The nonprofit health system narrowed its operating loss while continuing to grapple with financial and policy pressures as it progresses towards profitability.

KEY TAKEAWAYS

Providence cut its operating loss in the second quarter to $21 million, improving from a $123 million loss a year ago.

Revenue rose 3% year-over-year to $7.91 billion, driven by higher patient volumes and better commercial rates.

The health system faces ongoing “polycrisis” challenges, including rising supply costs, staffing mandates, insurer denials, and looming Medicaid cuts, which have already prompted layoffs, hiring pauses, and leadership restructuring.

Providence made promising strides toward financial sustainability in the second quarter as higher patient volumes helped trim an operating loss that has weighed heavily on its balance sheet.

Yet the Renton, Washington-based health system warned that a compounding set of external pressures, which it labeled a “polycrisis,” still poses formidable challenges to its mission and future.

For the three months ended June 30, the nonprofit reported an operating loss of $21 million, equating to an operating margin of –0.3%, representing a marked improvement from the $123 million loss (–1.6%) posted over the same period in 2024. Compared with the previous quarter, the gain was even starker as Providence trimmed its deficit by $223 million. Through the first six months of the year, the health system had an operating loss of $265 million (-1.7%).

Revenue growth was fueled by higher patient volumes and improved commercial rates, Providence highlighted. Operating revenue rose 3% year-over-year to $7.91 billion as inpatient admissions (up 3%), outpatient visits (up 3%), case mix–adjusted admissions (up 3%), physician visits (up 8%), and outpatient surgeries (up 5%) all contributed.

On the expense side, Providence managed a 2% rise in operating costs to $7.93 billion, thanks largely to productivity gains, including a 43% reduction in agency contract labor. However, supply costs swelled by 9% and pharmacy expenses jumped by 12% year-over-year.

Providence, along with the healthcare industry at large, faces what CEO Erik Wexler called a “polycrisis” due to a mix of inflation, tariff-driven supply pressures, new state laws on staffing and charity care, insurer reimbursement delays and denials, and looming federal Medicaid cuts, especially from the One Big Beautiful Bill Act, which the health system said “threatens to intensify health care pressures.”

Those factors are significantly influencing hospitals’ and health systems’ decision-making. Providence has made staffing adjustments that include cutting 128 jobs in Oregon earlier this month, a restructuring in June that eliminated 600 full-time equivalent positions, apause on nonclinical hiring in April, and leadership reorganization since Wexler took over as CEO in January.

Accounts receivable is another area that has been indicative of headwinds, with Providence noting that while it improved in the second quarter, it “remains elevated compared to historical trends.”

Even with the roadblocks in its path, Providence is working towards profitability after being in the red for several years running.

“I’m incredibly proud of the progress we’ve made and grateful to our caregivers and teams across Providence St. Joseph Health for their continued dedication,” Wexler said in the news release. “The strain remains, especially with emerging challenges like H.R.1, but we will continue to respond to the times and answer the call while transforming for the future.”

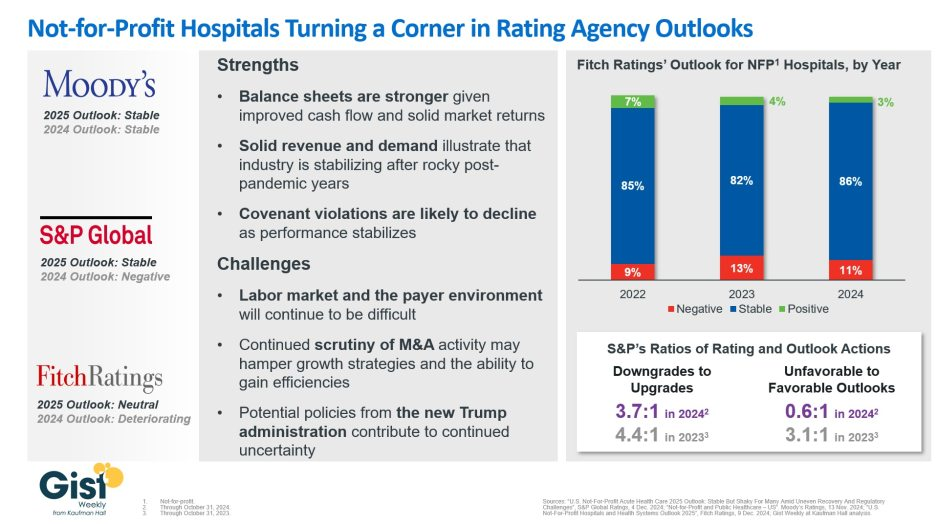

In late 2023, S&P Global and Fitch Ratings viewed the not-for-profit (NFP) hospital sector as negative or deteriorating, reflecting the difficult financial position many were in following the pandemic.

