Nonprofit hospitals are reporting thinner margins this year, stretched by rising labor, supply and capital costs, and will be pressed to make big changes to their business models or risk negative rating actions, Fitch Ratings said in a report out Tuesday.

Warning that it could take years for provider margins to recover to pre-pandemic levels, Fitch outlined a series of steps necessary to manage the inflationary pressures. Those moves include steeper rate increases in the short term and “relentless, ongoing cost-cutting and productivity improvements” over the medium term, the ratings agency said.

Further out on the horizon, “improvement in operating margins from reduced levels will require hospitals to make transformational changes to the business model,” Fitch cautioned.

Dive Insight:

It has been a rough year so far for U.S. hospitals, which are navigating labor shortages, rising operating costs and a rebound in healthcare utilization that has followed the suppressed demand of the early pandemic.

The strain on operations has resulted in five straight months of negative margins for health systems, according to Kaufman Hall’s latest hospital performance report.

Fitch said the majority of the hospitals it follows have strong balance sheets that will provide a cushion for a period of time. But with cost inflation at levels not seen since the late 1970s and early 1980s, and the potential for additional coronavirus surges this fall and winter, more substantial changes to hospitals’ business models could be necessary to avoid negative rating actions, the agency said.

Providers will look to secure much higher rate increases from commercial payers. However, insurers are under similar pressures as hospitals and will push back, using leverage gained through the sector’s consolidation, the report said.

As a result, commercial insurers’ rate increases are likely to exceed those of recent years, but remain below the rate of inflation in the short term, Fitch said. Further, federal budget deficits make Medicare or Medicaid rate adjustments to offset inflation unlikely.

An early look at state regulatory filings this summer suggests insurers who offer plans on the Affordable Care Act exchanges will seek substantial premium hikes in 2023, according to an analysis from the Kaiser Family Foundation. The median rate increase requested by 72 ACA insurers was 10% in the KFF study.

Inflation is pushing more providers to consider mergers and acquisitions to create economies of scale, Fitch said. But regulators are scrutinizing deals more strenuously due to concerns that consolidation will push prices even higher. With increased capital costs, rising interest rates and ongoing supply chain disruptions, hospitals’ plans for expansion or renovations will cost more or may be postponed, the report said.

Private insurers pay high and rising prices to hospitals. But whether this is “good” or “bad” depends on what’s behind this phenomenon. Do high prices reflect investments in quality? Or do they instead reflect issues like lack of competition due to hospital consolidation? The answer matters for efforts to reduce health care spending.

In a new paper in the Journal of Health Economics, Craig Garthwaite, Christopher Ody and Amanda Starc investigated whether the prospect of financial rewards drove differences in hospital quality measures — including things like mortality rates, patient experience, technology adoption and emergency department wait times. Specifically, the authors’ examined whether hospitals are more likely to invest in quality if they will be rewarded through higher prices. This is more feasible if they’re serving lots of commercially insured patients, since private insurers may pay higher rates if patients value those hospitals. But that strategy may not be successful in areas with large shares of the population on Medicare and Medicaid, which do not negotiate prices.

The researchers found that:

Hospitals in areas with more privately insured patients had higher quality scores compared to hospitals with more publicly insured patients.

Hospitals targeting more privately insured patients also had higher costs than those relying more on payers like Medicare and Medicaid.

These results suggest hospitals make strategic investments in quality to attract privately insured patients. This is consistent with what one might expect from market competition and the results of other recent research. These findings do not, however, imply that prices are “optimal.” Prices also reflect factors like provider consolidation that have little observable effects on quality. Indeed, hospital prices likely reflect a mix of valuable and wasteful spending.

The analysis does have limitations. The authors used the demographics of the areas around the hospital instead of each hospital’s actual potential mix of patients. In addition, it is possible that some quality differences across hospitals actually reflect differences between patients with private and public insurance which aren’t easy to capture in data. However, the authors’ results were similar across several quality measures, including those where this is less of a concern.

These results can help better inform efforts to reduce health care costs. Policymakers interested in reducing hospital prices should be aware that doing so might reduce investments in quality. This suggests placing a greater emphasis on policies that target prices stemming from clear sources of inefficiencies, like consolidation, since such tradeoffs are likely smaller.

