Large, not-for-profit hospitals/health systems are getting a disproportionate share of unflattering attention these days. Last week was no exception: Here’s a smattering of their coverage:

Jiang et al “Factors Associated with Hospital Commercial Negotiated Price for Magnetic Resonance Imaging of Brain” JAMA Network Open March 21. 2023;6(3):e233875. doi:10.1001/jamanetworkopen.2023.3875

Whaley et al What’s Behind Losses At Large Nonprofit Health Systems? Health Affairs March 24, 2023 10.1377/forefront.20230322.44474

A Pa. hospital’s revoked property tax exemption is a ‘warning shot’ to other nonprofits, expert says KYW Radio Philadelphia March 24, 2023 ww.msn.com/en-us/news/us/a-pa-hospital-s-revoked-property-tax-exemption-is-a-warning-shot-to-other-nonprofits-expert-says

These come on the heals of the Medicare Advisory Commission’s (MedPAC) March 2023 Report to Congress advising that all but safety-net hospitals are in reasonably good shape financially (contrary to industry assertions) and increased lawmaker scrutiny of “ill-gotten gains” in healthcare i.e., Moderna’s vaccine windfall, Medicare Advantage overpayments and employer activism about hospital price-gauging in several states.

Like every sector in healthcare, hospitals enter budget battles with good stories to tell about cost-reductions and progress in price transparency compliance. But in the current political and economic environment, large, not-for-profit hospitals and health systems seem to be targets of more adverse coverage than others as illustrated above. Like many NFP institutions in society (higher education, organized religion, government), erosion of trust is palpable. Not-for-profit hospitals and health systems are no exception.

The themes emerging from last week’s coverage are familiar:

‘Not-for-profit hospitals/health systems, do not provide value commensurate with the tax exemptions they get.’

‘Not for profit hospitals & health systems take advantage of their markets and regulations to create strong brands and generate big profits.’.

‘Not for profit hospitals & health systems charge more than investor-owned hospitals: the victims are employers and consumers who pay higher-than-necessary prices for their services.’

‘NFP operators invest in risky ventures: when the capital market slumps, they are ill-prepared to manage. Risky investments, not workforce and supply chain issues, are the root causes of NFP financial stress. They’re misleading the public purposely.’

‘Executives in NFP systems are overpaid and patient collection policies are more aggressive than for-profits. NFP boards are ineffective.’

The stimulants for this negative attention are equally familiar:

Proprietary studies by think tanks, trade associations, labor unions and consultancies designed to “prove a point” for/against not-for-profit hospitals/health systems.

Government reports about hospital spending, waste, fraud, workforce issues, patient safety, concentration and compliance with transparency rules.

Aggressive national/local reporting by journalists inclined to discount NFP messaging.

Public opinion polls about declining trust in the system and growing concern about price transparency, affordability and equitable access.

Politicians who use soundbites and dog whistles about NFP hospitals to draw attention to themselves.

The cumulative effect of these is confusion, frustration and distrust of not-for-profit hospitals and health systems. Most believe not-for-profit hospitals/health systems do not own the moral high ground they affirm to regulators and their communities (though religiously-affiliated systems have an edge). Most are unaware that more than half of all hospitals (54%) are not-for-profit and distinctions between safety net, rural, DSH, teaching and other forms of NFP ownership are non-specific to their performance.

What’s clear to the majority is that hospitals are expensive and essential. They’re soft targets representing 31.1% of the health system’s total spend ($4.3 trillion in 2021) increasing 4.9% annually in the last decade while inflation and GDP growth were less.

So why are not-for-profit systems bearing the brunt of hospital criticism?

Simply put: many NFP systems act more like Big Business than shepherds of community health. In fact, 4 of the top 10 multi-hospital system operators is investor owned: HCA (184), CHS (84), LifePoint (84), Tenet (65). In addition, 3 others are in the top 50: Ardent (30), UHS (26), Quorum (22). So, corporatization of hospital care using private capital and public markets for growth is firmly entrenched in the sector exposing not-for-profit operators to competition that’s better funded and more nimble. And, per industry studies, not-for-profits tend to stay in markets longer and operate unprofitable services more frequently than their investor-owned competitors. But does this matter to insurers, community leaders, legislators, employers, hospital employees and physicians? Some but not much.

My take:

There are no easy answers for not-for-profit hospitals/heath systems. The issue is about more than messaging and PR. It’s about more than Medicare reimbursement (7.5% below cost), protecting programs like 340B, keeping tax exemptions and maintaining barriers against physician-owned hospitals. The issue is NOT about operating income vs. investment income: in every business, both are essential and in each, economic cycles impact gains/losses. Each of these is important but only band-aids on an open wound in U.S. healthcare.

Near-term (the next 2 years), opportunities for not-for-profit hospitals involve administrative simplification to reduce costs and improve the efficiencies and effectiveness of the workforce. Clinical documentation using ChatGPT/Bard-like tools can have a massive positive impact—that’s just a start. Advocacy, public education and Board preparedness require bigger investments of time and resources. But that’s true for every hospital, regardless of ownership. These are table stakes to stay afloat.

The longer-term issue for NFPs is bigger:

It’s about defining the future of the U.S. health system in 2030 and beyond—the roles to be played and resources necessary for it to skate to where the puck is going. It’s about defining the role played by private employers and whether they’ll pay 220% more than Medicare pays to keep providers and insurers solvent. It’s about how underserved and unhealthy people are managed. It’s about defining systemness in healthcare and standardizing processes. It’s about defining sources of funding and optimal use of resources. Not-for-profit systems should drive these discussions in the communities they serve and at a national level.

MedPAC’s 17 member Commission will play a vital role, but equally important to this design process are inputs from employers, consumers and thought leaders who bring fresh insight. Until then, not-for-profit health systems will be soft targets for unflattering media because protecting the status quo is paramount to insiders who benefit from its dysfunction. Incrementalism defined as innovation is a recipe for failure.

It’s time to begin a discussion about the future of the U.S. health system—all of it, not just high-profile sectors like not-for-profit hospitals/health systems who are currently its soft target.