In recent weeks, S&P and Fitch upgraded their 2025 sector outlook for NFP hospitals to stable and neutral respectively, joining Moody’s Ratings, which held stable from last year.

This week’s graphic illustrates the rating agencies’ latest views on NFP hospitals, which point to a promising but uneven recovery for the industry.

Overall, the reports detail that stronger balance sheets, solid revenues, and improved demand have reduced the likelihood of covenant violations and strengthened NFP hospitals’ positions.

However, challenges persist that could impede further progress. The labor market, payer environment, antitrust enforcement, and a new administration all present complications for the continued recovery of NFP hospitals. Nonetheless, the reports indicate significant improvement for the industry since the post-pandemic ratings downturn.

Fitch’s report noted that the share of NFP hospitals with a stable outlook has reached a three-year high. Meanwhile, S&P reported that there are now almost twice as many NFP hospitals with favorable outlooks compared to unfavorable ones, a dramatic flip from 2023, which had a 3.1:1 ratio of unfavorable to favorable outlooks.

These ratings changes reflect the hard work put in by NFP hospitals across the country to improve their financial performance and find new ways to serve their communities sustainably.

However, the recovery remains “shaky” and incomplete, and hospitals still face a long road ahead as they reconfigure to a new normal.

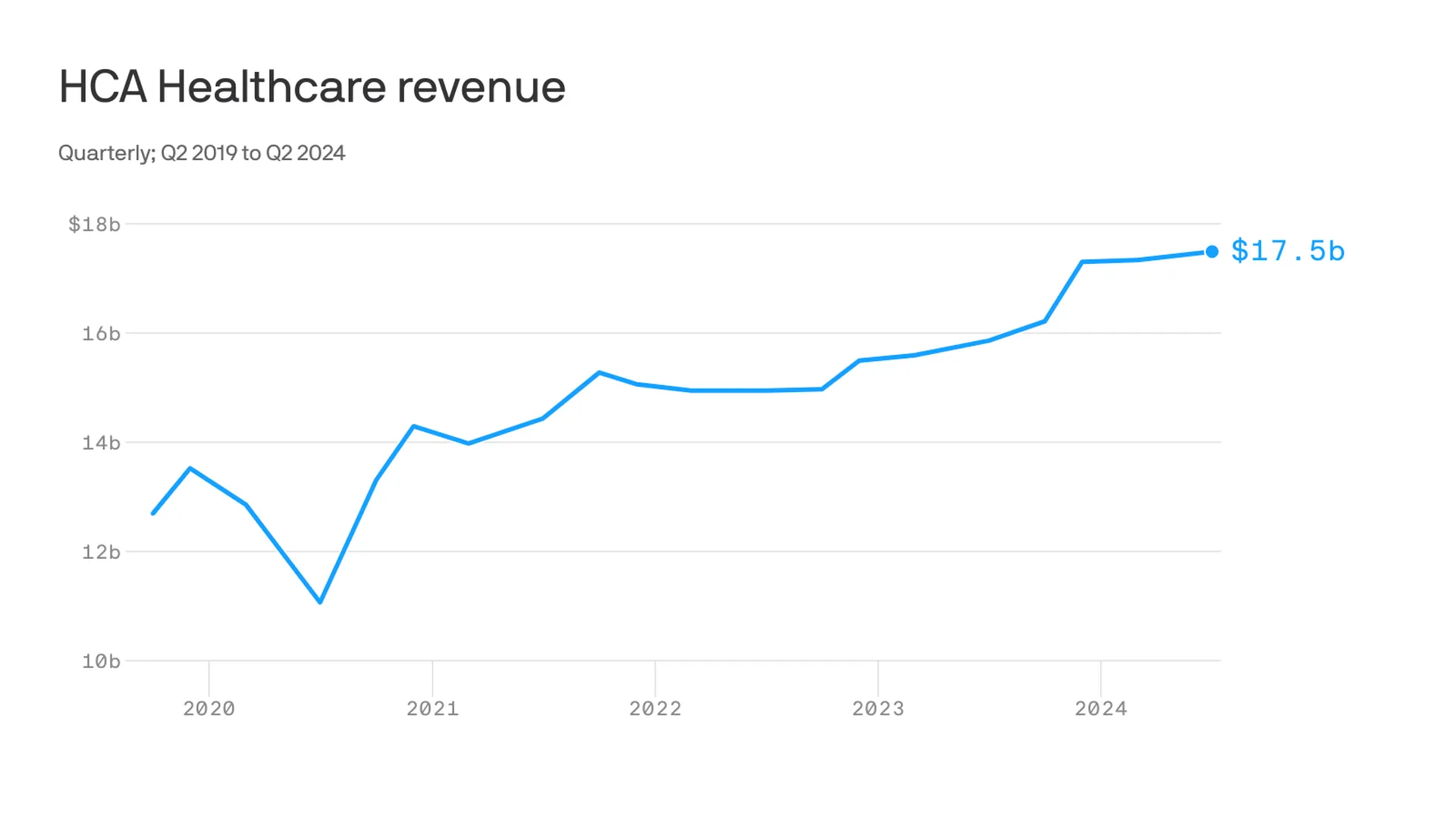

Some of America’s largest hospital systems saw their financials soar in the first half of 2024. And yet, more than 700 facilities across the country still are at risk of closing.

Why it matters:

It’s a familiar tale of the rich getting richer, as big, mostly for-profit health systems see improved margins while smaller facilities in outlying areas are barely hanging on.

That could worsen access for some of the most vulnerable Americans — and hasten consolidation in an industry that’s been a magnet for M&A.

The big picture:

Health systems with big footprints, including large academic medical centers, have weathered the pandemic and economic headwinds and are seeing margins as good or better than before COVID-19.

Nashville-based industry behemoth HCA Healthcare posted 23% year-over-year profit growth for the quarter, revising its forecast for the rest of the year, projecting it’ll reach as much as $6 billion. It posted a 10% year-over-year increase in revenue.

King of Prussia, Pennsylvania-based Universal Health Services similarly reported a strong quarter, posting nearly 69% growth on its bottom line over the same period last year while Dallas-based Tenet Healthcare reported a 111% jump in its net income over the same quarter last year.

Yes, but:

Smaller nonprofit hospitals, especially in rural areas, that made it through the crisis with the help of government aid are paring services like maternity wards and struggling to stay open.

“There are a lot of hospitals that survived, but their balance sheets are so weakened, their margin for error is basically zero at this point,” said Mike Eaton, senior vice president of strategy at population health company Navvis.