Nothing kills the momentum and excitement of race day more than the yellow flag and deployed safety car. Unsafe track conditions, usually caused by an accident, debris on the track or a stopped vehicle, can cause the marshals to slow down the race. Momentum moderates and adrenaline wanes. Drivers are forbidden from overtaking, and victory is temporarily out of sight for all but the lead car. As I watched the Indy 500, 24 Hours at Le Mans and a handful of Formula One grand prix over the last several weeks, it struck me that postacute sector M&A (home health, hospice, Medicaid PCS, pediatric PDN/therapy) is currently racing under yellow flag conditions. Temporary, but nonetheless frustrating for all constituents involved.

The post-acute sector’s two record setting years in terms of transaction activity, valuation multiples and quality of companies acquired, 2020 and 2021, now appear to be in the rearview mirror. In their stead is a sluggish 2022, with companies staying in their lanes, focused inwardly on operations and trying to regain levels of growth and profitability of prior years. It should come as no surprise that sector activity has slowed: (i) the supply of actionable platforms is materially lower than in the prior two years; (ii) the COVID spawned labor market continues to create one of the most challenging operating environments in recent memory; (iii) home health reimbursement faces a potentially challenging outlook when the CY 2023 HH PPS rule is finalized in the Fall; and (iv) buyers are less willing to give credit for COVID-related EBITDA adjustments.

Lower Inventory of Actionable Platforms Many of the most actionable privately-held and sponsor-owned platforms transacted at a kinetic pace in 2019, 2020 and 2021. As a result, the number of available platforms is relatively low, and the sector is currently in a holding pattern, where businesses are (i) focused on operating in a challenging environment, (ii) too early in their hold period, or (iii) waiting for financial performance to improve, before coming to market. There is a large and growing backlog of businesses that we expect to come to market when overall conditions improve, potentially as early as Q4 2022. But in the meantime, the market is generally in wait and see mode.

Labor Market’s Impact on Performance Q4 2021 was one of the most challenging quarters for post-acute operators, particularly hospice, as the Omicron variant wreaked havoc on staffing and admissions volumes. Despite strong referral volumes and demand for post-acute services, the inability to

sufficiently hire and retain clinical staff has had a material impact on monthly sequential growth and TTM performance. For many, Q1 2022 was only marginally better, and for some, Q2 2022 continues to present challenges, although, anecdotally, the clinical labor market appears to be improving and may even accelerate due to the looming recession. As a result, companies are deciding, or being forced, to delay sale processes as they attempt to replace poor financial performance in Q4 2021 and Q1 2022 with improved 2H 2022 growth and profitability.

Pending CY 2023 Home Health PPS Rule Based on the proposed rule released last week, CMS estimates that Medicare payments to home health agencies in CY 2023 would decrease in the aggregate by -4.2%, or -$810 million compared to CY 2022. Without getting too technical and comprehensive, this decrease reflects the effects of the proposed 2.9% home health payment update percentage ($560 million increase), an estimated 6.9% decrease that reflects the effects of the proposed prospective, permanent behavioral assumption adjustment of -7.69% ($1.33 billion decrease), and an estimated 0.2% decrease that reflects the effects of a proposed update to the fixed-dollar loss ratio (FDL) used in determining outlier payments ($40 million decrease). Prospective home health sellers will most likely wait for better clarity on the final rule before coming to market.

Market Push Back on COVID-Related EBITDA Adjustments Buyers and lenders have materially increased their scrutiny of COVID-related volume adjustments to EBITDA. Early in the pandemic, the market was quite willing to pay sellers for normalized volumes and financial performance, as if “COVID had not happened.” 27 months later, the market is taking a harder line. “What if” earnings credit is no longer being given wholesale. The market has taken the position that labor staffing challenges and higher labor wage expense are here to stay (for now), and, unless a seller has clearly demonstrated a trend to the contrary, little to no valuation / leverage credit will be given for such adjustments. As a result, prospective sellers must increasingly rely on actual earnings to ensure the achievement of valuation expectations.

