At the end of a meeting last week with a health system executive team, the system’s COO asked us a question: “Your concept of a consumer-focused health system centered around treating patients as members describes exactly how we want to relate to our patients, but we’re not sure about the timing. Could you give us a list of the ‘no regrets’ investments you’d recommend for health systems looking to do this?”

We frequently get asked about “no regrets” strategies:

decisions or investments that will be accretive in both the current fee-for-service system as well as a future payment and operational model oriented around consumer value. The idea is understandably appealing for systems concerned about changing their delivery model too quickly in advance of payment change. And there is a long list of strategies that would make a system stronger in both fee-for-service and value: cost reduction, value-driven referral management, and online scheduling, just to name a few.

But as we pointed out, the decision to pursue only the no-regrets moves is a clear signal that the organization’s strategy is still tied to the current payment model.

If the system is truly ready to change, strategy development should start with identifying the most important investments for delivering consumer value. It’s fine to acknowledge that a health system is not yet ready, but we cautioned the team that they should not rely on the external market to provide signals for when they should undertake real change in strategy.

External signals—from payers, competitors, or disruptors—will come too slowly, or perhaps never. At some point, the health system should be prepared to lead innovation, introduce a new model of value to the market, and define and promote the incentives to support it.

Real change will require disruption of parts of the current business and cannot be accomplished with “no-regrets investments” alone.

Academic medicine combines healthcare with higher education, the two sectors of the American economy that have exhibited outsized cost growth during the past 50 years. The result is a stunning disconnection between the business practices of academic medical centers (AMCs) and the supply-demand dynamics reshaping healthcare delivery.

Market, technological and regulatory forces are pushing the healthcare industry to deliver higher-value care that generates better outcomes at lower costs. A parallel movement is shifting resources out of specialty and acute care services into primary, preventive, behavioral health and chronic disease care services. In the process, care delivery is decentralizing and becoming more consumer-centric.

AMCs Double Down

Counter to these trends, academic medicine is doubling down on high-cost, centralized, specialty-focused care delivery. Privilege has its price. Several AMCs — including Mass General Brigham, IU Health, UCSF, Ohio State and UPMC — are undertaking multibillion-dollar expansions of their existing campuses. Collectively, AMCs expect American society to fund their continued growth and profitability irrespective of cost, effectiveness and contribution to health status.

Despite being tax-exempt and having access to a large pool of free labor (residents), AMCs charge the highest treatment prices in most markets. [1] Archaic formulas allocate residency “slots” and lucrative Graduate Medical Education payments (over $20 billion annually) disproportionately into specialty care and more-established AMCs. Given their cushy funding arrangements, it’s no wonder AMCs fight vigorously to maintain an out-of-date status quo.

Legacy practices from the early 1900s still dominate medical education, medical research and clinical care. Like tenured faculty, academic physicians manage their practices with little interference. Clinical deans rule their departments with a free hand. With few exceptions, interdisciplinary coordination is an oxymoron. The result is fragmented care delivery that tolerates duplication, medical error and poor patient service.

Irresistible consumerism confronts immovable institutional inertia. As exhibited by substantial operating losses at many AMCs, their foundations are beginning to crack. [2]

Medicine’s Rise from Poverty to Prosperity

In his 1984 Pulitzer Prize-winning work, Paul Starr chronicles the social transformation of American medicine during the 19th and 20th centuries. Prior to the 1900s, doctors had low social status. Most care took place in the home. Pay was low. The profession lacked professional standards. There were too many quacks. Most doctors lived hand-to-mouth.

As the century turned, several cultural, economic, scientific and legal developments converged to elevate the profession’s status in American society. Stricter licensing reduced the supply of physicians and closed most existing medical schools. Legislation and legal rulings restricted corporate ownership of medical practices and enshrined physicians’ operating autonomy. Scientific breakthroughs gave medicine more healing power.

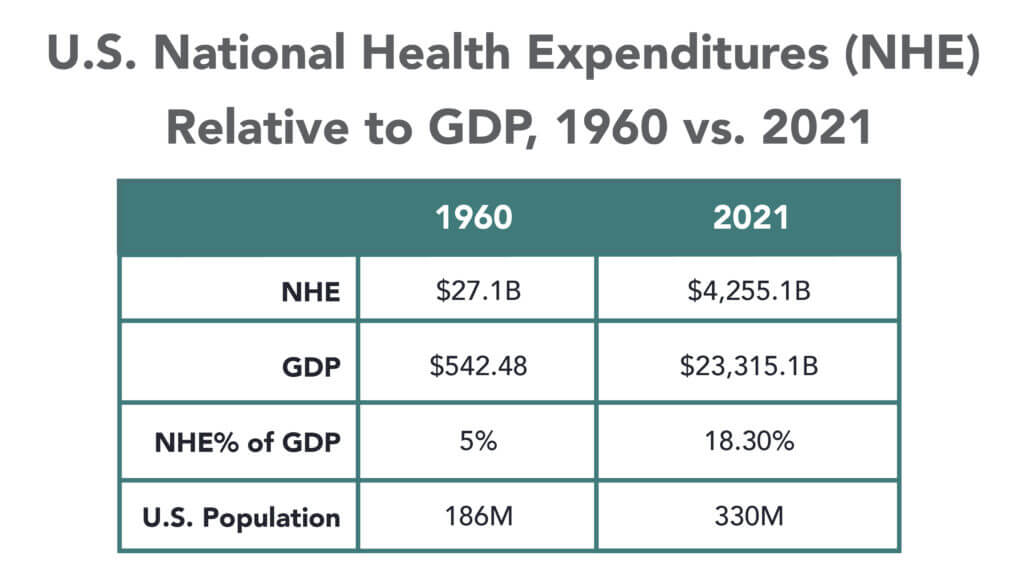

Through the decades that followed, the American Medical Association and state medical societies frustrated external attempts to control medical delivery externally and institute national health insurance. They insisted on fee-for-service payment and the absolute right of patients to choose their doctors. These are causal factors underlying healthcare’s skyrocketing cost increases, growing from 5% of the U.S. gross domestic product (GDP) in 1960 to over 18% in 2021.

Academic and community-based physicians have always had a tenuous relationship. Status and prestige accompany academic affiliations. Academic practices require referrals from community physicians but rarely consult with them on treatment protocols. For their part, community physicians marvel at the lack of market awareness exhibited by academic practices. They have tolerated one another to perpetuate collective physician control over healthcare operations.

Incomes and prestige for both community and academic physicians rose as the medical profession limited practitioner supply, established payment guidelines, encouraged specialization, controlled service delivery and socialized capital investment. One hundred years later, the business of healthcare still exhibits these characteristics. Gleaming new medical centers testify to the profession’s success in socializing capital investment and maintaining autonomy over hospital operations.

Entrenched beliefs and behaviors explain why most hospitals, despite their high construction costs, are largely deserted after 4 p.m. and on weekends. They explain the maldistribution of facilities and practitioners. They explain the overdevelopment of specialty care. They explain the underinvestment in preventive care, mental health services and public health.

