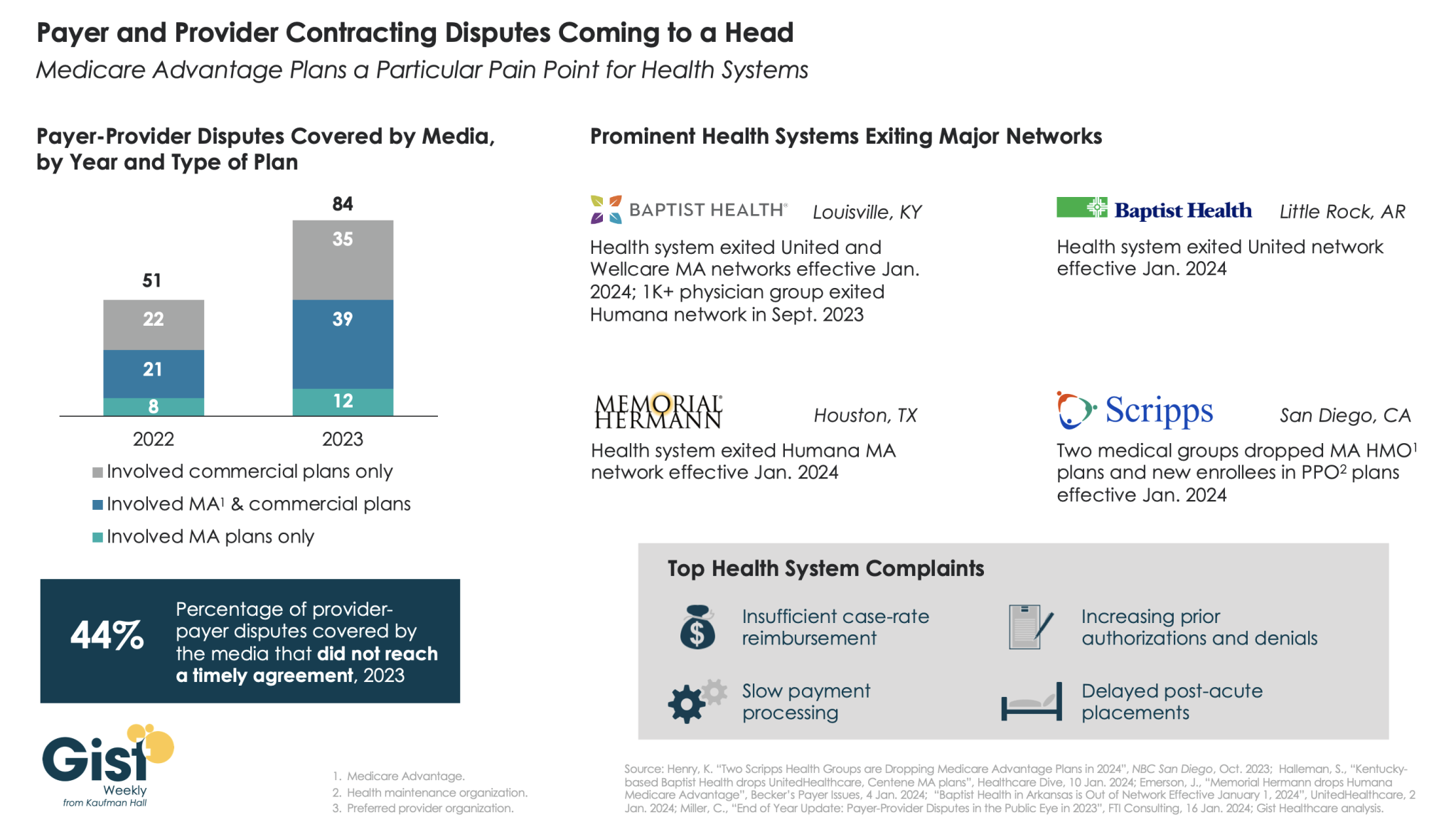

In this week’s graphic, we highlight new data on the increase in payer-provider contracting disputes covered by the media.

From 2022 to 2023, there was a 69 percent increase in the number of payer-provider contracting disputes that received media coverage. Nearly half of last year’s disputes did not reach agreement and resulted in network exits.

Large provider organizations—including Louisville, KY-based Baptist Health, Little Rock, AR-based Baptist Health, Houston, TX-based Memorial Hermann Health System, and two large medical groups affiliated with San Diego-based Scripps Health—dropped Medicare Advantage (MA) plans from at least one major payer, like United or Humana, as of Jan. 1, 2024.

Some dropped the payer’s commercial plans as well. Provider organizations leaving these networks have cited insufficient reimbursement rates and unsatisfactory business practices that drive up their cost of care delivery, especially around increased prior authorization requirements.

While contracting disputes will ultimately be influenced by the competitive strength of a given provider and payer in a particular market, it’s important for both sides to recognize thatthe patients in the middle of these disputes can be the ones most harmed when they can no longer see their trusted physicians.

On Wednesday, Bloomfield, CT-based Cigna announced a definitive agreement with Chicago, IL-based Health Care Service Corporation (HCSC), a large Blue Cross Blue Shield insurer, to sell its 600K-member MA business, as well as its Medicare prescription drug plan and Medigap offerings, for $3.3B.

The two insurers also agreed to a four-year services agreement where Cigna’s Evernorth Health Services subsidiary, which includes Express Scripts, will continue to provide pharmacy benefit services to the Medicare businesses.

While Cigna is exiting the MA market, other major payers—including UnitedHealth and Humana—are seeing their MA profits drop amid an increase in utilization, according to analysis from Moody’s Investors Service.

The Gist:While it initially appeared that Cigna’s divesture of its MA business would position it to combine more smoothly with Humana, this deal with HCSC makes sense even in the wake of that reportedly called off merger.

Cigna has been a bit player in MA for years, covering only two percent of MA lives in 2023, and the shrinking pie of MA profits will discourage all but the most successful or uniquely positioned payers.

But while increasing utilization rates are contributing to a declining outlook for payers, MA is still a solidly profitable business, covering over half of Medicare beneficiaries and still growing by millions of lives each year.

The MA payers that last are going to have to work harder at integrating their various care and data assets, and more carefully manage spend for an aging cohort of seniors with increasingly complex needs.

Baptist Health said reimbursements for the medications were determined by a payment model that was later invalidated, and the insurer continues to benefit from a “windfall” of underpayments due to the health system, according to the lawsuit.

The suit comes months after the CMS finalized a rule that aimed to fix years of illegal payment cuts in the 340B program. Hospitals had previously argued the solution didn’t consider how MA insurers would benefit financially from the remedy.

Dive Insight:

The 340B program requires pharmaceutical companies to give discounts — which can range from 25% to 50% of the medication’s cost — to providers who serve low-income communities.

The program aims to help safety-net providers better serve vulnerable groups, and it has grown significantly since 340B was created in 1992.

But in 2018, the CMS cut Medicare payments for certain drugs acquired under the 340B program, setting off a legal challenge that hospitals eventually won in front of the Supreme Court four years later.

To fix the underpayments, regulators decided to pay each hospital in 340B a lump sum that would total $9 billion overall. But the fix needed to be budget neutral, so the CMS would cut payments to all hospitals for non-drug items and services over 16 years.

In comments on the proposal, the American Hospital Association argued there was a “significant problem” with the plan, noting many MA insurers pay hospitals according to traditional Medicare rates.