Hospitals that once could manage their expenses and the needs of communities are “going to really struggle to invest in what comes next,” he said.

Between the lines:

The biggest health systems have benefited from less volatility, seeing stabilizing drug prices and more predictable supply chains and labor costs, per a new report from Strata Decision Technology.

“It’s at least something you can manage to,” Steve Wasson, Strata’s chief data and intelligence officer, told Axios.

Revenues already were up thanks to renegotiated contracts health systems struck with payers last year, Wasson said.

There also have been changes on the federal side that boosted Medicare admissions and put some hospitals in line to be reimbursed for billions in underpayments from the 340B drug discount program.

Zoom in:

It’s all translated to operating margins that are up 17% year-to-date compared with the same time period in 2023, according to the latest Kaufman Hall National Hospital Flash Report.

Volumes as measured by hospital discharges per day are up 4% year-to-date.

Expenses per day are also up 6% year to date, including labor (4%), supplies (8%) and drugs (8%), but are far less volatile and thus easier to plan for, said Erik Swanson, senior vice president at Kaufman Hall.

But there’s a growing gulf between the top third of U.S. hospitals, which are seeing outsize growth, and the rest, Swanson said.

Threat level: A new report from the Center for Healthcare Quality and Payment Reform estimated 703 hospitals — or more than one-third of rural hospitals — are at risk of closure, based on Centers for Medicare and Medicaid Services financial information from July. Losses on privately insured patients are the biggest culprit.

“We’re looking at 50% of rural operating in the red. The situation is very challenging,” Michael Topchik, partner at Chartis Center for Rural Health, told Axios.

These smaller hospitals may still be there, but there will continue to be a steady erosion of the kinds of services they offer, such as obstetrics, cancer care and general surgery, he said.

What’s next:

Private equity investment in rural health care is already booming and with it, prospects for service and staffing cuts.

The South generally has the highest concentration of private equity-owned rural hospitals, often with lower patient satisfaction and fewer full-time staff compared with non-acquired hospitals, according to the Private Equity Stakeholder Project.

Congress is ramping up oversight of private equity investments in the sector, though most lawmakers are loath to take steps to actually halt deals.

Portland-based Oregon Health & Science University told staff June 6 that it plans to lay off at least 500 employees, citing financial issues.

“Our expenses, including supplies and labor costs, continue to outpace increases in revenue,” top leaders told staff in a message shared with Becker’s. “Despite our efforts to increase our revenue, our financial position requires difficult choices about internal structures, workforce and programs to ensure that we achieve our state-mandated missions and thrive over the long term.”