Value-Focused Backlash Portends Reckoning

These beliefs and behaviors are contributing to AMC’s current economic dislocation. Dependent upon public subsidies and premium treatment payments to maintain financial sustainability, high-cost AMCs are particularly vulnerable to value-based competitors.

The marketplace is attacking inefficient clinical care with tech-savvy, consumer-friendly business models. Care delivery is decentralizing even as many AMCs invest more heavily in campus-based medicine. A market-based reckoning confronts academic medicine.

A visit up north illustrates the general unwillingness of academic physicians to accept market realities and their continued insistence on maintaining full control over the academic medical enterprise. It’s like watching a train wreck occur in slow motion.

Minnesota Madness

After experiencing severe economic distress, the University of Minnesota sold its University of Minnesota Medical Center (UMMC) to Fairview Health in 1997. Fairview currently operates UMMC in partnership with the University of Minnesota Physicians (UMP) under the banner of M Health Fairview.

In September 2022, Sanford Health and Fairview Health signed a letter of intent to merge. The new combined company would bear the Sanford name with its headquarters in Sioux Falls, South Dakota. Despite the opportunity to double its catchment area for specialty referrals, the University and UMP oppose the merger with Sanford. They fear out-of-state ownership could compromise the integrity of UMMC’s operations.

Fairview wants the Sanford merger to help it address massive operating losses resulting, in part, from its contractual arrangements with UMP. Negotiations between the parties have become acrimonious. Amid the turmoil, the University and UMP announced in January 2023 their intention to acquire UMMC from Fairview and build a new state-of-the-art medical center on the University’s Minneapolis campus.

The University has named this proposal “MPact Health Care Innovation.” It calls for the Minnesota state legislature to fund the multibillion-dollar cost of acquiring, building and operating the new medical enterprise. Typical of academic medical practices, UMP expects external sources to pony up the funding to support their high-cost centralized business model while they continue to call the shots.

The arrogance and obliviousness of the University’s proposal is staggering. Minnesota struggles with rising rates of chronic disease and inequitable healthcare access for low-income urban and rural communities. The idea that a massive governmental investment in academic medicine will “bridge the past and future for a healthier Minnesota” as the MPact tagline proclaims is ludicrous.

Out of Touch

Like the rest of the country, Minnesota is experiencing declining life expectancy. Despite spending more than double the average per-capita healthcare cost of other wealthy countries, the United States scores among the worst in health status measures. Spending more on high-end academic medicine won’t change these dismal health outcomes. Spending more on preventive care, health promotion and social determinants of health could.

The real gem in the University of Minnesota’s medical enterprise is its medical school. It has trained 70% of the state’s physicians. It ranks third and fourth nationally in primary care and family medicine. It is advancing a progressive approach to interdisciplinary and multi-professional care.

If the Minnesota state legislature really wants to advance health in Minnesota, it should expand funding for the University’s aligned health schools and community-based programs without funding the acquisition and expansion of the University’s clinical facilities.

No Privilege Without Performance

Our nation must stop enabling academic medicine’s excesses. Funding AMCs’ insatiable appetite for facilities and specialized care delivery is counterproductive. It is time for academic medicine to embrace preventive health, holistic care delivery and affordable care access.

Privilege comes with responsibility. AMCs that resist the pivot to value-based care and healthier communities deserve to lose market relevance.

America has the means to create a healthier society. It requires shifting resources out of healthcare into public health. We must have the will to make community-based health networks a reality. It starts by saying no to needless expansion of acute care facilities.

Healthcare’s most recent billion-dollar deal took the industry by surprise, leaving medical experts and hospital leaders grappling to comprehend its implications.

In case you missed it, California-based Kaiser Foundation Health Plan and Hospitals, which make up the insurance and facilities half of Kaiser Permanente, announced the acquisition of Geisinger, a Pennsylvania-based health system once acknowledged by President Obama for delivering “high-quality care.”

Upon regulatory approval, Geisinger will become the first organization to join Risant Health, Kaiser Foundation’s newly created $5 billion subsidiary. According to Kaiser, the aim is to build “a portfolio of likeminded, nonprofit, value-oriented, community-based health systems anchored in their respective communities.”

Having spent 18 years as CEO of The Permanente Medical Group, the half of Kaiser Permanente responsible for the delivery of medical care, I took great interest in the announcement. And I wasn’t alone. My phone rang off the hook for weeks with calls from reporters, policy experts and healthcare executives.

After hundreds of conversations, here are the three most common questions I received about the acquisition—and the implications for doctors, insurers, health-system competitors and patients all over the country.

Question 1: Why did Kaiser acquire Geisinger?

Most callers wanted to know about Kaiser’s motivation, figuring there must’ve been more to the acquisition than the press release indicated. Although I don’t have inside information, I believe they were right. Here’s why:

Kaiser Permanente has a long and ongoing reputation for delivering nation-leading care. The organization has consistently earned the highest quality and patient-satisfaction rankings from the National Committee for Quality Assurance (NCQA), Leapfrog Group, JD Power and Medicare.

And yet, despite a 78-year history, dozens of hospitals and 13 million members across eight states, Kaiser Permanente is still considered a coastal—not national—health system. It maintains a huge market share in California and a strong presence in the Mid-Atlantic states, yet the organization has failed repeatedly to replicate that success in other geographies.

With that context, I see two compelling reasons why the Kaiser Foundation Health Plan and Hospitals wish to become a national brand:

Influence. Elected officials and regulatory bodies often turn to healthcare’s biggest players to set legislative agendas and carve out national policy. At that table, there are a limited number of seats. By shedding its reputation as a “local” health system, Kaiser could earn one.

Survival. In recent years, companies like Amazon, CVS and Walmart have been scooping up organizations that provide primary care, telehealth, home health and specialty care services. These “retail giants” are spending up to $13 billion per acquisition. And they’re consuming already-successful healthcare companies like One Medical, Oak Street Health, Signify, Pill Pack and many others. Like an army preparing for war, these corporate behemoths are amassing the components needed to battle the traditional healthcare incumbents and ultimately oust them entirely.

The Geisinger deal expands Kaiser’s footprint, adding 600,000 patients, 10 hospitals and 100 specialty and primary care clinics. These assets lend gravitas, even though Geisinger also comes with a 2022 operating loss of $239 million.

The lesson to draw from this first question is clear: size matters. The days of solo physicians and stand-alone hospitals are over. Nostalgia for medicine’s folksy, home-spun past is understandable but futile. To survive, healthcare players must get bigger quickly or team up with someone who can. That insight leads to the next question and lesson.

Question 2: How much value will Kaiser give Geisinger?

Almost everyone I’ve spoken with understands Kaiser’s desire for greater national influence, but they’re less sure how this deal will affect Geisinger Health.

Geisinger’s Pennsylvania-based hospitals and clinics have been locked in territorial battles for years with surrounding health systems. More recently, the pandemic, combined with staffing shortages and national inflation, have challenged Geisinger’s clinical performance and eroded its bottom line.