Payers would benefit from reducing the non-drug payments to hospitals, and wouldn’t be required to repay 340B providers for the lower payments between 2018 and 2022, commenters argued on the rule, which was finalized in November.

In response, regulators said they appreciated the concerns, but that they were outside the scope of the rule and “CMS cannot interfere in the payment rates that MAOs [Medicare Advantage organizations] set in contracts with providers and facilities.”

In the Baptist lawsuit, the health system reported it contacted Humana multiple times about retroactive adjustments and remedy payments, but the insurer’s counsel disputed any obligation to make those payments.

“Humana’s refusal to act has worked a substantial windfall to Humana as it continues to hold funds provided by CMS for Humana’s Medicare Advantage plans without reimbursing Baptist Health for the amounts owed to it under the Agreement,” the system said in the lawsuit.

Humana said it does not comment on ongoing litigation.

Jayne Kleinman is bombarded with Medicare Advantage promotions every open enrollment period — even though she has no interest in leaving traditional Medicare, which allows seniors to choose their doctors and get the care they want without interference from multi-billion-dollar insurance companies.

“My biggest problem with being barraged is that so many of the ads were inaccurate,” Kleinman, a retired social services professional in New Haven County, Connecticut, told HEALTH CARE un-covered.

“They neglect to say that the amount of coverage you get is limited. They don’t talk about what you are losing by leaving traditional Medicare. It feels like insurance companies are manipulating us to get Medicare Advantage plans sold so that they can control the system, as opposed to treating us like human beings.”

Seniors face a torrent of Medicare Advantage advertising: an analysis by KFF found 9,500 daily TV ads during open enrollment in 2022. A recent survey by the Commonwealth Fund found that 30% of seniors received seven or more phone calls weekly from Medicare Advantage marketers during the most recent open enrollment (Oct. 15 to Dec. 7) for 2024 coverage.

In 2023, a critical milestone was passed: over half of seniors are now enrolled in privatized Medicare Advantage plans. The marketing for these plans nearly always fails to mention how hard it is to return to traditional Medicare once you are in Medicare Advantage, and that the MA plans have closed provider networks and require prior authorization for medical procedures. Instead, the marketing emphasizes the fringe benefits offered by Medicare Advantage plans like gym memberships.

U.S. Sen. Ron Wyden (D-Ore.), chairman of the Senate Finance Committee, criticized the widespread and predatory marketing of Medicare Advantage in a report in November 2022 and has continued to pressure the Biden administration to do more to address the problem.

The report said that consumer complaints about Medicare Advantage marketing more than doubled from 2020 to 2021 to 41,000. It cites cases such as that of an Oregon man whose switch to Medicare Advantage meant he could no longer afford his prescription drugs, as well as a 94-year-old woman with dementia in a rural area who bought a Medicare Advantage plan that required her to obtain care miles further from her residence than she had to travel before.

When open enrollment began last fall, it was “the start of a marketing barrage as marketing middlemen look to collect seniors’ information in order to bombard them with direct mail, emails, and phone calls to get them to enroll,” Wyden stated in a letter to the Centers for Medicare and Medicaid Services (CMS), which was signed by the other Democrats on the Senate Finance Committee.

Just three weeks after Wyden sent the letter, CMS released a proposed rule reforming Medicare Advantage practices that the main lobby group for Medicare Advantage plans, the Better Medicare Alliance, endorsed.

But key recommendations by Wyden were missing, including a ban on list acquisition by Medicare Advantage third-party marketing organizations, which includes brokers, and banning brokers that call beneficiaries multiple times a day for days in a row.

Among the prominent third-party marketing organizations is TogetherHealth, a subsidiary of Benefytt Technologies, which runs ads featuring former football star Joe Namath.

In August 2022, the Federal Trade Commission forced Benefytt to repay $100 million for fraudulent activities. The month before, the Securities and Exchange Commission levied more than $12 million in fines against Benefytt.

But CMS continues to allow Benefytt to work as a broker. Benefytt is owned by Madison Dearborn Partners, a Chicago-based private equity firm with ties to former Chicago mayor and current Ambassador to Japan Rahm Emanuel. Benefytt collects leads on potential customers, which they then sell to brokers and insurers to aggressively target seniors. CMS did not provide comment as to why they had not blocked Benefytt’s continuing work as a third-party marketing organization for Medicare.

Two different rounds of rule-making on Medicare Advantage marketing in 2023 instead focused on such reforms as reining in exaggerated claims and excessive broker compensation.

The enormous profits generated by Medicare Advantage plans — costing the federal government as much as $140 billion annually in overpayments to private companies — explains what drives the aggressive and often unethical marketing practices, said David Lipschutz, an associate director at the Center for Medicare Advocacy.

“The fact is, there is an increasingly imbalanced playing field between Medicare Advantage and traditional Medicare,” he said. “Medicare Advantage is being favored in many ways. Medicare Advantage plans are paid more than what traditional Medicare spends on a given beneficiary.

Those factors combined with the fact that they generate such profits for insurance companies, leads to those companies doing everything they can to maximize enrollment.”

Adding to the problem, Lipschutz argued, was the enormous influence of the health insurance industry in Washington. Health insurers spent more than $33 million lobbying Washington in just the first three quarters of 2023 alone.

“There is no real organized lobby for traditional Medicare, or organized advertising efforts,” he said. “During open enrollment, 80% of Medicare-related ads have to do with Medicare Advantage. We regularly encounter very well-educated and savvy folks who are tripped up by advertising and lured in by the bells and whistles. The deck is stacked against the consumer.”

Private equity firms have made a large investment in the Medicare Advantage brokerage and marketing sector, in addition to Madison Dearborn’s acquisition of Benefytt. Bain Capital, which Sen. Mitt Romney (R-Utah) co-founded, invested $150 million in Enhance Health, a Medicare Advantage broker, in 2021.

The CEO of EasyHealth, another private equity-backed brokerage, toldModern Healthcare in 2021 that “Insurance distribution is our Trojan horse into healthcare services.”

As federal law requires truth in advertising, a group of advocacy organizations–led by the Center for Medicare Advocacy, Disability Rights Connecticut, and the National Health Law Project–cited what they considered blatantly deceptive marketing by UnitedHealthcare to people who are eligible for both Medicare and Medicaid, in a complaint to CMS.

UnitedHealthcare had purchased ads in the Hartford Courant asking seniors in large bold-faced type: “Eligible for Medicare and Medicaid? You could get more with UnitedHealthcare.”

People who are eligible for both Medicare and Medicaid due to their income level are better off in traditional Medicare than Medicare Advantage given that Medicaid covers their out-of-pocket costs, meaning that they have wide latitude to choose their doctors, hospitals and medical procedures.

Sheldon Toubman, an attorney with Disability Rights Connecticut who worked to draft the complaint, framed the ad in the broader context of poor marketing practices by the Medicare Advantage industry.

“I have been aware for a long time of basically fraudulent advertising in the MA insurance industry,” Toubman told HEALTH CARE un-covered. “There’s an overriding misrepresentation — they tell you how great Medicare Advantage is, and never the downsides.

“There are two big downsides of going out of traditional Medicare:

They don’t tell you that you give up the broad Medicare provider network, which has nearly every doctor. And should you need expensive medical care in Medicare Advantage, you will learn there are prior authorization requirements. Traditional Medicare does almost no prior authorization, so you don’t have that obstacle. They don’t ever tell you any of that,” he said.