Willamette Week was first to report the news, which follows Oregon Health & Science University and Portland-based Legacy Health signing a binding, definitive agreement to come together as one health system under OHSU Health. OHSU Health would comprise 12 hospitals and, more than 32,000 employees and will be one of the largest providers of services to Medicaid members in Oregon.

An Oregon Health & Science University spokesperson told Becker’s more information about the layoffs will be provided in the coming weeks.

In the June 6 message, leaders told staff that “while we work to address short-term financial challenges, we must also plan for an impactful and successful future. We understand that last week’s announcement regarding the Legacy Health definitive agreement, while exciting and potentially transformational, raises questions about how we can afford the required investment in light of our financial situation.”

They added that a capital investment in Legacy “represents a strategic expansion designed to enhance our capacity,” and will be funded by borrowing with 30-year bonds.

“These capital dollars cannot be used to close gaps in our fiscal year 2025 OHSU budget or to pay our members. The OHSU Strategic Alignment and budgetary work would be necessary with or without the Legacy Health integration,” leaders said.

OHSU has planned a town hall next week to further discuss the combination with Legacy.

Leaders said discussions between managers and members about workforce reductions will begin after the annual review and contract renewal process, with additional reductions occurring over the next few months.

Peoria, Ill.-based OSF HealthCare has seen drastic improvements to its financial performance over the last two years, a performance that has allowed the health system to see revenue growth and expand its M&A footprint.

OSF was able to turn around a $43.2 million operating loss (-4.5% margin) in the first quarter ended Dec. 31, 2022, to a $0.9 million gain over the same period in 2023.

But the health system didn’t stop there and, in the first six months ended March 31, 2023, transformed a $60.9 million operating loss to an $8.9 million gain for the same period in 2024.

OSF HealthCare CFO Michael Allen connected with Becker’s to discuss the strategies that helped OSF get to a more steady financial place and some of their plans for the future.

Question: What strategies has OSF HealthCare implemented to help it turn the corner financially?

Michael Allen: OSF Healthcare has improved operating results by more than $70 million compared to FY2023, after seeing an even larger improvement from FY2022 to FY2023. After a very difficult FY2022, from a financial perspective, the organization launched a series of initiatives to return to positive margins.

There has been a focus on reducing the reliance on contract labor, nursing and other key clinical positions, with better recruiting and retaining initiatives. The organization is actively implementing automation for repeatable tasks in hard-to-recruit administrative functions and is actively managing supply and pharmaceutical costs against inflationary pressures.

OSF has also seen revenue growth from patient demand, expanding markets, capacity management and improved payment levels from government and commercial payers.

Q: KSB Hospital and OSF HealthCare recently entered into merger negotiations. How do you expect hospital consolidation to evolve in your market as many small, independent providers continue to face financial challenges and struggle to improve their bottom lines?

MA: The economics of the healthcare delivery system model is challenging in most markets, but particularly difficult for small and independent hospitals and clinics. Given the structure of the payment system and the rising operating costs, I don’t see this pressure easing any time soon.

OSF is looking forward to our opportunity to extend our healthcare ministry to KSB and the greater Dixon area and continue their great legacy of patient care.

Q: What advice would you have for other health system financial leaders looking to get their margins up this year?

MA:There are no silver bullets to improving margins. It’s the daily work of using our costs wisely and executing on important strategies that will win the day. Automation, elimination of non-value-added costs and continuously looking for opportunities to get the best care, patient engagement and workforce engagement is where OSF and other health systems will continue to focus.

Q: An increasing number of hospitals and health systems across the U.S. are dropping some or all of their commercial Medicare Advantage contracts. Where do you see the biggest challenges and opportunities for health systems navigating MA?

MA: As more and more patients and payers are entering Medicare Advantage, we continue to watch our metrics on payment levels to ensure we are being paid fairly and within contract terms for our payer partners.

There does appear to be a trend of increasing denials that often aren’t justified or are not within our contract terms, and we will continuously work to rectify those issues with our payers to ensure our patients receive the appropriate care and OSF is paid fairly for services provided.

In last month’s blog, we discussed the importance of financial planning, both for internal audiences—including the leadership team and the board of trustees—and for external audiences—including prospective students and their families, rating agencies, alumni and other stakeholders. This month, in the first of a series of blogs focused on key finance-related issues, we’re turning our attention to a broader and deeper internal audience, asking the question, “What is your institution’s financial literacy?”

The terms described in this blog will be very familiar to members of college and university finance teams and to many institutional leaders as well.