Assuming Kaiser plans to invest roughly $1 billion in each of the four to five health systems it’s planning to acquire, that surge in cash inflow will provide Geisinger with temporary financial safety. But the bigger question is how will Kaiser improve Geisinger’s value-proposition enough to grow its market share?

In public comments, Kaiser leaders spoke of the acquisition as an opportunity for Risant to “improve the health of millions of people by increasing access to value-based care and coverage, and raising the bar for value-based approaches that prioritize patient quality outcomes.”

Many of the experts I spoke with understand Kaiser’s value intent. But they question how Kaiser can could deliver on that promise since The Permanente Medical Group (TPMG) wasn’t involved in the deal.

If, hypothetically, Kaiser and Permanente leaders were to strike a deal to collaborate in the future, TPMG’s physician leaders could bring tremendous knowledge, experience and expertise to the table. Otherwise, I agree with those who’ve expressed doubt that Kaiser, alone, will be able to significantly improve Geisinger’s clinical performance.

Health plans and insurance companies play an important role in financing medical care. They possess rich data on performance and can offer incentives that boost access to higher-quality care. But insurers don’t work directly with individual doctors to coordinate medical care or advance clinical solutions on behalf of patients. And without strong physician leadership, the pace of positive change slows to a crawl. As a example, research conducted within The Permanente Medical Group found that it takes only three years to turn a proven clinical advance into standard practice—that’s nearly six times faster than the national average.

For decades, the secret sauce for Kaiser Permanente has been the cohesive success of its three parts: Kaiser Health Plan, Kaiser Foundation Hospitals and The Permanente Medical Group.

And KP’s results speak for themselves:

90% control of hypertension for members (compared to 60% for the rest of the country)

30% fewer deaths from heart attack and stroke (compared to the rest of the country)

20% fewer deaths from colon cancer

The big lesson: insurance, by itself, doesn’t drive major improvements in medicine. It must be a combined effort between forward-looking insurers and innovative, high-performing clinicians.

But there’s another takeaway here for doctors everywhere: now is the time to join forces with other clinicians in your community. Together, you can collaborate to improve clinical quality. You can augment access and make care more affordable for patients. Simultaneously, this is the time for the insurers and the retail giants to figure out which medical groups can deliver the best care and make the best partners. Neither side will flourish alone. And this leads to a third question and lesson.

Question 3: Will the deal work?

Almost all of my conversations ended with this query. I say it’s too early to tell. But as I look years down the road, one part of the deal, in particular, gives me doubt.

Today, Geisinger uses a hybrid reimbursement model—blending both “value-based” care payments with traditional “fee-for-service” insurance plans. In addition to offering its own coverage, it contracts with a variety of other insurance companies. Rarely have I seen this scattered approach succeed.

Most healthcare observers understand the inherent flaw in the “fee for service” (FFS) model is also its greatest appeal to providers: the more you do the more you earn. FFS is how nearly all financial transactions take place in America (i.e., provide a service, earn a fee). In medicine, however, this financial model results in frequent over-testing and over-treatment with minimal if any improvement in clinical outcomes, according to researchers.

The “value-based” alternative to FFS involves prepaying for care—a model often referred to as “capitation.” In short, capitation involves a single fee, paid upfront for all the medical care provided to a defined population of patients for one year based on their age and health status. The better an organization at preventing disease and avoiding complications from chronic illness, the greater its success in both clinical quality and affordability.

Within the small world of capitated healthcare payments, there’s an important element that often gets overlooked. It makes a big difference who receives that lump-sum payment.

In the case of Kaiser Permanente, capitated payments are made directly to the medical group and the physicians who are responsible for providing care. In almost every other health system, an insurance company collects capitated payments but then pays the medical providers on a fee-for-service basis. Even though the arrangement is referred to as capitated, the incentives are overwhelmingly tied to the volume of care (not the value of that care).

In a mixed-payment model, doctors and hospitals invariably prioritize the higher paying FFS patients over the capitated ones. When I think about these conflicting incentives, I’m reminded of a prominent medical group in California. It had a main entrance for its fee-for-service patients and a second, smaller one off to the side for capitated patients.

I doubt the time spent with the patient—or the overall care provided—was equal for both groups. When income is based on quantity of care, not quality, clinicians focus more on treating the complications of chronic disease and medical errors rather than preventing them in the first place. Geisinger has walked this tightrope in the past, but as economic pressures mount, I fear doctors will find the two sets of incentives conflicting and difficult to navigate.

The big lesson: as financial pressures mount, the most effective approaches of the past will likely fail in the future. All healthcare organizations will need to make a decision: keep trying to drive volume and prices up through FFS or shift to capitation. Getting caught in the middle is a prescription for failure.

Examining the healthcare acquisitions made by Amazon and CVS, it’s clear these giants have decided to move aggressively toward a model more like Kaiser Permanente’s—one that brings insurance, pharmacy, physicians and sophisticated IT systems under one roof. These companies, along with Walmart, are aggressively marching down a path toward capitation, focusing on Medicare Advantage (the value-based option for Americans 65+) as an entry point.

So far, Geisinger has hedged its bets by maintaining a hybrid revenue stream. I doubt they can do so successfully in the future. That brings us to a final question.

The biggest question remaining

Over the next decade, hospital systems, insurers and retailers will battle for healthcare supremacy. The most recent Kaiser-Geisinger deal reflects an industry that’s undergoing massive change as health systems face intensifying pressure to remain relevant.

The most important issue to resolve is whether these shifts will ultimately help or harm patients. I’m optimistic for a positive outcome.

Whether or not the retail giants displace the incumbents, they will redefine what it takes to win. For all their faults, companies like Amazon and Walmart care a lot about meeting the needs of customers—a mindset rarely found in today’s healthcare world. As these companies grow ever larger, they’ll place consumer-oriented demands on doctors and hospitals. This will require care providers to deliver higher quality care at more affordable prices.

The retailers will only do deals with the best of the best. And they’ll kick the underachievers to the curb. They’ll use their sophisticated IT systems to better coordinate and innovate medical care. Insurers, hospitals and doctors who fail to keep up will be left behind.

Over time, patients will find themselves with far more choices and control than they have today. And I’m optimistic that will be good for the health of our nation.

Tomorrow, America’s Physician Groups (APG) will kick-off its Annual Spring Conference “Going the Distance” in San Diego with breakout sessions focused on wide ranging operational issues and 3 general sessions that address restoring trust in the profession, lessons from the pandemic and Medicare Advantage.

Next Thursday, the American Medical Association (AMA) will kick off its 5-day House of Delegates session in Chicago with a plethora of resolutions and votes on the docket and committee reports on issues like the ethical impact of private equity on physicians in private equity owned practices, health insurer payment integrity and much more.

These meetings are coincident with the expected resolution of the debt-ceiling dispute in Congress which essentially leaves current Medicare and Medicaid payments to physicians and others in tact through 2025. So, for at least the time being, surprises in insurer payments to physicians are not anticipated.

Nonetheless, it’s a critical time for APG and AMA as their members face unparalleled market pressures:

Trust in the profession has eroded. Media attention to its bad actors has expanded.

