Here is a summary of recent credit rating downgrades, going back to the last Becker’s roundup on Jan. 17.

Operating concerns and a bleak financial outlook for some resulted in the following changes:

Geisinger Health System (Danville, Pa.): Moody’s Investors Service downgraded Geisinger Health System’s outstanding bonds from “A1” to “A2” Feb. 13 amid expectations of continued cash flow weakness.

The outlook for the system, which has about $1.3 billion in debt, is stable.

Marshfield (Wis.) Clinic Health System: The system suffered a credit downgrade because of recent operating losses and amid expectations of no immediate financial improvement.

The S&P Global move Feb. 7 to downgrade the system to “BBB+” from “A-” follows a similar move from Fitch Jan. 18.

Marshfield signed a memorandum of understanding with Duluth, Minn.-based Essentia Health to discuss a potential merger Oct. 12 that would include 25 hospitals.

Tower Health (West Reading, Pa.): Troubled Tower Health, which is currently undergoing a strategic review and selling off several assets, suffered a rating downgrade on its bonds, S&P Global reported Feb. 6, adding that the outlook is negative.

“The downgrade reflects Tower Health’s significant ongoing operating losses that are expected to continue in fiscal 2023, and a steep decline in unrestricted reserves to a level that we view as highly vulnerable,” said S&P Global Ratings credit analyst Anne Cosgrove.

Fairview Health (Minneapolis): Moody’s Investors Service downgraded the revenue bond ratings of Fairview Health from “A3” to “Baa1.”

The downgrade reflects Moody’s projection that weak operating performance will be challenging to overcome due to increased labor costs and lower inpatient volume. Inflation and annual transfers to the University of Minnesota in Minneapolis will also hamper margins, Moody’s said.

The U.S. economy added 517,000 jobs in January, and the unemployment rate fell to 3.4% — the lowest level in over a half-century, the government said on Friday.

Why it matters:

Employers added jobs at an unexpectedly rapid pace, the latest sign of a hot labor market despite aggressive moves by the Federal Reserve to cool it down.

The numbers are more than double the 190,000 forecasters anticipated.

Details:

The extraordinary reportcomes as the Fed continues to dial back its pace of interest rates and prepares to raise rates further to restrain the economy and chill still-high inflation.

Fed chair Jerome Powell has acknowledged progress on slowing inflation in recent months while noting risks lie ahead. Among them is wage growth, which is rising at a pace still too swift for the Fed’s comfort.

In January, average hourly earnings rose 0.3% — or 4.4% over the previous year, according to Friday’s data.

The big picture:

The data also showed that employment in 2023 was even stronger than initially thought, with roughly 568,000 more jobs than previously reported.

The update was part of the Labor Department’s annual revisions, which incorporate more complete data from insurance records and updated seasonal adjustments.

The executives featured in this article are all speaking at the Becker’s Healthcare 13th Annual Meeting April 3-6, 2023, at the Hyatt Regency in Chicago.

Question: What will hospitals and health systems look like in 10 years? What will be different and what will be the same?

Michael A. Slubowski. President and CEO of Trinity Health (Livonia, Mich.): In 10 years, inpatient hospitals will be more focused on emergency care, intensive/complex care following surgery or complex medical conditions, and short-stay/observation units. Only the most complex surgical cases and complex medical cases will be inpatient status. Most elective surgery and diagnostic services will be done in freestanding surgery, procedural and imaging centers. Many patients with chronic medical conditions will be managed at home using digital monitoring. More seniors will be cared for in homes and/or in PACE programs versus skilled nursing facilities.

Mark A. Schuster, MD, PhD. Founding Dean and Chief Executive Officer of Kaiser Permanente Bernard J. Tyson School of Medicine (Pasadena, Calif.): The future of hospitals might not actually unfold in hospitals. I expect that more and more of what we now do in hospitals will move into the home. The technology that makes this transition possible is already out there: Remote monitoring of vital signs and lab tests, remote visual exams, and videoconferencing with patients. And all of this technology will improve even more over the next 10 years — turning at-home care from a dream into a reality.

Imagine no longer being kept awake all night by beeps and alarms coming from other patients’ rooms or kept away from family by limited visiting hours. The benefits are especially welcome for people who live in rural places and other areas with limited medical facilities. Who knows? Maybe robotics will make some in-home surgeries not so far off!

Of course, not all patients have a safe or stable home environment where they could receive care, so hospitals aren’t going away anytime soon. I’m not suggesting that most current patients could be cared for remotely in a decade — but I do think we’re moving in that direction. So those of us who work in education will need to train medical, nursing, and other students for a healthcare future that looks quite different from the healthcare present and takes place in settings we couldn’t imagine 10 years ago.

Shireen Ahmad. System Director, Operations and Finance of CommonSpirit Health (Chicago): The biggest change I anticipate is a continuation in the decentralization of health services delivery that has typically been provided by hospitals. This will result in a reduction of hospitals with fewer services performed in acute settings and with more services provided in non-acute ones.

With recent reimbursement changes, CMS is helping to set the tone of where care is delivered. Hospitals are beginning to rationalize services, including who and where care is delivered. For example, pharmacies often carry clinics that provide vaccinations, but in France, one can go to a pharmacy for care and sterilization of minor wounds while only paying for bandages, medication and other supplies used in the visit. I would not be surprised if, in 10 years, one could get an MRI at their local Walmart or schedule routine screenings and tests at the grocery store with faster, more accurate results as they check out their produce.