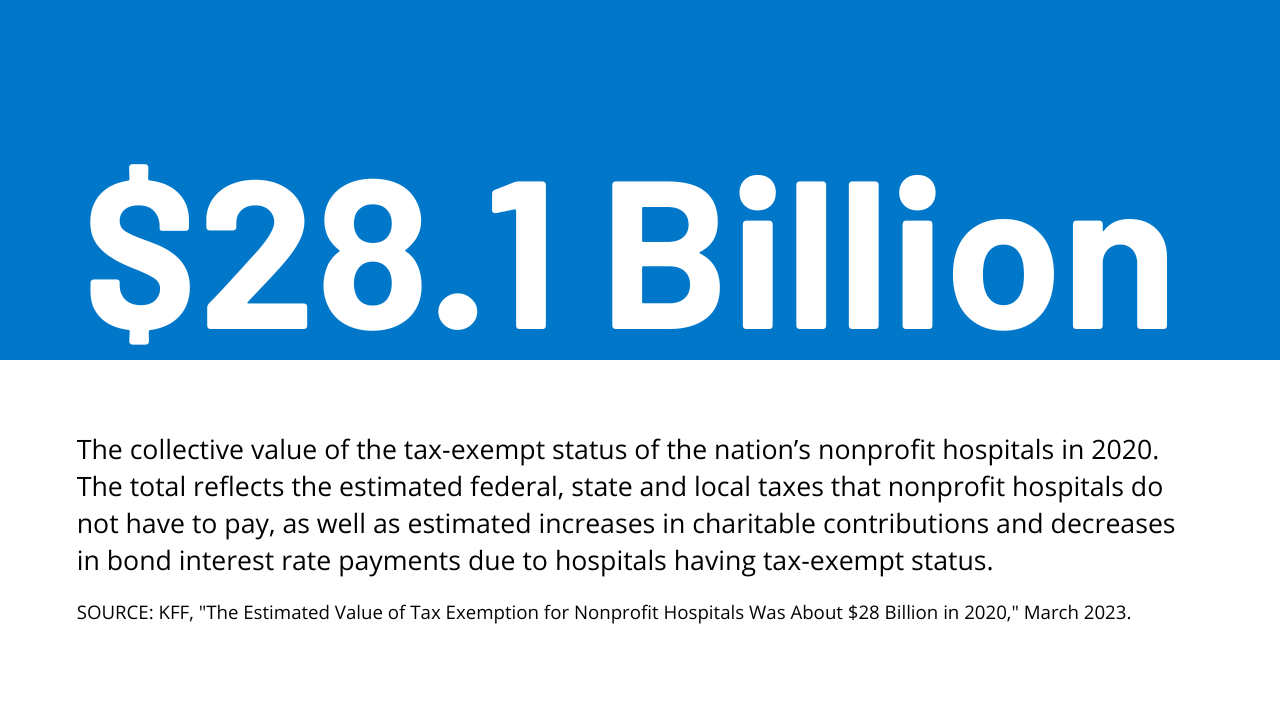

Over the years, somepolicymakers have questioned whether nonprofit hospitals—which account for nearly three-fifths (58%) of community hospitals—provide sufficient benefit to their communities to justify their exemption from federal, state, and local taxes.

This issue has been the subject of renewed interest in light of reports of nonprofit hospitals taking aggressive steps to collect unpaid medical bills, including suingpatients over unpaid medical debt, including patients who are likely eligible for financial assistance. Further, recent research indicates that nonprofithospitals devote a similar or smaller share of their operating expenses to charity care in comparison to for-profit hospitals. In light of these concerns, several policy ideas have been floated to better align the level of community benefits provided by nonprofit hospitals with the value of their tax exemption.

This data note provides an estimate of the value of tax exemption for nonprofit facilities based on hospital cost reports, filings with the Internal Revenue Service (IRS), and American Hospital Association (AHA) survey data (see Methods for additional details). We define the value of tax exemption as the benefit of not having to pay federal and state corporate income taxes, typically not having to pay state and local sales taxes and local property taxes, and any increases in charitable contributions and decreases in bond interest rate payments that might arise due to receiving tax-exempt status.

Results

The total estimated value of tax exemption for nonprofit hospitals was about $28 billion in 2020 (Figure 1). This represented over two-fifths (44%) of net income (i.e., revenues minus expenses) earned by nonprofit facilities in that year. To put the value of tax exemption in perspective, our estimate is similar to the total value of Medicare and Medicaid disproportionate share hospital (DSH) payments in the same year ($31.9 billion in fiscal year 2020) (i.e., supplemental payments to hospitals that care for a disproportionate share of low-income patients which are intended, in part, to offset the costs of charity care and other uncompensated care).

The estimated value of federal tax-exempt status was $14.4 billion in 2020, which represents about half (51%) of the total value of tax exemption. This is primarily due to the estimated value of not having to pay federal corporate income taxes ($10.3 billion). In addition, we assumed that individuals contribute more to tax-exempt hospitals because they can deduct donations from their income tax base ($2.5 billion) and issue bonds at lower interest rates because the interest is not taxed ($1.6 billion). Our estimates of changes in charitable contributions and interest rates on bonds only account for federal tax rates for simplicity and may therefore understate the total value of tax exemption because they do not account for the effects of state taxes.

The total estimated value of state and local tax-exempt status was $13.7 billion in 2020, which represents about half (49%) of the total value of tax exemption. This amount includes the estimated value of not having to pay state or local sales taxes ($5.7 billion), local property taxes ($5.0 billion) or state corporate income taxes ($3.0 billion).

The total estimated value of tax exemption (about $28 billion) exceeded total estimated charity care costs ($16 billion) among nonprofit hospitals in 2020 (Figure 2), though charity care represents only a portion of the community benefits reported by these facilities. Hospital charity care programs provide free or discounted services to eligible patients who are unable to afford their care and represent one of several different types of community benefits reported by hospitals.

The Internal Revenue Service (IRS) also defines community benefits to include unreimbursed Medicaid expenses, unreimbursed health professions education, and subsidized health services that are not means-tested, among other activities. One study estimated that the value of tax exemption exceeded the value of community benefits broadly for about one-fifth (19%) of nonprofit hospitals during 2011-2018 or about two-fifths (39%) when considering the incremental value of community benefits provided relative to for-profit facilities. Other research suggests that nonprofithospitalsdevote a similar or smaller share of their operating expenses to charity care and unreimbursed Medicaid costs—which accounted for most of the value of community benefits in 2017—when compared to for-profit hospitals.

The value of tax exemption grew from about $19 billion in 2011 to about $28 billion in 2020, representing a 45 percent increase (Figure 3). The value of tax exemption increased in most of the years (7 out of 9) in our analysis, though there was a notable decrease of $5.8 billion in 2018. The largest single-year increase was $4.1 billion in 2020. The large decrease in the value of tax exemption in 2018 coincided with the implementation of the Tax Cuts and Jobs Act of 2017, which permanently reduced the federal corporate income tax rate from 35 to 21 percent and therefore decreased the value of being exempt from federal income taxes.

The large increase in the value of tax exemption in 2020 overlapped with the start of the COVID-19 pandemic. This increase primarily reflects a large increase in aggregate net income for nonprofit hospitals in 2020. Although there were disruptions in hospital operations in 2020, hospitals received substantial amounts of government relief, and it is possible that other sources of revenue, such as from investment income, may have also increased. Increases in net income in turn increased the value of not having to pay federal and state income taxes.

Increases in the estimated value of tax exemption over time also reflect net income growth that preceded the pandemic as well as increases in estimated property values, supply expenses, and charitable contributions, each of which would carry tax implications if hospitals lost their tax-exempt status (e.g., with some supply expenses being subject to sales taxes). Even when setting aside the strong financial performance of nonprofit hospitals in 2020 as a potential outlier, total net income among nonprofit facilities increased substantially in the preceding years, before increasing further in 2020. Although we are not able to directly observe the value of the real estate owned by hospitals, the estimated value of exemption from local property taxes—which is based on our analysis of property taxes paid by for-profit hospitals—increased by 63 percent from 2011 to 2019. Finally, the supply expenses in our analysis increased by 44 percent and charitable contributions increased by 49 percent from 2011 to 2019.