Settings have changed: the majority now work as employees of large groups owned by hospitals or private equity sponsors.

Consumer (patient) expectations about physician quality, access and service are more exacting.

Technologies that improve precision in diagnostics and therapies and integration of social determinants in care planning have altered where, how and by whom care is delivered.

Affordability and lack of price transparency are fundamental concerns for U.S. consumers (and voters), employers and Congress. While drug PBMs, hospitals and health insurers are a focus of attention, physicians are not far behind.

Private equity and retail giants are creatine formidable competition in primary and specialty care.

Media coverage of “bad actors” engaged in fraudulent activity (i.e. unnecessary care, medications, et al) has increased.

Operating losses in hospitals remain significant limiting hospital investments in their employed medical practices.

Both organizations remain steadfast in the belief that the future for U.S. healthcare is physician centric:

For APG, it’s anchored in a core belief that changing payer incentives from fee-for-service to value is the essential means toward the system’s long-term sustainability and effectiveness. (APG represents 335 physician organizations)

For AMA, “true north” is the profession’s designated role as caregivers and stewards of the public’s health and wellbeing. (AMA’s membership includes 22% of the nation’s 1.34 million practicing physicians, medical students and residents).

But market conditions have taken their toll on physician psyche even as CMS has altered its value agenda.

Physicians are highly paid professionals. Per Sullivan Cotter and Kaufman Hall, their finances took a hit during the pandemic and their finances in 2022-2023 has been stymied by inflationary pressures. Thus, most worry about their income and they’re hyper-sensitive to critics of their compensation.

Fueling their frustration, virtually all believe insurance companies are reimbursement bullies, hospitals spend too much on executive salaries (aka suits) and administration and not enough on patient care and patients are increasingly difficult and unreasonable. Most think the profession hasn’t done enough to protect them and 65% say they’re burned out. That’s where APG and AMA find themselves relative to their members.

My take:

The backdrop for the APG and AMA meetings in the next 2 weeks could not be more daunting. Inflationary pressures dog the health economy as each advances an advocacy agenda suitable to their member’s needs.

But something is missing: a comprehensive, coherent, visionary view of the health system’s future in the next 10-20 years wherein physicians will play a key role.

That view should include…

How value and affordability are defined and actualized in policies and practice.

How the caregiver workforce is developed, composed and evaluated based on shifting demand.

How incentives should be set and funding sourced and rationalized across all settings and circumstances of service.

How consumerism can be operationalized.

How prices and costs in every sector (including physician services) can become readily accessible.

How a seamless system of health can be built.

How physician training and performance can be modernized to participate effectively in the system’s future.

The U.S. health system’s future is not a repeat of its past. Recognizing this, physicians and the professional associations like APG and AMA that serve them have an obligation to define its future state NOW.

Some physicians are on the brink of despair; others are at the starting line ready to take on the challenge.

Walgreens’ growing U.S. healthcare segment is continuing to bolster the retail health chain’s financial performance. The business, which includes value-based provider VillageMD, recorded $1.6 billion in sales in the second quarter, an increase of $1.1 billion from last year.

VillageMD sales were up 30%, including a boost from its recent acquisition of medical group Summit Health. Specialty pharmacy Shields Health Solutions grew sales 41%, while at-home care provider CareCentrix’s sales were up 25%.

Thanks in part to a jump in revenue in its healthcare segment, Walgreens’ results beat Wall Street expectations even as profit declined more than 20% amid lower COVID-19 vaccine volumes and test sales, higher salary costs, opioid litigation charges and costs associated with its $3.5 billion investment in its Summit acquisition.

Dive Insight:

Walgreens has been working to expand its business scope beyond pharmacies to more consumer-centric healthcare, and has acquired a number of companies to build out its growing U.S. healthcare division.

In its earnings results for the second quarter ended Feb. 28, the business reported gross profit of $32 million, as income from Shields and CareCentrix was offset by VillageMD expansion costs. VillageMD added 133 clinics compared to the second quarter last year.

“With the closing of VillageMD’s acquisition of Summit Health, [Walgreens] is now one of the largest players in primary care,” CEO Roz Brewer said in the company’s earnings release on Tuesday.

VillageMD also acquired a Connecticut-based medical group in March for an undisclosed amount. That group, called Starling Physicians, operates more than 30 primary care and multi-specialty practices across the state.

Starling “will contribute heavily to revenue and EBITDA growth in the second half of 2023,” said Walgreens CFO James Kehoe on a Tuesday morning call with investors. “Overall, the primary care business and the specialty care business is doing really, really well.”

Despite the recent deals, Walgreens is moving beyond its peak investment period in healthcare, management said on the call. VillageMD, for example, plans to concentrate growth and investments in specific markets where it can be “hyper-relevant” moving forward, according to Walgreens President John Standley.

The concept of the “medical mall” is not new. Health systems and physician groups have long looked to build larger outpatient facilities that include several physician specialties, diagnostics, and outpatient procedure all under one roof—sometimes even converting defunct shopping malls. But recently some providers have questioned whether this “one stop shop” approach is delivering the value expected.

One CFO shared, the cost to build and operate these large facilities can be daunting: “we had two of these in our capital plan, but the real estate and construction costs are enormous. Given where margins are this year, we just couldn’t justify them.”

Others have also questioned whether their medical malls provide the value they anticipated. Another leader noted that “it seemed to make sense to put 15 primary care docs under one roof, which let us co-locate a host of other services. But patients told us they’d rather have primary care close to home. And a more distributed ‘low-key’ footprint might have been cheaper.” He also mentioned their operations fell short of the vision: “just because we have primary care and CT under one roof, doesn’t mean we can get a patient on the scanner right after their appointment.”

A physician group with two medical malls found that while they expected the vision to appeal to busy, commercially-insured patients, “it turned out that people with transportation issues or a lot of chronic conditions were the ones who chose to go there…it ended up being primarily a public-pay population, and we can’t support the cost.”

Consumers have rejected shopping malls for more distributed and technology-driven retail options. Given the cost of the medical mall, it’s worth considering whether they’ll apply the same logic to healthcare.

Urgent care centers have become increasingly popular among patients in recent years. And while the facilities may be a more convenient care option than others, experts have voiced concerns about potential downsides, Nathaniel Meyersohn writes for CNN.

What is driving the urgent care ‘boom’?

Urgent care centers have been in the United States since the 1970s, but they were widely regarded as “docs in a box,” with slow growth in their early years. Then, during the COVID-19 pandemic, demand for tests and treatments drove an increase in patients at urgent care sites around the country. According to the Urgent Care Association (UCA), patient volume at urgent care centers has increased by 60% since 2019.

As patient volumes and demand increased, growth for new urgent care centers surged. Currently, there are a record 11,150 urgent care centers in the United States, with around 7% growth annually, UCA said. Notably, this figure excludes clinics inside retail stores and freestanding EDs.

According to estimates from IBISWorld, the urgent care market will reach roughly $48 billion in revenue in 2023, a 21% increase from 2019.

