U.S. Hospital YTD Operating Margin Index November 2021-December 2023

The observations and questions from this chart are both interesting and required reading for hospital executives:

Why were hospitals profitable at the 4% plus level through the worst of the 2021 Covid period?

What exactly happened between December of 2021 and January of 2022 that resulted in a profitability decrease from a positive 4.2% to a negative 3.4%?

Despite the best efforts of hospital executives, overall operating margins were negative throughout calendar year 2022 and did not return to positive territory until March of 2023.

Hospital margins remained positive throughout 2023 and into 2024. However, overall margins have remained below those experienced in both 2021 and in the pre-Covid year of 2019.

The above questions and observations have proven interesting, and the ongoing numbers have proven quite useful in many quarters of healthcare. But recently I was talking with Erik Swanson, who is the leader of the Kaufman Hall Flash Report and our executive behind the data, numbers, and statistics. Erik and I were speculating about all of the above observations, but our key speculation was whether the 2023 operating margin results actually reflected a hospital financial turnaround or, in fact, were there “numbers behind the numbers” that told a different and much more nuanced story. So Erik and I asked different questions and took a much deeper dive into the Flash Report numbers. The results of that dive were quite telling:

Too many hospitals are still losing money. Despite the fact that the Operating Margin Index median for 2023 and into 2024 was over 2%, when you look harder at the Flash Report data, you find that 40% of American hospitals continue to lose money from operations into 2024.

There is a group of hospitals that have substantially recovered financially. Interestingly, the data shows over time that the high-performing hospitals in the country are doing better and better. They are effectively pulling away from the pack.

This leads to the key question: Why are high-performing hospitals doing better? It turns out that several key strategic and managerial moves are responsible for high-performing hospitals’ better and growing operating profitability:

Outpatient revenue. Hospitals with higher and accelerating outpatient revenue were, in general, more profitable.

Contract labor. Hospitals that have lowered their percentage of contract labor most quickly are now showing better operating profitability.

An important managerial fact.The Flash Report found that hospitals with aggressive reductions in contract labor were also correlated to rising wage rates for full-time employees. In other words, rising wage rates have appeared to attract and retain full-time staff which, in turn, has allowed those hospitals to reduce contract labor more quickly, all of which has led to higher profitability.

Average length of stay.No surprise here. A lower average length of stay is correlated to improved profitability. Those hospitals that have hyper-focused on patient throughput, which has led to appropriate and prompt patient discharge, have also proven this to be a positive financial strategy.

Lower financial performers have financially stagnated throughout the pandemic. The data shows that throughout the pandemic, hospitals with good financial results improved those results, but of more consequence, hospitals with poor financial performance saw that performance worsen. The Flash Report documents that the poorest financially performing hospitals currently show negative operating margins ranging from negative 4% to negative 19%. Continuation of this level of financial performance is not only unstainable but also makes crucial re-investment in community healthcare impossible.

The urban hospital/rural hospital myth. A popular and often quoted hospital comparison is that there is an observable financial divide between urban and rural hospitals. Erik Swanson and I found that recent data does not support this common perception. When you compare “all rurals” to “all urbans” on the basis of average operating margin, no statistically significant difference emerges. However, what does emerge—and is a very important statistical observation—is that the lowest performing 20% of rural hospitals are, in fact, generating much lower margins then their urban counterparts this year. It is at this lowest level of rural hospital performance where the real damage is being done.

Rural hospitals and obstetrics. The data does confirm one very important American healthcare issue: Obstetrics and delivery services are one of the leading money losers of all hospital service offerings. And the data further confirms that rural hospitals are closing obstetric departments with more frequency in order to protect the financial viability of the overall rural hospital enterprise. This is a health policy issue of major and growing consequence.

The point here is that data, numbers, and statistics matter both to setting long-term social health policy agendas and to the strategic management of complex provider organizations. But the other point is that the quality and depth of the analysis is an equally important part of the process. A first glance at the numbers may suggest one set of outcomes. However, a deeper, more careful and penetrating analysis may reveal critical quantitative conclusions that are much more telling and sophisticated and can accurately guide first-class organizational decision-making. Hopefully the analytics here are a good example of this very point.

Walgreens announced this week that it will be shutting down all of its Florida-based VillageMD primary care clinics. Fourteen clinics in the Sunshine State have already closed, with the remaining 38 expected to follow by March 15.

This move comes in the wake of a $1B cost-cutting initiative announced by Walgreens executives last fall, which included plans to shutter at least 60 VillageMD clinics across five markets in 2024.

Last month VillageMD exited the Indiana market, where it was operating a dozen clinics.

Despite downsizing its primary-care footprint, Walgreens says it remains committed to its expansion into the healthcare delivery sector, having invested $5.2B in VillageMD in 2021 and purchased Summit Health-CityMD for $9B through VillageMD in 2023.

The Gist:Having made significant investments in provider assets, Walgreens now faces the difficult task of creating an integrated and sustainable healthcare delivery model, which takes time.

Unlike long-established healthcare providers who feel more loyal to serving their local communities, nontraditional healthcare providers like Walgreens can more easily pick and choose markets based on profitability.

While this move is disruptive to VillageMD patients in Florida and the other markets it’s exiting, Walgreens seems to be answering to its investors, who have been dissatisfied with its recent earnings.