If the pandemic has taught us anything, there will always be a need for acute care and our society will always need hospitals to provide care to sick patients. This is not something I would anticipate changing. However, the need to provide most care in a hospital will change with the result leading to fewer hospitals in total. Far from being a bleak outlook, however, I believe that healthier, sustainable health systems will prevail if they are able to provide a greater spectrum of care in broader settings focussing on quality and convenience.

Gerard Brogan. Senior Vice President and Chief Revenue Officer of Northwell Health (New Hyde Park, N.Y.): Operationally, hospitals and health systems will be more designed around the patient experience rather than the patient accommodating to the hospital design and operations. Specifically, more geared toward patient choice, shopping for services, and price competition for out-of-pocket expenses. In order to bring costs down, rational control of utilization will be more important than ever. Hopefully, we will be able to shrink the administrative costs of delivering care. Structurally, more care will continue to be done ambulatory, with hospitals having a greater proportion of beds having critical care capability and single rooms for infection control, putting pressure on the cost per square foot to operate. Sustainable funding strategies for safety net hospitals will be needed.

Mike Gentry. Executive Vice President and COO of Sentara Healthcare (Norfolk, Va.): During the next 10 years, more rural hospitals will become critical assessment facilities. The legislation will be passed to facilitate this transition. Relationships with larger sponsoring health systems will support easy transitions to higher acuity services as required. In urban areas, fewer hospitals with greater acuity and market share will often match the 50 percent plus market share of health plans. The ambulatory transition will have moved beyond only surgical procedures into outpatient but expanded historical medical inpatient status in ED/observation hubs.

The consumer/patient experience will be vastly improved. Investments in mobile digital applications will provide greatly enhanced communication, transparency of clinical status, timelines, the likelihood of expected outcomes and cost. Patients will proactively select from a menu of treatment options provided by predictive AI. The largest 10 health systems will represent 25 percent of the total U.S. acute care market share, largely due to consumer-centric strategic investments that have outpaced their competitors. Health systems will have vastly larger pharma operations/footprints.

Ketul J. Patel. CEO of Virginia Mason Franciscan Health (Seattle) and Division President, Pacific Northwest of CommonSpirit Health (Chicago): This is a transformative time in the healthcare industry, as hospitals and healthcare systems are evolving and innovating to meet the growing and changing needs of the communities we serve. The pandemic accelerated the digital transformation of healthcare. We have seen the proliferation of new technologies — telemedicine, artificial intelligence, robotics, and precision medicine — becoming an integral part of everyday clinical care. Healthcare consumers have become empowered through technology, with greater control and access to care than ever before.

Against this backdrop, in the next decade we’ll see healthcare consumerism influencing how health systems transform their hospitals. We will continue incorporating new technologies to improve healthcare delivery, offering more convenient ways to access high-quality care, and lowering the overall cost of care.

SMART hospitals, including at Virginia Mason Franciscan Health, are utilizing AI to harness real-time data and analysis to revolutionize patient and provider experiences and improve the quality of care. VMFH was the first health system in the Pacific Northwest to introduce a virtual hospital nearly a decade ago, which provides virtual services in the hospital across the continuum of care to improve quality and safety through remote patient monitoring and care delivery.

As hospitals become more high-tech, more nimble, and more efficient over the next 10 years, there will be less emphasis on brick-and-mortar buildings as we continue to move care away from the hospital toward more convenient settings for the patient. We recently launched VMFH Home Recovery Care, which brings all the essential elements of hospital-level care into the comfort and convenience of patients’ homes, offering a safe and effective alternative to the traditional inpatient stay.

Health systems and hospitals must simplify the care experience while reducing the overall cost of care. VMFH is building Washington state’s first hybrid emergency room/urgent care center, which eliminates the guesswork for patients unsure of where to go for care. By offering emergent and urgent care in a single location, patients get the appropriate level of care, at the right price, in one convenient location.

As healthcare delivery becomes more sophisticated in this digital age, we must not lose sight of why we do this work: our patients. There is no device or innovation that can truly replace the care and human intelligence provided by our nurses, APPs and physicians. So, while hospitals and health systems might look and feel different in 2033, our mission will remain the same: to provide exceptional, compassionate care to all — especially the most vulnerable.

David Sylvan. President of University Hospitals Ventures (Cleveland): American healthcare is facing an imperative. It’s clear that incremental improvements alone won’t manifest the structural outcomes that are largely overdue. The good news is that the healthcare industry itself has already initiated the disruption and self-disintermediation. I would hope that in the next 10 years, our offerings in healthcare truly reflect our efforts to adopt consumerism and patient choice, alleviate equity barriers and harness efficiencies while reducing time waste.

We know that some of this will come about through technology design, build and adoption, especially in the areas of generative artificial intelligence. But we also know that some of this will require a process overhaul, with learnings gleaned from other industries that have already solved adjacent challenges. What won’t change in 10 years will be the empathy and quality of care that the nation’s clinicians provide to patients and their caregivers daily.

Joseph Webb. CEO of Nashville (Tenn.) General Hospital: The United States healthcare industry operates within a culture that embraces capitalism as an economic system. The practice of capitalism facilitates a framework that is supported by the theory of consumerism. This theory posits that the more goods and services are purchased and consumed, the stronger an economy will be. With that in mind, healthcare is clearly a driver in the U.S. economy, and therefore, major capital and technology are continuously infused into healthcare systems. Healthcare is currently approaching 20 percent of the U.S. gross domestic product and will continue to escalate over the next 10 years.

