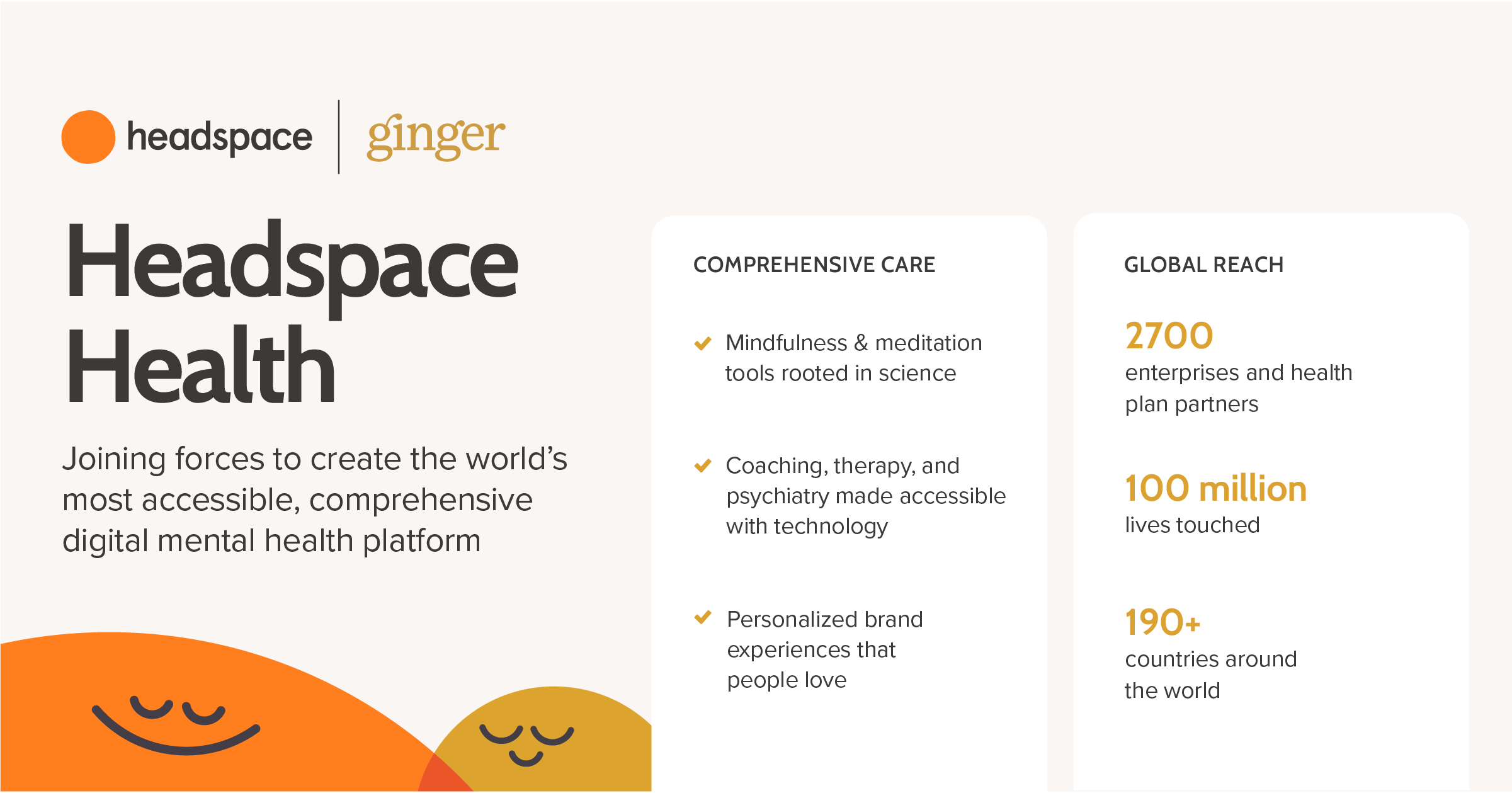

Two of the best-known companies in the virtual mental health space announced plans to merge this week, creating a $3B player poised to dominate this fast-growing segment of healthcare demand.