But it is marketing to dual-eligible individuals that is arguably the most problematic, Toubman argued. “They have Medicare and they are also low income. Because they are low-income, they also have Medicaid.

“Medicaid is a broader program — it covers a lot of things that Medicare doesn’t cover.

In Connecticut, 92,000 dual-eligible seniors have been ‘persuaded’ to sign up for Medicare Advantage. What’s outrageous about the marketing is they get you to sign up by offering extra services. … If you look at the ad in the Hartford Courant, it says you could get more, with the only real benefit being $130 per month toward food. But you now have this problem of a more limited provider network and prior authorization. UnitedHealth is doing false advertising.”

It’s a nationwide problem, Toubman said. “All insurers are doing this everywhere. We’re asking CMS and the Federal Trade Commission to conduct a nationwide investigation of this kind of problem. The failure to tell people that they give up their broader Medicare network — they don’t tell anybody that.”

For Jayne Kleinman, the unending ads are about one thing only: insurance industry profits. “Medicare Advantage has been strictly based on the people who make millions of dollars at the top of the company making more,” she said. “It’s all about money, not about you as an individual. Every time I saw an ad I’d get angry every single time — because I felt they were misleading people. The Medicare Advantage insurers are trying to scam people out of an interest of making money.”

In Sunday’s Axios’ AM, Mike Allen observed “Republicans know immigration alone could sink Biden. So, Trump and House Republicans will kill anything, even if it meets or exceeds their wishes. Biden knows immigration alone could sink him. So he’s willing to accept what he once considered unacceptable — to save himself.”

Mike called this a “truth Bomb” and he’s probably right: the polarizing issue of immigration is tantamount to a bomb falling on the political system forcing well-entrenched factions to re-think and alter their strategies.

In 2024, in U.S. healthcare, three truth bombs are in-bound. They’re the culmination of shifts in the U.S.’ economic, demographic, social and political environment and fueled by accelerants in social media and Big Data.

Truth bomb: The regulatory protections that have buoyed the industry’s growth are no longer secure.

Despite years of effectively lobbying for protections and money, the industry’s major trade groups face increasingly hostile audiences in city hall, state houses and the U.S. Congress.

The focus of these: the business practices that regulators think protect the status quo at the public’s expense. Example: while the U.S. House spent last week in their districts, Senate Committees held high profile hearings about Medicare Advantage marketing tactics (Finance Committee), consumer protections in assisted living (Special Committee on Aging), drug addiction and the opioid misuse (Banking) and drug pricing (HELP). In states, legislators are rationalizing budgets for Medicaid and public health against education, crime and cybersecurity and lifting scope of practice constraints that limit access.

Drug makers face challenges to patents (“march in rights”) and state-imposed price controls. The FTC and DOJ are challenging hospital consolidation they think potentially harmful to consumer choice and so. Regulators and lawmakers are less receptive to sector-specific wish lists and more supportive of populist-popular rules that advance transparency, disable business relationships that limit consumer choices and cede more control to individuals. Given that the industry is built on a business-to-business (B2B) chassis, preparing for a business to consumer (B2C) time bomb will be uncomfortable for most.

Truth bomb: Affordability in U.S. is not its priority.

The Patient Protection and Affordability Act 2010 advanced the notion that annual healthcare spending growth should not exceed more than 1% of the annual GDP. It also advanced the premise that spending should not exceed 9.5% of household adjusted gross income (AGI) and associated affordability with access to insurance coverage offering subsidies and Medicaid expansion incentives to achieve near-universal coverage. In 2024, that percentage is 8.39%.

Like many elements of the ACA, these constructs fell short: coverage became its focus; affordability secondary.

The ranks of the uninsured shrank to 9% even as annual aggregate spending increased more than 4%/year. But employers and privately insured individuals saw their costs increase at a double-digit pace: in the process, 41% of the U.S. population now have unpaid medical debt: 45% of these have income above $90,000 and 61% have health insurance coverage. As it turns out, having insurance is no panacea for affordability: premiums increase just as hospital, drug and other costs increase and many lower- and middle-income consumers opt for high-deductible plans that expose them to financial insecurity. While lowering spending through value-based purchasing and alternative payments have shown promise, medical inflation in the healthcare supply chain, unrestricted pricing in many sectors, the influx of private equity investing seeking profit maximization for their GPs, and dependence on high-deductible insurance coverage have negated affordability gains for consumers and increasingly employers. Benign neglect for affordability is seemingly hardwired in the system psyche, more aligned with soundbites than substance.

Truth bomb: The effectiveness of the system is overblown.

Numerous peer reviewed studies have quantified clinical and administrative flaws in the system. For instance, a recent peer reviewed analysis in the British Medical Journal concluded “An estimated 795 000 Americans become permanently disabled or die annually across care settings because dangerous diseases are misdiagnosed. Just 15 diseases account for about 50.7% of all serious harms, so the problem may be more tractable than previously imagined.”

The inadequacy of personnel and funding in primary and preventive health services is well-documented as the administrative burden of the system—almost 20% of its spending. Satisfaction is low. Outcomes are impressive for hard-to-diagnose and treat conditions but modest at best for routine care. It’s easier to talk about value than define and measure it in our system: that allows everyone to declare their value propositions without challenge.

Truth bombs are falling in U.S. healthcare. They’re well-documented and financed. They take no prisoners and exact mass casualties.

Most healthcare organizations default to comfortable defenses. That’s not enough. Cyberwarfare, precision-guided drones and dirty bombs require a modernized defense. Lacking that, the system will be a commoditized public utility for most in 15 years.

PS: Last week’s report, “The Holy War between Hospitals and Insurers…” (The Keckley Report – Paul Keckley) prompted understandable frustration from hospitals that believe insurers do not serve the public good at a level commensurate with the advantages they enjoy in the industry. However, justified, pushback by hospitals against insurers should be framed in the longer-term context of the role and scope of services each should play in the system long-term. There are good people in both sectors attempting to serve the public good. It’s not about bad people; it’s about a flawed system.

Last week, venture capital firm General Catalyst announced its plan to acquire Summa Health, an Akron, OH-based integrated delivery system with three hospitals, a large medical group, a health plan, and an annual revenue of around $2B. The terms of the deal were not disclosed, though General Catalyst previously indicated it aimed to spend $1-3B to acquire a health system.

Pending regulatory approval, Summa will convert to a for-profit entity and become a fully owned subsidiary of General Catalyst’s recently launched Health Assurance Transformation Corporation (HATCo).

HATCo, under the leadership of former Intermountain Health CEO Marc Harrison, was founded with the intention of acquiring a health system to serve as a blueprint for General Catalyst’s vision of healthcare transformation.

The Gist:While there’s a dearth of evidence for what kind of health system makes a good venture capital investment, Summa’s concentrated footprint of integrated delivery assets, robust Medicare Advantage plan, and position in an aging, yet competitive, market certainly seem attractive given HATCo’s stated goals.

If it closes, the partnership will provide Summa with an influx of capital and General Catalyst with a “proving ground” for both its vision of healthcare transformation and its portfolio of technology solutions. But while it’s one thing to get Summa’s board to sign on, General Catalyst will now have to reckon with other important stakeholders.

Summa’s physicians will be the gatekeepers of change at the local level, and their buy-in will be required for any continued push toward value-based care or successful product roll-out.

