It’s no secret the brand name prescription drug costs are high. The rising costs have been blamed by health care analysts on kickbacks within the drug supply chain demanded by the federal government, drug distributors (wholesalers), health insurance companies and pharmacy benefit managers (PBMs).

How about $356 billion worth of pure glut in the prescription drug supply chain, according to the analysis by DCI. Simply put, the market price established for these drugs by manufacturers has $356 billion worth of markups that mainly accommodate the financial demands (i.e. kickbacks or rebates) of groups that profit off the prescription drug system in the United States, health insurers and their PBMs in particular.

And that’s an all-time record.

Why?

Get ready to choke on your popcorn.

In the 1990s the federal government mandated in the Medicaid program that drug manufacturers offer a minimum rebate of 23% off the purchase price of brand name drugs. The feds also mandated that if drug manufacturers offer a better rebate on those drugs to someone else, the government also gets that same rebate.

The thought was no one gets a better deal than the federal government.

Rebates expanded again as PBMs continued to gain more control over the drug supply chain. The PBMs now force drug manufacturers to offer significant concessions in order to get on the list of approved medications – known as a formulary – available to patients with health insurance.

To account for these demands, drug manufacturers set the list price for their brand name drugs with these price concessions baked into the number.

DCI’s analysis found that baking is $356 billion of goodies for health care companies paid for by the government and you.

It’s the same kind of concept as a U.S. popular clothing retailer that displays inflated retail costs on the tags of goods and then right below displaying a lower “sale” price to make the consumer think they got a deal.

Here’s another way of thinking of it: Just like Congress has a lot of “pork” in its spending bills, there’s also a lot of pork in prescription drug costs that have very little to do with anything, other than increase profits for the health care industry.

Though the federal government intended to create a better system for taxpayers back in the 1990s when it demanded rebates in the Medicaid system, it instead created a feeding frenzy for companies in the drug supply chain.

In the year 2000 just a handful of companies in the drug supply chain dotted the Fortune 100 list of most financially successful companies. Today there are four such companies in the top 10.

The Minnesota-based health care conglomerate UnitedHealth leads that pack. The company’s profits have soared in the last two decades largely due to increasing medical costs and prescription drug costs paid by Americans. It has leaped over companies like Exxon Mobile and Apple to become the third largest company in America. Only Walmart and Amazon take in more revenue.

The company employs more than 400,000, including doctors and clinicians and has its own pharmacy benefits manager called Optum Rx.

We reported last month that Americans spent $464 billion last year on prescription drugs. That was also an all-time record, which will likely be set again and again and again until reforms are enacted.

Elevance, which owns Blue Cross plans, is now reeling from Wall Street losses thanks to its Medicare Advantage business.

The company now known as Elevance, which owns Blue Cross plans in 14 states, took a drubbing on Wall Street yesterday after executives told shareholders that it had to pay out way more in medical claims during the second quarter than expected, especially in its Medicare Advantage business. As a reminder, Wall Street hates to hear such news, so much so that investors rushed to sell their shares in the company, sending the stock price to $296.39 – a 52-week low – before closing at $302.45 yesterday afternoon. That’s down 47% from the all-time high of $567.36 it reached last September.

The news was so distressing for people who still have investments in for-profit health insurers that many of them finally bailed, getting the message that the entire sector is likely not the best place to make money these days. All seven of the companies (Centene, Cigna, CVS/Aetna, Elevance, Humana, Molina and UnitedHealth) saw big drops in their stock price with two others (Centene and Molina) also falling to 52-week lows. The companies’ stock is continuing to tank today as I write this.

When Denial Becomes a Liability

UnitedHealth has historically been the first of the companies to release quarterly earnings, but it stepped back as leader of the pack this quarter after that giant’s recent troubles on Wall Street. UnitedHealth missed financial analysts’ profit expectations last quarter and withdrew its profit guidance for the year, an unprecedented move for that company, which terrified its shareholders. UnitedHealth’s stock price has lost nearly 55% of its value since reaching a high of $630.73 last November.

Like UnitedHealth, Elevance had been a Wall Street darling until a business practice common in the health insurance game – refusing to pay for patients’ medically necessary care – finally caught up with it.

I’m talking about prior authorization, the benign sounding term that covers a number of ways a health insurer banks money by saying no to a doctor’s plea to cover a patient’s treatment or medications. The fundamental problem is that by refusing to pay for care a patient needs, that patient likely will get sicker and wind up needing even more expensive care down the road. Insurance company beancounters know that can happen, but they also know there is a decent chance that that potentially high-cost patients will not even be enrolled in one of the company’s health plans when the day finally arrives that they have to go to the hospital, which, of course, might have been avoided if the initial treatment had been approved in the first place.

We’re not just talking about a stay in the hospital. One permutation of prior auth is called step therapy in which an insurer demands that a patient try other medications on the insurer’s list of preferred drugs (its “formulary”) before approving the drug a doctor believes will work best. Sometimes it’s called “fail first.” In other words, a patient must endure pain and suffering for weeks or months taking an ineffective drug on an insurer’s formulary – the price of which the insurer has negotiated to its financial advantage with a drug maker – before the insurer will agree to cover the medication the doctor believes will be more effective. The doctor will then have to persuade the insurer that the insurer’s preferred drug failed. We’ll dive deeper into that insurer-induced nightmare in a future post, but know for now that it is a big and expensive time-suck that doctors have to endure while insurers can keep unused premium dollars in their investment accounts.