Returning to our racing analogy, post-acute sector M&A is currently under a yellow flag. And while yellow flag conditions produce little to no racing action, and can last for many laps, they are still only temporary. Drivers and their teams can use the time to their advantage – to “box” or “pit” in order to change tires, refuel or tweak the car – so that they are ready to drop the hammer once the yellow flag is lifted. This is exactly what the higher quality post-acute platforms are doing. Some of the most exciting action in a race comes once the safety car exits the track and green flag racing resumes. Given the strong near- and long-term demographic and sector trends supporting the post-acute sector, and the almost unlimited demand for high quality post-acute platforms, there is little doubt that M&A activity will resume with a vengeance.

Steward Health Care is abandoning its proposal to sell five Utah hospitals to HCA Healthcare, and New Jersey-based RWJBarnabas Health dropped its plan to purchase New Brunswick, NJ-based Saint Peter’s Healthcare System. These pivots come just weeks after the Federal Trade Commission (FTC) filed suits to block the transactions, saying they would reduce market competition. The FTC said in a statement that these deals “should never have been proposed in the first place,” and “…the FTC will not hesitate to take action in enforcing the antitrust laws to protect healthcare consumers who are faced with unlawful hospital consolidation.”

The Gist: These latest mergers follow the fate of the proposed Lifespan and Care New England merger in Rhode Island, and the New Jersey-based Hackensack Meridian Health and Englewood Health merger, which were both abandoned after FTC challenges earlier this year.

Antitrust observers find these recent challenges unsurprising, as all were horizontal, intra-market deals of the kind that commonly raise antitrust concerns. What will be more telling is whether antitrust regulators can successfully mount challenges of cross-market mergers, or vertical mergers between hospitals, physicians, and insurers.

Citi, The American Hospital Association (AHA) and the Healthcare Financial Management Association (HFMA) recently hosted the 22nd annual Not-for-Profit Healthcare Investor Conference. The event was in person, after being virtual in 2021 and canceled in 2020 due to the pandemic. Leaders from over 25 diverse health systems, as well as private equity and fund managers, presented in panel discussions and traditional formats. The following summary attempts to synthesize key themes and particularly interesting work by leading health systems. The conference title was “Refining the Now, Reshaping What’s Next.”

Is Healthcare Headed for Best of Times or Worst of Times?

Clearly the pandemic showed how essential and adaptive the US healthcare industry is, and especially how incredible healthcare workers continue to be. It also exposed and accelerated many underlying dynamics, such as impact of disparities, clinical labor shortages and supply chain challenges. On balance, at this year’s conference presenters remained quite optimistic about the future, and felt that despite enormous pain, the pandemic has helped to accelerate positive transformation across healthcare.

At the same time, almost all presenters referenced future headwinds from labor and supply inflation, concerns about increasing payment pressures, and the continued need to address disparities and social justice. That being said, there was not much disclosure at the conference about just how bad things could get in the future given accelerated operational and financial risks.

As usual at such a conference, there was much passion, creativity, sharing and celebration. While each organization and market differ somewhat, the following are common themes discussed.

Key Themes

Enormous Workforce Challenges – Every speaker referenced workforce as being THE key issue they are facing, specifically retirement, recruitment, retention, well-being and cost. We have talked for years about a future caregiver shortage, but this reality was accelerated by the pandemic. The majority of health systems saw single-digit turnover rates grow to 20-30%, and the cost of temporary labor such as traveling nurses, decimate operating margins. The many strategies discussed at the conference went beyond simply paying more to attract and retain staff. A key question is whether organization-specific strategies will be enough, or whether we need a broader societal and industry-wide collaborative effort to dramatically increase training slots for nurses and other allied health professionals.

Pandemic Stressed Organizations and Accelerated Transformation – At the 2021 virtual Citi/AHA/HFMA conference, many posited that the country was past the worst of the pandemic. (In fact this author’s summary of last year’s conference was titled “Sunrise After the Storm”). That was before the Omicron wave hit hard in Q1 2022. First-quarter 2022 operating margins were negative for most but not all healthcare systems due to cumulative impact of Omicron, temporary labor and supply costs, especially since the governmental support that partially offset those costs in 2020 ended. Organizations and their teams remain resilient, but highly stressed. Risks and challenges associated with future waves continue, as well as high reliance on foreign drug and supply manufacturing. While highly distracting and painful, many organizations discussed how the pandemic actually accelerated the pace of transformation. Necessity drives required action, and at least temporarily overcomes political and cultural barriers to change.