“Urgent care has grown rapidly because of convenience, gaps in primary care, high costs of emergency room visits, and increased investment by health systems and private-equity groups,” Meyersohn writes.

Urgent care center growth also “highlights the crisis in the US primary care system,” Meyersohn writes, noting that the Association of American Medical Colleges said it expects a shortage of up to 55,000 primary care physicians in the next decade.

In addition, it can be difficult to book an immediate visit with a primary care provider. Urgent care sites have longer hours during the week and are open on weekends, making it easier to get an appointment. According to UCA, roughly 80% of the U.S. population is within a 10-minute drive of an urgent care center.

“There’s a need to keep up with society’s demand for quick turnaround, on-demand services that can’t be supported by underfunded primary care,” said Susan Kressly, a retired pediatrician and fellow at the American Academy of Pediatrics.

Meanwhile, health insurers and hospitals have also prioritized keeping people out of the ED. In the early 2000s, they started opening their own urgent care sites and implementing strategies to deter ED visits.

The passage of the Affordable Care Act also triggered an increase in urgent care providers, with millions of newly insured Americans accessing healthcare.

In addition, data from PitchBook suggests that private-equity and venture capital funds invested billions into deals for urgent care centers.

“If they can make it a more convenient option, there’s a lot of revenue here,” said Ateev Mehrotra, a professor of healthcare policy and medicine at Harvard Medical School who has researched urgent care clinics. “It’s not where the big bucks are in health care, but there’s a substantial number of patients.”

The increase in urgent care sites may present challenges

Many doctors, healthcare advocates, and researchers have voiced concerns at the increase in urgent care sites, noting that there are potential downsides.

“Frequent visits to urgent care sites may weaken established relationships with primary care doctors,” Meyersohn writes. “They can also lead to more fragmented care and increase overall health care spending, research shows.”

In addition, some experts have questioned the quality of care at urgent care centers, particularly how well they serve low-income communities.

In a 2018 study by Pew Charitable Trusts and CDC, researchers found that urgent care centers overprescribe antibiotics, especially those used to treat common colds, the flu, and bronchitis.

“It’s a reasonable solution for people with minor conditions that can’t wait for primary care providers,” said Vivian Ho, a health economist at Rice University. “When you need constant management of a chronic illness, you should not go there.”

Some doctors and researchers also expressed concern that patients are visiting urgent care centers instead of a primary care provider altogether.

“What you don’t want to see is people seeking a lot [of] care outside their pediatrician and decreasing their visits to their primary care provider,” said Rebecca Burns, the urgent care medical director at the Lurie Children’s Hospital of Chicago.

“There are also concerns about the oversaturation of urgent care centers in higher-income areas that have more consumers with private health care and limited access in medically underserved areas,” Meyersohn writes.

A 2016 study from the University of California at San Francisco found thaturgent care centers typically do not serve rural areas, areas that have a high concentration of low-income patients, or areas that have a low concentration of privately-insured patients.

According to the researchers, this “uneven distribution may potentially exacerbate health disparities.”

The executives featured in this article are all speaking at the Becker’s Healthcare 13th Annual Meeting April 3-6, 2023, at the Hyatt Regency in Chicago.

Question: What will hospitals and health systems look like in 10 years? What will be different and what will be the same?

Michael A. Slubowski. President and CEO of Trinity Health (Livonia, Mich.): In 10 years, inpatient hospitals will be more focused on emergency care, intensive/complex care following surgery or complex medical conditions, and short-stay/observation units. Only the most complex surgical cases and complex medical cases will be inpatient status. Most elective surgery and diagnostic services will be done in freestanding surgery, procedural and imaging centers. Many patients with chronic medical conditions will be managed at home using digital monitoring. More seniors will be cared for in homes and/or in PACE programs versus skilled nursing facilities.

Mark A. Schuster, MD, PhD. Founding Dean and Chief Executive Officer of Kaiser Permanente Bernard J. Tyson School of Medicine (Pasadena, Calif.): The future of hospitals might not actually unfold in hospitals. I expect that more and more of what we now do in hospitals will move into the home. The technology that makes this transition possible is already out there: Remote monitoring of vital signs and lab tests, remote visual exams, and videoconferencing with patients. And all of this technology will improve even more over the next 10 years — turning at-home care from a dream into a reality.

Imagine no longer being kept awake all night by beeps and alarms coming from other patients’ rooms or kept away from family by limited visiting hours. The benefits are especially welcome for people who live in rural places and other areas with limited medical facilities. Who knows? Maybe robotics will make some in-home surgeries not so far off!

Of course, not all patients have a safe or stable home environment where they could receive care, so hospitals aren’t going away anytime soon. I’m not suggesting that most current patients could be cared for remotely in a decade — but I do think we’re moving in that direction. So those of us who work in education will need to train medical, nursing, and other students for a healthcare future that looks quite different from the healthcare present and takes place in settings we couldn’t imagine 10 years ago.

Shireen Ahmad. System Director, Operations and Finance of CommonSpirit Health (Chicago): The biggest change I anticipate is a continuation in the decentralization of health services delivery that has typically been provided by hospitals. This will result in a reduction of hospitals with fewer services performed in acute settings and with more services provided in non-acute ones.

With recent reimbursement changes, CMS is helping to set the tone of where care is delivered. Hospitals are beginning to rationalize services, including who and where care is delivered. For example, pharmacies often carry clinics that provide vaccinations, but in France, one can go to a pharmacy for care and sterilization of minor wounds while only paying for bandages, medication and other supplies used in the visit. I would not be surprised if, in 10 years, one could get an MRI at their local Walmart or schedule routine screenings and tests at the grocery store with faster, more accurate results as they check out their produce.

If the pandemic has taught us anything, there will always be a need for acute care and our society will always need hospitals to provide care to sick patients. This is not something I would anticipate changing. However, the need to provide most care in a hospital will change with the result leading to fewer hospitals in total. Far from being a bleak outlook, however, I believe that healthier, sustainable health systems will prevail if they are able to provide a greater spectrum of care in broader settings focussing on quality and convenience.

Gerard Brogan. Senior Vice President and Chief Revenue Officer of Northwell Health (New Hyde Park, N.Y.): Operationally, hospitals and health systems will be more designed around the patient experience rather than the patient accommodating to the hospital design and operations. Specifically, more geared toward patient choice, shopping for services, and price competition for out-of-pocket expenses. In order to bring costs down, rational control of utilization will be more important than ever. Hopefully, we will be able to shrink the administrative costs of delivering care. Structurally, more care will continue to be done ambulatory, with hospitals having a greater proportion of beds having critical care capability and single rooms for infection control, putting pressure on the cost per square foot to operate. Sustainable funding strategies for safety net hospitals will be needed.

Mike Gentry. Executive Vice President and COO of Sentara Healthcare (Norfolk, Va.): During the next 10 years, more rural hospitals will become critical assessment facilities. The legislation will be passed to facilitate this transition. Relationships with larger sponsoring health systems will support easy transitions to higher acuity services as required. In urban areas, fewer hospitals with greater acuity and market share will often match the 50 percent plus market share of health plans. The ambulatory transition will have moved beyond only surgical procedures into outpatient but expanded historical medical inpatient status in ED/observation hubs.