The Conversion That Changed Everything

But let’s go back to Elevance, which until recently was called Anthem and before that WellPoint. Many of its subsidiaries still use the term Anthem in its branding, like the biggest under its corporate umbrella, Anthem Blue Cross of California. All of those Blues plans operated on a nonprofit basis until a savvy executive named Leonard Schaeffer, who was CEO of Anthem of California back when it was still a nonprofit, pulled off a deal that would put him on the path to considerable fame and fortune, a first-of-its-kind “conversion” that would prove to be a major reason why the U.S. has the most complex, expensive and inefficient health care system on the planet.

According to his official bio on the website of the Leonard D. Schaffer Fellows in Government Service, which is affiliated with some of the country’s most prestigious universities, Schaeffer was recruited as CEO of Blue Cross of California in 1986 when, we are told, it was near bankruptcy. We’re also told that Schaeffer “managed the turnaround of Blue Cross of California and the IPO (initial public offering, i.e., converting it to for-profit status) creating WellPoint in 1993. During his tenure, WellPoint made 17 acquisitions and endowed four charitable foundations with assets of over $6 billion. Under Schaeffer’s leadership, WellPoint’s value grew from $11 million to over $49 billion.”

One might think from reading that last sentence that Schaeffer himself wrote big personal checks to endow those foundations, but establishing those nonprofit foundations (which includes the California Endowment, the California Health Care Foundation and the California Wellness Foundation) was demanded by California regulators as a condition of their approval of the IPO. The money was referred to as a conversion fund (converting from nonprofit to for-profit status), and it came from the proceeds of the IPO.

But Schaffer did indeed make a ton of money from the deal and WellPoint’s subsequent acquisition by a rival company that also owned recently converted Blues plans, Anthem, in 2004.

One of the organizations that opposed the WellPoint-Anthem deal, Consumer Watchdog, wrote at the time that:

Payments to WellPoint executives after the company’s buyout by Anthem Inc. could top $600 million if regulators and shareholders do not modify the acquisition terms, according to documents received from California regulators by the Foundation for Taxpayer and Consumer rights under a Public Records Act Request late Tuesday.

The documents detail potential payments in excess of those estimated by the company to shareholders at $200 million in a recent proxy. Executives will receive cash bonuses worth between $146 million and $365 million under the proposed terms of the company buyout by Anthem, in addition to over $251 million in stock options. WellPoint CEO Leonard Schaeffer has already begun exercising his stock options as of June 1st at sweetheart prices – earning him $16 million on that one day alone and increasing the size of his shares by hundreds of thousands.

When we look back at the history of health insurance in this country, we can thank this one man for the rapid shifting of Americans out of what historically had been nonprofit health insurance plans that initially were community-rated, meaning they charged everybody the same premium, regardless of gender, health status, occupation or address, and did not use gimmicks like prior authorization to boost profits. Being nonprofits, they couldn’t even book profits, although many of them did amass millions more in “reserves” than regulators required for solvency reasons.

I was working at Cigna when WellPoint joined the club of big for-profit insurers in 1993, along with Aetna, Humana (where I also previously worked), UnitedHealth, which was a relatively small player back then, and giant “multiline” insurers like MetLife, Prudential and Travelers. All of those last three decided to sell their health insurance operations to UnitedHealth and Aetna, putting those companies on the path to becoming the behemoths they are today.

And Schaeffer would wind up being one of America’s richest men, and, to his credit, he has been personally philanthropic. We know that because his name shows up all over the place in U.S. health care think-tank world. Indeed, his name is now associated far more with groups and institutions engaged in public policy than the “platinum parachute,” to use Consumer Watchdog’s term, he got when he and a few colleagues engineered the sale of WellPoint to Anthem. As his bio notes:

In 2009, Schaeffer established the Schaeffer Center for Health Policy and Economics at the University of Southern California, which emphasizes the interdisciplinary approach to research and analysis to support evidence-based health policy. In 2015, he established the Schaeffer Fellows in Government Service program which has supported 418 undergraduates to date in high-level, summer government internships. In 2004, he established the Schaeffer Institute for Public Policy & Government Service. He has also endowed chairs in health care financing and policy at the Brookings Institution, Harvard Medical School, the National Academy of Medicine, UC Berkeley and USC.

If Schaeffer still owns shares in Elevance, he is a bit poorer today than he was yesterday morning, but he’s probably still doing OK. Shares of Elevance’s stock have increased 1731% in value since they started trading on the New York Stock Exchange in October 2001, even with the company’s very bad Thursday on the Street.

I’ve been at thisfor so long and have seen so much. And it’s hard to overstate how significant the latest revelations from The Wall Street Journal are. According to its reporting, the U.S. Department of Justice’s criminal health care-fraud unit is questioning former UnitedHealth Group employees about the company’s Medicare billing practices regarding how the company records diagnoses that trigger higher payments from taxpayers.