Also, in 10 years, there will be major shifts in ownership structures, e.g., mergers, acquisitions, and consolidations. Many healthcare organizations/hospitals will be unable to sustain operations due to shrinking profit margins. This will lead to a higher likelihood of increasing closures among rural hospitals due to a lack of adequate reimbursement and rising costs associated with salaries for nurses, respiratory therapists, etc., as well as purchasing pharmaceuticals.

Aging baby boomers with chronic medical conditions will continue to dominate healthcare demand as a cohort group. To mitigate the rising costs of care, healthcare systems and providers will begin to rely even more heavily on artificial intelligence and smart devices. Population health initiatives will become more prevalent as the cost to support fragmented care becomes cost-prohibitive and payers such as CMS will continue to lead the way toward value-based care.

Because of structural and social conditions that tend to drive social determinants of health, which are fundamental causes of health disparities, achieving health equity will continue to be a major challenge in the U.S. Health equity is an elusive goal that can only be achieved when there is a more equitable distribution of SDOH.

Gary Baker. CEO, Hospital Division of HonorHealth (Scottsdale, Ariz.): In 10 years, I would expect hospitals in health systems to become more specialized for higher acuity service lines. Providing similar acute services at multiple locations will become difficult to maintain. Recruiting and retaining specialty clinical talent and adopting new technologies will require some redistribution of services to improve clinical quality and efficiency. Your local hospital may not provide a service and will be a navigator to the specialty facilities. Many services will be provided in ambulatory settings as technology and reimbursement allow/require. Investment in ambulatory services will continue for the next 10 years.

Michael Connelly. CEO Emeritus of Bon Secours Mercy Health (Cincinnati): Our society will be forced to embrace economic limits on healthcare services. The exploding elderly population, in combination with a shrinking workforce to fund Medicare/Medicaid and Social Security, will force our health system to ration care in new ways. These realities will increase the role of primary care as the needed coordinator of health services for patients. Diminishing fragmented healthcare and redundant care will become an increasing focus for health policy.

David Rahija. President of Skokie Hospital, NorthShore University HealthSystem (Evanston, Ill.): Health systems will evolve from being just a collection of hospitals, providers, and services to providing and coordinating care across a longitudinal care continuum. Health systems that are indispensable health partners to patients and communities by providing excellent outcomes through seamless, coordinated, and personalized care across a disease episode and a life span will thrive. Providers that only provide transactional care without a holistic, longitudinal relationship will either close or be consolidated. Care tailored to the personalized needs of patients and communities using team care models, technology, genomics, and analytics will be key to executing a personalized, seamless, and coordinated model of care.

Alexa Kimball, MD. President and CEO of Harvard Medical Faculty Physicians at Beth Israel Deaconess Medical Center (Boston): Ten years from now, hospitals will largely look the same — at least from the outside. Brick-and-mortar buildings aren’t going away anytime soon. What will differ is how care is delivered beyond the traditional four walls. Expect to see a more patient-centered and responsive system organized around what individuals need — when and where they need it.

Telehealth and remote patient monitoring will enable greater accessibility for patients in underserved areas and those who cannot get to a doctor’s office. Technology will not only enable doctors to deliver more personalized treatment plans but will also dramatically reshape physician workflows and processes. These digital tools will streamline administrative tasks, integrate voice commands, and provide more conducive work environments. I also envision greater access to data for both providers and patients. New self-service solutions for care management, scheduling, pricing, shopping for services, etc., will deliver a more proactive patient experience and make it easier to navigate their healthcare journey.

Ronda Lehman, PharmD. President of Mercy Health – Lima (Ohio):

This is a highly challenging question to address as we continue to reevaluate how healthcare is being delivered following several difficult years and knowing that financial challenges still loom. That said, when I am asked what it will look like, I am keenly aware of the fact that it only will look that way if we can envision a better way to improve the health of our communities. So 10 years from now, we need to have easier and more patient-driven access to care.

We will need to stop doing ‘to people’ and start caring ‘with people.’ Artificial intelligence and proliferous information that is readily available to consumers will continue to pave the way to patients being more empowered and educated about their options. So what will differentiate healthcare of the future? Enabling patients to make informed decisions.

Undoubtedly, technology will continue to advance, and along with it, the associated costs of research and development, but healthcare can only truly change if providers fundamentally shift their approach to how we care for patients. It is imperative that we need to transform from being the gatekeepers of valuable resources and services to being partners with patients on their journey. If that is what needs to be different, then what needs to be the same? We need the same highly motivated, highly skilled and perhaps most importantly, highly compassionate caregivers selflessly caring for one another and their communities.

Mike Young. President and CEO of Temple University Health System (Philadelphia): Cell therapy, gene therapy, and immunotherapy will continue to rapidly improve and evolve, replacing many traditional procedures with precise therapies to restore normal human function — either through cell transfer, altering of genetic information, or harnessing the body’s natural immune system to attack a particular disease like cancer, cystic fibrosis, heart disease, or diabetes. As a result, hospitals will decrease in footprint, while the labs dedicated to defining precision medicine will multiply in size to support individual- and disease-specific infusion, drug, and manipulative therapies.