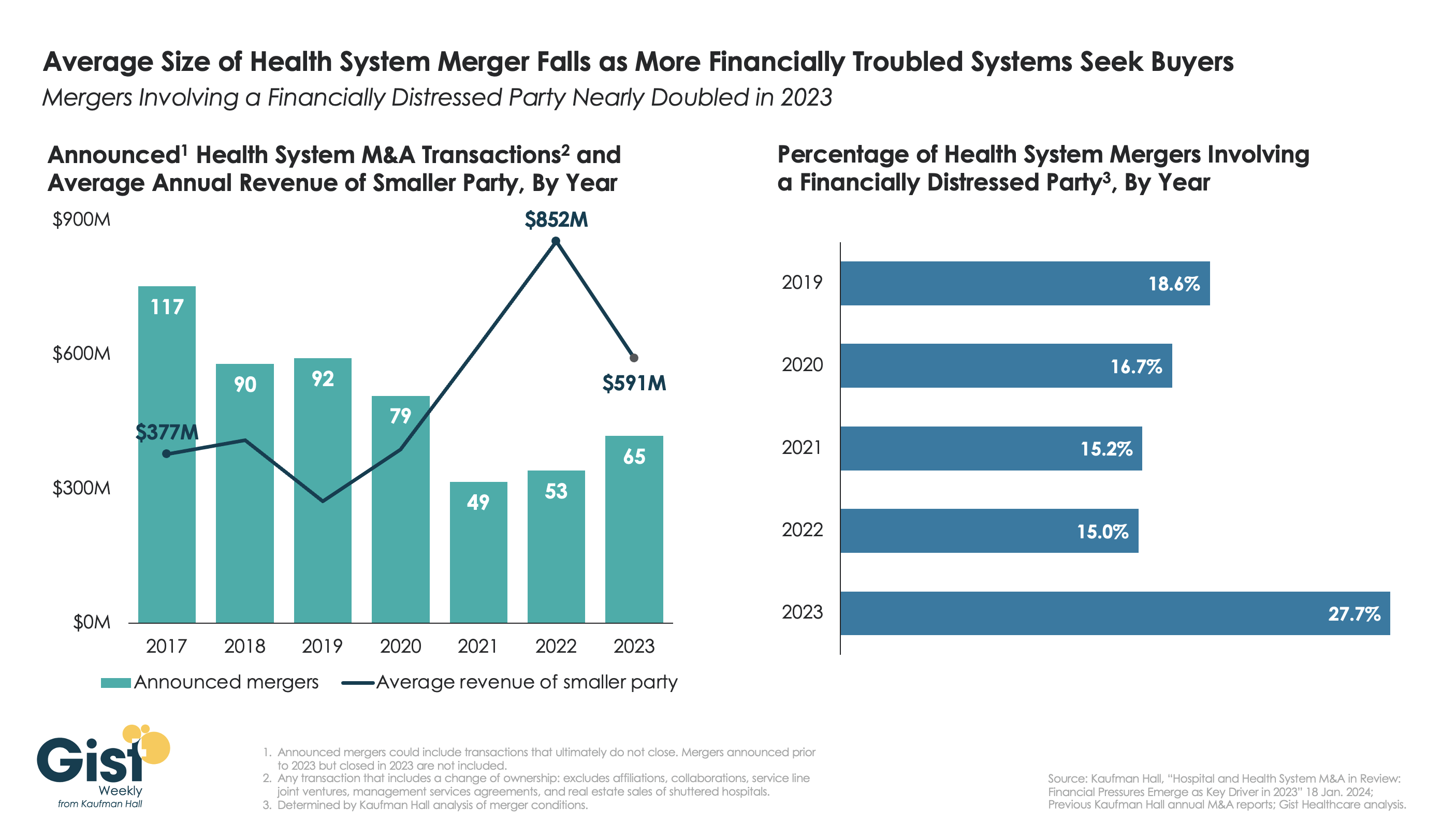

This week’s graphic highlights data from Kaufman Hall’s recently released 2023 Hospital and Health System M&A Report on the current dynamics in health system mergers and acquisitions (M&A) activity.

After a slowdown during the pandemic, 2023 saw an uptick in M&A activity with 65 announced transactions, the most since 2020. Continuing the trend of the past two years, the number of announced “mega mergers,” in which the smaller party had at least $1B in annual revenue, represented more than a tenth of total announced transactions.

However, the average size of mergers fell in 2023, as financial distress emerged as a key driver of M&A activity. The percent of mergers involving a financially distressed party spiked to nearly 28 percent in 2023, almost double the level seen in prior years.

CARES Act funding had buoyed some health systems’ balance sheets through the pandemic, but with the end of federal aid, more systems needed to seek shelter through scale.

With the median hospital operating margin still barely hitting two percent, we anticipate this heightened level M&A activity to continue in 2024 as health systems search for stronger partners that can help them stabilize financially.

On Monday, Fitch Ratings, the New York City-based credit rating agency, released a report predicting that the US not-for-profit hospital sector will see average operating margins reset in the one-to-two percent range, rather than returning to historical levels of above three percent.

Following disruptions from the pandemic that saw utilization drop and operating costs rise, hospitals have seen a slower-than-expected recovery.

But, according to Fitch, these rebased margins are unlikely to lead to widespread credit downgrades as most hospitals still carry robust balance sheets and have curtailed capital spending in response.

The Gist:As labor costs stabilize and volumes return, the median hospital has been able to maintain a positive operating margin for the past ten months.

But nonprofit hospitals are in a transitory period, one with both continued challenges—including labor costs that rebased at a higher rate and ongoing capital restraints—and opportunities—including the increase in outpatient demand, which has driven hospital outpatient revenue up over 40 percent from 2020 levels.