For years, independent policy experts and *some* regulators have warned that the private Medicare Advantage program has become a breeding ground for upcoding and tax dollar waste. The tactic being scrutinized by the DOJ is called “upcoding.” Essentially, Medicare Advantage companies have an incentive to “find” new illnesses — even among patients who might not need additional treatment because the more serious the diagnoses, the bigger the government payouts to the company.

According to the Journal, prosecutors, FBI agents, and the Health and Human Services Inspector General have been asking ex-employees about special training for doctors, software that flags profitable conditions, and even bonuses for physicians who recode patient files. One former UnitedHealth doctor told the Journal that prosecutors inquired about pressure to use certain diagnosis codes and bonus pay for certain health care decisions that financially favored UnitedHealth.

The Journal’s data shows that UnitedHealth’s members received certain lucrative diagnoses at higher rates than patients in other Medicare Advantage plans — billions of extra dollars that ultimately come from taxpayers. In one example, they reportedly pulled in about $2,700 more taxpayer dollars per patient visit when nurses went into seniors’ homes to hunt for additional conditions.

In a statement, UnitedHealth insists they “remain focused on what matters most: delivering better outcomes, more benefits, and lower costs for the people we serve.”

This latest criminal investigation joins at least two other DOJ probes into UnitedHealth’s billing and potential antitrust violations. And it’s yet another reminder that the Medicare Advantage program — which, much to many advocates alarm, now covers more than half of all Medicare enrollees – is desperately in need of real oversight.

If there’s any silver lining, it’s that courageous former employees are speaking up. They know what I know: This “profit-maximizing” through “upcoding” and “favorable selection” drains billions that could be better spent on actual patient care and pad Wall Street profits.

The healthcare industry is still licking its wounds from $1 trillion in federal funding cuts included in the One Big Beautiful Bill Act (OBBBA) signed into law July 4.

Adding insult to injury, the Center for Medicare and Medicaid services issued a 913-page proposed rule last Tuesday that includes unwelcome changes especially troublesome for hospitals i.e. adoption of site neutral payments, expansion of hospital price transparency requirements, reduction of inpatient-only services, acceleration of hospital 340B discount repayment obligations and more.

The combination of the two is bad news for healthcare overall and hospitals especially: the timing is precarious:

Economic uncertainty: Economists believe a recession is less likely but uncertainty about tariffs, fear about rising inflation, labor market volatility a housing market slowdown and speculation about interest rates have capital markets anxious. Healthcare is capital intense: the impact of the two in tandem with economic uncertainty is unsettling.

Consumer spending fragility: Consumer spending is holding steady for the time being but housing equity values are dropping, rents are increasing, student loan obligations suspended during Covid are now re-activated, prices for hospital and physicians are increasing faster than other necessities and inflation ticked up slightly last month. Consumer out-of-pocket spending for healthcare products and services is directly impacted by purchases in every category.

Heightened payer pressures: Insurers and employers are expecting double-digit increases for premiums and health benefits next year blaming their higher costs on hospitals and drugs, OBBBA-induced insurance coverage lapses and systemic lack of cost-accountability. For insurers, already reeling from 2023-2024 financial reversals, forecasts are dire. Payers will heighten pressure on healthcare providers—especially hospitals and specialists—as a result.

Why healthcare appears to have borne the brunt of the funding cuts in the OBBBA is speculative:

Might a case have been made for cuts in other departments? Might healthcare programs other than Medicaid have been ripe for “waste, fraud and abuse” driven cuts? Might technology-driven administrative costs reductions across the expanse of federal and state government been more effective than DOGE- blunt experimentation?

Healthcare is 18% of the GDP and 28% of total federal spending: that leaves room for cuts in other industries.

Why hospitals, along with nursing homes and public health programs, are likely to bear the lion’s share of OBBBA’ cut fallout and CMS’ proposed rule disruptions is equally vexing. Might the high-profile successes of some not-for-profit hospital operators have drawn attention? Might Congress have been attentive to IRS Form 990 filings for NFP operators and quarterly earnings of investor-owned systems and assume hospital finances are OK? Might advocacy efforts to maintain the status quo with facility fees, 340B drug discounts, executive compensation et al been overshadowed by concerns about consolidation-induced cost increases and disregard for affordability? Hospital emergency rooms in rural and urban communities, nursing homes, public health programs and many physicians will be adversely impacted by the OBBBA cuts: the impact will vary by state. What’s not clear is how much.

My take:

Having read both the OBBBA and CMS proposed rules and observed reactions from industry, two things are clear to me:

The antipathy toward the healthcare industry among the public and in Congress played a key role in passage of the OBBBA and regulatory changes likely to follow.

Polls show three-fourths of likely voters want to see transformational change to healthcare and two-thirds think the industry is more concerned with its profit over their care: these views lend to hostile regulatory changes. The public and the majority of elected officials think the industry prioritizes protection of the status quo over obligations to serve communities and the greater good.

