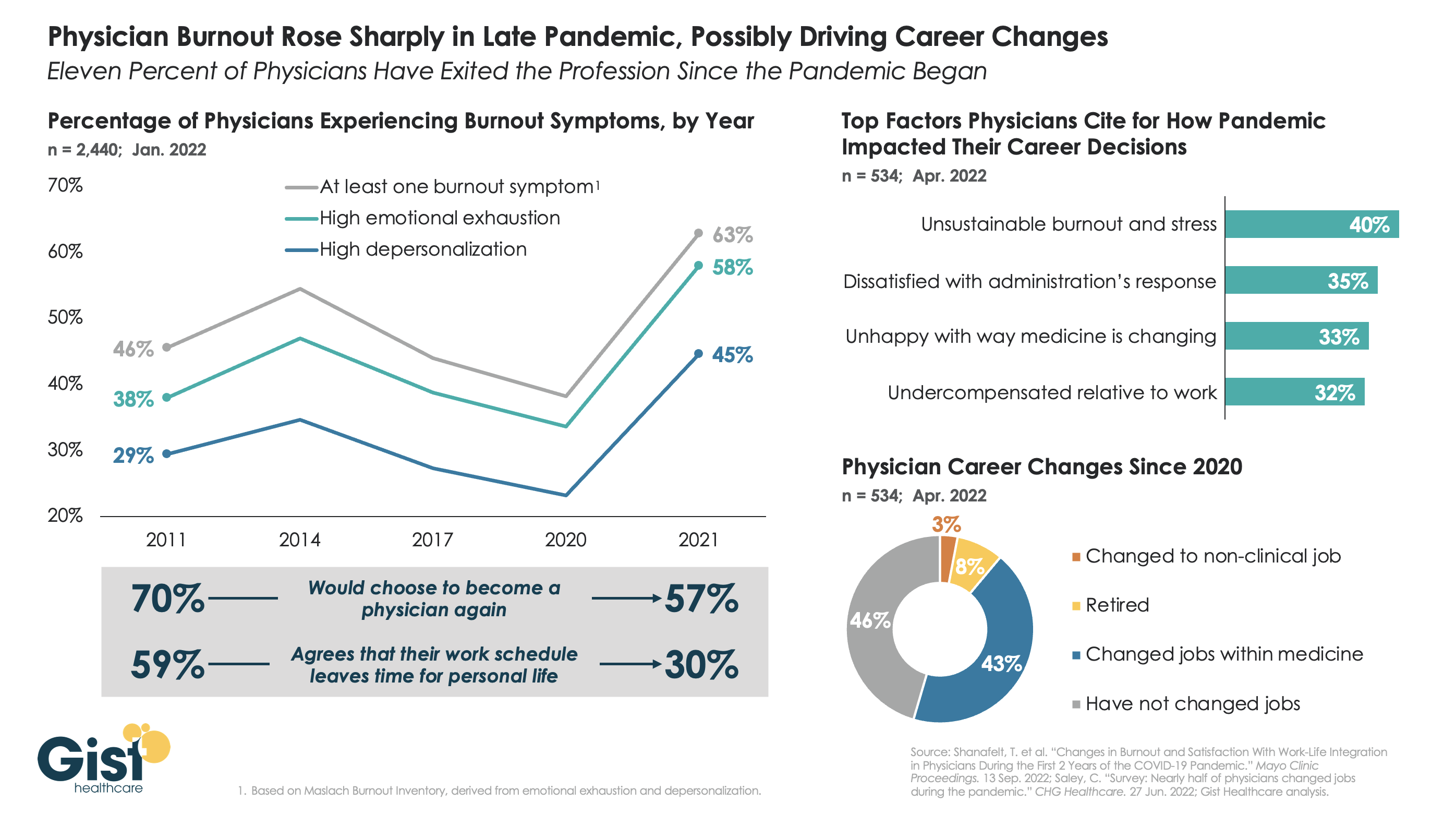

Three critical healthcare struggles will define the year to come with cutthroat competition and intense disputes being played out in public:

1. A Nation Divided Over Abortion Rights

2. The Generative AI Revolution In Medicine

3. The Tug-Of-War Over Healthcare Pricing American healthcare, much like any battlefield, is fraught with conflict and turmoil. As we navigate 2024, the wars ahead seem destined to intensify before any semblance of peace can be attained. Let me know your thoughts once you read mine.

Modern medicine, for most of its history, has operated within a collegial environment—an industry of civility where physicians, hospitals, pharmaceutical companies and others stayed in their lanes and out of each other’s business.

It used to be that clinicians made patient-centric decisions, drugmakers and hospitals calculated care/treatment costs and added a modest profit, while insurers set rates based on those figures. Businesses and the government, hoping to save a little money, negotiated coverage rates but not at the expense of a favored doctor or hospital. Disputes, if any, were resolved quietly and behind the scenes.

Times have changed as healthcare has taken a 180-degree turn. This year will be characterized by cutthroat competition and intense disputes played out in public. And as the once harmonious world of healthcare braces for battle, three critical struggles take centerstage. Each one promises controversy and profound implications for the future of medicine:

1. A Nation Divided Over Abortion Rights

For nearly 50 years, from the landmark Roe v. Wade decision in 1973 to its overruling by the 2022 Dobbs case, abortion decisions were the province of women and their doctors. This dynamic has changed in nearly half the states.

This spring, the Supreme Court is set to hear another pivotal case, this one on mifepristone, an important drug for medical abortions. The ruling, expected in June, will significantly impact women’s rights and federal regulatory bodies like the FDA.