And, behind the scenes, General Catalyst will have to convince its investors that this longer-term play to rethink care delivery will offer financial returns worth the wait.

For many providers, 2023 provided a return to profitability (albeit at modest levels) following the devastating operating and investment losses experienced in 2022.Kaufman Hall’s National Hospital Flash Report data illustrated generally improving operating margins throughout the year, leveling off at 2.0% in November on a year-to-date basis.

This level of performance is commendable given 2022 and early 2023 margins, although it is still well below the 3% to 4% range which we believe is needed for long-term sustainability in the not-for-profit healthcare world. We may well have reached a point of stability with respect to operating performance, but at a lower level.

The question for hospital and health system leaders is whether this level of operating stability provides sustainability?

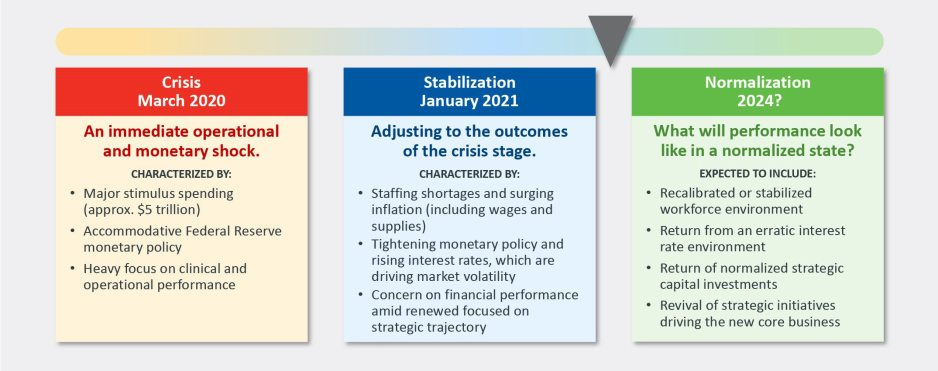

From stabilization to normalization

Since the pandemic began in 2020, the progress of recovery has been viewed over three phases: crisis, stabilization, and normalization. In last year’s outlook, we noted that we were in the midst of a potentially multi-year stabilization phase, which would continue to be marked with volatility—including ongoing labor market dislocations, inflationary pressures, and restrictive monetary policies. As we enter 2024, there are signs that we are now at the bridge between stabilization and normalization (Figure 1).

Figure 1: The Three Phases of Recovery from the Covid Pandemic

“The question for hospital and health system leaders is whether that level of stability provides sustainability?”

These signs include evidence that the first two indicators for normalization—a recalibrated or stabilized workforce environment and a return from an erratic interest rate environment—are coming into place. In our 2023 State of Healthcare Performance Improvement survey, respondents indicated that the spike in contract labor utilization that has been a dominant factor in operating expense increases was subsiding. Sixty percent of respondents said that utilization of contract labor was decreasing, and 36% said it was holding steady. Only 4% noted an increase in contract labor usage. Overall employee cost inflation seems to be subsiding as well: for all three labor categories in our survey (clinical, administrative, and support services), more organizations were able to hold salary increases to the 0% – 5% range in 2023 than in 2022.

There is good news on the interest rate front as well. After a series of rate increases in 2023, the Federal Reserve has held steady the last six months and has signaled rate cuts in 2024. Inflation has cooled markedly (albeit not yet at target levels), and employment rates have held steady. The Fed may have achieved a “soft landing” that satisfies its dual mandate of stable prices and maximum sustainable employment. Borrowing costs for not-for-profit hospital issuers have declined nearly 100 basis points in the last two months and we are expecting a return to more normal issuance levels in the first half of 2024.

There are other indications of normalization, including in the rating agencies’ outlooks for 2024. Regardless of the headline, all saw significant improvement in healthcare performance 2023.

The final answer to the question of whether the healthcare industry is entering the normalization phase likely will hinge on the last two indicators. Will we see a return of normalized strategic capital investments, and will we see a revival of strategic initiatives driving the core business (perhaps newly imagined)?

In effect, are health care systems simply surviving or are they thriving?

Looking forward, several factors could either bolster or undermine healthcare leaders’ confidence and willingness to resume a more normal level of investment in both capital needs and strategic growth. These include:

Politics and the 2024 elections. When North Carolina—a state that has traditionally leaned “red”—decided to opt into the Affordable Care Act’s (ACA’s) Medicaid expansion in 2023, it seemed that political debates over the ACA might be in the rearview mirror. But last November, former president Trump—currently the leading candidate for the Republican presidential nomination after strong wins in the Iowa caucuses and New Hampshire primary—indicated his intent to replace the ACA with something else. President Biden is now making protection and expansion of the ACA a key part of his 2024 campaign. What had appeared to be a settled issue may be a significant point of contention in the 2024 presidential election and beyond.

Although we do not anticipate any significant healthcare-related legislation in advance of the 2024 elections, healthcare leaders should be prepared for renewed attention to the costs of government-funded healthcare programs leading up to and following the elections. The national debt has increased rapidly over the past 20 years, tripling from $11 trillion in 2003 to $33 trillion in 2023. If the deficit and national debt become an important issue in the election, a move toward a balanced budget—akin to the Balanced Budget Act of 1997—post election could lead to further cuts to Medicare and Medicaid.

Temporary relief payments. Health systems continue to receive one-time cash infusions through the 340B settlement, Federal Emergency Management Agency (FEMA) payments and other governmental programs. Approximately 1,600 hospitals have or will be receiving a lump-sum payment to compensate them for a change in the Department of Health & Human Services’ (HHS’s) reimbursement rates for the 340B program from 2018 to 2022, which was ruled unlawful by the Supreme Court in a 2022 decision. The total amount to be distributed is approximately $9 billion and began hitting bank accounts in January 2024.

But what the right hand giveth, the left hand taketh away. Budget neutrality requirements will force HHS to recoup this offset—amounting to approximately $7.8 billion—which it will do by reducing payments for non-drug items and services to all Outpatient Prospective Payment System (OPPS) providers by 0.5% until the offset has been fully recouped, beginning in calendar year 2026. HHS estimates that this process will take approximately 16 years. Is this a harbinger of lower payments on other key governmental programs?

Many hospitals also continue to receive Covid-related payments from FEMA for expenses occurred during the pandemic. In addition, state supplemental payments—especially under Medicaid managed care and fee-for-service programs—are providing some relief. The Centers for Medicare & Medicaid Services has issued a proposed rule, however, that would limit states’ use of provider-based funding sources, such as provider taxes, and cap the rate of growth for state-directed payments.

As all of these payment programs dry up over the next few years, hospitals will need to replace the revenue and/or get leaner on the expense side in order to maintain today’s level of performance.

The hollowing of the commercial health insurance market. Our colleague, Joyjit Saha Choudhury, recently published a blog on the hollowing of the commercial health insurance market, driven by long-term concerns over the affordability of healthcare. While volumes have been recovering to pre-pandemic levels, this hollowing threatens the loss of the most profitable volumes and will pressure hospitals and health systems to create and deliver value, compete for inclusion in narrow networks, and develop more direct relationships with the employer community.