The consumer/patient experience will be vastly improved. Investments in mobile digital applications will provide greatly enhanced communication, transparency of clinical status, timelines, the likelihood of expected outcomes and cost. Patients will proactively select from a menu of treatment options provided by predictive AI. The largest 10 health systems will represent 25 percent of the total U.S. acute care market share, largely due to consumer-centric strategic investments that have outpaced their competitors. Health systems will have vastly larger pharma operations/footprints.

Ketul J. Patel. CEO of Virginia Mason Franciscan Health (Seattle) and Division President, Pacific Northwest of CommonSpirit Health (Chicago): This is a transformative time in the healthcare industry, as hospitals and healthcare systems are evolving and innovating to meet the growing and changing needs of the communities we serve. The pandemic accelerated the digital transformation of healthcare. We have seen the proliferation of new technologies — telemedicine, artificial intelligence, robotics, and precision medicine — becoming an integral part of everyday clinical care. Healthcare consumers have become empowered through technology, with greater control and access to care than ever before.

Against this backdrop, in the next decade we’ll see healthcare consumerism influencing how health systems transform their hospitals. We will continue incorporating new technologies to improve healthcare delivery, offering more convenient ways to access high-quality care, and lowering the overall cost of care.

SMART hospitals, including at Virginia Mason Franciscan Health, are utilizing AI to harness real-time data and analysis to revolutionize patient and provider experiences and improve the quality of care. VMFH was the first health system in the Pacific Northwest to introduce a virtual hospital nearly a decade ago, which provides virtual services in the hospital across the continuum of care to improve quality and safety through remote patient monitoring and care delivery.

As hospitals become more high-tech, more nimble, and more efficient over the next 10 years, there will be less emphasis on brick-and-mortar buildings as we continue to move care away from the hospital toward more convenient settings for the patient. We recently launched VMFH Home Recovery Care, which brings all the essential elements of hospital-level care into the comfort and convenience of patients’ homes, offering a safe and effective alternative to the traditional inpatient stay.

Health systems and hospitals must simplify the care experience while reducing the overall cost of care. VMFH is building Washington state’s first hybrid emergency room/urgent care center, which eliminates the guesswork for patients unsure of where to go for care. By offering emergent and urgent care in a single location, patients get the appropriate level of care, at the right price, in one convenient location.

As healthcare delivery becomes more sophisticated in this digital age, we must not lose sight of why we do this work: our patients. There is no device or innovation that can truly replace the care and human intelligence provided by our nurses, APPs and physicians. So, while hospitals and health systems might look and feel different in 2033, our mission will remain the same: to provide exceptional, compassionate care to all — especially the most vulnerable.

David Sylvan. President of University Hospitals Ventures (Cleveland): American healthcare is facing an imperative. It’s clear that incremental improvements alone won’t manifest the structural outcomes that are largely overdue. The good news is that the healthcare industry itself has already initiated the disruption and self-disintermediation. I would hope that in the next 10 years, our offerings in healthcare truly reflect our efforts to adopt consumerism and patient choice, alleviate equity barriers and harness efficiencies while reducing time waste.

We know that some of this will come about through technology design, build and adoption, especially in the areas of generative artificial intelligence. But we also know that some of this will require a process overhaul, with learnings gleaned from other industries that have already solved adjacent challenges. What won’t change in 10 years will be the empathy and quality of care that the nation’s clinicians provide to patients and their caregivers daily.

Joseph Webb. CEO of Nashville (Tenn.) General Hospital: The United States healthcare industry operates within a culture that embraces capitalism as an economic system. The practice of capitalism facilitates a framework that is supported by the theory of consumerism. This theory posits that the more goods and services are purchased and consumed, the stronger an economy will be. With that in mind, healthcare is clearly a driver in the U.S. economy, and therefore, major capital and technology are continuously infused into healthcare systems. Healthcare is currently approaching 20 percent of the U.S. gross domestic product and will continue to escalate over the next 10 years.

Also, in 10 years, there will be major shifts in ownership structures, e.g., mergers, acquisitions, and consolidations. Many healthcare organizations/hospitals will be unable to sustain operations due to shrinking profit margins. This will lead to a higher likelihood of increasing closures among rural hospitals due to a lack of adequate reimbursement and rising costs associated with salaries for nurses, respiratory therapists, etc., as well as purchasing pharmaceuticals.

Aging baby boomers with chronic medical conditions will continue to dominate healthcare demand as a cohort group. To mitigate the rising costs of care, healthcare systems and providers will begin to rely even more heavily on artificial intelligence and smart devices. Population health initiatives will become more prevalent as the cost to support fragmented care becomes cost-prohibitive and payers such as CMS will continue to lead the way toward value-based care.

Because of structural and social conditions that tend to drive social determinants of health, which are fundamental causes of health disparities, achieving health equity will continue to be a major challenge in the U.S. Health equity is an elusive goal that can only be achieved when there is a more equitable distribution of SDOH.

Gary Baker. CEO, Hospital Division of HonorHealth (Scottsdale, Ariz.): In 10 years, I would expect hospitals in health systems to become more specialized for higher acuity service lines. Providing similar acute services at multiple locations will become difficult to maintain. Recruiting and retaining specialty clinical talent and adopting new technologies will require some redistribution of services to improve clinical quality and efficiency. Your local hospital may not provide a service and will be a navigator to the specialty facilities. Many services will be provided in ambulatory settings as technology and reimbursement allow/require. Investment in ambulatory services will continue for the next 10 years.

Michael Connelly. CEO Emeritus of Bon Secours Mercy Health (Cincinnati): Our society will be forced to embrace economic limits on healthcare services. The exploding elderly population, in combination with a shrinking workforce to fund Medicare/Medicaid and Social Security, will force our health system to ration care in new ways. These realities will increase the role of primary care as the needed coordinator of health services for patients. Diminishing fragmented healthcare and redundant care will become an increasing focus for health policy.

David Rahija. President of Skokie Hospital, NorthShore University HealthSystem (Evanston, Ill.): Health systems will evolve from being just a collection of hospitals, providers, and services to providing and coordinating care across a longitudinal care continuum. Health systems that are indispensable health partners to patients and communities by providing excellent outcomes through seamless, coordinated, and personalized care across a disease episode and a life span will thrive. Providers that only provide transactional care without a holistic, longitudinal relationship will either close or be consolidated. Care tailored to the personalized needs of patients and communities using team care models, technology, genomics, and analytics will be key to executing a personalized, seamless, and coordinated model of care.

Alexa Kimball, MD. President and CEO of Harvard Medical Faculty Physicians at Beth Israel Deaconess Medical Center (Boston): Ten years from now, hospitals will largely look the same — at least from the outside. Brick-and-mortar buildings aren’t going away anytime soon. What will differ is how care is delivered beyond the traditional four walls. Expect to see a more patient-centered and responsive system organized around what individuals need — when and where they need it.