Discussion

The estimated value of tax exemption for nonprofit hospitals increased from about $19 billion in 2011 to about $28 billion in 2020. The rising value of tax exemption means that federal, state, and local governments have been forgoing increasing amounts of revenue over time to provide tax benefits to nonprofit hospitals, crowding out other uses of those funds. This has raised questions about whether nonprofit facilities provide sufficient benefit to their communities to justify this tax benefit. Federal regulations require, among other things, that nonprofit hospitals provide some level of charity care and other community benefits as a condition of receiving tax-exempt status. However, a 2020 Government Accountability Office (GAO) report raised questions about whether the government has adequately enforced this requirement. Further, some argue that the federal definition of “community benefits” is too broad—e.g., by including medical training and research that could benefit hospitals directly—though others believe that the definition is too narrow. Most states have additional community benefit requirements for nonprofit or broader groups of hospitals—such as providing charity care to patients below a specified income threshold—though there is little information about the effectiveness of these regulations or the extent to which they are enforced.

Several policy ideas have been floated at the federal and state level that would increase the regulation of community benefits spending among nonprofit hospitals or among hospitals more generally. These include proposals to create or expand state requirements that hospitals provide charity care to patients below a specified income threshold, mandate that nonprofit hospitals provide a minimum amount of community benefits, establish a floor-and-trade system where hospitals would be required to either provide a minimum amount of charity care or subsidize other hospitals that do so, create mechanisms to increase the uptake of charity care, expandoversight and enforcement of community benefit requirements, replace current tax benefits with a subsidy that is tied to the value of community benefits provided, and introducereforms intended to better align community benefits with local or regional needs.

These policy options would inevitably involve tradeoffs. While they may expand the provision of certain community benefits, hospitals would incur new costs as a result, which could in turn have implications for what services they offer, how much they charge commercially insured patients, and how much they invest in the quality of care.

At a meeting with hospital system CEOs last Wednesday, one asked: “has healthcare reached the tipping point?” I replied ‘not yet but it’s getting close.’

I iterated factors that make these times uniquely difficult in every sector:

An uncertain economy that’s unlikely to fully recover until next year.

The growth of Medicaid and Medicare coverage that shifts their financial shortfall to employers and taxpayers who are fed up and pushing back.

A vicious political environment that rewards partisan brinksmanship and focus-group tested soundbites to manipulate voters on complex issues in healthcare.

The growing domination of Big Business in each sector that have used acquisitions + corporatization to their advantage.

The widening role of private equity in funding non-conventional solutions that disrupt the status quo (and the uncertain future for many of these).

The federal courts system that’s increasingly the arbiter over access, fairness, quality and freedoms in healthcare.

The lingering impact of the pandemic.

And growing public disgust and distrust as the system’s altruism and good will is undermined by pervasive concern for profit.

Unprecedented! But events like those last week prompt hitting the pause button: not everyone pays attention to healthcare like many of us. The slaughter of 6 innocents in Nashville hit close to home: it’s about guns, mental health and life and death. The appeal of tech-giants to press the pause button on Generative AI for at least 6 months was sobering. The ravage of tornados that left thousands insecure without food, housing or hope seemed unfair. Mounting tensions with Russia and complex negotiations with China that reminded us that the U.S. competes in a global economy. And President Trump’s court appearance tomorrow will stoke doubt about our justice system at a time when it’s role in healthcare and society is expanding.

I am a healthcare guy. I am prone to see the world through the lens of the U.S. health industry and keen to understand its trends, tipping points and future. There’s plenty to watch: this week will be no exception. The punch list is familiar:

Medicaid coverage: Many will be watching the fallout of from state redetermination requirements for Medicaid coverage starting as soon as this week with disenrollment in Arizona, Arkansas, Idaho, New Hampshire and South Dakota.

Medicare Advantage: Health insurers will be modifying their Medicare Advantage strategies to adapt to CMS’ risk adjustment and Value-based Insurance Design modifications announced last week.

Prescription drug prices: PBMs and drug companies will face growing skepticism as Senate and House committees continue investigations about price gauging and collusion. Hospitals will be making adjustments to higher operating losses as states cut their Medicaid rolls.

Technology: The 7500 VIVA attendees will be doing follow-up to secure entrées for their technologies and solutions among prospective buyers.

Physicians: And physicians will intensify campaigns against insurers and hospitals now seen as adversaries while lobbying Congress for more money and greater income opportunities i.e., physician-owned hospitals.

Hospitals: On the offense against site-neutral payments, physician owned hospitals, drug prices and inadequate reimbursement from health insurers.

All will soldier on but the food fights in healthcare and broader headwinds facing the industry suggest a tipping point might be near.

I am not a fatalist: the future for healthcare is brighter than its past, but not for everyone. Strategies predicated on protecting the past are obsolete. Strategies that consider consumers incapable of active participation in the delivery and financing of their care are archaic. Strategies that depend on unbridled consolidation and opaque pricing are naïve. And strategies that limit market access for non-traditional players are artifacts of the gilded age gone by when each sector protected its own against infidels outside.

These times call for two changes in every board room and C Suite in of every organization in healthcare:

Broader vision: Understanding healthcare’s future in the broader context of American society, democracy and capitalism: Beltway insiders and academics prognosticate based on lag indicators that are decreasingly valid for forecasting. Media pundits on healthcare fail to report context and underpinnings. Management teams are operating under short-term financial incentives lacking longer-term applicability. Consultants are telling C suites what they want to hear. And boards are being mis-educated about trends of consequence that matter. Understanding the future and building response scenarios is out of sight and out of mind to insiders more comfortable being victims than creators of the new normal.

Board leadership: Equipping boards to make tough decisions: Governance in healthcare is not taken seriously unless an organization’s investors are unhappy, margins are shrinking or disgruntled employees create a stir. Few have a systematic process for looking at healthcare 10 years out and beyond their business. Every Board must refresh its thinking about what tomorrow in healthcare will be and adjust. It’s easier for board to approve plans for the near-term than invest for the long-term: that’s why outsiders today will be tomorrow’s primary incumbents.

So, is U.S healthcare near its tipping point? I don’t know for sure, but it seems clear the tipping point is nearer than at any point in its history. It’s time for fresh thinking and new players.

It feels like governance questions are coming to the fore in a lot of places these days, at least judging by several recent conversations we’ve had with health system CEOs. Probably not surprising, given the number of potential mergers and other partnerships under consideration.

As one CEO told us, growth byM&A raises particularly thorny issues for a not-for-profit system board. “Our governance structure grew out of a single hospital board, which was made up of community members and local physician leaders,” he told us. As the system acquired hospitals in adjacent markets, the combined board took on a representational character—each hospital had local stakeholders involved in governance. “Now we’re talking about merging with an out-of-state system, and our board suddenly seems way too parochial and unsophisticated. Everyone’s still asking what’s in it for their community.” That’s a frustration we hear frequently.