Growing Pursuit of Scale, Including through M&A and Partnerships – All health systems continue to be highly complex with multiple competing “big-dot” priorities. Multiple systems described their current M&A and growth strategies, pursuit of scale, as well as how these strategies were impacted by the pandemic. While the provider community remains highly unconsolidated on a national basis, mergers are more frequent, including between non-contiguous markets. Systems said that larger size, coupled with disciplined management, can reduce cost structure and improve quality and patient experience. While some pursue scale through organic growth initiatives or M&A, others described success in creating scale by leveraging partnerships with “best-in-class” niche organizations and other outside expertise.

Health Equity, Diversity and ESG as Core to Mission – Consistent with last year, most speakers discussed their efforts to address health equity, social justice, diversity, and Social Determinants of Health. Many health systems have developed robust strategies quickly as the pandemic spotlighted the impact of existing disparities. There is increasing interest in Environment, Social and Governance (ESG) initiatives, including environmental stewardship to improve the health of their communities and the world by reducing their carbon footprint and medical waste.

Patient-Centric Care Transformation Continues as a Priority – The pandemic significantly accelerated the shift to telehealth and virtual care. Many health systems are increasing their efforts to design care around the patient instead of the traditional provider centric focus. While the need for inpatient care will always continue, more care is taking place in settings closer to or at home, with digital enablement. Expansion of personalized medicine, genetic testing and therapies, and drug discovery are transforming how healthcare is provided.

Affordability and Value-Based Care – US healthcare costs as a percentage of GDP increased from 18% in 2019 to almost 20% in 2020, mainly driven by the pandemic. There remains a dichotomy between reliance on fee-for-service payment and commitment to value-based care. Although only 11% of commercial payment is currently through two-sided risk arrangements, almost all presenting health systems discussed their strategies to continue moving to value-based care and to improve affordability. Some systems are leveraging their integrated health plans and/or expanding risk-based contracts. Many are trying to reduce unnecessary care through adoption of evidence-based models and to shift care to less costly settings.

Inflation and Accelerating Financial Pressures – Health systems are facing unprecedented increases in labor and supply costs, that are likely to continue into the foreseeable future. At the same time, commercial payment rate adjustments are “sticky low” as insurers and employers push back on rate increases. Governmental payment rate increases are less than cost inflation. In addition to current cuts like the re-implementation of sequestration, longer-term cuts to provider assessment programs, provider-based billing, disproportionate share and Medicaid expansion may severely impact many organizations over time. Benefits like 340b discounts are also experiencing pressure. Post-pandemic clinical-volume trends remain unclear, and additional governmental support associated with future pandemic waves is unlikely. Adding to these challenges, declines in stock and bond prices are negatively impacting currently strong balance sheets.

Conclusion: Best or Worst of Times in Healthcare?

Time will tell, in retrospect, if the next five years will be the best of times, worst of times, or both in healthcare. Optimists point to the resiliency of healthcare organizations; enormous opportunity to reduce unnecessary cost through adoption of evidence-based care and scale; pipeline of new cures and technology; and opportunities to address social and health equity. Pessimists point to likely unprecedented financial pressures and operational challenges due to endemic labor and supply shortages; high-cost inflation vs. constrained payment rates; and future uncertainty about the pandemic, the economy and investment markets.

The situation will undoubtedly vary by market and organization as reflected in conference presentations, but all systems will likely face substantial pressure. As one speaker noted “humans have a great ability to respond to pain,” so this may be the inflection point where more healthcare systems radically accelerate necessary change to improve health, make healthcare more equitable and affordable, with higher quality and better outcomes. Some health systems are clearly doing that, with pace, nimbleness and passion. Can the industry as a whole accomplish it successfully?

Consumers and employers recently filed lawsuits against Hartford HealthCare, HCA Healthcare, and Advocate Aurora Health, accusing the health systems of using their market power to increase prices through anticompetitive contracting practices. New reporting from the Wall Street Journal finds that all three suits are receiving funding from billionaire John Arnold, through his charitable foundation Arnold Ventures, which has sponsored several efforts to reduce healthcare spending. While the health systems say that the claims are baseless, the law firm leading the suits, Fairmark Partners, says that it’s attempting to enforce antitrust laws through the courts.