Related, the growing penetration of Medicare Advantage plans is reducing the number of traditional Medicare beneficiaries. Many CFOs report that these programs can be the most difficult with which to work given their high denial rates and required pre-authorization rates. A new rule requiring insurers to streamline prior authorizations for Medicare Advantage, Medicaid, and Affordable Care Act plans may help alleviate this issue; however, it will be incumbent upon management teams to stay ahead of them. Aging demographics are also reducing the percentage of commercially insured patients for many hospitals and health systems, further exacerbating the problem. This combination of fewer commercial patients (who often subsidize governmental patients) and more pressure on receiving the duly owed commercial revenue threatens to be an ongoing headache for management teams.

Ongoing impact of the Baby Boom generation. Despite the good news on inflation—and indications that the Fed may begin lowering interest rates in 2024—the economy is by no means out of the woods yet. The Baby Boom generation, which holds more than 50% of the wealth in the U.S. and is seemingly price agnostic, still has many years of spending ahead, in healthcare and general purchasing. This will likely continue to pressure inflation, especially in the healthcare sector, where demand will continue to grow. As the generation starts to shrink, the resulting wealth transfer will be the largest ever in our country’s history and have profound (and unforeseen) consequences on the overall economy and healthcare in general.

In sum, these other factors will continue to affect the sector (both positively and negatively) and require health system management teams to navigate an everchanging world. While many signs point toward short-term relief, the longer-term challenges persist. Improvements in the short term may, however, provide the opportunity to reposition organizations for the future.

How hospitals and health systems should respond

Healthcare leaders should view ongoing uncertainty in the political and economic climate as a tailwind as much as a headwind. This uncertainty, in other words, should be a motivation to put in place strategies that will buffer healthcare organizations from potential bumps in the road ahead. Setting balance sheet strategy should be a part of an organization’s planning process.

How an organization sets that strategy, measures its performance, and makes improvements will set apart top-performing organizations.

Although heightened debt issuance early in 2024 signals a return for many systems to a climate of investment, there is still limited energy around strategy and debt conversations in many boardrooms, especially in those organizations where financial improvement continues to lag. The last two years have illustrated that hospitals and health systems will not be able to cut their way to profitability. Lackluster performance cannot and will not improve without some level of strategic change, whether it is through market share gains, payer mix shift, or operational improvements. This strategic change requires investment and investment requires capital. Capital can be obtained in many forms—whether through growth in capital reserves, improved cash flow, or new debt issuance—but is essential for change. Reengaging in conversations about strategy and growth should be an imperative in 2024 and will require reexamining how that growth is funded.

Healthcare leaders should engage their partners as they continue or refocus on:

Changing the conversation from debt capacity to capital capacity. Management teams need to determine what they can afford to spend on capital if the new normal of cash flow will be constrained going forward. Capital capacity is and should be agnostic to the source of that capital, such as debt, cash flow from operations, or liquidity reserves. Healthcare leaders must focus on what they can spend, before deciding how to fund that spending. The conversation will need to balance investment for the future with maintaining key credit metrics in the short term.

Conducting a capitalization analysis. Separate but related to the previous entry, how much leverage should your organization have relative to its overall capitalization? Ostensibly, many organizations have been paying principal while curtailing borrowing needs, so capitalization may have improved. While that may be the case, many organizations have depleted reserves and/or experienced investment losses that have reduced capitalization. Understanding where the organization stands is an essential next step.

Evaluating surplus return. Consider surplus return as investment income net of interest expense. Organizations should evaluate their ability to reliably generate both operating cash flow and net surplus. How an organization’s balance sheet is positioned to generate returns and manage risk will be a critical success factor.

Focusing on the metrics that matter. These include operating cashflow margin, cash to debt, debt to revenue, and days cash on hand. As key metrics for rating analysts and investors continue to evolve, management teams need to make sure they are focused on the correct numbers. The discussion should be dually focused on ensuring adequate-to-ample headroom to basic financial covenants as well as a comparison to key medians and peers. Strong financial planning will address how these metrics can be improved over time through synergies, growth, and diversification strategies.

Although it has been a difficult few years, hospitals and health systems seem to have moved onto a more stable footing over the last twelve months. In order to build upon the upward trajectory, now is the time to harness strategy, planning, and investment to move organizations from stability to sustainability.

Asexpected, 2023 saw a material increase in downgrades over 2022 while the number of upgrades declined from the prior year. Volume showed favorable growth for many hospitals during 2023 although some indicators remained below pre-pandemic levels. Other hospitals reported a payer mix shift toward more Medicare as the population continued to age and Medicare Advantage plans gained momentum at the expense of commercial revenues. Continued labor challenges drove expense growth, even with many organizations reporting a reduction in temporary labor, as permanent hires pressured salary and benefit expenses. Some of the downgrades reflected pronounced operating challenges that led to covenant violations while others were due to a material increase in leverage viewed to be too high for the rating category.

Figure1: Downgrades at Moody’s, S&P, and Fitch

Here are five key takeaways:

The ratio of downgrades to upgrades reached a high level for all three rating agencies: Moody’s, 3.2-to-1; S&P: 3.8-to-1; and Fitch: 3.5-to-1. In 2022, the ratio crested just above 2.0-to-1 at the highest among the three firms.

Downgrades covered a wide swath of hospitals, ranging from single-site general acute care facilities to academic medical centers as well as large regional and multistate systems. Many of the hospital downgrades were concentrated in New York, Pennsylvania, Ohio, and Washington. All rating categories saw downgrades, although the majority were clustered in the Baa/BBB and lower categories.

Multi-notch downgrades were mainly relegated to ratings that were already deep into speculative grade. Multi-notch upgrades were due to mergers or acquisitions where the debt was guaranteed by or added to the legal borrowing group of the higher rated system.

Upgrades reflected fundamental improvement in financial performance and debt service coverage along with strengthening balance sheet indicators. Like the downgraded organizations, upgraded hospitals and health systems ranged from single-site hospitals to expansive, super-regional systems. Some of the upgrades reflected mergers into higher-rated systems.

The wide span between downgrades to upgrades in 2023 would suggest that the credit gap between highly rated hospitals (say, the “A” or “Aa/AA” category) compared to “Baa/BBB” and speculative grade is widening. That said, given that rating affirmations remain the predominant rating activity annually, the rating agencies reported only a subtle shift in the overall distribution of ratings since the beginning of the pandemic in their panel discussion at Kaufman Hall’s October 2023 Healthcare Leadership Conference.

One person’s prediction for 2024?

It’s a safe bet that downgrades will outpace upgrades given the persistent challenges, although the ratio may narrow if the improvement in current performanceholds. That said, the rating agencies are maintaining mixed views for 2024. S&P and Fitch are sticking with negative and deteriorating outlooks, respectively, while Moody’s has revised its outlook to stable, anticipating that the rough times of 2022 are behind us.

All three rating agencies predict that we are not out of the woods yet when it comes to covenant challenges, especially in the lower rating categories or for those organizations that report a second year of covenant violations.

Earlier this month, leaders from more than 400 organizations descended on San Francisco for J.P. Morgan‘s 42nd annual healthcare conference to discuss some of the biggest issues in healthcare today. Here’s how Advisory Board experts are thinking about Modern Healthcare’s 10 biggest takeaways — and our top resources for each insight.

How we’re thinking about the top 10 takeaways from JPM’s annual healthcare conference

Following the conference, Modern Healthcare provided a breakdown of the top-of-mind issues attendees discussed.

Here’s how our experts are thinking about the top 10 takeaways from the conference — and the resources they recommend for each insight.