There are legitimate reasons why a tax-exempt community institution should have local representation on the board, advocating for local priorities and resources. But a larger, multi-state board must also oversee the entire portfolio of assets, and make trade-offs across markets, sometimes making decisions that favor one hospital over another.

The larger system board also has a greater need for sophistication, both on business and healthcare issues, as its members are often responsible for billions of dollars of assets. What frequently results from this tension is a nesting series of system and community boards, with varying degrees of accountability—a recipe for tangled, lengthy decision processes, and an enormous time-sink for senior system executives. We’re keeping our eye out for next-generation solutions to the governance question in healthcare—let us know what you’re seeing.

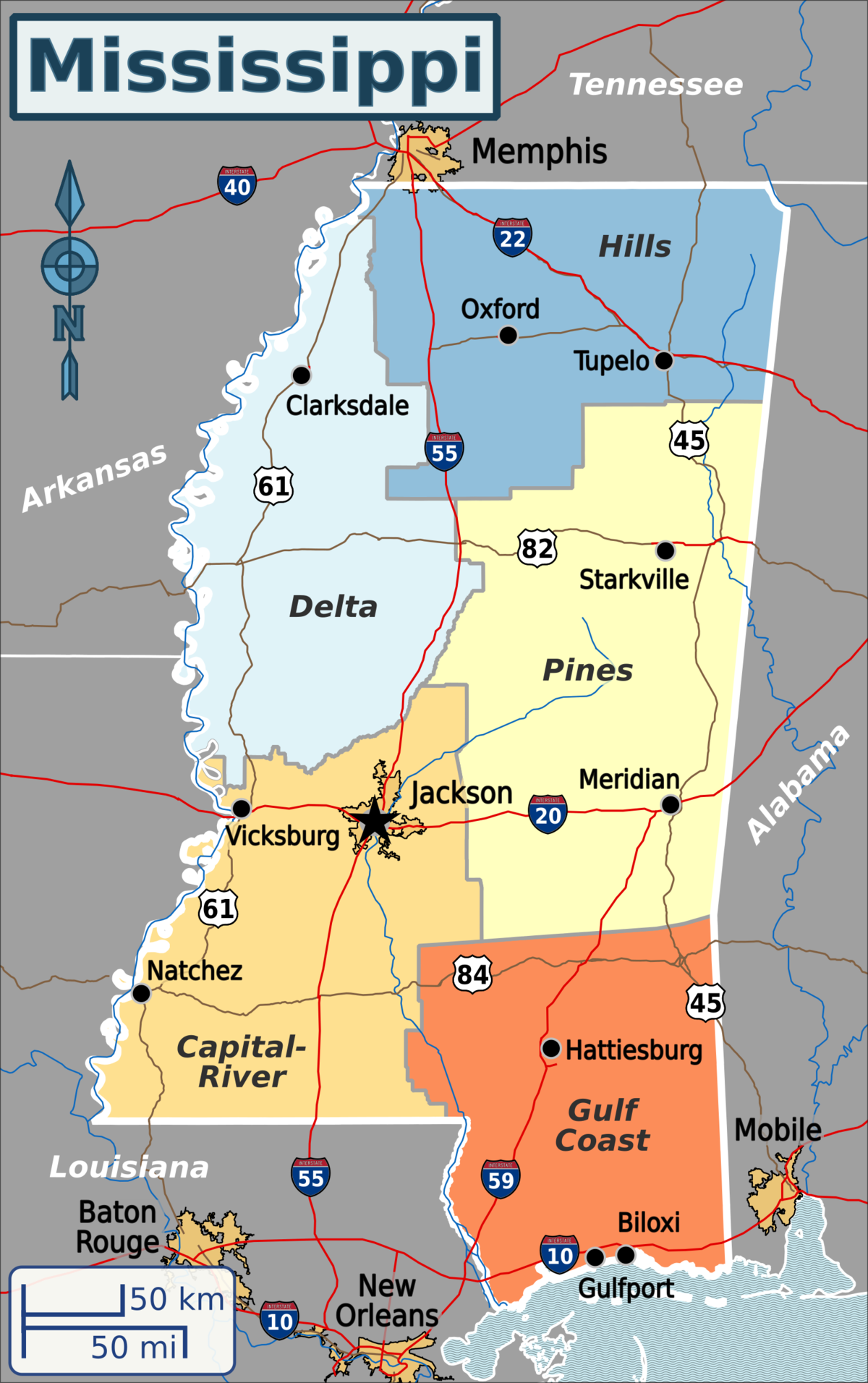

Published this week in the New York Times, this article describes the decaying state of Greenwood Leflore Hospital, a 117 year-old facility in the Mississippi Delta that may be within months of closure. While rural hospitals across the country are struggling, Mississippi’s firm opposition to Medicaid expansion has exacerbated the problem in that state, by depriving providers of an additional $1.4B per year in federal funds. Instead, only a few of the state’s 100-plus hospitals actually turn an annual profit, and uncompensated care costs are almost 10 percent of the average hospital’s operating costs.

Despite a dozen or more hospitals at imminent risk of closure, Mississippi officials would rather use the state’s $3.9B budget surplus to lower or eliminate the state income tax.

The Gist:Expanding Medicaid doesn’t just reduce rates of uncompensated care provided by hospitals, it changes the volume and type of care they provide.

Further, Medicaid expansion has been found to result in significant reductions in all-cause mortality.

Ensuring that low-income residents in Mississippi and other non-expansion states have access to Medicaid would allow providers to administer more preventive care and manage chronic diseases more effectively, before costly exacerbations require hospitalization.

Hard-pressed to come up with significant savings to reduce the deficit, some Senate Republicans are taking a closer look at reforms to Medicare Advantage in light of reports that insurance companies are collecting billions of dollars in extra profits by over-diagnosing older patients.

But the idea of cracking down on Medicare Advantage overpayments to insurance companies divides Republicans, who have traditionally championed the program.

Proponents of Medicare Advantage reform anticipated it will face strong opposition from the insurance industry, one of the most powerful special interest groups in Washington.

Sen. Bill Cassidy (La.), the top-ranking Republican on the Senate Health, Education, Labor and Pensions Committee, is leading the push to reduce Medicare overpayments.

“Medicare is going insolvent. If we don’t do anything, it’s going to go insolvent. We have a whole package of things, all of them bipartisan, and we’re doing it essentially to have something out there so that if somebody decides to do something, there will be things that are examined, considered and bipartisan” to vote on, he said.

“I come up with lots of stuff. We thought it through policy and think it’s policy that can make it all the way through,” he said.

Cassidy’s office says his bill could extend the solvency of Medicare by saving as much as $80 billion in federal funds over the next decade without cutting benefits.

He emphasizes that it would not cut Medicare Advantage benefits, but critics of the legislation are sure to challenge that claim.

“We’re not undermining Medicare Advantage,” he said.

“In fact, I would say this is a better alternative than what CMS is doing by rule,” he added, referring to a new rule-making action by the Biden administration to recover overpayments in Medicare Advantage through the Centers for Medicare & Medicaid Services.

The Medicare Payment Advisory Panel estimates that Medicare Advantage plans collected $124 billion in overpayments from 2008 to 2023. They collected an estimated $44 billion overpayments in 2022 and 2023 alone, according to MedPAC.