The Gist: Amid the Biden administration’s increased scrutiny of health system anticompetitive behavior, state governments and philanthropic groups are also taking a more active role in challenging hospital deals and contracting practices.

While these groups have targeted hospital prices because they’re a significant source of increased healthcare spending, these lawsuits do little to address the perverse underlying incentives that push hospitals to seek higher prices from commercial patients, to cross-subsidize what they view as insufficient pricing from public payers.

LHC, a postacute care behemoth with several hundred home health and hospice locations, as well as a dozen long-term care hospitals, would greatly expand Optum’s ability to provide home-based and long-term care. The FTC’s second request for information threatens to delay the deal, which was set to close in the latter half of this year.

The Gist: The LHC deal is the second UnitedHealth Group (UHG) transaction that antitrust regulators have targeted recently. The Department of Justice filed alawsuit earlier this year to block UHG’s acquisition of Change Healthcare, alleging that acquiring a direct competitor for claims solutions would reduce competition.

The FTC has historically focused its efforts on horizontal integration, but the LHC scrutiny, in combination with a recent inquiry into pharmacy benefit managers, indicates its focus may be expanding to vertical integration.

The Federal Reserve just raised interest rates by three-quarters of a percentage point, the biggest single increase in interest rates since 1994. It’s another move in the Fed’s effort to tackle the fastest inflation in four decades.

I understand the Fed’s urgency, but it has entered dangerous territory. If the Fed continues down this path – as it has signaled it will – the economy will be plunged into a recession. Every time over the last half century the Fed has raised interest rates this much and this quickly, it has caused a recession.

Besides, interest rate increases will not remedy the major causes of the current inflation – huge pent-up worldwide demand from two years of pandemic, shortages of goods and services responding to that demand, Putin’s war in Ukraine, and big profitable corporations with enough pricing power to use inflation as a cover for pushing up prices even further.