Headspace, a direct-to-consumer provider of app-based “mindfulness” meditation programs, will combine with Ginger, which sells text- and video-based coaching and therapy services to employers and insurers. Between them, the two companies claim to serve over 100M users worldwide.

Headspace is best known as a consumer-focused app, while Ginger largely serves business and payer clients. The combined company, to be called Headspace Health, will surely look to consolidate offerings into a comprehensive mental health service for employees, targeting a benefits market that is rapidly becoming overwhelmed with startup providers of virtual point solutions.

Behavioral health telemedicine utilization skyrocketed during last year’s COVID surge, and has been the one area of virtual care not to fall back to earth since—we’ve learned that virtual is often a superior approach for many mental health services.

Two questions arose in our minds after the Headspace/Ginger merger was announced. First, does the combined company bring a broad enough value proposition to overcome employer frustration with a highly fragmented market, or will the new Headspace Health eventually need to be part of a larger insurer platform to capture the opportunity in front of it? And second, does “mindfulness” even work?

The academic evidence is decidedly mixed, but the popularity of Headspace and other meditation apps, especially among Millennial consumers, might make that question moot. The mindfulness “wrapper” on more traditional mental health services may prove to be very popular with employees, and could become a must-have element of employers’ benefit packages.

The Federal Trade Commission has been hit by a “tidal wave” of merger filings and cannot review them all before required deadlines.

The FTC is now sending letters to merging entities warning them that the agency may deem a combination unlawful even if the companies decide to merge.

“Companies that choose to proceed with transactions that have not been fully investigated are doing so at their own risk,” the regulator said in a statement Tuesday.

The alert may give pause to hospitals merging at a steady clip. Unwinding deals once they’re already consummated can be costly and complex. The premerger filings give regulators a chance to stop anticompetitive mergers before a deals closes, preventing harm to consumers and businesses in the meantime.

The FTC received 343 premerger filings in the month of July, more than three times the amount from July of last year, when 112 transactions were submitted for review.

So far this year, more than 2,000 transactions have been submitted through the month of July, according to figures with the FTC, eclipsing the 815 filings over the same time period last year.

Federal regulators have forced hospital to unwind mergers before.

The FTC forced ProMedica to unwind its buyup of St. Luke’s Hospital in the Toledo area after alleging the deal would severely hinder competition. The FTC later approved a divestiture plan in 2016 after a long battle in court.

It came even as the FTC had signaled it plans to prioritize enforcement in a number of key industries including healthcare.

Plus, last year the FTC said it was expanding a key tool in its arsenal to potentially help police future deals.

Mergers that exceed a certain threshold — currently $92 million — are required to submit a premerger filing with the FTC per the Hart-Scott-Rodino Act.

The filing initiates a review period in which the FTC and Department of Justice investigate the deal.

Typically, the agencies have 30 days to determine whether additional information is needed. If so, the deal is on hold until the companies respond with the needed information, and after that the agencies have a limited number of days to file a challenge if they deem the tie-up unlawful.

The FTC can also terminate the waiting period early, allowing the deal to proceed.

However, the agency maintains the right to challenge any deal regardless of whether it was reviewed or not.

One of the underappreciated ways in which health systems create value in our healthcare economy, as was recently the topic of discussion with the CEO of an organization we work with, is their role as a “safety net”. We weren’t talking about safety-net providers in the traditional sense—those which serve low-income populations. Rather, we were talking about the ability of larger health systems to acquire and invest in smaller hospitals that might otherwise risk going out of business entirely due to economic pressures.

When economic shocks hit, as was recently the case with COVID, we often see firms close; think of all the restaurant and hospitality businesses forced to shut down over the past year. As the economy rebounds, new business spring up to take their places—that kind of “creative destruction” is commonplace in the larger economy. But when a hospital is forced to shut its doors, it’s a different story, one that could be potentially disastrous for the community.