The result: winners and losers in each sector, lack of continuity and interoperability, runaway costs and poor outcomes.

No sector in healthcare stands as the surrogate for the health and wellbeing of the population. There are well-intended players in each sector who seek the moral high ground for healthcare, but their boards and leaders put short-term sustainability above long-term systemness and purpose. That void needs to be filled.

The timing of these changes is predictably political.

Most of the lower-cost initiatives in both the OBBBA changes and CMS proposals carry obligations to commence in 2026—in time for the November 2026 mid-term campaigns. Most of the results, including costs and savings, will not be known before 2028 or after. They’re geared toward voters inclined to think healthcare is systemically fraudulent, wasteful and self-serving.

And they’re just the start: officials across the Departments of Health and Human Services, Justice, Commerce, Labor and Veterans Affairs will add to the lists.

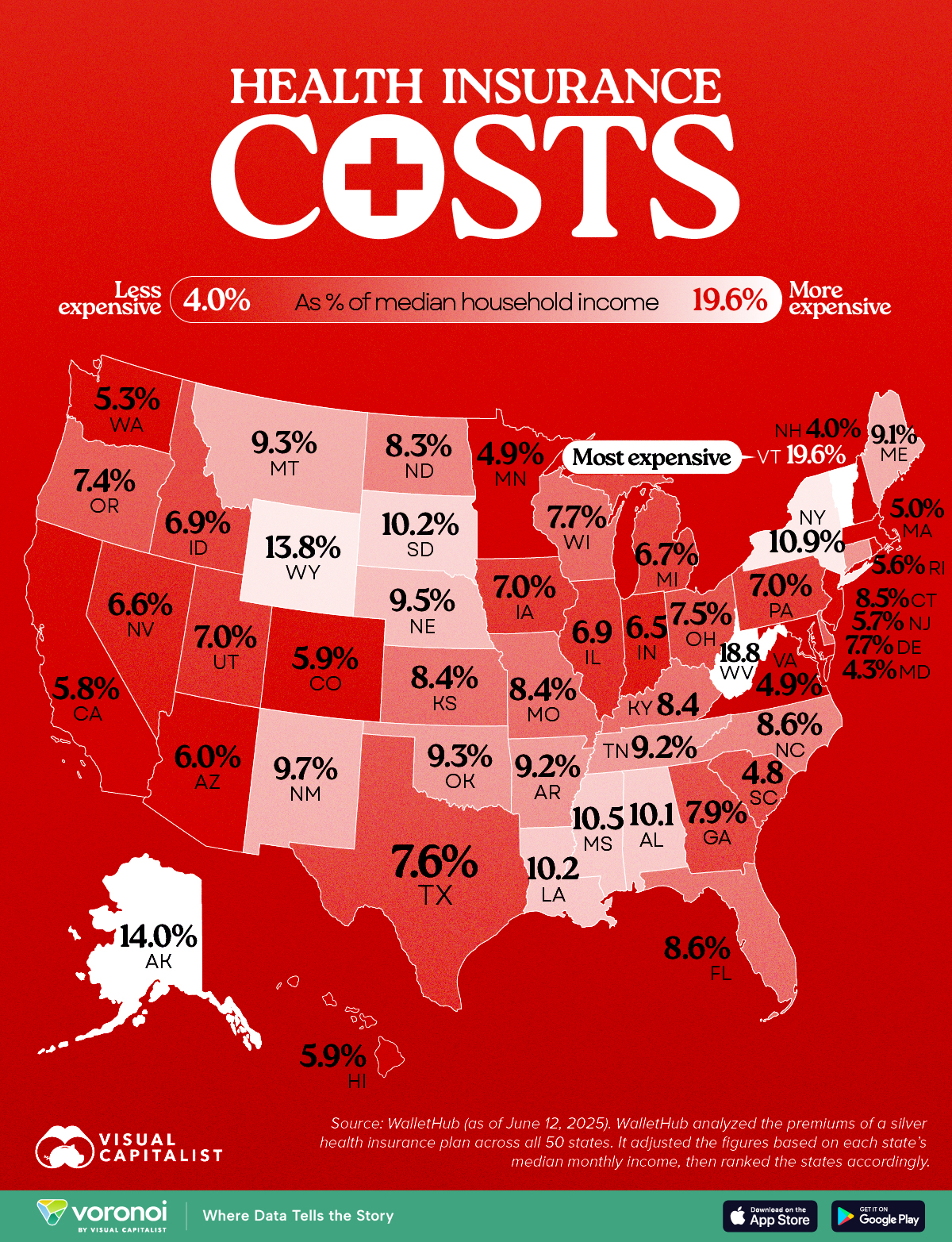

Health Insurance as a Share of Median Income by U.S. State

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

Key Takeaways

Vermont tops the list, with insurance costing 19.6% of median income.

New Hampshire residents spend just 4% of their income on health insurance, the lowest in the nation.

Americans pay wildly different amounts for health insurance depending on where they live. This map shows which states pay the most (and least) when health insurance costs are measured as a share of median income.

