrust Law New England Journal of Medicine March 18, 2023; 388:1057-1060 DOI: 10.1056/NEJMp2201629

“Over the past 30 years, health care consolidation has gone largely unchecked by federal and state antitrust enforcers, which has resulted in higher prices, stagnant quality of care, and limited access to care for patients. Similarly, consolidation has contributed to the availability of fewer employment options, limited wage growth, longer hours, and staff shortages for health care providers.

Antitrust law is designed to prevent such harms, but its failure to evolve alongside the health care industry has led to pervasive consolidation, which now necessitates regulation in some markets to address market-power abuses that competitive forces can no longer govern…

Although mergers are often justified with promises of improved quality or patient access, evidence supporting these claims is lacking.

Clinical integration as envisioned in accountable care organizations, for example, requires substantial oversight, training, and investment that goes well beyond the financial integration involved in most mergers. Most studies have found either no changes or a reduction in quality after provider mergers. Consolidation can also limit access to care; post-merger facility closures, reductions in charity care, and elimination of abortion and other reproductive health services have often occurred.

Consolidation among insurers also affects health care prices and quality. Insurers with market power can increase premiums above competitive levels by exercising monopoly power or can push provider payments below competitive levels by exercising monopsony power. Lower premiums are commonly found in areas with more insurers, whereas in the absence of competition, insurers that obtain price concessions from providers may not pass savings on to consumers.4 Some evidence suggests, however, that moderate amounts of insurer consolidation may be associated with improved patient experience, since providers in such markets have an incentive to compete on quality.

Given the health care industry’s growing complexity, future oversight could involve a combination of more responsive antitrust enforcement and creative regulatory interventions. Combining competitive and regulatory forces may offer the only hope for controlling health care prices, restoring high-quality care, protecting health care workers, and preserving and expanding access to care.”

Large, not-for-profit hospitals/health systems are getting a disproportionate share of unflattering attention these days. Last week was no exception: Here’s a smattering of their coverage:

Jiang et al “Factors Associated with Hospital Commercial Negotiated Price for Magnetic Resonance Imaging of Brain” JAMA Network Open March 21. 2023;6(3):e233875. doi:10.1001/jamanetworkopen.2023.3875

Whaley et al What’s Behind Losses At Large Nonprofit Health Systems? Health Affairs March 24, 2023 10.1377/forefront.20230322.44474

A Pa. hospital’s revoked property tax exemption is a ‘warning shot’ to other nonprofits, expert says KYW Radio Philadelphia March 24, 2023 ww.msn.com/en-us/news/us/a-pa-hospital-s-revoked-property-tax-exemption-is-a-warning-shot-to-other-nonprofits-expert-says

These come on the heals of the Medicare Advisory Commission’s (MedPAC) March 2023 Report to Congress advising that all but safety-net hospitals are in reasonably good shape financially (contrary to industry assertions) and increased lawmaker scrutiny of “ill-gotten gains” in healthcare i.e., Moderna’s vaccine windfall, Medicare Advantage overpayments and employer activism about hospital price-gauging in several states.

Like every sector in healthcare, hospitals enter budget battles with good stories to tell about cost-reductions and progress in price transparency compliance. But in the current political and economic environment, large, not-for-profit hospitals and health systems seem to be targets of more adverse coverage than others as illustrated above. Like many NFP institutions in society (higher education, organized religion, government), erosion of trust is palpable. Not-for-profit hospitals and health systems are no exception.

The themes emerging from last week’s coverage are familiar:

‘Not-for-profit hospitals/health systems, do not provide value commensurate with the tax exemptions they get.’

‘Not for profit hospitals & health systems take advantage of their markets and regulations to create strong brands and generate big profits.’.

‘Not for profit hospitals & health systems charge more than investor-owned hospitals: the victims are employers and consumers who pay higher-than-necessary prices for their services.’

‘NFP operators invest in risky ventures: when the capital market slumps, they are ill-prepared to manage. Risky investments, not workforce and supply chain issues, are the root causes of NFP financial stress. They’re misleading the public purposely.’

‘Executives in NFP systems are overpaid and patient collection policies are more aggressive than for-profits. NFP boards are ineffective.’

The stimulants for this negative attention are equally familiar:

Proprietary studies by think tanks, trade associations, labor unions and consultancies designed to “prove a point” for/against not-for-profit hospitals/health systems.