Unlike traditional fee-for-service Medicare, Medicare Advantage plans are offered by private companies. Both are funded by taxpayers through general revenues, payroll taxes and beneficiaries’ premiums.

Cassidy is also leading a bipartisan working group to reform Social Security to extend its solvency. Members include Sens. Angus King (I-Maine) and Mitt Romney (R-Utah).

“To have a significant impact on fiscal policy, you’d have to look at entitlements,” said Romney, who called Medicare Advantage “an area we’re going to be looking at very shortly — the committee will be looking at Medicare Advantage,

the cost of Medicare Advantage …. It’s become more expensive than the old fee-for-service Medicare.”

In a follow-up interview Thursday, Romney said senators are also looking at reforms to Pharmacy Benefit Managers, the companies that serve as middle-men between drug manufacturers, insurance companies and pharmacies.

Romney said, “in the past, Medicare Advantage has been a lower-cost way of providing Medicare than fee-for-service Medicare.”

“If that’s changing, I’d like to understand why and make sure we don’t create impediments to the lower-cost Medicare Advantage,” he said.

Sen. Mike Braun (R-Ind.) said Medicare Advantage overpayment “definitely” is a “reform issue.”

“I’ve been the loudest voice on reforming health care and that’s a commonsense idea,” he said. “Whatever it takes to bring down health care costs.

“I’m one of the most free-market people here, but the health care industry is not a free market. It’s like an unregulated utility,” he said. “There’s so much opaqueness.”

But some Republicans are already trying to paint efforts to reduce overpayments as cuts to Medicare Advantage.

“The problem with Medicare Advantage is President Biden is cutting $540 per member per year. That’s the problem. Medicare Advantage has been very successful,” said Sen. Roger Marshall (R-Kan.), an OB/GYN who practiced medicine for more than 25 years.

National Republican Senatorial Committee Chairman Steve Daines (R-Mont.) accused Biden of “proposing Medicare Advantage cuts” when the president accused some Republicans of wanting to sunset Medicare at his Feb. 7 State of the Union address.

Medicare Advantage is getting more popular among Democrats as well as the number of blue state enrollees in the program soars. The number of Americans enrolled in Medicare Advantage has nearly doubled over the last 12 years, according to the Kaiser Family Foundation.

Cassidy’s proposal, which he introduced with progressive Sen. Jeff Merkley (D-Ore.) on Monday, could draw broader interest from Republicans.

Sen. John Cornyn (R-Texas), an adviser to the Senate GOP leadership, called Medicare Advantage a “success.”

“That doesn’t mean that it should be immune from oversight, so I’ll be interested to see what they have to say,” he said.

Cassidy and Merkley say that Medicare Advantage plans have a financial incentive to make beneficiaries appear sicker than they are because they are paid a standard rate based on the health of individual patients. Their bill, the No Unreasonable Payment, Coding or Diagnoses for Elderly (No Upcode Act) would require risk models based on more extensive diagnostic data over a period of two years.

The goal is to narrow the disparity in how patients are assessed by traditional Medicare and Medicare Advantage.

Studies and audits conducted by CMS and the Department of Health and Human Services’ inspector general found that insurance companies collected billion of dollars in overpayments because of diagnoses that were not later supported by enrollees’ medical records.

The Kaiser Family Foundation reported in August that more than 28 million people — or about 48 percent of the eligible Medicare population — were enrolled in Medicare Advantage plans in 2022. They accounted for $427 billion or 55 percent of total federal Medicare spending.

Researchers estimate 15 million people will lose their Medicaid starting April 1 when states begin removing people from the low-income health insurance program for the first time in three years.

In March 2020, Congress banned states from removing people from Medicaid during the pandemic in exchange for more federal funding for state Medicaid programs. Medicaid enrollment is usually tied to people’s incomes, and individuals normally have to regularly prove they still qualify in what’s known as a redetermination. (In the 39 states and Washington, D.C., that have expanded Medicaid, a family of four has to make less than $40,000 to qualify. In non-expansion states, the cutoff is even lower.)

With redeterminations paused, Medicaid enrollment nationwide has grown from 71 million in February 2020 to an estimated 95 million in March 2023.Research shows Medicaid coverage is associated with better access to care, more financial security, better health and lower mortality. During the pandemic, beneficiaries have been able to enjoy these benefits without worrying about confirming their eligibility.

In December, Congress voted to let states restart the process of clearing their rolls on April 1, what’s sometimes referred to as “unwinding.”Lawmakers are giving states 14 months to redetermine millions of people’s eligibility — an unprecedented task made even more difficult by serious staffing and experience shortages in many Medicaid offices.

“It’s going to be a big lift,” said Sayeh Nikpay, a health policy researcher at the University of Minnesota and Tradeoffs Senior Research Advisor. “States have never had to do this many redeterminations this quickly before, and there’s a lot of uncertainty about what will happen.”

We asked Nikpay to pick out a few relevant studies to help us understand what is happening and how states and employers could keep more people insured. Here are three she identified as particularly helpful.

Two types of people will lose coverage

The Office of the Assistant Secretary for Planning and Evaluation, which provides research for the U.S. Department of Health and Human Services, released a report in August 2022 that estimated 15 million people will lose Medicaid coverage as a result of the unwinding. (The estimate is similar to another analysis by the independent Urban Institute.)

ASPE breaks those 15 million people into two groups. In the first group are people who make too much money to qualify for Medicaid. ASPE estimates there are about 8 million people in that category, and they should be able to get insurance through work or the Obamacare exchanges.

In the second group are roughly 7 million people ASPE estimates are still eligible but will lose coverage because of what’s called “administrative churn.”This can happen if the Medicaid office can’t get in touch with someone to confirm their eligibility because they’ve moved or changed their phone number or if they’re unable to make an in-person appointment because of work or child care responsibilities. (The Urban Institute projects about 4 million people will be in this group.)

These two groups represent a key tension to the unwinding process: States want to shed people who make too much money, but officials also know eligible people often lose coverage during redeterminations, and that danger is heightened given the scale and speed of this process.

Making the switch from Medicaid to private insurance

This next paper looks at the first group: the roughly 8 million people expected to move from Medicaid to private coverage, and specifically the roughly 4 million who are expected to get coverage through the Obamacare exchanges. Adrianna McIntyre, an assistant professor of health policy at Harvard, wrote in JAMA Health Forum in October 2022 about the most effective ways to move people from Medicaid onto private Obamacare plans.

There’s limited data on this, but based on the few studies available, McIntyre found that only 3 to 5 percent of people who leave Medicaid end up getting an Obamacare plan. Many policymakers are relying on the Obamacare exchanges to provide a life preserver to millions of people losing Medicaid coverage, but the research cited by McIntyre shows getting people into these plans is not guaranteed and will take focused effort by states.

McIntyre’s review cites several randomized controlled trials where states tested different ways of increasing enrollment in Obamacare plans. These studies found simple reminders from the state – like physical letters, emails and phone calls help – boost sign-ups anywhere from 7 to 16 percent.