The data for this visualization comes from WalletHub. It analyzed silver-tier health plan premiums in all 50 states and compared them to local median incomes to determine cost burdens.

Vermont and West Virginia Lead in Cost Burden

In Vermont, residents spend 19.6% of their monthly income on health insurance, the highest share in the country. West Virginia follows closely at 18.8%.

The South and Mountain West Feel the Pinch

Many Southern and Mountain West states, like Mississippi, Wyoming, and Louisiana, also rank high in insurance cost burden. These regions tend to have poorer health outcomes and lower median incomes, exacerbating affordability issues. As Brookings notes, Medicaid expansion status and rural demographics heavily influence insurance markets in these areas.

New Hampshire and the Northeast Are Least Burdened

New Hampshire residents spend just 4% of their income on health insurance, the lowest in the nation.

Massachusetts, Maryland, and Minnesota also enjoy low cost burdens. These states often have robust state-run exchanges, higher incomes, and broader Medicaid expansion, all of which help reduce costs.

Medicaid cuts have received the lion’s share of attention from critics of Republicans’ sweeping tax cuts legislation, but the GOP’s decision not to extend enhanced ObamaCare subsidies could have a much more immediate impact ahead of next year’s midterms.

Extra subsidies put in place during the coronavirus pandemic are set to expire at the end of the year, and there are few signs Republicans are interested in tackling the issue at all.

To date, only Sens. Lisa Murkowski (R-Alaska) and Thom Tillis (R-N.C.) have spoken publicly about wanting to extend them.

The absence of an extension in the “big, beautiful bill” was especially notable given the sweeping changes the legislation makes to the health care system, and it gives Democrats an easy message: If Republicans in Congress let the subsidies expire at the end of the year, premiums will spike, and millions of people across the country could lose health insurance.

In a statement released last month as the House was debating its version of the bill, House and Senate Democratic health leaders pointed out what they said was GOP hypocrisy.

“Their bill extends hundreds of tax policies that expire at the end of the year. The omission of this policy will cause millions of Americans to lose their health insurance and will raise premiums on 24 million Americans,” wrote Senate Finance Committee ranking member Ron Wyden (D-Ore.), House Ways and Means Committee ranking member Richard Neal (D-Mass.) and House Energy and Commerce Committee ranking member Frank Pallone (D-N.J.).

“The Republican failure to stop this premium spike is a policy choice, and it needs to be recognized as such.”

More than 24 million Americans are enrolled in the insurance marketplace this year, and about 90 percent — more than 22 million people — are receiving enhanced subsidies.

“All of those folks will experience quite large out-of-pocket premium increases,” said Ellen Montz, who helped run the federal ObamaCare exchanges under the Biden administration and is now a managing director with Manatt Health.

“When premiums become less affordable, you have this kind of self-fulfilling prophecy where the youngest and the healthiest people drop out of the marketplace, and then premiums become even less affordable in the next year,” Montz said.

The subsidies have been an extremely important driver of ObamaCare enrollment. Experts say if they were to expire, those gains would be erased.

According to the Congressional Budget Office (CBO), 4.2 million people are projected to lose insurance by 2034 if the subsidies aren’t renewed.

Combined with changes to Medicaid in the new tax cut law, at least 17 million Americans could be uninsured in the next decade.

The enhanced subsidies increase financial help to make health insurance plans more affordable. Eligible applicants can use the credit to lower insurance premium costs upfront or claim the tax break when filing their return.

Premiums are expected to increase by more than 75 percent on average, with people in some states seeing their payments more than double, according to health research group KFF.

Devon Trolley, executive director of Pennie, the Affordable Care Act (ACA) exchange in Pennsylvania, said she expects at least a 30 percent drop in enrollment if the subsidies expire.

The state starts ramping up its open enrollment infrastructure in mid-August, she said, so time is running short for Congress to act.

“The only vehicle left for funding the tax credits, if they were to extend them, would be the government funding bill with a deadline of September 30, which we really see as the last possible chance for Congress to do anything,” Trolley said.

Trolley said three-quarters of enrollees in the state’s exchange have never purchased coverage without the enhanced tax credits in place.

“They don’t know sort of a prior life of when the coverage was 82 percent more expensive. And we are very concerned this is going to come as a huge sticker shock to people, and that is going to significantly erode enrollment,” Trolley said.

The enhanced subsidies were first put into effect during the height of the coronavirus pandemic as part of former President Biden’s 2021 economic recovery law and then extended as part of the Inflation Reduction Act.

The CBO said permanently extending the subsidies would cost $358 billion over the next 10 years.

Republicans have balked at the cost. They argue the credits hide the true cost of the health law and subsidize Americans who don’t need the help. They also argue the subsidies have been a driver of fraudulent enrollment by unscrupulous brokers seeking high commissions.

Sen. Bill Cassidy (R-La.), chair of the Senate Health, Education, Labor and Pensions Committee, last year said Congress should reject extending the subsidies.

The Republican Study Committee’s 2025 fiscal budget said the subsidies “only perpetuate a never-ending cycle of rising premiums and federal bailouts — with taxpayers forced to foot the bill.”