Government reports about hospital spending, waste, fraud, workforce issues, patient safety, concentration and compliance with transparency rules.

Aggressive national/local reporting by journalists inclined to discount NFP messaging.

Public opinion polls about declining trust in the system and growing concern about price transparency, affordability and equitable access.

Politicians who use soundbites and dog whistles about NFP hospitals to draw attention to themselves.

The cumulative effect of these is confusion, frustration and distrust of not-for-profit hospitals and health systems. Most believe not-for-profit hospitals/health systems do not own the moral high ground they affirm to regulators and their communities (though religiously-affiliated systems have an edge). Most are unaware that more than half of all hospitals (54%) are not-for-profit and distinctions between safety net, rural, DSH, teaching and other forms of NFP ownership are non-specific to their performance.

What’s clear to the majority is that hospitals are expensive and essential. They’re soft targets representing 31.1% of the health system’s total spend ($4.3 trillion in 2021) increasing 4.9% annually in the last decade while inflation and GDP growth were less.

So why are not-for-profit systems bearing the brunt of hospital criticism?

Simply put: many NFP systems act more like Big Business than shepherds of community health. In fact, 4 of the top 10 multi-hospital system operators is investor owned: HCA (184), CHS (84), LifePoint (84), Tenet (65). In addition, 3 others are in the top 50: Ardent (30), UHS (26), Quorum (22). So, corporatization of hospital care using private capital and public markets for growth is firmly entrenched in the sector exposing not-for-profit operators to competition that’s better funded and more nimble. And, per industry studies, not-for-profits tend to stay in markets longer and operate unprofitable services more frequently than their investor-owned competitors. But does this matter to insurers, community leaders, legislators, employers, hospital employees and physicians? Some but not much.

My take:

There are no easy answers for not-for-profit hospitals/heath systems. The issue is about more than messaging and PR. It’s about more than Medicare reimbursement (7.5% below cost), protecting programs like 340B, keeping tax exemptions and maintaining barriers against physician-owned hospitals. The issue is NOT about operating income vs. investment income: in every business, both are essential and in each, economic cycles impact gains/losses. Each of these is important but only band-aids on an open wound in U.S. healthcare.

Near-term (the next 2 years), opportunities for not-for-profit hospitals involve administrative simplification to reduce costs and improve the efficiencies and effectiveness of the workforce. Clinical documentation using ChatGPT/Bard-like tools can have a massive positive impact—that’s just a start. Advocacy, public education and Board preparedness require bigger investments of time and resources. But that’s true for every hospital, regardless of ownership. These are table stakes to stay afloat.

The longer-term issue for NFPs is bigger:

It’s about defining the future of the U.S. health system in 2030 and beyond—the roles to be played and resources necessary for it to skate to where the puck is going. It’s about defining the role played by private employers and whether they’ll pay 220% more than Medicare pays to keep providers and insurers solvent. It’s about how underserved and unhealthy people are managed. It’s about defining systemness in healthcare and standardizing processes. It’s about defining sources of funding and optimal use of resources. Not-for-profit systems should drive these discussions in the communities they serve and at a national level.

MedPAC’s 17 member Commission will play a vital role, but equally important to this design process are inputs from employers, consumers and thought leaders who bring fresh insight. Until then, not-for-profit health systems will be soft targets for unflattering media because protecting the status quo is paramount to insiders who benefit from its dysfunction. Incrementalism defined as innovation is a recipe for failure.

It’s time to begin a discussion about the future of the U.S. health system—all of it, not just high-profile sectors like not-for-profit hospitals/health systems who are currently its soft target.