Hospitals will continue to shepherd the patient journey through these therapies and also will continue to handle the most complex cases requiring high-tech medical and surgical procedures. Medical education will likely evolve in parallel, focusing more on genetic causation and treatment of disease, as well as proficiency with increasingly sophisticated AI diagnostic technologies to provide adaptive care on a patient-by-patient basis.

Tom Siemers. Chief Executive Officer of Wilbarger General Hospital (Vernon, Texas): My predictions include the national healthcare landscape will be dominated by a dozen or so large systems. ‘Consolidation’ will be the word that describes the healthcare industry over the next 10 years. Regional systems will merge into large, national systems. Independent and rural hospitals will become increasingly rare. They simply won’t be able to make the capital investments necessary to replace outdated facilities and equipment while vying with other organizations for scarce, licensed personnel.

Jim Heilsberg. CFO of Tri-State Memorial Hospital & Medical Campus (Clarkston, Wash.): Tri-State Hospital continues to expand services for outpatient services while maintaining traditionally needed inpatient services. In 10 years, there will be expanded outpatient services that include leveraged technology that will allow the patient to be cared for in a yet-to-be-seen care model, including traditional hospital settings and increasing home care setting solutions.

Jennifer Olson. COO of Children’s Minnesota (St. Paul, Minn.): I believe we will see more and better access to healthcare over the next 10 years. Advances in diagnostics, monitoring, and artificial intelligence will allow patients to access services at more convenient times and locations, including much more frequently at home, thereby extending health systems’ reach well beyond their walls.

What I don’t think will ever change is the heart our healthcare professionals bring with them to work every day. I see it here at Children’s Minnesota and across our industry: the unwavering commitment our caregivers have to help people live healthier lives.

If I had one wish for the future, it would be that we become better equipped to address the social determinants of health: all of the factors outside the walls of our hospitals and clinics that affect our patients’ well-being. Part of that means relaxing regulations to allow better communication and sharing of information among healthcare providers and public and private entities, so we can take a more holistic approach to improve health and decrease disparities. It also will require a fundamental shift in how health and healthcare are paid for.

Stonish Pierce. COO of Holy Cross Health, Trinity Health Florida: Over the next decade, many health systems will pivot from being ‘hospital’ systems to true ‘health’ systems. Based largely on responding to The Joint Commission’s New Requirements to Reduce Health Care Disparities, many health systems will place greater emphasis on reducing health disparities, enhanced attention to providing culturally competent care, addressing social determinants of health (including, but not limited to food, housing and transportation) and health equity. I’m proud to work for Trinity Health, a system that has already directed attention toward addressing health disparities, cultural competency and health equity.

Many systems will pivot from offering the full continuum of services at each hospital and instead focus on the core services for their respective communities, which enables long-term financial sustainability. At the same time, we will witness the proliferation of partnerships as adept health systems realize that they cannot fulfill every community’s needs alone. Depending upon the specialty and region of the country, we may see some transitioning away from the RVU physician compensation model to base salaries and value-based compensation to ensure health systems can serve their communities in the long term.

Driven largely by continued workforce supply shortages, we will also see innovation achieve its full potential. This will include, but not be limited to, virtual care models, robots to address functions currently performed by humans, and increased adoption of artificial intelligence and remote monitoring. Healthcare overall will achieve parity in technological adoption and innovation that we take for granted and have grown accustomed to in industries such as banking and the consumer service industries.

For what will remain the same, we can anticipate that government reimbursement will still not cover the cost of providing care, although systems will transition to offering care models and services that enable the best long-term financial sustainability. We will continue to see payers and retail pharmacies continue to evolve as consumer-friendly providers. We will continue to see systems make investments in ambulatory care and the most critically ill patients will remain in our hospitals.

Jamie Davis. Executive Director, Revenue Cycle Management of Banner Health (Phoenix): I think that we will see a continued shift in places of service to lower-cost delivery sources and unfavorable payer mix movement to Medicare Advantage and health exchange plans, degrading the value of gross revenue. The increased focus on cost containment, value-based care, inflation, and pricing transparency will hopefully push payers and providers to move to a more symbiotic relationship versus the adversarial one today. Additionally, we may see disruption in the technology space as the venture capital and private equity purchase boom that happened from 2019 to 2021 will mature and those entities come up for sale. If we want to continue to provide the best quality health outcomes to our patients and maintain profitability, we cannot look the same in 10 years as we do today.

James Lynn. System Vice President, Facilities and Support Services of Marshfield Clinic Health System (Wis.): There will be some aspects that will be different. For instance, there will be more players in the market and they will begin capturing a higher percentage of primary care patients. Walmart, Walgreens, CVS, Amazon, Google and others will begin to make inroads into primary care by utilizing VR and AI platforms. More and more procedures will be the same day. Fewer hospital stays will be needed for recovery as procedures become less invasive and faster. There will be increasing pressure on the federal government to make healthcare a right for all legal residents and it will be decoupled from employment status. On the other hand, what will stay the same is even though hospital stays will become shorter for some, we will also be experiencing an ever-aging population, so the same number of inpatient beds will likely be needed.

Payers, pharmacy benefit managers and drug manufacturers are no strangers to heavy criticism from the public and providers alike. Now another sector of the healthcare system has found itself increasingly caught in the crosshairs of constituents looking to point a finger for the rising cost of care: hospitals.