1. Ambulatory care provides a growth opportunity for some health systems

By Elizabeth Orr, Vidal Seegobin, and Paul Trigonoplos

At the conference, many health system leaders said they are evaluating growth opportunities for outpatient services.

However, results from our Strategic Planner’s Survey suggest only the biggest systems are investing in building new ambulatory facilities. That data, alongside the high cost of borrowing and the trifurcation of credit that Fitch is predicting, suggests that only a select group of health systems are currently poised to leverage ambulatory care as a growth opportunity.

Systems with limited capital will be well served by considering other ways to reach patients outside the hospital through virtual care, a better digital front door, and partnerships. The efficiency of outpatient operations and how they connect through the care continuum will affect the ROI on ambulatory investments. Buying or building ambulatory facilities does not guarantee dramatic revenue growth, and gaining ambulatory market share does not always yield improved margins.

While physician groups, together with management service organizations, are very good at optimizing care environments to generate margins (and thereby profit), most health systems use ambulatory surgery center development as a defensive market share tactic to keep patients within their system.

This approach leaves margins on the table and doesn’t solve the growth problem in the long term. Each of these ambulatory investments would do well to be evaluated on both their individual profitability and share of wallet.

On January 24 and 25, Advisory Board will convene experts from across the healthcare ecosystem to inventory the predominant growth strategies pursued by major players, explore considerations for specialty care and ambulatory network development, understand volume and site-of-care shifts, and more. Register here to join us for the Redefining Growth Virtual Summit.

Also, check out our resources to help you plan for shifts in patient utilization:

2. Rebounding patient volumes further strain capacity

By Jordan Peterson, Eliza Dailey, and Allyson Paiewonsky

Many health system leaders noted that both inpatient and outpatient volumes have surpassed pre-pandemic levels, placing further strain on workforces.

The rebound in patient volumes, coupled with an overstretched workforce, underscores the need to invest in technology to extend clinician reach, while at the same time doubling down on operational efficiency to help with things like patient access and scheduling.

For leaders looking to leverage technology and boost operational efficiency, we have a number of resources that can help:

3. Health systems aren’t specific on AI strategies

By Paul Trigonoplos and John League

According to Modern Healthcare, nearly all health systems discussed artificial intelligence (AI) at the conference, but few offered detailed implementation plans and expectations.

Over the past year, a big part of the work for Advisory Board’s digital health and health systems research teams has been to help members reframe the fear of missing out (FOMO) that many care delivery organizations have about AI.

We think AI can and will solve problems in healthcare. Every organization should at least be observing AI innovations. But we don’t believe that “the lack of detail on healthcare AI applications may signal that health systems aren’t ready to embrace the relatively untested and unregulated technology,” as Modern Healthcare reported.

The real challenge for many care delivery organizations is dealing with the pace of change — not readiness to embrace or accept it. They aren’t used to having to react to anything as fast-moving as AI’s recent evolution. If their focus for now is on low-hanging fruit, that’s completely understandable. It’s also much more important for these organizations to spend time now linking AI to their strategic goals and building out their governance structures than it is to be first in line with new applications.

Check out our top resources for health systems working to implement AI:

Digital health companies like Teladoc, R1 RCM, Veradigm, and Talkspace all spoke out about their use of generative AI.

This does not surprise us at all. In fact, we would be more surprised if digital health companies were not touting their AI capabilities. Generative AI’s flexibility and ease of use make it an accessible addition to nearly any technology solution.

However, that alone does not necessarily make the solution more valuable or useful. In fact, many organizations would do well to consider how they want to apply new AI solutions and compare those solutions to the ones that they would have used in October 2022 — before ChatGPT’s newest incarnation was unveiled. It may be that other forms of AI, predictive analytics, or robotic process automation are as effective at a better cost.

Again, we believe that AI can and will solve problems in healthcare. We just don’t think it will solve every problem in healthcare, or that every solution benefits from its inclusion.

During the conference, providers criticized insurers for the rate of denials, Modern Healthcare reports.

Denials — along with other utilization management techniques like prior authorization — continue to build tension between payers and providers, with payers emphasizing their importance for ensuring cost effective, appropriate care and providers overwhelmed by both the administrative burden and the impact of denials on their finances.

Many health plans have announced major moves to reduce prior authorizations and CMS recently announced plans to move forward with regulations to streamline the prior authorization process. However, these efforts haven’t significantly impacted providers yet.

In fact, most providers report no decrease in denials or overall administrative burden. A new report found that claims denials increased by 11.99% in the first three quarters of 2023, following similar double digit increases in 2021 and 2022.

Our team is actively researching the root cause of this discrepancy and reasons for the noted increase in denials. Stay tuned for more on improving denials performance — and the broader payer-provider relationship — in upcoming 2024 Advisory Board research.

For now, check out this case study to see how Baptist Health achieved a 0.65% denial write-off rate.

6. Insurers are prioritizing Star Ratings and risk adjustment changes

By Mallory Kirby

Various insurers and providers spoke about “the fallout from star ratings and risk adjustment changes.”

2023 presented organizations focused on MA with significant headwinds. While many insurers prioritized MA growth in recent years, leaders have increased their emphasis on quality and operational excellence to ensure financial sustainability.

With an eye on these headwinds, it makes sense that insurers are upping their game to manage Star Ratings and risk adjustment. While MA growth felt like the priority in years past, this focus on operational excellence to ensure financial sustainability has become a priority.

We’ve already seen litigation from health plans contesting the regulatory changes that impact the bottom line for many MA plans. But with more changes on the horizon — including the introduction of the Health Equity Index as a reward factor for Stars and phasing in of the new Risk Adjustment Data Validation model — plans must prioritize long-term sustainability.

Check out our latest MA research for strategies on MA coding accuracy and Star Ratings:

Pharmacy benefit manager (PBM) leaders discussed the ways they are preparing for potential congressional action, including “updating their pricing models and diversifying their revenue streams.”

Healthcare leaders should be prepared for Congress to move forward with PBM regulation in 2024. A final bill will likely include federal reporting requirements, spread pricing bans, and preferred pricing restrictions for PBMs with their own specialty pharmacy. In the short term, these regulations will likely apply to Medicare and Medicaid population benefits only, and not the commercial market.

Congress isn’t the only entity calling for change. Several states passed bills in the last year targeting PBM transparency and pricing structures. The Federal Trade Commission‘s ongoing investigation into select PBMs looks at some of the same practices Congress aims to regulate. PBM commercial clients are also applying pressure. In 2023, Blue Cross Blue Shield of California‘s (BSC) decided to outsource tasks historically performed by their PBM partner. A statement from BSC indicated the change was in part due to a desire for less complexity and more transparency.

Here’s what this means for PBMs:

Transparency is a must

The level of scrutiny on transparency will force the hand of PBMs. They will have to comply with federal and state policy change and likely give something to their commercial partners to stay competitive. We’re already seeing this unfold across some of the largest PBMs. Recently, CVS Caremarkand Express Scripts launched transparent reimbursement and pricing models for participating in-network pharmacies and plan sponsors.

While transparency requirements will be a headache for larger PBMs, they might be a real threat to smaller companies. Some small PBMs highlight transparency as their main value add. As the larger PBMs focus more on transparency, smaller PBMs who rely on transparent offerings to differentiate themselves in a crowded market may lose their main competitive edge.