But what really seems to make a difference is reminders plus connecting people to someone who can get them signed up while they are on the phone. In one of those trials published in 2022, people in California who got a reminder email and a call connecting them to enrollment assistance were almost 50% more likely to sign up for a plan. Such extra effort is obviously costly, and it may not be a priority or financially feasible for some states.

McIntyre’s review did not include any research on what employers can do to help their workers transition from Medicaid to work-based coverage, but based on the studies McIntyre cited, Nikpay said she thinks it’s a good idea for employers to make sure people know Medicaid could be going away and provide as much help as possible in getting new coverage.

Making it easier to stay on Medicaid can have other benefits

The final study looks at the second group of people expected to lose Medicaid coverage: the 7 million people who may lose coverage due to administrative churn even though they are still eligible.

Some states have tried to limit that churn, and researchers at the RAND Corporation evaluated New York’s effort. Starting in 2014, New York allowed people to stay on Medicaid without any redeterminations for 12 months once enrolled.

In addition to keeping more people on Medicaid for longer, researchers found that after this policy was in place, hospital admissions and monthly costs per beneficiary went down. The researchers can’t say whether the continuous enrollment policy directly caused these improved outcomes, but the findings suggest that avoiding administrative churn can help people stay covered without ballooning costs.

“It seems reasonable to me,” Nikpay said of the findings, “that making it easier to stay on Medicaid, even outside of a global pandemic, could benefit people’s health given what we know about how Medicaid affects people.”

The AHA has previously noted the third party observers who demonstrate a tenuous grasp of the data and rules regarding federal hospital transparency requirements. Now, some of those same entities with deep pockets and an apparent vendetta against hospitals and health systems have turned their attention toward the broader financial challenges facing the field. The results, as described in a recent Health Affairs blog, are as expected — a complete misunderstanding of current economic realities.

The three most egregious suggestions in this piece are that hospitals are seeking some kind of bailout from the federal government, employers and patients; that investment losses are the most problematic aspect of hospital financing; and that hospitals’ analyses of their financial situation are dishonest.

We debunk these in turn.

Hospitals are seeking fair compensation, not a government bailout. The authors state that hospitals are asking “constituents to foot the bill for hospitals’ investment losses.” This is patently false. Indeed, if you read the request we made to Congress cited in their blog, hospitals and health systems are simply asking to get paid for the care they deliver or to lower unnecessary administrative costs. This includes asking Medicare to pay for the days hospitals care for patients who are otherwise ready for discharge. Increasingly, this has occurred because there is no space in the next site of care or the patient’s insurer has delayed the authorization for that care. Keeping someone in a hospital bed for days, if not weeks, requires skilled labor, supplies and basic infrastructure costs. This doesn’t even account for the impact on a patient’s health for not being in the most appropriate care setting. Today, hospitals are not paid for these days. Asking for fair compensation is not a bailout; it is a basic responsibility of any purchaser.

While investment income may be down, hospitals and health systems have faced massive expense increases in the last year. The authors note that patient care revenue was up “by just below 1 percent in relative terms from 2021 to 2022,” suggesting that implies a positive financial trend. However, hospital total expenses were up 7% in 2022 over 2021, and were up by even more, 20%, when compared to pre-pandemic levels, according to Kaufman Hall. And it’s not just the AHA and Kaufman Hall saying this either: in its 2023 outlook, credit rating agency Moody’s noted that “margins will remain constrained by high expenses.” Hospitals should not need to rely on investment income for operations. However, many have been forced into this situation by substantial underpayments from their largest payers (Medicare and Medicaid), which even the Medicare Payment Advisory Commission (MedPAC), an independent advisor to Congress, has acknowledged. MedPAC’s most recent report showed a negative 8.3% Medicare operating margin. Hospitals and health systems are experiencing run-away increases in the supplies, labor and technology needed to care for patients. At the same time, commercial insurance companies are increasing their use of policies that can cause dangerous delays in care for patients, result in undue burden on health care providers and add billions of dollars in unnecessary costs to the health care system.

Hospitals and health systems are committed to an honest examination of the facts. The authors imply that the studies documenting hospitals’ financial distress are biased. They note that certain studies conducted by Kaufman Hall are based on proprietary data and therefore “challenging to draw general inferences.” They then go on to cherry-pick metrics from specific non-profit health care systems voluntarily released financial disclosures to make general claims about “the primary driver of hospitals’ financial strain.” The authors and their financial backers clearly seem to have a preconceived narrative, and ignore all the other realities that hospital and health system leaders are confronting every day to ensure access to care and programs for the patients and communities they serve.

It is imperative to acknowledge financial challenges facing hospitals and health systems today. Too much is at stake for the patients and communities that depend upon hospitals and health systems to be there, ready to care.

I have been both a frontline officer and a staff officer at a health system. I started a solo practice in 1977 and cared for my rheumatology, internal medicine and geriatrics patients in inpatient and outpatient settings. After 23 years in my solo practice, I served 18 years as President and CEO of a profitable, CMS 5-star, 715-bed, two-hospital healthcare system.

From 2015 to 2020, our health system team added 0.6 years of healthy life expectancy for 400,000 folks across the socioeconomic spectrum. We simultaneously decreased healthcare costs 54% for 6,000 colleagues and family members. With our mentoring, four other large, self-insured organizations enjoyed similar measurable results. We wanted to put our healthcare system out of business. Who wants to spend a night in a hospital?

During the frontline part of my career, I had the privilege of “Being in the Room Where It Happens,” be it the examination room at the start of a patient encounter, or at the end of life providing comfort and consoling family. Subsequently, I sat at the head of the table, responsible for most of the hospital care in Southwest Florida. [1]

Many folks commenting on healthcare have never touched a patient nor led a large system. Outside consultants, no matter how competent, have vicarious experience that creates a different perspective.

At this point in my career, I have the luxury of promoting what I believe is in the best interests of patients — prevention and quality outcomes. Keeping folks healthy and changing the healthcare industry’s focus from a “repair shop” mentality to a “prevention program” will save the industry and country from bankruptcy. Avoiding well-meaning but inadvertent suboptimal care by restructuring healthcare delivery avoids misery and saves lives.

RESPONDING TO AN ATTACK

Preemptive reinvention is much wiser than responding to an attack. Unfortunately, few industries embrace prevention. The entire healthcare industry, including health systems, physicians, non-physician caregivers, device manufacturers, pharmaceutical firms, and medical insurers, is stressed because most are experiencing serious profit margin squeeze. Simultaneously the public has ongoing concerns about healthcare costs. While some medical insurance companies enjoyed lavish profits during COVID, most of the industry suffered. Examples abound, and Paul Keckley, considered a dean among long-time observers of the medical field, recently highlighted some striking year-end observations for 2022. [2]

Recent Siege Examples

Transparency is generally good but can and has led to tarnishing the noble profession of caring for others. Namely, once a sector starts bleeding, others come along, exacerbating the exsanguination. Current literature is full of unflattering public articles that seem to self-perpetuate, and I’ve highlighted standout samples below.