But since 2020, enrollment in the Affordable Care Act marketplace has grown faster in the states won by President Trump in 2024, primarily rural Southern red states that haven’t expanded Medicaid. Explaining to millions of Americans why their health insurance premiums are suddenly too expensive for them to afford could be politically unpopular for Republicans.

According to a recent KFF survey, 45 percent of Americans who buy their own health insurance through the ACA exchanges identify as Republican or lean Republican. Three in 10 said they identify as “Make America Great Again” supporters.

“So much of that growth has just been a handful of Southern red states … Texas, Florida, Georgia, the Carolinas,” said Cynthia Cox, vice president at KFF and director of the firm’s ACA program. “That’s where I think we’re going to see a lot more people being uninsured.”

Health insurers and their lobbying arms have spent $476.5 million since 2020 to block reform, protect profits, and mislead the public — and it’s coming straight from our premiums and tax dollars.

AHIP, the big PR and lobbying outfit for most health insurers, undoubtedly believes the praise it got from Trump administration officials and some members of Congress this week – when it announced changes insurers presumably will make voluntarily to alleviate the burden of prior authorization demands on patients and health care providers – has taken the heat off insurers. AHIP’s message to Washington politicos: You don’t need to pass any new laws to make us do the right thing. You can trust us, despite our decades of engaging in untrustworthy behavior to maximize profits.

After all, AHIP is nothing more than a PR and lobbying shop with millions of our dollars to play with. It has zero ability to force insurers to do what AHIP claims they will do. I know this because I worked closely with AHIP during my 20 years in the industry and represented Cigna on its strategic communications committee.

From Fox to “Fixer”?

AHIP pulled off its big show on Monday – and got plenty of generally fawning press coverage – because of all the money it and affiliated insurers throw around Washington every year to protect what has become an incredibly profitable status quo.

Collectively, the seven biggest for-profit insurers reported $70 billion in profits last year.

(Beleauered UnitedHealth alone reported $34.4 million in operating earnings.) And that’s just seven among dozens. One way they make that kind of dough, for their shareholders and top executives, is by using prior authorization to avoid paying for patients’ medically necessary care. Many people die as a result, while investors get richer. It’s that simple and that cold.

So just how much money does AHIP and the insurance industry spend to bamboozle members of Congress and the White House every year? We’re talking stupid money. And orders of magnitude more than nonprofits that advocate for reforms that would benefit patients instead of shareholders.

Nearly Half a Billion Ways They Tip the Scale

To find out just how much, I turned to OpenSecrets and did some math. OpenSecrets, as a reminder, is the well-named organization that keeps tabs on campaign contributions and lobbying expenses.

What I discovered is that AHIP has spent almost $65 million lobbying Congress and the Biden and Trump administrations since 2020. Its cousin, the Blue Cross Blue Shield Association, has spent even more. More than twice as much more.

And that, folks, is just the tip of the iceberg, and it doesn’t even include the tens of millions the industry spends on massive advertising campaigns inside the DC beltway that it’s not required to report. Or the dark money ads and advocacy the industry bankrolls.

But just the lobbying totals are mind-blowing. When you factor in the money spent by the big seven insurers and the other PR and lobbying groups that insurers funnel money to, the total grows to almost $500 million. You read that right: nearly half a billion dollars.

Most of that spending was during the Biden administration, but the industry is on track to break spending records during the first year of the current Trump administration. They are lobbying not only to beat back new laws and regulations that could constrain their prior authorization practices but also to protect their biggest cash cows: Medicare Advantage and their pharmacy benefit managers (PBMs).

Three PBMs – owned by Cigna, CVS/Aetna and UnitedHealth –control 80% of the pharmacy benefit market and determine which drugs we’ll have access to and how much we have to pay out of pocket even with insurance.

The Big Number

$476.5 million – That’s the amount of money health insurance corporations and four of their PR and lobbying groups – AHIP, BCBSA (which includes contributions from Elevance/Anthem as well as numerous other BCBS companies), the Pharmaceutical Care Management Association and the Better Medicare Alliance – have collectively spent on lobbying Congress and federal regulators between January 1, 2020, and March 31, 2025.

Keep in mind that that money is not coming out of executives’ paychecks. It’s coming out of our pockets. Insurers skim money from our premiums and taxes to finance their propaganda and lobbying efforts to keep the gravy train rolling. And it’s in addition to all the campaign cash they dole out every year, which I tabulated recently.

This is not to say that reform is impossible. Scrappy advocacy groups with a tiny fraction of that total have scored important victories over the years. But it is why progress is so slow and setbacks are so frequent.

But just imagine how all that money could be put to better use to ensure that all Americans, including those with insurance, are able to get the care they need when they need it. It’s clear that in addition to reforming our health care system, we need political reforms that make it more difficult for big corporations and their trade groups to influence elections and public policy.

Medicaid serves as a vital source of health insurance coverage for Americans living in rural areas, including children, parents, seniors, individuals with disabilities, and pregnant women. Congressional lawmakers are currently considering more than $800 billion in cuts to the Medicaid program, which would reduce Medicaid funding and terminate coverage for vulnerable Americans.