The point is that these terms should be familiar to as many individuals as possible throughout the institution: they form the foundation of a basic financial literacy that every college and university should foster across its faculty and staff.

What is financial literacy?

Financial literacy is the ability to understand where an institution stands at any given time with respect to key elements of its balance sheet and income statement. To state it simply, financial literacy means an understanding of the vital signs that describe the financial health of the institution. In medicine, the basic vital signs are body temperature, pulse rate, respiration rate, and blood pressure. In finance, the vital signs include measures of unrestricted cash, revenue, expenses, debt, and risk.

In medicine, there are professionals whose job is to dig deeper if any of the body’s vital signs are deteriorating. Similarly in finance, it is the job of the CFO and finance team to monitor the vital signs of the institution’s financial health and to seek causes and solutions of current troubles or to use changes in the vital signs to address potential future issues. For most of us—in medicine or finance—the goal should be a basic understanding of what the vital signs measure and whether they point to good health.

There are some key considerations for each financial vital sign:

Unrestricted Cash. The critical question related to unrestricted cash (also termed liquidity) is whether the institution has enough accessible liquidity to meet its daily expenses if its cash flow was unexpectedly interrupted. Days cash on hand is a balance sheet metric that is typically used to assess this issue: days cash on hand literally measures how long unrestricted cash reserves could cover the institution’s operating costs if its cash flow suddenly stopped.

The emphasis on “accessible liquidity” is an important element of this financial vital sign: it speaks to the ability to distinguish between institutional wealth versus liquidity. In higher education, an endowment can be an important source of the institution’s wealth, but many of the funds within an endowment cannot be easily accessed—they are, by and large, not liquid funds or are highly restricted as to their use. Readily available, unrestricted cash reserves are what an institution must rely on to meet its day-to-day expenses should cash flow be interrupted or reduced.

Revenue. Because an institution needs to maintain or grow its cash reserves and allocate them sparingly, the amount of revenue coming in—from tuition and fees and from other sources of additional income (see below)—is also an important vital sign. An institution should obviously be taking in enough revenue to cover its expenses without drawing on its cash reserves.

Additionally, however, given continued growth in expenses, revenue growth (through enrollment growth, student mix, and/or program mix) is a significant measure of ongoing vitality.

Financial health is also enhanced if an institution does not rely too heavily on a single revenue source. For schools with an endowment, for example, the amount of income the endowment can generate to support operations is an important source of additional income. More generally, additional income can come from such auxiliary revenue sources as residential fees, fundraising, special events, concessions, and a host of other sources. These additional revenue sources, while potentially small on an individual basis, can be material on a cumulative basis.

Expenses. How much does it cost to produce the education that a college or university provides to its students? If that cost is approaching—or worse, surpassing—the net tuition revenue and additional income that the institution brings in, what is being done—or could be done—to reduce those costs? Expenses are perhaps most similar to body temperature in medical vital signs; if they get too high, they must be brought down before the health of the institution begins to decline. And the measure of expenses should be viewed overall for the institution as well as on a per student basis to communicate the “value” of different student types to the organization.

Debt. Debt is an essential component of the funding of significant capital projects that colleges and universities must undertake to maintain updated and competitive facilities. Just as most people need to take out a mortgage to afford a home purchase—spreading the cost of the home over a multiyear payment period—so too do institutions often need debt to finance large capital expenditures. But the amount of debt (also termed “leverage”) can also be an indicator of the institution’s financial health. That health begins to decline if the amount of debt relative to an institution’s assets or annual income grows too large, or if the amount required to pay for the debt (i.e., to meet the scheduled principal and interest payments—the debt service) puts too much of a burden on the cash flow generated from the institution’s day-to-day operations. If the debt service becomes too high relative to cash flow, the institution may face onerous legal requirements, or even default, which may severely constrain its ability to provide the range of programs desired and expected by its student population.

Risk. Risk is an indicator that identifies potential weaknesses in any of the preceding indicators that could jeopardize the institution’s financial health. For basic financial literacy, only the most significant risks need to be identified: over-reliance on tuition revenue in a market with declining enrollments, for example, or over-reliance on endowment income in the event of market instability. Once an institution consistently measures its risks, it can begin to determine what level of risk is appropriate and address strategies to manage that risk.

Why does financial literacy matter?

Promoting financial literacy throughout an institution cultivates a common understanding of financial health that provides context for leadership’s decisions and a common language to address issues. If tuition revenue is declining, for example, financially literate faculty members should better understand the need to prioritize academic programs that not only meet the academic needs of their students, but also can draw more students or produce healthier margins. If cost-cutting measures are required to reduce expenses, financially literate staff should understand the genesis of the need for reductions and why the institution cannot simply draw on its endowment to close the gap. Furthermore, acknowledging and describing the most significant risks an institution faces using a common language makes clear the need for action if one or more of those risks begins to materialize.