While the future margin outlook for individual hospitals will depend on factors that vary greatly across markets, organizations that thrive in this new era will be the ones willing to pivot, take risks, and invest heavily in outpatient services.

Creating a great rating agency presentation is imperative to telling your story. I’ve probably seen a thousand presentations across the past three decades and I can say without a doubt that a great presentation will find its way into the rating committee. Show me a crisp, detailed, well-organized presentation, and I’ll show you a ratings analyst who walks away with high confidence that the management team can navigate the industry challenges ahead.

During the pandemic, Kaufman Hall recommended that hospitals move financial performance to the top of the presentation agenda. Better presentations chronicled the immediate, “line item by line item” steps management was taking to stop the financial bleeding and access liquidity. We still recommend this level of detail in your presentations, but as many hospitals relocate their bottom line, management teams are now returning to discussing longer-term strategy and financial performance in their presentations.

Beyond the facts and figures, many hospitals ask me what the rating analysts REALLY want to know. Over those one thousand presentations I’ve seen, the presentations that stood out the most addressed the three themes below:

What makes your organization essential? Hospitals maintain limited price elasticity as Medicare and Medicaid typically comprise at least half of patient service revenue, leaving only a small commercial slice to subsidize operations. The ability to negotiate meaningful rate increases with payers will largely rest on the ability to prove why the hospital is a “must-have” in the network. In other words, a health plan that can’t sell a product without a hospital in its network is the definition of essential. This conversation now also includes Medicare Advantage plans as penetration rates increase rapidly across the country. Essentiality may be demonstrated by distinct services, strong clinical outcomes and robust medical staff, multiple access points across a certain geography, or data that show the hospital is a low-cost alternative compared to other providers. Volume trends, revenue growth, and market share show that essentiality. A discussion on essentiality is particularly needed for independent providers who operate in crowded markets.

What makes your financial performance durable? Many hospitals are showing a return to better performance in recent quarters. Showing how your organization will sustain better financial results is important. Analysts will want to know what the new “run rate” is and why it is durable. What are the undergirding factors that make the better margins sustainable? Drivers may include negotiated rate increases from commercial payers and revenue cycle improvements. On the expense side, a well-chronicled plan to achieve operating efficiencies should receive material airtime in the presentation, particularly regarding labor. It is universally understood that high labor costs are a permanent, structural challenge for hospitals, so any effort to bend the labor cost curve will be well received. Management should also isolate non-recurring revenue or expenses that may drive results, such as FEMA funds or 340B settlements. To that end, many states have established new direct-to-provider payment programs which may be meaningful for hospitals. Expect questions on whether these funds are subject to annual approval by the state or CMS. The analysts will take a sharpened pencil to a growing reliance on these funds.

The durability of financial performance should be represented with highly detailed multi-year projections complete with computed margin, debt, and liquidity ratios. Know that analysts will create their own conservative projections if these are not provided, which effectively limits your voice in the rating committee.

We also recommend that hospitals include a catalogue of MTI and bank covenants in the presentation. Complying with covenants are part of the agreement that hospitals make with their lenders, and it is the organization’s responsibility to report how it’s performing against these covenants. General philosophy on headroom to covenants also provides insight to management’s operating philosophy. For example, is it the organization’s goal to have narrow, adequate, or ample headroom to the covenants and why? As the rating agencies will tell you, ratings are not solely based on covenant performance, but all rating factors influence your ability to comply with the covenants.

What makes your capital plan affordable? Every rating committee will ask what the hospital’s future capital needs are and how those capital needs will be supported by cash flow, also known as “capital capacity.” To answer that question, a hospital must understand what it can afford, based on financial projections. Funding sources may require debt, which requires a debt capacity analysis with goals on debt burden, coverage, and liquidity targets. Over the years, better presentations explain the organization’s capital model, outline the funding sources, and discuss management’s tolerance for leverage.

There is always a lot to cover when meeting with the rating agencies and a near endless array of metrics and indicators to provide. As I’ve written before, how you tell the story is as important as the story itself. If you can weave these three themes throughout the presentation, then you will have a greater shot at having your best voice heard in rating committee.

Companies grappling with liquidity concerns are looking to cut costs and streamline operations, according to a new survey.

Dive Brief:

Over three-quarters of healthcare chief financial officers expect to see profitability increases in 2024, according to a recent survey from advisory firm BDO USA. However, to become profitable, many organizations say they will have to reduce investments in underperforming service lines, or pursue mergers and acquisitions.

More than 40% of respondents said theywill decrease investments in primary care and behavioral health services in 2024, citing disruptions from retail players. They will shift funds to home care, ambulatory services and telehealth that provide higher returns, according to the report.

Nearly three-quarters of healthcare CFOs plan to pursue some type of M&A deal in the year ahead, despite possible regulatory threats.

Dive Insight:

Though inflationary pressures have eased since the height of the COVID-19 pandemic, healthcare CFOs remain cognizant of managing costs amid liquidity concerns, according to the report.

The firmpolled 100 healthcare CFOs serving hospitals, medical groups, outpatient services, academic centers and home health providers with revenues from $250 million to $3 billion or more in October 2023.

Just over a third of organizations surveyed carried more than 60 days of cash on hand. In comparison, a recent analysis from KFF found that financially strong health systems carried at least 150 days of cash on hand in 2022.

Liquidity is a concern for CFOs given high rates of bond and loan covenant violations over the past year. More than half of organizations violated such agreements in 2023, while 41% are concerned they will in 2024, according to the report.