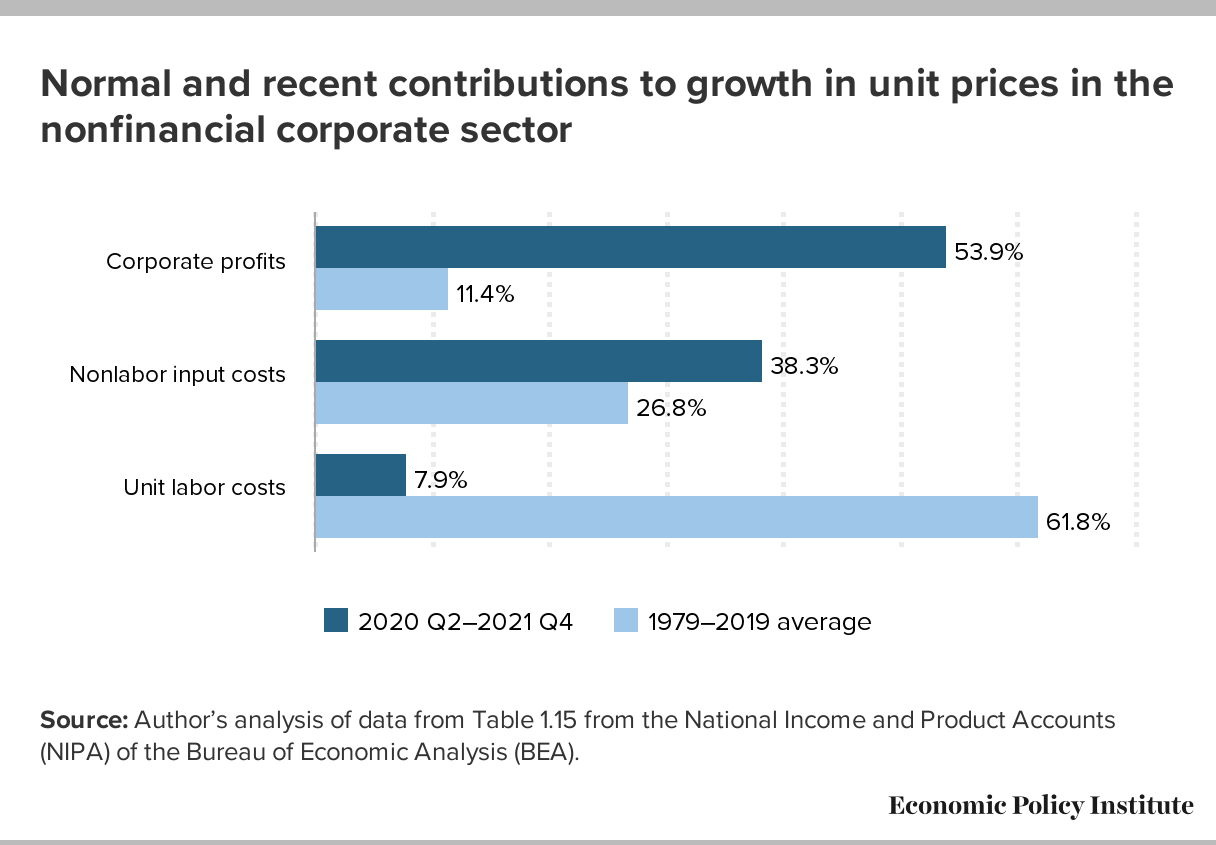

The Fed assumes that price increases are being driven by wage increases — so-called “wage-price inflation.” That’s incorrect. Wages are lagging behind inflation. A more accurate description of what we’re now seeing might be called “profit-price inflation” — prices driven upward by corporations seeking increased profits. (See chart below, from the Economic Policy Institute.)

A recession will be especially harmful to people who are most vulnerable to downturns in the economy — who are the first to be fired (and last to be hired again when the economy turns upward): lower-wage workers, disproportionately women and people of color.

RWJBarnabas Health on Tuesday called off its attempt to acquire St. Peter’s Healthcare System in New Brunswick, N.J., days after the Federal Trade Commission sued to block the proposed transaction.

This week’s contributor is Aditi Sen, the Director of Research and Policy at the Health Care Cost Institute. Her work uses HCCI’s unique data resources to conduct analyses that inform policy to promote a sustainable, accessible and high-value health care system.

High health care prices in the U.S. make it hard for people to access care, difficult for employers to provide insurance, and challenging for policymakers to balance health care spending with other budgetary priorities. That’s why it’s important to understand what drives prices higher and identify policies to keep prices from getting so high.

In a new paper in Health Affairs, Vilsa Curto, Anna Sinaiko and Meredith Rosenthal examined whether hospital and health systems’ acquisition of and contracting with physician practices – two forms of what is often called vertical integration – has led to higher prices for physician services. The researchers combined four sets of data from Massachusetts from 2013-2017 for their analysis.

They found that:

The percent of physicians who joined health systems grew meaningfully: The percent of primary care physicians who remained independent dropped from 42% in 2013 to 31.5% in 2017, and the percent of independent specialists fell from 26% to 17%.

Over this same period, prices for physician services rose. Price increases were especially large – 12% for primary care physicians and 6% for specialists – when physicians joined health systems that had a high share of admissions in their area.

This study stands out for several reasons. First, it shows vertical integration drives up health care prices. Second, the authors highlight actions states can and are considering taking to monitor and curb vertical integration, including antitrust enforcement and enacting laws to promote competition.

Finally, the Massachusetts data allow the public to better appreciate what’s happening across the state. Many earlier studies on health care consolidation have been limited to a subset of insurers, physicians or patients. Massachusetts is a leader when it comes to creating and sharing its data thanks to its all-payer claims database, which pulls together all the health care bills from private insurers and public programs like Medicare and Medicaid in the state. This critical information helps to illuminate patterns of care and prices and connect them to issues like consolidation and competition.Neither the federal government nor most states track how vertical integration mergers influence health care prices.

As these findings demonstrate, acquisitions and other forms of vertical integration impact what people pay for health care services. Given that prices in this sector continue to climb, this paper underscores the need for more state and national data to understand the downstream effects on all of us who use and participate in the U.S. health care system.