Financial literacy is also an important tool for cultivating the next generation of faculty leaders. When faculty members rise to leadership positions, it is essential that they understand that academic growth and strategic initiatives cannot succeed without sufficient resources to support them, or if they cannot generate the revenue needed to cover—or exceed—their costs.

By promoting financial literacy across the institution, the institution can help ensure that future leaders are acquiring the foundation needed for them to grow into informed decision-makers who understand the need to maintain the institution’s financial health.

Here are 30 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings and Moody’s Investors Service released in 2024.

Avera Health has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Sioux Falls, S.D.-based system’s strong operating risk and financial profile assessments, and significant size and scale, Fitch said.

Cedars-Sinai Health System has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Los Angeles-based system’s consistent historical profitability and its strong liquidity metrics, historically supported by significant philanthropy, Fitch said.

Children’s Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Dallas-based system’s continued strong performance from a focus on high margin and tertiary services, as well as a distinctly leading market share, Moody’s said.

Children’s Hospital Medical Center of Akron (Ohio) has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the system’s large primary care physician network, long-term collaborations with regional hospitals and leading market position as its market’s only dedicated pediatric provider, Moody’s said.

Children’s Hospital of Orange County has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Orange, Calif.-based system’s position as the leading provider for pediatric acute care services in Orange County, a position solidified through its adult hospital and regional partnerships, ambulatory presence and pediatric trauma status, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The rating reflects the Minneapolis-based system’s strong balance sheet, robust liquidity position and dominant pediatric market position, Fitch said.

Cincinnati Children’s Hospital Medical Center has an “Aa2” rating and stable outlook with Moody’s. The rating is supported by its national and international reputation in clinical services and research, Moody’s said.

Cook Children’s Medical Center has an “Aa2” rating and stable outlook with Moody’s. The ratings agency said the Fort Worth Texas-based system will benefit from revenue diversification through its sizable health plan, large physician group, and an expanding North Texas footprint.

El Camino Health has an “AA” rating and a stable outlook with Fitch. The rating reflects the Mountain View, Calif.-based system’s strong operating profile assessment with a history of generating double-digit operating EBITDA margins anchored by a service area that features strong demographics as well as a healthy payer mix, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by its strong operating risk assessment, leading market position in its immediate service area and strong financial profile,” Fitch said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Mullica Hill, N.J.-based system will return to strong operating cash flows following the operating challenges of 2022 and 2023, as well as the successful integration of Inspira Medical Center of Mannington (formerly Salem Medical Center).

JPS Health Network has an “AA” rating and stable outlook with Fitch. The rating reflects the Fort Worth, Texas-based system’s sound historical and forecast operating margins, the ratings agency said.

Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Somerville, Mass.-based system’s strong reputation for clinical services and research at its namesake academic medical center flagships that drive excellent patient demand and help it maintain a strong market position, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The rating reflects the Grand Blanc, Mich.-based system’s leading market position over a broad service area covering much of Michigan, the ratings agency said.

Med Center Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Bowling Green, Ky.-based system’s strong operating risk assessment and leading market position in a primary service area with favorable population growth, Fitch said.

Nicklaus Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Miami-based system’s position as the “premier pediatric hospital in South Florida with a leading and growing market share,” Fitch said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Winston-Salem, N.C.-based system’s recent acquisition of three South Carolina hospitals from Dallas-based Tenet Healthcare will be accretive to its operating performance as the hospitals are highly profited and located in areas with growing populations and good income levels.

Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Portland-based system’s top-class academic, research and clinical capabilities, Moody’s said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the health system’s strong and consistent operating performance and a growing presence in a demographically favorable market, Fitch said.

Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system’s rating is driven by a strong financial profile combined with a leading market position with broad coverage in both acute care services and health plan operations, Fitch said.

Rush University System for Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Chicago-based system’s strong financial profile and an expectation that operating margins will rebound despite ongoing macro labor pressures, the rating agency said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The rating reflects the Cape Girardeau, Mo.-based system’s strong financial profile, characterized by robust liquidity metrics, Fitch said.

Saint Luke’s Health System has an “Aa2” rating and stable outlook with Moody’s. The Kansas City, Mo.-based system’s rating was upgraded from “A1” after its merger with St. Louis-based BJC HealthCare was completed in January.

Salem (Ore.) Health has an”AA-” rating and stable outlook with Fitch. The rating reflects the system’s dominant marketing positive in a stable service area with good population growth and demand for acute care services, Fitch said.