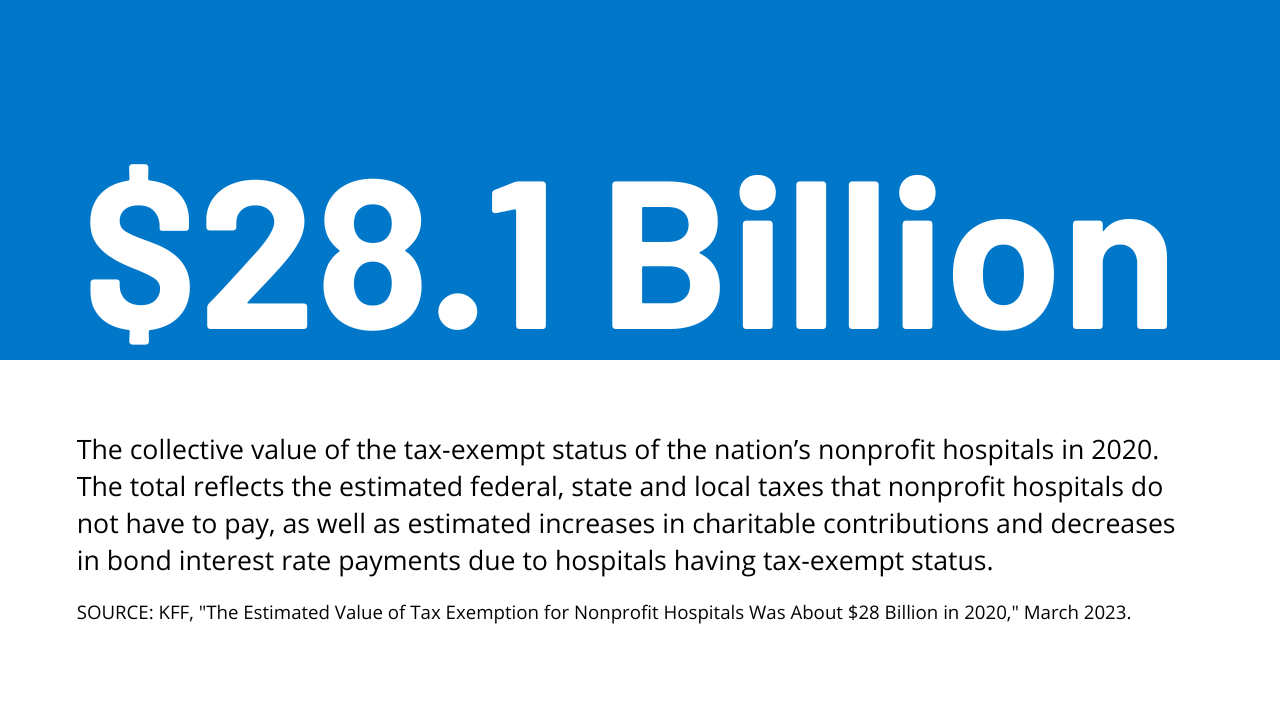

Over the years, somepolicymakers have questioned whether nonprofit hospitals—which account for nearly three-fifths (58%) of community hospitals—provide sufficient benefit to their communities to justify their exemption from federal, state, and local taxes.

This issue has been the subject of renewed interest in light of reports of nonprofit hospitals taking aggressive steps to collect unpaid medical bills, including suingpatients over unpaid medical debt, including patients who are likely eligible for financial assistance. Further, recent research indicates that nonprofithospitals devote a similar or smaller share of their operating expenses to charity care in comparison to for-profit hospitals. In light of these concerns, several policy ideas have been floated to better align the level of community benefits provided by nonprofit hospitals with the value of their tax exemption.

This data note provides an estimate of the value of tax exemption for nonprofit facilities based on hospital cost reports, filings with the Internal Revenue Service (IRS), and American Hospital Association (AHA) survey data (see Methods for additional details). We define the value of tax exemption as the benefit of not having to pay federal and state corporate income taxes, typically not having to pay state and local sales taxes and local property taxes, and any increases in charitable contributions and decreases in bond interest rate payments that might arise due to receiving tax-exempt status.

Results

The total estimated value of tax exemption for nonprofit hospitals was about $28 billion in 2020 (Figure 1). This represented over two-fifths (44%) of net income (i.e., revenues minus expenses) earned by nonprofit facilities in that year. To put the value of tax exemption in perspective, our estimate is similar to the total value of Medicare and Medicaid disproportionate share hospital (DSH) payments in the same year ($31.9 billion in fiscal year 2020) (i.e., supplemental payments to hospitals that care for a disproportionate share of low-income patients which are intended, in part, to offset the costs of charity care and other uncompensated care).