PBMs will have to try new strategies to boost revenue

PBM practice of guiding prescriptions to their own specialty pharmacy or those providing more competitive pricing is a key strategy for revenue. Stricter regulations on spread pricing and patient steerage will prompt PBMs to look for additional revenue levers.

PBMs are already getting started — with Express Scripts reporting they will cut reimbursement for wholesale brand name drugs by about 10% in 2024. Other PBMs are trying to diversify their business opportunities. For example, CVS Caremark’s has offered a new TrueCost model to their clients for an additional fee. The model determines drug prices based on the net cost of drugs and clearly defined fee structures. We’re also watching growing interest in cross-benefitutilization management programs for specialty drugs. These offerings look across both medical and pharmacy benefits to ensure that the most cost-effective drug is prescribed for patients.

At the conference, retailers such as CVS, Walgreens, and Amazon doubled down on their healthcare services strategies.

Typically, disruptors do not get into care delivery because they think it will be easy. Disruptors get into care delivery because they look at what is currently available and it looks so hard — hard to access, hard to understand, and hard to pay for.

Many established players still view so-called disruptors as problematic, but we believe that most tech companies that move into healthcare are doing what they usually do — they look at incumbent approaches that make it hard for customers and stakeholders to access, understand, and pay for care, and see opportunities to use technology and innovative business models in an attempt to target these pain points.

CVS, Walgreens, and Amazon are pursuing strategies that are intended to make it more convenient for specific populations to get care. If those efforts aren’t clearly profitable, that does not mean that they will fail or that they won’t pressure legacy players to make changes to their own strategies. Other organizations don’t have to copy these disruptors (which is good because most can’t), but they must acknowledge why patient-consumers are attracted to these offerings.

For more information on how disruptors are impacting healthcare, check out these resources:

9. Financial pressures remain for many health systems

By Vidal Seegobin and Marisa Nives

Health systems are recovering from the worst financial year in recent history. While most large health systems presenting at the conference saw their finances improve in 2023, labor challenges and reimbursement pressures remain.

We would be remiss to say that hospitals aren’t working hard to improve their finances. In fact, operating margins in November 2023 broke 2%. But margins below 3% remain a challenge for long-term financial sustainability.

One of the more concerning trends is that margin growth is not tracking with a large rebound in volumes. There are number of culprits: elevated cost structures, increased patient complexity, and a reimbursement structure shifting towards government payers.

For many systems, this means they need to return to mastering the basics: Managing costs, workforce retention, and improving quality of care. While these efforts will help bridge the margin gap, the decoupling of volumes and margins means that growth for health systems can’t center on simply getting bigger to expand volumes.

Maximizing efficiency, improving access, and bending the cost curve will be the main pillars for growth and sustainability in 2024.

To learn more about what health system strategists are prioritizing in 2024, read our recent survey findings.

Also, check out our resources on external partnerships and cost-saving strategies:

During the conference, MA insurers reported seeing a spike in utilization driven by increased doctor’s visits and elective surgeries.

These increased medical expenses are putting more pressure on MA insurers’ margins, which are already facing headwinds due to CMS changes in MA risk-adjustment and Star Ratings calculations.

However, this increased utilization isn’t all bad news for insurers. Part of the increased utilization among seniors can be attributed to more preventive care, such as an uptick in RSV vaccinations.

In UnitedHealth Group‘s* Q4 earnings call, CFO John Rex noted that, “Interest in getting the shot, especially among the senior population, got some people into the doctor’s office when they hadn’t visited in a while,” which led to primary care physicians addressing other care needs. As seniors are referred to specialty care to address these needs, plans need to have strategies in place to better manage their specialist spend.

The new year dawned on a health insurance industry beset by challenges.

Only 7% of health plan executives view 2024 positively after being hammered by the coronavirus pandemic, regulatory turbulence and rising cost pressures, according to a Deloitte survey.

Costs are spiking, and health insurers remain uncertain how the lingering effects of COVID-19 will impact care utilization. Medicaid redeterminations are rewriting the coverage landscape state by state, while Medicare Advantage — the darling of payers’ business sheets — experiences significant regulatory upheaval.

Meanwhile, 2024 is a presidential election year. That’s adding more political uncertainty into the picture as Washington hammers payers over claims denials and the business practices of pharmacy benefit units.

Here’s what experts see coming down the pike for health insurers this year.

The uninsured rate will go up

The number of Americans without insurance coverage is almost certainly going to rise this year as states overhaul their Medicaid rolls, experts say.

During the pandemic, continuous enrollment protections led a record number of people to enroll in Medicaid. But earlier this year, states resumed checking eligibility for the safety-net program. Around 14.4 million Americans have been removed from Medicaid due to the redeterminations process, many for administrative reasons like incorrect paperwork despite remaining eligible.

“We are going to see an increase in the uninsured rate for children and probably adults as well as a consequence,” said Joan Alker, executive director of the Georgetown University Center for Children and Families.

The question is how big of an increase, experts said. Redeterminations began in April, but lagging information and state differences in data reporting has made it difficult to determine where individuals are turning for coverage, and in what numbers.

Early signs suggest some people losing Medicaid have found plans in the Affordable Care Act exchanges, though it’s probably “a very small percentage,” Alker said. More than 20 million people have signed up for ACA coverage since open enrollment began in November — an all-time high, according to data released by the Biden administration in early January.

Experts say the growth is due in part to redeterminations, along with the effects of more generous federal subsidies. Those subsidies are slated to expire in 2025, meaning ACA enrollment should stay elevated until then.

But it’s unlikely everyone who loses Medicaid will find a home on the marketplaces. The cost of family coverage without an employer remains out of reach for many Americans. It’s also too early to determine how many people terminated from Medicaid have shifted into employer coverage — that data should also emerge as 2024 continues, said Matt Fiedler, a senior fellow with the Brookings Schaeffer Initiative on Health Policy.

Federal regulators have also taken a number of actions to try and curb improper procedural Medicaid losses, like cracking down on states with high levels of child disenrollments. Yet, procedural terminations are unlikely to improve significantly this year, experts said.

“We do see a very hopeful trend” in some states, like Washington and Oregon, embracing longer periods of continuous eligibility, Alker noted.

The government has ramped up ACA marketplace outreach, which — along with macro forces like a strong labor market — are positive signs that individuals no longer eligible for Medicaid may find alternative coverage, whether in the ACA exchanges or through employment.

But “it’s likely we’ll see an increase in the uninsured rate. I think the question is how much,” Fiedler said.

Increasing vigilance around costs

Healthcare costs are projected to grow much faster in 2024 than the historical average, fueled by inflation, supply chain disruption and labor pressures increasing provider wages. Those costs are burdening employers already stressed by worker mental health and deferred preventive screenings that could worsen health conditions down the line.

As a result, employers are investing heavily in mental health and substance use disorder services. Seven out of ten employers say mental healthcare access is a priority in 2024, and employers say they’ll turn to virtual care providers to address the need, according to a Business Group on Health survey.

As a result, employers are increasingly demanding integrated platforms combining different benefits, continuing a pivot away from the point solutions they were deluged with during the pandemic. Payers are racing to meet that need.

This year, UnitedHealthcare plans to integrate more than 20 standalone products into a “supported benefits platform,” said Dan Kueter, CEO of the payer’s employer and individual business, during an investor day in November.