Telehealth and remote patient monitoring will enable greater accessibility for patients in underserved areas and those who cannot get to a doctor’s office. Technology will not only enable doctors to deliver more personalized treatment plans but will also dramatically reshape physician workflows and processes. These digital tools will streamline administrative tasks, integrate voice commands, and provide more conducive work environments. I also envision greater access to data for both providers and patients. New self-service solutions for care management, scheduling, pricing, shopping for services, etc., will deliver a more proactive patient experience and make it easier to navigate their healthcare journey.

Ronda Lehman, PharmD. President of Mercy Health – Lima (Ohio):

This is a highly challenging question to address as we continue to reevaluate how healthcare is being delivered following several difficult years and knowing that financial challenges still loom. That said, when I am asked what it will look like, I am keenly aware of the fact that it only will look that way if we can envision a better way to improve the health of our communities. So 10 years from now, we need to have easier and more patient-driven access to care.

We will need to stop doing ‘to people’ and start caring ‘with people.’ Artificial intelligence and proliferous information that is readily available to consumers will continue to pave the way to patients being more empowered and educated about their options. So what will differentiate healthcare of the future? Enabling patients to make informed decisions.

Undoubtedly, technology will continue to advance, and along with it, the associated costs of research and development, but healthcare can only truly change if providers fundamentally shift their approach to how we care for patients. It is imperative that we need to transform from being the gatekeepers of valuable resources and services to being partners with patients on their journey. If that is what needs to be different, then what needs to be the same? We need the same highly motivated, highly skilled and perhaps most importantly, highly compassionate caregivers selflessly caring for one another and their communities.

Mike Young. President and CEO of Temple University Health System (Philadelphia): Cell therapy, gene therapy, and immunotherapy will continue to rapidly improve and evolve, replacing many traditional procedures with precise therapies to restore normal human function — either through cell transfer, altering of genetic information, or harnessing the body’s natural immune system to attack a particular disease like cancer, cystic fibrosis, heart disease, or diabetes. As a result, hospitals will decrease in footprint, while the labs dedicated to defining precision medicine will multiply in size to support individual- and disease-specific infusion, drug, and manipulative therapies.

Hospitals will continue to shepherd the patient journey through these therapies and also will continue to handle the most complex cases requiring high-tech medical and surgical procedures. Medical education will likely evolve in parallel, focusing more on genetic causation and treatment of disease, as well as proficiency with increasingly sophisticated AI diagnostic technologies to provide adaptive care on a patient-by-patient basis.

Tom Siemers. Chief Executive Officer of Wilbarger General Hospital (Vernon, Texas): My predictions include the national healthcare landscape will be dominated by a dozen or so large systems. ‘Consolidation’ will be the word that describes the healthcare industry over the next 10 years. Regional systems will merge into large, national systems. Independent and rural hospitals will become increasingly rare. They simply won’t be able to make the capital investments necessary to replace outdated facilities and equipment while vying with other organizations for scarce, licensed personnel.

Jim Heilsberg. CFO of Tri-State Memorial Hospital & Medical Campus (Clarkston, Wash.): Tri-State Hospital continues to expand services for outpatient services while maintaining traditionally needed inpatient services. In 10 years, there will be expanded outpatient services that include leveraged technology that will allow the patient to be cared for in a yet-to-be-seen care model, including traditional hospital settings and increasing home care setting solutions.

Jennifer Olson. COO of Children’s Minnesota (St. Paul, Minn.): I believe we will see more and better access to healthcare over the next 10 years. Advances in diagnostics, monitoring, and artificial intelligence will allow patients to access services at more convenient times and locations, including much more frequently at home, thereby extending health systems’ reach well beyond their walls.

What I don’t think will ever change is the heart our healthcare professionals bring with them to work every day. I see it here at Children’s Minnesota and across our industry: the unwavering commitment our caregivers have to help people live healthier lives.

If I had one wish for the future, it would be that we become better equipped to address the social determinants of health: all of the factors outside the walls of our hospitals and clinics that affect our patients’ well-being. Part of that means relaxing regulations to allow better communication and sharing of information among healthcare providers and public and private entities, so we can take a more holistic approach to improve health and decrease disparities. It also will require a fundamental shift in how health and healthcare are paid for.

Stonish Pierce. COO of Holy Cross Health, Trinity Health Florida: Over the next decade, many health systems will pivot from being ‘hospital’ systems to true ‘health’ systems. Based largely on responding to The Joint Commission’s New Requirements to Reduce Health Care Disparities, many health systems will place greater emphasis on reducing health disparities, enhanced attention to providing culturally competent care, addressing social determinants of health (including, but not limited to food, housing and transportation) and health equity. I’m proud to work for Trinity Health, a system that has already directed attention toward addressing health disparities, cultural competency and health equity.

Many systems will pivot from offering the full continuum of services at each hospital and instead focus on the core services for their respective communities, which enables long-term financial sustainability. At the same time, we will witness the proliferation of partnerships as adept health systems realize that they cannot fulfill every community’s needs alone. Depending upon the specialty and region of the country, we may see some transitioning away from the RVU physician compensation model to base salaries and value-based compensation to ensure health systems can serve their communities in the long term.

Driven largely by continued workforce supply shortages, we will also see innovation achieve its full potential. This will include, but not be limited to, virtual care models, robots to address functions currently performed by humans, and increased adoption of artificial intelligence and remote monitoring. Healthcare overall will achieve parity in technological adoption and innovation that we take for granted and have grown accustomed to in industries such as banking and the consumer service industries.

For what will remain the same, we can anticipate that government reimbursement will still not cover the cost of providing care, although systems will transition to offering care models and services that enable the best long-term financial sustainability. We will continue to see payers and retail pharmacies continue to evolve as consumer-friendly providers. We will continue to see systems make investments in ambulatory care and the most critically ill patients will remain in our hospitals.

Jamie Davis. Executive Director, Revenue Cycle Management of Banner Health (Phoenix): I think that we will see a continued shift in places of service to lower-cost delivery sources and unfavorable payer mix movement to Medicare Advantage and health exchange plans, degrading the value of gross revenue. The increased focus on cost containment, value-based care, inflation, and pricing transparency will hopefully push payers and providers to move to a more symbiotic relationship versus the adversarial one today. Additionally, we may see disruption in the technology space as the venture capital and private equity purchase boom that happened from 2019 to 2021 will mature and those entities come up for sale. If we want to continue to provide the best quality health outcomes to our patients and maintain profitability, we cannot look the same in 10 years as we do today.

James Lynn. System Vice President, Facilities and Support Services of Marshfield Clinic Health System (Wis.): There will be some aspects that will be different. For instance, there will be more players in the market and they will begin capturing a higher percentage of primary care patients. Walmart, Walgreens, CVS, Amazon, Google and others will begin to make inroads into primary care by utilizing VR and AI platforms. More and more procedures will be the same day. Fewer hospital stays will be needed for recovery as procedures become less invasive and faster. There will be increasing pressure on the federal government to make healthcare a right for all legal residents and it will be decoupled from employment status. On the other hand, what will stay the same is even though hospital stays will become shorter for some, we will also be experiencing an ever-aging population, so the same number of inpatient beds will likely be needed.