Often the most economically vulnerable hospitals are sole providers for their communities; without them, critical medical services could be much less accessible for patients. Enter multi-hospital health systems, which have often stepped in to acquire hospitals in jeopardy.

By providing access to capital, technology, and management infrastructure, systems have probably kept hundreds of such smaller hospitals in business over the past several decades. Policy analysts are quick to criticize health systems for value destruction: leveraging scale to raise prices, and so forth.

Often valid criticism, but it would be myopic to overlook the fact that systems have also allowed many vulnerable communities to retain access to a viable local hospital. The pushback is often to posit that we simply have too many hospitals to begin with—but try telling that to patients and communities who have lost access to their local source of care.

An estimate from the Partnership for America’s Healthcare Future predicts that nearly four out of five 60- to 64-year-olds would enroll in Medicare, with two-thirds transitioning from existing commercial plans, if “Medicare at 60” becomes a reality.

In the graphic above, we’ve modeled the financial impact this shift would have on a “typical” five-hospital health system, with $1B in revenue and an industry-average two percent operating margin.

If just over half of commercially insured 60- to 64-year-olds switch to Medicare, the health system would see a $61M loss in commercial revenue.

There would be some revenue gains, especially from patients who switch from Medicaid, but the net result of the payer mix shift among the 60 to 64 population would be a loss of $30M, or three percent of annual revenue, large enough to push operating margin into the red, assuming no changes in cost structure. (Our analysis assumed a conservative estimate for commercial payment rates at 240 percent of Medicare—systems with more generous commercial payment would take a larger hit.)

Coming out of the pandemic, hospitals face rising labor costs and unpredictable volume in a more competitive marketplace. While “Medicare at 60” could provide access to lower-cost coverage for a large segment of consumers, it would force a financial reckoning for many hospitals, especially standalone hospitals and smaller systems.

As some employers look to contract directly with hospitals in an effort to lower healthcare costs, researchers found that large self-insured employers likely do not have enough market power to extract lower prices, according to a study published in The American Journal of Managed Care.

The study examined the relationship between employer market power and hospital prices every year between 2010 and 2016 in the nation’s 10 most concentrated labor markets.

The study found that hospital market power far outweighs employer market power, suggesting employers will not be successful in lowering prices alone, but may want to consider forging purchase alliances with local government employee groups, the research paper said.

Dive Insight:

In recent years, some larger employers have cut out the middlemen to strike deals directly with hospitals.

Perhaps most notably, J.P. Morgan, Amazon and Berkshire Hathaway joined forces to bend the cost of care in the U.S. Despite all the fanfare, the venture, named Haven, later fell apart, illustrating how difficult it is to change the nation’s healthcare system.

By circumventing traditional health insurers, companies are hoping they themselves can negotiate better deals.

But this latest study throws cold water on that strategy, at least in part. “Our study suggests that almost all employers, operating alone, simply do not have the market power to impose a threat of effective negotiation,” the paper found.

One of the paper’s main aims is to measure market power of hospitals and employers, and the results are striking. The average hospital market power far exceeds that of the employer in the 10 metropolitan areas researchers examined.

The average hospital market power was more than 80 times greater than that of the employer, putting into context just how askew the power dynamics are.

These employers are not wrong for wanting to strike out on their own, the researchers point out.

Many self-insured employers bear the insurance risk while entering into administrative services only arrangements with insurers which provide just that, administrative type services.

But insurers in these arrangements may not have any incentive to lower prices. The paper pointed to another working research paper that found ASO plans pay more for the same service, at the same hospital compared to those in fully insured arrangements.

“The empirical evidence suggests that insurers, because they lack the incentive, may not be negotiating lower prices for their ASO enrollees,” according to the study.

Even though employers may not have enough market power on their own, researchers offered up a solution: team up with state or local government employee groups to increase market power to obtain lower hospital prices.

A new report from consulting firm Avalere Health and the nonprofit Physicians Advocacy Institute finds that the pandemic accelerated the rise in physician employment, with nearly 70 percent of doctors now employed by a hospital, insurer or investor-owned entity.