As sharp words against the industry bubble up more often and encompass a wider variety of issues, it marks an important turn in the ethos of American healthcare. Most policymakers have historically wanted hospitals on their side, and health systems are often the largest employer within their communities and in many states.

“In my career, I’ve never seen things more aligned to the detriment of hospitals than it is now,” Paul Keckley, PhD, said. Dr. Keckley is a widely known industry analyst and editor of The Keckley Report, a weekly newsletter discussing healthcare policy and current trends.

Confidence in the medical system as a whole fell from 51 percent in 2020 to a record low of 38 percent in 2022. Though the healthcare system is among all major U.S. institutions facing record-low public confidence, are hospitals ready for an era of widespread distrust?

“We’re going into hospital purgatory. It’s a period in which old rules may not work in the future,” Dr. Keckley said. “The only thing we know for sure is that it’s not going to get easier.”

State-versus-hospital fights have popped up throughout the U.S. over the past year. Most recently, in Colorado, a back and forth unfolded between Gov. Jared Polis and the state’s hospital association over who is ultimately responsible for high care costs. In a speech Jan. 17, the Democratic governor accused Colorado’s hospitals of overcharging patients and sitting on significant cash reserves.

“It’s time that we hold them accountable,” he said.

The Colorado Hospital Association says the data supporting those claims does not reflect the several ongoing industry challenges, among them labor shortages, regulatory burdens and inflationary pressures.

“Unfortunately, we continue to hear rhetoric against the hospitals and health systems that have worked diligently on healthcare quality, access and affordability,” CHA said in a statement to Becker’s. “Colorado’s hospitals and health systems have been working with the administration on many of these programs, including reinsurance, hospital discounted care, price transparency, out-of-network patient protections, and more.”

Some 1,500 miles eastward, another incident of hospital-community conflict grew. In January, Pennsylvania lawmakers promoted a nonpartisan report that accuses UPMC of building a monopoly in the state through consolidation over the last decade — the Pittsburgh-based system refuted the claims, saying they were based on “flawed data.”

To the south, North Carolina officials accused the state’s seven largest health systems in June of using pandemic aid to enrich themselves. Hospitals said the accusations were based on “cherry-picked data” spun in a way that does not reflect their ongoing challenges.

As state- and market-level fights against hospitals intensify and grab national attention, hospitals and health systems may find themselves less familiar in steadying public perception than their payer and pharmaceutical counterparts, who are no strangers to vocal opponents.

“With public opinion shifting a bit amid COVID, and with some anecdotal evidence that hospitals are doing some bad things, state policymakers feel that they are enjoying the political will to make these gestures,” Ge Bai, PhD, said. “It’s also a key issue for voters. Even if they don’t do anything in reality, the gesture will probably get political capital.”

Dr. Bai is a professor of accounting and health policy at Baltimore-based Johns Hopkins University. She believes a key underlying factor driving hospital critiques as of late is the reduced public confidence in medicine by way of the pandemic.

“The hospital industry has moved away from its traditional charitable mission and toward a business orientation that is undeniable,” she said. “With the [pandemic] dust settling, I think a lot of people realize the clinicians are the heroes, but hospitals are maybe not as altruistic as they once thought.”

In 2021, over 70 percent of Americans said they trusted physicians and nurses, but only 22 percent said the same about hospital executives, according to a study from the University of Chicago and The Associated Press-NORC Center for Public Affairs Research.

“It’s a tough job and a complicated business to run, and everybody in the community has an opinion about it based on anecdotal evidence,” Dr. Keckley said. “I think much of the blame too for hospitals taking a lot of hits has been boards that are not prepared to govern.”

For both Drs. Keckley and Bai, there are other major issues they each point to as contributing factors to the growing wariness around hospital operations:

A lack of compliance with CMS price transparency rules. Some of the most recent studies estimate hospital compliance rates could range from 16 percent to 55 percent, while hospitals say the issue has been mischaracterized. CMS has penalized very few hospitals for noncompliance since the rule took effect in 2021.

The decades-long trend of consolidation hitting a tipping point. With consolidation, hospitals have long argued the trend would lead to more efficiency, care access, quality of care and lower costs. One of the most comprehensive consolidation studies to date was released Jan. 24 in JAMA and concluded that merged health systems have led to “marginally better care at significantly higher costs.”

“Hospitals are doing exactly what they’re supposed to do — make money to survive and expand,” Dr. Bai said. “Instead of blaming individual players, we have to raise the bar and think about who created the system in the first place that makes competition so difficult — the government.”

State retirement benefits plans struggling financially. Though not a new trend, unfunded healthcare benefits promised to retired public employees and their dependents continues to grow around the country, incentivizing state lawmakers to look in new directions to save on costs. Unfunded retiree healthcare liabilities across all states surpassed $1 trillion in 2019, according to the American Legislative Exchange Council.

Competition from other healthcare sectors. Competition for patients has arrived from other healthcare sectors, especially from payers. In 2023, UnitedHealth Group’s Optum owns or is affiliated with the most physicians in the country at 60,000, though it’s likely higher after several large acquisitions last year.

“The center of gravity in healthcare has shifted from hospitals that muscled their way into scaling,” Dr. Keckley said. “The reality is that providing hospital services in non-hospital settings that are safe, effective and less costly is where the market, and insurers, are going.”