The Federal Government is the largest spender in the healthcare industry and therefore the most influential. Not surprisingly, congressional lobbying was intense during the last two weeks of 2022 in a partially successful effort to ameliorate spending cuts for Medicare payments for physicians and hospitals. Lobbying spend by Big Pharma, Blue Cross/Blue Shield, American Hospital Association, and American Medical Association are all in the top ten spenders again. [3, 4, 5] These organizations aren’t lobbying for prevention, they’re lobbying to keep the status quo.

Concern about consistent quality should always be top of mind. “Diagnostic Errors in the Emergency Department: A Systematic Review,” shared by the Agency for Healthcare Research and Quality, compiled 279 studies showing a nearly 6% error rate for the 130 million people who visit an ED yearly. Stroke, heart attack, aortic aneurysm, spinal cord injury, and venous thromboembolism were the most common harms. The defense of diagnostic errors in emergency situations is deemed of secondary importance to stabilizing the patient for subsequent diagnosing. Keeping patients alive trumps everything. Commonly, patient ED presentations are not clear-cut with both false positive and negative findings. Retrospectively, what was obscure can become obvious. [6, 7]

Spending mirrors motivations. The Wall Street Journal article “Many Hospitals Get Big Drug Discounts. That Doesn’t Mean Markdowns for Patients” lays out how the savings from a decades-old federal program that offers big drug discounts to hospitals generally stay with the hospitals. Hospitals can chose to sell the prescriptions to patients and their insurers for much more than the discounted price. Originally the legislation was designed for resource-challenged communities, but now some hospitals in these programs are profiting from wealthy folks paying normal prices and the hospitals keeping the difference. [8]

“Hundreds of Hospitals Sue Patients or Threaten Their Credit, a KHN Investigation Finds. Does Yours?” Medical debt is a large and growing problem for both patients and providers. Healthcare systems employ collection agencies that typically assess and screen a patient’s ability to pay. If the credit agency determines a patient has resources and has avoided paying his/her debt, the health system send those bills to a collection agency. Most often legitimately impoverished folks are left alone, but about two-thirds of patients who could pay but lack adequate medical insurance face lawsuits and other legal actions attempting to collect payment including garnishing wages or placing liens on property. [9]

“Hospital Monopolies Are Destroying Health Care Value,” written by Rep. Victoria Spartz (R-Ind.) in The Hill, includes a statement attributed to Adam Smith’s The Wealth of Nations, “that the law which facilitates consolidation ends in a conspiracy against the public to raise prices.” The country has seen over 1,500 hospital mergers in the past twenty years — an example of horizontal consolidation. Hospitals also consolidate vertically by acquiring physician practices. As of January 2022, 74 percent of physicians work directly for hospitals, healthcare systems, other physicians, or corporate entities, causing not only the loss of independent physicians but also tighter control of pricing and financial issues. [10] The healthcare industry is an attractive target to examine. Everyone has had meaningful healthcare experiences, many have had expensive and impactful experiences. Although patients do not typically understand the complexity of providing a diagnosis, treatment, and prognosis, the care receiver may compare the experience to less-complex interactions outside healthcare that are customer centric and more satisfying.

PROFIT-MARGIN SQUEEZE

Both nonprofit and for-profit hospitals must publish financial statements. Three major bond rating agencies (Fitch Ratings, Moody’s Investors Service, and S & P Global Ratings) and other respected observers like KaufmanHall, collate, review, and analyze this publicly available information and rate health systems’ financial stability.

One measure of healthcare system’s financial strength is operating margin, the amount of profit or loss from caring for patients. In January of 2023 the median, or middle value, of hospital operating margin index was -1.0%, which is an improvement from January 2022 but still lags 2021 and 2020.

Erik Swanson, SVP at KaufmanHall, says 2022,

“Is shaping up to be one of the worst financial years on record for hospitals. Expense pressures — particularly with the cost of labor — outpaced revenues and drove poor performance. While emergency department visits and operating room minutes increased slightly, hospitals struggled to discharge patients due to internal staffing shortages and shortages at post-acute facilities,” [11]

Another force exacerbating health system finance is the competent, if relatively new retailers (CVS, Walmart, Walgreens, and others) that provide routine outpatient care affordably. Ninety percent of Americans live within ten miles of a Walmart and 50% visit weekly. CVS and Walgreens enjoy similar penetration. Profit-margin squeeze, combined with new convenient options to obtain routine care locally, will continue disrupting legacy healthcare systems.

Providers generate profits when patients access care. Additionally, “easy” profitable outpatient care can and has switched to telemedicine. Kaiser-Permanente (KP), even before the pandemic, provided about 50% of the system’s care through virtual visits. Insurance companies profit when services are provided efficiently or when members don’t use services. KP has the enviable position of being both the provider and payor for their members. The balance between KP’s insurance company and provider company favors efficient use of limited resources. Since COVID, 80% of all KP’s visits are virtual, a fact that decreases overhead, resulting in improved profit margins. [12]

On the other hand, KP does feel the profit-margin squeeze because labor costs have risen. To avoid a nurse labor strike, KP gave 21,000 nurses and nurse practitioners a 22.5% raise over four years. KP’s most recent quarter reported a net loss of $1.5B, possibly due to increased overhead. [13]

The public, governmental agencies, and some healthcare leaders are searching for a more efficient system with better outcomes

at a lower cost. Our nation cannot continue to spend the most money of any developed nation and have the worst outcomes. In a globally competitive world, limited resources must go to effective healthcare, balanced with education, infrastructure, the environment, and other societal needs. A new healthcare model could satisfy all these desires and needs.

Even iconic giants are starting to feel the pain of recent annual losses in the billions. Ascension Health, Cleveland Clinic, Jefferson Health, Massachusetts General Hospital, ProMedica, Providence, UPMC, and many others have gone from stable and sustainable to stressed and uncertain. Mayo Clinic had been a notable exception, but recently even this esteemed system’s profit dropped by more than 50% in 2022 with higher wage and supply costs up, according to this Modern Healthcare summary. [14]

The alarming point is even the big multigenerational health system leaders who believed they had fortress balance sheets are struggling. Those systems with decades of financial success and esteemed reputations are in jeopardy. Changing leadership doesn’t change the new environment.

Nonprofit healthcare systems’ income typically comes from three sources — operations, namely caring for patients in ways that are now evolving as noted above; investments, which are inherently risky evidence by this past year’s record losses; and philanthropy, which remains fickle particularly when other investment returns disappoint potential donors. For-profit healthcare systems don’t have the luxury of philanthropic support but typically are more efficient with scale and scope.

The most stable and predictable source of revenue in the past was from patient care. As the healthcare industry’s cost to society continues to increase above 20% of the GDP, most medically self-insured employers and other payors will search for efficiencies. Like it or not, persistently negative profit margins will transform healthcare.

Demand for nurses, physicians, and support folks is increasing, with many shortages looming near term. Labor costs and burnout have become pressing stresses, but more efficient delivery of care and better tools can ameliorate the stress somewhat. If structural process and technology tools can improve productivity per employee, the long-term supply of clinicians may keep up. Additionally, a decreased demand for care resulting from an effective prevention strategy also could help.