Understand the health care industry’s most urgent challenges—and greatest opportunities.

The health care industry is facing an increasingly tough business climate dominated by increasing costs and prices, tightening margins and capital, staffing upheaval, and state-level policymaking. These urgent, disruptive market forces mean that leaders must navigate an unusually high number of short-term crises.

But these near-term challenges also offer significant opportunities. The strategic choices health care leaders make now will have an outsized impact—positive or negative—on their organization’s long-term goals, as well as the equitability, sustainability, and affordability of the industry as a whole.

This briefing examines the biggest market forces to watch, the key strategic decisions that health care organizations must make to influence how the industry operates, and the emerging disruptions that will challenge the traditional structures of the entire industry.

Preview the insights below and download the full executive briefing (using the link above) now to learn the top 16 insights about the state of the health care industry today.

Preview the insights

Part 1 | Today’s market environment includes an overwhelming deluge of crises—and they all command strategic attention

Insight #1

The converging financial pressures of elevated input costs, a volatile macroeconomic climate, and the delayed impact of inflation on health care prices are exposing the entire industry to even greater scrutiny over affordability. Keep reading on pg. 6

Insight #2

The clinical workforce shortage is not temporary. It’s been building to a structural breaking point for years. Keep reading on pg. 8

Insight #3

Demand for health care services is growing more varied and complex—and pressuring the limited capacity of the health care industry when its bandwidth is most depleted. Keep reading on pg. 10

Insight #4

Insurance coverage shifted dramatically to publicly funded managed care. But Medicaid enrollment is poised to disperse unevenly after the public health emergency expires, while Medicare Advantage will grow (and consolidate). Keep reading on pg. 12

Part II | Competition for strategic assets continues at a rapid pace—influencing how and where patient care is delivered.

Insight #5

The current crisis conditions of hospital systems mask deeper vulnerabilities: rapidly eroding power to control procedural volumes and uncertainty around strategic acquisition and consolidation. Keep reading on pg. 15

Insight #6

Health care giants—especially national insurers, retailers, and big tech entrants—are building vertical ecosystems (and driving an asset-buying frenzy in the process). Keep reading on pg. 17

Insight #7

As employment options expand, physicians will determine which owners and partners benefit from their talent, clinical influence, and strategic capabilities—but only if these organizations can create an integrated physician enterprise. Keep reading on pg. 19

Insight #8

Broader, sustainable shifts to home-based care will require most care delivery organizations to focus on scaling select services. Keep reading on pg. 21

Insight #9

A flood of investment has expanded telehealth technology and changed what interactions with patients are possible. This has opened up new capabilities for coordinating care management or competing for consumer attention. Keep reading on pg. 23

Insight #10

Health care organizations are harnessing data and incentives to curate consumers choices—at both the service-specific and ecosystem-wide levels. Keep reading on pg. 25

Part III | Emerging structural disruptions require leaders to reckon with impacts to future business sustainability.

Insight #11

For value-based care to succeed outside of public programs, commercial plans and providers must coalesce around a sustainable risk-based payment approach that meets employers’ experience and cost needs. Keep reading on pg. 28

Insight #12

Industry pioneers are taking steps to integrate health equity into quality metrics. This could transform the health care business model, or it could relegate equity initiatives to just another target on a dashboard. Keep reading on pg. 30

Insight #13

Unprecedented behavioral health needs are hitting an already fragmented, marginalized care infrastructure. Leaders across all sectors will need to make difficult compromises to treat and pay for behavioral health like we do other complex, chronic conditions. Keep reading on pg. 32

Insight #14

As the population ages, the fragile patchwork of government payers, unpaid caregivers, and strained nursing homes is ill-equipped to provide sustainable, equitable senior care. This is putting pressure on Medicare Advantage plans to ultimately deliver results. Keep reading on pg. 34

Insight #15

The enormous pipeline of specialized high-cost therapies in development will see limited clinical use unless the entire industry prepares for paradigm shifts in evidence evaluation, utilization management, and financing. Keep reading on pg. 36

Insight #16

Self-funded employers, who are now liable for paying “reasonable” amounts, may contest the standard business practices of brokers and plans to avoid complex legal battles with poor optics. Keep reading on pg. 38

Since the early days of the pandemic, the healthcare industry has faced seemingly insurmountable challenges to ensure access to high-quality care. While healthcare providers have performed admirably in the face of these challenges, patients are still seeing access challenges that are impacting their behaviors — which can lead to challenges in the long run.

In the 2022 BDO Patient Experience Survey, they sought to learn how patients feel about their providers and healthcare experience — from making appointments and interacting with care providers, to how patients access health insurance and who patients turn to for routine care.

From the survey of over 3,000 U.S. adults, they came across a few key takeaways:

1. Delaying routine care is the new norm

Americans face a troubling dilemma: While 92% have health insurance and 91% have a regular care provider, 58% admit to delaying routine medical care in the past 12 months.

For routine (non-emergency) care, 69% of respondents report seeing a primary care physician and 12% routinely visit primary care nurse/nurse practitioner or physician assistant. Just 9% do not have a provider for routine medical care. Our survey found that Americans use a wide variety of health insurance options with employer-sponsored insurance (32%) being the most popular, followed by Medicare (28%), Medicaid (14%) and individual private insurance (7%). While 8% report having no health insurance, even those with insurance faced significant barriers to care.

Of those who delayed seeking medical care in the past 12 months, 30% cite unaffordability due to high out-of-pocket costs and 19% say they could not afford to seek care due to a lack of insurance. In addition to the high costs of medical care, many Americans struggle with a lack of cost transparency.

2. Cost transparency is a continuing problem

Nearly a third of Americans (31%) have never tried to obtain cost estimates for medical care. When patients do not know what healthcare will cost, many avoid seeking necessary care. A critical way we can improve patient access to healthcare is to understand how patients like to obtain cost estimates.

Of patients surveyed who have sought cost estimates, most prefer to reach out to a person, with 38% preferring to contact their insurance provider and 37% opting to ask the healthcare provider’s administrative staff. On the digital side, 31% say they obtained cost estimates by looking at online patient portals and 27% look to health provider or medical facility websites.

3. Most patients experience frustration when seeking and receiving care

We know that long appointments lead times and high costs cause patients to put off care — but how do patients feel about the actual care they receive? 69% of Americans experience frustration during routine medical appointments, with having to wait for a late provider (29%), not getting enough time with the provider (22%) and having too much paperwork to fill out (21%) being the most common frustrations.

When providers make it easier for patients to receive care, their efforts are noticed. Patients say providers make care more accessible by offering telehealth appointments (32%), reaching out to proactively schedule appointments (29%), offering walk-in appointments (27%) and implementing online/self-service scheduling (23%).

Patients are facing a challenging care environment — and so are providers. Fortunately, there are ways that providers can improve access and the care experience for their patients without breaking their budgets.