Seattle Children’s Hospital has an “AA” rating and a stable outlook with Fitch. The rating reflects the system’s strong market position as the only children’s hospital in Seattle and provider of pediatric care to an area that covers four states, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system’s rating is supported by a strong financial profile, multistate presence and scale with good revenue diversity, Fitch said.

St. Elizabeth Medical Center has an “AA” rating and stable outlook with Fitch. The rating reflects the Edgewood, Ky.-based system’s strong liquidity, leading market position and strong financial management, Fitch said.

Stanford Health Care has an “Aa3” rating and positive outlook with Moody’s. The rating reflects the Palo Alto, Calif.-based system’s clinical prominence, patient demand and its location in an affluent and well insured market, Moody’s said.

University of Colorado Health has an “AA” rating and stable outlook with Fitch. The Aurora-based system’s rating reflects a strong financial profile benefiting from a track record of robust operating margins and the system’s growing share of a growth market anchored by its position as the only academic medical center in the state, Fitch said.

Willis-Knighton Medical Center has an “AA-” rating and positive outlook with Fitch. The outlook reflects the Shreveport, La.-based system’s improving operating performance relative to the past two fiscal years combined with Fitch’s expectation for continued improvement in 2024 and beyond.

Since 2022, S&P Global Ratings has tracked an increase in violations of debt agreements as macro economic pressures and low operating margins challenge providers.

Dive Brief:

The number of nonprofit health systems violating their financial agreements with lenders or investors has increased since 2022 as providers struggle to meet debt obligations amid challenging operating conditions, according to a new report from credit agency S&P Global Ratings.

This year, nonprofits will continue to be at heightened risk of violating covenant agreements, or conditions of debt that are put in place by lenders. Recently, the most common violations among nonprofits have been debt service coverage — the amount of days-cash-on-hand to debt ratios — as the sector continues to weather high expenses and weak revenues.

Most nonprofits have recently received extra time to remedy finances in the form of waivers or forbearance agreements, but other systems have merged with more financially stable organizations to meet lending agreements, according to the report.

Dive Insight:

Financial covenant violations among nonprofits began to increase at the onset of the COVID-19 pandemic.

In the early stages of the pandemic, violations were often tied to one-time pressures on operating income, such as mandatory stoppages of services.

However, violations have since evolved and now reflect nonprofits’ struggles with ongoing labor shortages and inflationary pressures, according to the report.

Providers in the speculative rating category were more likely to have violated financial covenants over the past two years and accounted for 60% of violations in S&P’s rated universe.

Some health systems have recovered from the pandemic much better than others, and those with healthier margins tend to be the ones that made a stronger push into outpatient care.

By the numbers:

There’s a wildly large and growing difference between the operating margins of top-performing health systems and those at the bottom, according to Kaufman Hall data shared with Axios. (Go deeper on their analysis.)

“The hospitals that are not performing well are performing worse, but the hospitals that are recovering are performing extremely well,” firm co-founder Kaufman told Axios.

“I would say hospitals that are not doing particularly well … they’re not capturing that outpatient work, or at least not at the level that they need to,” he added.

Yes, but:

Operating margin is only one measure of a hospital’s financial health, and total margins are often much higher, said Anderson, the Johns Hopkins professor.

“You diversify where there is potential profit, and they have moved into all sorts of things where there is profit,” he added.“They have a whole portfolio of ways to make money now that they didn’t have 20 years [ago].”

Some experts also say that hospitals aren’t disciplined about keeping costs down.

“I think partly what happened over time is that … investments were not treated as investments, but as costs,” said Cooper, the Yale economist.

Today is the federal income Tax Day. In 43 states, it’s in addition to their own income tax requirements. Last year, the federal government took in $4.6 trillion and spent $6.2 trillion including $1.9 trillion for its health programs. Overall, 2023 federal revenue decreased 15.5% and spending was down 8.4% from 2022 and the deficit increased to $33.2 trillion. Healthcare spending exceeded social security ($1.351 trillion) and defense spending ($828 billion) and is the federal economy’s biggest expense.

Along with the fragile geopolitical landscape involving relationships with China, Russia and Middle East, federal spending and the economy frame the context for U.S. domestic policies which include its health system. That’s the big picture.

Today also marks the second day of the American Hospital Association annual meeting in DC. The backdrop for this year’s meeting is unusually harsh for its members:

Increased government oversight:

Five committees of Congress and three federal agencies (FTC, DOJ, HHS) are investigating competition and business practices in hospitals, with special attention to the roles of private equity ownership, debt collection policies, price transparency compliance, tax exemptions, workforce diversity, consumer prices and more.