To remain solvent, 44% of CFOs expect to have more strategic conversations about their economic resiliency in 2024, exploring external partnerships, options for service line adjustments and investments in workforce and technology optimization.

Most organizations are interested in exploring sales, according to the report. Financially struggling organizations are among the most likely to consider deals. Nearly one in three organizations that violated their bond or loan covenants in 2023 are planning a carve-out or divestiture this year. Organizations with less than 30 days of cash on hand are also likely to consider carve-outs.

Organizations will also turn to automation to cut costs. Ninety-eight percent of organizations surveyed had pilotedgenerative AI tools in a bid to alleviate resource and cost constraints, according to the consultancy.

“Healthcare leaders believe AI will be essential to helping clinicians operate at the top of their licenses, focusing their time on patient care and interaction over administrative or repetitive tasks,” authors wrote. Nearly one in three CFOs plan to leverage automation and AI in the next 12 months.

However, CFOs are keeping an eye on the risks. As more data flows through their organizations, they are increasingly concerned about cybersecurity. More than half of executives surveyed said data breaches are a bigger risk in 2024 compared to 2023.

“We have a collaborative culture; it’s one of our system’s core values. But it takes us far too long to make decisions.” A health system CEO made this comment at a recent meeting, giving voice to a dilemma many system executives are no doubt facing. Of course, leaders want their teams to collaborate—in any important decision, we want to hear different voices, consider diverse points of view, and incorporate various areas of expertise.

On the other hand, collaboration takes time, which we don’t have right now.It also can add complexity, be the enemy of clear direction, and muddy accountability. This CEO went on to make an essential connection: “My concern is that this protracted decision making isn’t just a process problem, but that it’s showing up in our results.

Take performance improvement—we all quickly agreed we need to cut costs, but it’s taking far too long for us to act, and I fear we’ll have trouble holding the new line over time.” She further mused

“I wonder if this problem is, at least in part, due to how we make decisions. We don’t make them quickly enough, they aren’t clear enough, and we don’t have the most effective system of accountability.”

On one hand, traditional hospital culture is rightly grounded in the safety, hierarchy, and tradition of a do-no-harm world. But on the other hand, today’s economic, technological, and competitive environments require an approach to operations, revenue, and growth that has the aggressiveness of a Fortune 50 company. This should not be an either-or situation. Health systems can uphold a culture of safety while also fostering nontraditional values that will drive the organization assertively toward the future – all while committing to change.

For many providers, 2023 provided a return to profitability (albeit at modest levels) following the devastating operating and investment losses experienced in 2022.Kaufman Hall’s National Hospital Flash Report data illustrated generally improving operating margins throughout the year, leveling off at 2.0% in November on a year-to-date basis.

This level of performance is commendable given 2022 and early 2023 margins, although it is still well below the 3% to 4% range which we believe is needed for long-term sustainability in the not-for-profit healthcare world. We may well have reached a point of stability with respect to operating performance, but at a lower level.

The question for hospital and health system leaders is whether this level of operating stability provides sustainability?

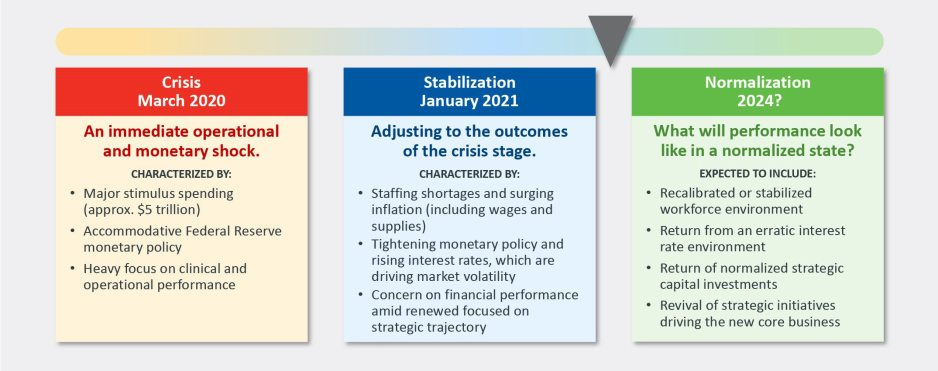

From stabilization to normalization

Since the pandemic began in 2020, the progress of recovery has been viewed over three phases: crisis, stabilization, and normalization. In last year’s outlook, we noted that we were in the midst of a potentially multi-year stabilization phase, which would continue to be marked with volatility—including ongoing labor market dislocations, inflationary pressures, and restrictive monetary policies. As we enter 2024, there are signs that we are now at the bridge between stabilization and normalization (Figure 1).

Figure 1: The Three Phases of Recovery from the Covid Pandemic

“The question for hospital and health system leaders is whether that level of stability provides sustainability?”

These signs include evidence that the first two indicators for normalization—a recalibrated or stabilized workforce environment and a return from an erratic interest rate environment—are coming into place. In our 2023 State of Healthcare Performance Improvement survey, respondents indicated that the spike in contract labor utilization that has been a dominant factor in operating expense increases was subsiding. Sixty percent of respondents said that utilization of contract labor was decreasing, and 36% said it was holding steady. Only 4% noted an increase in contract labor usage. Overall employee cost inflation seems to be subsiding as well: for all three labor categories in our survey (clinical, administrative, and support services), more organizations were able to hold salary increases to the 0% – 5% range in 2023 than in 2022.