Despite the uptick in states and Americans that have gone into fault-finding mode against hospitals and those running them, operating a financially successful hospital or health system in 2023 is a monumental task, perhaps even close to impossible for many. Last year, approximately half of U.S. hospitals finished the year with a negative margin, making it “the worst financial year” for the industry since the start of the pandemic, according to Kaufman Hall’s latest “National Flash Hospital Report.”

“Hospitals aren’t going into this with a huge amount of goodwill at their backs, and I think that’s what they need to be prepared for,” Dr. Keckley said. “You can’t just go in and tell the story of ‘look at what we do for the community’ or ‘look at all the people we employ’ — that is not going to work anymore.”

On Monday, Indiana-based Elevance Health, formerly known as Anthem, announced it has signed a deal to add Blue Cross Blue Shield of Louisiana (BCBSLA) to its network of Blues plans for an undisclosed sum. BCBSLA covers two-thirds of the state’s commercial insurance market, and has partnered with Elevance for five years to serve Louisiana’s dual-eligible population.

Elevance will operate BCBS plans in 15 states and cover 49M beneficiaries should the acquisition go through, though the move faces regulatory obstacles around folding nonprofit BCBSLA into its for-profit business.

The Gist:This deal is a harbinger for similar combinations to come. We’ve long been expecting more roll-ups of state- and regional-level plans as they struggle to compete with the for-profit national giants.

Standalone regional plans often lack the scale to diversify their businesses and emulate the successful strategic playbooks of national insurers like UnitedHealth Group and Humana, which have rapidly expanded into the more profitable areas of care provision, provider support services, and pharmacy benefit management.

State-level Blues plans have long been dominant in the PPO-driven commercial market, but have experienced mixed success in expanding into Medicare Advantage and other segments. If these mid-sized insurance players find they can’t compete alone, it won’t bode well for the cohort of much smaller “insurtech” startups.

After the number of health system mergers and acquisitions (M&A) reached a recent low in 2021, last year saw a slight rebound in deal volume, while continuing the trend toward mergers between larger systems.

Using data from Kaufman Hall’s 2022 M&A report, the graphic below shows that the number of announced health system M&A transactions dropped by over 50 percent from 2017 to 2022, while the average revenue of the smaller system in each deal increased by over 125 percent. The steadily rising average size of the smaller party is a product of both larger transactions occurring more frequently and smaller deals happening less often.

Since 2019, when the average seller posted $272M in annual revenue, the number of billion-dollar revenue systems merging together has more than doubled, while pickups of hospitals with less than $100M in annual revenue declined by over 65 percent.

Between the industry’s march toward consolidation, which has left only 20 percent of hospitals independent, and the market pressures created by vertically-integrated payers, we expect “mega-mergers” to be the new normal, especially as health system leaders look to build cross-regional scale while regulators continue to heavily scrutinize in-market combinations.

The U.S. economy grew at an annualized 2.9% rate in the final months of 2022, the Commerce Department said on Thursday.

Why it matters:

Economists are bracing for a significant slowdown in economic activity as the Federal Reserve’s interest rates hikes take hold, but that certainly wasn’t the case in the final months of last year.

Economists expected the Gross Domestic Product figures to show the economy grew at a 2.6% annualized rate last quarter, after expanding at a 3.2% pace in the prior quarter.

Details:

Consumer spending and businesses built up private inventories gave GDP the biggest boost. Among the biggest drags: fixed investment, a category that includes housing.

By the numbers:

Over the calendar year, GDP grew by 2.1% in 2022 — a decent pace, especially considering the historically aggressive rate hikes by the Federal Reserve that sought to restrain economic activity to contain inflation.

Those rate hikes hit the housing sector particularly hard, which dragged down overall growth earlier last year.

Catch up quick:

The first half of 2022 was dogged by fears that the economy had entered a recession, after back-to-back quarters of contractions. But by the second half of the year, the economy had returned to growth mode.

The growth over 2022 was an expected slowdown from the 5.9% achieved in 2021, when the economy bounced back from the pandemic shock.

In our decades of working in healthcare, we’ve never seen a time when payer-provider negotiations have been more tense. Emboldened insurers, having seen strong growth during the pandemic, are entering contract negotiations with an aggressive posture.

“They weren’t even willing to discuss a rate increase,” one CFO shared as he described his health system’s recent negotiations with a large national insurer. “The plan’s opening salvo was a fifteen percent rate cut!”

Health systems are feeling lucky to get even a two or three percent rate bump, well short of the historical average of seven percent—and far short of what would be needed to account for skyrocketing labor, supply, and drug costs. According to executives we work with, efforts to describe the current labor crisis and resulting cost impacts with payers are largely falling on deaf ears.

This scenario is playing out in markets across the country, with more insurers and health systems announcing that they are “terming” their contract, publicly stating they will cut ties should the stalemate in negotiations persist.

Speaking off the record, a system executive shared how this played out for them. With negotiations at an impasse, a large insurer began the process of notifying beneficiaries that the system would soon be out-of-network, and patients would be reassigned to new primary care providers. The health plan assumed that the other systems in the market would see this as a growth opportunity—and was shocked when they discovered that other providers were already operating at capacity, unable to accommodate additional patients from the “terminated” system.

Mounting concerns about access brought the plan back to the table. Even in the best of times, a major insurer cutting ties with a health system is extremely disruptive for consumers, who must shift their care to new providers or pay out-of-network rates. But given current capacity challenges in hospitals nationwide, major network disruptions can be even more dire for patients—and may force payers and providers to walk back from the brink of contract termination.