Traditionally, abortions were surgical procedures. Today, over half of all terminations are medically induced, primarily using a two-drug combination, including mifepristone. Since its approval in 2000, mifepristone has been prescribed to over 5 million women, and it boasts an excellent safety record. But anti-abortion groups, now challenging this method, have proposed stringent legal restrictions: reducing the administration window from 10 to seven weeks post-conception, banning distribution of the drug by mail, and mandating three in-person doctor visits, a burdensome requirement for many. While physicians could still prescribe misoprostol, the second drug in the regimen, its effectiveness alone pales in comparison to the two-drug combo.

Should the Supreme Court overrule and overturn the FDA’s clinical expertise on these matters, abortion activists fear the floodgates will open, inviting new challenges against other established medications like birth control.

In response, several states have fortified abortion rights through ballot initiatives, a trend expected to gain momentum in the November elections. This legislative action underscores a significant public-opinion divide from the Supreme Court’s stance. In fact, a survey published in Nature Human Behavior reveals that 60% of Americans support legal abortion.

Path to resolution: Uncertain. Traditionally, SCOTUS rulings have mirrored public opinion on key social issues, but its deviation on abortion rights has failed to shift public sentiment, setting the stage for an even fiercer clash in years to come. A Supreme Court ruling that renders abortion unconstitutional would contradict the principles outlined in the Dobbs decision, but not all states will enact protective measures. As a result, America’s divide on abortion rights is poised to deepen.

2. The Generative AI Revolution In Medicine

A year after ChatGPT’s release, an arms race in generative AI is reshaping industries from finance to healthcare. Organizations are investing billions to get a technological leg up on the competition, but this budding revolution has sparked widespread concern.

In Hollywood, screenwriters recently emerged victorious from a 150-day strike, partially focused on the threat of AI as a replacement for human workers. In the media realm, prominent organizations like The New York Times, along with a bevy of celebs and influencers, have initiated copyright infringement lawsuits against OpenAI, the developer of ChatGPT.

The healthcare sector faces its own unique battles. Insurers are leveraging AI to speed up and intensify claim denials, prompting providers to counter with AI-assisted appeals.

But beyond corporate skirmishes, the most profound conflict involves the doctor-patient relationship. Physicians, already vexed by patients who self-diagnose with “Dr. Google,” find themselves unsure whether generative AI will be friend or foe. Unlike traditional search engines, GenAI doesn’t just spit out information. It provides nuanced medical insights based on extensive, up-to-date research. Studies suggest that AI can already diagnose and recommend treatments with remarkable accuracy and empathy, surpassing human doctors in ever-more ways.

Path to resolution: Unfolding. While doctors are already taking advantage of AI’s administrative benefits (billing, notetaking and data entry), they’re apprehensive that ChatGPT will lead to errors if used for patient care. In this case, time will heal most concerns and eliminate most fears. Five years from now, with ChatGPT predicted to be 30 times more powerful, generative AI systems will become integral to medical care. Advanced tools, interfacing with wearables and electronic health records, will aid in disease management, diagnosis and chronic-condition monitoring, enhancing clinical outcomes and overall health.

3. The Tug-Of-War Over Healthcare Pricing

From routine doctor visits to complex hospital stays and drug prescriptions, every aspect of U.S. healthcare is getting more expensive. That’s not news to most Americans, half of whom say it is very or somewhat difficult to afford healthcare costs.

But people may be surprised to learn how the pricing wars will play out this year—and how the winners will affect the overall cost of healthcare.

Throughout U.S. healthcare, nurses are striking as doctors are unionizing. After a year of soaring inflation, healthcare supply-chain costs and wage expectations are through the roof. A notable example emerged in California, where a proposed $25 hourly minimum wage for healthcare workers was later retracted by Governor Newsom amid budget constraints.

Financial pressures are increasing. In response, thousands of doctors have sold their medical practices to private equity firms. This trend will continue in 2024 and likely drive up prices, as much as 30% higher for many specialties.

Meanwhile, drug spending will soar in 2024 as weight-loss drugs (costing roughly $12,000 a year) become increasingly available. A groundbreaking sickle cell disease treatment, which uses the controversial CRISPR technology, is projected to cost nearly $3 million upon release.

To help tame runaway prices, the Centers for Medicare & Medicaid Services will reduce out-of-pocket costs for dozens of Part B medications “by $1 to as much as $2,786 per average dose,” according to White House officials. However, the move, one of many price-busting measures under the Inflation Reduction Act, has ignited a series of legal challenges from the pharmaceutical industry.

Big Pharma seeks to delay or overturn legislation that would allow CMS to negotiate prices for 10 of the most expensive outpatient drugs starting in 2026.

Path to resolution: Up to voters. With national healthcare spending expected to leap from $4 trillion to $7 trillion by 2031, the pricing debate will only intensify. The upcoming election will be pivotal in steering the financial strategy for healthcare. A Republican surge could mean tighter controls on Medicare and Medicaid and relaxed insurance regulations, whereas a Democratic sweep could lead to increased taxes, especially on the wealthy. A divided government, however, would stall significant reforms, exacerbating the crisis of unaffordability into 2025.

Is Peace Possible?

American healthcare, much like any battlefield, is fraught with conflict and turmoil. As we navigate 2024, the wars ahead seem destined to intensify before any semblance of peace can be attained.

Yet, amidst the strife, hope glimmers: The rise of ChatGPT and other generative AI technologies holds promise for revolutionizing patient empowerment and systemic efficiency, making healthcare more accessible while mitigating the burden of chronic diseases. The debate over abortion rights, while deeply polarizing, might eventually find resolution in a legislative middle ground that echoes Roe’s protections with some restrictions on how late in pregnancy procedures can be performed.

Unfortunately, some problems need to get worse before they can get better. I predict the affordability of healthcare will be one of them this year. My New Year’s request is not to shoot the messenger.