The estimated value of federal tax-exempt status was $14.4 billion in 2020, which represents about half (51%) of the total value of tax exemption. This is primarily due to the estimated value of not having to pay federal corporate income taxes ($10.3 billion). In addition, we assumed that individuals contribute more to tax-exempt hospitals because they can deduct donations from their income tax base ($2.5 billion) and issue bonds at lower interest rates because the interest is not taxed ($1.6 billion). Our estimates of changes in charitable contributions and interest rates on bonds only account for federal tax rates for simplicity and may therefore understate the total value of tax exemption because they do not account for the effects of state taxes.

The total estimated value of state and local tax-exempt status was $13.7 billion in 2020, which represents about half (49%) of the total value of tax exemption. This amount includes the estimated value of not having to pay state or local sales taxes ($5.7 billion), local property taxes ($5.0 billion) or state corporate income taxes ($3.0 billion).

The total estimated value of tax exemption (about $28 billion) exceeded total estimated charity care costs ($16 billion) among nonprofit hospitals in 2020 (Figure 2), though charity care represents only a portion of the community benefits reported by these facilities. Hospital charity care programs provide free or discounted services to eligible patients who are unable to afford their care and represent one of several different types of community benefits reported by hospitals.

The Internal Revenue Service (IRS) also defines community benefits to include unreimbursed Medicaid expenses, unreimbursed health professions education, and subsidized health services that are not means-tested, among other activities. One study estimated that the value of tax exemption exceeded the value of community benefits broadly for about one-fifth (19%) of nonprofit hospitals during 2011-2018 or about two-fifths (39%) when considering the incremental value of community benefits provided relative to for-profit facilities. Other research suggests that nonprofithospitalsdevote a similar or smaller share of their operating expenses to charity care and unreimbursed Medicaid costs—which accounted for most of the value of community benefits in 2017—when compared to for-profit hospitals.

The value of tax exemption grew from about $19 billion in 2011 to about $28 billion in 2020, representing a 45 percent increase (Figure 3). The value of tax exemption increased in most of the years (7 out of 9) in our analysis, though there was a notable decrease of $5.8 billion in 2018. The largest single-year increase was $4.1 billion in 2020. The large decrease in the value of tax exemption in 2018 coincided with the implementation of the Tax Cuts and Jobs Act of 2017, which permanently reduced the federal corporate income tax rate from 35 to 21 percent and therefore decreased the value of being exempt from federal income taxes.

The large increase in the value of tax exemption in 2020 overlapped with the start of the COVID-19 pandemic. This increase primarily reflects a large increase in aggregate net income for nonprofit hospitals in 2020. Although there were disruptions in hospital operations in 2020, hospitals received substantial amounts of government relief, and it is possible that other sources of revenue, such as from investment income, may have also increased. Increases in net income in turn increased the value of not having to pay federal and state income taxes.

Increases in the estimated value of tax exemption over time also reflect net income growth that preceded the pandemic as well as increases in estimated property values, supply expenses, and charitable contributions, each of which would carry tax implications if hospitals lost their tax-exempt status (e.g., with some supply expenses being subject to sales taxes). Even when setting aside the strong financial performance of nonprofit hospitals in 2020 as a potential outlier, total net income among nonprofit facilities increased substantially in the preceding years, before increasing further in 2020. Although we are not able to directly observe the value of the real estate owned by hospitals, the estimated value of exemption from local property taxes—which is based on our analysis of property taxes paid by for-profit hospitals—increased by 63 percent from 2011 to 2019. Finally, the supply expenses in our analysis increased by 44 percent and charitable contributions increased by 49 percent from 2011 to 2019.

Discussion

The estimated value of tax exemption for nonprofit hospitals increased from about $19 billion in 2011 to about $28 billion in 2020. The rising value of tax exemption means that federal, state, and local governments have been forgoing increasing amounts of revenue over time to provide tax benefits to nonprofit hospitals, crowding out other uses of those funds. This has raised questions about whether nonprofit facilities provide sufficient benefit to their communities to justify this tax benefit. Federal regulations require, among other things, that nonprofit hospitals provide some level of charity care and other community benefits as a condition of receiving tax-exempt status. However, a 2020 Government Accountability Office (GAO) report raised questions about whether the government has adequately enforced this requirement. Further, some argue that the federal definition of “community benefits” is too broad—e.g., by including medical training and research that could benefit hospitals directly—though others believe that the definition is too narrow. Most states have additional community benefit requirements for nonprofit or broader groups of hospitals—such as providing charity care to patients below a specified income threshold—though there is little information about the effectiveness of these regulations or the extent to which they are enforced.