Medicare payment shortfall:

CMS just issued (last week) its IPPS rate adjustment for 2025: a 2.6% bump that falls short of medical inflation and is certain to exacerbate wage pressures in the hospital workforce. Per a Bank of American analysis last week, “it appears healthcare payrolls remain below pre-pandemic trend” with hospitals and nursing homes lagging ambulatory sectors in recovering.”

Persistent negative media coverage:

The financial challenges for Mission (Asheville), Steward (Massachusetts) and others have been attributed to mismanagement and greed by their corporate owners and reports from independent watchdogs (Lown, West Health, Arnold Ventures, Patient Rights Advocate) about hospital tax exemptions, patient safety, community benefits, executive compensation and charity care have amplified unflattering media attention to hospitals.

Physicians discontent:

59% of physicians in the U.S. are employed by hospitals; 18% by private equity-backed investors and the rest are “independent”. All are worried about their income. All think hospitals are wasteful and inefficient. Most think hospital employment is the lesser of evils threatening the future of their profession. And those in private equity-backed settings hope regulators leave them alone so they can survive. As America’s Physician Group CEO Susan Dentzer observed: “we knew we’re always going to need hospitals; but they don’t have to look or operate the way they do now. And they don’t have to be predicated on a revenue model based on people getting more elective surgeries than they actually need. We don’t have to run the system that way; we do run the healthcare system that way currently.”

The Value Agenda in limbo:

Since the Affordable Care Act (2010), the CMS Center for Innovation has sponsored and ultimately disabled all but 6 of its 54+ alternative payment programs. As it turns out, those that have performed best were driven by physician organizations sans hospital control. Last week’s release of “Creating a Sustainable Future for Value-Based Care: A Playbook of Voluntary Best Practices for VBC Payment Arrangements.” By the American Medical Association, the National Association of ACOs (NAACOs) and AHIP, the trade group representing America’s health insurance payers is illustrative. Noticeably not included: the American Hospital Association because value-pursuers think for hospitals it’s all talk.

National insurers hostility:

Large, corporate insurers have intensified reimbursement pressure on hospitals while successfully strengthening their collective grip on the U.S. health insurance sector. 5 insurers control 50% of the U.S. health insurance market: 4 are investor owned. By contrast, the 5 largest hospital systems control 17% of the hospital market: 1 is investor-owned. And bumpy insurer earnings post-pandemic has prompted robust price increases: in 2022 (the last year for complete data and first year post pandemic), medical inflation was 4.0%, hospital prices went up 2.2% but insurer prices increased 5.9%.

Costly capital:

The U.S. economy is in a tricky place: inflation is stuck above 3%, consumer prices are stable and employment is strong. Thus, the Fed is not likely to drop interest rates making hospital debt more costly for hospitals—especially problematic for public, safety net and rural hospitals. The hospital business is capital intense: it needs $$ for technologies, facilities and clinical innovations that treat medical demand. For those dependent on federal funding (i.e. Medicare), it’s unrealistic to think its funding from taxpayers will be adequate. Ditto state and local governments. For those that are credit worthy, capital is accessible from private investors and lenders. For at least half, it’s problematic and for all it’s certain to be more expensive.

Campaign 2024 spotlight:

In Campaign 2024, healthcare affordability is an issue to likely voters. It is noticeably missing among the priorities in the hospital-backed Coalition to Strengthen America’s Healthcare advocacy platform though 8 states have already created “affordability” boards to enact policies to protect consumers from medical debts, surprise hospital bills and more.

Understandably, hospitals argue they’re victims. They depend on AHA, its state associations, and its alliances with FAH, CHA, AEH and other like-minded collaborators to fight against policies that erode their finances i.e. 340B program participation, site-neutral payments and others. They rightfully assert that their 7/24/365 availability is uniquely qualifying for the greater good, but it’s not enough. These battles are fought with energy and resolve, but they do not win the war facing hospitals.

AHA spent more than $30 million last year to influence federal legislation but it’s an uphill battle. 70% of the U.S. population think the health system is flawed and in need of transformative change. Hospitals are its biggest player (30% of total spending), among its most visible and vulnerable to market change.

Some think hospitals can hunker down and weather the storm of these 8 challenges; others think transformative change is needed and many aren’t sure. And all recognize that the future is not a repeat of the past.

For hospitals, including those in DC this week, playing victim is not a strategy. A vision about the future of the health system that’s accessible, affordable and effective and a comprehensive plan inclusive of structural changes and funding is needed. Hospitals should play a leading, but not exclusive, role in this urgently needed effort.

Lacking this, hospitals will be public utilities in a system of health designed and implemented by others.