Cigna, which focuses on employer-sponsored plans, plans to add more services to its behavioral health navigator to help employers personalize the platform for their employees this year, said CEO David Cordani during a November earnings call.

For their part, health insurers are likely to raise premiums and combat hospital reimbursement hikes in 2024 to control costs, according to credit rating agency Fitch Ratings.

However, that outlook is complicated by uncertainty around how much elevated care utilization seen in 2023 will continue. Some payers, like UnitedHealth and Humana, are forecasting high utilization, while others like CVS have said they expect it to drop.

More payers might pursue mergers and acquisitions or build out internal musculoskeletal management programs to control costs, said Prateesh Maheshwari, a managing director at venture capital firm Maverick Ventures. Hip and knee surgeries were an oft-cited driver of utilization last year.

Still, publicly traded health insurance companies could see their margins moderately decrease in 2024, Fitch said.

GLP-1 coverage will increase — slowly

Surging demand for GLP-1s means insurance coverage for the drugs is expected to increase next year, putting more stress on the nation’s pressured healthcare payment system. GLP-1s, or glucagon-like peptide-1 drugs, have historically been used to treat diabetes but have shown efficacy in weight loss.

The drugs are exceedingly expensive, butthat hasn’t stopped peoplefrom trying to get theirhands on GLP-1s — off-label or not. TD Cowen predicts GLP-1 sales could reach $102 billion by 2030, with $41 billion of that for obesity.

More private payers are considering covering the drugs next year, though the doors to coverage aren’t being thrown wide open. According to a November survey by the International Foundation of Employee Benefit Plans, while 76% of employers provide GLP-1 drug coverage for diabetes, just 27% provide coverage for weight loss.

Yet, 13% are considering adding coverage for weight loss.

As insurance coverage increases, payers will ensure only eligible patients are accessing the drugs through checks like step therapy, said Nathan Ray, head of healthcare M&A at consultancy West Monroe. As a result, access could remain restricted.

Payers will also tie coverage for GLP-1s to additional behavioral management programs. That trend has proved a gold rush for chronic condition management companies and telehealth providers, which have rushed to stand up new business lines for weight loss that include GLP-1s.

“Things like this, that include the opportunity for medication along with the accompaniment of behavioral change, is where I think the market will go in 2024,” said Heather Dlugolenski, Cigna’s U.S. commercial strategy officer.

Proponents of weight loss medication are also eyeing a potential overturn of the ban on Medicare coverage of weight loss drugs next year. A growing number of lawmakers (and drugmakers standing to profit from Medicare coverage) have come out in support of a bill introduced in 2023 to allow Medicare to cover anti-obesity drugs.

The bill is unlikely to be prioritized given Washington has a lot on its plate during the election year, but passage isn’t out of the realm of possibility, experts said.

Medicare Advantage will continue to grow under Washington’s watchful eye

In MA, the government contracts with private insurers to manage the care of Medicare seniors. MA has become increasingly popular, swelling to cover 31 million people last year — a boon for insurers offering the coverage, which can be twice as profitable for private payers than other types of plans.

As such, MA plans have been advertising heavily, trumpeting their supplemental benefits like gym memberships or subsidized groceries. Seniors find those benefits attractive, Brookings’ Fiedler said, and may not understand that MA plans may not cover as much medical care as traditional Medicare.

”My best bet would be MA enrollment in the near term continues to grow,” Fiedler said. “I don’t think we’re at the ceiling yet.”

Despite elevated costs in 2023 from seniors using more medical care, insurers generally didn’t cut back on plan benefits this year as they continue to compete for members.

Yet, the program hasn’t been without its complications. Payers cried foul last year over tweaks to MA rates, star ratings and reimbursement audits, with Humana and Elevance suing to stop the changes.

MA “should remain a key long-term growth driver for managed care, but we see a more challenging setup in 2024 as weaker funding, risk coding changes, and lower Star ratings combine to pressure margins,” J.P. Morgan analysts wrote in an outlook report published late last year.

Insurers were also plagued in 2023 by congressional hearings and lawsuits over their claims reviews processes, sparking criticism that seniors may not be receiving the care they’re due.

Scrutiny from Washington around such practices is likely to continue.

“We are seeing both in the Senate and House a lot of interest in peeling back the layers of the onion of how big health plans are operating their Medicare Advantage programs. That’s going to continue to be an issue,” said Reed Stephens, a healthcare chair at law firm Winston & Strawn who focuses on risk.

Though it’s unlikely that legislation will be passed reforming MA, Reed said. Overall, regulatory and political turbulence should subside somewhat this year.

The rate and marketing changes were “short of the last train out of the station,” said Brookings’ Fiedler. “The administration is unlikely to want a big fight with MA plans in an election year.”

The Mark Cuban effect: Payers with PBMs will launch more ‘transparent’ options

Major pharmacy benefit managers will introduce more options billed as transparent and cost-effective to retain clients after some turned to upstart competitors last year.

PBM clients are clamoring for outcomes-based pricing, with structures tying PBM compensation to measures like adherence, according to a J.P. Morgan survey from late 2023. Clients also want transparency, whether more data sharing or full administration models.

The changes aren’t revolutionary, but they hint at ongoing distrust of major PBMs from benefits teams, J.P. Morgan said.

UnitedHealth’s Optum Rx, Cigna’s Express Scripts and CVS Caremark — which together control 80% of prescriptions in the U.S. — have all recently launched new programs, partnerships or models they say are more affordable and transparent to meet the demand.

The industry is likely to see more moves along those lines in 2024, experts say — especially as Congress considers legislation to reform PBMs. The Lower Costs, More Transparency Act passed the House in December. The bill is seen as unlikely to clear the Senate, but specific measures, like forced PBM transparency, could make it into larger legislative packages.

The passing of measures around transparency could satisfy politicians’ need for a win when it comes to drug pricing without creating meaningful reform in the sector, according to Jefferies analyst Brian Tanquilut.

Yet, momentum to do something about high drug costs will certainly carry into this year. Presidential candidates on both sides of the aisle are expected to wield the issue on the campaign trail.

“The companies in those markets are going to have to stay nimble and keep on their toes,” said Winston & Strawn’s Stephens.

M&A, especially vertical integration, carries on

Companies like UnitedHealth, CVS and Humana will continue building out networks of physical care sites in 2024. New M&A guidelines from the Department of Justice and Federal Trade Commission could raise the bar for merger approvals, but the value proposition for insurers to acquire healthcare providers is too high for them to be dissuaded, experts said.

Payers will continue to pursue as many deals “as they can find willing, available targets,” said West Monroe’s Ray.

By directing members to owned locations for medical needs, health insurers can essentially pay themselves for providing a service, keeping more revenue in-house. As a result, payers — especially those with a large presence in MA, which incentivizes organizations to better manage cost — will stay on the hunt for acquisition targets.

While healthcare M&A was relatively slow in 2023, 68% of senior leaders in the sector expect deal volume to rise in 2024, according to a survey by investment bank Jefferies.

Optum — which employs or is affiliated with around one-tenth of all doctors in the U.S. — is already eyeing M&A. The health services arm of UnitedHealth is currently pursuing an acquisition of a physician-owned clinic chain in Oregon, even as it comes off a number of big provider buys in 2023, including the multi-billion-dollar acquisitions of home health providers Amedisys and LHC Group.

Cigna has also said it plans to look for smaller strategic acquisitions to grow its business, after a potential merger with rival Humana crumbled late last year.