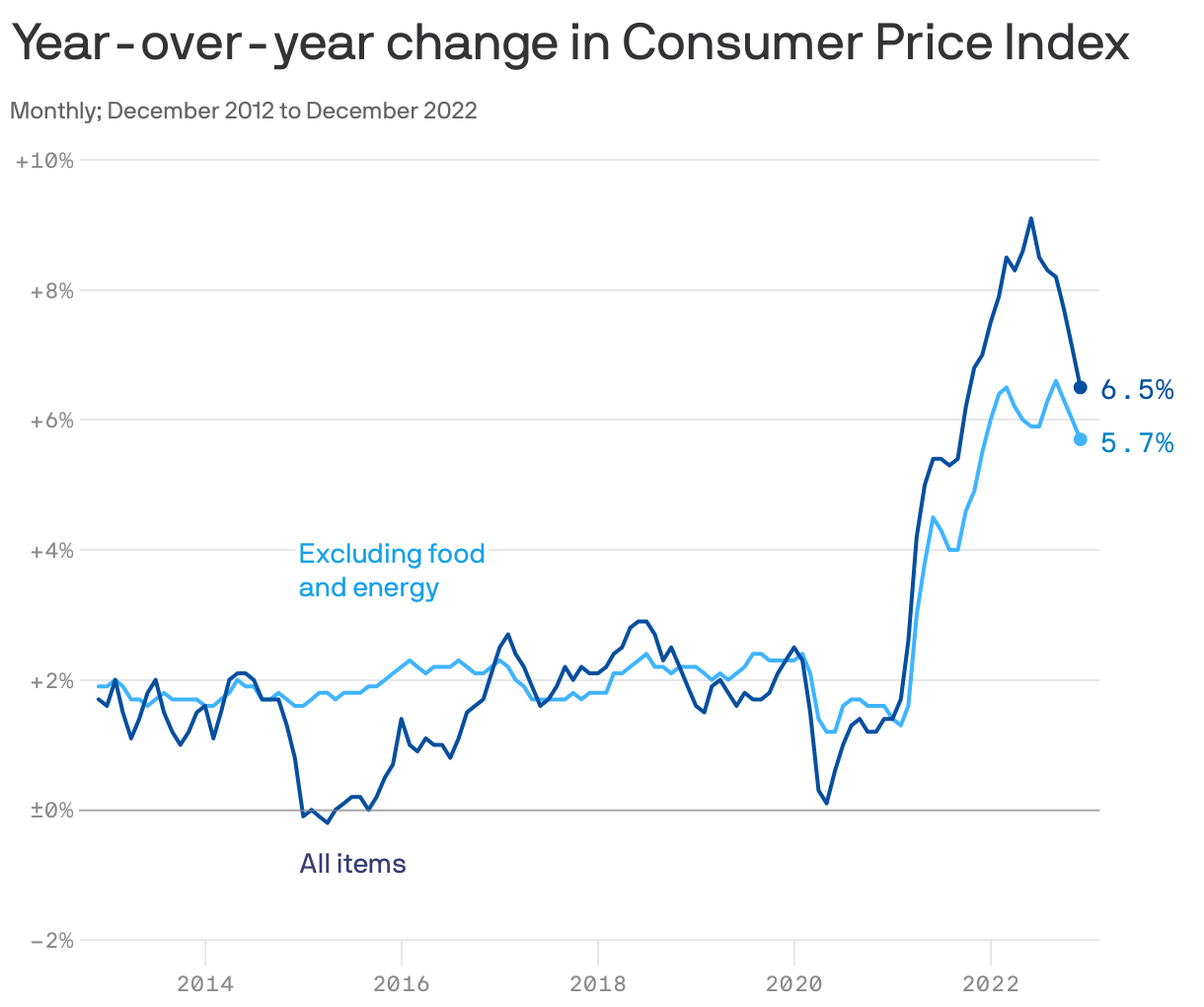

It may be time to update your inflation narrative.

The ultra-hot readings that defined the first half of 2022 appear to be firmly in the rearview mirror, improving the odds that price pressures can dissipate further without excessive economic pain.

That’s the key takeaway from the December Consumer Price Index released this morning, which confirmed notably cooler inflation as the year came to a close.

Why it matters:

The nation’s inflation problem isn’t over, but so far inflation is slowing while the job market is still healthy, an enviable combination.

As Princeton economist Alan Blinder put it in an op-ed last week, inflation was “vastly lower” in the second half of 2022 than the first; yet, “hardly anyone seems to have noticed.”

By the numbers:

In the final three months of 2022, core inflation (which excludes food and fuel costs) came in at an annualized 3.1% — higher than the Fed aims for, but hardly crisis levels. In the second quarter of the year, that number was 7.9%.

It’s a stunning decline, occurring alongside a labor market that by nearly all measures is still flourishing. Just this morning, the Labor Department announced that jobless claims fell to an ultra-low 205,000 last week.

State of play:

Grocery prices rose 1.1% in the final three months of the year, an uncomfortably high rate, but not as extreme as the rates seen earlier in 2022.

Gasoline prices, pushed up by Russia’s invasion of Ukraine, were once the crucial reason why inflation was rising. In recent months, the opposite has been true: December pump prices slid 9.4%, helping drag the overall index into negative territory.

Disinflation was at work for many other goods, including used cars (-2.5%) and new vehicles (-0.1%) where prices have reversed, helped by easing supply chain bottlenecks.