The proposed changes would also result in a significant reduction in Medicaid reimbursement that could result in rural hospital closures.

The National Rural Health Association recently partnered with experts from Manatt Health to shed light on the potential impacts of those cuts on rural residents and the hospitals that care for them over the next decade.

NRHA held a press conference on June 24 that can be accessed with passcode MBTZf4$H. NRHA chief policy officer Carrie Cochran-McClain discussed the findings with Manatt Health partner and former deputy administrator at CMS Cindy Mann and the real world implications of the details of this report with three NRHA member hospital and health system leaders

Report findings provide insight into the impact on rural America at a critical moment in the Congressional debate over the future of the reconciliation package.

The report shows the significant impact from coverage losses that rural communities will face given:

Medicaid plays an outsized role in rural America, covering a larger share of children and adults in rural communities than in urban ones.

Nearly half of all children and one in five adults in small towns and rural areas rely on Medicaid or CHIP for their health insurance.

Medicaid covers nearly one-quarter of women of childbearing age and finances half of all births in these communities.

According to Manatt’s estimates, rural hospitals will lose 21 cents out of every dollar they receive in Medicaid funding due to the One Big Beautiful Bill Act. Total cuts in Medicaid reimbursement for rural hospitals—including both federal and state funds—over the ten-year period outlined in the bill would reach almost $70 billion for hospitals in rural areas.

Reductions in Medicaid funding of this magnitude would likely accelerate rural hospital closures and reduce access to care for rural residents, exacerbating economic hardship in communities where hospitals are major employers.

As a key insurer in rural communities, Medicaid provides a financial lifeline for rural health care providers — including hospitals, rural health clinics, community health centers, and nursing homes—that are already facing significant financial distress. These cuts may lead to more hospitals and other rural facility closures, and for those rural hospitals that remain open, lead to the elimination or curtailment of critical services, such as obstetrics.

“Medicaid is a substantial source of federal funds in rural communities across the country. The proposed changes to Medicaid will result in significant coverage losses, reduce access to care for rural patients, and threaten the viability of rural facilities,” said Alan Morgan, CEO of the National Rural Health Association.

“It’s very clear that Medicaid cuts will result in rural hospital closures resulting in loss of access to care for those living in rural America.”

A media briefing will be held on Tuesday, June 24, from noon to 1:00 PMEST to provide more information about the analysis. This event will feature representatives from NRHA, Manatt Health, and rural hospital leaders across the country. Questions may be submitted in advance, as well as during the press conference. To register for and join the media briefing, click on the Zoom link here.

NRHA is a non-profit membership organization that provides leadership on rural health issues with tens of thousands of members nationwide. Our membership includes nearly every component of rural America’s health care, including rural community hospitals, critical access hospitals, doctors, nurses, and patients. We work to improve rural America’s health needs through government advocacy, communications, education, and research. Learn more about the association at RuralHealth.US.

About Manatt Health

Manatt Health is a leading professional services firm specializing in health policy, health care transformation, and Medicaid redesign. Their modeling draws upon publicly available state data including Medicaid financial management report data from the Centers for Medicare and Medicaid Services, enrollment and expenditure data from the Medicaid Budget and Expenditure System, and data from the Medicaid and CHIP Payment and Access Commission. The Manatt Health Model is tailored specifically to rural health and has been reviewed in consultation with states and other key stakeholders.

The Supreme Court on Friday upheld a key Affordable Care Act requirement that insurance companies cover certain preventative measures recommended by an expert panel.

Justices upheld the constitutionality of the provision in a 6-3 decision and protected access to preventative care for about 150 million Americans.

The justices found that the secretary of the Department of Health and Human Services has the power to appoint and fire members of the U.S. Preventative Services Task Force (USPSTF).

The cases started when a small business in Texas and some individuals filed a lawsuit against the panel’s recommendation that pre-exposure prophylaxis (PreP) for HIV be included as a preventative care service.

They argued that covering PreP went against their religious beliefs and would “encourage homosexual behavior, intravenous drug use, and sexual activity outside of marriage between one man and one woman.”

The plaintiffs further argued that the USPSTF mandates are unconstitutional because panel members are “inferior officers” who are not appointed by the president or confirmed by the Senate.

While the panel is independent, they said that since their decisions impact millions of people members should be confirmed.

A U.S. district judge in 2023 ruled that all preventative-care coverage imposed since the ACA was signed into law areinvalid and a federal appeals court judge ruled in agreement last year.

The Biden administration appealed the rulings to the Supreme Court, and the Trump administration chose to defend the law despite its long history of disparaging Obamacare.

Though public health groups celebrated the ruling Friday, some noted another potential outcome.

“While this is a foundational victory for patients, patients have reason to be concerned that the decision reaffirms the ability of the HHS secretary, including our current one, to control the membership and recommendations of the US Preventive Services Task Force that determines which preventive services are covered,” Anthony Wright, executive director of Families USA, said in a statement.

“We must be vigilant to ensure Secretary Kennedy does not undo coverage of preventive services by taking actions such as his recent firing of qualified health experts from the CDC’s independent vaccine advisory committee and replacing them with his personal allies.”