Researchers evaluated shifts to employment in the two-year period between January 2019 and January 2021, finding that 48,400 additional doctors left independent practice to join a health system or other company, with the majority of the change occurring during the pandemic. While 38 percent chose employment by a hospital or health system,the majority of newly employed doctors are now employed by a “corporate entity”, including insurers, disruptors and investor-owned companies.

(Researchers said they were unable to accurately break down corporate employers by entity, and that the study likely undercounts the number of physician practices owned by private equity firms, given the lack of transparency in that segment.) Growth rates in the corporate sector dwarfed health system employment, increasing a whopping 38 percent over the past two years, in comparison to a 5 percent increase for hospitals.

We expect this pace will continue throughout this year and beyond, as practices seek ongoing stability and look to manage the exit of retiring partners, enticed by the outsized offers put on the table by investors and payers.

As we reported recently, healthcare M&A hit record highs in the first quarter of 2021—with deal activity in the physician practice space surging 87 percent. The graphic above highlights private equity firms’ increasing investment in the sector over the last five years. Both the number and size of PE-backed healthcare deals have increased substantially from 2015 to 2020, up 39 and 45 percent respectively.

In 2020, physician practices and services comprised nearly a fifth of all transactions, with PE firms driving the majority. One in five physician transactions involvedprimary care practices—a signal that investors are banking on profits to be made in the shift to value-based care models.

Meanwhile, PE firms are still rolling up high-margin specialty practices, with ophthalmology, orthopedics, dermatology, and anesthesiology groups all receiving significant funding in 2020. PE investment in physician practices will likely continue to accelerate, as investors view healthcare as a promising place to deploy readily available capital.

But we remain convinced that private equity investors have little interest in being long-term owners of practices,and will ultimately look for an exit by selling “rolled-up” physician entities to health systems or insurers.

This week, the Supreme Court declined to hear an appeal challenging Medicare’s 2019 regulation calling for “site-neutral payment” for services provided by hospitals in outpatient settings, clearing the way for the rule’s implementation. The appeal was filed by the American Hospital Association (AHA), along with numerous hospitals and health systems, after a lower court ruling last year upheld the change to Medicare’s reimbursement policies.

The rule aims to level the playing field betweenindependent providers and hospital-owned clinics by curtailing hospitals’ ability to charge higher “facility fees” for services provided in locations they own. Site-neutral payment has been a longstanding target of criticism by health economists and policymakers, who cite the pricing advantage as a driver of consolidation in the industry, which has tended to push the cost of care upward.

The AHA expressed disappointment in the Court’s decision not to hear the appeal,saying that the changes to payment policy “directly undercut the clear intent of Congress to protect them because of the many real and crucial differences between them and other sites of care.” The primary difference, of course, is hospitals’ need to fully allocate their costs across all the services they bill for, making care in lower-acuity settings more expensive than similar care delivered by practices that don’t have to subsidize inpatient hospitals and other costly assets.

Over the years that legitimate business need has turned into adeliberate business model—purchasing independent practices in order to take advantage of higher hospital pricing. As Medicare looks to manage Baby Boomer-driven cost growth, and employers and consumers grapple with rising health spending, expect increasingly rigorous efforts to push back against these kinds of pricing strategies.

Michael Freed, the former CFO of Spectrum Health, said he was “stunned” when he heard that the Grand Rapids, Mich.-based system plans to pursue a merger with Southfield, Mich.-based Beaumont Health, for myriad reasons.

In a June 24 open letter to Spectrum’s board of directors, Mr. Freed said during his tenure they discussed possible mergers routinely and that a Spectrum-Beaumont combination “brought nothing new with it” and wouldn’t enhance value.

“The markets didn’t overlap, so there were no significant administrative savings opportunities. The ability of each hospital to grow wasn’t enhanced by adding the other to the ‘system,'” Mr. Freed wrote. “In short, I never saw how such a merger could improve health, enhance value or make care more affordable. I still don’t.”