Shelter costs pushed inflation upward, surging 0.8% in December. But private-sector data points to rents on new leases falling in recent months, which would only filter into the CPI data over time. That makes for a more benign inflation outlook in 2023.

What to watch:

That’s not to say there aren’t risks ahead. The war in Ukraine is ongoing, and another energy price shock could occur.

The Fed has also focused in on the services sector, where price increases have slowed from last summer but remain frothy. The risk is that business costs associated with the still-tight labor market (like higher wages) will pass through to prices for consumers.

The bottom line:

Inflation will still be a worry in 2023, but much less so than it seemed a few months ago.

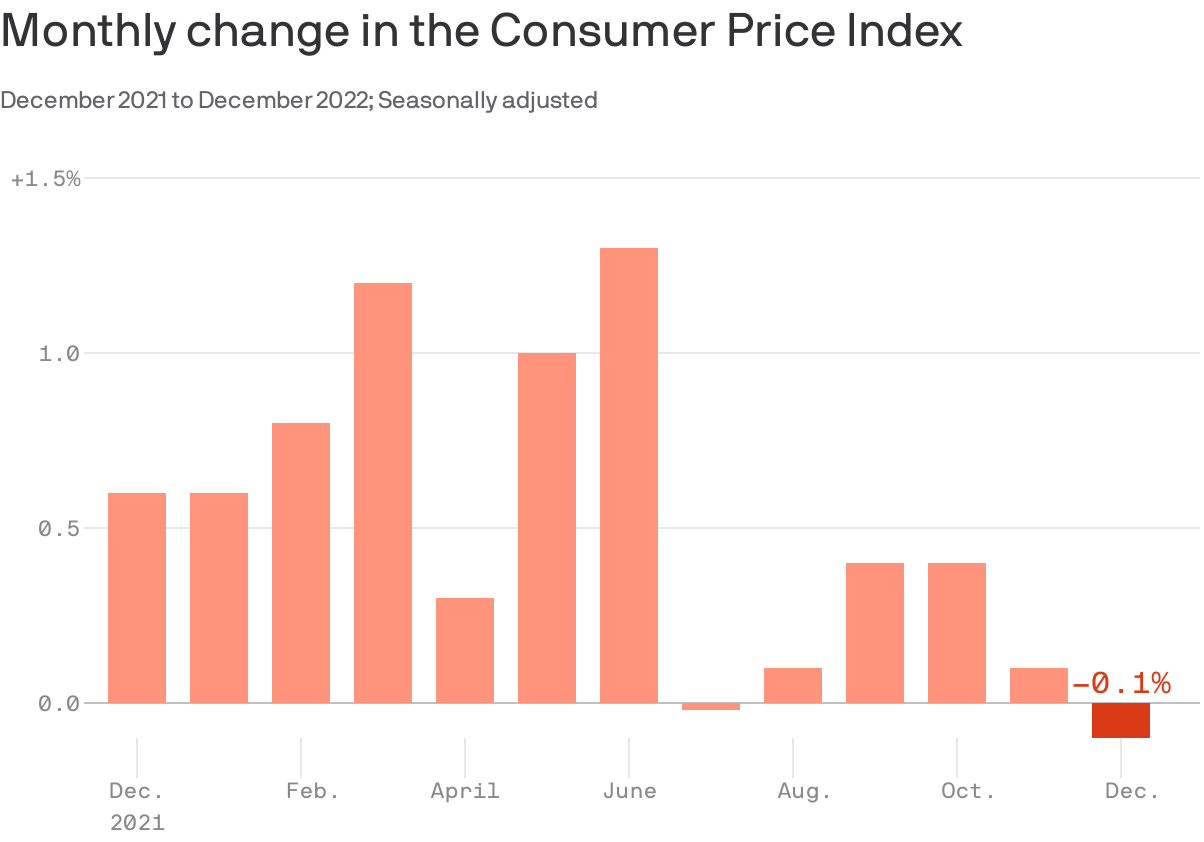

U.S. consumers got a reprieve from soaring costs in December: the Consumer Price Index declined on a monthly basis, the first drop since last summer as falling prices for items including gasoline and used carsdragged the overall index down.

By the numbers:

The index, which captures price changes across a basket of consumer goods and services, fell 0.1%, following an increase by the same amount in November. Over the past 12 months ending in December, the index is up 6.5%, falling from 7.1% through November.

Core CPI, which excludes food and fuel costs, rose by0.3% last month. Over the last 12 months through December, the index rose 5.7%. In November, those figures were 0.2% and 6%, respectively.

Why it matters:

The hot inflation that persisted through much of last year continues to show signs of receding — offering at least some relief for shoppers, the White House and the Federal Reserve, though some underlying inflation pressure remains.

Where it stands:

The data caps a year in which consumer prices rose rapidly, though the pace of cost increases began to slow in the final months of the year.

As consumers shifted spending and supply chains began to heal, price increases for a range of goods have cooled or, in some cases, costs have fallen outright.

Between the lines:

The Federal Reserve, which has been raising interest rates aggressively to tame inflation, is watching the services sector closely, where inflation can be more challenging to stamp out.

A sub-index measuring price moves within the services category (excluding housing) accelerated by 0.4%, after two straight months of cooler readings

Still, in the 12 months through December, this sub-index is up 7.4%(compared to 7.3% in November).