Several policy ideas have been floated at the federal and state level that would increase the regulation of community benefits spending among nonprofit hospitals or among hospitals more generally. These include proposals to create or expand state requirements that hospitals provide charity care to patients below a specified income threshold, mandate that nonprofit hospitals provide a minimum amount of community benefits, establish a floor-and-trade system where hospitals would be required to either provide a minimum amount of charity care or subsidize other hospitals that do so, create mechanisms to increase the uptake of charity care, expandoversight and enforcement of community benefit requirements, replace current tax benefits with a subsidy that is tied to the value of community benefits provided, and introducereforms intended to better align community benefits with local or regional needs.

These policy options would inevitably involve tradeoffs. While they may expand the provision of certain community benefits, hospitals would incur new costs as a result, which could in turn have implications for what services they offer, how much they charge commercially insured patients, and how much they invest in the quality of care.

At a meeting with hospital system CEOs last Wednesday, one asked: “has healthcare reached the tipping point?” I replied ‘not yet but it’s getting close.’

I iterated factors that make these times uniquely difficult in every sector:

An uncertain economy that’s unlikely to fully recover until next year.

The growth of Medicaid and Medicare coverage that shifts their financial shortfall to employers and taxpayers who are fed up and pushing back.

A vicious political environment that rewards partisan brinksmanship and focus-group tested soundbites to manipulate voters on complex issues in healthcare.

The growing domination of Big Business in each sector that have used acquisitions + corporatization to their advantage.

The widening role of private equity in funding non-conventional solutions that disrupt the status quo (and the uncertain future for many of these).

The federal courts system that’s increasingly the arbiter over access, fairness, quality and freedoms in healthcare.

The lingering impact of the pandemic.

And growing public disgust and distrust as the system’s altruism and good will is undermined by pervasive concern for profit.

Unprecedented! But events like those last week prompt hitting the pause button: not everyone pays attention to healthcare like many of us. The slaughter of 6 innocents in Nashville hit close to home: it’s about guns, mental health and life and death. The appeal of tech-giants to press the pause button on Generative AI for at least 6 months was sobering. The ravage of tornados that left thousands insecure without food, housing or hope seemed unfair. Mounting tensions with Russia and complex negotiations with China that reminded us that the U.S. competes in a global economy. And President Trump’s court appearance tomorrow will stoke doubt about our justice system at a time when it’s role in healthcare and society is expanding.

I am a healthcare guy. I am prone to see the world through the lens of the U.S. health industry and keen to understand its trends, tipping points and future. There’s plenty to watch: this week will be no exception. The punch list is familiar:

Medicaid coverage: Many will be watching the fallout of from state redetermination requirements for Medicaid coverage starting as soon as this week with disenrollment in Arizona, Arkansas, Idaho, New Hampshire and South Dakota.

Medicare Advantage: Health insurers will be modifying their Medicare Advantage strategies to adapt to CMS’ risk adjustment and Value-based Insurance Design modifications announced last week.

Prescription drug prices: PBMs and drug companies will face growing skepticism as Senate and House committees continue investigations about price gauging and collusion. Hospitals will be making adjustments to higher operating losses as states cut their Medicaid rolls.

Technology: The 7500 VIVA attendees will be doing follow-up to secure entrées for their technologies and solutions among prospective buyers.

Physicians: And physicians will intensify campaigns against insurers and hospitals now seen as adversaries while lobbying Congress for more money and greater income opportunities i.e., physician-owned hospitals.

Hospitals: On the offense against site-neutral payments, physician owned hospitals, drug prices and inadequate reimbursement from health insurers.

All will soldier on but the food fights in healthcare and broader headwinds facing the industry suggest a tipping point might be near.

I am not a fatalist: the future for healthcare is brighter than its past, but not for everyone. Strategies predicated on protecting the past are obsolete. Strategies that consider consumers incapable of active participation in the delivery and financing of their care are archaic. Strategies that depend on unbridled consolidation and opaque pricing are naïve. And strategies that limit market access for non-traditional players are artifacts of the gilded age gone by when each sector protected its own against infidels outside.