Most other successful industries work hard to produce products or services with fewer people. Remember what the industrial revolution did for America by increasing the productivity of each person in the early 1900s. Thereafter, manufacturing needed fewer employees.

PATIENTS’ NEEDS AND DESIRES

Patients want to live a long, happy and healthy life. The best way to do this is to avoid illness, which patients can do with prevention because 80% of disease is self-inflicted. When prevention fails, or the 20% of unstoppable episodic illness kicks in, patients should seek the best care.

The choice of the “best care” should not necessarily rest just on convenience but rather objective outcomes. Closest to home may be important for take-out food, but not healthcare.

Care typically can be divided into three categories — acute, urgent, and elective. Common examples of acute care include childbirth, heart attack, stroke, major trauma, overdoses, ruptured major blood vessel, and similar immediate, life-threatening conditions. Urgent intervention examples include an acute abdomen, gall bladder inflammation, appendicitis, severe undiagnosed pain and other conditions that typically have positive outcomes even with a modest delay of a few hours.

Most every other condition can be cared for in an appropriate timeframe that allows for a car trip of a few hours. These illnesses can range in severity from benign that typically resolve on their own to serious, which are life-threatening if left undiagnosed and untreated. Musculoskeletal aches are benign while cancer is life-threatening if not identified and treated.

Getting the right diagnosis and treatment for both benign and malignant conditions is crucial but we’re not even near perfect for either. That’s unsettling.

In a 2017 study,

“Mayo Clinic reports that as many as 88 percent of those patients [who travel to Mayo] go home [after getting a second opinion] with a new or refined diagnosis — changing their care plan and potentially their lives. Conversely, only 12 percent receive confirmation that the original diagnosis was complete and correct. In 21 percent of the cases, the diagnosis was completely changed; and 66 percent of patients received a refined or redefined diagnosis. There were no significant differences between provider types [physician and non-physician caregivers].” [15]

The frequency of significant mis- or refined-diagnosis and treatment should send chills up your spine. With healthcare we are not talking about trivial concerns like a bad meal at a restaurant, we are discussing life-threatening risks. Making an initial, correct first decision has a tremendous influence on your outcome.

Sleeping in your own bed is nice but secondary to obtaining the best outcome possible, even if car or plane travel are necessary. For urgent and elective diagnosis/treatment, travel may be a

good option. Acute illness usually doesn’t permit a few hours of grace, although a surprising number of stroke and heart attack victims delay treatment through denial or overnight timing. But even most of these delayed, recognized illnesses usually survive. And urgent and elective care gives the patient the luxury of some time to get to a location that delivers proven, objective outcomes, not necessarily the one closest to home.

Measuring quality in healthcare has traditionally been difficult for the average patient. Roadside billboards, commercials, displays at major sporting events, fancy logos, name changes and image building campaigns do not relate to quality. Confusingly, some heavily advertised metrics rely on a combination of subjective reputational and lagging objective measures. Most consumers don’t know enough about the sources of information to understand which ratings are meaningful to outcomes.

Arguably, hospital quality star ratings created by the Centers for Medicare and Medicaid Services (CMS) are the best information for potential patients to rate hospital mortality, safety, readmission, patient experience, and timely/effective care. These five categories combine 47 of the more than 100 measures CMS publicly reports. [16]

A 2017 JAMA article by lead author Dr. Ashish Jha said:

“Found that a higher CMS star rating was associated with lower patient mortality and readmissions. It is reassuring that patients can use the star ratings in guiding their health care seeking decisions given that hospitals with more stars not only offer a better experience of care, but also have lower mortality and readmissions.”

The study included only Medicare patients who typically are over 65, and the differences were most apparent at the extremes, nevertheless,

“These findings should be encouraging for policymakers and consumers; choosing 5-star hospitals does not seem to lead to worse outcomes and in fact may be driving patients to better institutions.” [17]

Developing more 5-star hospitals is not only better and safer for patients but also will save resources by avoiding expensive complications and suffering.

As a patient, doing your homework before you have an urgent or elective need can change your outcome for the better. Driving a

couple of hours to a CMS 5-star hospital or flying to a specialty hospital for an elective procedure could make a difference.

Business case studies have noted that hospitals with a focus on a specific condition deliver improved outcomes while becoming more efficient. [18] Similarly, specialty surgical areas within general hospitals have also been effective in improving quality while reducing costs. Mayo Clinic demonstrated this with its cardiac surgery department. [19] A similar example is Shouldice Hospital near Toronto, a focused factory specializing in hernia repairs. In the last 75 years, the Shouldice team has completed four hundred thousand hernia repairs, mostly performed under local anesthesia with the patient walking to and from the operating room. [20] [21]

THE BOTTOM LINE

The Mayo Brother’s quote, “The patient’s needs come first,” is more relevant today than when first articulated over a century ago. Driving treatment into distinct categories of acute, urgent, and elective, with subsequent directing care to the appropriate facilities, improves the entire care process for the patient. The saved resources can fund prevention and decrease the need for future care. The healthcare industry’s focus has been on sickness,

not prevention. The virtuous cycle’s flywheel effect of distinct categories for care and embracing prevention of illness will decrease misery and lower the percentage of GDP devoted to healthcare.

Editor’s note: This is a multi-part series on reinventing the healthcare industry. Part 2 addresses physicians, non-physician caregivers, and communities’ responses to the coming transformation.

The health of a community is measured by the health of its individual members, and the health of its members depends on their access to local, high-quality medical care. Health coverage is a key indicator of the health and wellness of an individual. When people have health insurance, they have greater access to care, reduced mortality, and better health outcomes, according to a report from the American Hospital Association.

However, the current approach taken by some of the nation’s largest health insurers, or payers, is putting this at jeopardy as payers focus on profits and quarterly earnings, strip rates and put the long-term viability of health systems at risk. With hospitals in the middle of the worst economic performance in decades, it is time for payers to own up to how their actions negatively impact the communities and those they claim to serve.

As a physician and the chief of population health at a large metro-area health system, Northeast Georgia Health System, my patients’ ability to readily access medical care at our facilities — and have that care be covered by insurance — matters greatly. Any disruption in a patient’s experience, such as restricting access to care by their health plan or going out of network with an insurance company, can wreak havoc on population health. It’s no secret that many health systems across the country have felt the weight of increased administrative and contractual burdens from health insurers as denial rates continue to creep upwards.

Health insurance companies, like the nation’s largest, UnitedHealthcare, have seen profits soar in recent years. UnitedHeatlhcare’s profits were up 28 percent during the third quarter of 2022 – achieving a profit of $5.3 billion in just those three months – before closing the year at $28.4 billion in net earnings in 2023. Elevance (formerly Anthem), Cigna, and Aetna have also posted record profits recently.

We have seen the impact of the pressure payers are putting on hospitals across the country. Nearly 200 hospitals have closed since 2005, according to the Sheps Center for Health Services Research at the University of North Carolina. Many of these hospitals have closed because they failed to receive fair contracted rates from large payers and thus were insolvent.

Community benefits like charity care, health education and economic impact are provided by hundreds of hospitals nationally, but that impact is at risk if they are not fairly compensated for the services they provide.