There is good news on the interest rate front as well. After a series of rate increases in 2023, the Federal Reserve has held steady the last six months and has signaled rate cuts in 2024. Inflation has cooled markedly (albeit not yet at target levels), and employment rates have held steady. The Fed may have achieved a “soft landing” that satisfies its dual mandate of stable prices and maximum sustainable employment. Borrowing costs for not-for-profit hospital issuers have declined nearly 100 basis points in the last two months and we are expecting a return to more normal issuance levels in the first half of 2024.

There are other indications of normalization, including in the rating agencies’ outlooks for 2024. Regardless of the headline, all saw significant improvement in healthcare performance 2023.

The final answer to the question of whether the healthcare industry is entering the normalization phase likely will hinge on the last two indicators. Will we see a return of normalized strategic capital investments, and will we see a revival of strategic initiatives driving the core business (perhaps newly imagined)?

In effect, are health care systems simply surviving or are they thriving?

Looking forward, several factors could either bolster or undermine healthcare leaders’ confidence and willingness to resume a more normal level of investment in both capital needs and strategic growth. These include:

Politics and the 2024 elections. When North Carolina—a state that has traditionally leaned “red”—decided to opt into the Affordable Care Act’s (ACA’s) Medicaid expansion in 2023, it seemed that political debates over the ACA might be in the rearview mirror. But last November, former president Trump—currently the leading candidate for the Republican presidential nomination after strong wins in the Iowa caucuses and New Hampshire primary—indicated his intent to replace the ACA with something else. President Biden is now making protection and expansion of the ACA a key part of his 2024 campaign. What had appeared to be a settled issue may be a significant point of contention in the 2024 presidential election and beyond.

Although we do not anticipate any significant healthcare-related legislation in advance of the 2024 elections, healthcare leaders should be prepared for renewed attention to the costs of government-funded healthcare programs leading up to and following the elections. The national debt has increased rapidly over the past 20 years, tripling from $11 trillion in 2003 to $33 trillion in 2023. If the deficit and national debt become an important issue in the election, a move toward a balanced budget—akin to the Balanced Budget Act of 1997—post election could lead to further cuts to Medicare and Medicaid.

Temporary relief payments. Health systems continue to receive one-time cash infusions through the 340B settlement, Federal Emergency Management Agency (FEMA) payments and other governmental programs. Approximately 1,600 hospitals have or will be receiving a lump-sum payment to compensate them for a change in the Department of Health & Human Services’ (HHS’s) reimbursement rates for the 340B program from 2018 to 2022, which was ruled unlawful by the Supreme Court in a 2022 decision. The total amount to be distributed is approximately $9 billion and began hitting bank accounts in January 2024.

But what the right hand giveth, the left hand taketh away. Budget neutrality requirements will force HHS to recoup this offset—amounting to approximately $7.8 billion—which it will do by reducing payments for non-drug items and services to all Outpatient Prospective Payment System (OPPS) providers by 0.5% until the offset has been fully recouped, beginning in calendar year 2026. HHS estimates that this process will take approximately 16 years. Is this a harbinger of lower payments on other key governmental programs?

Many hospitals also continue to receive Covid-related payments from FEMA for expenses occurred during the pandemic. In addition, state supplemental payments—especially under Medicaid managed care and fee-for-service programs—are providing some relief. The Centers for Medicare & Medicaid Services has issued a proposed rule, however, that would limit states’ use of provider-based funding sources, such as provider taxes, and cap the rate of growth for state-directed payments.

As all of these payment programs dry up over the next few years, hospitals will need to replace the revenue and/or get leaner on the expense side in order to maintain today’s level of performance.

The hollowing of the commercial health insurance market. Our colleague, Joyjit Saha Choudhury, recently published a blog on the hollowing of the commercial health insurance market, driven by long-term concerns over the affordability of healthcare. While volumes have been recovering to pre-pandemic levels, this hollowing threatens the loss of the most profitable volumes and will pressure hospitals and health systems to create and deliver value, compete for inclusion in narrow networks, and develop more direct relationships with the employer community.

Related, the growing penetration of Medicare Advantage plans is reducing the number of traditional Medicare beneficiaries. Many CFOs report that these programs can be the most difficult with which to work given their high denial rates and required pre-authorization rates. A new rule requiring insurers to streamline prior authorizations for Medicare Advantage, Medicaid, and Affordable Care Act plans may help alleviate this issue; however, it will be incumbent upon management teams to stay ahead of them. Aging demographics are also reducing the percentage of commercially insured patients for many hospitals and health systems, further exacerbating the problem. This combination of fewer commercial patients (who often subsidize governmental patients) and more pressure on receiving the duly owed commercial revenue threatens to be an ongoing headache for management teams.

Ongoing impact of the Baby Boom generation. Despite the good news on inflation—and indications that the Fed may begin lowering interest rates in 2024—the economy is by no means out of the woods yet. The Baby Boom generation, which holds more than 50% of the wealth in the U.S. and is seemingly price agnostic, still has many years of spending ahead, in healthcare and general purchasing. This will likely continue to pressure inflation, especially in the healthcare sector, where demand will continue to grow. As the generation starts to shrink, the resulting wealth transfer will be the largest ever in our country’s history and have profound (and unforeseen) consequences on the overall economy and healthcare in general.

In sum, these other factors will continue to affect the sector (both positively and negatively) and require health system management teams to navigate an everchanging world. While many signs point toward short-term relief, the longer-term challenges persist. Improvements in the short term may, however, provide the opportunity to reposition organizations for the future.