These times call for two changes in every board room and C Suite in of every organization in healthcare:

Broader vision: Understanding healthcare’s future in the broader context of American society, democracy and capitalism: Beltway insiders and academics prognosticate based on lag indicators that are decreasingly valid for forecasting. Media pundits on healthcare fail to report context and underpinnings. Management teams are operating under short-term financial incentives lacking longer-term applicability. Consultants are telling C suites what they want to hear. And boards are being mis-educated about trends of consequence that matter. Understanding the future and building response scenarios is out of sight and out of mind to insiders more comfortable being victims than creators of the new normal.

Board leadership: Equipping boards to make tough decisions: Governance in healthcare is not taken seriously unless an organization’s investors are unhappy, margins are shrinking or disgruntled employees create a stir. Few have a systematic process for looking at healthcare 10 years out and beyond their business. Every Board must refresh its thinking about what tomorrow in healthcare will be and adjust. It’s easier for board to approve plans for the near-term than invest for the long-term: that’s why outsiders today will be tomorrow’s primary incumbents.

So, is U.S healthcare near its tipping point? I don’t know for sure, but it seems clear the tipping point is nearer than at any point in its history. It’s time for fresh thinking and new players.

It feels like governance questions are coming to the fore in a lot of places these days, at least judging by several recent conversations we’ve had with health system CEOs. Probably not surprising, given the number of potential mergers and other partnerships under consideration.

As one CEO told us, growth byM&A raises particularly thorny issues for a not-for-profit system board. “Our governance structure grew out of a single hospital board, which was made up of community members and local physician leaders,” he told us. As the system acquired hospitals in adjacent markets, the combined board took on a representational character—each hospital had local stakeholders involved in governance. “Now we’re talking about merging with an out-of-state system, and our board suddenly seems way too parochial and unsophisticated. Everyone’s still asking what’s in it for their community.” That’s a frustration we hear frequently.

There are legitimate reasons why a tax-exempt community institution should have local representation on the board, advocating for local priorities and resources. But a larger, multi-state board must also oversee the entire portfolio of assets, and make trade-offs across markets, sometimes making decisions that favor one hospital over another.

The larger system board also has a greater need for sophistication, both on business and healthcare issues, as its members are often responsible for billions of dollars of assets. What frequently results from this tension is a nesting series of system and community boards, with varying degrees of accountability—a recipe for tangled, lengthy decision processes, and an enormous time-sink for senior system executives. We’re keeping our eye out for next-generation solutions to the governance question in healthcare—let us know what you’re seeing.

Published this week in the New York Times, this article describes the decaying state of Greenwood Leflore Hospital, a 117 year-old facility in the Mississippi Delta that may be within months of closure. While rural hospitals across the country are struggling, Mississippi’s firm opposition to Medicaid expansion has exacerbated the problem in that state, by depriving providers of an additional $1.4B per year in federal funds. Instead, only a few of the state’s 100-plus hospitals actually turn an annual profit, and uncompensated care costs are almost 10 percent of the average hospital’s operating costs.

Despite a dozen or more hospitals at imminent risk of closure, Mississippi officials would rather use the state’s $3.9B budget surplus to lower or eliminate the state income tax.

The Gist:Expanding Medicaid doesn’t just reduce rates of uncompensated care provided by hospitals, it changes the volume and type of care they provide.

Further, Medicaid expansion has been found to result in significant reductions in all-cause mortality.

Ensuring that low-income residents in Mississippi and other non-expansion states have access to Medicaid would allow providers to administer more preventive care and manage chronic diseases more effectively, before costly exacerbations require hospitalization.

Hard-pressed to come up with significant savings to reduce the deficit, some Senate Republicans are taking a closer look at reforms to Medicare Advantage in light of reports that insurance companies are collecting billions of dollars in extra profits by over-diagnosing older patients.

But the idea of cracking down on Medicare Advantage overpayments to insurance companies divides Republicans, who have traditionally championed the program.

Proponents of Medicare Advantage reform anticipated it will face strong opposition from the insurance industry, one of the most powerful special interest groups in Washington.

Sen. Bill Cassidy (La.), the top-ranking Republican on the Senate Health, Education, Labor and Pensions Committee, is leading the push to reduce Medicare overpayments.

“Medicare is going insolvent. If we don’t do anything, it’s going to go insolvent. We have a whole package of things, all of them bipartisan, and we’re doing it essentially to have something out there so that if somebody decides to do something, there will be things that are examined, considered and bipartisan” to vote on, he said.