Mr. Freed was Spectrum’s CFO from May 1995 to December 2013. During his tenure, he helped oversee the formation of Spectrum and a substantive period of growth for the Michigan system. Mr. Freed also served as CEO of Spectrum’s health plan, Priority Health, from May 2012 until he retired in January 2016.

In his letter, Mr. Freed outlined several reasons he was “stunned” by the pursuit of the merger that would create a health system with 22 hospitals, 305 outpatient centers and about $13 billion in operating revenue.

Mr. Freed wrote that the merger with Beaumont, which is based in Southfield, Mich., may not be in the best interest of West Michigan. He said the combination of the two systems raises questions about whether governance truly will remain in the region and with Spectrum, if financial transparency will continue and if Spectrum will continue to honor the consent decree it signed in 1997 establishing a set of operational guidelines.

If the merger moves forward, “debt can be placed on the books of West Michigan while investments EARNED IN West Michigan could be spent in SE Michigan … and vice versa,” Mr. Freed wrote. “If this entity should someday merge with other out-of-state entities, West Michigan could find itself investing in healthcare in other states as well, rather than in its own health.”

Mr. Freed raised concerns over the agreement between Spectrum and Beaumont to create a 16-person board of directors, seven of whom would come from Spectrum and seven from Beaumont. The CEO would come from Spectrum, and one new board member will be appointed.

“While this structure looks to favor Spectrum Health initially, it would only take the hiring of a board member more favorable to Beaumont Health and the replacement of the CEO (in favor of Beaumont Health) for Spectrum Health to find itself outvoted 9 to 7 on key issues,” Mr. Freed said.

Additionally, Mr. Freed noted that the merger has the potential for massive financial losses to West Michigan. In particular, Mr. Freed said losses would stem from the financial assets of Spectrum and Priority Health no longer residing in West Michigan.

“I’ll admit, I don’t see any value in this merger,” Mr. Freed wrote. “I only see the potential for massive financial loss, both historically and an undetermined amount going forward, to the region that produced all of Spectrum Health.”

Mr. Freed urged the Spectrum board to take a few steps before moving forward with the merger, including selling or divesting Priority Health.

“When you sign the documents that will permanently change this region, your signature will forever hold you accountable for the repercussions,” Mr. Freed wrote. “Please sign carefully.”

Spectrum Health told MiBiz it remains committed to the commitments in the 1997 consent agreement and that it “remains enthusiastic” about the merger.

“Spectrum Health is fully committed to fulfilling its consent decree obligations and will continue to uphold its tenets,” the health system said. “We remain confident that creating a new system not only meets our current obligations to our local communities but will also improve the health of individuals in West Michigan and throughout the state.”

On Thursday, Grand Rapids-based Spectrum Health and Southfield-based Beaumont Health signed a letter of intent to merge, in a combination that would create a 22-hospital, $12B company that would become Michigan’s largest health system.

Spectrum CEO Tina Freese Decker will lead the combined company, while Beaumont CEO John Fox will assist with the merger, then depart. The proposed deal would not only create a system spanning much of Michigan, but would also allow for theexpansion of Spectrum’s health plan, Priority Health, which accounted for more than $5B of the system’s $8B in revenue, into the Detroit market.

This is the third proposed merger since 2019 for Beaumont, which saw its planned combinations with Ohio-based Summa Health fall apart early in the pandemic; the system’s planned merger with Illinois-based Advocate-Aurora Health was called off in 2020 amid pushback from the system’s medical staff. Both deals fell apart due to challenges in communication and cultural compatibility—which will likely also be the greatest potential stumbling blocks for a Spectrum-Beaumont partnership.

The recently abandoned combination between NC-based Cone Health and VA-based Sentara Healthcare also appears to have fallen apart due to cultural challenges, as have many other recent health system deals. Yet despite a string of cautionary tales, health system mergers continue apace—a sign of the pressure industry players are under to seek scale in order to contend with the growing ranks of disruptive (and well-funded) competitors.