How hospitals and health systems should respond

Healthcare leaders should view ongoing uncertainty in the political and economic climate as a tailwind as much as a headwind. This uncertainty, in other words, should be a motivation to put in place strategies that will buffer healthcare organizations from potential bumps in the road ahead. Setting balance sheet strategy should be a part of an organization’s planning process.

How an organization sets that strategy, measures its performance, and makes improvements will set apart top-performing organizations.

Although heightened debt issuance early in 2024 signals a return for many systems to a climate of investment, there is still limited energy around strategy and debt conversations in many boardrooms, especially in those organizations where financial improvement continues to lag. The last two years have illustrated that hospitals and health systems will not be able to cut their way to profitability. Lackluster performance cannot and will not improve without some level of strategic change, whether it is through market share gains, payer mix shift, or operational improvements. This strategic change requires investment and investment requires capital. Capital can be obtained in many forms—whether through growth in capital reserves, improved cash flow, or new debt issuance—but is essential for change. Reengaging in conversations about strategy and growth should be an imperative in 2024 and will require reexamining how that growth is funded.

Healthcare leaders should engage their partners as they continue or refocus on:

Changing the conversation from debt capacity to capital capacity. Management teams need to determine what they can afford to spend on capital if the new normal of cash flow will be constrained going forward. Capital capacity is and should be agnostic to the source of that capital, such as debt, cash flow from operations, or liquidity reserves. Healthcare leaders must focus on what they can spend, before deciding how to fund that spending. The conversation will need to balance investment for the future with maintaining key credit metrics in the short term.

Conducting a capitalization analysis. Separate but related to the previous entry, how much leverage should your organization have relative to its overall capitalization? Ostensibly, many organizations have been paying principal while curtailing borrowing needs, so capitalization may have improved. While that may be the case, many organizations have depleted reserves and/or experienced investment losses that have reduced capitalization. Understanding where the organization stands is an essential next step.

Evaluating surplus return. Consider surplus return as investment income net of interest expense. Organizations should evaluate their ability to reliably generate both operating cash flow and net surplus. How an organization’s balance sheet is positioned to generate returns and manage risk will be a critical success factor.

Focusing on the metrics that matter. These include operating cashflow margin, cash to debt, debt to revenue, and days cash on hand. As key metrics for rating analysts and investors continue to evolve, management teams need to make sure they are focused on the correct numbers. The discussion should be dually focused on ensuring adequate-to-ample headroom to basic financial covenants as well as a comparison to key medians and peers. Strong financial planning will address how these metrics can be improved over time through synergies, growth, and diversification strategies.

Although it has been a difficult few years, hospitals and health systems seem to have moved onto a more stable footing over the last twelve months. In order to build upon the upward trajectory, now is the time to harness strategy, planning, and investment to move organizations from stability to sustainability.

Health systems are recovering from the worst financial year in recent history. We surveyed strategic planners to find out their top priorities for 2024 and where they are focusing their energy to achieve growth and sustainability. Read on to explore the top six findings from this year’s survey.

Research questions

With this survey, we sought the answers to five key questions:

How do health system margins, volumes, capital spending, and FTEs compare to 2022 levels?

How will rebounding demand impact financial performance?

How will strategic priorities change in 2024?

How will capital spending priorities change next year?

Bigger is Better for Financial Recovery

What did we find?

Hospitals are beginning to recover from the lowest financial points of 2022, where they experienced persistently negative operating margins. In 2023, the majority of respondents to our survey expected positive changes in operating margins, total margins, and capital spending. However, less than half of the sample expected increases in full-time employee (FTE) count. Even as many organizations reported progress in 2023, challenges to workforce recovery persisted.

40%

Of respondents are experiencing margins below 2022 levels

Importantly, the sample was relatively split between those who are improving financial performance and those who aren’t. While 53% of respondents projected a positive change to operating margins in 2023, 40% expected negative changes to margin.

One exception to this split is large health systems. Large health systems projected above-average recovery of FTE counts, volume, and operating margins. This will give them a higher-than-average capital spending budget.

Why does this matter?

These findings echo an industry-wide consensus on improved financial performance in 2023. However, zooming in on the data revealed that the rising tide isn’t lifting all boats. Unequal financial recovery, especially between large and small health systems, can impact the balance of independent, community, and smaller providers in a market in a few ways. Big organizations can get bigger by leveraging their financial position to acquire less resourced health systems, hospitals, or provider groups. This can be a lifeline for some providers if the larger organization has the resources to keep services running. But it can be a critical threat to other providers that cannot keep up with the increasing scale of competitors.

Variation in financial performance can also exacerbate existing inequities by widening gaps in access. A key stakeholder here is rural providers. Rural providers are particularly vulnerable to financial pressures and have faced higher rates of closure than urban hospitals. Closures and consolidation among these providers will widen healthcare deserts. Closures also have the potential to alter payer and case mix (and pressure capacity) at nearby hospitals.

Volumes are decoupled from margins

What did we find?

Positive changes to FTE counts, reduced contract labor costs, and returning demand led the majority of respondents in our survey to project organizational-wide volume growth in 2023. However, a significant portion of the sample is not successfully translating volume growth to margin recovery.

44%

Of respondents who project volume increases also predict declining margins

On one hand, 84% of our sample expected to achieve volume growth in 2023. And 38% of respondents expected 2023 volume to exceed 2022 volume by over 5%. But only 53% of respondents expected their 2023 operating margins to grow — and most of those expected that the growth would be under 5%. Over 40% of respondents that reported increases in volume simultaneously projected declining margins.