Last Thursday, the Make America Healthy Again Commission released its 68-page report “Making America’s Children Healthy Again Assessment” featuring familiar themes—the inadequacy of attention to chronic disease by the health system, the “over-medicalization” of patient care vis a vis prescription medicines et al, the contamination of the food-supply by harmful ingredients, and more.

HHS Secretary Kennedy, EPA Administrator Zeldin and Agriculture Secretary Rollins pledged war on the corporate healthcare system ‘that has failed the public’ and an all-of-government approach to remedies for burgeoning chronic care needs.

Also Thursday, the House of Representatives passed its budget reconciliation bill by a vote of 215-214. The 1000-page bill cuts federal spending by $1.6 trillion (including $698 billion from Medicaid) and adds $2.3 trillion (CBO estimate/$3.4 to $5 trillion per Yale Budget Lab) to the national deficit over the next decade. It now goes to the Senate where changes to reduce federal spending to pre-pandemic level will be the focus.

With a 53-37 advantage and 22 of the 36 Senate seats facing mid-term election races in November, 2026, the Senate Republican version of the “Big Beautiful Bill” will include more spending cuts while pushing more responsibility to states for funding and additional cuts. The gap between the House and Senate versions will be wider than currently anticipated by House Republicans potentially derailing the White House promise of a final Big Beautiful Bill by July 4.

And, over the last week and holiday weekend, the President announced a new 25% tariff on Apple devices manufactured in India and new tariffs targeting the EU; threatened cuts to federal grants to Harvard and cessation of its non-citizen student enrollment, a ‘get-tougher’ policy on Russia to pressure an end of its Ukraine conflict, and a pledge to Americans on Memorial that it will double down on ‘peace thru strength’ in its Make America Great Again campaign.

These have 2 things in common:

1-They’re incomplete. None is a finished product.

The MAHA Commission, working with the Departments of Health & Human Services, Interior and Agriculture, is tasked to produce another report within 90 days to provide more details about a plan. The FY26 budgeting process is wrought with potholes—how to satisfy GOP deficit hawks vs. centrist lawmakers facing mid-term election, how to structure a bill that triggers sequestration cuts to Medicare (projected $490 billion/10 yrs. per CBO), how to quickly implement Medicaid work requirements and marketplace enrollment cuts that could leave insurance coverage for up to 14 million in limbo, and much more. And the President’s propensity to “flood the zone” with headline-grabbing Truth Social tweets, Executive Orders and provocative rhetoric on matters at home and abroad will keep media occupied and healthcare spending in the spotlight.

2-They play to the MAGA core.

The MAGA core is primarily composed of older, white, Christian men driven by a belief that the United States has lost its exceptionalism through WOKE policies i.e. DEI in workplaces and government, open borders, globalization and excessive government spending and control. In the 2024 Presidential election, the MAGA core expanded incrementally among Black, Hispanic, and younger voters whose concerns about food, energy and housing prices prompted higher-than expected turnout. The MAGA core believes in meritocracy, nationalism, smaller government, lower taxes, local control and free-market policies that encourage private investment in the economy. The core is price sensitive.

The health system per se is not a concern but it’s the affordability and lack of price transparency are. They respect doctors and frontline caregivers but think executives are overpaid and prone to self-promotion. And the MAGA core think lawmakers have been complicit in the system’s lack of financial accountability largely beneficial to elites.

Looking ahead to the summer, a “Big Beautiful Bill” will pass with optics that allow supporters to claim fiscal constraint and lower national debt and opponents to decry insensitive spending cuts and class warfare against low-and-middle-class households.

Federal cuts to Medicaid and SNAP (Supplemental Nutrition Assistance Program) will be prominent targets in both groups—one a portrayal of waste, fraud and abuse and the other tangible evidence of societal inequity and lack of moral purpose. Each thinks the other void of a balanced perspective. Each thinks the health system is underperforming and in need of transformational change but agreement about how to get there unclear.

As MAHA promotes its agenda, Congress passes a budget and MAGA advances its anti-establishment agenda vis a vis DOGE et al, healthcare operators will be in limbo. The dust will settle somewhat this summer, but longer-term bets will be modified for most organizations as compliance risks change, state responsibilities expand, capital markets react and Campaign 2026 unfolds.

And in most households, concern about the affordability of medical care will elevate as federal and state funding cuts force higher out of pocket costs on consumers and demand for lower prices.

The summer will be busy for everyone in healthcare.

PS: Changes in the housing market are significant for healthcare: 36% of the CPI is based on shelter vs. 8% for medical services & products, 14% for food and 6% for energy/transportation. While the overall CPI increased 2.3% in the last 12 months, medical services prices increased 3.1%. contributing to heightened price sensitivity and delayed payments.

It has not escaped lawmaker attention: revenue cycle management business practices (debt collection) are being scrutinized in hospitals and community benefit declarations by not-for-profit hospitals re-evaluated. The economics of healthcare are not immune to broader market trends nor is spending for healthcare in households protected from day-to-day fluctuations in prices for other goods and services.