“I come up with lots of stuff. We thought it through policy and think it’s policy that can make it all the way through,” he said.

Cassidy’s office says his bill could extend the solvency of Medicare by saving as much as $80 billion in federal funds over the next decade without cutting benefits.

He emphasizes that it would not cut Medicare Advantage benefits, but critics of the legislation are sure to challenge that claim.

“We’re not undermining Medicare Advantage,” he said.

“In fact, I would say this is a better alternative than what CMS is doing by rule,” he added, referring to a new rule-making action by the Biden administration to recover overpayments in Medicare Advantage through the Centers for Medicare & Medicaid Services.

The Medicare Payment Advisory Panel estimates that Medicare Advantage plans collected $124 billion in overpayments from 2008 to 2023. They collected an estimated $44 billion overpayments in 2022 and 2023 alone, according to MedPAC.

Unlike traditional fee-for-service Medicare, Medicare Advantage plans are offered by private companies. Both are funded by taxpayers through general revenues, payroll taxes and beneficiaries’ premiums.

Cassidy is also leading a bipartisan working group to reform Social Security to extend its solvency. Members include Sens. Angus King (I-Maine) and Mitt Romney (R-Utah).

“To have a significant impact on fiscal policy, you’d have to look at entitlements,” said Romney, who called Medicare Advantage “an area we’re going to be looking at very shortly — the committee will be looking at Medicare Advantage,

the cost of Medicare Advantage …. It’s become more expensive than the old fee-for-service Medicare.”

In a follow-up interview Thursday, Romney said senators are also looking at reforms to Pharmacy Benefit Managers, the companies that serve as middle-men between drug manufacturers, insurance companies and pharmacies.

Romney said, “in the past, Medicare Advantage has been a lower-cost way of providing Medicare than fee-for-service Medicare.”

“If that’s changing, I’d like to understand why and make sure we don’t create impediments to the lower-cost Medicare Advantage,” he said.

Sen. Mike Braun (R-Ind.) said Medicare Advantage overpayment “definitely” is a “reform issue.”

“I’ve been the loudest voice on reforming health care and that’s a commonsense idea,” he said. “Whatever it takes to bring down health care costs.

“I’m one of the most free-market people here, but the health care industry is not a free market. It’s like an unregulated utility,” he said. “There’s so much opaqueness.”

But some Republicans are already trying to paint efforts to reduce overpayments as cuts to Medicare Advantage.

“The problem with Medicare Advantage is President Biden is cutting $540 per member per year. That’s the problem. Medicare Advantage has been very successful,” said Sen. Roger Marshall (R-Kan.), an OB/GYN who practiced medicine for more than 25 years.

National Republican Senatorial Committee Chairman Steve Daines (R-Mont.) accused Biden of “proposing Medicare Advantage cuts” when the president accused some Republicans of wanting to sunset Medicare at his Feb. 7 State of the Union address.

Medicare Advantage is getting more popular among Democrats as well as the number of blue state enrollees in the program soars. The number of Americans enrolled in Medicare Advantage has nearly doubled over the last 12 years, according to the Kaiser Family Foundation.

Cassidy’s proposal, which he introduced with progressive Sen. Jeff Merkley (D-Ore.) on Monday, could draw broader interest from Republicans.

Sen. John Cornyn (R-Texas), an adviser to the Senate GOP leadership, called Medicare Advantage a “success.”

“That doesn’t mean that it should be immune from oversight, so I’ll be interested to see what they have to say,” he said.

Cassidy and Merkley say that Medicare Advantage plans have a financial incentive to make beneficiaries appear sicker than they are because they are paid a standard rate based on the health of individual patients. Their bill, the No Unreasonable Payment, Coding or Diagnoses for Elderly (No Upcode Act) would require risk models based on more extensive diagnostic data over a period of two years.

The goal is to narrow the disparity in how patients are assessed by traditional Medicare and Medicare Advantage.

Studies and audits conducted by CMS and the Department of Health and Human Services’ inspector general found that insurance companies collected billion of dollars in overpayments because of diagnoses that were not later supported by enrollees’ medical records.

The Kaiser Family Foundation reported in August that more than 28 million people — or about 48 percent of the eligible Medicare population — were enrolled in Medicare Advantage plans in 2022. They accounted for $427 billion or 55 percent of total federal Medicare spending.