Why does this matter?

Health systems struggled to generate sufficient revenue during the pandemic because of reduced demand for profitable elective procedures. It is troubling that despite significant projected returns to inpatient and outpatient volumes, these volumes are failing to pull their weight in margin contribution. This is happening in the backdrop of continued outpatient migration that is placing downward pressure on profitable inpatient volumes.

There are a variety of factors contributing to this phenomenon. Significant inflationary pressures on supplies and drugs have driven up the cost of providing care. Delays in patient discharge to post-acute settings further exacerbate this issue, despite shrinking contract labor costs. Reimbursements have not yet caught up to these costs, and several systems report facing increased denials and delays in reimbursement for care. However, there are also internal factors to consider. Strategists from our study believe there are outsized opportunities to make improvements in clinical operational efficiency — especially in care variation reduction, operating room scheduling, and inpatient management for complex patients.

Strategists look to technology to stretch capital budgets

What did we find?

Capital budgets will improve in 2024, albeit modestly. Sixty-three percent of respondents expect to increase expenditures, but only a quarter anticipate an increase of 6% or more. With smaller budget increases, only some priorities will get funded, and strategists will have to pick and choose.

Respondents were consistent on their top priority. Investments in IT and digital health remained the number one priority in both 2022 and 2023. Other priorities shifted. Spending on areas core to operations, like facility maintenance and medical equipment, increased in importance. Interest in funding for new ambulatory facilities saw the biggest change, falling down two places.

Why does this matter?

Capital budgets for health systems may be increasing, but not enough. With the high cost of borrowing and continued uncertainty, health systems still face a constrained environment. Strategists are looking to get the biggest bang for their buck. Technology investments are a way to do that. Digital solutions promise high impact without the expense or risk of other moves, like building new facilities, which is why strategists continue to prioritize spending on technology.

The value proposition of investing in technology has changed with recent advances in artificial intelligence (AI), and our respondents expressed a high level of interest in AI solutions. New applications of AI in healthcare offer greater efficiencies across workforce, clinical and administrative operations, and patient engagement — all areas of key concern for any health system today.

Building is reserved for those with the largest budgets

What did we find?

Another way to stretch capital budgets is investing in facility improvements rather than new buildings. This allows health systems to minimize investment size and risk. Our survey found that, in general, strategists are prioritizing capital spending on repairs and renovation while deprioritizing building new ambulatory facilities.

When the responses to our survey are broken out by organization type, a different story emerges. The largest health systems are spending in ways other systems are not. Systems with six or more hospitals are increasing their overall capital expenditures and are planning to invest in new facilities. In contrast, other systems are not increasing their overall budgets and decreasing investments in new facilities.

AMCs are the only exception. While they are decreasing their overall budget, they are increasing their spending on new inpatient facilities.

Why does this matter?

Health systems seek to attract patients with new facilities — but only the biggest systems can invest in building outpatient and inpatient facilities. The high ranking of repairs in overall capital expenditure priorities suggests that all systems are trying to compete by maintaining or improving their current facilities. Will renovations be enough in the face of expanded building from better financed systems? The urgency to respond to the pandemic-accelerated outpatient shift means that building decisions made today, especially in outpatient facilities, could affect competition for years to come. And our survey responses suggest that only the largest health system will get the important first-mover advantage in this space.

AMCs are taking a different tack in the face of tight budgets and increased competition. Instead of trying to compete across the board, AMCs are marshaling resources for redeployment toward inpatient facilities. This aligns with their core identity as a higher acuity and specialty care providers.

Partnerships and affiliations offer potential solutions for health systems that lack the resources for building new facilities. Health systems use partnerships to trade volumes based on complexity. Partnerships can help some health systems to protect local volumes while still offering appropriate acute care at their partner organization. In addition, partnerships help health systems capture more of the patient journey through shared referrals. In both of these cases, partnerships or affiliations mitigate the need to build new inpatient or outpatient facilities to keep patients.

Eighty percent of respondents to our survey continued to lose patient volumes in 2023. Despite this threat to traditional revenue, health systems are turning from revenue diversification practices. Respondents were less likely to operate an innovation center or invest in early-stage companies in 2023. Strategists also reported notably less participation in downside risk arrangements, with a 27% decline from 2022 to 2023.

Why does this matter?

The retreat from revenue diversification and risk arrangements suggests that health systems have little appetite for financial uncertainty. Health systems are focusing on financial stabilization in the short term and forgoing practices that could benefit them, and their patients, in the long term.

Strategists should be cautious of this approach. Retrenchment on innovation and value-based care will hold health systems back as they confront ongoing disruption. New models of care, patient engagement, and payment will be necessary to stabilize operations and finances. Turning from these programs to save money now risks costing health systems in the future.

Market intelligence and strategic planning are essential for health systems as they navigate these decisions. Holding back on initiatives or pursuing them in resource-constrained environments is easier when you have a clear course for the future and can limit reactionary cuts.

Advisory Board’s long-standing research on developing strategy suggests five principles for focused strategy development:

Strategic plans should confront complexity. Sift through potential future market disruptions and opportunities to establish a handful of governing market assumptions to guide strategy.

Ground strategy development in answers to a handful of questions regarding future competitive advantage. Ask yourself: What will it take to become the provider of choice?

Communicate overarching strategy with a clear, coherent statement that communicates your overall health system identity.

A strategic vision should be supported by a limited number of directly relevant priorities. Resist the temptation to fill out “pro forma” strategic plan.

Pair strategic priorities with detailed execution plans, including initiative roadmaps and clear lines of accountability.

Strategists align on a strategic vision to go back to basics

What did we find?

Despite uneven recovery, health systems widely agree on which strategic initiatives they will focus more on, and which they will focus less on. Health system leaders are focusing their attention on core operations — margins, quality, and workforce — the basics of system success. They aim to achieve this mandate in three ways. First, through improving efficiency in care delivery and supply chain. Second, by transforming key elements of the care delivery system. And lastly, through leveraging technology and the virtual environment to expand job flexibility and reduce administrative burden.

Health systems in our survey are least likely to take drastic steps like cutting pay or expensive steps like making acquisitions. But they’re also not looking to downsize; divesting and merging is off the table for most organizations going into 2024.

Why does this matter?

The strategic priorities healthcare leaders are working toward are necessary but certainly not easy. These priorities reflect the key challenges for a health system — margins, quality, and workforce. Luckily, most of strategists’ top priorities hold promise for addressing all three areas.

This triple mandate of improving margins, quality, and workforce seems simple in theory but is hard to get right in practice. Integrating all three core dimensions into the rollout of a strategic initiative will amplify that initiative’s success. But, neglecting one dimension can diminish returns. For example, focusing on operational efficiency to increase margins is important, but it’ll be even more effective if efforts also seek to improve quality. It may be less effective if you fail to consider clinicians’ workflow.

Health systems that can return to the basics, and master them, are setting a strong foundation for future growth. This growth will be much more difficult to attain without getting your house in order first.

Vendors and other health system partners should understand that systems are looking to ace the basics, not reinvent the wheel. Vendors should ensure their products have a clear and provable return on investment and can map to health systems’ strategic priorities. Some key solutions health systems will be looking for to meet these priorities are enhanced, easy-to-follow data tools for clinical operations, supply chain and logistics, and quality. Health systems will also be interested in tools that easily integrate into provider workflow, like SDOH screening and resources or ambient listening scribes.

Going back to basics

Craft your strategy

1. Rebuild your workforce.

One important link to recovery of volume is FTE count. Systems that expect positive changes in FTEs overwhelmingly project positive changes in volume. But, on average, less than half of systems expected FTE growth in 2023. Meanwhile, high turnover, churn, and early retirement has contributed to poor care team communication and a growing experience-complexity gap. Prioritize rebuilding your workforce with these steps:

Recover: Ensure staff recover from pandemic-era experiences by investing in workforce well-being. Audit existing wellness initiatives to maximize programs that work well, and rethink those that aren’t heavily utilized.

Recruit: Compete by addressing what the next generation of clinicians want from employment: autonomy, flexibility, benefits, and diversity, equity, and inclusion (DEI). Keep up to date with workforce trends for key roles such as advance practice providers, nurses, and physicians in your market to avoid blind spots.

Retain: Support young and entry-level staff early and often while ensuring tenured staff feel valued and are given priority access to new workforce arrangements like hybrid and gig work. Utilize virtual inpatient nurses and virtual hubs to maintain experienced staff who may otherwise retire. Prioritize technologies that reduce the burden on staff, rather than creating another box to check, like ambient listening or asynchronous questionnaires.

2. Become the provider of choice with patient-centric care.

Becoming the provider of choice is crucial not only for returning to financial stability, but also for sustained growth. To become the provider of choice in 2024, systems must address faltering consumer perspectives with a patient-centric approach. Keep in mind that our first set of recommendations around workforce recovery are precursors to improving patient-centered care. Here are two key areas to focus on:

Front door: Ensure a multimodal front door strategy. This could be accomplished through partnership or ownership but should include assets like urgent care/extended hour appointments, community education and engagement, and a good digital experience.

Social determinants of health: A key aspect of patient-centered care is addressing the social needs of patients. Our survey found that addressing SDOH was the second highest strategic priority in 2023. Set up a plan to integrate SDOH screenings early on in patient contact. Then, work with local organizations and/or build out key services within your system to address social needs that appear most frequently in your population. Finally, your workforce DEI strategy should focus on diversity in clinical and leadership staff, as well as teaching clinicians how to practice with cultural humility.

3. Recouple volume and margins.

The increasingly decoupled relationship between volume and margins should be a concern for all strategists. There are three parts to improving volume related margins: increasing volume for high-revenue procedures, managing costs, and improving clinical operational efficiency.

Revenue growth: Craft a response to out-of-market travel for surgery. In many markets, the pool of lucrative inpatient surgical volumes is shrinking. Health systems are looking to new markets to attract patients who are willing to travel for greater access and quality. Read our findings to learn more about what you need to attract and/or defend patient volumes from out-of-market travel.

Cost reduction: Although there are many paths health systems can take to manage costs, focusing on tactics which are the most likely to result in fast returns and higher, more sustainable savings, will be key. Some tactics health systems can deploy include preventing unnecessary surgical supply waste, making employees accountable for their health costs, and reinforcing nurse-led sepsis protocols.

Clinical operational efficiency: The number one strategic priority in 2023, according to our survey, was clinical operational efficiency, no doubt in response to faltering margins. Within this area, the top place for improvement was care variation reduction (CVR). Ensure you’re making the most out of CVR efforts by effectively prioritizing where to spend your time. Improve operational efficiency outside of CVR by improving OR efficiency and developing protocols for complex inpatient management.